Contemporary Issues in Accounting: A Research Report Analysis

VerifiedAdded on 2022/10/09

|15

|2720

|98

Report

AI Summary

This report delves into the contemporary issue of sustainability reporting within the field of accounting. It begins by establishing the importance of sustainability for stakeholders and corporations, highlighting the increasing awareness of environmental, social, and governance issues. The practical motivation stems from the growing stakeholder concern for sustainability, transparency, and effective market functioning. The theoretical motivation focuses on addressing the gaps in current sustainability practices and the consistency of disclosures. The report reviews literature on sustainability reporting practices, emphasizing its role in corporate strategy and transparency. Key theories, including agency, stakeholder, and legitimacy theories, are examined to understand the dynamics of sustainability reporting. The analysis includes critical evaluations of existing research, presenting a hypothesis regarding the effectiveness of sustainability reporting practices. The paper concludes by assessing the company's intentions for the disclosures on the different sustainability issues, for instance environment, community, people, customers, employees and others, and how it impacts stakeholders.

Running Head: CONTEMPORARY ISSUES IN ACCOUNTING

CONTEMPORARY ISSSUES IN ACCOUNTING

Name of the Student

Name of the University

Author Note

CONTEMPORARY ISSSUES IN ACCOUNTING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction................................................................................................................................2

Practical Motivation...................................................................................................................2

Theoretical Motivation...............................................................................................................3

Literature Review.......................................................................................................................3

Practices of Sustainability Reporting.....................................................................................3

Hypothesis..................................................................................................................................7

Reference....................................................................................................................................8

Table of Contents

Introduction................................................................................................................................2

Practical Motivation...................................................................................................................2

Theoretical Motivation...............................................................................................................3

Literature Review.......................................................................................................................3

Practices of Sustainability Reporting.....................................................................................3

Hypothesis..................................................................................................................................7

Reference....................................................................................................................................8

2CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

Sustainability forms core of the corporate sustainability as well as it is of utmost

concerns for all stakeholders. In the recent few years, the awareness among corporates have

been increased for addressing the issues related to the governance, social as well as

environment for contributing towards the sustainable development. The sustainable

organization development occurs by the improvement of their social and the environmental

performance. However, this has become the global challenge for almost all the businesses

around the world for sustain in the long run. The requirements for incorporating sustainability

practices into the core strategy of the business are need of the hour (Higgins, Milne and Van

Gramberg 2015).

During the past two decades, the need for the corporate sustainability as well as

reporting of the practices of sustainability has acquired pivotal importance, which has

become integral part of overall business strategy of company. Further, increase in concerns of

negative social and environmental impact has resulted into analyzing the company’s

effectiveness in sustainability reporting practices. Hence, this research paper will discuss

regarding effectiveness of sustainability reporting practices adopted by firm.

Practical Motivation

The stakeholders off the economy in the recent years are more concerned about the

sustainability practices. The increasing practice of the sustainability reporting has created

transparency as well as help market for functioning in the more effective as well as efficient

manner. Further, the decisions made by stakeholders are based on the understanding of

effectiveness level of the disclosures made by the company on various aspects.

Introduction

Sustainability forms core of the corporate sustainability as well as it is of utmost

concerns for all stakeholders. In the recent few years, the awareness among corporates have

been increased for addressing the issues related to the governance, social as well as

environment for contributing towards the sustainable development. The sustainable

organization development occurs by the improvement of their social and the environmental

performance. However, this has become the global challenge for almost all the businesses

around the world for sustain in the long run. The requirements for incorporating sustainability

practices into the core strategy of the business are need of the hour (Higgins, Milne and Van

Gramberg 2015).

During the past two decades, the need for the corporate sustainability as well as

reporting of the practices of sustainability has acquired pivotal importance, which has

become integral part of overall business strategy of company. Further, increase in concerns of

negative social and environmental impact has resulted into analyzing the company’s

effectiveness in sustainability reporting practices. Hence, this research paper will discuss

regarding effectiveness of sustainability reporting practices adopted by firm.

Practical Motivation

The stakeholders off the economy in the recent years are more concerned about the

sustainability practices. The increasing practice of the sustainability reporting has created

transparency as well as help market for functioning in the more effective as well as efficient

manner. Further, the decisions made by stakeholders are based on the understanding of

effectiveness level of the disclosures made by the company on various aspects.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CONTEMPORARY ISSUES IN ACCOUNTING

Theoretical Motivation

This research paper addresses the recent gaps in the practice of sustainability practices

of firm in context of effectiveness as well consistency of current sustainability disclosures

practices. It has been analyzed that despite of rising interests of academics and practitioners

on sustainability practice, still the gap exists. This gap motivates to do the research on

effectiveness in sustainability reporting practices implementations.

Literature Review

Practices of Sustainability Reporting

The pressures from the stakeholders have compelled the businesses for proving their

transparency, accountability as well as effectiveness of governance through the disclosures of

the corporate sustainability. Sustainability is defined as the ability for existing constantly.

Moreover, sustainability reporting practices is the report that is published by the company

about social, environmental as well as economic impacts that are caused by day-to-day

business activities. The fundamental for achieving the sustainable practices is building as

well as maintaining the trust level in businesses (Dissanayake, Tilt and Xydias-Lobo 2016).

In order to cater the diverse needs of the stakeholders as well as achieving the

continuous improvements, it becomes important for the businesses for engaging with the

targeted stakeholders and obtaining the meaningful feedback on their processes of

performance as well as reporting. This helps in meeting the demands of stakeholders as well

as improving the future sustainability agenda of businesses. Further, the effectiveness of

sustainability reporting practice is more or less dependent upon company’s intention for its

implementation. Sustainable reports the real picture of company in relation to sustainable

practices. The two important variable includes consistency ad intention of implementing

Theoretical Motivation

This research paper addresses the recent gaps in the practice of sustainability practices

of firm in context of effectiveness as well consistency of current sustainability disclosures

practices. It has been analyzed that despite of rising interests of academics and practitioners

on sustainability practice, still the gap exists. This gap motivates to do the research on

effectiveness in sustainability reporting practices implementations.

Literature Review

Practices of Sustainability Reporting

The pressures from the stakeholders have compelled the businesses for proving their

transparency, accountability as well as effectiveness of governance through the disclosures of

the corporate sustainability. Sustainability is defined as the ability for existing constantly.

Moreover, sustainability reporting practices is the report that is published by the company

about social, environmental as well as economic impacts that are caused by day-to-day

business activities. The fundamental for achieving the sustainable practices is building as

well as maintaining the trust level in businesses (Dissanayake, Tilt and Xydias-Lobo 2016).

In order to cater the diverse needs of the stakeholders as well as achieving the

continuous improvements, it becomes important for the businesses for engaging with the

targeted stakeholders and obtaining the meaningful feedback on their processes of

performance as well as reporting. This helps in meeting the demands of stakeholders as well

as improving the future sustainability agenda of businesses. Further, the effectiveness of

sustainability reporting practice is more or less dependent upon company’s intention for its

implementation. Sustainable reports the real picture of company in relation to sustainable

practices. The two important variable includes consistency ad intention of implementing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CONTEMPORARY ISSUES IN ACCOUNTING

sustainability practice as dependent variable and sustainability reporting practices as

independent variable (Hughen, Lulseged and Upton 2014).

Framework

The agency theory is based on managers and owners relationships. There is

informational asymmetry as well as conflict of interest between company’s managers and

other stakeholders. This theory has gained significance after the series of scandals of the

corporate failures. The perceived risks of the company by the investors will be high, if

company does not make public disclosures. Therefore, sustainability reporting reduce this

informational asymmetry and perceived risk by investor by increasing market efficiencies

and reducing cost of the capital (Lodhia and Hess 2014).

The stakeholders’ theory has been emerged as the backbone of the sustainability

reporting. This theory makes the basic assumptions that the strategic management leads

towards the competitive advantages, which allows the higher level of the value creation. The

firms are having the accountability for broad stakeholders compare to only investors. The

sustainability reporting practice signifies towards strengthen the relationship between society

and firms, under which the companies is operating. In case of ignorance of stakeholders’

interest, there would be greater impact on company’s reputations, which would unfavorably

affect their financial performances (Jorge et al. 2015).

The legitimacy theory is related to the stakeholders’ theory, as the legitimacy is

something that is granted by the stakeholders of the organization. The companies are required

to justify their actions as well as ensure the understanding among all various stakeholders.

This theory stresses on the fact that organization should be accountable towards their actions.

The sustainable reporting stresses on the importance of the demonstrations of the social

sustainability practice as dependent variable and sustainability reporting practices as

independent variable (Hughen, Lulseged and Upton 2014).

Framework

The agency theory is based on managers and owners relationships. There is

informational asymmetry as well as conflict of interest between company’s managers and

other stakeholders. This theory has gained significance after the series of scandals of the

corporate failures. The perceived risks of the company by the investors will be high, if

company does not make public disclosures. Therefore, sustainability reporting reduce this

informational asymmetry and perceived risk by investor by increasing market efficiencies

and reducing cost of the capital (Lodhia and Hess 2014).

The stakeholders’ theory has been emerged as the backbone of the sustainability

reporting. This theory makes the basic assumptions that the strategic management leads

towards the competitive advantages, which allows the higher level of the value creation. The

firms are having the accountability for broad stakeholders compare to only investors. The

sustainability reporting practice signifies towards strengthen the relationship between society

and firms, under which the companies is operating. In case of ignorance of stakeholders’

interest, there would be greater impact on company’s reputations, which would unfavorably

affect their financial performances (Jorge et al. 2015).

The legitimacy theory is related to the stakeholders’ theory, as the legitimacy is

something that is granted by the stakeholders of the organization. The companies are required

to justify their actions as well as ensure the understanding among all various stakeholders.

This theory stresses on the fact that organization should be accountable towards their actions.

The sustainable reporting stresses on the importance of the demonstrations of the social

5CONTEMPORARY ISSUES IN ACCOUNTING

values that are created while operating in the environmentally sustainable manner

(Fernandez-Feijoo, Romero and Ruiz 2014).

Critical Analysis

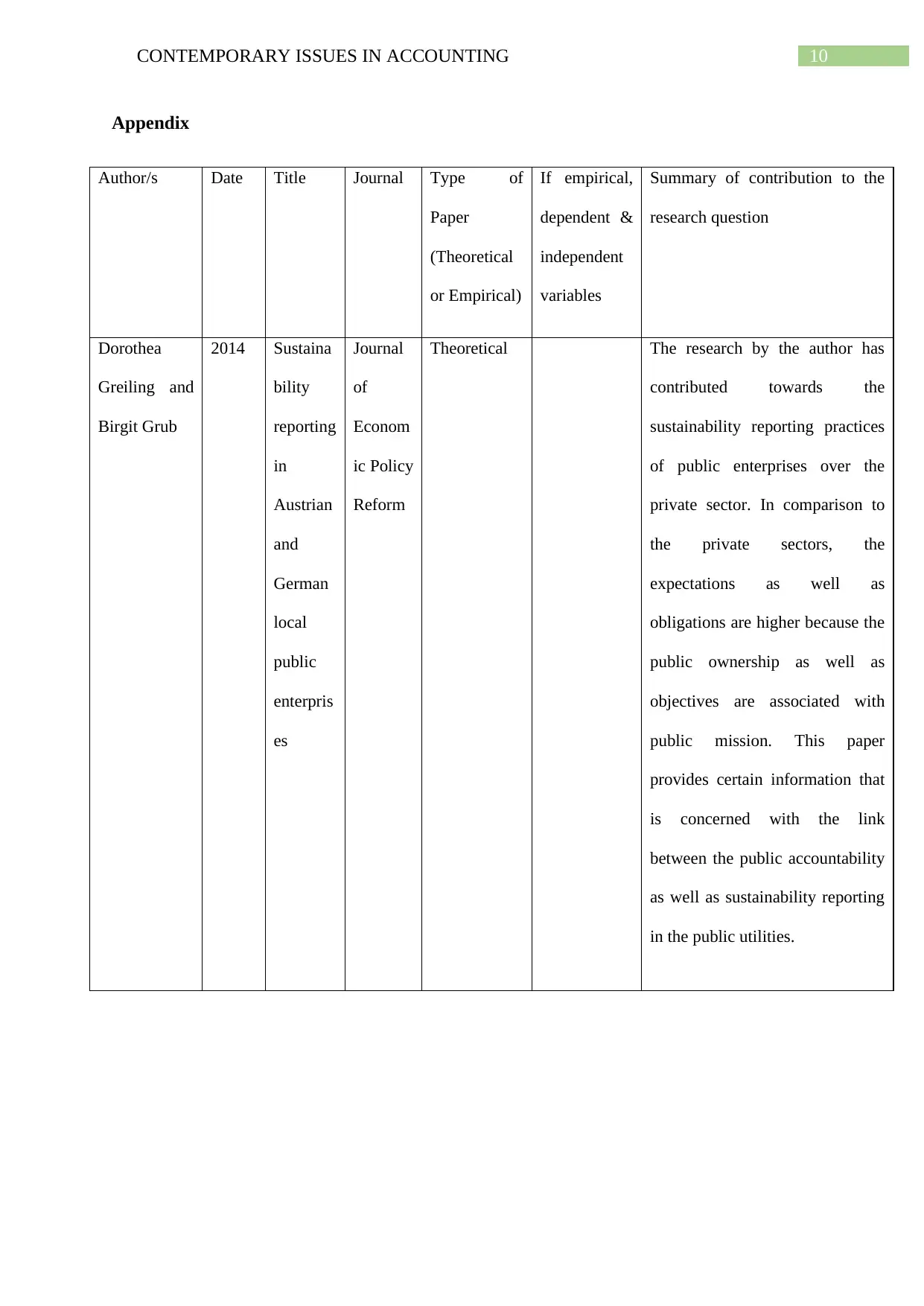

Greiling has stated in his article that there is existence of possible gap when it comes

to link public accountability to the practices of sustainability reporting. The author stated that

reporting as well as level of the accountability must needs to be evaluated with respect to the

informational needs as well as readers of report (Greiling and Grüb 2014).

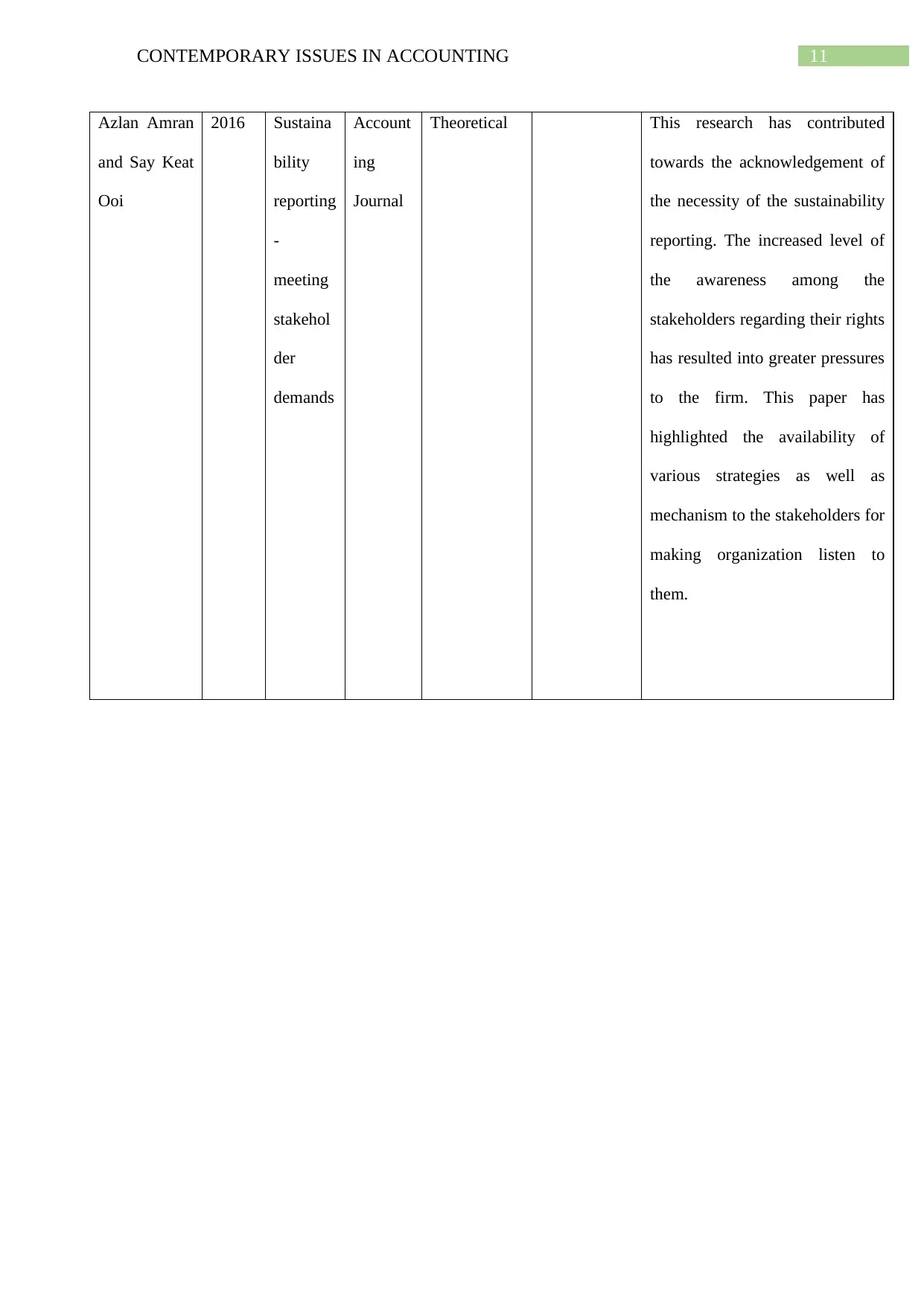

Amran has stated that sustainability reporting may not be voluntary with the rapid

changing reporting outlook as well as emergence of the standards and regulations. The author

stated that sustainability practice is now become important for the operational success.

Further, the business organizations are into greater pressure because of the increasing level of

the awareness among the stakeholders, which has resulted into moving towards disclosures

by the firms (Amran and Keat Ooi 2014).

Charl has stated regarding new conceptual model of sustainability practices of

corporate with management control & reporting in his article. According to author,

integration of sustainability practices with the management control & reporting practices

offers great benefit in terms of providing better operations and better communications.

Sustainability practices of the organization could improve in the better way by the help of

understanding and implementing balance scorecard practices (De Villiers, Rouse and Kerr

2016).

Rodrigo in his article has given the statement in his article that the company’s

decisions regarding publishing the sustainability report is influenced by their internal

motivations and external stimuli. Further, it is internal motivation plays vital role in practices

of company’s sustainability practices (Lozano, Nummert and Ceulemans 2016).

values that are created while operating in the environmentally sustainable manner

(Fernandez-Feijoo, Romero and Ruiz 2014).

Critical Analysis

Greiling has stated in his article that there is existence of possible gap when it comes

to link public accountability to the practices of sustainability reporting. The author stated that

reporting as well as level of the accountability must needs to be evaluated with respect to the

informational needs as well as readers of report (Greiling and Grüb 2014).

Amran has stated that sustainability reporting may not be voluntary with the rapid

changing reporting outlook as well as emergence of the standards and regulations. The author

stated that sustainability practice is now become important for the operational success.

Further, the business organizations are into greater pressure because of the increasing level of

the awareness among the stakeholders, which has resulted into moving towards disclosures

by the firms (Amran and Keat Ooi 2014).

Charl has stated regarding new conceptual model of sustainability practices of

corporate with management control & reporting in his article. According to author,

integration of sustainability practices with the management control & reporting practices

offers great benefit in terms of providing better operations and better communications.

Sustainability practices of the organization could improve in the better way by the help of

understanding and implementing balance scorecard practices (De Villiers, Rouse and Kerr

2016).

Rodrigo in his article has given the statement in his article that the company’s

decisions regarding publishing the sustainability report is influenced by their internal

motivations and external stimuli. Further, it is internal motivation plays vital role in practices

of company’s sustainability practices (Lozano, Nummert and Ceulemans 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CONTEMPORARY ISSUES IN ACCOUNTING

Wan Karimah has given the statement in his article that the organizations have in

general clear sustainability policy for planning and make commitments regarding protecting

environment and acting responsibly towards their practices. However, the major concern

arises in converting policies and the company’s commitments in the measurable indicators.

This help the company to easily access their current position in relation to the practices of

sustainability and identifying priority areas for leading towards effectiveness of the strategy

implementations of sustainability (Wan Ahmad, de Brito and Tavasszy 2016).

This research paper has attempted to find the gap of the existing literatures on the

evidences that whether the organization implements the practice of sustainability on

documents or whether they actually mean that they are concerned about the sustainability

practices for the stakeholders to show that they actually mean what is being reported. This

paper has focused on the company’s intention to report effective sustainability practices.

There are certain companies who follow sustainability practices just on paper by merely

putting tick mark on the disclosures checklist. Although, in reality they are not much prone to

the practices of sustainability for the aspects of environment, economic, social, community

and environmental aspects (Piecyk and Björklund 2015). The organizations are required to

follow the laws that relates to sustainability for the disclosures relating to various sustainable

concerns of organization. Further, the focus of this research paper is on company’s intention

to follow practices of sustainability reporting in effective manner and whether in the

contemporary business scenario, its practices is increasing or not. In this concern, many

academics as well as researchers have provided their views and evidences that highlights the

major concerns relating to practices of disclosures and reporting effectiveness by the

companies (Fonseca, McAllister and Fitzpatrick 2014).

Hence, significant increases in the effectiveness of practices of sustainability

reporting majorly depends on the company’s intentions for the disclosures on the different

Wan Karimah has given the statement in his article that the organizations have in

general clear sustainability policy for planning and make commitments regarding protecting

environment and acting responsibly towards their practices. However, the major concern

arises in converting policies and the company’s commitments in the measurable indicators.

This help the company to easily access their current position in relation to the practices of

sustainability and identifying priority areas for leading towards effectiveness of the strategy

implementations of sustainability (Wan Ahmad, de Brito and Tavasszy 2016).

This research paper has attempted to find the gap of the existing literatures on the

evidences that whether the organization implements the practice of sustainability on

documents or whether they actually mean that they are concerned about the sustainability

practices for the stakeholders to show that they actually mean what is being reported. This

paper has focused on the company’s intention to report effective sustainability practices.

There are certain companies who follow sustainability practices just on paper by merely

putting tick mark on the disclosures checklist. Although, in reality they are not much prone to

the practices of sustainability for the aspects of environment, economic, social, community

and environmental aspects (Piecyk and Björklund 2015). The organizations are required to

follow the laws that relates to sustainability for the disclosures relating to various sustainable

concerns of organization. Further, the focus of this research paper is on company’s intention

to follow practices of sustainability reporting in effective manner and whether in the

contemporary business scenario, its practices is increasing or not. In this concern, many

academics as well as researchers have provided their views and evidences that highlights the

major concerns relating to practices of disclosures and reporting effectiveness by the

companies (Fonseca, McAllister and Fitzpatrick 2014).

Hence, significant increases in the effectiveness of practices of sustainability

reporting majorly depends on the company’s intentions for the disclosures on the different

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CONTEMPORARY ISSUES IN ACCOUNTING

sustainability issues, for instance environment, community, people, customers, employees

and others. The practice of sustainability reporting plays important role for company’s

stakeholders. The shareholder of the company as well as other stakeholders takes their

decisions based on organizational views and disclosures made by them on the sustainable

practices (Lodhia and Hess 2014).

Hypothesis

Following are the hypothesis, which is developed after the critical analysis of the

issues and researches on the topic of sustainability reporting practices by the companies:

H0: There is significant increase in effectiveness of the implementing the

sustainability reporting practices by contemporary organizations.

H1: There is no significant increase in effectiveness of the implementing the

sustainability reporting practices by contemporary organizations.

sustainability issues, for instance environment, community, people, customers, employees

and others. The practice of sustainability reporting plays important role for company’s

stakeholders. The shareholder of the company as well as other stakeholders takes their

decisions based on organizational views and disclosures made by them on the sustainable

practices (Lodhia and Hess 2014).

Hypothesis

Following are the hypothesis, which is developed after the critical analysis of the

issues and researches on the topic of sustainability reporting practices by the companies:

H0: There is significant increase in effectiveness of the implementing the

sustainability reporting practices by contemporary organizations.

H1: There is no significant increase in effectiveness of the implementing the

sustainability reporting practices by contemporary organizations.

8CONTEMPORARY ISSUES IN ACCOUNTING

Reference

Amran, A. and Keat Ooi, S., 2014. Sustainability reporting: meeting stakeholder

demands. Strategic Direction, 30(7), pp.38-41.

De Villiers, C., Rouse, P. and Kerr, J., 2016. A new conceptual model of influences driving

sustainability based on case evidence of the integration of corporate sustainability

management control and reporting. Journal of Cleaner Production, 136, pp.78-85.

Dissanayake, D., Tilt, C. and Xydias-Lobo, M., 2016. Sustainability reporting by publicly

listed companies in Sri Lanka. Journal of Cleaner Production, 129, pp.169-182.

Fernandez-Feijoo, B., Romero, S. and Ruiz, S., 2014. Effect of stakeholders’ pressure on

transparency of sustainability reports within the GRI framework. Journal of business

ethics, 122(1), pp.53-63.

Fonseca, A., McAllister, M.L. and Fitzpatrick, P., 2014. Sustainability reporting among

mining corporations: a constructive critique of the GRI approach. Journal of cleaner

production, 84, pp.70-83.

Greiling, D. and Grüb, B., 2014. Sustainability reporting in Austrian and German local public

enterprises. Journal of Economic Policy Reform, 17(3), pp.209-223.

Higgins, C., Milne, M.J. and Van Gramberg, B., 2015. The uptake of sustainability reporting

in Australia. Journal of Business Ethics, 129(2), pp.445-468.

Hughen, L., Lulseged, A. and Upton, D.R., 2014. Improving stakeholder value through

sustainability and integrated reporting. The CPA journal, 84(3), p.57.

Jorge, M.L., Madueño, J.H., Cejas, M.Y.C. and Peña, F.J.A., 2015. An approach to the

implementation of sustainability practices in Spanish universities. Journal of Cleaner

Production, 106, pp.34-44.

Reference

Amran, A. and Keat Ooi, S., 2014. Sustainability reporting: meeting stakeholder

demands. Strategic Direction, 30(7), pp.38-41.

De Villiers, C., Rouse, P. and Kerr, J., 2016. A new conceptual model of influences driving

sustainability based on case evidence of the integration of corporate sustainability

management control and reporting. Journal of Cleaner Production, 136, pp.78-85.

Dissanayake, D., Tilt, C. and Xydias-Lobo, M., 2016. Sustainability reporting by publicly

listed companies in Sri Lanka. Journal of Cleaner Production, 129, pp.169-182.

Fernandez-Feijoo, B., Romero, S. and Ruiz, S., 2014. Effect of stakeholders’ pressure on

transparency of sustainability reports within the GRI framework. Journal of business

ethics, 122(1), pp.53-63.

Fonseca, A., McAllister, M.L. and Fitzpatrick, P., 2014. Sustainability reporting among

mining corporations: a constructive critique of the GRI approach. Journal of cleaner

production, 84, pp.70-83.

Greiling, D. and Grüb, B., 2014. Sustainability reporting in Austrian and German local public

enterprises. Journal of Economic Policy Reform, 17(3), pp.209-223.

Higgins, C., Milne, M.J. and Van Gramberg, B., 2015. The uptake of sustainability reporting

in Australia. Journal of Business Ethics, 129(2), pp.445-468.

Hughen, L., Lulseged, A. and Upton, D.R., 2014. Improving stakeholder value through

sustainability and integrated reporting. The CPA journal, 84(3), p.57.

Jorge, M.L., Madueño, J.H., Cejas, M.Y.C. and Peña, F.J.A., 2015. An approach to the

implementation of sustainability practices in Spanish universities. Journal of Cleaner

Production, 106, pp.34-44.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CONTEMPORARY ISSUES IN ACCOUNTING

Lodhia, S. and Hess, N., 2014. Sustainability accounting and reporting in the mining

industry: current literature and directions for future research. Journal of Cleaner

Production, 84, pp.43-50.

Lozano, R., Nummert, B. and Ceulemans, K., 2016. Elucidating the relationship between

sustainability reporting and organisational change management for sustainability. Journal of

cleaner production, 125, pp.168-188.

Piecyk, M.I. and Björklund, M., 2015. Logistics service providers and corporate social

responsibility: sustainability reporting in the logistics industry. International Journal of

Physical Distribution & Logistics Management, 45(5), pp.459-485.

Wan Ahmad, W.N.K., de Brito, M.P. and Tavasszy, L.A., 2016. Sustainable supply chain

management in the oil and gas industry: a review of corporate sustainability reporting

practices. Benchmarking: An International Journal, 23(6), pp.1423-1444.

Lodhia, S. and Hess, N., 2014. Sustainability accounting and reporting in the mining

industry: current literature and directions for future research. Journal of Cleaner

Production, 84, pp.43-50.

Lozano, R., Nummert, B. and Ceulemans, K., 2016. Elucidating the relationship between

sustainability reporting and organisational change management for sustainability. Journal of

cleaner production, 125, pp.168-188.

Piecyk, M.I. and Björklund, M., 2015. Logistics service providers and corporate social

responsibility: sustainability reporting in the logistics industry. International Journal of

Physical Distribution & Logistics Management, 45(5), pp.459-485.

Wan Ahmad, W.N.K., de Brito, M.P. and Tavasszy, L.A., 2016. Sustainable supply chain

management in the oil and gas industry: a review of corporate sustainability reporting

practices. Benchmarking: An International Journal, 23(6), pp.1423-1444.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CONTEMPORARY ISSUES IN ACCOUNTING

Appendix

Author/s Date Title Journal Type of

Paper

(Theoretical

or Empirical)

If empirical,

dependent &

independent

variables

Summary of contribution to the

research question

Dorothea

Greiling and

Birgit Grub

2014 Sustaina

bility

reporting

in

Austrian

and

German

local

public

enterpris

es

Journal

of

Econom

ic Policy

Reform

Theoretical The research by the author has

contributed towards the

sustainability reporting practices

of public enterprises over the

private sector. In comparison to

the private sectors, the

expectations as well as

obligations are higher because the

public ownership as well as

objectives are associated with

public mission. This paper

provides certain information that

is concerned with the link

between the public accountability

as well as sustainability reporting

in the public utilities.

Appendix

Author/s Date Title Journal Type of

Paper

(Theoretical

or Empirical)

If empirical,

dependent &

independent

variables

Summary of contribution to the

research question

Dorothea

Greiling and

Birgit Grub

2014 Sustaina

bility

reporting

in

Austrian

and

German

local

public

enterpris

es

Journal

of

Econom

ic Policy

Reform

Theoretical The research by the author has

contributed towards the

sustainability reporting practices

of public enterprises over the

private sector. In comparison to

the private sectors, the

expectations as well as

obligations are higher because the

public ownership as well as

objectives are associated with

public mission. This paper

provides certain information that

is concerned with the link

between the public accountability

as well as sustainability reporting

in the public utilities.

11CONTEMPORARY ISSUES IN ACCOUNTING

Azlan Amran

and Say Keat

Ooi

2016 Sustaina

bility

reporting

-

meeting

stakehol

der

demands

Account

ing

Journal

Theoretical This research has contributed

towards the acknowledgement of

the necessity of the sustainability

reporting. The increased level of

the awareness among the

stakeholders regarding their rights

has resulted into greater pressures

to the firm. This paper has

highlighted the availability of

various strategies as well as

mechanism to the stakeholders for

making organization listen to

them.

Azlan Amran

and Say Keat

Ooi

2016 Sustaina

bility

reporting

-

meeting

stakehol

der

demands

Account

ing

Journal

Theoretical This research has contributed

towards the acknowledgement of

the necessity of the sustainability

reporting. The increased level of

the awareness among the

stakeholders regarding their rights

has resulted into greater pressures

to the firm. This paper has

highlighted the availability of

various strategies as well as

mechanism to the stakeholders for

making organization listen to

them.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.