Strategic Sustainable Accounting Report: Timberland & Skechers

VerifiedAdded on 2022/10/02

|10

|1838

|11

Report

AI Summary

This report, focusing on strategic sustainable accounting, evaluates the production decisions of Timberland and Skechers, highlighting the application of linear programming in optimizing output and profitability. The analysis explores the impact of machine constraints, the viability of new machinery investments, and methods to improve contribution margins. The study utilizes tools like Solver to derive optimal production points, considering factors such as machine hours, direct labor costs, and variable overheads. The report emphasizes the importance of resource management and the application of linear programming models in making effective business decisions. The report also takes into consideration the social and environmental aspects of introducing new machinery. The report concludes by highlighting the importance of production optimization and the use of technology to gain a competitive advantage.

1

Strategic Sustainable accounting

Student name

Institution

Strategic Sustainable accounting

Student name

Institution

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive summary

The ability of the managers to make optimal decisions is the difference between excellence and

failure in organizations. One area that needs to be given attention is the production process. For

optimum profitability a firm has to produce enough units to supply the market demand at the

lowest cost possible. This can only be achieved by accounting for the use of all the resources in

the production. In most cases this can be a complex decision affected by several variables. Liner

programming is one of the techniques that can be applied by managers to analyse the situation

and ease the burden of deriving the optimal production points. This study did evaluate the

production decisions of Timberland and Sketchers. In both the firms, it was realized that linear

models are an effective part of decision making. For Timberland organization, the use of linear

programming was able to optimise output when machine hours were limited as well as assist the

managers evaluate the financial viability of introducing new machinery. In the case of Sketchers,

liner programming models were vital in estimating the optimal production point both when

maximizing profits as well as when maximizing the contribution margin. With the introduction

of tools like solver, liner programming can now be applied with ease by managers at different

levels to analyse optimal decisions.

Executive summary

The ability of the managers to make optimal decisions is the difference between excellence and

failure in organizations. One area that needs to be given attention is the production process. For

optimum profitability a firm has to produce enough units to supply the market demand at the

lowest cost possible. This can only be achieved by accounting for the use of all the resources in

the production. In most cases this can be a complex decision affected by several variables. Liner

programming is one of the techniques that can be applied by managers to analyse the situation

and ease the burden of deriving the optimal production points. This study did evaluate the

production decisions of Timberland and Sketchers. In both the firms, it was realized that linear

models are an effective part of decision making. For Timberland organization, the use of linear

programming was able to optimise output when machine hours were limited as well as assist the

managers evaluate the financial viability of introducing new machinery. In the case of Sketchers,

liner programming models were vital in estimating the optimal production point both when

maximizing profits as well as when maximizing the contribution margin. With the introduction

of tools like solver, liner programming can now be applied with ease by managers at different

levels to analyse optimal decisions.

3

Table of Contents

Introduction......................................................................................................................................4

Question 2- Product mix and tactical decisions...............................................................................4

1. Impact of machine constraint................................................................................................4

2. Limitation of machine hours to 12000..................................................................................5

3. Evaluating viability of renting a new machinery..................................................................5

Question 3- Linear programming....................................................................................................7

1. Optimal production using solver..........................................................................................7

2. Ways to improve the contribution margin............................................................................8

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

Table of Contents

Introduction......................................................................................................................................4

Question 2- Product mix and tactical decisions...............................................................................4

1. Impact of machine constraint................................................................................................4

2. Limitation of machine hours to 12000..................................................................................5

3. Evaluating viability of renting a new machinery..................................................................5

Question 3- Linear programming....................................................................................................7

1. Optimal production using solver..........................................................................................7

2. Ways to improve the contribution margin............................................................................8

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

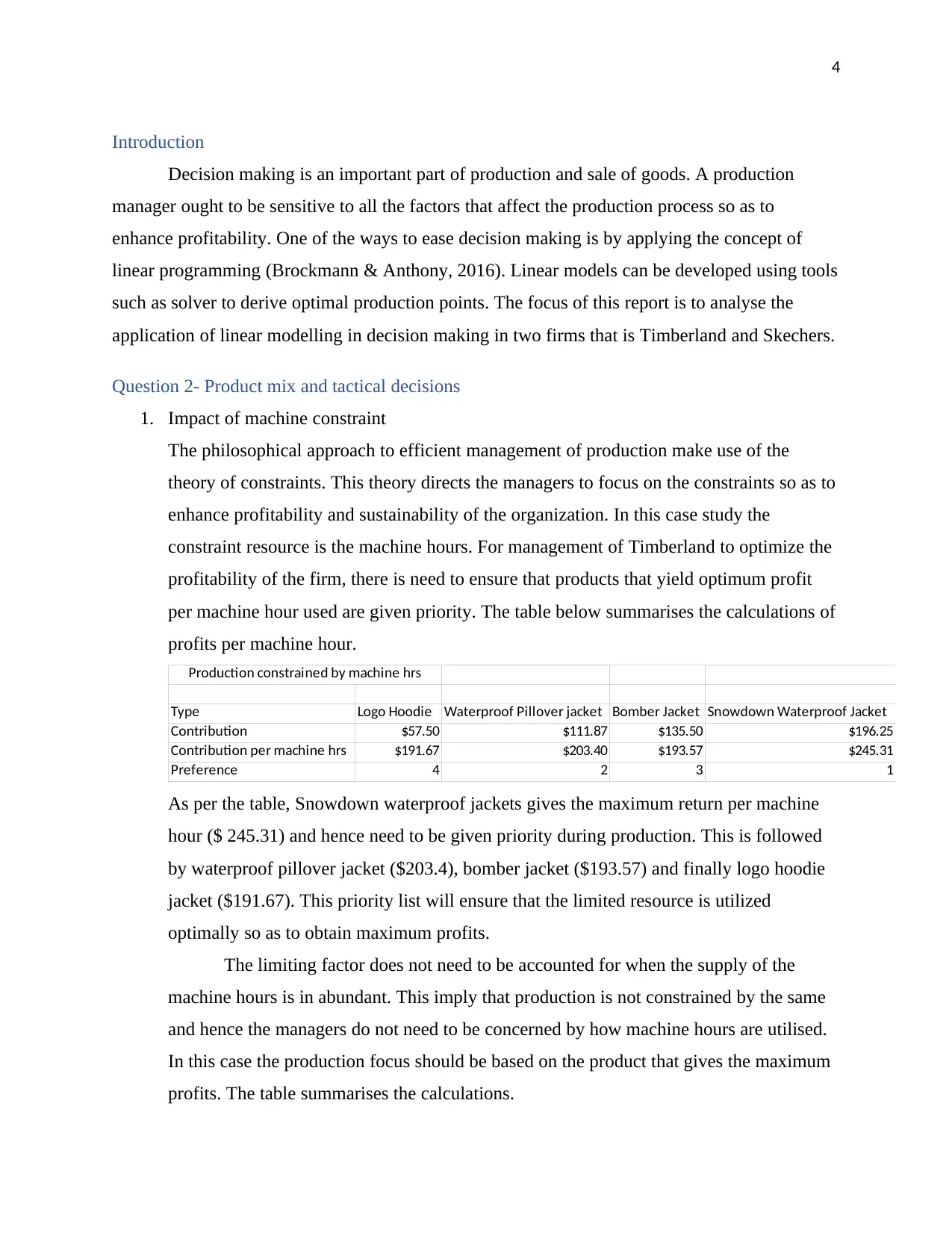

Introduction

Decision making is an important part of production and sale of goods. A production

manager ought to be sensitive to all the factors that affect the production process so as to

enhance profitability. One of the ways to ease decision making is by applying the concept of

linear programming (Brockmann & Anthony, 2016). Linear models can be developed using tools

such as solver to derive optimal production points. The focus of this report is to analyse the

application of linear modelling in decision making in two firms that is Timberland and Skechers.

Question 2- Product mix and tactical decisions

1. Impact of machine constraint

The philosophical approach to efficient management of production make use of the

theory of constraints. This theory directs the managers to focus on the constraints so as to

enhance profitability and sustainability of the organization. In this case study the

constraint resource is the machine hours. For management of Timberland to optimize the

profitability of the firm, there is need to ensure that products that yield optimum profit

per machine hour used are given priority. The table below summarises the calculations of

profits per machine hour.

Type Logo Hoodie Waterproof Pillover jacket Bomber Jacket Snowdown Waterproof Jacket

Contribution $57.50 $111.87 $135.50 $196.25

Contribution per machine hrs $191.67 $203.40 $193.57 $245.31

Preference 4 2 3 1

Production constrained by machine hrs

As per the table, Snowdown waterproof jackets gives the maximum return per machine

hour ($ 245.31) and hence need to be given priority during production. This is followed

by waterproof pillover jacket ($203.4), bomber jacket ($193.57) and finally logo hoodie

jacket ($191.67). This priority list will ensure that the limited resource is utilized

optimally so as to obtain maximum profits.

The limiting factor does not need to be accounted for when the supply of the

machine hours is in abundant. This imply that production is not constrained by the same

and hence the managers do not need to be concerned by how machine hours are utilised.

In this case the production focus should be based on the product that gives the maximum

profits. The table summarises the calculations.

Introduction

Decision making is an important part of production and sale of goods. A production

manager ought to be sensitive to all the factors that affect the production process so as to

enhance profitability. One of the ways to ease decision making is by applying the concept of

linear programming (Brockmann & Anthony, 2016). Linear models can be developed using tools

such as solver to derive optimal production points. The focus of this report is to analyse the

application of linear modelling in decision making in two firms that is Timberland and Skechers.

Question 2- Product mix and tactical decisions

1. Impact of machine constraint

The philosophical approach to efficient management of production make use of the

theory of constraints. This theory directs the managers to focus on the constraints so as to

enhance profitability and sustainability of the organization. In this case study the

constraint resource is the machine hours. For management of Timberland to optimize the

profitability of the firm, there is need to ensure that products that yield optimum profit

per machine hour used are given priority. The table below summarises the calculations of

profits per machine hour.

Type Logo Hoodie Waterproof Pillover jacket Bomber Jacket Snowdown Waterproof Jacket

Contribution $57.50 $111.87 $135.50 $196.25

Contribution per machine hrs $191.67 $203.40 $193.57 $245.31

Preference 4 2 3 1

Production constrained by machine hrs

As per the table, Snowdown waterproof jackets gives the maximum return per machine

hour ($ 245.31) and hence need to be given priority during production. This is followed

by waterproof pillover jacket ($203.4), bomber jacket ($193.57) and finally logo hoodie

jacket ($191.67). This priority list will ensure that the limited resource is utilized

optimally so as to obtain maximum profits.

The limiting factor does not need to be accounted for when the supply of the

machine hours is in abundant. This imply that production is not constrained by the same

and hence the managers do not need to be concerned by how machine hours are utilised.

In this case the production focus should be based on the product that gives the maximum

profits. The table summarises the calculations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Type Logo Hoodie Waterproof Pillover jacket Bomber Jacket Snowdown Waterproof Jacket

Contribution $57.50 $111.87 $135.50 $196.25

Preference 4 3 2 1

Production not constrained by machine hrs

Based on profitability, the snowdown waterproof jackets need to be prioritised during

production as they give the maximum profit of $196.25 per unit. This is followed by

bomber jacket ($ 135.5), waterproof pillover jacket ($111.87) and finally logo hoodie

($57.5). When production is not constrained by the machine hours it implies that the

supply of the resource is enough for all the levels of production. Under this circumstance

the production manager will optimise the revenue of the firm by prioritising the

production of items that yield higher profits.

2. Limitation of machine hours to 12000

The availability of only 12000 machine hours means that the total units produced should

not consume more than 12000 hrs while at the same time yielding optimal profit.

Modelling units produced

Type Logo Hoodie Waterproof Pillover jacket Bomber Jacket Snowdown Waterproof Jacket

Units 3916 7500 5000 4000

Revenue $469,920.00 $1,500,000.00 $1,150,000.00 $1,200,000.00

Costs

Direct material $78,320.00 $262,500.00 $175,000.00 $160,000.00

Direct labour $78,320.00 $187,500.00 $140,000.00 $120,000.00

Variable overhead $58,740.00 $140,625.00 $105,000.00 $90,000.00

Fixed overhead $29,370.00 $70,350.00 $52,500.00 $45,000.00

Total $244,750.00 $660,975.00 $472,500.00 $415,000.00

Constraint Total

Machine hrs 1174.8 4125 3500 3200 11999.8 <= 12000

Annual demand 10000 7500 5000 4000

Profits $225,170.00 $839,025.00 $677,500.00 $785,000.00

Objective function

Total profits $2,526,695.00

Using linear programming modelling as indicated by the table above, the management of

Timberland will obtain optimal profit by producing a total of 3916 units of logo hoodie,

7500 units of waterproof pillover jackets, 5000 units of bomber jackets and 4000 units of

snowdown waterproof jackets. This will yield a total profit of $ 2,526,695. The

production is limited by machine hours and also by the available market.

3. Evaluating viability of renting a new machinery

For the introduction of new machinery to be successful in a manufacturing sector its

impact needs to be assessed both economically, socially as well as environmentally

(Brunton, et al., 2013). Economic analysis of the machinery is done through assessing the

Type Logo Hoodie Waterproof Pillover jacket Bomber Jacket Snowdown Waterproof Jacket

Contribution $57.50 $111.87 $135.50 $196.25

Preference 4 3 2 1

Production not constrained by machine hrs

Based on profitability, the snowdown waterproof jackets need to be prioritised during

production as they give the maximum profit of $196.25 per unit. This is followed by

bomber jacket ($ 135.5), waterproof pillover jacket ($111.87) and finally logo hoodie

($57.5). When production is not constrained by the machine hours it implies that the

supply of the resource is enough for all the levels of production. Under this circumstance

the production manager will optimise the revenue of the firm by prioritising the

production of items that yield higher profits.

2. Limitation of machine hours to 12000

The availability of only 12000 machine hours means that the total units produced should

not consume more than 12000 hrs while at the same time yielding optimal profit.

Modelling units produced

Type Logo Hoodie Waterproof Pillover jacket Bomber Jacket Snowdown Waterproof Jacket

Units 3916 7500 5000 4000

Revenue $469,920.00 $1,500,000.00 $1,150,000.00 $1,200,000.00

Costs

Direct material $78,320.00 $262,500.00 $175,000.00 $160,000.00

Direct labour $78,320.00 $187,500.00 $140,000.00 $120,000.00

Variable overhead $58,740.00 $140,625.00 $105,000.00 $90,000.00

Fixed overhead $29,370.00 $70,350.00 $52,500.00 $45,000.00

Total $244,750.00 $660,975.00 $472,500.00 $415,000.00

Constraint Total

Machine hrs 1174.8 4125 3500 3200 11999.8 <= 12000

Annual demand 10000 7500 5000 4000

Profits $225,170.00 $839,025.00 $677,500.00 $785,000.00

Objective function

Total profits $2,526,695.00

Using linear programming modelling as indicated by the table above, the management of

Timberland will obtain optimal profit by producing a total of 3916 units of logo hoodie,

7500 units of waterproof pillover jackets, 5000 units of bomber jackets and 4000 units of

snowdown waterproof jackets. This will yield a total profit of $ 2,526,695. The

production is limited by machine hours and also by the available market.

3. Evaluating viability of renting a new machinery

For the introduction of new machinery to be successful in a manufacturing sector its

impact needs to be assessed both economically, socially as well as environmentally

(Brunton, et al., 2013). Economic analysis of the machinery is done through assessing the

6

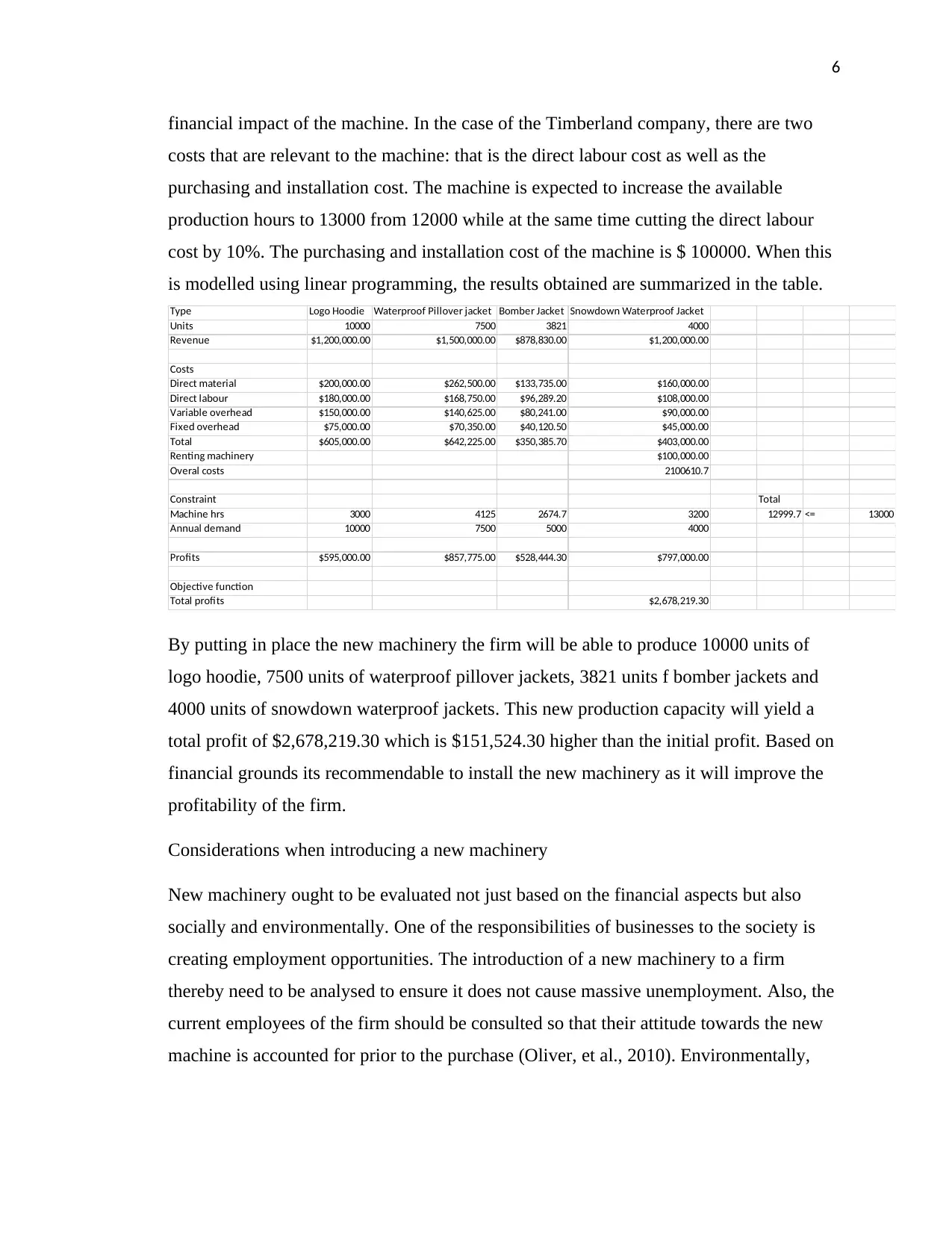

financial impact of the machine. In the case of the Timberland company, there are two

costs that are relevant to the machine: that is the direct labour cost as well as the

purchasing and installation cost. The machine is expected to increase the available

production hours to 13000 from 12000 while at the same time cutting the direct labour

cost by 10%. The purchasing and installation cost of the machine is $ 100000. When this

is modelled using linear programming, the results obtained are summarized in the table.

Type Logo Hoodie Waterproof Pillover jacket Bomber Jacket Snowdown Waterproof Jacket

Units 10000 7500 3821 4000

Revenue $1,200,000.00 $1,500,000.00 $878,830.00 $1,200,000.00

Costs

Direct material $200,000.00 $262,500.00 $133,735.00 $160,000.00

Direct labour $180,000.00 $168,750.00 $96,289.20 $108,000.00

Variable overhead $150,000.00 $140,625.00 $80,241.00 $90,000.00

Fixed overhead $75,000.00 $70,350.00 $40,120.50 $45,000.00

Total $605,000.00 $642,225.00 $350,385.70 $403,000.00

Renting machinery $100,000.00

Overal costs 2100610.7

Constraint Total

Machine hrs 3000 4125 2674.7 3200 12999.7 <= 13000

Annual demand 10000 7500 5000 4000

Profits $595,000.00 $857,775.00 $528,444.30 $797,000.00

Objective function

Total profits $2,678,219.30

By putting in place the new machinery the firm will be able to produce 10000 units of

logo hoodie, 7500 units of waterproof pillover jackets, 3821 units f bomber jackets and

4000 units of snowdown waterproof jackets. This new production capacity will yield a

total profit of $2,678,219.30 which is $151,524.30 higher than the initial profit. Based on

financial grounds its recommendable to install the new machinery as it will improve the

profitability of the firm.

Considerations when introducing a new machinery

New machinery ought to be evaluated not just based on the financial aspects but also

socially and environmentally. One of the responsibilities of businesses to the society is

creating employment opportunities. The introduction of a new machinery to a firm

thereby need to be analysed to ensure it does not cause massive unemployment. Also, the

current employees of the firm should be consulted so that their attitude towards the new

machine is accounted for prior to the purchase (Oliver, et al., 2010). Environmentally,

financial impact of the machine. In the case of the Timberland company, there are two

costs that are relevant to the machine: that is the direct labour cost as well as the

purchasing and installation cost. The machine is expected to increase the available

production hours to 13000 from 12000 while at the same time cutting the direct labour

cost by 10%. The purchasing and installation cost of the machine is $ 100000. When this

is modelled using linear programming, the results obtained are summarized in the table.

Type Logo Hoodie Waterproof Pillover jacket Bomber Jacket Snowdown Waterproof Jacket

Units 10000 7500 3821 4000

Revenue $1,200,000.00 $1,500,000.00 $878,830.00 $1,200,000.00

Costs

Direct material $200,000.00 $262,500.00 $133,735.00 $160,000.00

Direct labour $180,000.00 $168,750.00 $96,289.20 $108,000.00

Variable overhead $150,000.00 $140,625.00 $80,241.00 $90,000.00

Fixed overhead $75,000.00 $70,350.00 $40,120.50 $45,000.00

Total $605,000.00 $642,225.00 $350,385.70 $403,000.00

Renting machinery $100,000.00

Overal costs 2100610.7

Constraint Total

Machine hrs 3000 4125 2674.7 3200 12999.7 <= 13000

Annual demand 10000 7500 5000 4000

Profits $595,000.00 $857,775.00 $528,444.30 $797,000.00

Objective function

Total profits $2,678,219.30

By putting in place the new machinery the firm will be able to produce 10000 units of

logo hoodie, 7500 units of waterproof pillover jackets, 3821 units f bomber jackets and

4000 units of snowdown waterproof jackets. This new production capacity will yield a

total profit of $2,678,219.30 which is $151,524.30 higher than the initial profit. Based on

financial grounds its recommendable to install the new machinery as it will improve the

profitability of the firm.

Considerations when introducing a new machinery

New machinery ought to be evaluated not just based on the financial aspects but also

socially and environmentally. One of the responsibilities of businesses to the society is

creating employment opportunities. The introduction of a new machinery to a firm

thereby need to be analysed to ensure it does not cause massive unemployment. Also, the

current employees of the firm should be consulted so that their attitude towards the new

machine is accounted for prior to the purchase (Oliver, et al., 2010). Environmentally,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

introduction of the new machine needs to be evaluated to ensure it is friendly to the

ecosystem.

Question 3- Linear programming

1. Optimal production using solver

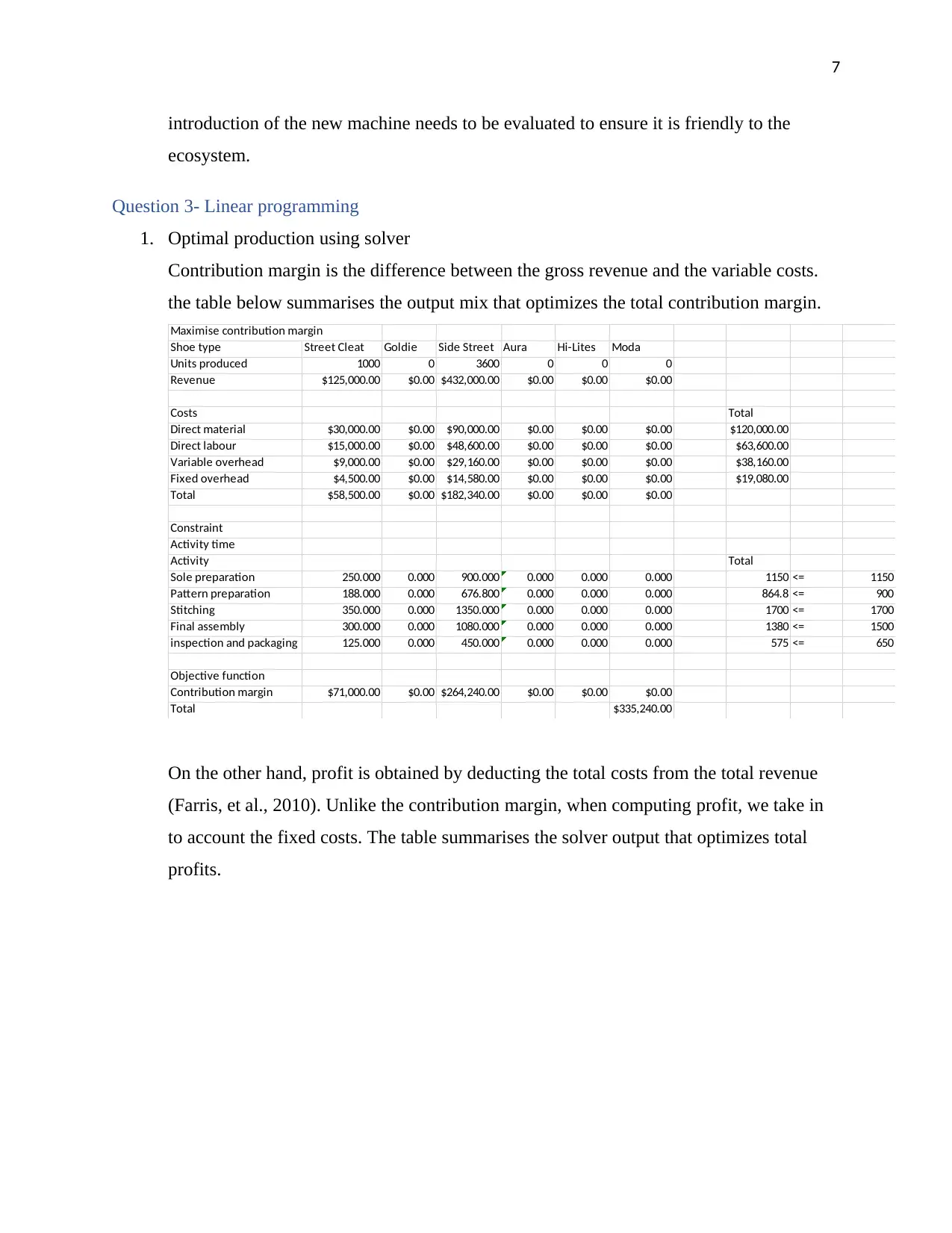

Contribution margin is the difference between the gross revenue and the variable costs.

the table below summarises the output mix that optimizes the total contribution margin.

Maximise contribution margin

Shoe type Street Cleat Goldie Side Street Aura Hi-Lites Moda

Units produced 1000 0 3600 0 0 0

Revenue $125,000.00 $0.00 $432,000.00 $0.00 $0.00 $0.00

Costs Total

Direct material $30,000.00 $0.00 $90,000.00 $0.00 $0.00 $0.00 $120,000.00

Direct labour $15,000.00 $0.00 $48,600.00 $0.00 $0.00 $0.00 $63,600.00

Variable overhead $9,000.00 $0.00 $29,160.00 $0.00 $0.00 $0.00 $38,160.00

Fixed overhead $4,500.00 $0.00 $14,580.00 $0.00 $0.00 $0.00 $19,080.00

Total $58,500.00 $0.00 $182,340.00 $0.00 $0.00 $0.00

Constraint

Activity time

Activity Total

Sole preparation 250.000 0.000 900.000 0.000 0.000 0.000 1150 <= 1150

Pattern preparation 188.000 0.000 676.800 0.000 0.000 0.000 864.8 <= 900

Stitching 350.000 0.000 1350.000 0.000 0.000 0.000 1700 <= 1700

Final assembly 300.000 0.000 1080.000 0.000 0.000 0.000 1380 <= 1500

inspection and packaging 125.000 0.000 450.000 0.000 0.000 0.000 575 <= 650

Objective function

Contribution margin $71,000.00 $0.00 $264,240.00 $0.00 $0.00 $0.00

Total $335,240.00

On the other hand, profit is obtained by deducting the total costs from the total revenue

(Farris, et al., 2010). Unlike the contribution margin, when computing profit, we take in

to account the fixed costs. The table summarises the solver output that optimizes total

profits.

introduction of the new machine needs to be evaluated to ensure it is friendly to the

ecosystem.

Question 3- Linear programming

1. Optimal production using solver

Contribution margin is the difference between the gross revenue and the variable costs.

the table below summarises the output mix that optimizes the total contribution margin.

Maximise contribution margin

Shoe type Street Cleat Goldie Side Street Aura Hi-Lites Moda

Units produced 1000 0 3600 0 0 0

Revenue $125,000.00 $0.00 $432,000.00 $0.00 $0.00 $0.00

Costs Total

Direct material $30,000.00 $0.00 $90,000.00 $0.00 $0.00 $0.00 $120,000.00

Direct labour $15,000.00 $0.00 $48,600.00 $0.00 $0.00 $0.00 $63,600.00

Variable overhead $9,000.00 $0.00 $29,160.00 $0.00 $0.00 $0.00 $38,160.00

Fixed overhead $4,500.00 $0.00 $14,580.00 $0.00 $0.00 $0.00 $19,080.00

Total $58,500.00 $0.00 $182,340.00 $0.00 $0.00 $0.00

Constraint

Activity time

Activity Total

Sole preparation 250.000 0.000 900.000 0.000 0.000 0.000 1150 <= 1150

Pattern preparation 188.000 0.000 676.800 0.000 0.000 0.000 864.8 <= 900

Stitching 350.000 0.000 1350.000 0.000 0.000 0.000 1700 <= 1700

Final assembly 300.000 0.000 1080.000 0.000 0.000 0.000 1380 <= 1500

inspection and packaging 125.000 0.000 450.000 0.000 0.000 0.000 575 <= 650

Objective function

Contribution margin $71,000.00 $0.00 $264,240.00 $0.00 $0.00 $0.00

Total $335,240.00

On the other hand, profit is obtained by deducting the total costs from the total revenue

(Farris, et al., 2010). Unlike the contribution margin, when computing profit, we take in

to account the fixed costs. The table summarises the solver output that optimizes total

profits.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Maximise total profit

Shoe type Street Cleat Goldie Side Street Aura Hi-Lites Moda

Units produced 1000 0 3600 0 0 0

Revenue $125,000.00 $0.00 $432,000.00 $0.00 $0.00 $0.00

Costs Total

Direct material $30,000.00 $0.00 $90,000.00 $0.00 $0.00 $0.00 $120,000.00

Direct labour $15,000.00 $0.00 $48,600.00 $0.00 $0.00 $0.00 $63,600.00

Variable overhead $9,000.00 $0.00 $29,160.00 $0.00 $0.00 $0.00 $38,160.00

Fixed overhead $4,500.00 $0.00 $14,580.00 $0.00 $0.00 $0.00 $19,080.00

Total $58,500.00 $0.00 $182,340.00 $0.00 $0.00 $0.00

Constraint

Activity time

Activity Total

Sole preparation 250.000 0.000 900.000 0.000 0.000 0.000 1150 <= 1150

Pattern preparation 188.000 0.000 676.800 0.000 0.000 0.000 864.8 <= 900

Stitching 350.000 0.000 1350.000 0.000 0.000 0.000 1700 <= 1700

Final assembly 300.000 0.000 1080.000 0.000 0.000 0.000 1380 <= 1500

inspection and packaging 125.000 0.000 450.000 0.000 0.000 0.000 575 <= 650

Objective function

profit $66,500.00 $0.00 $249,660.00 $0.00 $0.00 $0.00

Total $316,160.00

In both the cases return is optimized when 1000 units of street cleat and 3600 units of

side street brands are produced by the firm (Borndörer & & Grötschel, 2012). The

production mix are considered optimal as they lead to maximum return given the

production constraints.

2. Ways to improve the contribution margin

The contribution margin allows a firm to evaluate the amount of profits that is generated

from each product brand that a firm deal in (Tsui, 2011). Increasing the contribution

margin of a product brand means the firm have to increase the amount of profit each

product yields. This can be achieved in 3 main ways:

i. Decreasing the cost of direct material, this can be done by sourcing for materials

from firms that sell at a cheaper price or buying in bulk to take advantage of

economies of scale

ii. Reducing the cost of direct labour, this can be achieved by putting in place less

labour-intensive machinery.

iii. Reducing the variable overhead, this can be attained by proper management

strategies that are aimed at cutting down unnecessary variable overheads and

proper utilization of production support services.

Maximise total profit

Shoe type Street Cleat Goldie Side Street Aura Hi-Lites Moda

Units produced 1000 0 3600 0 0 0

Revenue $125,000.00 $0.00 $432,000.00 $0.00 $0.00 $0.00

Costs Total

Direct material $30,000.00 $0.00 $90,000.00 $0.00 $0.00 $0.00 $120,000.00

Direct labour $15,000.00 $0.00 $48,600.00 $0.00 $0.00 $0.00 $63,600.00

Variable overhead $9,000.00 $0.00 $29,160.00 $0.00 $0.00 $0.00 $38,160.00

Fixed overhead $4,500.00 $0.00 $14,580.00 $0.00 $0.00 $0.00 $19,080.00

Total $58,500.00 $0.00 $182,340.00 $0.00 $0.00 $0.00

Constraint

Activity time

Activity Total

Sole preparation 250.000 0.000 900.000 0.000 0.000 0.000 1150 <= 1150

Pattern preparation 188.000 0.000 676.800 0.000 0.000 0.000 864.8 <= 900

Stitching 350.000 0.000 1350.000 0.000 0.000 0.000 1700 <= 1700

Final assembly 300.000 0.000 1080.000 0.000 0.000 0.000 1380 <= 1500

inspection and packaging 125.000 0.000 450.000 0.000 0.000 0.000 575 <= 650

Objective function

profit $66,500.00 $0.00 $249,660.00 $0.00 $0.00 $0.00

Total $316,160.00

In both the cases return is optimized when 1000 units of street cleat and 3600 units of

side street brands are produced by the firm (Borndörer & & Grötschel, 2012). The

production mix are considered optimal as they lead to maximum return given the

production constraints.

2. Ways to improve the contribution margin

The contribution margin allows a firm to evaluate the amount of profits that is generated

from each product brand that a firm deal in (Tsui, 2011). Increasing the contribution

margin of a product brand means the firm have to increase the amount of profit each

product yields. This can be achieved in 3 main ways:

i. Decreasing the cost of direct material, this can be done by sourcing for materials

from firms that sell at a cheaper price or buying in bulk to take advantage of

economies of scale

ii. Reducing the cost of direct labour, this can be achieved by putting in place less

labour-intensive machinery.

iii. Reducing the variable overhead, this can be attained by proper management

strategies that are aimed at cutting down unnecessary variable overheads and

proper utilization of production support services.

9

Conclusion

For economical and efficient business operation to be achieved in an organisation,

production optimisation needs to be given at most priority. This will improve the competitive

advantage of the form and hence assists in ensuring sustainability. Proper utilization of the

available resources will ensure the business improves its competitive advantage and hence be

able to offer stronger competition for market share. The emergence of technologies such as

solver tools can be of help when it comes to modelling production so as to derive optimal

production mix.

Conclusion

For economical and efficient business operation to be achieved in an organisation,

production optimisation needs to be given at most priority. This will improve the competitive

advantage of the form and hence assists in ensuring sustainability. Proper utilization of the

available resources will ensure the business improves its competitive advantage and hence be

able to offer stronger competition for market share. The emergence of technologies such as

solver tools can be of help when it comes to modelling production so as to derive optimal

production mix.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

References

Borndörer, R. & & Grötschel, M., 2012. Designing telecommunication networks by integer

programming, Berlin: Institut für Mathematik.

Brockmann, E. N. & Anthony, W. P., 2016. Tacit knowledge and strategic decision making. Group &

Organization Management, 27(4), p. 436–455.

Brunton, B. W., Botvinick, M. M. & Brody, C. D., 2013. Rats and humans can optimally accumulate

evidence for decision-making. Science, 340(6128), p. 95–98.

Farris, P. W., Bendle, N. T., Pfeifer, P. E. & R., D. J., 2010. Marketing Metrics: The Definitive Guide to

Measuring Marketing Performance, New Jersey: Pearson Education.

Goldratt, E. M., 2009. Standing on the shoulders of giants: production concepts versus production

applications. The Hitachi Tool Engineering example. Gestão & produção, 16(3), p. 333–343.

Oliver, T. M. et al., 2010. Introducing new technology safely. Qual Saf Health Care , 19(2), pp. i9-i14.

Tsui, T. C., 2011. Interstate Comparison—Use of Contribution Margin in Determination of Price

Fixing. [Online]

Available at: https://works.bepress.com/tatchee_tsui/2/

[Accessed 15 August 2019].

References

Borndörer, R. & & Grötschel, M., 2012. Designing telecommunication networks by integer

programming, Berlin: Institut für Mathematik.

Brockmann, E. N. & Anthony, W. P., 2016. Tacit knowledge and strategic decision making. Group &

Organization Management, 27(4), p. 436–455.

Brunton, B. W., Botvinick, M. M. & Brody, C. D., 2013. Rats and humans can optimally accumulate

evidence for decision-making. Science, 340(6128), p. 95–98.

Farris, P. W., Bendle, N. T., Pfeifer, P. E. & R., D. J., 2010. Marketing Metrics: The Definitive Guide to

Measuring Marketing Performance, New Jersey: Pearson Education.

Goldratt, E. M., 2009. Standing on the shoulders of giants: production concepts versus production

applications. The Hitachi Tool Engineering example. Gestão & produção, 16(3), p. 333–343.

Oliver, T. M. et al., 2010. Introducing new technology safely. Qual Saf Health Care , 19(2), pp. i9-i14.

Tsui, T. C., 2011. Interstate Comparison—Use of Contribution Margin in Determination of Price

Fixing. [Online]

Available at: https://works.bepress.com/tatchee_tsui/2/

[Accessed 15 August 2019].

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.