Comprehensive Analysis of Swap Derivative Instruments in Finance

VerifiedAdded on 2020/04/07

|13

|2875

|146

Report

AI Summary

This report provides a comprehensive overview of swap derivative instruments in finance. It begins with an introduction to derivatives, focusing on swaps as risk management tools. The report details various types of swaps, including interest rate swaps, currency swaps, and others, explaining their functions and applications. It explores the importance of swaps for managing risk, hedging against interest rate changes, and modifying debt obligations. The report also examines the typical users of swaps, such as corporations and financial institutions, and their use as a risk management tool. It covers pricing methods, regulatory effects, and disclosure requirements as per the Securities Exchange Commission. Furthermore, the study applies financial engineering to swap derivative instruments and other securities. The report concludes by summarizing the key aspects of swap derivative instruments and their significance in the financial landscape.

Running head: FINANCE

Finance

Name of the Student:

Name of the University:

Author Note:

Finance

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2FINANCE

Table of Contents

Introduction......................................................................................................................................3

Swap derivative instruments............................................................................................................3

Types of swaps derivative instruments............................................................................................3

Importance of swaps derivative instruments...................................................................................6

Typical users....................................................................................................................................6

Usage as a risk management tool.....................................................................................................7

Pricing..............................................................................................................................................8

Effects of guidelines and Disclosure necessities of the instruments as required by the Securities

Exchange Commission....................................................................................................................8

Applying financial engineering to swap derivative instrument and other securities.......................9

Conclusion.....................................................................................................................................11

Reference List................................................................................................................................12

Table of Contents

Introduction......................................................................................................................................3

Swap derivative instruments............................................................................................................3

Types of swaps derivative instruments............................................................................................3

Importance of swaps derivative instruments...................................................................................6

Typical users....................................................................................................................................6

Usage as a risk management tool.....................................................................................................7

Pricing..............................................................................................................................................8

Effects of guidelines and Disclosure necessities of the instruments as required by the Securities

Exchange Commission....................................................................................................................8

Applying financial engineering to swap derivative instrument and other securities.......................9

Conclusion.....................................................................................................................................11

Reference List................................................................................................................................12

3FINANCE

Introduction

This study deals with discussion of derivative instruments named as forwards, futures,

swaps and options (Weber, 2016). All these derivative instruments work as risk management

instruments where these instruments plays an essential part in managing risk for international

companies as well as portfolio supervisors and recognized depositors. Using these derivative

instruments provide wide range of opportunities to the speculators in and across the world

(Bingham & Kiesel, 2013). The current segment identifies one derivative instrument (swap) for

discussion purpose. There are different types of swap derivative instruments that are commonly

used by the speculators and these are interest rate swaps and currency swaps that are traded over

the counters between fiscal organizations. In addition, these agreements are not traded on

exchanges. Furthermore, retail investors never trade in swaps (Sundaresan & Sushko, 2015). The

current segment proper explains the working of swap derivative instruments in the most efficient

way.

Swap derivative instruments

A swap is one of the derivative contracts that are made between two parties for

exchanging of cash flows in the future (Rahman et al., 2015).

Types of swaps derivative instruments

There are even other types of swaps that are mentioned below with proper justification:

Basis rate swap

Bond swap

Commodity swap

Introduction

This study deals with discussion of derivative instruments named as forwards, futures,

swaps and options (Weber, 2016). All these derivative instruments work as risk management

instruments where these instruments plays an essential part in managing risk for international

companies as well as portfolio supervisors and recognized depositors. Using these derivative

instruments provide wide range of opportunities to the speculators in and across the world

(Bingham & Kiesel, 2013). The current segment identifies one derivative instrument (swap) for

discussion purpose. There are different types of swap derivative instruments that are commonly

used by the speculators and these are interest rate swaps and currency swaps that are traded over

the counters between fiscal organizations. In addition, these agreements are not traded on

exchanges. Furthermore, retail investors never trade in swaps (Sundaresan & Sushko, 2015). The

current segment proper explains the working of swap derivative instruments in the most efficient

way.

Swap derivative instruments

A swap is one of the derivative contracts that are made between two parties for

exchanging of cash flows in the future (Rahman et al., 2015).

Types of swaps derivative instruments

There are even other types of swaps that are mentioned below with proper justification:

Basis rate swap

Bond swap

Commodity swap

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4FINANCE

Credit Default swap

Volatility swap

Interest rate swap

Currency swap

Forex swap

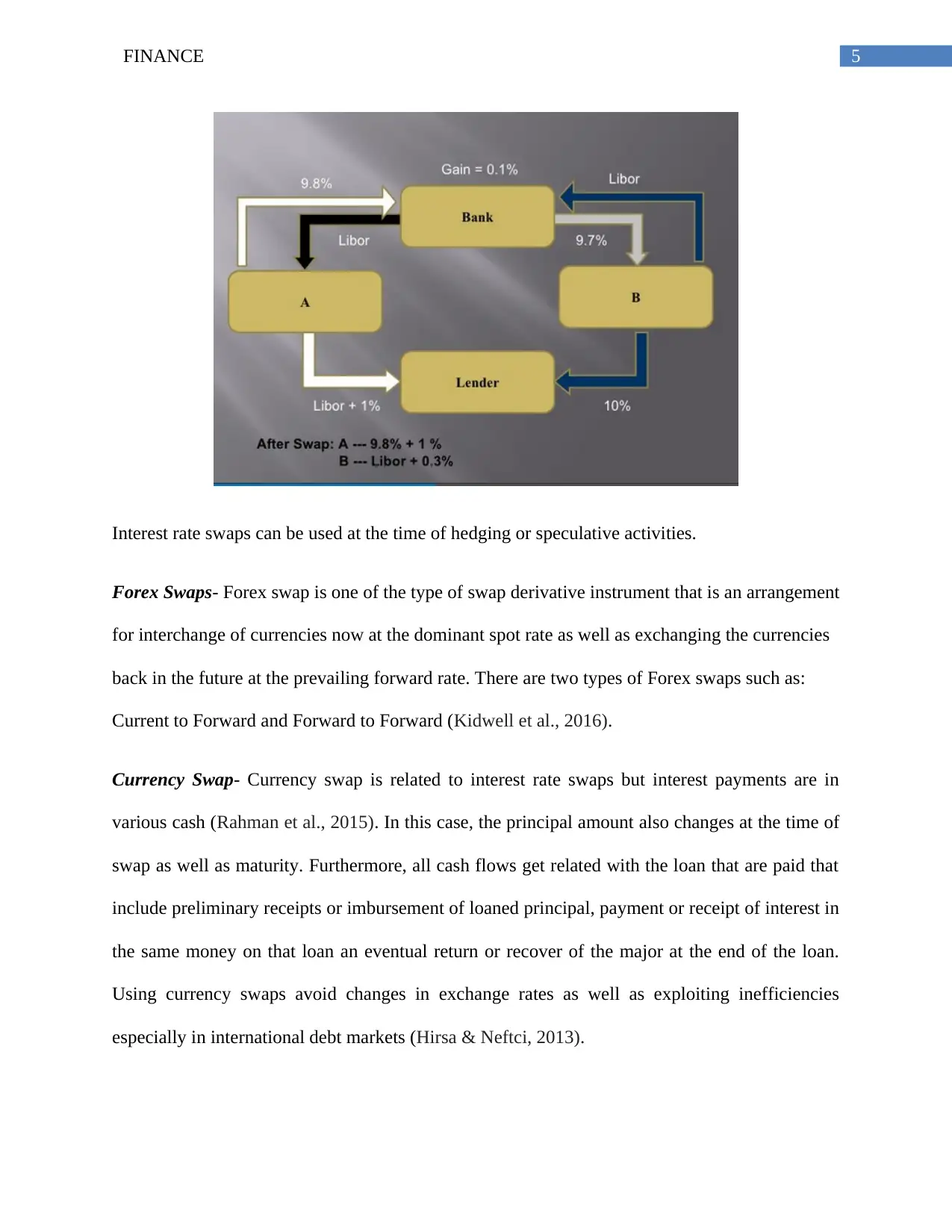

Interest rate swaps- Interest rate swaps is one of the type of swaps derivative instrument that are

essentially exchange of interest payments between two counter parties. There are three kinds of

interest rate swaps that include floating for fixed, fixed for floating and floating for floating. In

this swap, there is no exchange of principal and only coupon movements (Popova & Simkins,

2015).

For instance:

Fixed rate Floating rate

Company A 11% LIBOR+1%

Company B 10% LIBOR+0.5%

Credit Default swap

Volatility swap

Interest rate swap

Currency swap

Forex swap

Interest rate swaps- Interest rate swaps is one of the type of swaps derivative instrument that are

essentially exchange of interest payments between two counter parties. There are three kinds of

interest rate swaps that include floating for fixed, fixed for floating and floating for floating. In

this swap, there is no exchange of principal and only coupon movements (Popova & Simkins,

2015).

For instance:

Fixed rate Floating rate

Company A 11% LIBOR+1%

Company B 10% LIBOR+0.5%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5FINANCE

Interest rate swaps can be used at the time of hedging or speculative activities.

Forex Swaps- Forex swap is one of the type of swap derivative instrument that is an arrangement

for interchange of currencies now at the dominant spot rate as well as exchanging the currencies

back in the future at the prevailing forward rate. There are two types of Forex swaps such as:

Current to Forward and Forward to Forward (Kidwell et al., 2016).

Currency Swap- Currency swap is related to interest rate swaps but interest payments are in

various cash (Rahman et al., 2015). In this case, the principal amount also changes at the time of

swap as well as maturity. Furthermore, all cash flows get related with the loan that are paid that

include preliminary receipts or imbursement of loaned principal, payment or receipt of interest in

the same money on that loan an eventual return or recover of the major at the end of the loan.

Using currency swaps avoid changes in exchange rates as well as exploiting inefficiencies

especially in international debt markets (Hirsa & Neftci, 2013).

Interest rate swaps can be used at the time of hedging or speculative activities.

Forex Swaps- Forex swap is one of the type of swap derivative instrument that is an arrangement

for interchange of currencies now at the dominant spot rate as well as exchanging the currencies

back in the future at the prevailing forward rate. There are two types of Forex swaps such as:

Current to Forward and Forward to Forward (Kidwell et al., 2016).

Currency Swap- Currency swap is related to interest rate swaps but interest payments are in

various cash (Rahman et al., 2015). In this case, the principal amount also changes at the time of

swap as well as maturity. Furthermore, all cash flows get related with the loan that are paid that

include preliminary receipts or imbursement of loaned principal, payment or receipt of interest in

the same money on that loan an eventual return or recover of the major at the end of the loan.

Using currency swaps avoid changes in exchange rates as well as exploiting inefficiencies

especially in international debt markets (Hirsa & Neftci, 2013).

6FINANCE

Importance of swaps derivative instruments

Swaps derivative instruments assist company’s hedge alongside interest rate contact by

reducing insecurity of future cash flows (Rahman et al., 2015). In addition, swapping help

companies for revising their obligation circumstances for taking benefit of present or predictable

upcoming market circumstances. Both currency as well as interest swaps are treated as monetary

tools for lowering the amount needed to service a debt. Currency and interest rate swaps guides

companies for taking benefit of the worldwide markets in an effective way by bringing organized

two parties that already have an benefit in various markets. There are some of the risks

connected with the opportunity where new party fails to meet the current responsibilities and the

paybacks are received by the company at the time of participating in a swap that outweighs the

costs (Gregory, 2014).

Typical users

Swaps derivative instruments are used by Corporations where they use swaps to a

number of various activities in value to a currency or detailed types of cash flows (Rahman et al.,

2015). These particular derivative instruments allow Business Corporation to value from

dealings that would not be likely in a appropriate or lucrative way. Swaps is one of the derivative

instruments that provide Corporations and chance to change the performance of their possessions

without really swapping possession of those resources and exceptionally prevalent as a technique

for managing risk as well as revenue generation. This derivative instrument are generally done

through a swap broker where the business deals in swaps as well as makes money off the bid-ask

spread between the bid price and ask price on these interactions. Spread is the variance between

the bid prices and ask price (Duffie & Stein, 2015).

Importance of swaps derivative instruments

Swaps derivative instruments assist company’s hedge alongside interest rate contact by

reducing insecurity of future cash flows (Rahman et al., 2015). In addition, swapping help

companies for revising their obligation circumstances for taking benefit of present or predictable

upcoming market circumstances. Both currency as well as interest swaps are treated as monetary

tools for lowering the amount needed to service a debt. Currency and interest rate swaps guides

companies for taking benefit of the worldwide markets in an effective way by bringing organized

two parties that already have an benefit in various markets. There are some of the risks

connected with the opportunity where new party fails to meet the current responsibilities and the

paybacks are received by the company at the time of participating in a swap that outweighs the

costs (Gregory, 2014).

Typical users

Swaps derivative instruments are used by Corporations where they use swaps to a

number of various activities in value to a currency or detailed types of cash flows (Rahman et al.,

2015). These particular derivative instruments allow Business Corporation to value from

dealings that would not be likely in a appropriate or lucrative way. Swaps is one of the derivative

instruments that provide Corporations and chance to change the performance of their possessions

without really swapping possession of those resources and exceptionally prevalent as a technique

for managing risk as well as revenue generation. This derivative instrument are generally done

through a swap broker where the business deals in swaps as well as makes money off the bid-ask

spread between the bid price and ask price on these interactions. Spread is the variance between

the bid prices and ask price (Duffie & Stein, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7FINANCE

Usage as a risk management tool

Swaps derivative instruments are used for managing risk in wide variety of ways. Firstly,

individual can use swaps for ensuring satisfactory cash flows either through timing or through

the types of assets that is being exchanged. Timing with the coupon on bonds and assets being

swapped as with foreign altercation swaps that enhances a business establishment has the right

type of money. Therefore, the strict nature of the risk need to be achieved as it be contingent

upon the type of swap being used (Donohoe, 2015).

The simplest way to look at how businesses can use swaps for managing risks after

following simple example by using interest-rate swaps (Duffie & Stein, 2015).

Company A owns $1000000 in fixed rate bonds where the earnings is kept at 5% on annual basis

that is $50,000 in cash flow every year

Company A is of the opinion that interest rates increases at 10% that yields $1000000 annual

cash flows but exchanges all $1000000 for bonds that yields higher rates that itself is costly

affair (Duffie & Stein, 2015)

Company A visit to a swap broker and exchanges rights of the company to the future cash flows.

Company A as well as swap broker together continues to exchange these cash flows over the life

of the swap that ends on a date that is determined at the time of contract is signed ( Duffie &

Stein, 2015).

In this particular instance, it shows that swaps help Company A for managing risk by

making obtainable to Company A where the opportunity of altering its speculation portfolio

Usage as a risk management tool

Swaps derivative instruments are used for managing risk in wide variety of ways. Firstly,

individual can use swaps for ensuring satisfactory cash flows either through timing or through

the types of assets that is being exchanged. Timing with the coupon on bonds and assets being

swapped as with foreign altercation swaps that enhances a business establishment has the right

type of money. Therefore, the strict nature of the risk need to be achieved as it be contingent

upon the type of swap being used (Donohoe, 2015).

The simplest way to look at how businesses can use swaps for managing risks after

following simple example by using interest-rate swaps (Duffie & Stein, 2015).

Company A owns $1000000 in fixed rate bonds where the earnings is kept at 5% on annual basis

that is $50,000 in cash flow every year

Company A is of the opinion that interest rates increases at 10% that yields $1000000 annual

cash flows but exchanges all $1000000 for bonds that yields higher rates that itself is costly

affair (Duffie & Stein, 2015)

Company A visit to a swap broker and exchanges rights of the company to the future cash flows.

Company A as well as swap broker together continues to exchange these cash flows over the life

of the swap that ends on a date that is determined at the time of contract is signed ( Duffie &

Stein, 2015).

In this particular instance, it shows that swaps help Company A for managing risk by

making obtainable to Company A where the opportunity of altering its speculation portfolio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8FINANCE

without any cost and incredible to process for reorganizing ability possession (Cont & Kokholm,

2014).

Consequently, Company A makes an additional $50,000 per year in bond returns. Unlike

other investments, the business also losses money if interest rates for decreasing rather than

increase as Company A projected. It is the responsibility of the swap broker to help various

Business Corporations those benefits from swapping organized in an effective way. Therefore,

swap broker earns money by charging a fee (Choudhry et al., 2014).

Pricing

Currency swaps are priced or valued in same ways as interest rate swaps through use of

discounted cash flow analysis for obtaining zero coupon versions of the swap curves (Duffie &

Stein, 2015). In addition, the currency swaps in real transacts at inception with no net value.

Furthermore, over the life of the instrument, this swap derivative instrument can go in the money

or out of the money or it can stay at the money (Bryan & Rafferty, 2014).

Effects of guidelines and Disclosure necessities of the instruments as required by the

Securities Exchange Commission

Swaps regulation is one of the parts of the Dodd-Frank Act as well as have fallen under

the jurisdiction of different supervisory agencies like Commodity Futures Trading Commission

as well as Securities and Exchange Commission. There are other agencies that address swaps

execution facilities like Financial Services Authority as well as European Commission (Board,

2015).

without any cost and incredible to process for reorganizing ability possession (Cont & Kokholm,

2014).

Consequently, Company A makes an additional $50,000 per year in bond returns. Unlike

other investments, the business also losses money if interest rates for decreasing rather than

increase as Company A projected. It is the responsibility of the swap broker to help various

Business Corporations those benefits from swapping organized in an effective way. Therefore,

swap broker earns money by charging a fee (Choudhry et al., 2014).

Pricing

Currency swaps are priced or valued in same ways as interest rate swaps through use of

discounted cash flow analysis for obtaining zero coupon versions of the swap curves (Duffie &

Stein, 2015). In addition, the currency swaps in real transacts at inception with no net value.

Furthermore, over the life of the instrument, this swap derivative instrument can go in the money

or out of the money or it can stay at the money (Bryan & Rafferty, 2014).

Effects of guidelines and Disclosure necessities of the instruments as required by the

Securities Exchange Commission

Swaps regulation is one of the parts of the Dodd-Frank Act as well as have fallen under

the jurisdiction of different supervisory agencies like Commodity Futures Trading Commission

as well as Securities and Exchange Commission. There are other agencies that address swaps

execution facilities like Financial Services Authority as well as European Commission (Board,

2015).

9FINANCE

The General Disclosure Statement for Transactions that goes together with the Interest

Rate Derivatives Disclosures that contains significant information and disclosures on matters

relating to associated material risks, features, conflicts of interest as well as incentives (Duffie &

Stein, 2015). It is the responsibility of the swap dealer to either disclose or furnish at the time of

transacting activities. Individuals need to review carefully information as well as disclosures

before entering into any swap derivative instruments. There are terms used for interest rate swap

that enter in general way for determining statement. The standard forms of interest rate swaps

confirmation as it is ready available that include IRS Confirmation, IRS Confirmation with

embedded floor, Rate Cap Confirmation as well as Swaption Confirmation (Bingham & Kiesel,

2013).

Applying financial engineering to swap derivative instrument and other securities

The price of shedding risk can be treated as other risk that gives some upside potential of

the future transactions or in simple terms rate movement (Battiston et al., 2013). The allegations

explain some of the recent cases that leverage swaps that underscore the need for making such

understanding in a clear ways. Swap agreements can be termed as one of the prevalent types of

over the counter derivative contracts (Choudhry et al., 2014). The popularity of the market stems

comes from financial success where the market participants have experienced by making use of

swap agreements for managing risks in association with the commercial and financing

transactions. As far as financial engineering is concerned, it is important for the swap dealers to

identify as well as isolate with different risks in association with financial portfolios by

developing swap agreements that mainly address risks. There are numerous market contributors

that in actually had incurred considerable losses from trading swap agreements. Furthermore, the

The General Disclosure Statement for Transactions that goes together with the Interest

Rate Derivatives Disclosures that contains significant information and disclosures on matters

relating to associated material risks, features, conflicts of interest as well as incentives (Duffie &

Stein, 2015). It is the responsibility of the swap dealer to either disclose or furnish at the time of

transacting activities. Individuals need to review carefully information as well as disclosures

before entering into any swap derivative instruments. There are terms used for interest rate swap

that enter in general way for determining statement. The standard forms of interest rate swaps

confirmation as it is ready available that include IRS Confirmation, IRS Confirmation with

embedded floor, Rate Cap Confirmation as well as Swaption Confirmation (Bingham & Kiesel,

2013).

Applying financial engineering to swap derivative instrument and other securities

The price of shedding risk can be treated as other risk that gives some upside potential of

the future transactions or in simple terms rate movement (Battiston et al., 2013). The allegations

explain some of the recent cases that leverage swaps that underscore the need for making such

understanding in a clear ways. Swap agreements can be termed as one of the prevalent types of

over the counter derivative contracts (Choudhry et al., 2014). The popularity of the market stems

comes from financial success where the market participants have experienced by making use of

swap agreements for managing risks in association with the commercial and financing

transactions. As far as financial engineering is concerned, it is important for the swap dealers to

identify as well as isolate with different risks in association with financial portfolios by

developing swap agreements that mainly address risks. There are numerous market contributors

that in actually had incurred considerable losses from trading swap agreements. Furthermore, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10FINANCE

remarkable progression of the market gets along with the losses that took place on matters

relating to swap market that need regulations (Bingham & Kiesel, 2013).

Currently, it is noted that the swap dealings are not subject to any of the single

supervisory agenda. In addition, the swap transactions are mainly regulated to the extent to

which market contributors starts trading with these dealings that are controlled on regular basis

(Araujo & Leão, 2016). For instance, banks that are major OTC derivative dealers that are

overseen by federal bank controllers as it is subject to specific supervisory necessities where the

regulators are exposed

There are other major swap dealers where the insurance companies as well as securities

firms are subject to limited or federal oversight (Battiston et al., 2013). In addition, the outdated

method used for adaptable the financial markets that had been allocated by the supervisory

consultant of new monetary products that are based on whether the product falls within the

description of a safety or a futures

It is important to classify swap agreements as futures or securities as it differentiate in

both securities as well as futures (Choudhry et al., 2014). In addition, the OTC derivatives

market deals with pioneering market that projects financial instruments that are generally tailored

for meeting fiscal needs of counterparties. This type of instruments cannot be classified into

future or securities. It need subjecting to these instruments that exist from securities or

commodities laws that streamlines product developments as well as it prevent OTC derivative

dealers from competing efficiently with the foreign OTC derivatives that are subject to less

preventive instruction (Battiston et al., 2013).

remarkable progression of the market gets along with the losses that took place on matters

relating to swap market that need regulations (Bingham & Kiesel, 2013).

Currently, it is noted that the swap dealings are not subject to any of the single

supervisory agenda. In addition, the swap transactions are mainly regulated to the extent to

which market contributors starts trading with these dealings that are controlled on regular basis

(Araujo & Leão, 2016). For instance, banks that are major OTC derivative dealers that are

overseen by federal bank controllers as it is subject to specific supervisory necessities where the

regulators are exposed

There are other major swap dealers where the insurance companies as well as securities

firms are subject to limited or federal oversight (Battiston et al., 2013). In addition, the outdated

method used for adaptable the financial markets that had been allocated by the supervisory

consultant of new monetary products that are based on whether the product falls within the

description of a safety or a futures

It is important to classify swap agreements as futures or securities as it differentiate in

both securities as well as futures (Choudhry et al., 2014). In addition, the OTC derivatives

market deals with pioneering market that projects financial instruments that are generally tailored

for meeting fiscal needs of counterparties. This type of instruments cannot be classified into

future or securities. It need subjecting to these instruments that exist from securities or

commodities laws that streamlines product developments as well as it prevent OTC derivative

dealers from competing efficiently with the foreign OTC derivatives that are subject to less

preventive instruction (Battiston et al., 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11FINANCE

Conclusion

At the end of the study, it is concluded that swap derivative instruments had been

properly discussed in the study. The above analysis explains the types of swap derivative

instruments and how far it is important in real life. Swap derivative instruments is a risk

management tool that are used by Multinational Corporation, portfolio managers as well as

institutional investors. At the time of pursuing opportunities, it is important to cause revenue

through swaps derivative instruments where the procedure is no different. The swap is to take

benefits of differentials in the spot as well as anticipates future values in relation to swap

derivative instruments. It is not very much difficult to measure the value of swap. At the time of

estimating the future value, the calculations takes into account the time value of money as well

as probability of event occurrences that are treated for making the estimation of value of futures.

Therefore, the swap is nothing more than a grouping of spot rate interchange as well as future

exchange in a single contract.

Conclusion

At the end of the study, it is concluded that swap derivative instruments had been

properly discussed in the study. The above analysis explains the types of swap derivative

instruments and how far it is important in real life. Swap derivative instruments is a risk

management tool that are used by Multinational Corporation, portfolio managers as well as

institutional investors. At the time of pursuing opportunities, it is important to cause revenue

through swaps derivative instruments where the procedure is no different. The swap is to take

benefits of differentials in the spot as well as anticipates future values in relation to swap

derivative instruments. It is not very much difficult to measure the value of swap. At the time of

estimating the future value, the calculations takes into account the time value of money as well

as probability of event occurrences that are treated for making the estimation of value of futures.

Therefore, the swap is nothing more than a grouping of spot rate interchange as well as future

exchange in a single contract.

12FINANCE

Reference List

Araujo, G. S., & Leão, S. (2016). OTC derivatives: Impacts of regulatory changes in the non-

financial sector. Journal of Financial Stability, 25, 132-149.

Battiston, S., Caldarelli, G., Georg, C. P., May, R., & Stiglitz, J. (2013). Complex

derivatives. Nature Physics, 9, 123-125.

Bingham, N. H., & Kiesel, R. (2013). Risk-neutral valuation: Pricing and hedging of financial

derivatives. Springer Science & Business Media.

Board, F. S. (2015). OTC derivatives market reforms. Ninth progress report on

implementation, 24.

Bryan, D., & Rafferty, M. (2014). Financial derivatives as social policy beyond

crisis. Sociology, 48(5), 887-903.

Choudhry, M., Moskovic, D., Wong, M., Baig, S., Liu, Z., Lizzio, M., & Voicu, A. (2014).

Credit Derivatives I: Instruments and Applications. Fixed Income Markets: Management,

Trading, Hedging, Second Edition, 375-419.

Cont, R., & Kokholm, T. (2014). Central clearing of OTC derivatives: bilateral vs multilateral

netting. Statistics & Risk Modeling, 31(1), 3-22.

Donohoe, M. P. (2015). The economic effects of financial derivatives on corporate tax

avoidance. Journal of Accounting and Economics, 59(1), 1-24.

Duffie, D., & Stein, J. C. (2015). Reforming LIBOR and other financial market benchmarks. The

Journal of Economic Perspectives, 29(2), 191-212.

Reference List

Araujo, G. S., & Leão, S. (2016). OTC derivatives: Impacts of regulatory changes in the non-

financial sector. Journal of Financial Stability, 25, 132-149.

Battiston, S., Caldarelli, G., Georg, C. P., May, R., & Stiglitz, J. (2013). Complex

derivatives. Nature Physics, 9, 123-125.

Bingham, N. H., & Kiesel, R. (2013). Risk-neutral valuation: Pricing and hedging of financial

derivatives. Springer Science & Business Media.

Board, F. S. (2015). OTC derivatives market reforms. Ninth progress report on

implementation, 24.

Bryan, D., & Rafferty, M. (2014). Financial derivatives as social policy beyond

crisis. Sociology, 48(5), 887-903.

Choudhry, M., Moskovic, D., Wong, M., Baig, S., Liu, Z., Lizzio, M., & Voicu, A. (2014).

Credit Derivatives I: Instruments and Applications. Fixed Income Markets: Management,

Trading, Hedging, Second Edition, 375-419.

Cont, R., & Kokholm, T. (2014). Central clearing of OTC derivatives: bilateral vs multilateral

netting. Statistics & Risk Modeling, 31(1), 3-22.

Donohoe, M. P. (2015). The economic effects of financial derivatives on corporate tax

avoidance. Journal of Accounting and Economics, 59(1), 1-24.

Duffie, D., & Stein, J. C. (2015). Reforming LIBOR and other financial market benchmarks. The

Journal of Economic Perspectives, 29(2), 191-212.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.