Sweet Menu Restaurant: Sources of Finance and Financial Planning

VerifiedAdded on 2020/02/03

|15

|4203

|26

Report

AI Summary

This report provides a comprehensive financial analysis of Sweet Menu Restaurant, focusing on its expansion plans. It explores various sources of finance, including internal sources like retained earnings and external sources such as long-term bank loans and the issue of shares, evaluating their implications and suitability for the restaurant's expansion. The report delves into the costs associated with different financing options, emphasizing the importance of financial planning for effective resource utilization, cash management, and investment decisions. It also examines the information needs of different decision-makers, including investors, suppliers, and the government, and assesses the impact of financing choices on financial statements, including profit and loss accounts and balance sheets. Furthermore, the report analyzes budgeting, unit cost calculations, project viability, and the interpretation of financial statements, offering a detailed understanding of the restaurant's financial operations and strategic decision-making processes.

MFRD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Sources of finance available to business................................................................................3

1.2 Implications of the sources of finance...................................................................................4

1.3 Most appropriate sources of finance for Sweet Menu Restaurant expansion plans..............4

TASK 2............................................................................................................................................5

2.1 Costs of different sources of finance.....................................................................................5

2.2 Importance of financial planning for Sweet Menu Restaurant..............................................6

2.3 Information needs of different decision makers in Sweet Menu Restaurant.........................7

2.4 Impact of sources of finance on financial statements............................................................7

TASK 3............................................................................................................................................8

3.1 Analysis of budget and appropriate decision making............................................................8

3.2 Calculation of unit costs and making pricing decisions.........................................................9

3.3 Assessing the viability of projects.........................................................................................9

TASK 4..........................................................................................................................................11

4.1 Main financial statements....................................................................................................11

4.2 Comparing formats of financial statements for different types of business........................11

4.3 Interpretation of financial statements of two restaurant using ratios...................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

2

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Sources of finance available to business................................................................................3

1.2 Implications of the sources of finance...................................................................................4

1.3 Most appropriate sources of finance for Sweet Menu Restaurant expansion plans..............4

TASK 2............................................................................................................................................5

2.1 Costs of different sources of finance.....................................................................................5

2.2 Importance of financial planning for Sweet Menu Restaurant..............................................6

2.3 Information needs of different decision makers in Sweet Menu Restaurant.........................7

2.4 Impact of sources of finance on financial statements............................................................7

TASK 3............................................................................................................................................8

3.1 Analysis of budget and appropriate decision making............................................................8

3.2 Calculation of unit costs and making pricing decisions.........................................................9

3.3 Assessing the viability of projects.........................................................................................9

TASK 4..........................................................................................................................................11

4.1 Main financial statements....................................................................................................11

4.2 Comparing formats of financial statements for different types of business........................11

4.3 Interpretation of financial statements of two restaurant using ratios...................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

2

INTRODUCTION

Management of finances is referred to as planning, organizing, directing as well as

controlling financial activities that relates with the procurement and utilization of funds of the

business. It can be meant as application of general management principles to financial resources

of the organization (The financial plan, 2014). In the present study, management of financial

resources has been discussed in context of Sweet Menu Restaurant. The organization is reputed

restaurant that is located in Gants Hill of East London. The present report entails to understand

the financial sources available with the business. Further, it involves implications of finance as

resources within the corporation.

TASK 1

1.1 Sources of finance available to business

In accordance with case, Sweet Menu Restaurant is a reputed business firm that is

engaged in offering inter-continental menus at economical rates. A plan has been developed by

the enterprise regarding opening of two branches in Central London and in Croydon. It has been

determined that outlet needs £300,000 and £500,000 to start up new restaurant at different

locations. For this, the organization needs to acquire funds from financial sources which have

been stated as under:

Internal sources

Retained earning It is considered as a part of profit that is saved

for the purpose of meeting contingencies for

future (Avlonitis and Indounas, 2005). Such

source can be used by Sweet Menu Restaurant

with an aim to fulfill its financial needs to a

significant level.

External sources

Long term bank loan Financial institutions are considered as most

suitable source that offers funds to the

businesses for particular duration time. With

3

Management of finances is referred to as planning, organizing, directing as well as

controlling financial activities that relates with the procurement and utilization of funds of the

business. It can be meant as application of general management principles to financial resources

of the organization (The financial plan, 2014). In the present study, management of financial

resources has been discussed in context of Sweet Menu Restaurant. The organization is reputed

restaurant that is located in Gants Hill of East London. The present report entails to understand

the financial sources available with the business. Further, it involves implications of finance as

resources within the corporation.

TASK 1

1.1 Sources of finance available to business

In accordance with case, Sweet Menu Restaurant is a reputed business firm that is

engaged in offering inter-continental menus at economical rates. A plan has been developed by

the enterprise regarding opening of two branches in Central London and in Croydon. It has been

determined that outlet needs £300,000 and £500,000 to start up new restaurant at different

locations. For this, the organization needs to acquire funds from financial sources which have

been stated as under:

Internal sources

Retained earning It is considered as a part of profit that is saved

for the purpose of meeting contingencies for

future (Avlonitis and Indounas, 2005). Such

source can be used by Sweet Menu Restaurant

with an aim to fulfill its financial needs to a

significant level.

External sources

Long term bank loan Financial institutions are considered as most

suitable source that offers funds to the

businesses for particular duration time. With

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the assistance of this, long term needs of new

concern can be accomplished (Bennouna and

et.al, 2010). The usage of funds can be done

for the purpose of carrying out business

operations.

Issue of shares It is regarded as an external financial source in

which firm acquires long term financial

resources from the public (Drury, 2009). The

funds that are obtained by restaurant can be

used as start-up capital by the new business.

1.2 Implications of the sources of finance

There are certain implications of the financial sources that are possessed by the newly

formed organization. In situation, when the organization makes use of amount from personal

saving then implication to such relates with dilution of control. This denotes that control over the

funds is lost by the individual which could have been used for the purpose of accomplishing

organizational requirements for future term.

Along with this there is an existence of certain implications that can result in situation

when funds are acquired by new concern from external sources. With the aim to start up new

concern, loan can be taken by Sweet Menu Restaurant. This requires company to keep some

assets for security (Eccles and Holt, 2005). In case, when payment of interest is not done within

specified duration of time then financial institution can take legal actions against the firm. Along

with this, bank can mortgage assets of the corporation with an aim to recover the amount

borrowed as loan. In case, if the recovery of the loan amount is not done from assets then

company is declared to be bankrupt. Such has huge impact on the credit rating of the firm.

Moreover, it results in affecting the goodwill of the business to a significant level (Helliar and

et.al, 2005). The funds can be obtained through issue of shares. For this, organization needs to

make timely payment of dividend to shareholders from part of profit. In case of non-fulfillment

4

concern can be accomplished (Bennouna and

et.al, 2010). The usage of funds can be done

for the purpose of carrying out business

operations.

Issue of shares It is regarded as an external financial source in

which firm acquires long term financial

resources from the public (Drury, 2009). The

funds that are obtained by restaurant can be

used as start-up capital by the new business.

1.2 Implications of the sources of finance

There are certain implications of the financial sources that are possessed by the newly

formed organization. In situation, when the organization makes use of amount from personal

saving then implication to such relates with dilution of control. This denotes that control over the

funds is lost by the individual which could have been used for the purpose of accomplishing

organizational requirements for future term.

Along with this there is an existence of certain implications that can result in situation

when funds are acquired by new concern from external sources. With the aim to start up new

concern, loan can be taken by Sweet Menu Restaurant. This requires company to keep some

assets for security (Eccles and Holt, 2005). In case, when payment of interest is not done within

specified duration of time then financial institution can take legal actions against the firm. Along

with this, bank can mortgage assets of the corporation with an aim to recover the amount

borrowed as loan. In case, if the recovery of the loan amount is not done from assets then

company is declared to be bankrupt. Such has huge impact on the credit rating of the firm.

Moreover, it results in affecting the goodwill of the business to a significant level (Helliar and

et.al, 2005). The funds can be obtained through issue of shares. For this, organization needs to

make timely payment of dividend to shareholders from part of profit. In case of non-fulfillment

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of this, legal actions can be taken by shareholders against new concern that can affect its survival

in the market for longer term.

1.3 Most appropriate sources of finance for Sweet Menu Restaurant expansion plans

In order to start up new business the most suitable sources of finance for Sweet Menu

Restaurant expansion plan have been enumerated in the manner below: Issue of shares: Through issuance of shares new concern can obtain long term funds from

public. It is regarded as permanent source of capital for corporation. Sweet Menu

Restaurant is required to make payment of dividend from profitability amount for the

funds invested by public (Ismail and et.al. 2005). This would result in decreasing the

profitability of the business to a greater extent. However, it assists in fulfilling the

financials requirements of the firm in an effective manner.

Bank loan: With the aim to conduct business operation, it is essential for a firm to acquire

financial resources from the bank. The amount that is borrowed as loan is for fixed

duration of time. However, with an aim to obtain the funds, organization needs to pay

interest on the loan amount. With this, corporation can fulfill its needs to meet future

contingencies in an appropriate manner. Along with this, it is regarded as a suitable

source that can assist Sweet Menu Restaurant in accomplishing its short, medium as well

as long term requirements.

TASK 2

2.1 Costs of different sources of finance

There is presence of several costs that are attached with different sources. These have

been presented below:

Opportunity cost It is considered as the cost of sacrificing which

is being incurred by the business when it let go

another best alternative (Shahwan, 2008). The

amount of retained earnings could have been

utilized by new concern towards

accomplishment of its future needs. This is

regarded as loss to the firm as the amount can

5

in the market for longer term.

1.3 Most appropriate sources of finance for Sweet Menu Restaurant expansion plans

In order to start up new business the most suitable sources of finance for Sweet Menu

Restaurant expansion plan have been enumerated in the manner below: Issue of shares: Through issuance of shares new concern can obtain long term funds from

public. It is regarded as permanent source of capital for corporation. Sweet Menu

Restaurant is required to make payment of dividend from profitability amount for the

funds invested by public (Ismail and et.al. 2005). This would result in decreasing the

profitability of the business to a greater extent. However, it assists in fulfilling the

financials requirements of the firm in an effective manner.

Bank loan: With the aim to conduct business operation, it is essential for a firm to acquire

financial resources from the bank. The amount that is borrowed as loan is for fixed

duration of time. However, with an aim to obtain the funds, organization needs to pay

interest on the loan amount. With this, corporation can fulfill its needs to meet future

contingencies in an appropriate manner. Along with this, it is regarded as a suitable

source that can assist Sweet Menu Restaurant in accomplishing its short, medium as well

as long term requirements.

TASK 2

2.1 Costs of different sources of finance

There is presence of several costs that are attached with different sources. These have

been presented below:

Opportunity cost It is considered as the cost of sacrificing which

is being incurred by the business when it let go

another best alternative (Shahwan, 2008). The

amount of retained earnings could have been

utilized by new concern towards

accomplishment of its future needs. This is

regarded as loss to the firm as the amount can

5

be used for financing crucial activities of the

business.

Interest With an aim to start up new business,

organization can take long term loans from

financial institutions. Interest is the cost

attached with such sources. It is essential for

Sweet Menu Restaurant to make timely

payment of interest to bank as a cost of

obtaining loan amount.

Dividends Through issuance of shares to the public,

organization can acquire funds for fulfillment

of long term needs. It is significant for Sweet

Menu Restaurant to pay certain amount as

dividend from part of profit in return of amount

borrowed from shareholders (Shim, 2008).

However it can result in decreasing the

profitability of Sweet Menu Restaurant to a

greater extent.

2.2 Importance of financial planning for Sweet Menu Restaurant

There is presence of greater importance of financial planning for the firm like Sweet

Menu Restaurant that has been discussed under: Effective utilization of financial resources: There is greater role of financial planning in

relation with effective as well as efficient utilization of resources. With the assistance of

this financial manager can take suitable decisions towards allocation of resources in

various activities of new business. Through budget planning organization can attain

success for longer run. Ensures management of cash: There has been huge significance of financial planning in

relation cash management. With this, Sweet Menu Restaurant can manage its outflow of

6

business.

Interest With an aim to start up new business,

organization can take long term loans from

financial institutions. Interest is the cost

attached with such sources. It is essential for

Sweet Menu Restaurant to make timely

payment of interest to bank as a cost of

obtaining loan amount.

Dividends Through issuance of shares to the public,

organization can acquire funds for fulfillment

of long term needs. It is significant for Sweet

Menu Restaurant to pay certain amount as

dividend from part of profit in return of amount

borrowed from shareholders (Shim, 2008).

However it can result in decreasing the

profitability of Sweet Menu Restaurant to a

greater extent.

2.2 Importance of financial planning for Sweet Menu Restaurant

There is presence of greater importance of financial planning for the firm like Sweet

Menu Restaurant that has been discussed under: Effective utilization of financial resources: There is greater role of financial planning in

relation with effective as well as efficient utilization of resources. With the assistance of

this financial manager can take suitable decisions towards allocation of resources in

various activities of new business. Through budget planning organization can attain

success for longer run. Ensures management of cash: There has been huge significance of financial planning in

relation cash management. With this, Sweet Menu Restaurant can manage its outflow of

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cash. In contrast to this, it also assists in managing the inflow of cash within firm. Thus,

growth and expansion of business operations can be ensured with the assistance financial

planning.

Assist in making selection of right investment option: It is important for Sweet Menu

Restaurant to choose right investment proposal. This can be carried out through

effectively through financial planning (Gaskell and Ashton, 2008). This is due to reason

that it acts as an aid in making evaluation of the investment based upon risk, objectives

etc. Such has major role in providing direction to the firm in relation to selection of most

appropriate option for investment that assist in accomplishment pre-defined targets.

2.3 Information needs of different decision makers in Sweet Menu Restaurant

In order to take decisions the users of information requires several information with

respect to business. Decision makers with their information needs have been enumerated in the

manner below: Investor: They need information regarding the profitability as well as efficiency position

of the business. Through this investor can make decision regarding the corporation where

investment can be made. It is essential that valuable return is provided to the investor in

return of the amount invested by them. Because of such profitability information plays

significant role for investor as it assist them in process of decision making. Supplier: It includes decision makers who provide inputs in raw material form to the

business. They require information regarding the credit rating of the organization (Prieto,

2006). Moreover with this information they can design tactical plan that are related with

deciding on whether input can be offered or not. Because of such reason business is

required to make timely payment of supplier's invoices.

Government: The information needed by regulatory authority is in relation with

profitability. Through this government can determine the tax amount that Sweet Menu

Restaurant is required to pay. Further investigation is done on whether the tax amount is

deposited or not. Through this government can conduct strategic operations that include

development of plan for next move of organization.

7

growth and expansion of business operations can be ensured with the assistance financial

planning.

Assist in making selection of right investment option: It is important for Sweet Menu

Restaurant to choose right investment proposal. This can be carried out through

effectively through financial planning (Gaskell and Ashton, 2008). This is due to reason

that it acts as an aid in making evaluation of the investment based upon risk, objectives

etc. Such has major role in providing direction to the firm in relation to selection of most

appropriate option for investment that assist in accomplishment pre-defined targets.

2.3 Information needs of different decision makers in Sweet Menu Restaurant

In order to take decisions the users of information requires several information with

respect to business. Decision makers with their information needs have been enumerated in the

manner below: Investor: They need information regarding the profitability as well as efficiency position

of the business. Through this investor can make decision regarding the corporation where

investment can be made. It is essential that valuable return is provided to the investor in

return of the amount invested by them. Because of such profitability information plays

significant role for investor as it assist them in process of decision making. Supplier: It includes decision makers who provide inputs in raw material form to the

business. They require information regarding the credit rating of the organization (Prieto,

2006). Moreover with this information they can design tactical plan that are related with

deciding on whether input can be offered or not. Because of such reason business is

required to make timely payment of supplier's invoices.

Government: The information needed by regulatory authority is in relation with

profitability. Through this government can determine the tax amount that Sweet Menu

Restaurant is required to pay. Further investigation is done on whether the tax amount is

deposited or not. Through this government can conduct strategic operations that include

development of plan for next move of organization.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.4 Impact of sources of finance on financial statements

Financial statements involve the transactions that are being carried out by the business. It

includes financial and operating transactions. Sweet Menu Restaurant makes use of different

financial sources that affects the balance sheet of the organization. Moreover the cost attached

with the financial sources influence the profit and loss statement to a significant level. As stated

above the most suitable financial sources involves issue of shares, retained earnings and loan

from bank. The cost associated with internal sources is opportunity cost which is not

demonstrated in profit and loss account. However it is demonstrated in statement of changes

under retained earnings.

Along with this bank loan includes the cost of interest which is regarded as expense of

organization. It is represented on the expenditure side of profitability statement. Further in

balance sheet it is deducted from cash under the head of current asset. In accordance with the

provided scenario, profit and loss account involves cost. Moreover the interest will be subtracted

from the cash amount whereas funds acquired are demonstrated on the liability side in balance

sheet (Rasid and et.al, 2011). For Sweet Menu Restaurant loan amount will be reflected under

head of noncurrent liabilities as long term loan. This amount enhances the cash with the firm

which is presented on asset side. In situation of issuance of shares dividend paid to shareholders

will be presented in profit and loss account. Moreover the amount borrowed from public is

considered liability and is shown in balance sheet. The analysis carried above presents that for

Sweet Menu Restaurant loan from bank and retained earnings are suitable sources of finance. As

such can assist in opening of new branches by business.

TASK 3

3.1 Analysis of budget and appropriate decision making

The cash as well as inventory budget of Blue Island Restaurant has been presented for the

next four months. The company offers huge competition to Sweet Menu Restaurant. Cash budget

analysis can be conducted through determination of changes in the cash incomes as well as

expenses. It has been determined that estimated figure demonstrates the sales contributed

towards the cash incomes of business (Tektas, Gunay and Gunay, 2005). As per the budget it can

be stated that there is increase in cash sales in every month. In the month of November the sales

are increasing to a significant level as compared to other two that is 16.12%. Sales in December

8

Financial statements involve the transactions that are being carried out by the business. It

includes financial and operating transactions. Sweet Menu Restaurant makes use of different

financial sources that affects the balance sheet of the organization. Moreover the cost attached

with the financial sources influence the profit and loss statement to a significant level. As stated

above the most suitable financial sources involves issue of shares, retained earnings and loan

from bank. The cost associated with internal sources is opportunity cost which is not

demonstrated in profit and loss account. However it is demonstrated in statement of changes

under retained earnings.

Along with this bank loan includes the cost of interest which is regarded as expense of

organization. It is represented on the expenditure side of profitability statement. Further in

balance sheet it is deducted from cash under the head of current asset. In accordance with the

provided scenario, profit and loss account involves cost. Moreover the interest will be subtracted

from the cash amount whereas funds acquired are demonstrated on the liability side in balance

sheet (Rasid and et.al, 2011). For Sweet Menu Restaurant loan amount will be reflected under

head of noncurrent liabilities as long term loan. This amount enhances the cash with the firm

which is presented on asset side. In situation of issuance of shares dividend paid to shareholders

will be presented in profit and loss account. Moreover the amount borrowed from public is

considered liability and is shown in balance sheet. The analysis carried above presents that for

Sweet Menu Restaurant loan from bank and retained earnings are suitable sources of finance. As

such can assist in opening of new branches by business.

TASK 3

3.1 Analysis of budget and appropriate decision making

The cash as well as inventory budget of Blue Island Restaurant has been presented for the

next four months. The company offers huge competition to Sweet Menu Restaurant. Cash budget

analysis can be conducted through determination of changes in the cash incomes as well as

expenses. It has been determined that estimated figure demonstrates the sales contributed

towards the cash incomes of business (Tektas, Gunay and Gunay, 2005). As per the budget it can

be stated that there is increase in cash sales in every month. In the month of November the sales

are increasing to a significant level as compared to other two that is 16.12%. Sales in December

8

have declined to a greater extent. Thus there is need for the manager to design plan that result in

increasing sales. On the contrary there are various components that make contribution towards

expenditure of firm. It includes capital expenditure for purchasing assets such as furniture and

Vans. However it involves operational expenses that are consist of expenses relating with

salaries, petrol charges, lightning, energy charges etc. In October the expenses of firm decline

that has increased in other two months. On the other hand, alteration in percentage depicts that

there is decline in cash expenses by 71.53% in the month of October. This is resulted from

elimination in cash expenses. On the basis of analysis it has been gained that capital expenditure

would lead to increase in expenses that affect the availability of cash. Through implementation

of suitable control tool reduction in expenses can be ensured.

By execution of suitable control tool, expenses can be reduced.

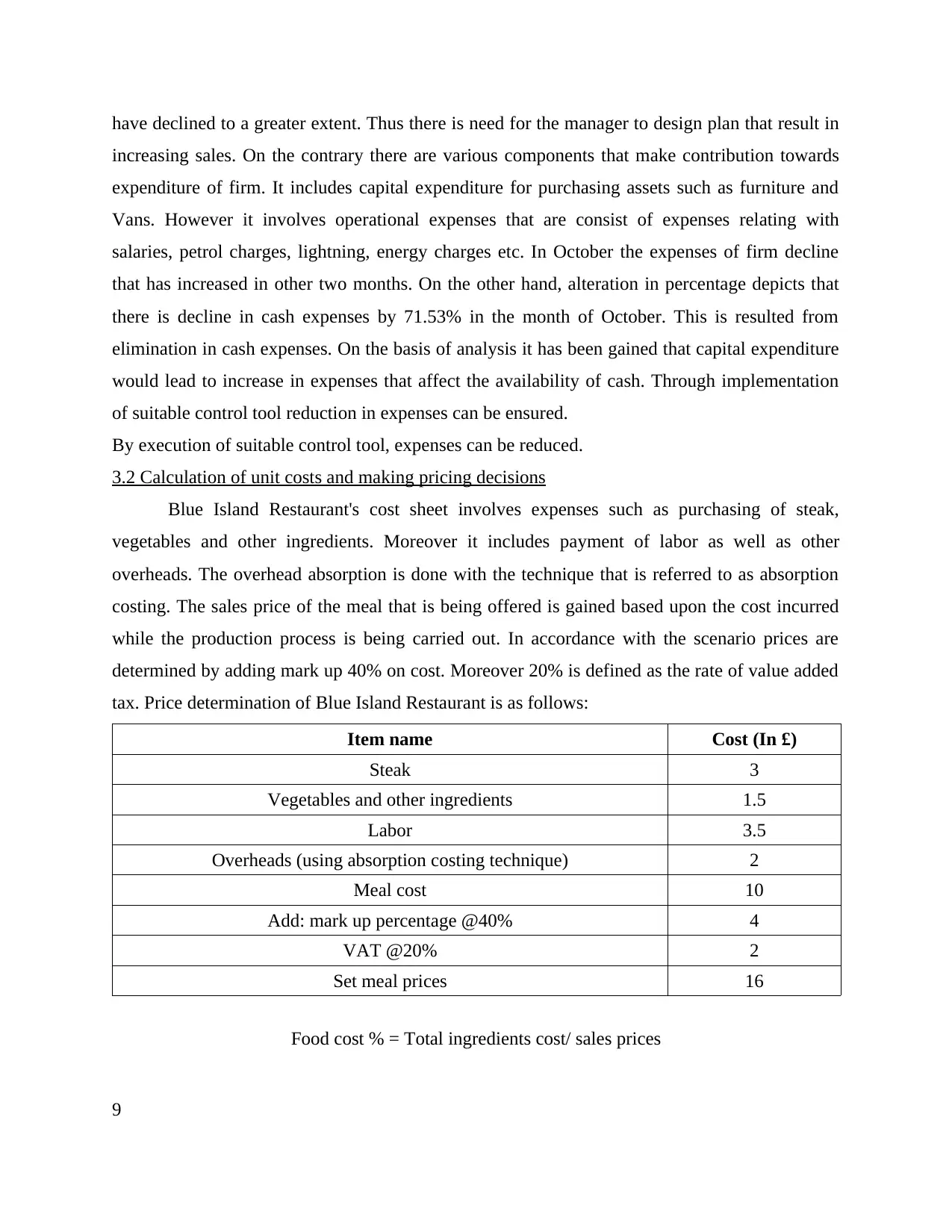

3.2 Calculation of unit costs and making pricing decisions

Blue Island Restaurant's cost sheet involves expenses such as purchasing of steak,

vegetables and other ingredients. Moreover it includes payment of labor as well as other

overheads. The overhead absorption is done with the technique that is referred to as absorption

costing. The sales price of the meal that is being offered is gained based upon the cost incurred

while the production process is being carried out. In accordance with the scenario prices are

determined by adding mark up 40% on cost. Moreover 20% is defined as the rate of value added

tax. Price determination of Blue Island Restaurant is as follows:

Item name Cost (In £)

Steak 3

Vegetables and other ingredients 1.5

Labor 3.5

Overheads (using absorption costing technique) 2

Meal cost 10

Add: mark up percentage @40% 4

VAT @20% 2

Set meal prices 16

Food cost % = Total ingredients cost/ sales prices

9

increasing sales. On the contrary there are various components that make contribution towards

expenditure of firm. It includes capital expenditure for purchasing assets such as furniture and

Vans. However it involves operational expenses that are consist of expenses relating with

salaries, petrol charges, lightning, energy charges etc. In October the expenses of firm decline

that has increased in other two months. On the other hand, alteration in percentage depicts that

there is decline in cash expenses by 71.53% in the month of October. This is resulted from

elimination in cash expenses. On the basis of analysis it has been gained that capital expenditure

would lead to increase in expenses that affect the availability of cash. Through implementation

of suitable control tool reduction in expenses can be ensured.

By execution of suitable control tool, expenses can be reduced.

3.2 Calculation of unit costs and making pricing decisions

Blue Island Restaurant's cost sheet involves expenses such as purchasing of steak,

vegetables and other ingredients. Moreover it includes payment of labor as well as other

overheads. The overhead absorption is done with the technique that is referred to as absorption

costing. The sales price of the meal that is being offered is gained based upon the cost incurred

while the production process is being carried out. In accordance with the scenario prices are

determined by adding mark up 40% on cost. Moreover 20% is defined as the rate of value added

tax. Price determination of Blue Island Restaurant is as follows:

Item name Cost (In £)

Steak 3

Vegetables and other ingredients 1.5

Labor 3.5

Overheads (using absorption costing technique) 2

Meal cost 10

Add: mark up percentage @40% 4

VAT @20% 2

Set meal prices 16

Food cost % = Total ingredients cost/ sales prices

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= £/10/£16*100

= 62.50%

Therefore it has been gained that meal price is £16. On this business is making 37.50% as

profit on cost. Thus this implies financial position of the business is sound.

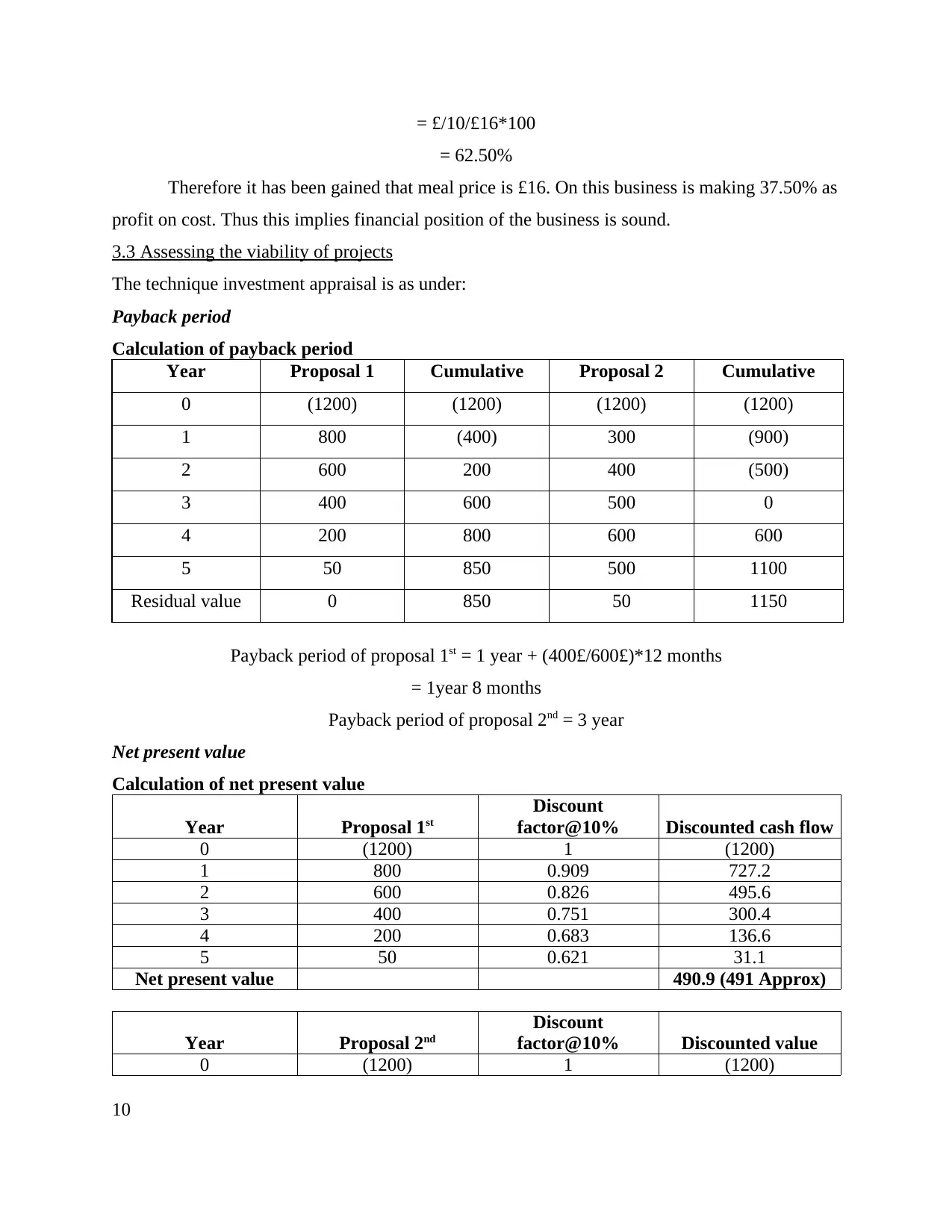

3.3 Assessing the viability of projects

The technique investment appraisal is as under:

Payback period

Calculation of payback period

Year Proposal 1 Cumulative Proposal 2 Cumulative

0 (1200) (1200) (1200) (1200)

1 800 (400) 300 (900)

2 600 200 400 (500)

3 400 600 500 0

4 200 800 600 600

5 50 850 500 1100

Residual value 0 850 50 1150

Payback period of proposal 1st = 1 year + (400£/600£)*12 months

= 1year 8 months

Payback period of proposal 2nd = 3 year

Net present value

Calculation of net present value

Year Proposal 1st

Discount

factor@10% Discounted cash flow

0 (1200) 1 (1200)

1 800 0.909 727.2

2 600 0.826 495.6

3 400 0.751 300.4

4 200 0.683 136.6

5 50 0.621 31.1

Net present value 490.9 (491 Approx)

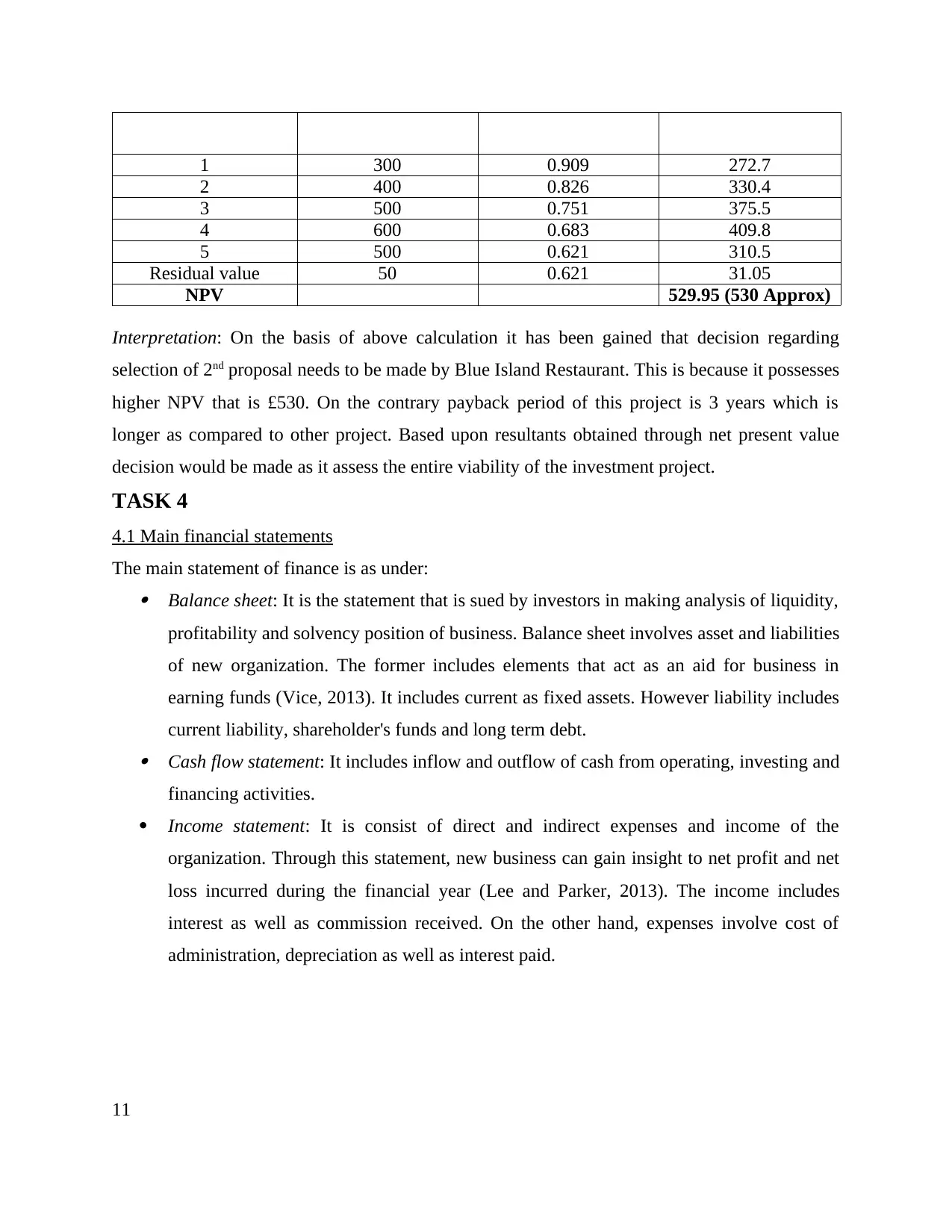

Year Proposal 2nd

Discount

factor@10% Discounted value

0 (1200) 1 (1200)

10

= 62.50%

Therefore it has been gained that meal price is £16. On this business is making 37.50% as

profit on cost. Thus this implies financial position of the business is sound.

3.3 Assessing the viability of projects

The technique investment appraisal is as under:

Payback period

Calculation of payback period

Year Proposal 1 Cumulative Proposal 2 Cumulative

0 (1200) (1200) (1200) (1200)

1 800 (400) 300 (900)

2 600 200 400 (500)

3 400 600 500 0

4 200 800 600 600

5 50 850 500 1100

Residual value 0 850 50 1150

Payback period of proposal 1st = 1 year + (400£/600£)*12 months

= 1year 8 months

Payback period of proposal 2nd = 3 year

Net present value

Calculation of net present value

Year Proposal 1st

Discount

factor@10% Discounted cash flow

0 (1200) 1 (1200)

1 800 0.909 727.2

2 600 0.826 495.6

3 400 0.751 300.4

4 200 0.683 136.6

5 50 0.621 31.1

Net present value 490.9 (491 Approx)

Year Proposal 2nd

Discount

factor@10% Discounted value

0 (1200) 1 (1200)

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 300 0.909 272.7

2 400 0.826 330.4

3 500 0.751 375.5

4 600 0.683 409.8

5 500 0.621 310.5

Residual value 50 0.621 31.05

NPV 529.95 (530 Approx)

Interpretation: On the basis of above calculation it has been gained that decision regarding

selection of 2nd proposal needs to be made by Blue Island Restaurant. This is because it possesses

higher NPV that is £530. On the contrary payback period of this project is 3 years which is

longer as compared to other project. Based upon resultants obtained through net present value

decision would be made as it assess the entire viability of the investment project.

TASK 4

4.1 Main financial statements

The main statement of finance is as under: Balance sheet: It is the statement that is sued by investors in making analysis of liquidity,

profitability and solvency position of business. Balance sheet involves asset and liabilities

of new organization. The former includes elements that act as an aid for business in

earning funds (Vice, 2013). It includes current as fixed assets. However liability includes

current liability, shareholder's funds and long term debt. Cash flow statement: It includes inflow and outflow of cash from operating, investing and

financing activities.

Income statement: It is consist of direct and indirect expenses and income of the

organization. Through this statement, new business can gain insight to net profit and net

loss incurred during the financial year (Lee and Parker, 2013). The income includes

interest as well as commission received. On the other hand, expenses involve cost of

administration, depreciation as well as interest paid.

11

2 400 0.826 330.4

3 500 0.751 375.5

4 600 0.683 409.8

5 500 0.621 310.5

Residual value 50 0.621 31.05

NPV 529.95 (530 Approx)

Interpretation: On the basis of above calculation it has been gained that decision regarding

selection of 2nd proposal needs to be made by Blue Island Restaurant. This is because it possesses

higher NPV that is £530. On the contrary payback period of this project is 3 years which is

longer as compared to other project. Based upon resultants obtained through net present value

decision would be made as it assess the entire viability of the investment project.

TASK 4

4.1 Main financial statements

The main statement of finance is as under: Balance sheet: It is the statement that is sued by investors in making analysis of liquidity,

profitability and solvency position of business. Balance sheet involves asset and liabilities

of new organization. The former includes elements that act as an aid for business in

earning funds (Vice, 2013). It includes current as fixed assets. However liability includes

current liability, shareholder's funds and long term debt. Cash flow statement: It includes inflow and outflow of cash from operating, investing and

financing activities.

Income statement: It is consist of direct and indirect expenses and income of the

organization. Through this statement, new business can gain insight to net profit and net

loss incurred during the financial year (Lee and Parker, 2013). The income includes

interest as well as commission received. On the other hand, expenses involve cost of

administration, depreciation as well as interest paid.

11

4.2 Comparing formats of financial statements for different types of business

Every organization develops statement of finances in the format which is stated by

Generally Accepted Accounting Practices (GAAP) and International Financial reporting

Standards (IFRS). In this regard several business types are as under: Sole trader: This business is owned by an individual. Further such business only prepares

simple statement of profit and loss. Partnership: Such business type develops financial statements such as balance sheet,

income statement as well as cash flow account (Rogers, 2014). Further it also prepares

partners capital account that demonstrates amount contributed by each partners and their

ratio of profit distribution.

Public limited company: This business type develops financial statements such as balance

sheet, income statement as well as cash flow account (Keller, 2013). In addition to this it

also develop financial statement as per international standards of accounting.

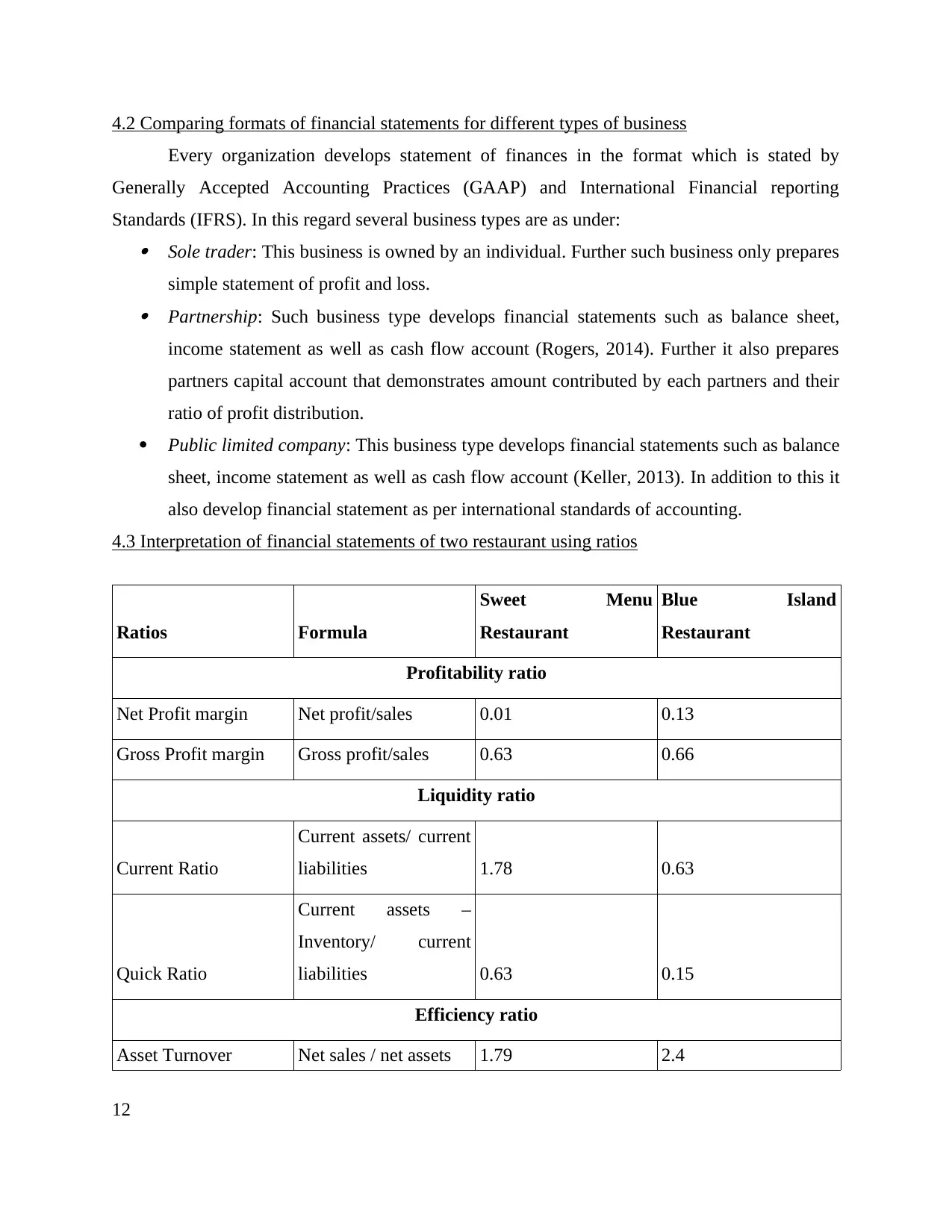

4.3 Interpretation of financial statements of two restaurant using ratios

Ratios Formula

Sweet Menu

Restaurant

Blue Island

Restaurant

Profitability ratio

Net Profit margin Net profit/sales 0.01 0.13

Gross Profit margin Gross profit/sales 0.63 0.66

Liquidity ratio

Current Ratio

Current assets/ current

liabilities 1.78 0.63

Quick Ratio

Current assets –

Inventory/ current

liabilities 0.63 0.15

Efficiency ratio

Asset Turnover Net sales / net assets 1.79 2.4

12

Every organization develops statement of finances in the format which is stated by

Generally Accepted Accounting Practices (GAAP) and International Financial reporting

Standards (IFRS). In this regard several business types are as under: Sole trader: This business is owned by an individual. Further such business only prepares

simple statement of profit and loss. Partnership: Such business type develops financial statements such as balance sheet,

income statement as well as cash flow account (Rogers, 2014). Further it also prepares

partners capital account that demonstrates amount contributed by each partners and their

ratio of profit distribution.

Public limited company: This business type develops financial statements such as balance

sheet, income statement as well as cash flow account (Keller, 2013). In addition to this it

also develop financial statement as per international standards of accounting.

4.3 Interpretation of financial statements of two restaurant using ratios

Ratios Formula

Sweet Menu

Restaurant

Blue Island

Restaurant

Profitability ratio

Net Profit margin Net profit/sales 0.01 0.13

Gross Profit margin Gross profit/sales 0.63 0.66

Liquidity ratio

Current Ratio

Current assets/ current

liabilities 1.78 0.63

Quick Ratio

Current assets –

Inventory/ current

liabilities 0.63 0.15

Efficiency ratio

Asset Turnover Net sales / net assets 1.79 2.4

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.