Report: Financial Planning for Sweet Menu Restaurant Expansion Project

VerifiedAdded on 2020/02/05

|18

|5027

|39

Report

AI Summary

This report analyzes the financial strategies for Sweet Menu Restaurant's expansion, focusing on the opening of new business units. It explores various sources of finance, including internal and external options like bank loans, retained earnings, and issuing shares, evaluating their implications and suitability. The report assesses the cost of different financing methods, emphasizing the importance of financial planning for the restaurant's growth. It delves into cash budget analysis, unit cost calculations, and the application of investment appraisal techniques to evaluate expansion proposals. Furthermore, the report examines the main financial statements and employs ratio analysis to interpret the financial positions of Sweet Menu Restaurant and a competitor, Blue Island restaurant, providing insights into their financial health and performance. The report recommends a bank loan as the most appropriate source of finance.

MFRD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance that can be used by Sweet Menu restaurant............................................1

1.2 Implication of various sources of finance..............................................................................2

1.3 Most appropriate sources of finance for Sweet Menu restaurant..........................................4

TASK 2............................................................................................................................................5

2.1 Cost of different sources of finance.......................................................................................5

2.2 Importance of financial planning to Sweet menu restaurant.................................................5

2.3 Impact of sources of finance on financial statements............................................................6

2.4 Impact of sources of finance on financial statements............................................................7

TASK 3............................................................................................................................................7

3.1 Analyse of cash budget and various decisions based upon it................................................7

3.2 calculation of Unit cost..........................................................................................................8

3.3 Viability of two proposal by using investment appraisal techniques..................................10

TASK 4..........................................................................................................................................13

4.1 Main financial statements....................................................................................................13

4.2 Comparing the financial statements format of different types of organisation...................14

4.3 Interpreting the financial statements of Sweet menu restaurant and Blue Island restaurant

using ratio analysis....................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance that can be used by Sweet Menu restaurant............................................1

1.2 Implication of various sources of finance..............................................................................2

1.3 Most appropriate sources of finance for Sweet Menu restaurant..........................................4

TASK 2............................................................................................................................................5

2.1 Cost of different sources of finance.......................................................................................5

2.2 Importance of financial planning to Sweet menu restaurant.................................................5

2.3 Impact of sources of finance on financial statements............................................................6

2.4 Impact of sources of finance on financial statements............................................................7

TASK 3............................................................................................................................................7

3.1 Analyse of cash budget and various decisions based upon it................................................7

3.2 calculation of Unit cost..........................................................................................................8

3.3 Viability of two proposal by using investment appraisal techniques..................................10

TASK 4..........................................................................................................................................13

4.1 Main financial statements....................................................................................................13

4.2 Comparing the financial statements format of different types of organisation...................14

4.3 Interpreting the financial statements of Sweet menu restaurant and Blue Island restaurant

using ratio analysis....................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

Finance is the resource that is available with the company in order to achieve its desired

organisational goals and objectives (Lee and et.al. 2015). In other words it can be said that

finance resource is the money that is available with the company for investing in order to

generate profit out of it. In managing financial resources manager of the company play a vital

role. Manager various strategies with an aim to utilize the available resources to the full extend

and to achieve the organizational desired objectives. In the following report Sweet Menu

restaurant which is the reputed restaurant situated in Gants Hill in East London. The restaurant

wants to expand its business by opening to new business units in Central London and Croydon.

In this report various sources of finance are discussed that are available with Sweet menu

restaurant along with its implications. In additional to this important of financial planning to

Sweet menu restaurant in context of expansion of its business is also mentioned. Along with this

investment techniques are used by the company in order to analyse which proposal will prove to

be best? At last in this report various ratios of both the companies are calculated in order to

analyse which company financial position is good.

TASK 1

1.1 Sources of finance that can be used by Sweet Menu restaurant

There are different types of internal and external sources of finance present with Sweet

Menu restaurant in order to raise its capital for the purpose of starting its two new business unit.

Some of the sources of finance that can be used by the company are listed below:-

Sources of finance features

Internal sources of finance

Angle investors By using this method Sweet Menu restaurant can raise its

capital by borrowing from its friends and family members in

order to fulfil their objectives (Murphy and Yetmar, 2010). For

using this method Sweet Menu restaurant is required to give

their friends shareholding in the company.

Retained earning Each and every organisation keep fixed amount of profit earned

by them with it in order to meet up its urgent requirements. This

1

Finance is the resource that is available with the company in order to achieve its desired

organisational goals and objectives (Lee and et.al. 2015). In other words it can be said that

finance resource is the money that is available with the company for investing in order to

generate profit out of it. In managing financial resources manager of the company play a vital

role. Manager various strategies with an aim to utilize the available resources to the full extend

and to achieve the organizational desired objectives. In the following report Sweet Menu

restaurant which is the reputed restaurant situated in Gants Hill in East London. The restaurant

wants to expand its business by opening to new business units in Central London and Croydon.

In this report various sources of finance are discussed that are available with Sweet menu

restaurant along with its implications. In additional to this important of financial planning to

Sweet menu restaurant in context of expansion of its business is also mentioned. Along with this

investment techniques are used by the company in order to analyse which proposal will prove to

be best? At last in this report various ratios of both the companies are calculated in order to

analyse which company financial position is good.

TASK 1

1.1 Sources of finance that can be used by Sweet Menu restaurant

There are different types of internal and external sources of finance present with Sweet

Menu restaurant in order to raise its capital for the purpose of starting its two new business unit.

Some of the sources of finance that can be used by the company are listed below:-

Sources of finance features

Internal sources of finance

Angle investors By using this method Sweet Menu restaurant can raise its

capital by borrowing from its friends and family members in

order to fulfil their objectives (Murphy and Yetmar, 2010). For

using this method Sweet Menu restaurant is required to give

their friends shareholding in the company.

Retained earning Each and every organisation keep fixed amount of profit earned

by them with it in order to meet up its urgent requirements. This

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is one of the cost effective method that can be used by Sweet

Menu restaurant in order to expand its business units.

Bank overdraft

External sources of finance

Issue of shares It is also one of the best methods that can be used by the Sweet

Menu restaurant in order to raise its capital (Orens and et. al.,

2009). By using equity shares and debentures to the general

public company can raise its capital. By using this method

company will be easily be able to open its two new business

units.

Leasing It is one of the best external sources of finance that can be used

by Sweet Menu restaurant in order to use the asset without

purchasing it. By using this method company can protect

themselves in context of obsoletation of technology.

Bank loan It is the method by using which Sweet Menu restaurant can

borrow money from the bank against the collateral security. By

using this method company will be able to meet its urgent

requirement of finance (Overton, 2007). By using this method

company can also avail various tax benefits.

1.2 Implication of various sources of finance

Sources Legal aspects Suitability Cost

Angles investors Sweet Menu restaurant

is required to issue

shares to the Angles

investors in order to

give them

shareholding in the

company.

By using this method

Sweet Menu restaurant

can easily be able to

meet its financial

requirement of funds

without following any

official formalities

Angles investors are

also the shareholders

of the company. Sweet

Menu restaurant is

required to pay

dividend to them. This

in turn increases the

2

Menu restaurant in order to expand its business units.

Bank overdraft

External sources of finance

Issue of shares It is also one of the best methods that can be used by the Sweet

Menu restaurant in order to raise its capital (Orens and et. al.,

2009). By using equity shares and debentures to the general

public company can raise its capital. By using this method

company will be easily be able to open its two new business

units.

Leasing It is one of the best external sources of finance that can be used

by Sweet Menu restaurant in order to use the asset without

purchasing it. By using this method company can protect

themselves in context of obsoletation of technology.

Bank loan It is the method by using which Sweet Menu restaurant can

borrow money from the bank against the collateral security. By

using this method company will be able to meet its urgent

requirement of finance (Overton, 2007). By using this method

company can also avail various tax benefits.

1.2 Implication of various sources of finance

Sources Legal aspects Suitability Cost

Angles investors Sweet Menu restaurant

is required to issue

shares to the Angles

investors in order to

give them

shareholding in the

company.

By using this method

Sweet Menu restaurant

can easily be able to

meet its financial

requirement of funds

without following any

official formalities

Angles investors are

also the shareholders

of the company. Sweet

Menu restaurant is

required to pay

dividend to them. This

in turn increases the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

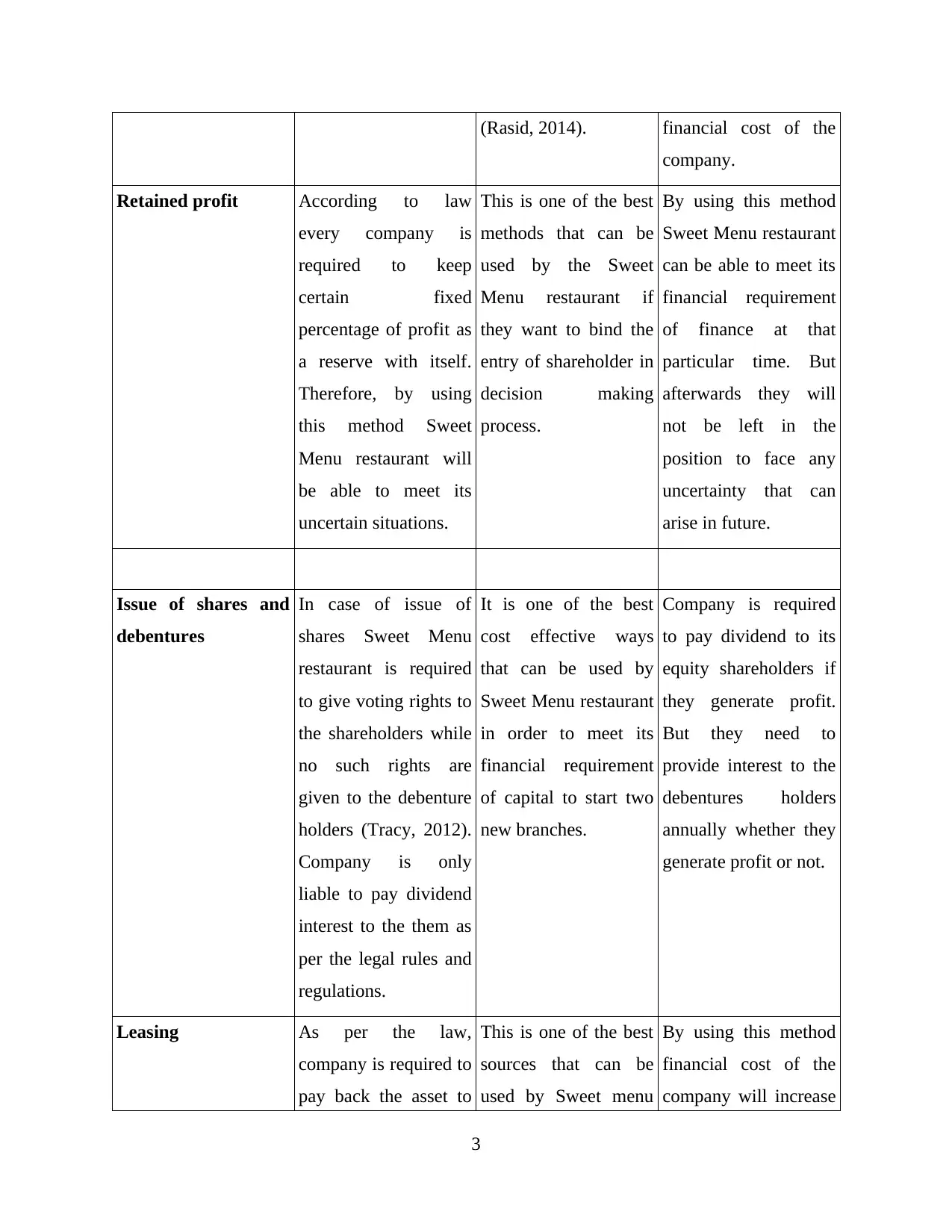

(Rasid, 2014). financial cost of the

company.

Retained profit According to law

every company is

required to keep

certain fixed

percentage of profit as

a reserve with itself.

Therefore, by using

this method Sweet

Menu restaurant will

be able to meet its

uncertain situations.

This is one of the best

methods that can be

used by the Sweet

Menu restaurant if

they want to bind the

entry of shareholder in

decision making

process.

By using this method

Sweet Menu restaurant

can be able to meet its

financial requirement

of finance at that

particular time. But

afterwards they will

not be left in the

position to face any

uncertainty that can

arise in future.

Issue of shares and

debentures

In case of issue of

shares Sweet Menu

restaurant is required

to give voting rights to

the shareholders while

no such rights are

given to the debenture

holders (Tracy, 2012).

Company is only

liable to pay dividend

interest to the them as

per the legal rules and

regulations.

It is one of the best

cost effective ways

that can be used by

Sweet Menu restaurant

in order to meet its

financial requirement

of capital to start two

new branches.

Company is required

to pay dividend to its

equity shareholders if

they generate profit.

But they need to

provide interest to the

debentures holders

annually whether they

generate profit or not.

Leasing As per the law,

company is required to

pay back the asset to

This is one of the best

sources that can be

used by Sweet menu

By using this method

financial cost of the

company will increase

3

company.

Retained profit According to law

every company is

required to keep

certain fixed

percentage of profit as

a reserve with itself.

Therefore, by using

this method Sweet

Menu restaurant will

be able to meet its

uncertain situations.

This is one of the best

methods that can be

used by the Sweet

Menu restaurant if

they want to bind the

entry of shareholder in

decision making

process.

By using this method

Sweet Menu restaurant

can be able to meet its

financial requirement

of finance at that

particular time. But

afterwards they will

not be left in the

position to face any

uncertainty that can

arise in future.

Issue of shares and

debentures

In case of issue of

shares Sweet Menu

restaurant is required

to give voting rights to

the shareholders while

no such rights are

given to the debenture

holders (Tracy, 2012).

Company is only

liable to pay dividend

interest to the them as

per the legal rules and

regulations.

It is one of the best

cost effective ways

that can be used by

Sweet Menu restaurant

in order to meet its

financial requirement

of capital to start two

new branches.

Company is required

to pay dividend to its

equity shareholders if

they generate profit.

But they need to

provide interest to the

debentures holders

annually whether they

generate profit or not.

Leasing As per the law,

company is required to

pay back the asset to

This is one of the best

sources that can be

used by Sweet menu

By using this method

financial cost of the

company will increase

3

the real owner after the

completion of the

specific time period.

restaurant in order to

protect themselves

from the condition of

salvation.

because company is

required to pay rent to

the lessor periodical.

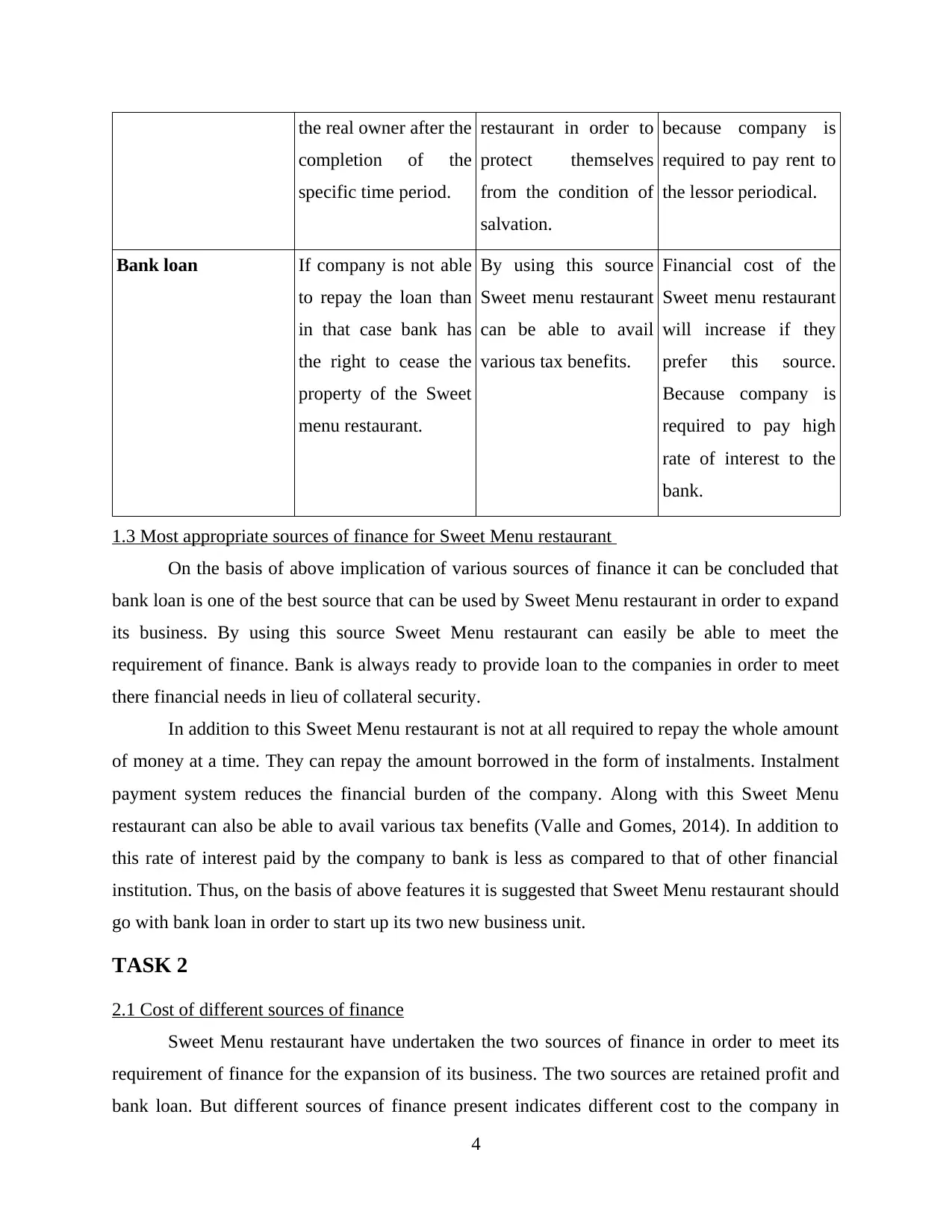

Bank loan If company is not able

to repay the loan than

in that case bank has

the right to cease the

property of the Sweet

menu restaurant.

By using this source

Sweet menu restaurant

can be able to avail

various tax benefits.

Financial cost of the

Sweet menu restaurant

will increase if they

prefer this source.

Because company is

required to pay high

rate of interest to the

bank.

1.3 Most appropriate sources of finance for Sweet Menu restaurant

On the basis of above implication of various sources of finance it can be concluded that

bank loan is one of the best source that can be used by Sweet Menu restaurant in order to expand

its business. By using this source Sweet Menu restaurant can easily be able to meet the

requirement of finance. Bank is always ready to provide loan to the companies in order to meet

there financial needs in lieu of collateral security.

In addition to this Sweet Menu restaurant is not at all required to repay the whole amount

of money at a time. They can repay the amount borrowed in the form of instalments. Instalment

payment system reduces the financial burden of the company. Along with this Sweet Menu

restaurant can also be able to avail various tax benefits (Valle and Gomes, 2014). In addition to

this rate of interest paid by the company to bank is less as compared to that of other financial

institution. Thus, on the basis of above features it is suggested that Sweet Menu restaurant should

go with bank loan in order to start up its two new business unit.

TASK 2

2.1 Cost of different sources of finance

Sweet Menu restaurant have undertaken the two sources of finance in order to meet its

requirement of finance for the expansion of its business. The two sources are retained profit and

bank loan. But different sources of finance present indicates different cost to the company in

4

completion of the

specific time period.

restaurant in order to

protect themselves

from the condition of

salvation.

because company is

required to pay rent to

the lessor periodical.

Bank loan If company is not able

to repay the loan than

in that case bank has

the right to cease the

property of the Sweet

menu restaurant.

By using this source

Sweet menu restaurant

can be able to avail

various tax benefits.

Financial cost of the

Sweet menu restaurant

will increase if they

prefer this source.

Because company is

required to pay high

rate of interest to the

bank.

1.3 Most appropriate sources of finance for Sweet Menu restaurant

On the basis of above implication of various sources of finance it can be concluded that

bank loan is one of the best source that can be used by Sweet Menu restaurant in order to expand

its business. By using this source Sweet Menu restaurant can easily be able to meet the

requirement of finance. Bank is always ready to provide loan to the companies in order to meet

there financial needs in lieu of collateral security.

In addition to this Sweet Menu restaurant is not at all required to repay the whole amount

of money at a time. They can repay the amount borrowed in the form of instalments. Instalment

payment system reduces the financial burden of the company. Along with this Sweet Menu

restaurant can also be able to avail various tax benefits (Valle and Gomes, 2014). In addition to

this rate of interest paid by the company to bank is less as compared to that of other financial

institution. Thus, on the basis of above features it is suggested that Sweet Menu restaurant should

go with bank loan in order to start up its two new business unit.

TASK 2

2.1 Cost of different sources of finance

Sweet Menu restaurant have undertaken the two sources of finance in order to meet its

requirement of finance for the expansion of its business. The two sources are retained profit and

bank loan. But different sources of finance present indicates different cost to the company in

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

terms of financial and opportunity cost. These costs have the high consequence on the growth

and profitability of the restaurant.

Financial cost: - Bank and various financial institutions impose high financial cost in

front of the company. Bank charges high rate of interest in order to collect financial assistance.

This in turn increases the financial cost of the Sweet Menu restaurant. Along with this Sweet

Menu restaurant is also required to repay the amount of money borrowed by them. This in turn

affects the liquidity and profitability of the company (Al-Bakri, Matar and Nour, 2014.).

Opportunities cost: - Opportunity cost is the cost that is beard by the company due to the

selection of another alternative. Suppose if company uses retained profit than in that case they

will not be able to pay dividend to shareholders in case of loss. This in turn will create negative

impression in the mind of shareholders against the company (Batta, Ganguly and Rosett, 2014).

In addition to this, company will not be able to meet up with any uncertain situation in effective

manner. These two features represent the opportunity cost that Sweet Menu restaurant need to

bear.

2.2 Importance of financial planning to Sweet menu restaurant

Financial planning is the process which helps an organisation to make various necessary

financial decisions in order generate more profit. By planning all its financial activities in

advance Sweet Menu restaurant will be able to move the restaurant towards the growth rate.

Importance of financial planning to Sweet Menu restaurant:-

Financial planning in advance will aid the company to coordinate all the activities of

various departments present within the organisation. This in turn will also assist the

Sweet Menu restaurant to collect the deeper knowledge about the funds that are required

by each and every department.

In addition to this Sweet Menu restaurant will also be able to utilise its financial

resources to the full extent by reducing its wastage. This in turn aids the company to

overcome the condition of deficit and surplus (Baum and Crosby, 2014).

Financial planning will also provide assistance to the Sweet Menu restaurant in

abstraction of the funds that need to be raised by the company by using various sources.

Along with this Sweet Menu restaurant will also be able to analyses the financial needs

that can arise in future. Sweet menu restaurant is also able to anticipate its sales and

growth by planning its financial activities.

5

and profitability of the restaurant.

Financial cost: - Bank and various financial institutions impose high financial cost in

front of the company. Bank charges high rate of interest in order to collect financial assistance.

This in turn increases the financial cost of the Sweet Menu restaurant. Along with this Sweet

Menu restaurant is also required to repay the amount of money borrowed by them. This in turn

affects the liquidity and profitability of the company (Al-Bakri, Matar and Nour, 2014.).

Opportunities cost: - Opportunity cost is the cost that is beard by the company due to the

selection of another alternative. Suppose if company uses retained profit than in that case they

will not be able to pay dividend to shareholders in case of loss. This in turn will create negative

impression in the mind of shareholders against the company (Batta, Ganguly and Rosett, 2014).

In addition to this, company will not be able to meet up with any uncertain situation in effective

manner. These two features represent the opportunity cost that Sweet Menu restaurant need to

bear.

2.2 Importance of financial planning to Sweet menu restaurant

Financial planning is the process which helps an organisation to make various necessary

financial decisions in order generate more profit. By planning all its financial activities in

advance Sweet Menu restaurant will be able to move the restaurant towards the growth rate.

Importance of financial planning to Sweet Menu restaurant:-

Financial planning in advance will aid the company to coordinate all the activities of

various departments present within the organisation. This in turn will also assist the

Sweet Menu restaurant to collect the deeper knowledge about the funds that are required

by each and every department.

In addition to this Sweet Menu restaurant will also be able to utilise its financial

resources to the full extent by reducing its wastage. This in turn aids the company to

overcome the condition of deficit and surplus (Baum and Crosby, 2014).

Financial planning will also provide assistance to the Sweet Menu restaurant in

abstraction of the funds that need to be raised by the company by using various sources.

Along with this Sweet Menu restaurant will also be able to analyses the financial needs

that can arise in future. Sweet menu restaurant is also able to anticipate its sales and

growth by planning its financial activities.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Thus, planning of the financial activities lead the company towards the success in the

competitive business world.

2.3 Impact of sources of finance on financial statements

Different types of stakeholder present in the corporate world require different types of

information in order to take various necessary decisions:- Stakeholders: - Shareholder is the one who invest their personal saving in the company in

order to earn high return on investment on them. They prefer the financial statements of

the company in order to find out the liquidity, profitability and solvency of the company.

They use these statements in order to decide whether they should invest in the company

or not. Employees: - Employees are the one who works for the betterment of the company.

These employees are interested in the income statements of the company (Broadbent and

Cullen, 2012). They prefer these statements in order to find out whether they are paid fair

salary or not. Manager: - Manager is the one who prepare various strategies in order to achieve the

organisational desired objectives. They prefer the income statement and cash flow

statements in order find out the liquidity position of the company (Chang and et.al, 2014).

In addition to this they also prefer balance sheet in order to collect the deeper information

about the financial performance of the company. Suppliers: - Suppliers are the one who supply raw material to the company. They prefer

income statements and balance sheet of the company in order to find out whether the

company is in a position to pay them for the goods supplied by them on time or not.

Government: - Government is the one who works for the betterment of the society. They

want that every organisation should grow and generate more employment opportunities.

In order to find out the actual position of the company and to calculate the amount of tax;

government prefer financial statements and audit report of the company (Guerrero, Maas

and Hogland, 2013).

2.4 Impact of sources of finance on financial statements

Different sources of finance of have different impact on the financial statements. Each

and every sources of finance affects the financial statements of the company. Therefore,

company should take care at the time of selecting the sources of finance (Guerrero, L. A., Maas

6

competitive business world.

2.3 Impact of sources of finance on financial statements

Different types of stakeholder present in the corporate world require different types of

information in order to take various necessary decisions:- Stakeholders: - Shareholder is the one who invest their personal saving in the company in

order to earn high return on investment on them. They prefer the financial statements of

the company in order to find out the liquidity, profitability and solvency of the company.

They use these statements in order to decide whether they should invest in the company

or not. Employees: - Employees are the one who works for the betterment of the company.

These employees are interested in the income statements of the company (Broadbent and

Cullen, 2012). They prefer these statements in order to find out whether they are paid fair

salary or not. Manager: - Manager is the one who prepare various strategies in order to achieve the

organisational desired objectives. They prefer the income statement and cash flow

statements in order find out the liquidity position of the company (Chang and et.al, 2014).

In addition to this they also prefer balance sheet in order to collect the deeper information

about the financial performance of the company. Suppliers: - Suppliers are the one who supply raw material to the company. They prefer

income statements and balance sheet of the company in order to find out whether the

company is in a position to pay them for the goods supplied by them on time or not.

Government: - Government is the one who works for the betterment of the society. They

want that every organisation should grow and generate more employment opportunities.

In order to find out the actual position of the company and to calculate the amount of tax;

government prefer financial statements and audit report of the company (Guerrero, Maas

and Hogland, 2013).

2.4 Impact of sources of finance on financial statements

Different sources of finance of have different impact on the financial statements. Each

and every sources of finance affects the financial statements of the company. Therefore,

company should take care at the time of selecting the sources of finance (Guerrero, L. A., Maas

6

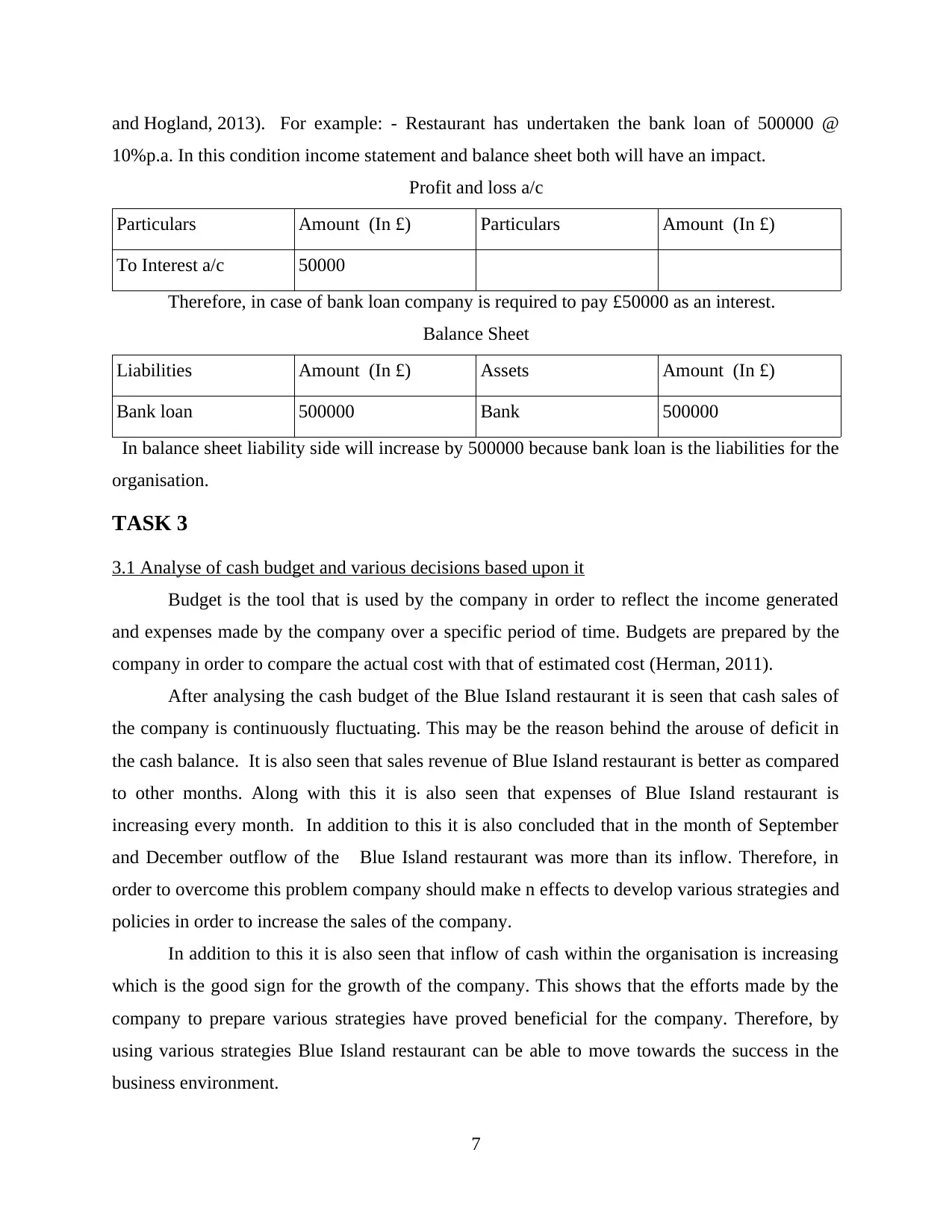

and Hogland, 2013). For example: - Restaurant has undertaken the bank loan of 500000 @

10%p.a. In this condition income statement and balance sheet both will have an impact.

Profit and loss a/c

Particulars Amount (In £) Particulars Amount (In £)

To Interest a/c 50000

Therefore, in case of bank loan company is required to pay £50000 as an interest.

Balance Sheet

Liabilities Amount (In £) Assets Amount (In £)

Bank loan 500000 Bank 500000

In balance sheet liability side will increase by 500000 because bank loan is the liabilities for the

organisation.

TASK 3

3.1 Analyse of cash budget and various decisions based upon it

Budget is the tool that is used by the company in order to reflect the income generated

and expenses made by the company over a specific period of time. Budgets are prepared by the

company in order to compare the actual cost with that of estimated cost (Herman, 2011).

After analysing the cash budget of the Blue Island restaurant it is seen that cash sales of

the company is continuously fluctuating. This may be the reason behind the arouse of deficit in

the cash balance. It is also seen that sales revenue of Blue Island restaurant is better as compared

to other months. Along with this it is also seen that expenses of Blue Island restaurant is

increasing every month. In addition to this it is also concluded that in the month of September

and December outflow of the Blue Island restaurant was more than its inflow. Therefore, in

order to overcome this problem company should make n effects to develop various strategies and

policies in order to increase the sales of the company.

In addition to this it is also seen that inflow of cash within the organisation is increasing

which is the good sign for the growth of the company. This shows that the efforts made by the

company to prepare various strategies have proved beneficial for the company. Therefore, by

using various strategies Blue Island restaurant can be able to move towards the success in the

business environment.

7

10%p.a. In this condition income statement and balance sheet both will have an impact.

Profit and loss a/c

Particulars Amount (In £) Particulars Amount (In £)

To Interest a/c 50000

Therefore, in case of bank loan company is required to pay £50000 as an interest.

Balance Sheet

Liabilities Amount (In £) Assets Amount (In £)

Bank loan 500000 Bank 500000

In balance sheet liability side will increase by 500000 because bank loan is the liabilities for the

organisation.

TASK 3

3.1 Analyse of cash budget and various decisions based upon it

Budget is the tool that is used by the company in order to reflect the income generated

and expenses made by the company over a specific period of time. Budgets are prepared by the

company in order to compare the actual cost with that of estimated cost (Herman, 2011).

After analysing the cash budget of the Blue Island restaurant it is seen that cash sales of

the company is continuously fluctuating. This may be the reason behind the arouse of deficit in

the cash balance. It is also seen that sales revenue of Blue Island restaurant is better as compared

to other months. Along with this it is also seen that expenses of Blue Island restaurant is

increasing every month. In addition to this it is also concluded that in the month of September

and December outflow of the Blue Island restaurant was more than its inflow. Therefore, in

order to overcome this problem company should make n effects to develop various strategies and

policies in order to increase the sales of the company.

In addition to this it is also seen that inflow of cash within the organisation is increasing

which is the good sign for the growth of the company. This shows that the efforts made by the

company to prepare various strategies have proved beneficial for the company. Therefore, by

using various strategies Blue Island restaurant can be able to move towards the success in the

business environment.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

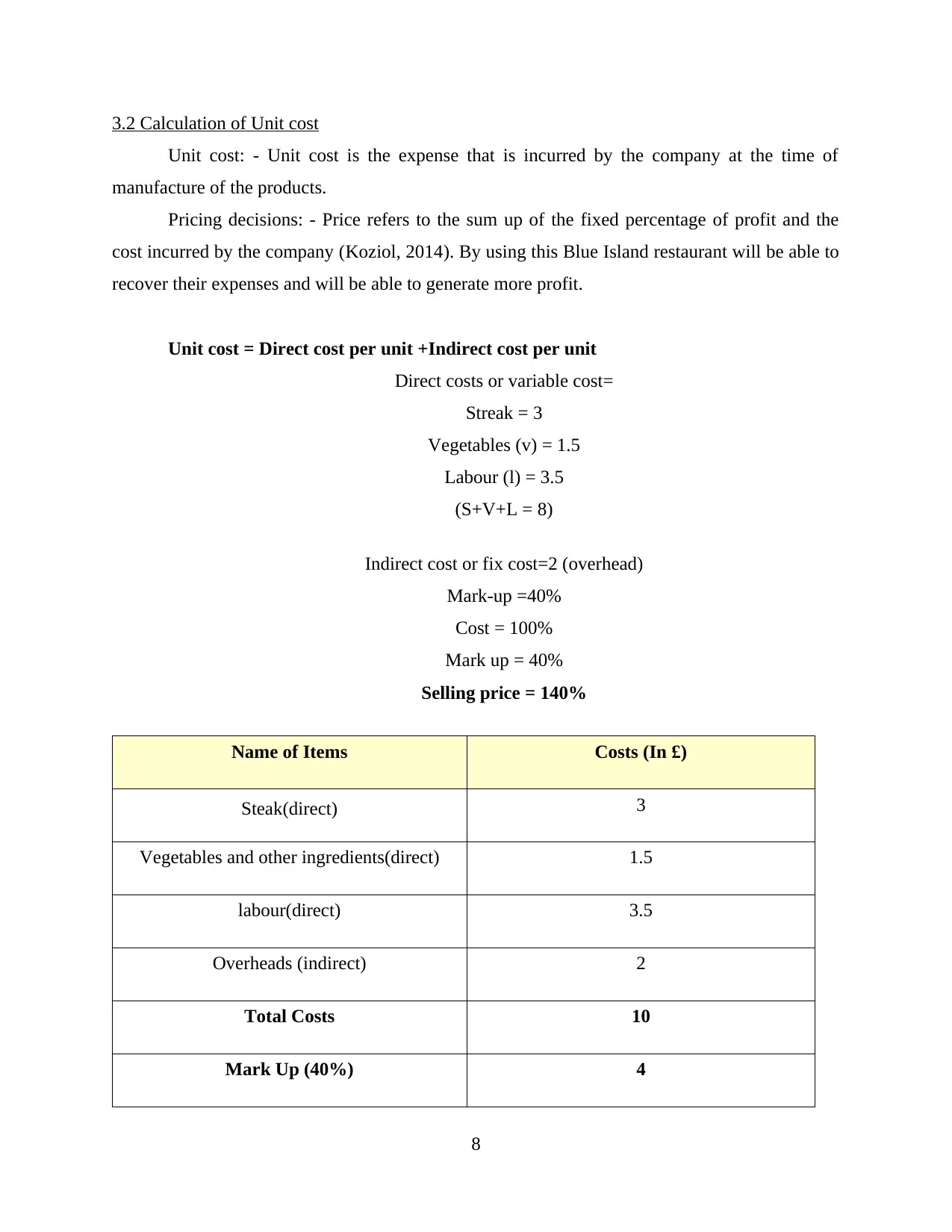

3.2 Calculation of Unit cost

Unit cost: - Unit cost is the expense that is incurred by the company at the time of

manufacture of the products.

Pricing decisions: - Price refers to the sum up of the fixed percentage of profit and the

cost incurred by the company (Koziol, 2014). By using this Blue Island restaurant will be able to

recover their expenses and will be able to generate more profit.

Unit cost = Direct cost per unit +Indirect cost per unit

Direct costs or variable cost=

Streak = 3

Vegetables (v) = 1.5

Labour (l) = 3.5

(S+V+L = 8)

Indirect cost or fix cost=2 (overhead)

Mark-up =40%

Cost = 100%

Mark up = 40%

Selling price = 140%

Name of Items Costs (In £)

Steak(direct) 3

Vegetables and other ingredients(direct) 1.5

labour(direct) 3.5

Overheads (indirect) 2

Total Costs 10

Mark Up (40%) 4

8

Unit cost: - Unit cost is the expense that is incurred by the company at the time of

manufacture of the products.

Pricing decisions: - Price refers to the sum up of the fixed percentage of profit and the

cost incurred by the company (Koziol, 2014). By using this Blue Island restaurant will be able to

recover their expenses and will be able to generate more profit.

Unit cost = Direct cost per unit +Indirect cost per unit

Direct costs or variable cost=

Streak = 3

Vegetables (v) = 1.5

Labour (l) = 3.5

(S+V+L = 8)

Indirect cost or fix cost=2 (overhead)

Mark-up =40%

Cost = 100%

Mark up = 40%

Selling price = 140%

Name of Items Costs (In £)

Steak(direct) 3

Vegetables and other ingredients(direct) 1.5

labour(direct) 3.5

Overheads (indirect) 2

Total Costs 10

Mark Up (40%) 4

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

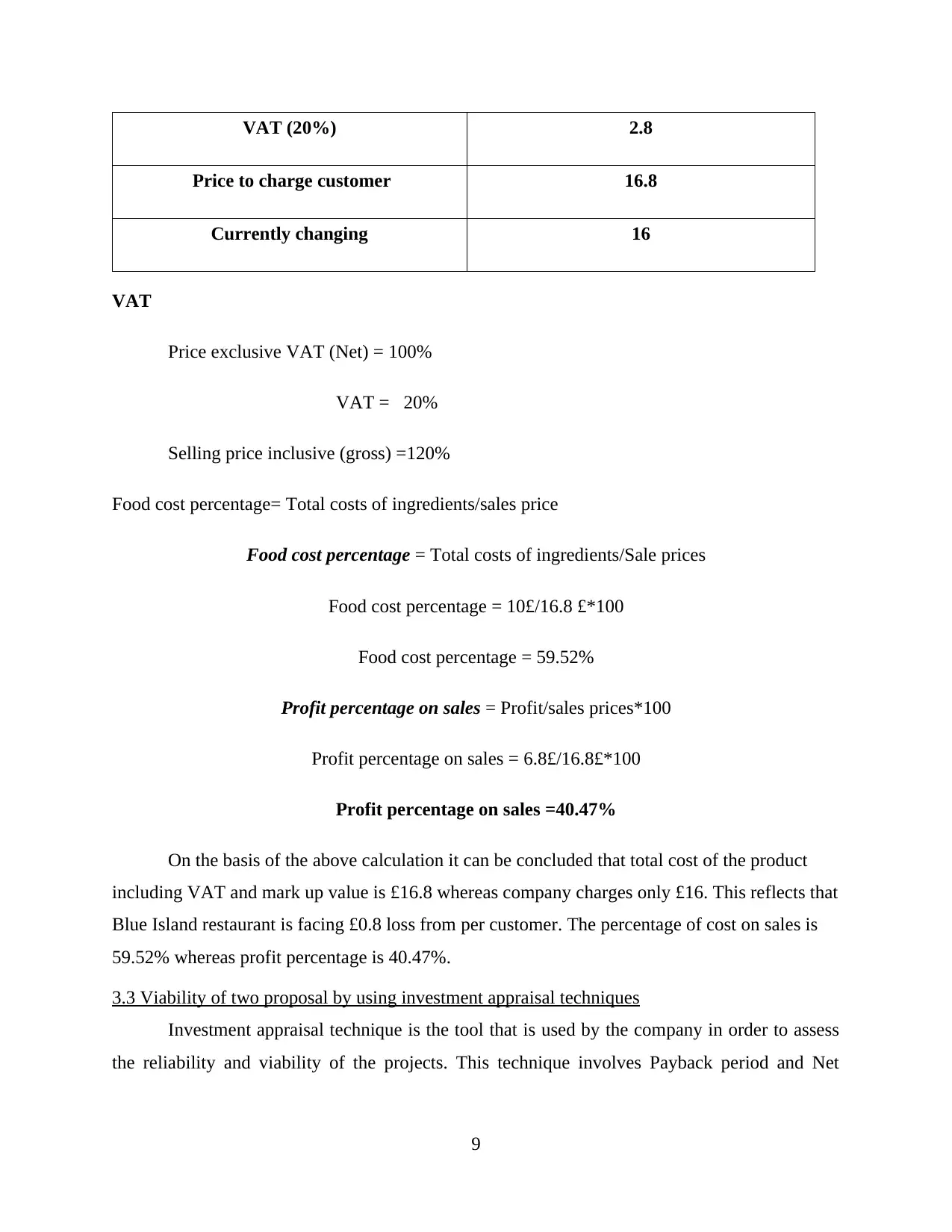

VAT (20%) 2.8

Price to charge customer 16.8

Currently changing 16

VAT

Price exclusive VAT (Net) = 100%

VAT = 20%

Selling price inclusive (gross) =120%

Food cost percentage= Total costs of ingredients/sales price

Food cost percentage = Total costs of ingredients/Sale prices

Food cost percentage = 10£/16.8 £*100

Food cost percentage = 59.52%

Profit percentage on sales = Profit/sales prices*100

Profit percentage on sales = 6.8£/16.8£*100

Profit percentage on sales =40.47%

On the basis of the above calculation it can be concluded that total cost of the product

including VAT and mark up value is £16.8 whereas company charges only £16. This reflects that

Blue Island restaurant is facing £0.8 loss from per customer. The percentage of cost on sales is

59.52% whereas profit percentage is 40.47%.

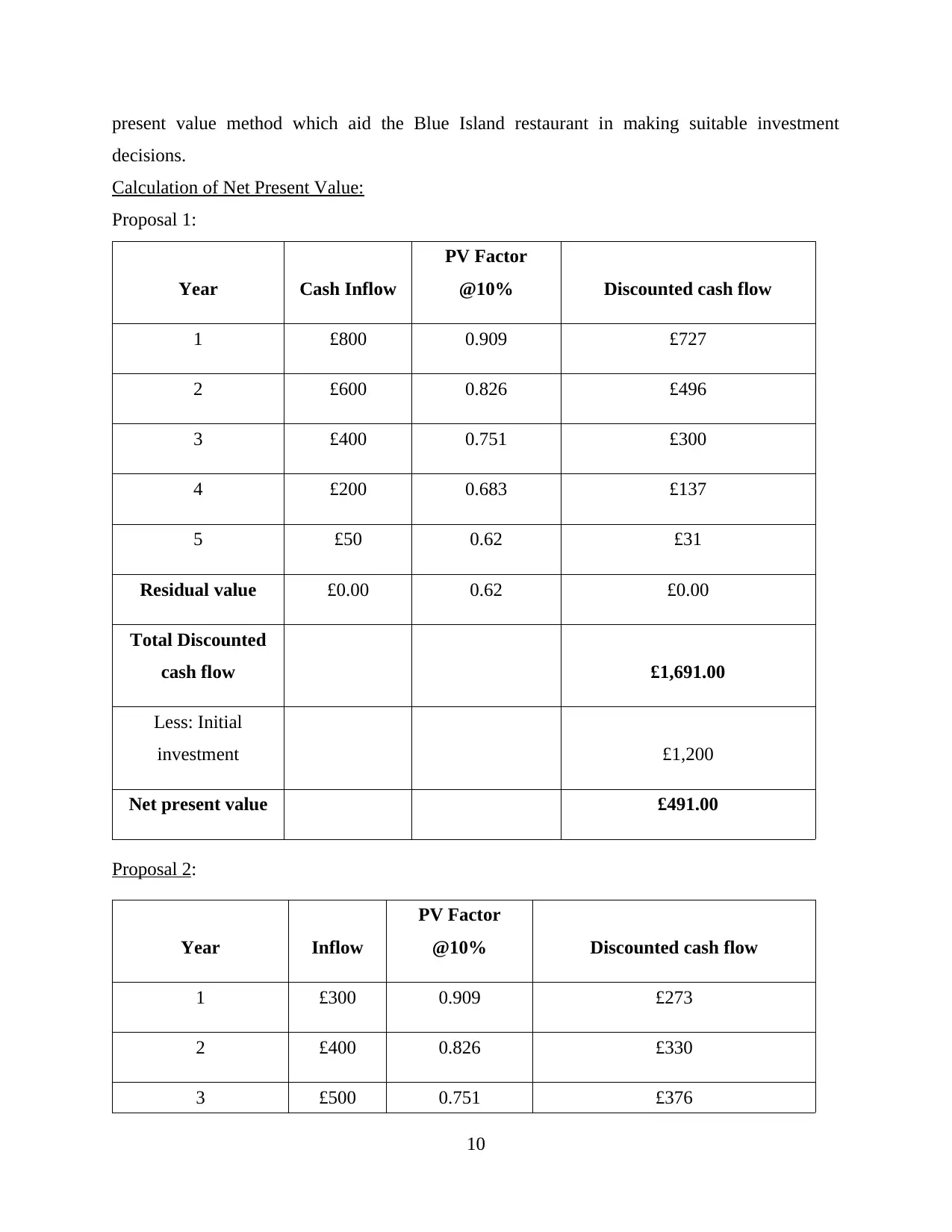

3.3 Viability of two proposal by using investment appraisal techniques

Investment appraisal technique is the tool that is used by the company in order to assess

the reliability and viability of the projects. This technique involves Payback period and Net

9

Price to charge customer 16.8

Currently changing 16

VAT

Price exclusive VAT (Net) = 100%

VAT = 20%

Selling price inclusive (gross) =120%

Food cost percentage= Total costs of ingredients/sales price

Food cost percentage = Total costs of ingredients/Sale prices

Food cost percentage = 10£/16.8 £*100

Food cost percentage = 59.52%

Profit percentage on sales = Profit/sales prices*100

Profit percentage on sales = 6.8£/16.8£*100

Profit percentage on sales =40.47%

On the basis of the above calculation it can be concluded that total cost of the product

including VAT and mark up value is £16.8 whereas company charges only £16. This reflects that

Blue Island restaurant is facing £0.8 loss from per customer. The percentage of cost on sales is

59.52% whereas profit percentage is 40.47%.

3.3 Viability of two proposal by using investment appraisal techniques

Investment appraisal technique is the tool that is used by the company in order to assess

the reliability and viability of the projects. This technique involves Payback period and Net

9

present value method which aid the Blue Island restaurant in making suitable investment

decisions.

Calculation of Net Present Value:

Proposal 1:

Year Cash Inflow

PV Factor

@10% Discounted cash flow

1 £800 0.909 £727

2 £600 0.826 £496

3 £400 0.751 £300

4 £200 0.683 £137

5 £50 0.62 £31

Residual value £0.00 0.62 £0.00

Total Discounted

cash flow £1,691.00

Less: Initial

investment £1,200

Net present value £491.00

Proposal 2:

Year Inflow

PV Factor

@10% Discounted cash flow

1 £300 0.909 £273

2 £400 0.826 £330

3 £500 0.751 £376

10

decisions.

Calculation of Net Present Value:

Proposal 1:

Year Cash Inflow

PV Factor

@10% Discounted cash flow

1 £800 0.909 £727

2 £600 0.826 £496

3 £400 0.751 £300

4 £200 0.683 £137

5 £50 0.62 £31

Residual value £0.00 0.62 £0.00

Total Discounted

cash flow £1,691.00

Less: Initial

investment £1,200

Net present value £491.00

Proposal 2:

Year Inflow

PV Factor

@10% Discounted cash flow

1 £300 0.909 £273

2 £400 0.826 £330

3 £500 0.751 £376

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.