Financial Resource Management Report: Sweet Menu Restaurant Expansion

VerifiedAdded on 2020/01/28

|18

|5575

|47

Report

AI Summary

This report provides a comprehensive financial analysis of Sweet Menu Restaurant, focusing on its expansion plans. It identifies and evaluates various sources of finance, including internal and external options such as retained earnings, bank loans, and share issuance, assessing the implications of each. The report analyzes the costs associated with different financing methods and emphasizes the importance of financial planning for new projects. It assesses the information needs of different decision-makers within the restaurant and explains the impact of financing choices on financial statements. Furthermore, the report delves into budgeting, unit cost calculations, and investment appraisal techniques like payback period and net present value to evaluate project viability. Finally, it discusses the main financial statements and interprets them using ratio analysis, providing a comparative view of the restaurant's financial performance.

MFRD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

introduction....................................................................................................................................1

task 1................................................................................................................................................1

1.1 Identification of the sources of finance available to Sweet Menu Restaurant Ltd................1

1.2 Assessment of the implications of the sources of finance.....................................................2

1.3 Evaluations of the most appropriate sources of finance for Sweet Menu Restaurant...........3

Task 2...............................................................................................................................................4

2.1 Analysing costs of the different sources of finance...............................................................4

2.2 Importance of financial planning for Sweet Menu Restaurant for new project....................4

2.3 Assessment of the information needs of different decision makers in Sweet Menu

Restaurant....................................................................................................................................5

2.4 Explaining impact of sources of finance on financial statements..........................................6

Task 3...............................................................................................................................................7

3.1 Analysis of the budget and making appropriate decisions....................................................7

3.2 Calculation of the unit costs (meal cost) and making pricing decisions................................7

3.3 Viability of two projects using investment appraisal techniques..........................................8

a) Payback period method:......................................................................................................8

b) Net Present Value (NPV)....................................................................................................9

Task 4.............................................................................................................................................10

4.1 Main financial statements....................................................................................................10

4.2 Comparison of appropriate formats of financial statements for different types of business

...................................................................................................................................................11

4.3 Interpretation of the financial statements using ratio analysis.............................................11

conclusion......................................................................................................................................12

references.......................................................................................................................................13

introduction....................................................................................................................................1

task 1................................................................................................................................................1

1.1 Identification of the sources of finance available to Sweet Menu Restaurant Ltd................1

1.2 Assessment of the implications of the sources of finance.....................................................2

1.3 Evaluations of the most appropriate sources of finance for Sweet Menu Restaurant...........3

Task 2...............................................................................................................................................4

2.1 Analysing costs of the different sources of finance...............................................................4

2.2 Importance of financial planning for Sweet Menu Restaurant for new project....................4

2.3 Assessment of the information needs of different decision makers in Sweet Menu

Restaurant....................................................................................................................................5

2.4 Explaining impact of sources of finance on financial statements..........................................6

Task 3...............................................................................................................................................7

3.1 Analysis of the budget and making appropriate decisions....................................................7

3.2 Calculation of the unit costs (meal cost) and making pricing decisions................................7

3.3 Viability of two projects using investment appraisal techniques..........................................8

a) Payback period method:......................................................................................................8

b) Net Present Value (NPV)....................................................................................................9

Task 4.............................................................................................................................................10

4.1 Main financial statements....................................................................................................10

4.2 Comparison of appropriate formats of financial statements for different types of business

...................................................................................................................................................11

4.3 Interpretation of the financial statements using ratio analysis.............................................11

conclusion......................................................................................................................................12

references.......................................................................................................................................13

TABLE OF FIGURES

Figure 1: Available sources of finance............................................................................................1

LIST OF TABLES

Table 1: Calculation of unit cost and selling price..........................................................................7

Table 2: Payback period for proposal 1...........................................................................................8

Table 3: Payback period for proposal 2...........................................................................................9

Table 4: NPV for proposal 1............................................................................................................9

Table 5: NPV for proposal 2..........................................................................................................10

Table 6: Ratio analysis of Sweet Menu and Blue Island Restaurant.............................................12

Figure 1: Available sources of finance............................................................................................1

LIST OF TABLES

Table 1: Calculation of unit cost and selling price..........................................................................7

Table 2: Payback period for proposal 1...........................................................................................8

Table 3: Payback period for proposal 2...........................................................................................9

Table 4: NPV for proposal 1............................................................................................................9

Table 5: NPV for proposal 2..........................................................................................................10

Table 6: Ratio analysis of Sweet Menu and Blue Island Restaurant.............................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Managing financial resources is an essential part of the organization. It allocates available

finance to different operations of the company. Management and allocation of funds are also

considered as a major function of financial department (Ramírez, Selsky and Van der Heijden,

2010). The current research project is based on managing financial resources and decisions. It is

based on Sweet Menu Restaurant that wants to start two new restaurants. The current research

emphasizes on sources of finance available for this organization. Further, study focuses on

different financial resources of the firm. Report will describe different information which helps

in making appropriate financial decisions. Further, financial performance of the organization is

also described the following paragraphs of the report.

TASK 1

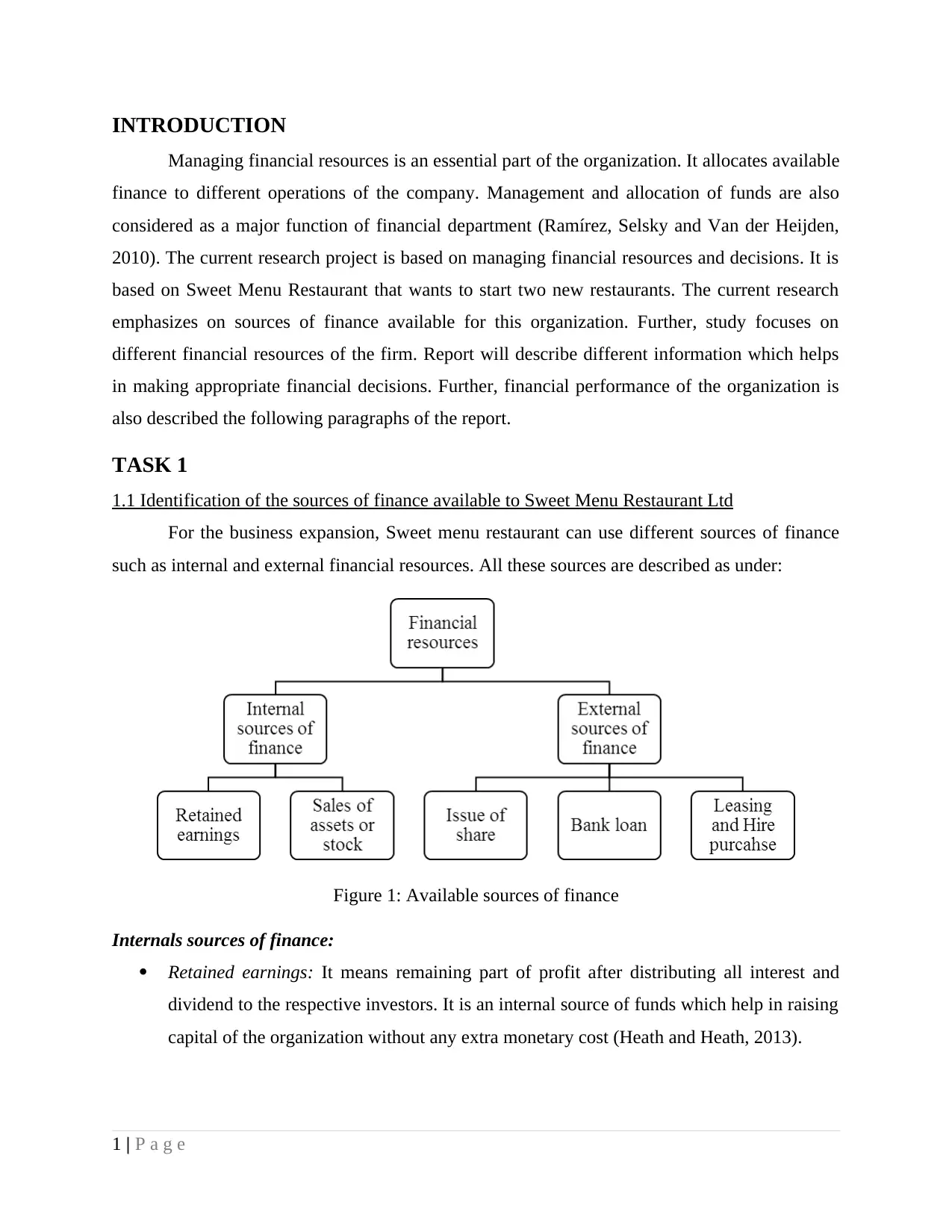

1.1 Identification of the sources of finance available to Sweet Menu Restaurant Ltd

For the business expansion, Sweet menu restaurant can use different sources of finance

such as internal and external financial resources. All these sources are described as under:

Figure 1: Available sources of finance

Internals sources of finance:

Retained earnings: It means remaining part of profit after distributing all interest and

dividend to the respective investors. It is an internal source of funds which help in raising

capital of the organization without any extra monetary cost (Heath and Heath, 2013).

1 | P a g e

Managing financial resources is an essential part of the organization. It allocates available

finance to different operations of the company. Management and allocation of funds are also

considered as a major function of financial department (Ramírez, Selsky and Van der Heijden,

2010). The current research project is based on managing financial resources and decisions. It is

based on Sweet Menu Restaurant that wants to start two new restaurants. The current research

emphasizes on sources of finance available for this organization. Further, study focuses on

different financial resources of the firm. Report will describe different information which helps

in making appropriate financial decisions. Further, financial performance of the organization is

also described the following paragraphs of the report.

TASK 1

1.1 Identification of the sources of finance available to Sweet Menu Restaurant Ltd

For the business expansion, Sweet menu restaurant can use different sources of finance

such as internal and external financial resources. All these sources are described as under:

Figure 1: Available sources of finance

Internals sources of finance:

Retained earnings: It means remaining part of profit after distributing all interest and

dividend to the respective investors. It is an internal source of funds which help in raising

capital of the organization without any extra monetary cost (Heath and Heath, 2013).

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

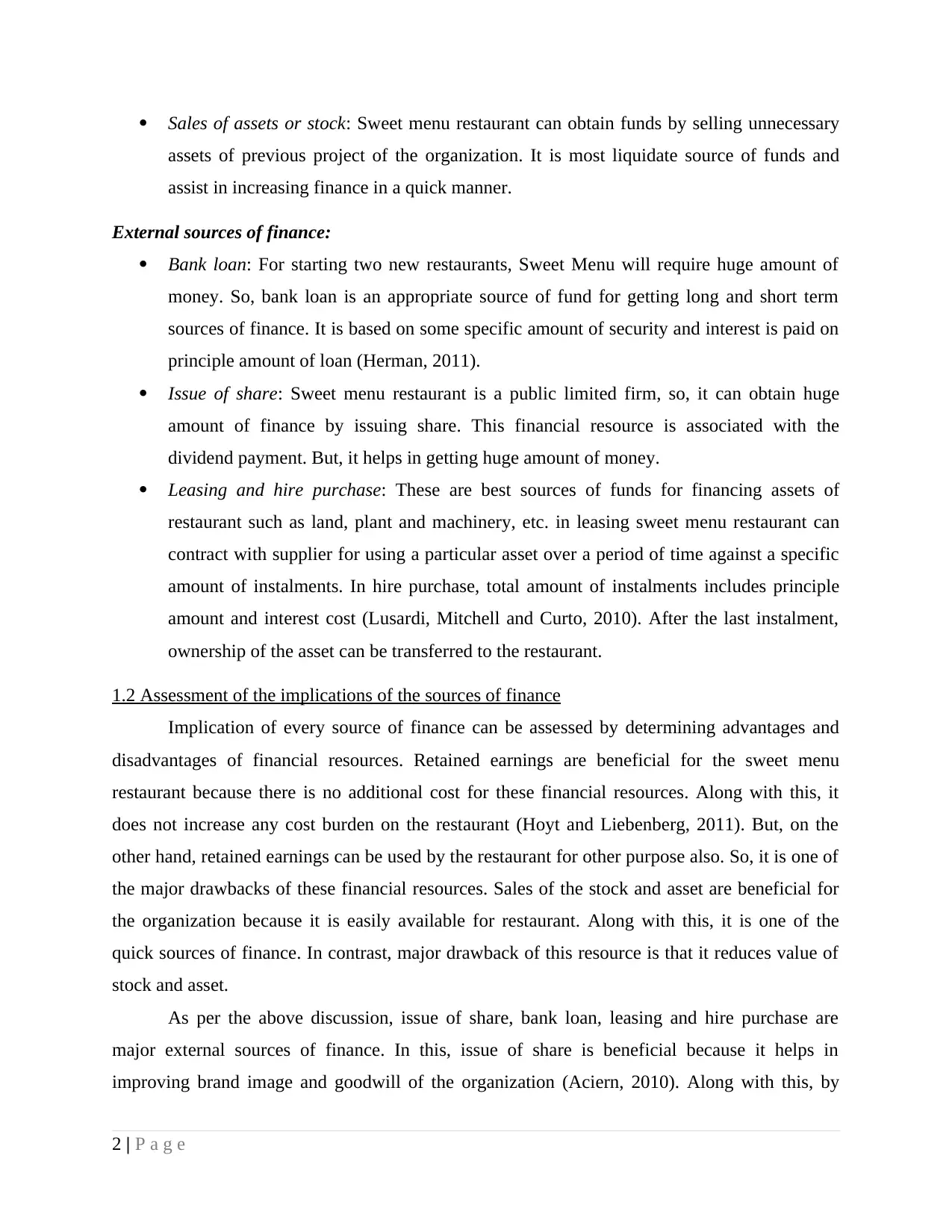

Sales of assets or stock: Sweet menu restaurant can obtain funds by selling unnecessary

assets of previous project of the organization. It is most liquidate source of funds and

assist in increasing finance in a quick manner.

External sources of finance:

Bank loan: For starting two new restaurants, Sweet Menu will require huge amount of

money. So, bank loan is an appropriate source of fund for getting long and short term

sources of finance. It is based on some specific amount of security and interest is paid on

principle amount of loan (Herman, 2011).

Issue of share: Sweet menu restaurant is a public limited firm, so, it can obtain huge

amount of finance by issuing share. This financial resource is associated with the

dividend payment. But, it helps in getting huge amount of money.

Leasing and hire purchase: These are best sources of funds for financing assets of

restaurant such as land, plant and machinery, etc. in leasing sweet menu restaurant can

contract with supplier for using a particular asset over a period of time against a specific

amount of instalments. In hire purchase, total amount of instalments includes principle

amount and interest cost (Lusardi, Mitchell and Curto, 2010). After the last instalment,

ownership of the asset can be transferred to the restaurant.

1.2 Assessment of the implications of the sources of finance

Implication of every source of finance can be assessed by determining advantages and

disadvantages of financial resources. Retained earnings are beneficial for the sweet menu

restaurant because there is no additional cost for these financial resources. Along with this, it

does not increase any cost burden on the restaurant (Hoyt and Liebenberg, 2011). But, on the

other hand, retained earnings can be used by the restaurant for other purpose also. So, it is one of

the major drawbacks of these financial resources. Sales of the stock and asset are beneficial for

the organization because it is easily available for restaurant. Along with this, it is one of the

quick sources of finance. In contrast, major drawback of this resource is that it reduces value of

stock and asset.

As per the above discussion, issue of share, bank loan, leasing and hire purchase are

major external sources of finance. In this, issue of share is beneficial because it helps in

improving brand image and goodwill of the organization (Aciern, 2010). Along with this, by

2 | P a g e

assets of previous project of the organization. It is most liquidate source of funds and

assist in increasing finance in a quick manner.

External sources of finance:

Bank loan: For starting two new restaurants, Sweet Menu will require huge amount of

money. So, bank loan is an appropriate source of fund for getting long and short term

sources of finance. It is based on some specific amount of security and interest is paid on

principle amount of loan (Herman, 2011).

Issue of share: Sweet menu restaurant is a public limited firm, so, it can obtain huge

amount of finance by issuing share. This financial resource is associated with the

dividend payment. But, it helps in getting huge amount of money.

Leasing and hire purchase: These are best sources of funds for financing assets of

restaurant such as land, plant and machinery, etc. in leasing sweet menu restaurant can

contract with supplier for using a particular asset over a period of time against a specific

amount of instalments. In hire purchase, total amount of instalments includes principle

amount and interest cost (Lusardi, Mitchell and Curto, 2010). After the last instalment,

ownership of the asset can be transferred to the restaurant.

1.2 Assessment of the implications of the sources of finance

Implication of every source of finance can be assessed by determining advantages and

disadvantages of financial resources. Retained earnings are beneficial for the sweet menu

restaurant because there is no additional cost for these financial resources. Along with this, it

does not increase any cost burden on the restaurant (Hoyt and Liebenberg, 2011). But, on the

other hand, retained earnings can be used by the restaurant for other purpose also. So, it is one of

the major drawbacks of these financial resources. Sales of the stock and asset are beneficial for

the organization because it is easily available for restaurant. Along with this, it is one of the

quick sources of finance. In contrast, major drawback of this resource is that it reduces value of

stock and asset.

As per the above discussion, issue of share, bank loan, leasing and hire purchase are

major external sources of finance. In this, issue of share is beneficial because it helps in

improving brand image and goodwill of the organization (Aciern, 2010). Along with this, by

2 | P a g e

using these resources sweet menu restaurant can raise its capital with big amount of finance. But,

it is linked with the dividend payment which can reduce profitability of the firm. Bank loan is

significant for the current restaurant because it helps in getting big amount of money for long

time. It provides time to return the loan amount and by using this source, organization can get

huge amount of money. But on the other hand, interest on loan and security amount increases the

total cost of the sources of finance which can affect the total income of sweet menu restaurant in

future. Similarly, leasing and hire purchases are the most appropriate source for financing asset

because it reduces initial investment of restaurant (Surroca, Tribó and Waddock, 2010). But on

the other hand instalment payments increases total cost of the asset.

Therefore, each and every source of finance has its own advantages and disadvantages.

So, before using these sources sweet menu restaurant is required to analyse their advantages and

disadvantages.

1.3 Evaluations of the most appropriate sources of finance for Sweet Menu Restaurant

Each and every resource can affect the financial performance of sweet menu restaurant in

positive and in a negative manner. According to the analysis, bank loan is the most appropriate

financial resource for sweet menu restaurant. It is suitable for this organization because the

restaurant can easily procure specific amount of loan very easily. Along with this, it is available

for short, medium and long term financing (Graham, Harvey and Puri, 2013). Along with this,

interest paid on the bank loan is tax deductible expenses for sweet menu restaurant which help in

increasing profit and reducing tax expenses of the organization.

Retained earnings are linked with opportunity cost but bank loan is associated with only

some specific amount of monetary cost. So, bank loan is better as compare to the retained

earnings. Obtaining funds from bank loan is a time consuming process for restaurant but on the

other hand sale of asset is one of the quickest source of fund. Along with this, it can also provide

money as compare to internal source of funds. Issue of share is associated with dividend payment

and rate of dividend is high as compare to interest payment. Leasing and hire purchase are also

costly source of funds as compare to bank loan (Kuhnen and Knutson, 2011). So, it is the most

suitable financial resource for sweet menu restaurant for raising its capital.

3 | P a g e

it is linked with the dividend payment which can reduce profitability of the firm. Bank loan is

significant for the current restaurant because it helps in getting big amount of money for long

time. It provides time to return the loan amount and by using this source, organization can get

huge amount of money. But on the other hand, interest on loan and security amount increases the

total cost of the sources of finance which can affect the total income of sweet menu restaurant in

future. Similarly, leasing and hire purchases are the most appropriate source for financing asset

because it reduces initial investment of restaurant (Surroca, Tribó and Waddock, 2010). But on

the other hand instalment payments increases total cost of the asset.

Therefore, each and every source of finance has its own advantages and disadvantages.

So, before using these sources sweet menu restaurant is required to analyse their advantages and

disadvantages.

1.3 Evaluations of the most appropriate sources of finance for Sweet Menu Restaurant

Each and every resource can affect the financial performance of sweet menu restaurant in

positive and in a negative manner. According to the analysis, bank loan is the most appropriate

financial resource for sweet menu restaurant. It is suitable for this organization because the

restaurant can easily procure specific amount of loan very easily. Along with this, it is available

for short, medium and long term financing (Graham, Harvey and Puri, 2013). Along with this,

interest paid on the bank loan is tax deductible expenses for sweet menu restaurant which help in

increasing profit and reducing tax expenses of the organization.

Retained earnings are linked with opportunity cost but bank loan is associated with only

some specific amount of monetary cost. So, bank loan is better as compare to the retained

earnings. Obtaining funds from bank loan is a time consuming process for restaurant but on the

other hand sale of asset is one of the quickest source of fund. Along with this, it can also provide

money as compare to internal source of funds. Issue of share is associated with dividend payment

and rate of dividend is high as compare to interest payment. Leasing and hire purchase are also

costly source of funds as compare to bank loan (Kuhnen and Knutson, 2011). So, it is the most

suitable financial resource for sweet menu restaurant for raising its capital.

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

2.1 Analysing costs of the different sources of finance

Every source of finance is associated with some specific amount of monetary and non-

monetary cost. These costs can increase the cost burden on restaurant which declines the total

profitability of the organization. There is no monetary cost on retained earnings because it is an

internal source of fund and it is easily available for the organization but it is associated with the

opportunity cost (Sheth and et.al, 2011). Similarly, sale of asset and stock are linked with the

depreciation cost which can affect total income and the organization.

Similarly, at the time of issue of share, sweet menu restaurant is required to pay specific

amount of dividend to its shareholders that increases total expenses and total income of the

organization. Rate of dividend is also high as compare to other resources so, it is one of the

costly sources of fund. Including this, for getting bank loan, restaurant needs to pay specific

security amount on behalf of the loan. It increases cost burden on organization. Along with this,

organization needs to pay specific amount of interest on principle amount of loan. It is the major

expenses for the organization (Bamber and Wang, 2010). On the other hand, because of loan the

company can get huge money by which restaurant can satisfy financial needs of the organization.

Leasing and hire purchase can be calculated by sum of all instalments. These instalments include

interest payment. Further, it also increases the total cost of asset. It is also considered as a costly

source of fund for the organization. Therefore, cost of financial resources augments the total

expenses of the firm which have positive and negative impact on the financial position of

restaurant (Campbell and et.al, 2011).

2.2 Importance of financial planning for Sweet Menu Restaurant for new project

Financial planning can be defined as a process of financial management which focuses on

available and required funds for expanding business of the restaurant. Along with this, it also

emphasizes on allocating funds and monetary performance of the organization (Financial

Resources Management Service (FRMS), 2016). Appropriate planning of available and required

finance is one of the most important tasks for success of business expansion project of sweet

menu restaurant. Planning of funds is beneficial for the organization because it helps in

effectively arranging and allocating funds as per the requirement of the business operations. It

also reduces unnecessary requirement of finance. Sound financial planning helps sweet menu

restaurant in investing in most viable or in the profitable projects (Financial Planning: it’s

4 | P a g e

2.1 Analysing costs of the different sources of finance

Every source of finance is associated with some specific amount of monetary and non-

monetary cost. These costs can increase the cost burden on restaurant which declines the total

profitability of the organization. There is no monetary cost on retained earnings because it is an

internal source of fund and it is easily available for the organization but it is associated with the

opportunity cost (Sheth and et.al, 2011). Similarly, sale of asset and stock are linked with the

depreciation cost which can affect total income and the organization.

Similarly, at the time of issue of share, sweet menu restaurant is required to pay specific

amount of dividend to its shareholders that increases total expenses and total income of the

organization. Rate of dividend is also high as compare to other resources so, it is one of the

costly sources of fund. Including this, for getting bank loan, restaurant needs to pay specific

security amount on behalf of the loan. It increases cost burden on organization. Along with this,

organization needs to pay specific amount of interest on principle amount of loan. It is the major

expenses for the organization (Bamber and Wang, 2010). On the other hand, because of loan the

company can get huge money by which restaurant can satisfy financial needs of the organization.

Leasing and hire purchase can be calculated by sum of all instalments. These instalments include

interest payment. Further, it also increases the total cost of asset. It is also considered as a costly

source of fund for the organization. Therefore, cost of financial resources augments the total

expenses of the firm which have positive and negative impact on the financial position of

restaurant (Campbell and et.al, 2011).

2.2 Importance of financial planning for Sweet Menu Restaurant for new project

Financial planning can be defined as a process of financial management which focuses on

available and required funds for expanding business of the restaurant. Along with this, it also

emphasizes on allocating funds and monetary performance of the organization (Financial

Resources Management Service (FRMS), 2016). Appropriate planning of available and required

finance is one of the most important tasks for success of business expansion project of sweet

menu restaurant. Planning of funds is beneficial for the organization because it helps in

effectively arranging and allocating funds as per the requirement of the business operations. It

also reduces unnecessary requirement of finance. Sound financial planning helps sweet menu

restaurant in investing in most viable or in the profitable projects (Financial Planning: it’s

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Meaning, Importance and Elements, 2016). It is a base for financial control because by using

appropriate financial targets, organization can compare actual and planned performance of the

restaurant which helps in making necessary changes for managing finance. Appropriate

utilization of finance is also one of the major benefits of financial planning. Suitable planning of

finance provides assistance at the time of making financial and investment decisions. It develops

appropriate coordination between different departments such as finance, marketing sales and

operations (Borrego, Froyd and Hall, 2010). Planning of funds is not only beneficial for the

present finance management but also for future financial management of sweet menu restaurant.

Therefore, improvement in current and future financial performance is an important benefit of

financial planning.

2.3 Assessment of the information needs of different decision makers in Sweet Menu Restaurant

Expansion of business is the major objective of sweet menu restaurant and for attaining

this objective, the firm is required to make number of decisions. All these decisions are made by

the different decision makers and they require distinct information which is described as follows:

Financial manager: All financial decisions are taken by the manager of finance

department of sweet menu restaurant. So, for making such decision manager requires

information about current and future financial requirements and performance of the firm.

In addition, manager of finance focuses on cost reduction and profit maximization. It is

important for the finance manger to have information about available project of

investment and proposed budget (Financial Resources Management Department, 2016).

Human resource manager: Personnel manager takes decisions about recruitment and

selection of human resource. Along with this, human resource manager also makes

arrangement for training and development program for the employee. For these decisions,

manager requires appropriate information about salary and wages of every employee as

well as human resource budget of sweet menu restaurant.

Marketing manager: Budget for advertisement and promotion of both restaurants is one

of the major information for making any marketing decisions for sweet menu restaurant.

Along with this, marketing manager needs facts and figures about advertisement

expenses of the company of past year (Benninga, 2010).

5 | P a g e

appropriate financial targets, organization can compare actual and planned performance of the

restaurant which helps in making necessary changes for managing finance. Appropriate

utilization of finance is also one of the major benefits of financial planning. Suitable planning of

finance provides assistance at the time of making financial and investment decisions. It develops

appropriate coordination between different departments such as finance, marketing sales and

operations (Borrego, Froyd and Hall, 2010). Planning of funds is not only beneficial for the

present finance management but also for future financial management of sweet menu restaurant.

Therefore, improvement in current and future financial performance is an important benefit of

financial planning.

2.3 Assessment of the information needs of different decision makers in Sweet Menu Restaurant

Expansion of business is the major objective of sweet menu restaurant and for attaining

this objective, the firm is required to make number of decisions. All these decisions are made by

the different decision makers and they require distinct information which is described as follows:

Financial manager: All financial decisions are taken by the manager of finance

department of sweet menu restaurant. So, for making such decision manager requires

information about current and future financial requirements and performance of the firm.

In addition, manager of finance focuses on cost reduction and profit maximization. It is

important for the finance manger to have information about available project of

investment and proposed budget (Financial Resources Management Department, 2016).

Human resource manager: Personnel manager takes decisions about recruitment and

selection of human resource. Along with this, human resource manager also makes

arrangement for training and development program for the employee. For these decisions,

manager requires appropriate information about salary and wages of every employee as

well as human resource budget of sweet menu restaurant.

Marketing manager: Budget for advertisement and promotion of both restaurants is one

of the major information for making any marketing decisions for sweet menu restaurant.

Along with this, marketing manager needs facts and figures about advertisement

expenses of the company of past year (Benninga, 2010).

5 | P a g e

Operation manager: Cost of goods sold and investment in machinery and equipment,

inventory cost are the major information which are required by the operation manager at

the time of making operation and production decisions for sweet menu restaurant.

Government: Decisions about tax payment and financial reporting of sweet menu

restaurant are taken by government of the nation. So, for making these decisions

government require information about financial performance of the restaurant (The Four

Major Decisions in Corporate Finance, 2016).

Supplier: Data about the required amount of raw material is the major information which

is required by the supplier at the time of making decisions about supply chain

management of sweet menu restaurant (Marazzi, 2011).

2.4 Explaining impact of sources of finance on financial statements

Financial statement helps in summarizing all financial transactions of Sweet menu

restaurant in an effective manner. This is a public limited company so, major financial statements

of the organization are income statement, profitable and loss account and cash flow statement of

the organization. All the above discussed financial resources have positive and negative impacts

on the financial statements. Retained earnings are not linked with any monetary cost so, it does

not affect income statement and cash flow statement of the organization. But it increases liability

in the balance sheet (Davies and Crawford, 2011). Sales of asset increase the depreciation cost

which is one of the major expenses of the organization. This expenditure reduces total income

and profitability in profit and loss account of sweet menu restaurant. Along with this, it reduces

the asset value in the balance sheet.

Bank loan increases the liability in balance sheet of sweet menu restaurant and it further

increases total expenses because of the interest payment. Interest amount reduces total

profitability and increase the total cash outflow of the organization. It is also considered as

expenses for the organization which affect profitability of the firm. Leasing and hire purchase is

associated with instalments which increase total expenses in income statement and reduce the

total cash inflow and augment the total cash out flow of the firm (Chen, Cheng and Mehta,

2013).

6 | P a g e

inventory cost are the major information which are required by the operation manager at

the time of making operation and production decisions for sweet menu restaurant.

Government: Decisions about tax payment and financial reporting of sweet menu

restaurant are taken by government of the nation. So, for making these decisions

government require information about financial performance of the restaurant (The Four

Major Decisions in Corporate Finance, 2016).

Supplier: Data about the required amount of raw material is the major information which

is required by the supplier at the time of making decisions about supply chain

management of sweet menu restaurant (Marazzi, 2011).

2.4 Explaining impact of sources of finance on financial statements

Financial statement helps in summarizing all financial transactions of Sweet menu

restaurant in an effective manner. This is a public limited company so, major financial statements

of the organization are income statement, profitable and loss account and cash flow statement of

the organization. All the above discussed financial resources have positive and negative impacts

on the financial statements. Retained earnings are not linked with any monetary cost so, it does

not affect income statement and cash flow statement of the organization. But it increases liability

in the balance sheet (Davies and Crawford, 2011). Sales of asset increase the depreciation cost

which is one of the major expenses of the organization. This expenditure reduces total income

and profitability in profit and loss account of sweet menu restaurant. Along with this, it reduces

the asset value in the balance sheet.

Bank loan increases the liability in balance sheet of sweet menu restaurant and it further

increases total expenses because of the interest payment. Interest amount reduces total

profitability and increase the total cash outflow of the organization. It is also considered as

expenses for the organization which affect profitability of the firm. Leasing and hire purchase is

associated with instalments which increase total expenses in income statement and reduce the

total cash inflow and augment the total cash out flow of the firm (Chen, Cheng and Mehta,

2013).

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

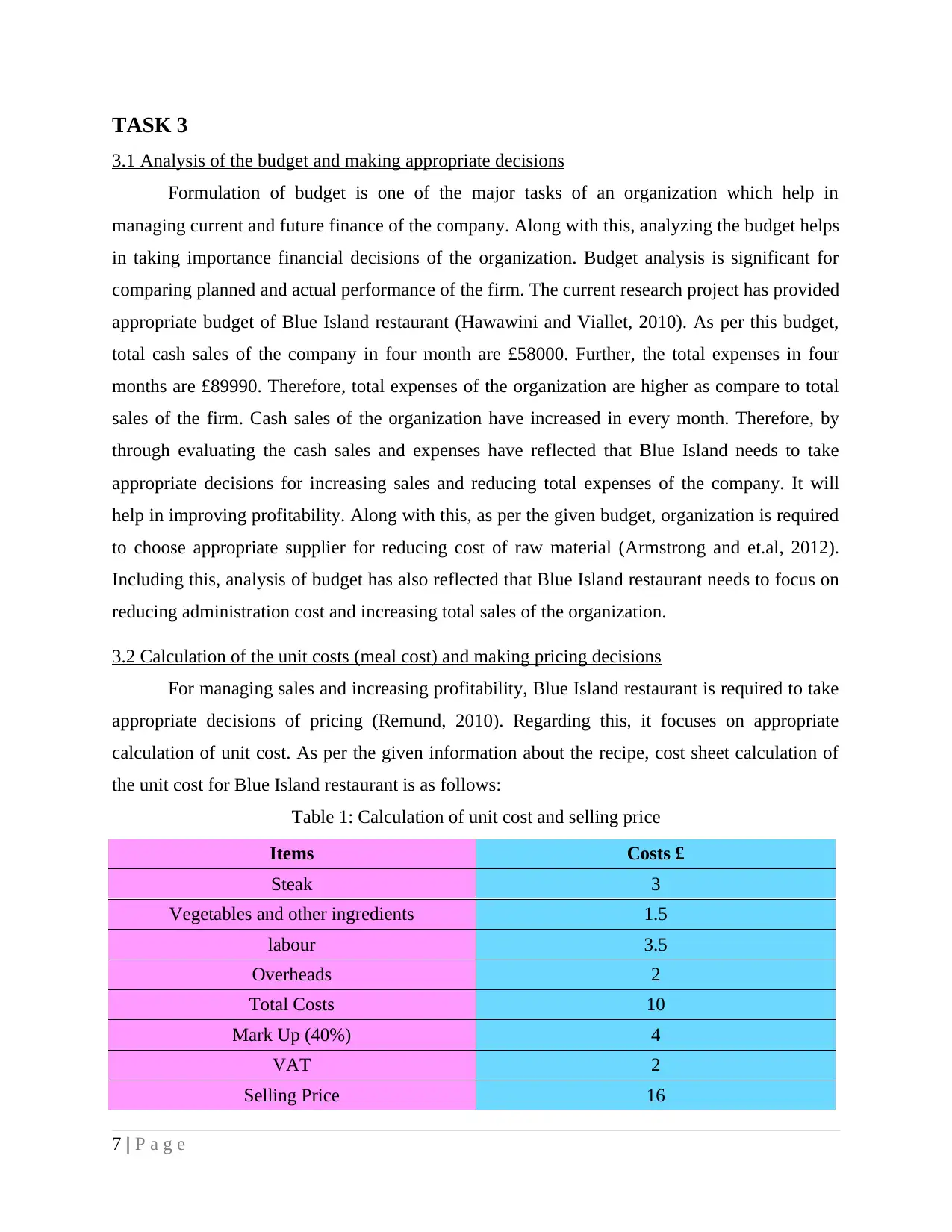

3.1 Analysis of the budget and making appropriate decisions

Formulation of budget is one of the major tasks of an organization which help in

managing current and future finance of the company. Along with this, analyzing the budget helps

in taking importance financial decisions of the organization. Budget analysis is significant for

comparing planned and actual performance of the firm. The current research project has provided

appropriate budget of Blue Island restaurant (Hawawini and Viallet, 2010). As per this budget,

total cash sales of the company in four month are £58000. Further, the total expenses in four

months are £89990. Therefore, total expenses of the organization are higher as compare to total

sales of the firm. Cash sales of the organization have increased in every month. Therefore, by

through evaluating the cash sales and expenses have reflected that Blue Island needs to take

appropriate decisions for increasing sales and reducing total expenses of the company. It will

help in improving profitability. Along with this, as per the given budget, organization is required

to choose appropriate supplier for reducing cost of raw material (Armstrong and et.al, 2012).

Including this, analysis of budget has also reflected that Blue Island restaurant needs to focus on

reducing administration cost and increasing total sales of the organization.

3.2 Calculation of the unit costs (meal cost) and making pricing decisions

For managing sales and increasing profitability, Blue Island restaurant is required to take

appropriate decisions of pricing (Remund, 2010). Regarding this, it focuses on appropriate

calculation of unit cost. As per the given information about the recipe, cost sheet calculation of

the unit cost for Blue Island restaurant is as follows:

Table 1: Calculation of unit cost and selling price

Items Costs £

Steak 3

Vegetables and other ingredients 1.5

labour 3.5

Overheads 2

Total Costs 10

Mark Up (40%) 4

VAT 2

Selling Price 16

7 | P a g e

3.1 Analysis of the budget and making appropriate decisions

Formulation of budget is one of the major tasks of an organization which help in

managing current and future finance of the company. Along with this, analyzing the budget helps

in taking importance financial decisions of the organization. Budget analysis is significant for

comparing planned and actual performance of the firm. The current research project has provided

appropriate budget of Blue Island restaurant (Hawawini and Viallet, 2010). As per this budget,

total cash sales of the company in four month are £58000. Further, the total expenses in four

months are £89990. Therefore, total expenses of the organization are higher as compare to total

sales of the firm. Cash sales of the organization have increased in every month. Therefore, by

through evaluating the cash sales and expenses have reflected that Blue Island needs to take

appropriate decisions for increasing sales and reducing total expenses of the company. It will

help in improving profitability. Along with this, as per the given budget, organization is required

to choose appropriate supplier for reducing cost of raw material (Armstrong and et.al, 2012).

Including this, analysis of budget has also reflected that Blue Island restaurant needs to focus on

reducing administration cost and increasing total sales of the organization.

3.2 Calculation of the unit costs (meal cost) and making pricing decisions

For managing sales and increasing profitability, Blue Island restaurant is required to take

appropriate decisions of pricing (Remund, 2010). Regarding this, it focuses on appropriate

calculation of unit cost. As per the given information about the recipe, cost sheet calculation of

the unit cost for Blue Island restaurant is as follows:

Table 1: Calculation of unit cost and selling price

Items Costs £

Steak 3

Vegetables and other ingredients 1.5

labour 3.5

Overheads 2

Total Costs 10

Mark Up (40%) 4

VAT 2

Selling Price 16

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total cost of the one unit of product and services of Blue Island restaurant is £10. But,

mark up cost and vat tax increases the selling process of each unit. According to the given

information, restaurant includes 40% mark-up cost on each unit. After adding mark-up cost and

Vat tax, restaurant can sale this particular unit in £16. Therefore, selling price of each unit is £16.

It helps in managing entire cost and getting appropriate profitability also. Overall, unit cost is

one of the major bases for deciding selling price for each unit (Brue, 2015).

3.3 Viability of two projects using investment appraisal techniques

For expanding business operation, Blue Island is required to invest appropriate amount of

funds in different investment projects. But, before making any decisions organization needs to

check the viability or profitability of these projects. There are number of investment appraisal

methods which can be used by the restaurant for this purpose. Discounted and non-discounted

methods are included in these techniques (Moutinho, 2011). In which payback period and Net

Present Value (NPV) method will be appropriate for checking viability of investment projects for

Blue Island. Calculation of payback period and NPV are as follows:

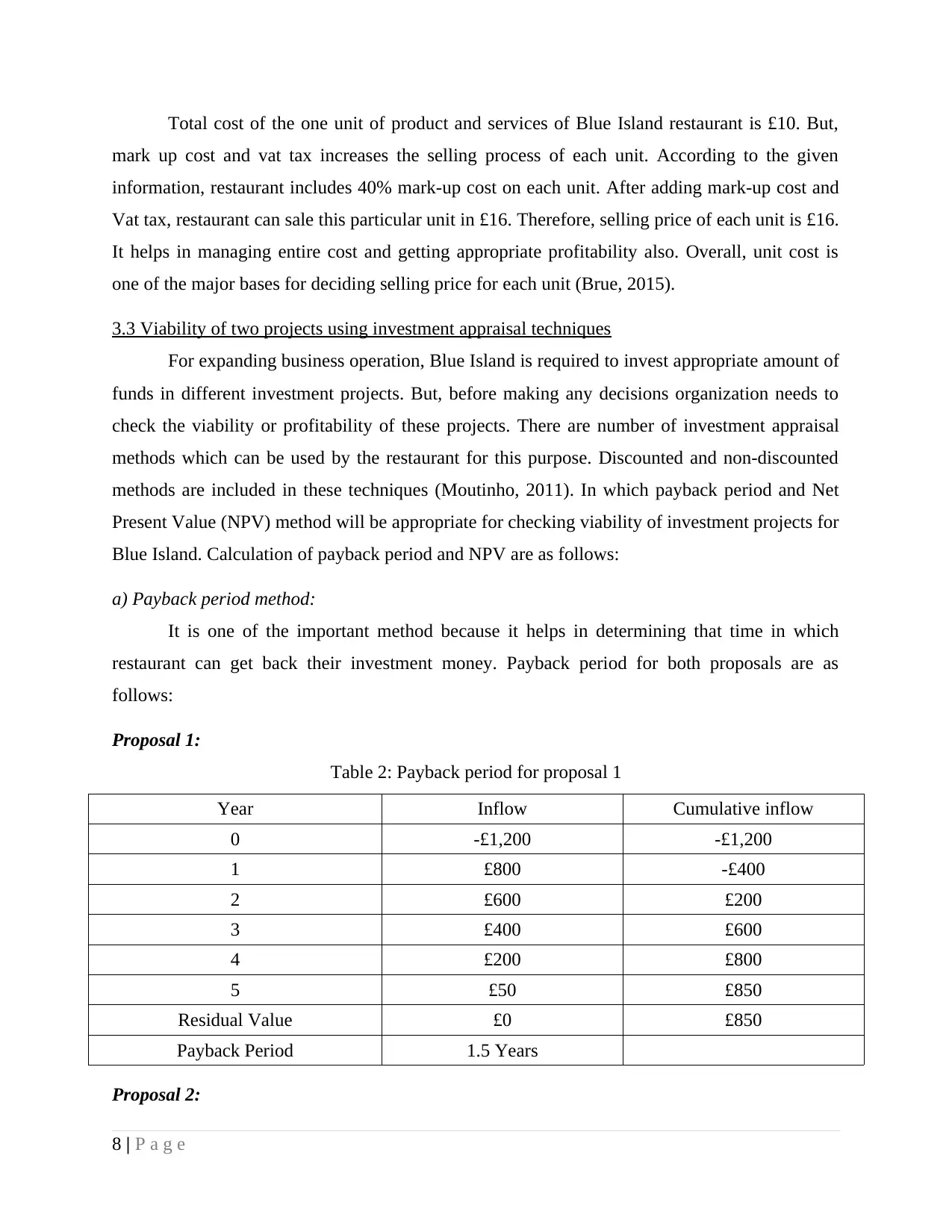

a) Payback period method:

It is one of the important method because it helps in determining that time in which

restaurant can get back their investment money. Payback period for both proposals are as

follows:

Proposal 1:

Table 2: Payback period for proposal 1

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £800 -£400

2 £600 £200

3 £400 £600

4 £200 £800

5 £50 £850

Residual Value £0 £850

Payback Period 1.5 Years

Proposal 2:

8 | P a g e

mark up cost and vat tax increases the selling process of each unit. According to the given

information, restaurant includes 40% mark-up cost on each unit. After adding mark-up cost and

Vat tax, restaurant can sale this particular unit in £16. Therefore, selling price of each unit is £16.

It helps in managing entire cost and getting appropriate profitability also. Overall, unit cost is

one of the major bases for deciding selling price for each unit (Brue, 2015).

3.3 Viability of two projects using investment appraisal techniques

For expanding business operation, Blue Island is required to invest appropriate amount of

funds in different investment projects. But, before making any decisions organization needs to

check the viability or profitability of these projects. There are number of investment appraisal

methods which can be used by the restaurant for this purpose. Discounted and non-discounted

methods are included in these techniques (Moutinho, 2011). In which payback period and Net

Present Value (NPV) method will be appropriate for checking viability of investment projects for

Blue Island. Calculation of payback period and NPV are as follows:

a) Payback period method:

It is one of the important method because it helps in determining that time in which

restaurant can get back their investment money. Payback period for both proposals are as

follows:

Proposal 1:

Table 2: Payback period for proposal 1

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £800 -£400

2 £600 £200

3 £400 £600

4 £200 £800

5 £50 £850

Residual Value £0 £850

Payback Period 1.5 Years

Proposal 2:

8 | P a g e

Table 3: Payback period for proposal 2

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £300 -£900

2 £400 -£500

3 £500 £0

4 £600 £600

5 £500 £1,100

Residual Value £50 £1,150

Payback Period 3 Years

Above calculation have reflected that, payback period for proposal 1 is 1.5 years and for

proposal 2 it is 3 years. Therefore, according to the payback period Blue Island restaurant can get

back its money in 1.5 years if it invests in proposal 1. On the other hand, if organization wants to

invest in proposal 2 than pay back period for this month is 3 years. Therefore, proposal 1 is best

because payback period for proposal 1 is less as compare to proposal 2. So, according to the

above calculation, restaurant needs to select proposal 1 as compare to proposal 2 (Perkins and

et.al, 2012).

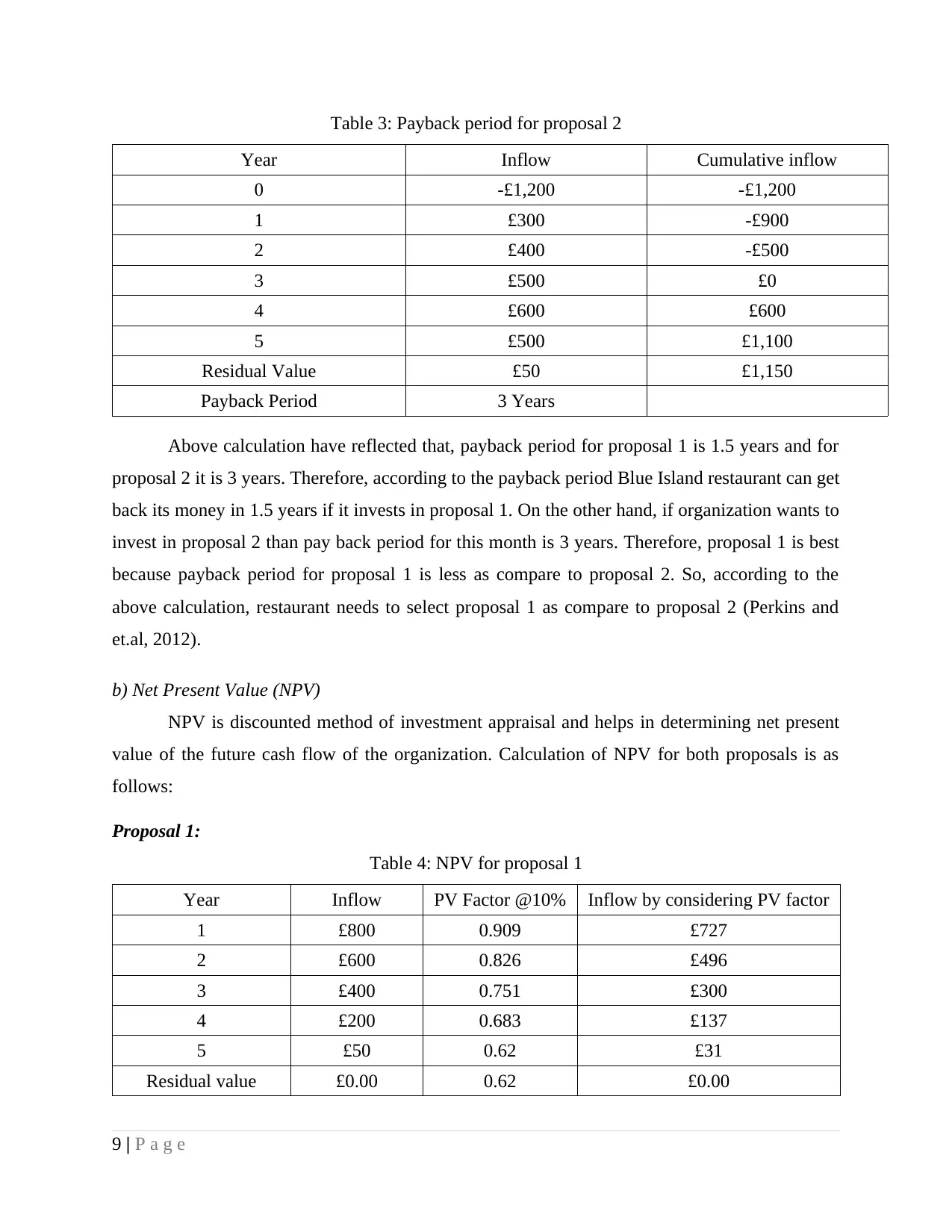

b) Net Present Value (NPV)

NPV is discounted method of investment appraisal and helps in determining net present

value of the future cash flow of the organization. Calculation of NPV for both proposals is as

follows:

Proposal 1:

Table 4: NPV for proposal 1

Year Inflow PV Factor @10% Inflow by considering PV factor

1 £800 0.909 £727

2 £600 0.826 £496

3 £400 0.751 £300

4 £200 0.683 £137

5 £50 0.62 £31

Residual value £0.00 0.62 £0.00

9 | P a g e

Year Inflow Cumulative inflow

0 -£1,200 -£1,200

1 £300 -£900

2 £400 -£500

3 £500 £0

4 £600 £600

5 £500 £1,100

Residual Value £50 £1,150

Payback Period 3 Years

Above calculation have reflected that, payback period for proposal 1 is 1.5 years and for

proposal 2 it is 3 years. Therefore, according to the payback period Blue Island restaurant can get

back its money in 1.5 years if it invests in proposal 1. On the other hand, if organization wants to

invest in proposal 2 than pay back period for this month is 3 years. Therefore, proposal 1 is best

because payback period for proposal 1 is less as compare to proposal 2. So, according to the

above calculation, restaurant needs to select proposal 1 as compare to proposal 2 (Perkins and

et.al, 2012).

b) Net Present Value (NPV)

NPV is discounted method of investment appraisal and helps in determining net present

value of the future cash flow of the organization. Calculation of NPV for both proposals is as

follows:

Proposal 1:

Table 4: NPV for proposal 1

Year Inflow PV Factor @10% Inflow by considering PV factor

1 £800 0.909 £727

2 £600 0.826 £496

3 £400 0.751 £300

4 £200 0.683 £137

5 £50 0.62 £31

Residual value £0.00 0.62 £0.00

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.