Financial Management Report for Sweet Menu Restaurant Expansion Plan

VerifiedAdded on 2020/02/05

|18

|5598

|94

Report

AI Summary

This report examines the financial management strategies employed by Sweet Menu Restaurant (SMR), focusing on the sources of finance available for business expansion. It analyzes both internal sources like retained earnings and sales of assets, and external sources such as bank loans, angel investors, venture capital, and shares. The report delves into the pros and cons of each funding source, evaluating their cost implications and suitability for SMR's expansion plans. Furthermore, it emphasizes the importance of financial planning, including capital structure, investment decisions, operational activities, and future issue management. The report also identifies key decision-makers, including banks, shareholders, government, and employees, and how they utilize SMR's financial information to make informed decisions. Overall, the report provides a comprehensive overview of financial management principles and their application within the context of SMR's business objectives.

MFRD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TASK 1............................................................................................................................................1

1.1................................................................................................................................................1

1.2................................................................................................................................................2

1.3................................................................................................................................................3

TASK 2............................................................................................................................................4

2.1................................................................................................................................................4

2.2................................................................................................................................................4

2.3................................................................................................................................................5

2.4................................................................................................................................................6

TASK 3............................................................................................................................................7

3.1................................................................................................................................................7

3.2................................................................................................................................................8

3.3................................................................................................................................................8

TASK 4 .........................................................................................................................................10

4.1..............................................................................................................................................10

4.2..............................................................................................................................................11

4.3..............................................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

TASK 1............................................................................................................................................1

1.1................................................................................................................................................1

1.2................................................................................................................................................2

1.3................................................................................................................................................3

TASK 2............................................................................................................................................4

2.1................................................................................................................................................4

2.2................................................................................................................................................4

2.3................................................................................................................................................5

2.4................................................................................................................................................6

TASK 3............................................................................................................................................7

3.1................................................................................................................................................7

3.2................................................................................................................................................8

3.3................................................................................................................................................8

TASK 4 .........................................................................................................................................10

4.1..............................................................................................................................................10

4.2..............................................................................................................................................11

4.3..............................................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial managements is very important that is required to be done by the finance

department of any corporate. Financial success of the firm is purely based on appropriate

decisions taken by management. In order to attain financial objective, company requires

formulating strategic plans so that financial opportunities can be identified. The present report is

based on a case study where Sweet Menu Restaurant(SMR) has been taken into consideration

(Jackson, 2010). The cited firm is well known for providing inter-continental food. Company

aims at expanding itself for which it is required to analyse the sources of finance. Cited

document is prepared with the purpose to explain various sources of finance that can be adopted

by company. In addition to this, the requisite financial statements of different firms are also

considered. Aim of this document is to enlighten the importance of financial management in the

cited firm.

TASK 1

1.1

Finance is the most essential element that is required to run a business effectively. To

initiate or expand a business, availability of different sources of finance is essential. Also, there

are two major sources of finance i.e. internal and external. Internal sources are those which are

arranged within organization. On the other side, external sources are available outside the

company (Hayre, 2015). As per the case study, management of SMR wants to open two new

branches in Central London and Croydon. For this, restaurant needs to arrange the amount of ₤

300,000 and ₤ 500,000 for two branches respectively. Apart from that, for the same, there are

various sources of finance available that can be adopted by management.

INTERNAL SOURCES Retained earnings: It is the amount which is kept aside from the profits of company. In

this, amount is taken after paying dividends to the shareholders and drawings by owners.

The management of cited firm can adopt this source as it does not carry fixed burden of

interest or instalments (Epstein and Buhovac, 2014). Sales of assets: In order to arrange the funds, company can use another source where the

assets are sold and from the same, cash is generated. It may remain helpful for SMR

because it can be useful for both; short and long term.

1

Financial managements is very important that is required to be done by the finance

department of any corporate. Financial success of the firm is purely based on appropriate

decisions taken by management. In order to attain financial objective, company requires

formulating strategic plans so that financial opportunities can be identified. The present report is

based on a case study where Sweet Menu Restaurant(SMR) has been taken into consideration

(Jackson, 2010). The cited firm is well known for providing inter-continental food. Company

aims at expanding itself for which it is required to analyse the sources of finance. Cited

document is prepared with the purpose to explain various sources of finance that can be adopted

by company. In addition to this, the requisite financial statements of different firms are also

considered. Aim of this document is to enlighten the importance of financial management in the

cited firm.

TASK 1

1.1

Finance is the most essential element that is required to run a business effectively. To

initiate or expand a business, availability of different sources of finance is essential. Also, there

are two major sources of finance i.e. internal and external. Internal sources are those which are

arranged within organization. On the other side, external sources are available outside the

company (Hayre, 2015). As per the case study, management of SMR wants to open two new

branches in Central London and Croydon. For this, restaurant needs to arrange the amount of ₤

300,000 and ₤ 500,000 for two branches respectively. Apart from that, for the same, there are

various sources of finance available that can be adopted by management.

INTERNAL SOURCES Retained earnings: It is the amount which is kept aside from the profits of company. In

this, amount is taken after paying dividends to the shareholders and drawings by owners.

The management of cited firm can adopt this source as it does not carry fixed burden of

interest or instalments (Epstein and Buhovac, 2014). Sales of assets: In order to arrange the funds, company can use another source where the

assets are sold and from the same, cash is generated. It may remain helpful for SMR

because it can be useful for both; short and long term.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reduction of working capital: Reduction in working capital can be useful for company

as it can be done by lengthening the working capital cycle. It can assist firm to reduce the

working capital requirement. As a result, amount saved in working capital can be utilised

by the firm for new opening purpose (DRURY, 2013).

EXTERNAL SOURCES Bank loan: It is an external source of finance where the amount is taken from financial

institution. Over the loan amount, person needs to pay a fixed amount of interest. In order

to gain funds, cited firm can take loan from the bank. It will assist company to gain

amount at specific rate of interest. Angel investors: Angel investors are the one who offer funds to start-up firms in

exchange of convertible debt or equity shares issued by company. These investors pay

amount up to the limit of $500000. They are not interested in the monetary returns from

organization but they want share in stake of company (Drechsler and Natter, 2012). Venture capital: Venture capitalist is the one who is interested in offering funds to the

entrepreneur who has innovative business ideas but no money to implement the same. In

addition to it, they take part in the profits of company.

Shares: It is a part of share capital of the firm. An organization issues shares to the public

and in return, they require paying dividend. It dilutes the ownership of company and take

part in the decision making process of cited firm (Chazi, Terra and Zanella, 2010).

However, the shareholder are the real owners of the company where an essential role is

being paid by them. They are interested in the dividends of the firm and they take part in

the annual general meetings of the organization.

1.2

Management of SMR requires understanding the pros and cons of all sources which it

uses. It can provide assistance to the cited firm to take requisite decisions regarding appropriate

source. The same is given as below. Retained earnings: The cited firm may get benefit of this source as it does not carry any

rate of interest. It is the process of ploughing back amount of firm (Broadbent and Cullen,

2012). So, it can be useful for the stated firm. On the other side, disadvantage of same is

that it may be a limited amount which cannot fulfil the needs of company. In addition to

it, amount of retained earnings can be taken after paying dividends and taxes where a

2

as it can be done by lengthening the working capital cycle. It can assist firm to reduce the

working capital requirement. As a result, amount saved in working capital can be utilised

by the firm for new opening purpose (DRURY, 2013).

EXTERNAL SOURCES Bank loan: It is an external source of finance where the amount is taken from financial

institution. Over the loan amount, person needs to pay a fixed amount of interest. In order

to gain funds, cited firm can take loan from the bank. It will assist company to gain

amount at specific rate of interest. Angel investors: Angel investors are the one who offer funds to start-up firms in

exchange of convertible debt or equity shares issued by company. These investors pay

amount up to the limit of $500000. They are not interested in the monetary returns from

organization but they want share in stake of company (Drechsler and Natter, 2012). Venture capital: Venture capitalist is the one who is interested in offering funds to the

entrepreneur who has innovative business ideas but no money to implement the same. In

addition to it, they take part in the profits of company.

Shares: It is a part of share capital of the firm. An organization issues shares to the public

and in return, they require paying dividend. It dilutes the ownership of company and take

part in the decision making process of cited firm (Chazi, Terra and Zanella, 2010).

However, the shareholder are the real owners of the company where an essential role is

being paid by them. They are interested in the dividends of the firm and they take part in

the annual general meetings of the organization.

1.2

Management of SMR requires understanding the pros and cons of all sources which it

uses. It can provide assistance to the cited firm to take requisite decisions regarding appropriate

source. The same is given as below. Retained earnings: The cited firm may get benefit of this source as it does not carry any

rate of interest. It is the process of ploughing back amount of firm (Broadbent and Cullen,

2012). So, it can be useful for the stated firm. On the other side, disadvantage of same is

that it may be a limited amount which cannot fulfil the needs of company. In addition to

it, amount of retained earnings can be taken after paying dividends and taxes where a

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

situation may arise where the firm requires paying high taxes. It can result into

decreasing amount which leads to affect the financial availability (Brigham, E. F. and

Houston, 2012). Sale of assets: The major pros and cons of this source is that company may get finance

without extra borrowings of money. In context to it, the sold assets can be aback by

company whenever it is needed. However, major disadvantage is loss of assets against

money. Bank loan: The major advantage of borrowing from banks is that the cited firm requires

paying fixed amount of interest as it is generally fixed over specific period. Apart from

that, management of SMR needs to provide collateral securities against the loan amount.

Venture capital: Benefit of this source is that the investors want to contribute in running

business. However, limitation of the stated source is that investors are interested in small

percentage of ownership of company (Ahmed, 2010).

1.3

On the basis of above analysis, appropriate sources of funds for company are mentioned

further. However, using these funds can lower down the cost of new business from which

company can increase its initial returns. Furthermore, appropriate funds are stated as below.

Bank loan: The cited firm can use borrowings from bank in order to open a new

business. It may remain fruitful for organization because fix rate of interest is paid by the

firm. Along with that, it leads to manage the financial resources of company along with

identifying the areas where further amount needs to be invested (The Importance of the

Cash Flow Statement. 2016). Shares: Company can adopt this source because at initial level, organization is not

required to pay good amount of dividend to the shareholders. It can assist the firm to

collect and save a good amount of money by issuing shares.

Retained earnings: As per the stated case study, the management of SMR wants to open

new branches at different places. However, it can cost the company so that cited firm

should adopt the source which can lower the cost at initial level. The firm can use

retained earnings so that any rate of interest is not necessarily be paid by the firm (Li,

2016).

3

decreasing amount which leads to affect the financial availability (Brigham, E. F. and

Houston, 2012). Sale of assets: The major pros and cons of this source is that company may get finance

without extra borrowings of money. In context to it, the sold assets can be aback by

company whenever it is needed. However, major disadvantage is loss of assets against

money. Bank loan: The major advantage of borrowing from banks is that the cited firm requires

paying fixed amount of interest as it is generally fixed over specific period. Apart from

that, management of SMR needs to provide collateral securities against the loan amount.

Venture capital: Benefit of this source is that the investors want to contribute in running

business. However, limitation of the stated source is that investors are interested in small

percentage of ownership of company (Ahmed, 2010).

1.3

On the basis of above analysis, appropriate sources of funds for company are mentioned

further. However, using these funds can lower down the cost of new business from which

company can increase its initial returns. Furthermore, appropriate funds are stated as below.

Bank loan: The cited firm can use borrowings from bank in order to open a new

business. It may remain fruitful for organization because fix rate of interest is paid by the

firm. Along with that, it leads to manage the financial resources of company along with

identifying the areas where further amount needs to be invested (The Importance of the

Cash Flow Statement. 2016). Shares: Company can adopt this source because at initial level, organization is not

required to pay good amount of dividend to the shareholders. It can assist the firm to

collect and save a good amount of money by issuing shares.

Retained earnings: As per the stated case study, the management of SMR wants to open

new branches at different places. However, it can cost the company so that cited firm

should adopt the source which can lower the cost at initial level. The firm can use

retained earnings so that any rate of interest is not necessarily be paid by the firm (Li,

2016).

3

On the basis of above comparison, the cited company can use these sources because with the

adoption of this company can save cost at initial level. It can ultimately assist the firm to invet

more money at initial level in required areas.

TASK 2

2.1

In order to analyse the cost of sources of finance, the management of the cited firm has

adopted three sources. All these sources can cost the company in some or other way. At the time

of borrowing from banks the firm needs to adopt the requisite process that is necessarily be

followed while taking loan (Viviers and Cohen, 2011). The process of loan is also lengthy and

generally it is seen that the bank offer funds after analysing the financial performance. In

addition to it, the interest paid by the company can be termed as financial cost. It is crucial for

the firm to pay monthly interest against the loan amount. On other side, while issuing shares the

company needs to issue prospectus which can increase cost. In addition to it, the company also

needs to pay dividend to the shareholders which can termed as a financial cost.

The management of cited firm can also use retained earning which can cost to for the

equity. But in general way it does not incur any cost as the amount is taken from the personal

earnings (Siano, Kitchen and Confetto, 2010).

2.2

Financial planning is the most important process that is required to be done by the

management of SMR. The company is going to open its new branches where the firm needs to

focus on planning the financial resources in a way that the saved amount can be used and

invested for further investments. There are some reasons stated below which will define the

importance of financial planning for the SMR.

Appropriate capital structure: In order to manage funds, various sources can be adopted by the

company. However, the company requires planning financial resources so that the management

can contribute in different areas. It leads to form an appropriate capital structure of the company.

Investment decisions: With the hep of effective financial planning, the cited firm will be able to

identify the areas that where investments can be done. The financial department of the firm will

be able to analyse the different investment proposal (Ojha, Gianiodis and Manuj, 2013).

Aids in operational activities: in order to analyse the success of production and distribution

functions of organization, it is essential to ensure the smooth flow of financial decisions. Because

4

adoption of this company can save cost at initial level. It can ultimately assist the firm to invet

more money at initial level in required areas.

TASK 2

2.1

In order to analyse the cost of sources of finance, the management of the cited firm has

adopted three sources. All these sources can cost the company in some or other way. At the time

of borrowing from banks the firm needs to adopt the requisite process that is necessarily be

followed while taking loan (Viviers and Cohen, 2011). The process of loan is also lengthy and

generally it is seen that the bank offer funds after analysing the financial performance. In

addition to it, the interest paid by the company can be termed as financial cost. It is crucial for

the firm to pay monthly interest against the loan amount. On other side, while issuing shares the

company needs to issue prospectus which can increase cost. In addition to it, the company also

needs to pay dividend to the shareholders which can termed as a financial cost.

The management of cited firm can also use retained earning which can cost to for the

equity. But in general way it does not incur any cost as the amount is taken from the personal

earnings (Siano, Kitchen and Confetto, 2010).

2.2

Financial planning is the most important process that is required to be done by the

management of SMR. The company is going to open its new branches where the firm needs to

focus on planning the financial resources in a way that the saved amount can be used and

invested for further investments. There are some reasons stated below which will define the

importance of financial planning for the SMR.

Appropriate capital structure: In order to manage funds, various sources can be adopted by the

company. However, the company requires planning financial resources so that the management

can contribute in different areas. It leads to form an appropriate capital structure of the company.

Investment decisions: With the hep of effective financial planning, the cited firm will be able to

identify the areas that where investments can be done. The financial department of the firm will

be able to analyse the different investment proposal (Ojha, Gianiodis and Manuj, 2013).

Aids in operational activities: in order to analyse the success of production and distribution

functions of organization, it is essential to ensure the smooth flow of financial decisions. Because

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

finance offered to operate these function is done with the help of financial planning. With the

consideration of same, the company needs to done financial planning.

Helps in optimum utilisation of finance: Finance is the most important tool that is required to

operate a business. However, financial planning is an integral process which can provide an

assistance to the company. It can help the company to make proper analysis of the funds.

To overcome future issues: With the help of effective financial planning, the cited firm can

analyse the areas that are needed to be solved in the future (Nga and Yien, 2013). It can help the

company to save and use the resources effectively. As a result, the company can save and invest

the amount for future needs.

2.3

There are different decision makers who access the information of Financial information

of the cited firm. It can be utilized by both the decision makers such as internal and external.

Requisite data and piece of information is used for different purposes. Various decision makers

are given below.

Bank loan: The creditworthiness of the organization can be better analysed with the help of

financial statements of the company. The cited information assist the organization to take

decision whether the bank should offer loan to the firm or not. In order to offer the same, the

company can be useful to analyse the position of the company. With the use of same the

financial institutions offer loan to the company who are able to manage financial resources

(Nelson, 2012).

Shareholders: Cash flow statements are remained useful for the shareholders of the company. It

assists the shareholders to analyse the inflow and outflow of cash. Profit and loss a/c

performance can be identified. In addition to it, the requisite decisions are interpreted by the

shareholders by considering the profitability statement of the SMR. With the use of this

statement, the shareholders of the firm will be able to take investment decisions (Murphy and

Yetmar, 2010).

Government: They required information to check whether the company have compiled with all

the rules and regulations of the government. Apart from this, proper assessment of tax is being

analysed by the government.

Employees: The requirement of information to the employees is remained useful in assessing the

profitability. This is done with a motive to manage the company affairs. For making business

5

consideration of same, the company needs to done financial planning.

Helps in optimum utilisation of finance: Finance is the most important tool that is required to

operate a business. However, financial planning is an integral process which can provide an

assistance to the company. It can help the company to make proper analysis of the funds.

To overcome future issues: With the help of effective financial planning, the cited firm can

analyse the areas that are needed to be solved in the future (Nga and Yien, 2013). It can help the

company to save and use the resources effectively. As a result, the company can save and invest

the amount for future needs.

2.3

There are different decision makers who access the information of Financial information

of the cited firm. It can be utilized by both the decision makers such as internal and external.

Requisite data and piece of information is used for different purposes. Various decision makers

are given below.

Bank loan: The creditworthiness of the organization can be better analysed with the help of

financial statements of the company. The cited information assist the organization to take

decision whether the bank should offer loan to the firm or not. In order to offer the same, the

company can be useful to analyse the position of the company. With the use of same the

financial institutions offer loan to the company who are able to manage financial resources

(Nelson, 2012).

Shareholders: Cash flow statements are remained useful for the shareholders of the company. It

assists the shareholders to analyse the inflow and outflow of cash. Profit and loss a/c

performance can be identified. In addition to it, the requisite decisions are interpreted by the

shareholders by considering the profitability statement of the SMR. With the use of this

statement, the shareholders of the firm will be able to take investment decisions (Murphy and

Yetmar, 2010).

Government: They required information to check whether the company have compiled with all

the rules and regulations of the government. Apart from this, proper assessment of tax is being

analysed by the government.

Employees: The requirement of information to the employees is remained useful in assessing the

profitability. This is done with a motive to manage the company affairs. For making business

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decision information like financial performance and position is required by the employees (Melo,

2012). The subordinates are majority interested in the information related with the salary and

bonus. However, all the stakeholder of the company needs to access the financial information at

different level. With the help of this, investment decision are taken. In addition to it, the

company has to deliver the in a way that the motives of the stakeholders can be attained (Keller,

2013).

2.4

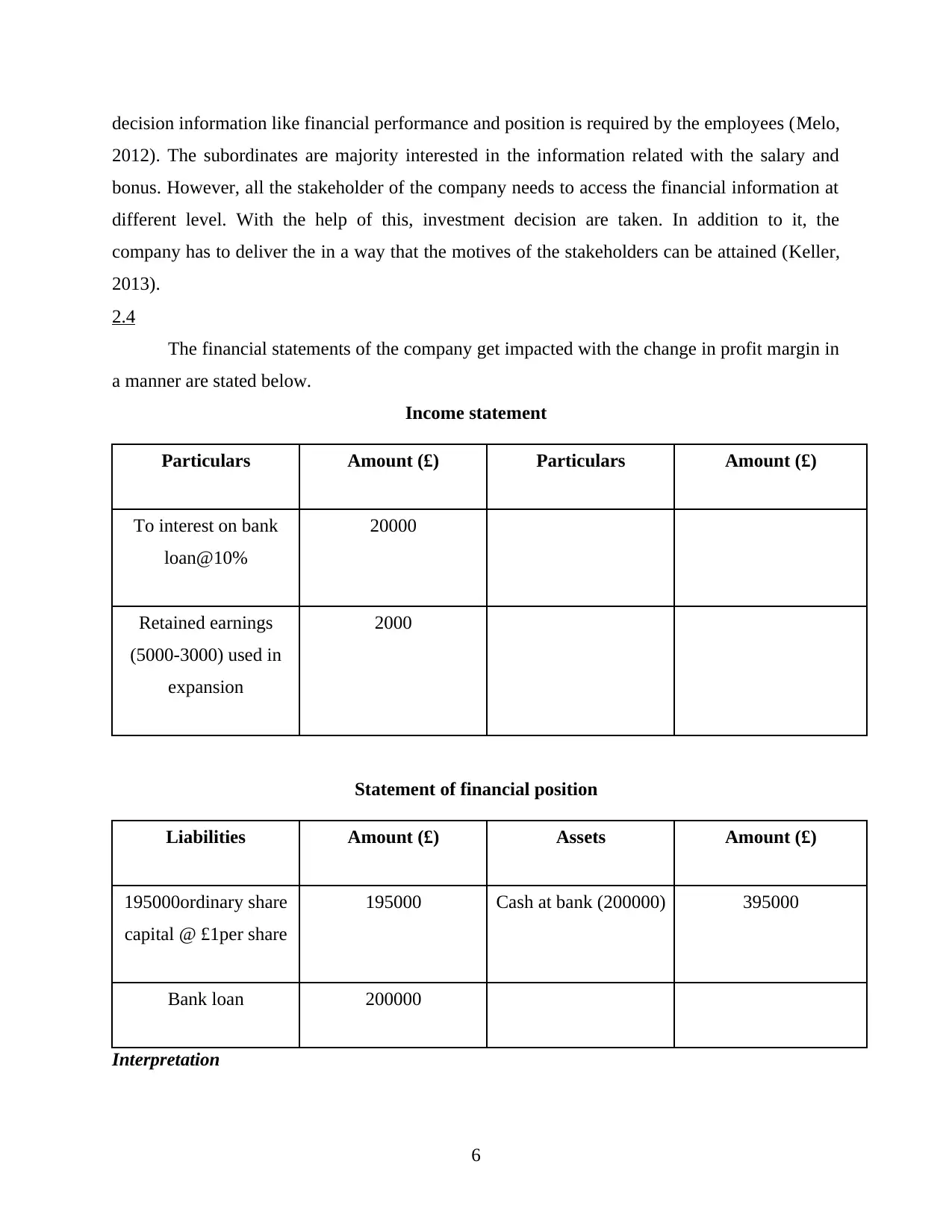

The financial statements of the company get impacted with the change in profit margin in

a manner are stated below.

Income statement

Particulars Amount (£) Particulars Amount (£)

To interest on bank

loan@10%

20000

Retained earnings

(5000-3000) used in

expansion

2000

Statement of financial position

Liabilities Amount (£) Assets Amount (£)

195000ordinary share

capital @ £1per share

195000 Cash at bank (200000) 395000

Bank loan 200000

Interpretation

6

2012). The subordinates are majority interested in the information related with the salary and

bonus. However, all the stakeholder of the company needs to access the financial information at

different level. With the help of this, investment decision are taken. In addition to it, the

company has to deliver the in a way that the motives of the stakeholders can be attained (Keller,

2013).

2.4

The financial statements of the company get impacted with the change in profit margin in

a manner are stated below.

Income statement

Particulars Amount (£) Particulars Amount (£)

To interest on bank

loan@10%

20000

Retained earnings

(5000-3000) used in

expansion

2000

Statement of financial position

Liabilities Amount (£) Assets Amount (£)

195000ordinary share

capital @ £1per share

195000 Cash at bank (200000) 395000

Bank loan 200000

Interpretation

6

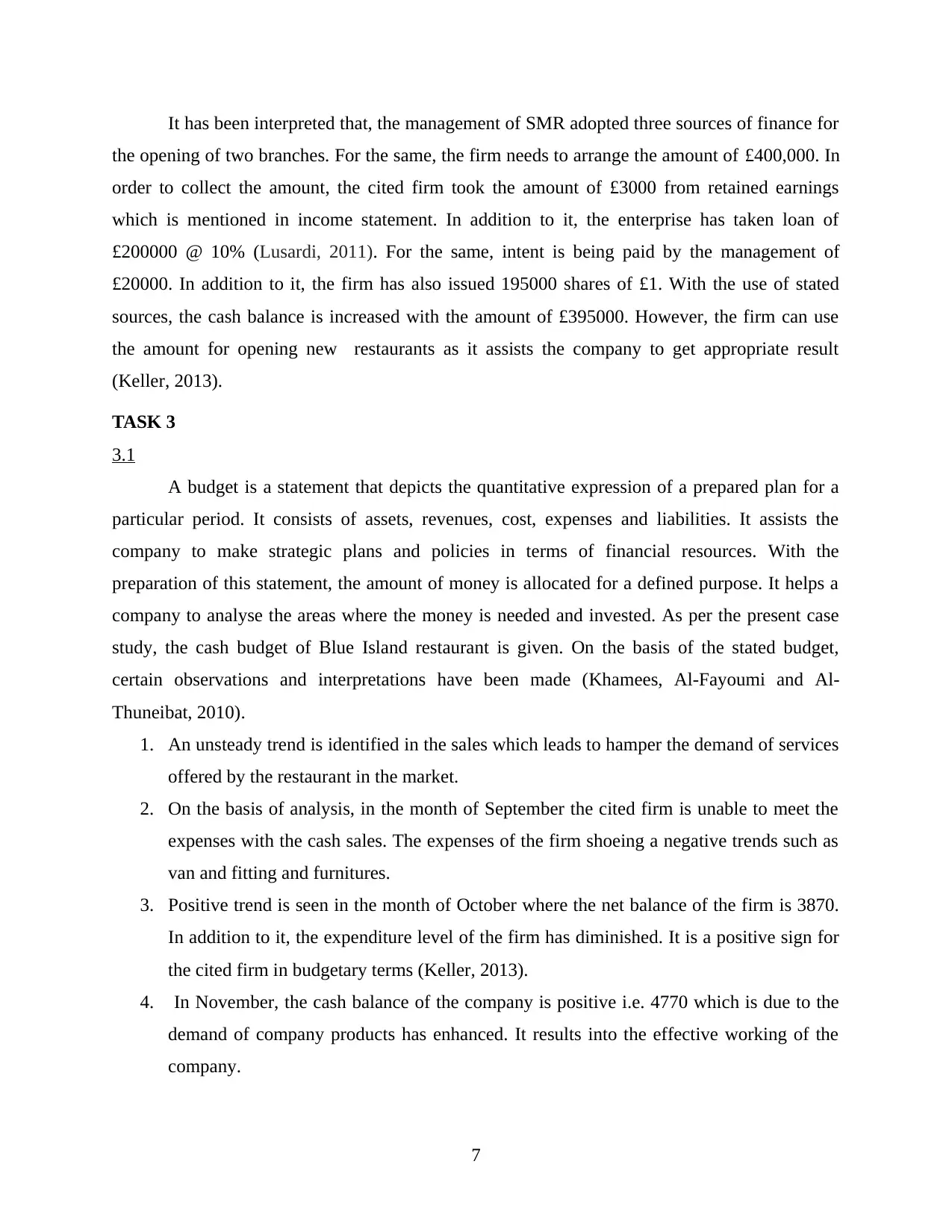

It has been interpreted that, the management of SMR adopted three sources of finance for

the opening of two branches. For the same, the firm needs to arrange the amount of £400,000. In

order to collect the amount, the cited firm took the amount of £3000 from retained earnings

which is mentioned in income statement. In addition to it, the enterprise has taken loan of

£200000 @ 10% (Lusardi, 2011). For the same, intent is being paid by the management of

£20000. In addition to it, the firm has also issued 195000 shares of £1. With the use of stated

sources, the cash balance is increased with the amount of £395000. However, the firm can use

the amount for opening new restaurants as it assists the company to get appropriate result

(Keller, 2013).

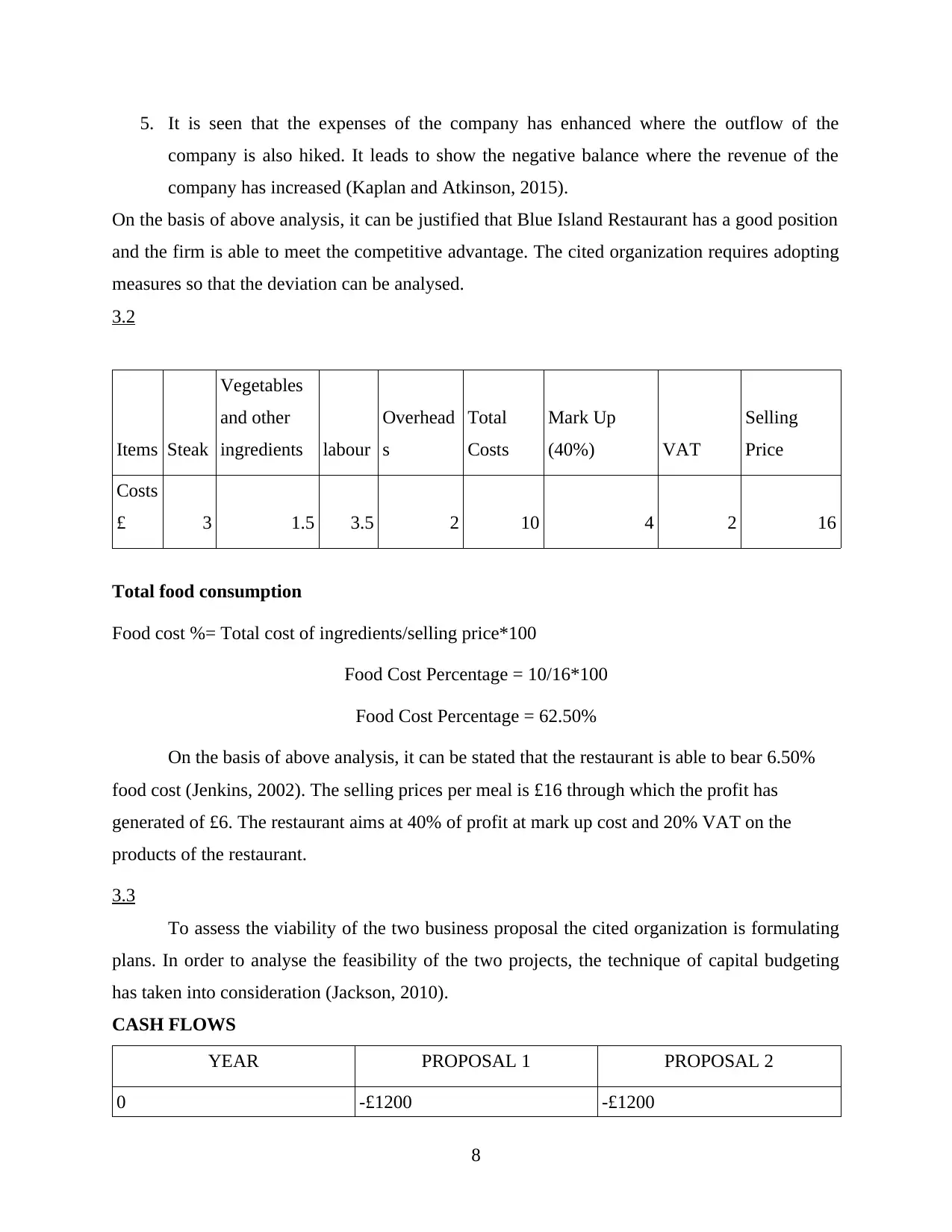

TASK 3

3.1

A budget is a statement that depicts the quantitative expression of a prepared plan for a

particular period. It consists of assets, revenues, cost, expenses and liabilities. It assists the

company to make strategic plans and policies in terms of financial resources. With the

preparation of this statement, the amount of money is allocated for a defined purpose. It helps a

company to analyse the areas where the money is needed and invested. As per the present case

study, the cash budget of Blue Island restaurant is given. On the basis of the stated budget,

certain observations and interpretations have been made (Khamees, Al-Fayoumi and Al-

Thuneibat, 2010).

1. An unsteady trend is identified in the sales which leads to hamper the demand of services

offered by the restaurant in the market.

2. On the basis of analysis, in the month of September the cited firm is unable to meet the

expenses with the cash sales. The expenses of the firm shoeing a negative trends such as

van and fitting and furnitures.

3. Positive trend is seen in the month of October where the net balance of the firm is 3870.

In addition to it, the expenditure level of the firm has diminished. It is a positive sign for

the cited firm in budgetary terms (Keller, 2013).

4. In November, the cash balance of the company is positive i.e. 4770 which is due to the

demand of company products has enhanced. It results into the effective working of the

company.

7

the opening of two branches. For the same, the firm needs to arrange the amount of £400,000. In

order to collect the amount, the cited firm took the amount of £3000 from retained earnings

which is mentioned in income statement. In addition to it, the enterprise has taken loan of

£200000 @ 10% (Lusardi, 2011). For the same, intent is being paid by the management of

£20000. In addition to it, the firm has also issued 195000 shares of £1. With the use of stated

sources, the cash balance is increased with the amount of £395000. However, the firm can use

the amount for opening new restaurants as it assists the company to get appropriate result

(Keller, 2013).

TASK 3

3.1

A budget is a statement that depicts the quantitative expression of a prepared plan for a

particular period. It consists of assets, revenues, cost, expenses and liabilities. It assists the

company to make strategic plans and policies in terms of financial resources. With the

preparation of this statement, the amount of money is allocated for a defined purpose. It helps a

company to analyse the areas where the money is needed and invested. As per the present case

study, the cash budget of Blue Island restaurant is given. On the basis of the stated budget,

certain observations and interpretations have been made (Khamees, Al-Fayoumi and Al-

Thuneibat, 2010).

1. An unsteady trend is identified in the sales which leads to hamper the demand of services

offered by the restaurant in the market.

2. On the basis of analysis, in the month of September the cited firm is unable to meet the

expenses with the cash sales. The expenses of the firm shoeing a negative trends such as

van and fitting and furnitures.

3. Positive trend is seen in the month of October where the net balance of the firm is 3870.

In addition to it, the expenditure level of the firm has diminished. It is a positive sign for

the cited firm in budgetary terms (Keller, 2013).

4. In November, the cash balance of the company is positive i.e. 4770 which is due to the

demand of company products has enhanced. It results into the effective working of the

company.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5. It is seen that the expenses of the company has enhanced where the outflow of the

company is also hiked. It leads to show the negative balance where the revenue of the

company has increased (Kaplan and Atkinson, 2015).

On the basis of above analysis, it can be justified that Blue Island Restaurant has a good position

and the firm is able to meet the competitive advantage. The cited organization requires adopting

measures so that the deviation can be analysed.

3.2

Items Steak

Vegetables

and other

ingredients labour

Overhead

s

Total

Costs

Mark Up

(40%) VAT

Selling

Price

Costs

£ 3 1.5 3.5 2 10 4 2 16

Total food consumption

Food cost %= Total cost of ingredients/selling price*100

Food Cost Percentage = 10/16*100

Food Cost Percentage = 62.50%

On the basis of above analysis, it can be stated that the restaurant is able to bear 6.50%

food cost (Jenkins, 2002). The selling prices per meal is £16 through which the profit has

generated of £6. The restaurant aims at 40% of profit at mark up cost and 20% VAT on the

products of the restaurant.

3.3

To assess the viability of the two business proposal the cited organization is formulating

plans. In order to analyse the feasibility of the two projects, the technique of capital budgeting

has taken into consideration (Jackson, 2010).

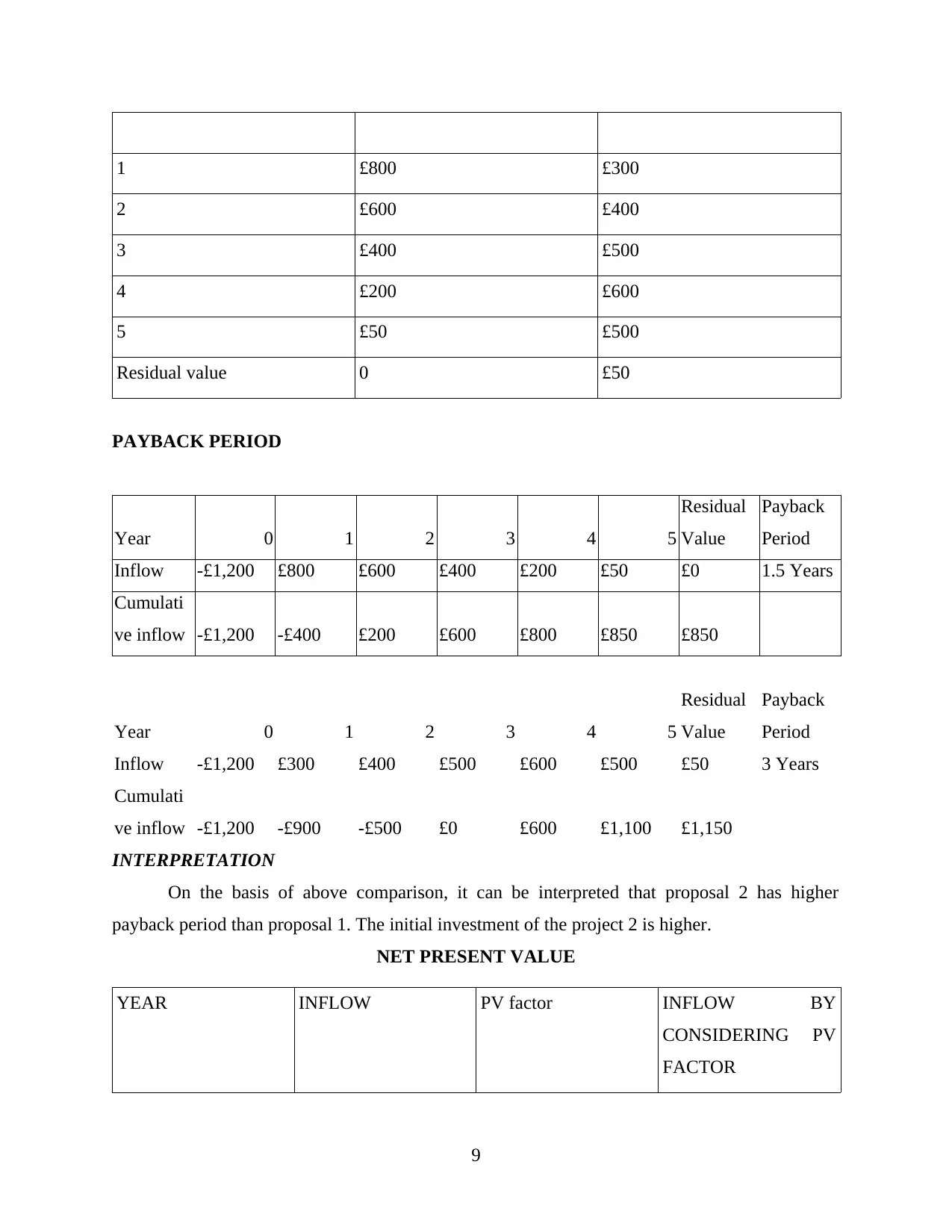

CASH FLOWS

YEAR PROPOSAL 1 PROPOSAL 2

0 -£1200 -£1200

8

company is also hiked. It leads to show the negative balance where the revenue of the

company has increased (Kaplan and Atkinson, 2015).

On the basis of above analysis, it can be justified that Blue Island Restaurant has a good position

and the firm is able to meet the competitive advantage. The cited organization requires adopting

measures so that the deviation can be analysed.

3.2

Items Steak

Vegetables

and other

ingredients labour

Overhead

s

Total

Costs

Mark Up

(40%) VAT

Selling

Price

Costs

£ 3 1.5 3.5 2 10 4 2 16

Total food consumption

Food cost %= Total cost of ingredients/selling price*100

Food Cost Percentage = 10/16*100

Food Cost Percentage = 62.50%

On the basis of above analysis, it can be stated that the restaurant is able to bear 6.50%

food cost (Jenkins, 2002). The selling prices per meal is £16 through which the profit has

generated of £6. The restaurant aims at 40% of profit at mark up cost and 20% VAT on the

products of the restaurant.

3.3

To assess the viability of the two business proposal the cited organization is formulating

plans. In order to analyse the feasibility of the two projects, the technique of capital budgeting

has taken into consideration (Jackson, 2010).

CASH FLOWS

YEAR PROPOSAL 1 PROPOSAL 2

0 -£1200 -£1200

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 £800 £300

2 £600 £400

3 £400 £500

4 £200 £600

5 £50 £500

Residual value 0 £50

PAYBACK PERIOD

Year 0 1 2 3 4 5

Residual

Value

Payback

Period

Inflow -£1,200 £800 £600 £400 £200 £50 £0 1.5 Years

Cumulati

ve inflow -£1,200 -£400 £200 £600 £800 £850 £850

Year 0 1 2 3 4 5

Residual

Value

Payback

Period

Inflow -£1,200 £300 £400 £500 £600 £500 £50 3 Years

Cumulati

ve inflow -£1,200 -£900 -£500 £0 £600 £1,100 £1,150

INTERPRETATION

On the basis of above comparison, it can be interpreted that proposal 2 has higher

payback period than proposal 1. The initial investment of the project 2 is higher.

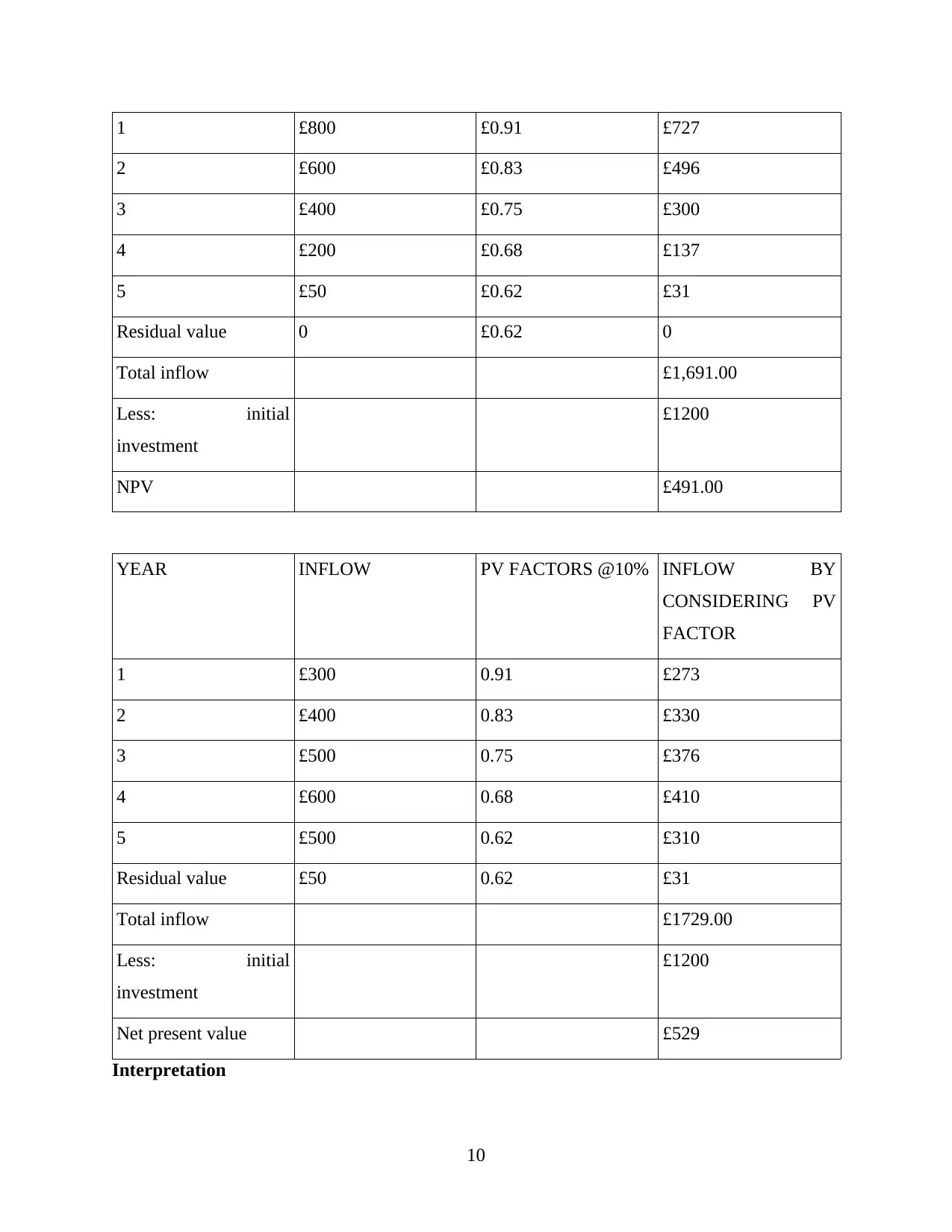

NET PRESENT VALUE

YEAR INFLOW PV factor INFLOW BY

CONSIDERING PV

FACTOR

9

2 £600 £400

3 £400 £500

4 £200 £600

5 £50 £500

Residual value 0 £50

PAYBACK PERIOD

Year 0 1 2 3 4 5

Residual

Value

Payback

Period

Inflow -£1,200 £800 £600 £400 £200 £50 £0 1.5 Years

Cumulati

ve inflow -£1,200 -£400 £200 £600 £800 £850 £850

Year 0 1 2 3 4 5

Residual

Value

Payback

Period

Inflow -£1,200 £300 £400 £500 £600 £500 £50 3 Years

Cumulati

ve inflow -£1,200 -£900 -£500 £0 £600 £1,100 £1,150

INTERPRETATION

On the basis of above comparison, it can be interpreted that proposal 2 has higher

payback period than proposal 1. The initial investment of the project 2 is higher.

NET PRESENT VALUE

YEAR INFLOW PV factor INFLOW BY

CONSIDERING PV

FACTOR

9

1 £800 £0.91 £727

2 £600 £0.83 £496

3 £400 £0.75 £300

4 £200 £0.68 £137

5 £50 £0.62 £31

Residual value 0 £0.62 0

Total inflow £1,691.00

Less: initial

investment

£1200

NPV £491.00

YEAR INFLOW PV FACTORS @10% INFLOW BY

CONSIDERING PV

FACTOR

1 £300 0.91 £273

2 £400 0.83 £330

3 £500 0.75 £376

4 £600 0.68 £410

5 £500 0.62 £310

Residual value £50 0.62 £31

Total inflow £1729.00

Less: initial

investment

£1200

Net present value £529

Interpretation

10

2 £600 £0.83 £496

3 £400 £0.75 £300

4 £200 £0.68 £137

5 £50 £0.62 £31

Residual value 0 £0.62 0

Total inflow £1,691.00

Less: initial

investment

£1200

NPV £491.00

YEAR INFLOW PV FACTORS @10% INFLOW BY

CONSIDERING PV

FACTOR

1 £300 0.91 £273

2 £400 0.83 £330

3 £500 0.75 £376

4 £600 0.68 £410

5 £500 0.62 £310

Residual value £50 0.62 £31

Total inflow £1729.00

Less: initial

investment

£1200

Net present value £529

Interpretation

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.