Swinburne University: ACC30005 Taxation Law Letter of Advice

VerifiedAdded on 2023/01/03

|11

|2593

|89

Report

AI Summary

This report is a taxation law letter of advice prepared for a business partnership, addressing key taxation issues. It analyzes the partners' income, including cash receipts and bonus amounts, determining whether they constitute ordinary income subject to taxation. The report examines various expenses, such as legal costs, bad debts, depreciation of assets, car running expenses, and travel expenses, to determine their deductibility under relevant tax legislation. It also considers the tax implications of partner salaries and the calculation of the partnership's net income, providing a detailed computation of the assessable income, allowable deductions, and the final distribution of income to each partner. The report references relevant case law and legislation to support its conclusions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Private and Confidential: Letter of Advice................................................................................2

References:...............................................................................................................................10

Table of Contents

Private and Confidential: Letter of Advice................................................................................2

References:...............................................................................................................................10

2TAXATION LAW

Private and Confidential: Letter of Advice

To Joe and Mary

From: ABC Tax Consultants

Date: 10th May 2019

Dear Jack

Scope:

The scope of this letter is to provide to the company and partners regarding their net

income from partnership, payments and distribution from partnership. The letter also attaches

the net income calculated from the partnership and the amount of net earnings from

partnership are attributable to the partners. The letter also summarises the opinion in relation

to each of the matters outlined below. The advisers strongly encourage the readers to read the

discussion in respect of the advice given.

Issues:

a) Whether the cash receipts from the business amounts to the normal proceeds of the

partnership business and taxable within the ordinary course of business?

b) Whether the expenses incurred by partnership is eligible for deduction under the

general provision of “section 8-1, ITAA 1997”?

c) Are the taxpayers allowed to claim deduction for the expenses occurred as repairs

under the “section 25-10, ITAA 1997”?

Rule:

As explained under the “division 5 of the ITAA 1936” partnership is not regarded as

the separate legal entity under the general law and the partnership is not required to pay tax

Private and Confidential: Letter of Advice

To Joe and Mary

From: ABC Tax Consultants

Date: 10th May 2019

Dear Jack

Scope:

The scope of this letter is to provide to the company and partners regarding their net

income from partnership, payments and distribution from partnership. The letter also attaches

the net income calculated from the partnership and the amount of net earnings from

partnership are attributable to the partners. The letter also summarises the opinion in relation

to each of the matters outlined below. The advisers strongly encourage the readers to read the

discussion in respect of the advice given.

Issues:

a) Whether the cash receipts from the business amounts to the normal proceeds of the

partnership business and taxable within the ordinary course of business?

b) Whether the expenses incurred by partnership is eligible for deduction under the

general provision of “section 8-1, ITAA 1997”?

c) Are the taxpayers allowed to claim deduction for the expenses occurred as repairs

under the “section 25-10, ITAA 1997”?

Rule:

As explained under the “division 5 of the ITAA 1936” partnership is not regarded as

the separate legal entity under the general law and the partnership is not required to pay tax

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

(Barkoczy 2016). It is partners that pay tax on the profits that is distributed through the

partnership.

Characterising the receipts as the ordinary income from the business comprises of the

two step procedure. This includes deciding whether the taxpayer is carrying the business or

the ascertaining whether the receipts are regarded as the usual incomes of the business

activity. As per the “section 6-5, ITAA 1997” usually most of the income that is received by

the taxpayer is treated as ordinary income (Freudenberg et al. 2017). The law court in the

case of “Scott v CT (1935)” held that the word income must not be regarded as the term of

art and there should be essential use of principles to treat the earnings as ordinary income

under the ordinary conceptions and use of mankind (Morgan and Castelyn 2018). A gain that

rises from the act done in carrying the activities of business or derived from carrying out the

isolated business scheme possess the nature of revenue. As held in “Hochestrasser v Mayes

(1960)” tin order to possess the nature of income the item should be gain for the taxpayer.

As explained in “section 8-1, ITAA 1997” there are two positive limbs where the

taxpayer can claim deduction. This indicates that the taxpayer is entitled to deduction for

expenses that is occurred in gaining or producing the assessable earnings. It also includes

expenses that is necessarily occurred in carrying the business for the purpose of earning

assessable income (Morgan, Mortimer and Pinto 2018). The court in “Hallstorms Pty Ltd v

FCT (1997)” stated that to determine whether the legal expenses are allowed for deduction

under “section 8-1, ITAA 1997” it is necessary to consider the nature of legal expenses.

The taxpayers or business are only permitted to claim deduction for bad debts when

the debts become bad or it has been written off under “section 63”. No deduction for bad

debt is permitted to the taxpayer relating to provision for bad debt (Robin and Barkoczy

2019). On the other hand, the capital allowance regimes under “section 40-25 (1)” allows an

(Barkoczy 2016). It is partners that pay tax on the profits that is distributed through the

partnership.

Characterising the receipts as the ordinary income from the business comprises of the

two step procedure. This includes deciding whether the taxpayer is carrying the business or

the ascertaining whether the receipts are regarded as the usual incomes of the business

activity. As per the “section 6-5, ITAA 1997” usually most of the income that is received by

the taxpayer is treated as ordinary income (Freudenberg et al. 2017). The law court in the

case of “Scott v CT (1935)” held that the word income must not be regarded as the term of

art and there should be essential use of principles to treat the earnings as ordinary income

under the ordinary conceptions and use of mankind (Morgan and Castelyn 2018). A gain that

rises from the act done in carrying the activities of business or derived from carrying out the

isolated business scheme possess the nature of revenue. As held in “Hochestrasser v Mayes

(1960)” tin order to possess the nature of income the item should be gain for the taxpayer.

As explained in “section 8-1, ITAA 1997” there are two positive limbs where the

taxpayer can claim deduction. This indicates that the taxpayer is entitled to deduction for

expenses that is occurred in gaining or producing the assessable earnings. It also includes

expenses that is necessarily occurred in carrying the business for the purpose of earning

assessable income (Morgan, Mortimer and Pinto 2018). The court in “Hallstorms Pty Ltd v

FCT (1997)” stated that to determine whether the legal expenses are allowed for deduction

under “section 8-1, ITAA 1997” it is necessary to consider the nature of legal expenses.

The taxpayers or business are only permitted to claim deduction for bad debts when

the debts become bad or it has been written off under “section 63”. No deduction for bad

debt is permitted to the taxpayer relating to provision for bad debt (Robin and Barkoczy

2019). On the other hand, the capital allowance regimes under “section 40-25 (1)” allows an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

entity to claim deduction for the sum that is equivalent to the decline in the value of the

depreciating asset which is held during the year.

A loss or outgoings is only allowed for deductions up to the degree that it is occurred

in gaining assessable earnings. The taxpayers are required to apportion the expenses that are

having dual purpose. As held in “Ronpibon Tin No Liability v FCT (1949)” it is necessary to

allocate the expenditure that has dual purpose (Robin 2019). In other words, the expenses

must be segregated between work and personal purpose and deduction is only allowed for

work purpose expenses.

The “taxation ruling of TR 97/23” explains that deduction for expenses occurred by

taxpayer for repair is allowed for deduction under the “section 25-10, ITAA 1997”. “Section

25-10, ITAA 1997” explains repairs as work done on the machinery, plant, tools or articles to

make good of defects (Sadiq 2019). It only involves the reinstatement of the effective

function of the asset that is being repaired without instigating any change in the character of

asset. The court in “Western Suburbs Cinemas Ltd v FCT (1952)” denied the taxpayer

deduction for new ceiling which was enhancement to the fixed asset and the cost should be

treated as capital in nature.

Repairs to new premises that is initial repair are considered as capital in nature. The

court in “W Thomas & Co Pty Ltd v FCT (1965)” held that cost incurred in repairing the

roof, glittering basement floor and painting the building following the acquisition was

considered as capital outlay and not permitted for deduction under “section 25-10, ITAA

1997”.

Expenses incurred by taxpayers in travelling for business purpose are allowed as

deductible expenditure. The taxpayers are required to keep record of their travel expenses and

should exclude any portion of the expenses that are incurred for the private purpose.

entity to claim deduction for the sum that is equivalent to the decline in the value of the

depreciating asset which is held during the year.

A loss or outgoings is only allowed for deductions up to the degree that it is occurred

in gaining assessable earnings. The taxpayers are required to apportion the expenses that are

having dual purpose. As held in “Ronpibon Tin No Liability v FCT (1949)” it is necessary to

allocate the expenditure that has dual purpose (Robin 2019). In other words, the expenses

must be segregated between work and personal purpose and deduction is only allowed for

work purpose expenses.

The “taxation ruling of TR 97/23” explains that deduction for expenses occurred by

taxpayer for repair is allowed for deduction under the “section 25-10, ITAA 1997”. “Section

25-10, ITAA 1997” explains repairs as work done on the machinery, plant, tools or articles to

make good of defects (Sadiq 2019). It only involves the reinstatement of the effective

function of the asset that is being repaired without instigating any change in the character of

asset. The court in “Western Suburbs Cinemas Ltd v FCT (1952)” denied the taxpayer

deduction for new ceiling which was enhancement to the fixed asset and the cost should be

treated as capital in nature.

Repairs to new premises that is initial repair are considered as capital in nature. The

court in “W Thomas & Co Pty Ltd v FCT (1965)” held that cost incurred in repairing the

roof, glittering basement floor and painting the building following the acquisition was

considered as capital outlay and not permitted for deduction under “section 25-10, ITAA

1997”.

Expenses incurred by taxpayers in travelling for business purpose are allowed as

deductible expenditure. The taxpayers are required to keep record of their travel expenses and

should exclude any portion of the expenses that are incurred for the private purpose.

5TAXATION LAW

Furthermore, expenses incurred by the taxpayer under the “section 8-1, ITAA 1997” for

relocation purpose are not considered deductible (Woellner et al. 2016). The taxpayer in

“Fullertone v FCT (1991)” was denied deduction for travel expenses because the expenses

were not sustained in deriving the taxable earnings.

A partnership is not allowed to enter into the employment contract with the partner.

As held in the case of “Rose v FCT (1951)” a person under the partnership cannot be both

the employer and employee as well (Sadiq 2019). The active partners are usually paid salary

because of the work they do. However, it is not treated as salary rather it is considered as

profits before the balances is shared among the partners. While computing the net income

under the section 90, the partner’s salaries are not considered for deduction purpose.

Application:

In response the rules explained above we look forward to implement the same in your

case. You reported the receipts from customers and sales bonus during the year. The amounts

received by you constitutes ordinary income from the business or the usual profits of the

business activity. Citing the judgement of court in “Scott v CT (1935)” it can be stated that

the cash receipts from business constitutes ordinary earnings under the ordinary concepts of

“section 6-5, ITAA 1997” (Woellner et al. 2016). You also reported bonus amount of

$25,000. The amount constitutes gain that arises from the act that is done in carrying the

activities of business. With reference to decision made in “Hochestrasser v Mayes (1960)”

the bonus is an income and taxable as ordinary earnings under the ordinary concepts of

“section 6-5, ITAA 1997”.

An expenses relating to the legal cost was incurred for successfully opposing the

development. With reference to “Hallstorms Pty Ltd v FCT (1997)” the legal expenditure of

$5000 incurred by the partners is not allowed for deduction because it was incurred by

Furthermore, expenses incurred by the taxpayer under the “section 8-1, ITAA 1997” for

relocation purpose are not considered deductible (Woellner et al. 2016). The taxpayer in

“Fullertone v FCT (1991)” was denied deduction for travel expenses because the expenses

were not sustained in deriving the taxable earnings.

A partnership is not allowed to enter into the employment contract with the partner.

As held in the case of “Rose v FCT (1951)” a person under the partnership cannot be both

the employer and employee as well (Sadiq 2019). The active partners are usually paid salary

because of the work they do. However, it is not treated as salary rather it is considered as

profits before the balances is shared among the partners. While computing the net income

under the section 90, the partner’s salaries are not considered for deduction purpose.

Application:

In response the rules explained above we look forward to implement the same in your

case. You reported the receipts from customers and sales bonus during the year. The amounts

received by you constitutes ordinary income from the business or the usual profits of the

business activity. Citing the judgement of court in “Scott v CT (1935)” it can be stated that

the cash receipts from business constitutes ordinary earnings under the ordinary concepts of

“section 6-5, ITAA 1997” (Woellner et al. 2016). You also reported bonus amount of

$25,000. The amount constitutes gain that arises from the act that is done in carrying the

activities of business. With reference to decision made in “Hochestrasser v Mayes (1960)”

the bonus is an income and taxable as ordinary earnings under the ordinary concepts of

“section 6-5, ITAA 1997”.

An expenses relating to the legal cost was incurred for successfully opposing the

development. With reference to “Hallstorms Pty Ltd v FCT (1997)” the legal expenditure of

$5000 incurred by the partners is not allowed for deduction because it was incurred by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

partners to protect its existing business structure and it is capital in nature (Robin 2019).

While the general legal expenses of $375 is allowed for deduction under “section 8-1, ITAA

1997”.

A provision for doubtful debt of 1.5% of the total sales was made by the Joe and

Mary. It can be stated that the provision for doubtful is non-deductible expenditure. While the

business written off the bad debt of $12,750 during the year. Under section 63, the partners

can claim deduction for the bad debt that were written off during the year.

Several office furniture was bought during 2018/19 for work purpose. With respect to

the capital allowance regimes under “section 40-25 (1)” the partners are permissible to

deduction for the sum that is equivalent to the fall in the value for the income year of the

furniture which is held during the year.

During the year expenses related to cars were reported by Mary and Joe. It is

estimated that around 45% of the running expenses were incurred for business purposes. The

taxpayers here Mary and Joe are required to apportion the running expenses of car as it has

dual purpose. Citing “Ronpibon Tin No Liability v FCT (1949)” deduction of running

expenses is only allowed for business proportion while the remaining portion is non-

deductible.

Initial repairs to the new premises relating to the special cabinets and office set up

were incurred by Joe and Mary for their Bush Furniture business. Setting up the special

cabinet and office furniture constitutes an initial repair which is considered as capital in

nature. Citing the judgement made in “W Thomas & Co Pty Ltd v FCT (1965)” cost incurred

in setting up the special cabinet and office furniture are considered as capital expenditure and

non-deductible under “section 25-10, ITAA 1997”.

partners to protect its existing business structure and it is capital in nature (Robin 2019).

While the general legal expenses of $375 is allowed for deduction under “section 8-1, ITAA

1997”.

A provision for doubtful debt of 1.5% of the total sales was made by the Joe and

Mary. It can be stated that the provision for doubtful is non-deductible expenditure. While the

business written off the bad debt of $12,750 during the year. Under section 63, the partners

can claim deduction for the bad debt that were written off during the year.

Several office furniture was bought during 2018/19 for work purpose. With respect to

the capital allowance regimes under “section 40-25 (1)” the partners are permissible to

deduction for the sum that is equivalent to the fall in the value for the income year of the

furniture which is held during the year.

During the year expenses related to cars were reported by Mary and Joe. It is

estimated that around 45% of the running expenses were incurred for business purposes. The

taxpayers here Mary and Joe are required to apportion the running expenses of car as it has

dual purpose. Citing “Ronpibon Tin No Liability v FCT (1949)” deduction of running

expenses is only allowed for business proportion while the remaining portion is non-

deductible.

Initial repairs to the new premises relating to the special cabinets and office set up

were incurred by Joe and Mary for their Bush Furniture business. Setting up the special

cabinet and office furniture constitutes an initial repair which is considered as capital in

nature. Citing the judgement made in “W Thomas & Co Pty Ltd v FCT (1965)” cost incurred

in setting up the special cabinet and office furniture are considered as capital expenditure and

non-deductible under “section 25-10, ITAA 1997”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

During the year the engine of the delivery van broke down and a new engine was put

into that costed $4,500. Installing a new engine with modified gas power constitute more than

just a normal repair. The new modified gas engine constitute work done of capital in nature.

Citing the decision made in “Western Suburbs Cinemas Ltd v FCT (1952)” the repairs to the

delivery van will be treated as non- deduction repairs under the “section 25-10, ITAA 1997”.

“Section 25-10, ITAA 1997”. It amounts to improvement to the fixed asset and the cost was

capital in nature.

You also reported overseas travel expenditure that was mainly reported for business

purpose. With respect to the guidelines provided by the ATO the travel expenditure that is

occurred for the airfares, accommodation, fares, meals and incidental expenditure are allowed

for deduction under the “section 8-1, ITAA 1997”. This is because the expenditure were

incurred by Joe and Mary is mainly directed towards gaining or producing the assessable

income. Hence it is allowed for deduction.

It is noticed that both Joe and Mary drew a salary of $50,000 each from the

partnership. With respect to decision made in “Rose v FCT (1951)” the salary drawn from

partnership is non-deductible under section 90, because it is considered as profits before the

balances is shared among the Joe and Mary.

The net income from the partnership and the distribution for each partners has been

calculated below;

During the year the engine of the delivery van broke down and a new engine was put

into that costed $4,500. Installing a new engine with modified gas power constitute more than

just a normal repair. The new modified gas engine constitute work done of capital in nature.

Citing the decision made in “Western Suburbs Cinemas Ltd v FCT (1952)” the repairs to the

delivery van will be treated as non- deduction repairs under the “section 25-10, ITAA 1997”.

“Section 25-10, ITAA 1997”. It amounts to improvement to the fixed asset and the cost was

capital in nature.

You also reported overseas travel expenditure that was mainly reported for business

purpose. With respect to the guidelines provided by the ATO the travel expenditure that is

occurred for the airfares, accommodation, fares, meals and incidental expenditure are allowed

for deduction under the “section 8-1, ITAA 1997”. This is because the expenditure were

incurred by Joe and Mary is mainly directed towards gaining or producing the assessable

income. Hence it is allowed for deduction.

It is noticed that both Joe and Mary drew a salary of $50,000 each from the

partnership. With respect to decision made in “Rose v FCT (1951)” the salary drawn from

partnership is non-deductible under section 90, because it is considered as profits before the

balances is shared among the Joe and Mary.

The net income from the partnership and the distribution for each partners has been

calculated below;

8TAXATION LAW

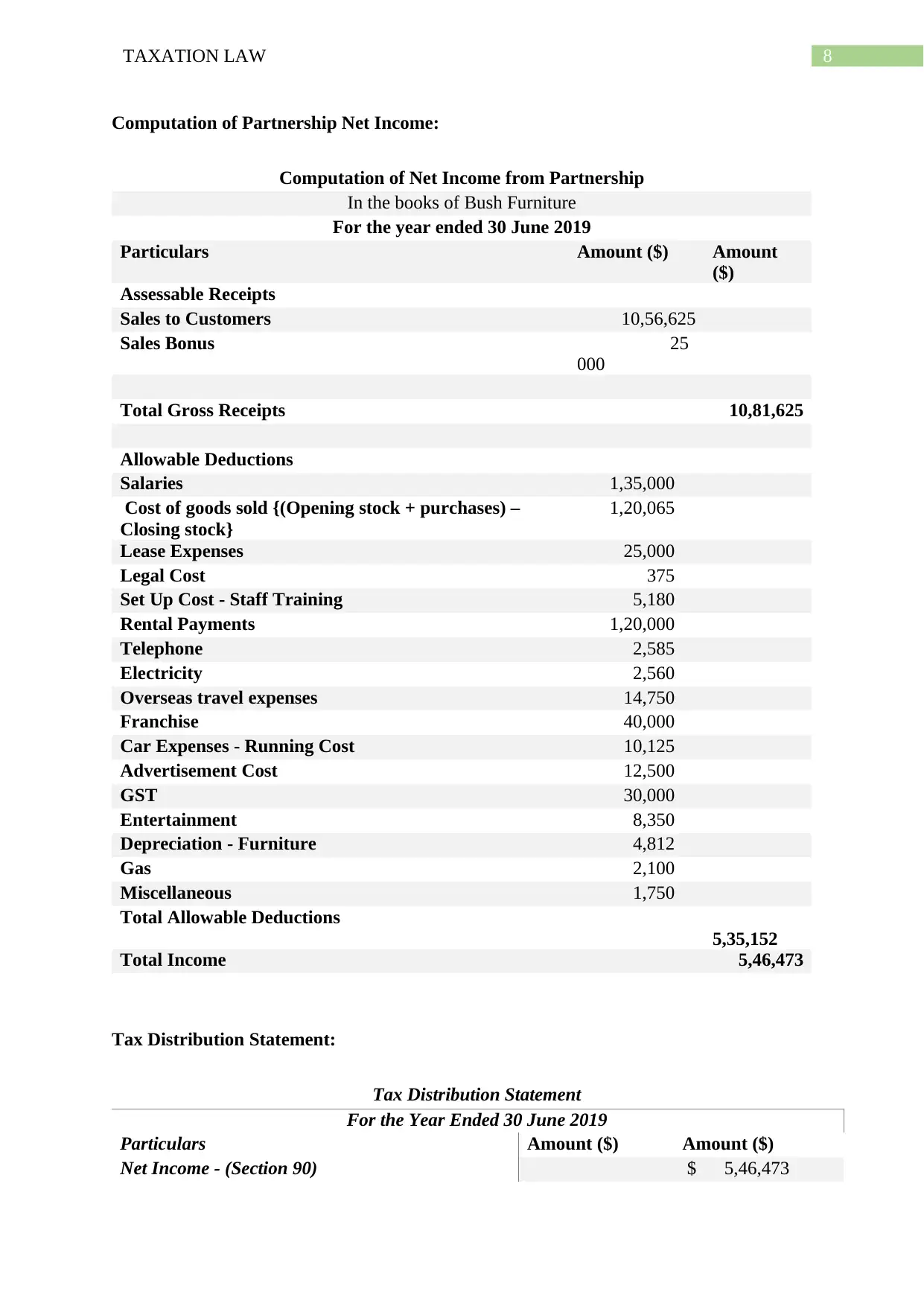

Computation of Partnership Net Income:

Computation of Net Income from Partnership

In the books of Bush Furniture

For the year ended 30 June 2019

Particulars Amount ($) Amount

($)

Assessable Receipts

Sales to Customers 10,56,625

Sales Bonus 25

000

Total Gross Receipts 10,81,625

Allowable Deductions

Salaries 1,35,000

Cost of goods sold {(Opening stock + purchases) –

Closing stock}

1,20,065

Lease Expenses 25,000

Legal Cost 375

Set Up Cost - Staff Training 5,180

Rental Payments 1,20,000

Telephone 2,585

Electricity 2,560

Overseas travel expenses 14,750

Franchise 40,000

Car Expenses - Running Cost 10,125

Advertisement Cost 12,500

GST 30,000

Entertainment 8,350

Depreciation - Furniture 4,812

Gas 2,100

Miscellaneous 1,750

Total Allowable Deductions

5,35,152

Total Income 5,46,473

Tax Distribution Statement:

Tax Distribution Statement

For the Year Ended 30 June 2019

Particulars Amount ($) Amount ($)

Net Income - (Section 90) $ 5,46,473

Computation of Partnership Net Income:

Computation of Net Income from Partnership

In the books of Bush Furniture

For the year ended 30 June 2019

Particulars Amount ($) Amount

($)

Assessable Receipts

Sales to Customers 10,56,625

Sales Bonus 25

000

Total Gross Receipts 10,81,625

Allowable Deductions

Salaries 1,35,000

Cost of goods sold {(Opening stock + purchases) –

Closing stock}

1,20,065

Lease Expenses 25,000

Legal Cost 375

Set Up Cost - Staff Training 5,180

Rental Payments 1,20,000

Telephone 2,585

Electricity 2,560

Overseas travel expenses 14,750

Franchise 40,000

Car Expenses - Running Cost 10,125

Advertisement Cost 12,500

GST 30,000

Entertainment 8,350

Depreciation - Furniture 4,812

Gas 2,100

Miscellaneous 1,750

Total Allowable Deductions

5,35,152

Total Income 5,46,473

Tax Distribution Statement:

Tax Distribution Statement

For the Year Ended 30 June 2019

Particulars Amount ($) Amount ($)

Net Income - (Section 90) $ 5,46,473

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

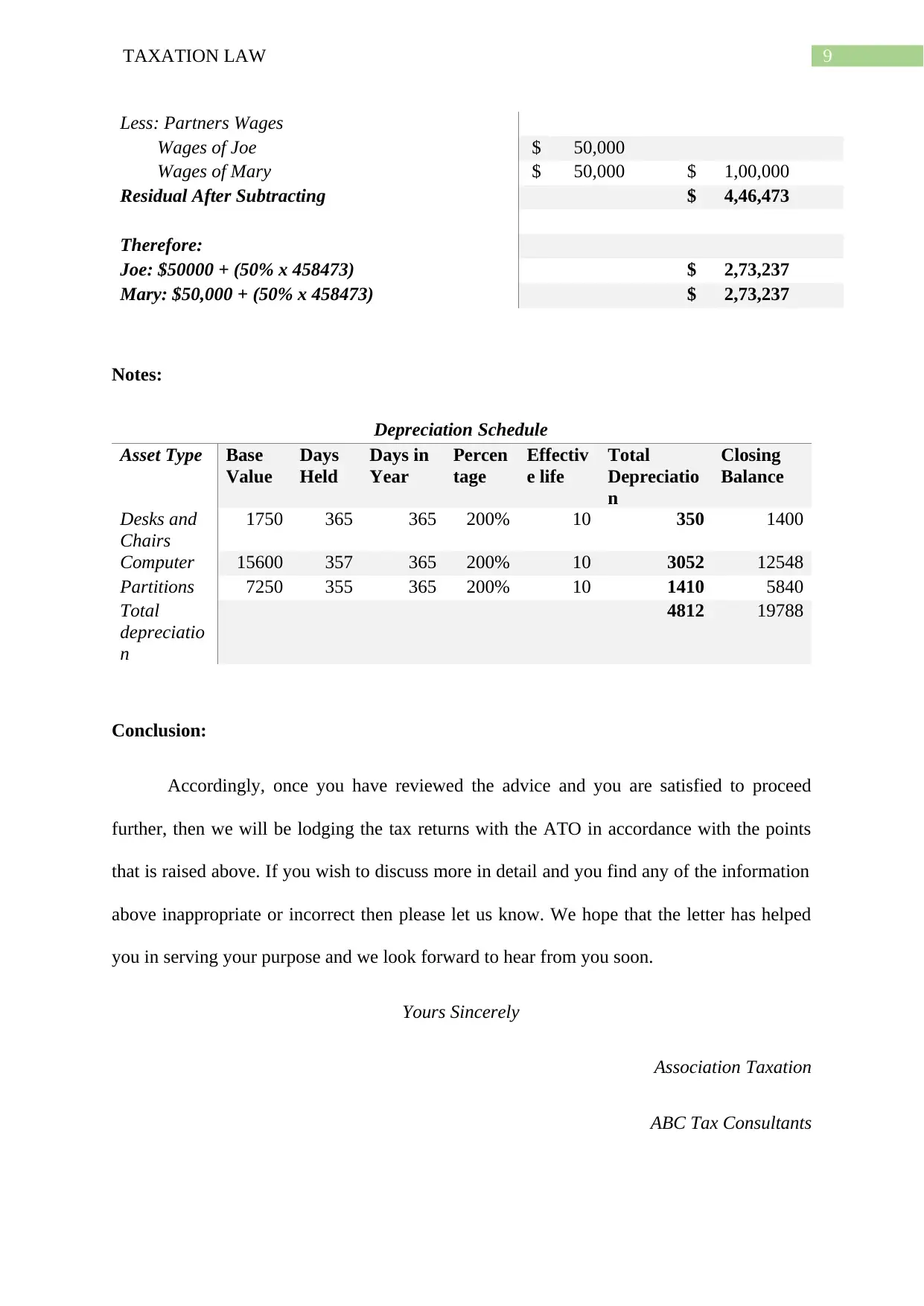

Less: Partners Wages

Wages of Joe $ 50,000

Wages of Mary $ 50,000 $ 1,00,000

Residual After Subtracting $ 4,46,473

Therefore:

Joe: $50000 + (50% x 458473) $ 2,73,237

Mary: $50,000 + (50% x 458473) $ 2,73,237

Notes:

Depreciation Schedule

Asset Type Base

Value

Days

Held

Days in

Year

Percen

tage

Effectiv

e life

Total

Depreciatio

n

Closing

Balance

Desks and

Chairs

1750 365 365 200% 10 350 1400

Computer 15600 357 365 200% 10 3052 12548

Partitions 7250 355 365 200% 10 1410 5840

Total

depreciatio

n

4812 19788

Conclusion:

Accordingly, once you have reviewed the advice and you are satisfied to proceed

further, then we will be lodging the tax returns with the ATO in accordance with the points

that is raised above. If you wish to discuss more in detail and you find any of the information

above inappropriate or incorrect then please let us know. We hope that the letter has helped

you in serving your purpose and we look forward to hear from you soon.

Yours Sincerely

Association Taxation

ABC Tax Consultants

Less: Partners Wages

Wages of Joe $ 50,000

Wages of Mary $ 50,000 $ 1,00,000

Residual After Subtracting $ 4,46,473

Therefore:

Joe: $50000 + (50% x 458473) $ 2,73,237

Mary: $50,000 + (50% x 458473) $ 2,73,237

Notes:

Depreciation Schedule

Asset Type Base

Value

Days

Held

Days in

Year

Percen

tage

Effectiv

e life

Total

Depreciatio

n

Closing

Balance

Desks and

Chairs

1750 365 365 200% 10 350 1400

Computer 15600 357 365 200% 10 3052 12548

Partitions 7250 355 365 200% 10 1410 5840

Total

depreciatio

n

4812 19788

Conclusion:

Accordingly, once you have reviewed the advice and you are satisfied to proceed

further, then we will be lodging the tax returns with the ATO in accordance with the points

that is raised above. If you wish to discuss more in detail and you find any of the information

above inappropriate or incorrect then please let us know. We hope that the letter has helped

you in serving your purpose and we look forward to hear from you soon.

Yours Sincerely

Association Taxation

ABC Tax Consultants

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Freudenberg, B., Chardon, T., Brimble, M. and Isle, M.B., 2017. Tax literacy of Australian

small businesses. J. Austl. Tax'n, 19, p.21.

Morgan, A. and Castelyn, D., 2018. Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, p.307.

Morgan, A., Mortimer, C. and Pinto, D., 2018. A practical introduction to Australian

taxation law 2018. Oxford University Press.

Robin and Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.), 2019. Australian

Taxation Law Select 2019: Legislation and Commentary. Oxford University Press.

Robin, H., 2019. Australian Taxation Law 2019. Oxford University Press.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

References:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Freudenberg, B., Chardon, T., Brimble, M. and Isle, M.B., 2017. Tax literacy of Australian

small businesses. J. Austl. Tax'n, 19, p.21.

Morgan, A. and Castelyn, D., 2018. Taxation Education in Secondary Schools. J.

Australasian Tax Tchrs. Ass'n, 13, p.307.

Morgan, A., Mortimer, C. and Pinto, D., 2018. A practical introduction to Australian

taxation law 2018. Oxford University Press.

Robin and Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.), 2019. Australian

Taxation Law Select 2019: Legislation and Commentary. Oxford University Press.

Robin, H., 2019. Australian Taxation Law 2019. Oxford University Press.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.