Assessing Sydney Airport's Adherence to the Conceptual Framework

VerifiedAdded on 2023/06/15

|14

|2348

|431

Report

AI Summary

This report critically analyzes Sydney Airport's adherence to the conceptual framework of accounting, focusing on its compliance with the objectives, recognition criteria for assets, liabilities, equity, revenue, and expenses, as well as the qualitative enhancing characteristics of financial reporting. It evaluates the company's alignment with Corporations Act 2001, AASB, and IFRS standards. The report further examines the use of flow charts, bar diagrams, and two-year comparisons in presenting financial data for timeliness, comparability, and enhanced data interpretation. The findings confirm that Sydney Airport's annual report is structured in accordance with regulatory requirements and maintains qualitative characteristics through various data visualization methods.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary Issues in Accounting

Name of Student:

Name of University:

Author’s Note:

Contemporary Issues in Accounting

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary

The report has been able to depict whether the financial data published by Sydney Airport has

adhered to the conceptual framework. The report will evaluate the compliance of the company

for “assets, liabilities, equities, expenses and revenues”. The discourse of the study has been

further able to identify the several types of the aspects associated to the qualitative enhancing

characteristics of financial reporting. The final part of the report has been further abet take into

consideration the various type of the report which has been considered with measuring the

qualitative measure of the different aspects associated to discerning the timeliness aspect,

comparability and enhanced data interpretation. The findings of the report have been able to

ascertain annual report of Sydney Airport is arranged in accordance to “Corporations Act 2001,

(AASB)” and “(IFRS)”. The qualitative characteristics has been further seen to be maintained

with the use of flow chart, bar diagram, pie chart and two year comparison.

CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary

The report has been able to depict whether the financial data published by Sydney Airport has

adhered to the conceptual framework. The report will evaluate the compliance of the company

for “assets, liabilities, equities, expenses and revenues”. The discourse of the study has been

further able to identify the several types of the aspects associated to the qualitative enhancing

characteristics of financial reporting. The final part of the report has been further abet take into

consideration the various type of the report which has been considered with measuring the

qualitative measure of the different aspects associated to discerning the timeliness aspect,

comparability and enhanced data interpretation. The findings of the report have been able to

ascertain annual report of Sydney Airport is arranged in accordance to “Corporations Act 2001,

(AASB)” and “(IFRS)”. The qualitative characteristics has been further seen to be maintained

with the use of flow chart, bar diagram, pie chart and two year comparison.

2

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Adherence to the objectives of the conceptual framework with its reporting.................................3

Adherence with the recognition criteria for reporting Assets, Liabilities, Equity, Revenue and

Expenses..........................................................................................................................................4

Adherence with the qualitative enhancing characteristics of financial reporting............................5

Adherence with enhancing characteristics of financial reporting....................................................6

Conclusion.......................................................................................................................................7

References........................................................................................................................................8

List of Appendix..............................................................................................................................9

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Adherence to the objectives of the conceptual framework with its reporting.................................3

Adherence with the recognition criteria for reporting Assets, Liabilities, Equity, Revenue and

Expenses..........................................................................................................................................4

Adherence with the qualitative enhancing characteristics of financial reporting............................5

Adherence with enhancing characteristics of financial reporting....................................................6

Conclusion.......................................................................................................................................7

References........................................................................................................................................8

List of Appendix..............................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

“Sydney (Kingsford Smith) Airport” or “Sydney Airport” located in Sydney, Australia is

considered as one of the primary airport which is seen to be responsible for serving airline

operators such as Qantas, Virgin Australia and Jetstar Airways. It has been further seen that the

airport is seen to be situated next to Botany Bay consist of three runways namely east–west,

north–south and third runways. This Airport has been further considering the operations as

longest continuously operated commercial airports and busiest airport in Australia with an intake

capacity of more than 41,870,000 passengers in 2016.

The study has analysed the data given in the annual report of Sydney Airport and able to

discern whether it has adhered to the conceptual framework. The report will evaluate the

compliance of the company for “assets, liabilities, equities, expenses and revenues”. The

discourse of the study has been further able to identify the different types of the aspects

associated to the qualitative enhancing characteristics of financial reporting. The final part of the

report has been further able take into consideration the various type of the report which has been

considered with measuring the qualitative measure of the different aspects associated to

discerning the timeliness aspect, comparability and enhanced data interpretation (Chaplin 2017).

Adherence to the objectives of the conceptual framework with its reporting

The conceptual framework of the report has been seen be related to the various types of

elements which has prescribed by “Australian Accounting Standards Board (AASB)”. The main

form of the contributing role of this has been based on the various types of the factors considered

with “Australian securities and investment commission at 2001”. As per the amendments

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

“Sydney (Kingsford Smith) Airport” or “Sydney Airport” located in Sydney, Australia is

considered as one of the primary airport which is seen to be responsible for serving airline

operators such as Qantas, Virgin Australia and Jetstar Airways. It has been further seen that the

airport is seen to be situated next to Botany Bay consist of three runways namely east–west,

north–south and third runways. This Airport has been further considering the operations as

longest continuously operated commercial airports and busiest airport in Australia with an intake

capacity of more than 41,870,000 passengers in 2016.

The study has analysed the data given in the annual report of Sydney Airport and able to

discern whether it has adhered to the conceptual framework. The report will evaluate the

compliance of the company for “assets, liabilities, equities, expenses and revenues”. The

discourse of the study has been further able to identify the different types of the aspects

associated to the qualitative enhancing characteristics of financial reporting. The final part of the

report has been further able take into consideration the various type of the report which has been

considered with measuring the qualitative measure of the different aspects associated to

discerning the timeliness aspect, comparability and enhanced data interpretation (Chaplin 2017).

Adherence to the objectives of the conceptual framework with its reporting

The conceptual framework of the report has been seen be related to the various types of

elements which has prescribed by “Australian Accounting Standards Board (AASB)”. The main

form of the contributing role of this has been based on the various types of the factors considered

with “Australian securities and investment commission at 2001”. As per the amendments

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CONTEMPORARY ISSUES IN ACCOUNTING

published in December 2013 the board for “measurement, presentation, reporting entity and de-

recognition”. The changes associated to the accounting and financial reforms brought by the

board has been further able to state on the various aspects for driving management stewardship

among the entities (Weller 2017).

As per the information published in the annual report of Sydney Airport is arranged in

accordance to “Corporations Act 2001, Australian Accounting Standards” which is seen to be

adopted by Australian “Accounting Standards Board (AASB)” and “International Financial

Reporting Standards (IFRS)”. The group of the new standard has been discerned to be revised

with the different types of the consideration which has been seen to be issues by AASB with

relevancy on the operations and effective in terms of the present period of reporting. The new

adoption of the revised interpretations and standards which are yet to be adopted has been also

clearly stated in the financial report. The impact of this has been seen to be yet to be adopted in

December 2016 (Wines and Scarborough 2015).

Adherence with the recognition criteria for reporting Assets, Liabilities, Equity, Revenue

and Expenses

The preparation of the annual report has been further seen to be conducted with the

consideration of historical cost convention which is seen to be modified with the revaluation of

the financial assets and liabilities. The primary activity of SAT1 Group has been further seen to

be taken into consideration the various type of the activities for holding of the financial assets.

The impartment of the intangible asset of the company has been further seen to be taken into

account with the discounted cash flow methodology in time period of twenty years. The net

tangible (NTA) does not include the non-controlling interests and are seen to be associated to the

CONTEMPORARY ISSUES IN ACCOUNTING

published in December 2013 the board for “measurement, presentation, reporting entity and de-

recognition”. The changes associated to the accounting and financial reforms brought by the

board has been further able to state on the various aspects for driving management stewardship

among the entities (Weller 2017).

As per the information published in the annual report of Sydney Airport is arranged in

accordance to “Corporations Act 2001, Australian Accounting Standards” which is seen to be

adopted by Australian “Accounting Standards Board (AASB)” and “International Financial

Reporting Standards (IFRS)”. The group of the new standard has been discerned to be revised

with the different types of the consideration which has been seen to be issues by AASB with

relevancy on the operations and effective in terms of the present period of reporting. The new

adoption of the revised interpretations and standards which are yet to be adopted has been also

clearly stated in the financial report. The impact of this has been seen to be yet to be adopted in

December 2016 (Wines and Scarborough 2015).

Adherence with the recognition criteria for reporting Assets, Liabilities, Equity, Revenue

and Expenses

The preparation of the annual report has been further seen to be conducted with the

consideration of historical cost convention which is seen to be modified with the revaluation of

the financial assets and liabilities. The primary activity of SAT1 Group has been further seen to

be taken into consideration the various type of the activities for holding of the financial assets.

The impartment of the intangible asset of the company has been further seen to be taken into

account with the discounted cash flow methodology in time period of twenty years. The net

tangible (NTA) does not include the non-controlling interests and are seen to be associated to the

5

CONTEMPORARY ISSUES IN ACCOUNTING

sole representation of the various types the factors which are seen to be taken into consideration

with interest attributable to the security holders. The liability consideration of the company is

based on the various types of the factors associated to distribution payable, deferred income and

payables, derivative financial instruments and provision to the employee benefits (Dale-Jones,

Hancock and Willey 2013).

The critical accounting estimates and judgments on the accounting policies has indicated

on the test of impairment and goodwill. The identifiable net asset which are acquired takes into

account various types of the consideration which has been seen to be related to the measurement

at a fair value acquisition date. The finance costs are recognised with the costs which are

incurred with the effective interest rate method except in cases where it is directly attributable to

the construction, achievement and production of the assets considered suitable in nature. The

standards yet to be adopted has been taken into account as per “AASB 9: Financial Instruments”,

“AASB 15: Revenue from Contracts with Customers” and “AASB 16: Leases” (Momblanch et

al. 2014).

Adherence with the qualitative enhancing characteristics of financial reporting

The fair value in the rights has been taken into account with determination of allowance

date using “Monte Carlo model”. The CPS tranche has been further seen to be discerned with the

consideration of date of grant using binomial option used for the evaluating model. As the

company accompanies financial reporting accordance with Corporations ACT 2001, it considers

publishing of true and fair view of information as published on 31 December 2016. It has ben

also discerned the preparation of the financial reports of the company which is based on

depicting fair view prepared in accordance with “Australian Accounting Standards and

CONTEMPORARY ISSUES IN ACCOUNTING

sole representation of the various types the factors which are seen to be taken into consideration

with interest attributable to the security holders. The liability consideration of the company is

based on the various types of the factors associated to distribution payable, deferred income and

payables, derivative financial instruments and provision to the employee benefits (Dale-Jones,

Hancock and Willey 2013).

The critical accounting estimates and judgments on the accounting policies has indicated

on the test of impairment and goodwill. The identifiable net asset which are acquired takes into

account various types of the consideration which has been seen to be related to the measurement

at a fair value acquisition date. The finance costs are recognised with the costs which are

incurred with the effective interest rate method except in cases where it is directly attributable to

the construction, achievement and production of the assets considered suitable in nature. The

standards yet to be adopted has been taken into account as per “AASB 9: Financial Instruments”,

“AASB 15: Revenue from Contracts with Customers” and “AASB 16: Leases” (Momblanch et

al. 2014).

Adherence with the qualitative enhancing characteristics of financial reporting

The fair value in the rights has been taken into account with determination of allowance

date using “Monte Carlo model”. The CPS tranche has been further seen to be discerned with the

consideration of date of grant using binomial option used for the evaluating model. As the

company accompanies financial reporting accordance with Corporations ACT 2001, it considers

publishing of true and fair view of information as published on 31 December 2016. It has ben

also discerned the preparation of the financial reports of the company which is based on

depicting fair view prepared in accordance with “Australian Accounting Standards and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CONTEMPORARY ISSUES IN ACCOUNTING

Corporations Act 2001”. In addition to this, the application of the necessary internal control has

been further realized to be based on the consideration of the changed types of the information

which is seen to be based on depicting true and fair view of the material misstatement for fraud

error. The various types of the historic cost conventions are changed with the revaluation of the

specific types of the financial assets which are seen to be considered with the various types of the

factors associated to depicting of fair value through profit and loss. In case of the business

combinations the main form of the acquisition method has been seen to be used with the

consideration of transferred acquisition measured at fair value (Danoucaras and Woodley 2013).

Adherence with enhancing characteristics of financial reporting

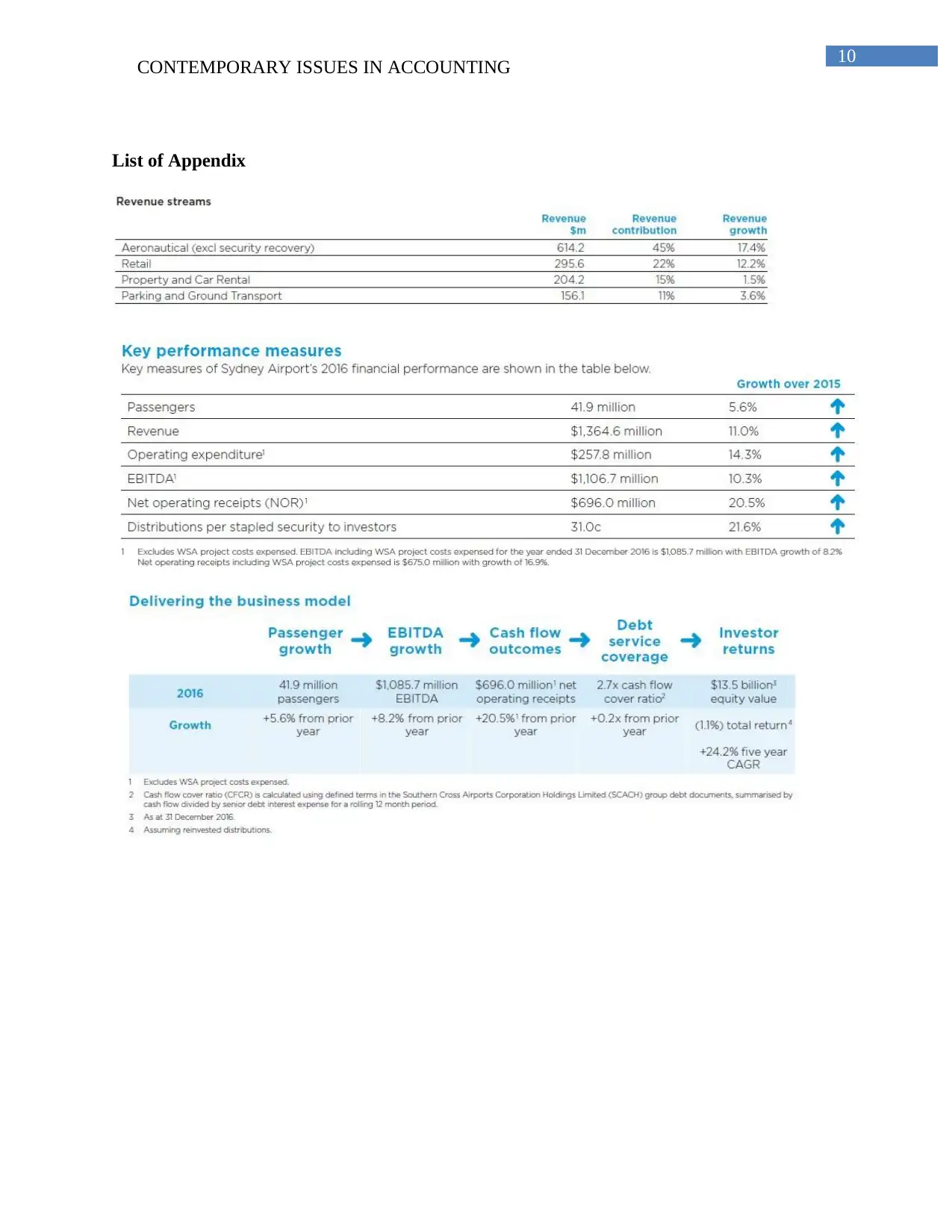

In order to depict the reports with a better comparative aspect and representation of the

data, the company has been seen to be using flow chart to represent the relevant data related to

passenger growth, Debt service coverage, outcomes of cash flow, EBITDA, outcomes of the

cash flows and investor returns (Müller 2014).

It has been further able to depict some of the key performance measures which has been

seen to be observed in terms of the growth of the financial performance in compare to 2015.

When representing the information on revenue streams, the company has categorised the data as

per revenue contribution and revenue growth. The aeronautical revenue of the company has been

distributed from 2012 to 2016. In order to represent the data in a better way the segregation has

been done as per 11% growth in Europe and Middle East, 22% growth in India, 3% growth in

New Zealand and 7% growth in South East Asia. The retail revenue segregation of the company

has been taken into consideration with bar diagram. In a similar way the car rental and revenue

CONTEMPORARY ISSUES IN ACCOUNTING

Corporations Act 2001”. In addition to this, the application of the necessary internal control has

been further realized to be based on the consideration of the changed types of the information

which is seen to be based on depicting true and fair view of the material misstatement for fraud

error. The various types of the historic cost conventions are changed with the revaluation of the

specific types of the financial assets which are seen to be considered with the various types of the

factors associated to depicting of fair value through profit and loss. In case of the business

combinations the main form of the acquisition method has been seen to be used with the

consideration of transferred acquisition measured at fair value (Danoucaras and Woodley 2013).

Adherence with enhancing characteristics of financial reporting

In order to depict the reports with a better comparative aspect and representation of the

data, the company has been seen to be using flow chart to represent the relevant data related to

passenger growth, Debt service coverage, outcomes of cash flow, EBITDA, outcomes of the

cash flows and investor returns (Müller 2014).

It has been further able to depict some of the key performance measures which has been

seen to be observed in terms of the growth of the financial performance in compare to 2015.

When representing the information on revenue streams, the company has categorised the data as

per revenue contribution and revenue growth. The aeronautical revenue of the company has been

distributed from 2012 to 2016. In order to represent the data in a better way the segregation has

been done as per 11% growth in Europe and Middle East, 22% growth in India, 3% growth in

New Zealand and 7% growth in South East Asia. The retail revenue segregation of the company

has been taken into consideration with bar diagram. In a similar way the car rental and revenue

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CONTEMPORARY ISSUES IN ACCOUNTING

has been seen to be discerned with different consideration which has been discerned as per the

growth from 2012 to 2016 (Kumarasiri and Jubb 2016).

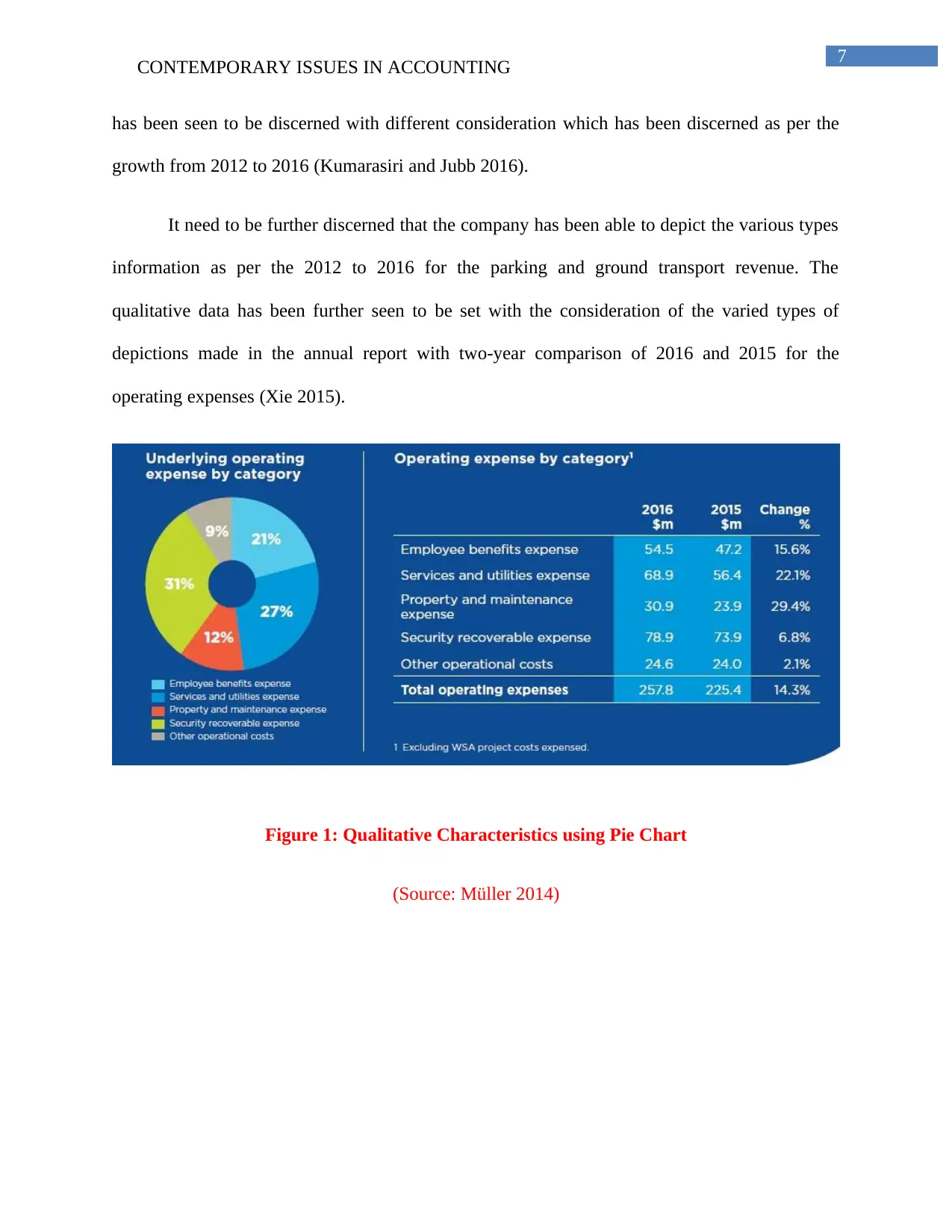

It need to be further discerned that the company has been able to depict the various types

information as per the 2012 to 2016 for the parking and ground transport revenue. The

qualitative data has been further seen to be set with the consideration of the varied types of

depictions made in the annual report with two-year comparison of 2016 and 2015 for the

operating expenses (Xie 2015).

Figure 1: Qualitative Characteristics using Pie Chart

(Source: Müller 2014)

CONTEMPORARY ISSUES IN ACCOUNTING

has been seen to be discerned with different consideration which has been discerned as per the

growth from 2012 to 2016 (Kumarasiri and Jubb 2016).

It need to be further discerned that the company has been able to depict the various types

information as per the 2012 to 2016 for the parking and ground transport revenue. The

qualitative data has been further seen to be set with the consideration of the varied types of

depictions made in the annual report with two-year comparison of 2016 and 2015 for the

operating expenses (Xie 2015).

Figure 1: Qualitative Characteristics using Pie Chart

(Source: Müller 2014)

8

CONTEMPORARY ISSUES IN ACCOUNTING

Figure 2: Qualitative Characteristics using Pie Chart and Bar Graph

(Source: Müller 2014)

Conclusion

The report has been able to depict that adherence to conceptual framework objectives has

been seen with “Corporations Act 2001, Australian Accounting Standards” which is seen to be

implemented by Australian “Accounting Standards Board (AASB)” and “International Financial

Reporting Standards (IFRS)”.Recognition criteria for reporting Assets has been discerned with

impartment of the intangible asset of the company has been further seen to be taken into account

with the discounted cash flow methodology in time period of twenty years. The liability has been

taken with factors associated to distribution payable, deferred income and payables, derivative

financial instruments and provision to the employee benefits. The finance expenses are

recognised with the expenses which are incurred with the “effective interest rate method” except

in cases where it is “directly attributable to the construction”, achievement and production of the

assets considered suitable in nature.

CONTEMPORARY ISSUES IN ACCOUNTING

Figure 2: Qualitative Characteristics using Pie Chart and Bar Graph

(Source: Müller 2014)

Conclusion

The report has been able to depict that adherence to conceptual framework objectives has

been seen with “Corporations Act 2001, Australian Accounting Standards” which is seen to be

implemented by Australian “Accounting Standards Board (AASB)” and “International Financial

Reporting Standards (IFRS)”.Recognition criteria for reporting Assets has been discerned with

impartment of the intangible asset of the company has been further seen to be taken into account

with the discounted cash flow methodology in time period of twenty years. The liability has been

taken with factors associated to distribution payable, deferred income and payables, derivative

financial instruments and provision to the employee benefits. The finance expenses are

recognised with the expenses which are incurred with the “effective interest rate method” except

in cases where it is “directly attributable to the construction”, achievement and production of the

assets considered suitable in nature.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CONTEMPORARY ISSUES IN ACCOUNTING

References

Chaplin, S. (2017) ‘Accounting Education and the Prerequisite Skills of Accounting Graduates:

Are Accounting Firms’ Moving the Boundaries?’, Australian Accounting Review, pp. 61–70.

doi: 10.1111/auar.12146.

Dale-Jones, G., Hancock, P. and Willey, K. (2013) ‘Accounting Students in an Australian

University Improve their Writing: But How Did it Happen?’, Accounting Education, 22(6), pp.

544–562. doi: 10.1080/09639284.2013.847321.

Danoucaras, A. N. and Woodley, A. (2013) ‘Alignment and Differences between the Australian

Water Accounting Standard and the Water Accounting Framework for the Minerals Industry’, in

Water in Mining Conference, Brisbane, QLD, 26-28 November 2013, pp. 26–28. Available at:

https://drive.google.com/open?id=0B1R-rSdERLu7QlJoeGg0OEVkOE0.

Kumarasiri, J. and Jubb, C. (2016) ‘Carbon emission risks and management accounting:

Australian evidence’, Accounting Research Journal, 29(2), pp. 137–153. doi: 10.1108/ARJ-03-

2015-0040.

Momblanch, A., Andreu, J., Paredes-Arquiola, J., Solera, A. and Pedro-Monzonís, M. (2014)

‘Adapting water accounting for integrated water resource management. The Júcar Water

Resource System (Spain)’, Journal of Hydrology, 519(PD), pp. 3369–3385. doi:

10.1016/j.jhydrol.2014.10.002.

Müller, J. (2014) ‘An accounting revolution? The financialisation of standard setting’, Critical

Perspectives on Accounting, 25(7), pp. 539–557. doi: 10.1016/j.cpa.2013.08.006.

Weller, S. A. (2017) ‘Accounting for Skill Shortages? Migration and the Australian Labour

Market’, Population, Space and Place, 23(2). doi: 10.1002/psp.1997.

Wines, G. and Scarborough, H. (2015) ‘Accounting Research Journal Australian government

budget balance numbers The hybrid nature of public sector accrual accounting’, Accounting

Research Journal Accounting Research Journal Accounting Research Journal, 28(2), pp. 143–

159. doi: 10.1108/ARJ-01-2014-0001.

Xie, Y. (2015) ‘Confusion over Accounting Conservatism: A Critical Review’, Australian

Accounting Review, 25(2), pp. 204–216. doi: 10.1111/auar.12061.

CONTEMPORARY ISSUES IN ACCOUNTING

References

Chaplin, S. (2017) ‘Accounting Education and the Prerequisite Skills of Accounting Graduates:

Are Accounting Firms’ Moving the Boundaries?’, Australian Accounting Review, pp. 61–70.

doi: 10.1111/auar.12146.

Dale-Jones, G., Hancock, P. and Willey, K. (2013) ‘Accounting Students in an Australian

University Improve their Writing: But How Did it Happen?’, Accounting Education, 22(6), pp.

544–562. doi: 10.1080/09639284.2013.847321.

Danoucaras, A. N. and Woodley, A. (2013) ‘Alignment and Differences between the Australian

Water Accounting Standard and the Water Accounting Framework for the Minerals Industry’, in

Water in Mining Conference, Brisbane, QLD, 26-28 November 2013, pp. 26–28. Available at:

https://drive.google.com/open?id=0B1R-rSdERLu7QlJoeGg0OEVkOE0.

Kumarasiri, J. and Jubb, C. (2016) ‘Carbon emission risks and management accounting:

Australian evidence’, Accounting Research Journal, 29(2), pp. 137–153. doi: 10.1108/ARJ-03-

2015-0040.

Momblanch, A., Andreu, J., Paredes-Arquiola, J., Solera, A. and Pedro-Monzonís, M. (2014)

‘Adapting water accounting for integrated water resource management. The Júcar Water

Resource System (Spain)’, Journal of Hydrology, 519(PD), pp. 3369–3385. doi:

10.1016/j.jhydrol.2014.10.002.

Müller, J. (2014) ‘An accounting revolution? The financialisation of standard setting’, Critical

Perspectives on Accounting, 25(7), pp. 539–557. doi: 10.1016/j.cpa.2013.08.006.

Weller, S. A. (2017) ‘Accounting for Skill Shortages? Migration and the Australian Labour

Market’, Population, Space and Place, 23(2). doi: 10.1002/psp.1997.

Wines, G. and Scarborough, H. (2015) ‘Accounting Research Journal Australian government

budget balance numbers The hybrid nature of public sector accrual accounting’, Accounting

Research Journal Accounting Research Journal Accounting Research Journal, 28(2), pp. 143–

159. doi: 10.1108/ARJ-01-2014-0001.

Xie, Y. (2015) ‘Confusion over Accounting Conservatism: A Critical Review’, Australian

Accounting Review, 25(2), pp. 204–216. doi: 10.1111/auar.12061.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CONTEMPORARY ISSUES IN ACCOUNTING

List of Appendix

CONTEMPORARY ISSUES IN ACCOUNTING

List of Appendix

11

CONTEMPORARY ISSUES IN ACCOUNTING

CONTEMPORARY ISSUES IN ACCOUNTING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.