Analysis of Commercial Real Estate Market: Case Study of Castle Towers

VerifiedAdded on 2023/06/12

|11

|3468

|88

Report

AI Summary

This report provides an economic evaluation of the Castle Towers shopping center in Castle Hill, Sydney, examining its role in the regional and sub-regional commercial retail property market. It discusses the commercial real estate landscape in Sydney, highlighting the city's attractiveness to businesses due to its economic freedom and talent pool. The report analyzes the impact of the Global Financial Crisis on the Australian financial markets and the supply of commercial real estate, along with current lending rates and wages affecting the economy. It also explores the expansion of Castle Hill Towers, future development plans, competition, and strategies, providing an outlook for the future of the property and the broader commercial real estate market in Sydney. Desklib offers similar solved assignments and past papers for students.

qwertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopas

dfghjklzxcvbnmrtyuiopasdfghjklzxcvb

[Type the document title]

[Type the document subtitle]

[Pick the date]

Geeta

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopas

dfghjklzxcvbnmrtyuiopasdfghjklzxcvb

[Type the document title]

[Type the document subtitle]

[Pick the date]

Geeta

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

1. Introduction.........................................................................................................................................2

2) Commercial Real Estate in Sydney...........................................................................................................2

3) The Regional and Sub Regional Commercial Retail Property Market of Sydney...................................2

4 Castle Towers...........................................................................................................................................3

4.1 Castle Tower: Infrastructure and Accessibility..................................................................................4

5 Financial Markets and the Supply of Commercial Real Estate in Australia in the Posts Global Financial

Crisis Period................................................................................................................................................4

6. Australia Economy: Lending Rates and Wages.......................................................................................5

7. The Expansion of Castle Hill Towers and Future Deveopment..............................................................7

8 Competition and Coping Up Strategies....................................................................................................8

9 Outlook for the Future..............................................................................................................................8

10 Conclusion..............................................................................................................................................9

1. Introduction.........................................................................................................................................2

2) Commercial Real Estate in Sydney...........................................................................................................2

3) The Regional and Sub Regional Commercial Retail Property Market of Sydney...................................2

4 Castle Towers...........................................................................................................................................3

4.1 Castle Tower: Infrastructure and Accessibility..................................................................................4

5 Financial Markets and the Supply of Commercial Real Estate in Australia in the Posts Global Financial

Crisis Period................................................................................................................................................4

6. Australia Economy: Lending Rates and Wages.......................................................................................5

7. The Expansion of Castle Hill Towers and Future Deveopment..............................................................7

8 Competition and Coping Up Strategies....................................................................................................8

9 Outlook for the Future..............................................................................................................................8

10 Conclusion..............................................................................................................................................9

1. Introduction

The Castle Towers shopping center in the sub region of Castle Hill in north Sydney is one of the

biggest shopping centers in the country. In the midst of an expansion, this shopping center has a

turn over of millions of dollars per day. In a world where commercial shopping centers are

struggling to make spaces worth the rent, the Sydney market is increasingly showing growth in

terms of rental prices. This report contains an economic evaluation of one such commercial

property the Castle Towers in Castle Hill.

2) Commercial Real Estate in Sydney

Compared to global giants, Sydney has a relatively small office stock, a measure to understand

the supply of office. In the year 2016, the prime yields of the commercial real estate space were

slightly over 5%, thank to the high liquidity cycle that has been maintained in Australia, since

2010. Sydney, as a market, is attractive to businesses thanks to a relatively high degree of

economic freedom in the city as well as the availability of talent pool. (Cushman and Wakefield

Capital Markets). The city has a talent pool of educated, English speaking young population.

This adds to the attractiveness of the job market, which is inherently linked to retail spending.

In addition to this, Australia is generally supportive of Free trade Agreements and general

business. As Australia’s trade ties grow stronger, Sydney as a market stands to gain, being one of

the topmost commercial cities of the country. (Cushman and Wakefield Capital Markets)

Cromwell Funds Management, (2017) has expected the vacancy space in commerical spaces in

Syndney to remain at less than 5%, while the growth of new stock of real estate property keeps

declining. The direct result of the increasing business, is the availability of a working

professional population. The deep pockets, combined with the low interest rates that make easy

credit available for spending, will hopefully trigger a boom in retail and leisure spending.

(Cromwell Property Group, 2018)

The Castle Towers shopping center in the sub region of Castle Hill in north Sydney is one of the

biggest shopping centers in the country. In the midst of an expansion, this shopping center has a

turn over of millions of dollars per day. In a world where commercial shopping centers are

struggling to make spaces worth the rent, the Sydney market is increasingly showing growth in

terms of rental prices. This report contains an economic evaluation of one such commercial

property the Castle Towers in Castle Hill.

2) Commercial Real Estate in Sydney

Compared to global giants, Sydney has a relatively small office stock, a measure to understand

the supply of office. In the year 2016, the prime yields of the commercial real estate space were

slightly over 5%, thank to the high liquidity cycle that has been maintained in Australia, since

2010. Sydney, as a market, is attractive to businesses thanks to a relatively high degree of

economic freedom in the city as well as the availability of talent pool. (Cushman and Wakefield

Capital Markets). The city has a talent pool of educated, English speaking young population.

This adds to the attractiveness of the job market, which is inherently linked to retail spending.

In addition to this, Australia is generally supportive of Free trade Agreements and general

business. As Australia’s trade ties grow stronger, Sydney as a market stands to gain, being one of

the topmost commercial cities of the country. (Cushman and Wakefield Capital Markets)

Cromwell Funds Management, (2017) has expected the vacancy space in commerical spaces in

Syndney to remain at less than 5%, while the growth of new stock of real estate property keeps

declining. The direct result of the increasing business, is the availability of a working

professional population. The deep pockets, combined with the low interest rates that make easy

credit available for spending, will hopefully trigger a boom in retail and leisure spending.

(Cromwell Property Group, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3) The Regional and Sub Regional Commercial Retail Property Market of Sydney

The average expected yield in the sub regional retail sector was 6.03% in the first quarter of 2017

and is estimated to be at 6.13% during the corresponding period in 2018. (Colliers International,

2017)

The average Gross Face rents in New South Wales are expected to rise from $1355 to $1381 and

the retail vacancy stood at 4.10%. this is lower than the full occupancy rate. If the population of

sydney grows further and the demand for retail commercial space increases, the prices of the

commercial market are expected to be inflated even further. New South Wales experienced a

population growth of 1.61% in 2016-2017 and there is a good chance that Sydney might benefit

to a great extent from this population growth. (Colliers International, 2017) In a siutation where

such rapid growth is expected, Commercial Property Managers must seek to have shorter leases

or seek to have leases where there is a default increase in rent by 4% at the end of the year.

While it is expected that the yields on the retail spaces in Australia to compress, the volume of

exchanges is expected to remain, making the retail space a viable solution. (Facility

Management, 2017)

In 2017, the national retail sales had grown by 40% as compared to the pre Global Financial

Levels. This could have been a result of the easy availability of credit owing to the low interest

rate policy that the Reserve Bank of Australia has maintained since the Global Financial Crisis.

A large part of that spending has been on relatively discretionary items like food, apparel and

hospitality sectors. (Colliers International, 2017)

Among the mix of the rental spaces, the contribution of Food and Beverage Industry and

entertainment is increasing. This trend is maintained in the regional sub centers. Hence, it would

make sense for sub centers to seek out Food and Beverage companies and increase their

contribution in the rent mix.

4 Castle Towers

The Castle Towers are located in the Castile Hill Property in Sydney. The sub regional property

has approximately 114,000 square meters (GLA Retail) of floor space. Owned by Queensland

Investment Corporation, it has a total available 5300 parking spaces. The Castle Towers is a

major retail hub with access to plenty of residential areas. Located in the booming area of North

The average expected yield in the sub regional retail sector was 6.03% in the first quarter of 2017

and is estimated to be at 6.13% during the corresponding period in 2018. (Colliers International,

2017)

The average Gross Face rents in New South Wales are expected to rise from $1355 to $1381 and

the retail vacancy stood at 4.10%. this is lower than the full occupancy rate. If the population of

sydney grows further and the demand for retail commercial space increases, the prices of the

commercial market are expected to be inflated even further. New South Wales experienced a

population growth of 1.61% in 2016-2017 and there is a good chance that Sydney might benefit

to a great extent from this population growth. (Colliers International, 2017) In a siutation where

such rapid growth is expected, Commercial Property Managers must seek to have shorter leases

or seek to have leases where there is a default increase in rent by 4% at the end of the year.

While it is expected that the yields on the retail spaces in Australia to compress, the volume of

exchanges is expected to remain, making the retail space a viable solution. (Facility

Management, 2017)

In 2017, the national retail sales had grown by 40% as compared to the pre Global Financial

Levels. This could have been a result of the easy availability of credit owing to the low interest

rate policy that the Reserve Bank of Australia has maintained since the Global Financial Crisis.

A large part of that spending has been on relatively discretionary items like food, apparel and

hospitality sectors. (Colliers International, 2017)

Among the mix of the rental spaces, the contribution of Food and Beverage Industry and

entertainment is increasing. This trend is maintained in the regional sub centers. Hence, it would

make sense for sub centers to seek out Food and Beverage companies and increase their

contribution in the rent mix.

4 Castle Towers

The Castle Towers are located in the Castile Hill Property in Sydney. The sub regional property

has approximately 114,000 square meters (GLA Retail) of floor space. Owned by Queensland

Investment Corporation, it has a total available 5300 parking spaces. The Castle Towers is a

major retail hub with access to plenty of residential areas. Located in the booming area of North

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

West Sydney, the Towers offer space for shopping, dining, entertainment and other commercial

purposes. Over 300 specialty retailers operate in the Castle Hill Towers. These include retail

services of every kind, right from clothing brands to restaurant chains to skin clinics. The retail

mix of the Castle Towers is well balanced with general super stores such as Kmart and specialty

stores such as wellness clinics.

4.1 Castle Tower: Infrastructure and Accessibility

Accessibility and the public infrastructure surrounding the mall are important from the point of

view of increasing the footfall at the mall. As the property is attached to a larger development

project of Castle Hill, it is accessible to a host of residential projects in the surrounding areas,

making it a very attractive investment. The property is surrounded by a number of establishments

that could a source of customers. These include the Western Australia University of Pamaratta.

The property is roughly 33 minutes of a drive by car from the Central Business District and is

surrounded by a host of residential projects other than Castle Hill. The property already enjoys

great accessibility by the road network with easy access to buses. (Cushman and Wakefield

Capital Markets)

5 Financial Markets and the Supply of Commercial Real Estate in Australia in the Posts

Global Financial Crisis Period

Prior to the Global Financial Crisis, the property was set for an expansion. However, as the

Global Financial Crisis hit the country, expansion of the property much like many other

properties. (Besser, 2007) The Global Financial Crisis of 2007-2008 had a significant impact on

the global, Australian as well as the Sydney property markets. The number of asset value write

downs sky rocketed and banking and non-banking financial funding hit new lows. Credit policies

of banks were oriented towards zero risk and several non-banking financial firms and

institutional foreign firms exited the market. (Ellis & Naughtin, 2010)

The Australian banking system, regulated by the Australian Prudential Regulatory Authority was

somewhat less competitive and more conservative than some other advanced economies like

USA, which insulated the financial system in Australia from the negative impacts of the financial

crisis to some extent. The exposure to subprime assets was lower. Yet, the contagion of the

Global Financial crisis affected Australia because lender repatriated funds to their home country,

leading to a liquidity crisis in Australia. As a result, the financial positions of several banks were

purposes. Over 300 specialty retailers operate in the Castle Hill Towers. These include retail

services of every kind, right from clothing brands to restaurant chains to skin clinics. The retail

mix of the Castle Towers is well balanced with general super stores such as Kmart and specialty

stores such as wellness clinics.

4.1 Castle Tower: Infrastructure and Accessibility

Accessibility and the public infrastructure surrounding the mall are important from the point of

view of increasing the footfall at the mall. As the property is attached to a larger development

project of Castle Hill, it is accessible to a host of residential projects in the surrounding areas,

making it a very attractive investment. The property is surrounded by a number of establishments

that could a source of customers. These include the Western Australia University of Pamaratta.

The property is roughly 33 minutes of a drive by car from the Central Business District and is

surrounded by a host of residential projects other than Castle Hill. The property already enjoys

great accessibility by the road network with easy access to buses. (Cushman and Wakefield

Capital Markets)

5 Financial Markets and the Supply of Commercial Real Estate in Australia in the Posts

Global Financial Crisis Period

Prior to the Global Financial Crisis, the property was set for an expansion. However, as the

Global Financial Crisis hit the country, expansion of the property much like many other

properties. (Besser, 2007) The Global Financial Crisis of 2007-2008 had a significant impact on

the global, Australian as well as the Sydney property markets. The number of asset value write

downs sky rocketed and banking and non-banking financial funding hit new lows. Credit policies

of banks were oriented towards zero risk and several non-banking financial firms and

institutional foreign firms exited the market. (Ellis & Naughtin, 2010)

The Australian banking system, regulated by the Australian Prudential Regulatory Authority was

somewhat less competitive and more conservative than some other advanced economies like

USA, which insulated the financial system in Australia from the negative impacts of the financial

crisis to some extent. The exposure to subprime assets was lower. Yet, the contagion of the

Global Financial crisis affected Australia because lender repatriated funds to their home country,

leading to a liquidity crisis in Australia. As a result, the financial positions of several banks were

eroded due losses incurred owing to asset write-offs and write-downs. (Ellis & Naughtin, 2010)

Australian banks relied heavily on international funding. The liquidity crisis caused by the

financial crisis made borrowing funds and gaining investors from the international markets more

expensive. (Jones Lang LaSalle, 2012)

Real Estate projects, typically, require a higher scale of funding and tend to be riskier than

housing funding. With real estate development finance competing with other property markets

such as housing or even other areas of lending, the funds for commercial development finance

dried up from every source.

In Queensland, for example, there were approximately 44 firms that provided credit for

development finance. This number shrunk to six, following the Global Financial Crisis. As the

debt markets closed, fearing a freefall in asset prices, the Australian Government proposed the

Australian Business Investment Plan. For this plan, the Australian Government, partnered with

the Big Four banks in Australia for $4 billion worth of debt refinancing, in order to prevents

further wrote offs and write downs. However, the capital markets were tentatively re-opened and

the plan was rejected. In spite of the re-opening of capital market, funding remained scarce in

the absence of the capital market, given that plenty of sources had exited the market. (Housing

supply in Australia : the impact of the availability of development finance , 2010) The exit of

sources founding ensured that the capital scarcity for commercial property market continued

beyond the crisis.

At the time, the withdrawal of funding left a deficit in the availibility development finance in the

market. Another impact of this crisis was the exit of mortgage funds in the market, leaving the

commercial real estate market to be crowded by banks. In case of banks, various sources of

demand compete for funding such as business loans, housing loan etc. as opposed to mortgage

loans that are specifically meant for mortgage lending. In 2010, banks were still reducing their

exposure to commercial real estate funding. Thus, many real estate developers were struggling to

obtain funds. (Jones Lang LaSalle, 2012)

This situation has changed in the recent times, as there has been a boom in investment in

commercial property in Sydney, given the availability of liquidity. (Cushman and Wakefield

Capital Markets)

Australian banks relied heavily on international funding. The liquidity crisis caused by the

financial crisis made borrowing funds and gaining investors from the international markets more

expensive. (Jones Lang LaSalle, 2012)

Real Estate projects, typically, require a higher scale of funding and tend to be riskier than

housing funding. With real estate development finance competing with other property markets

such as housing or even other areas of lending, the funds for commercial development finance

dried up from every source.

In Queensland, for example, there were approximately 44 firms that provided credit for

development finance. This number shrunk to six, following the Global Financial Crisis. As the

debt markets closed, fearing a freefall in asset prices, the Australian Government proposed the

Australian Business Investment Plan. For this plan, the Australian Government, partnered with

the Big Four banks in Australia for $4 billion worth of debt refinancing, in order to prevents

further wrote offs and write downs. However, the capital markets were tentatively re-opened and

the plan was rejected. In spite of the re-opening of capital market, funding remained scarce in

the absence of the capital market, given that plenty of sources had exited the market. (Housing

supply in Australia : the impact of the availability of development finance , 2010) The exit of

sources founding ensured that the capital scarcity for commercial property market continued

beyond the crisis.

At the time, the withdrawal of funding left a deficit in the availibility development finance in the

market. Another impact of this crisis was the exit of mortgage funds in the market, leaving the

commercial real estate market to be crowded by banks. In case of banks, various sources of

demand compete for funding such as business loans, housing loan etc. as opposed to mortgage

loans that are specifically meant for mortgage lending. In 2010, banks were still reducing their

exposure to commercial real estate funding. Thus, many real estate developers were struggling to

obtain funds. (Jones Lang LaSalle, 2012)

This situation has changed in the recent times, as there has been a boom in investment in

commercial property in Sydney, given the availability of liquidity. (Cushman and Wakefield

Capital Markets)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

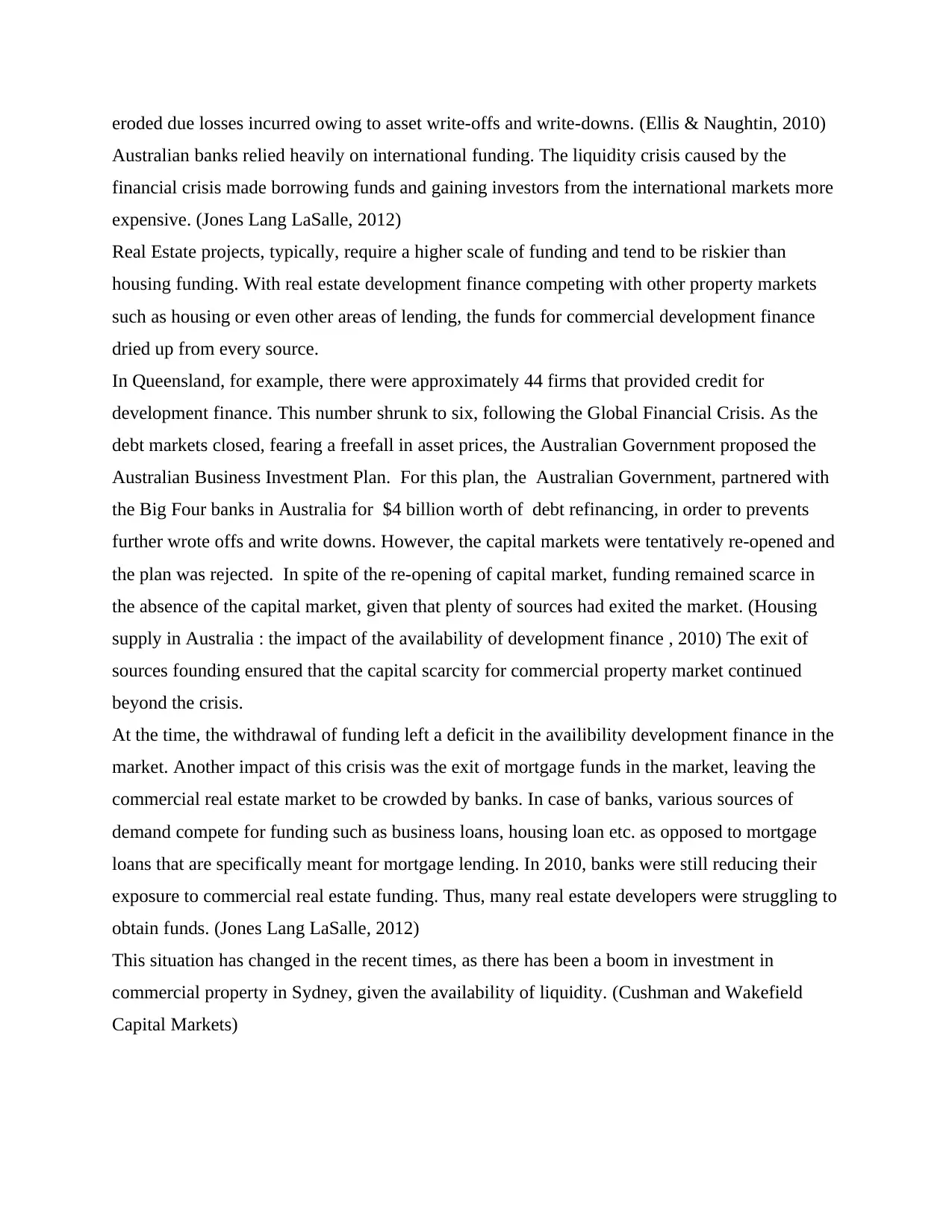

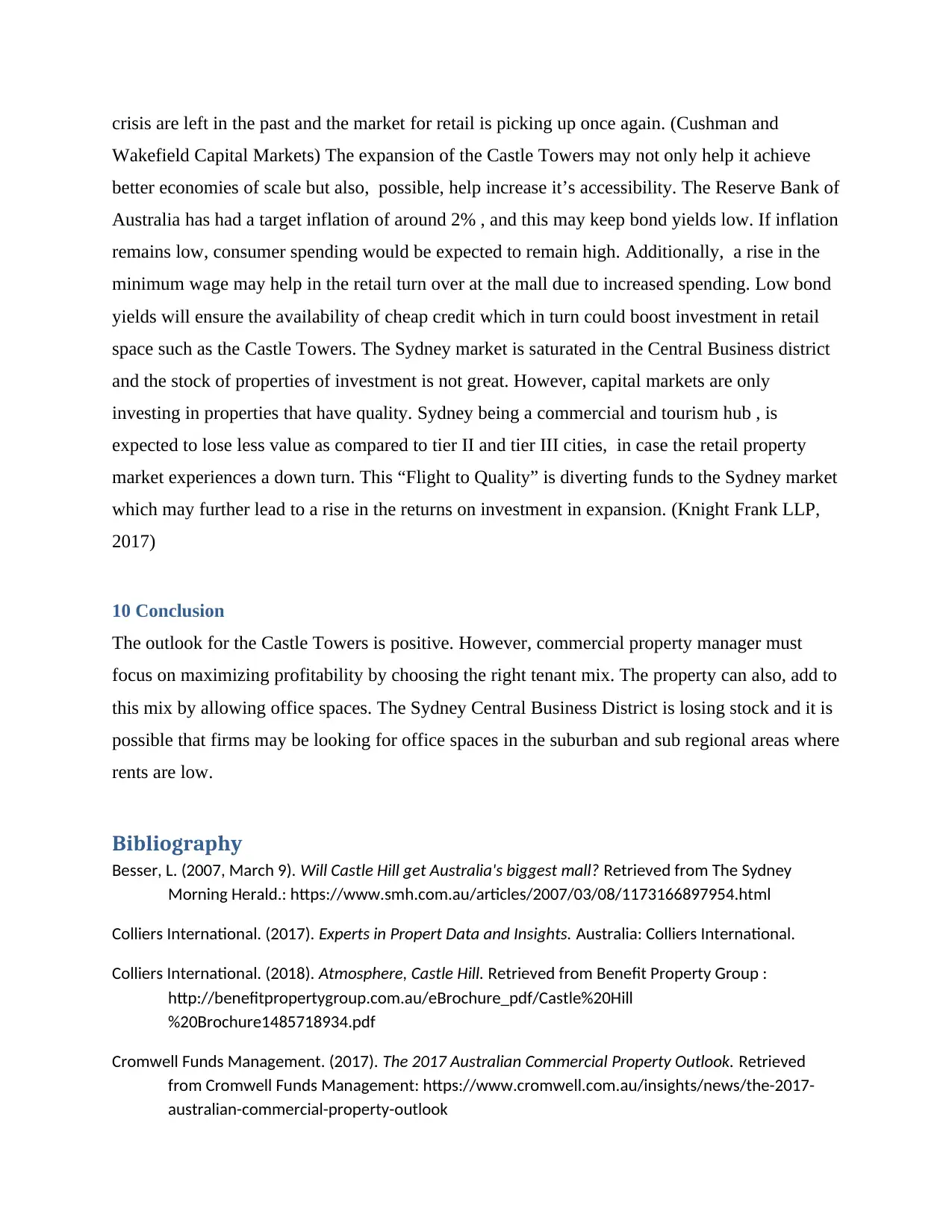

6. Australia Economy: Lending Rates and Wages

The economy of Australia will shape the conditions of demand and supply of retail space within

the country. Low lending rates would encourage investment in the commercial space sector

while high GDP forecast will ensure that consumption will remain high, thereby, increasing the

demand for retail space.

1990

1993

1996

1999

2002

2005

2008

2011

2014

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Cash Rates for Australia Since

1990

Cash Rates for

Australia Since 1...

Graph 1 : Cash rates for Australia Since 1990

Source: (Reserve Bank of Australia, 2017)

As seen in the graph above, the lending rates of the Reserve Bank of Australia have declined

continuously since 1990 and have hit an all time low in 2016. This makes investment in the

property more attractive due the availability of cheap credit.

The economy of Australia will shape the conditions of demand and supply of retail space within

the country. Low lending rates would encourage investment in the commercial space sector

while high GDP forecast will ensure that consumption will remain high, thereby, increasing the

demand for retail space.

1990

1993

1996

1999

2002

2005

2008

2011

2014

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Cash Rates for Australia Since

1990

Cash Rates for

Australia Since 1...

Graph 1 : Cash rates for Australia Since 1990

Source: (Reserve Bank of Australia, 2017)

As seen in the graph above, the lending rates of the Reserve Bank of Australia have declined

continuously since 1990 and have hit an all time low in 2016. This makes investment in the

property more attractive due the availability of cheap credit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Mar-2007

Feb-2008

Jan-2009

Dec-2009

Nov-2010

Oct-2011

Sep-2012

Aug-2013

Jul-2014

Jun-2015

May-2016

Apr-2017

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Year Ended Wage Growth in

Australia

Year Ended Wage Growth

in Australia

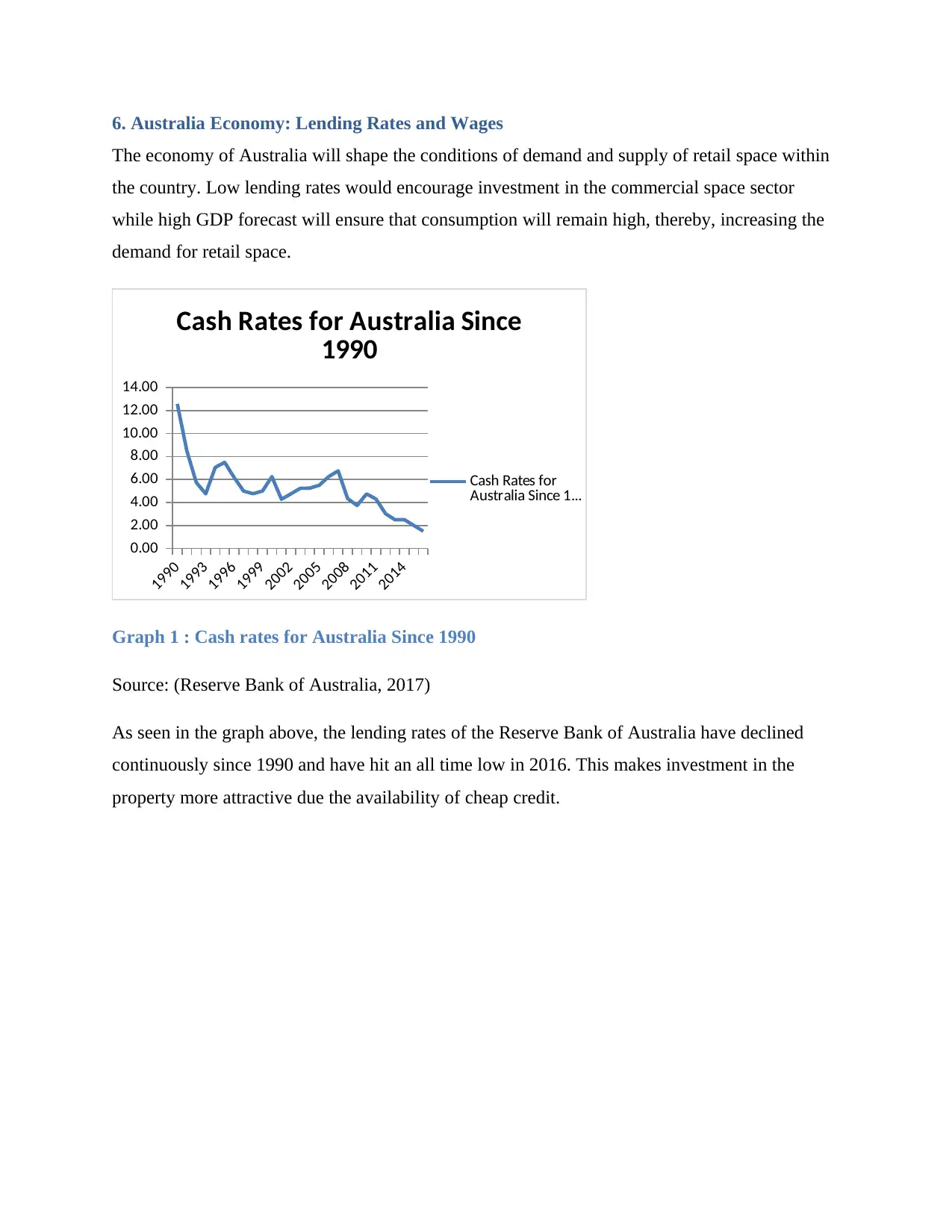

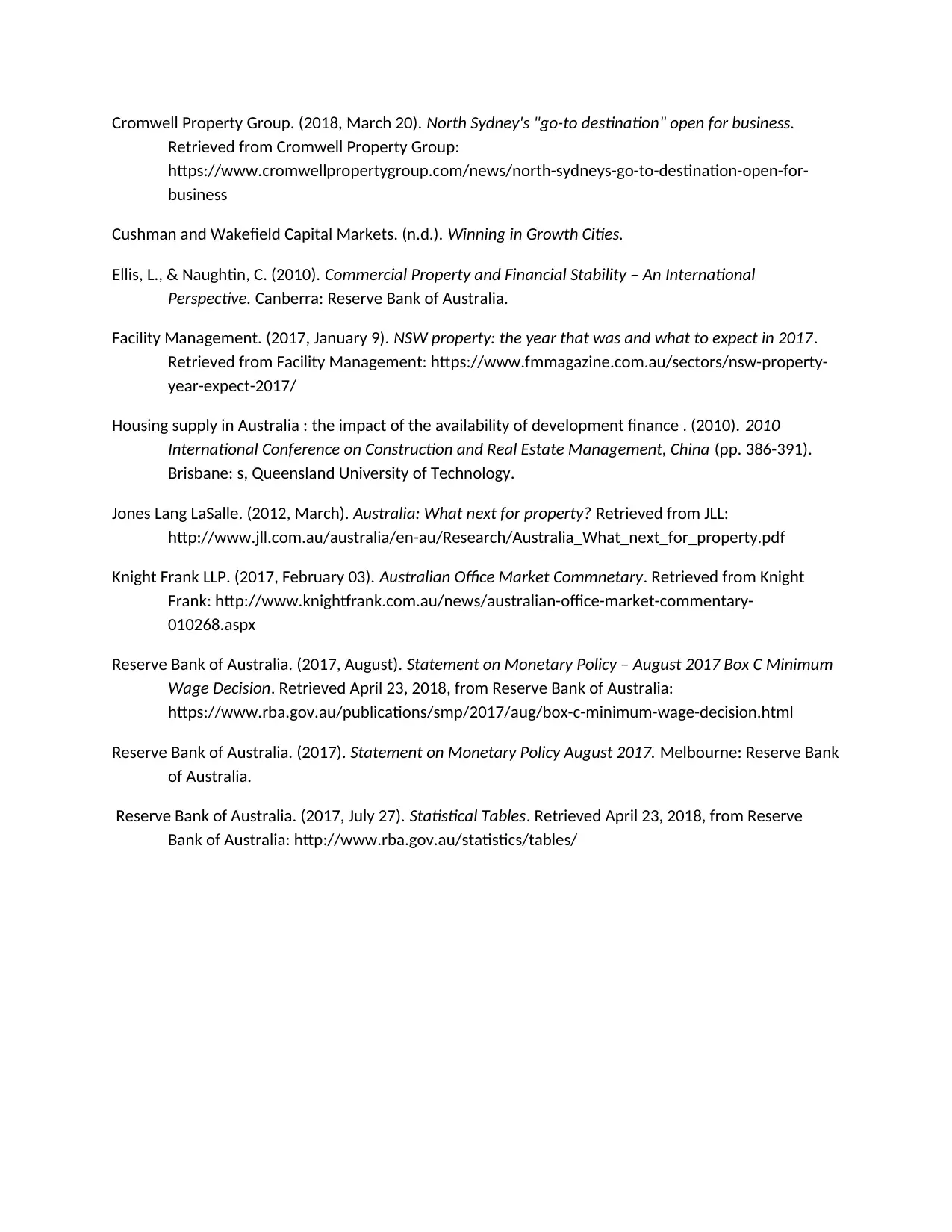

Graph 2 Year Ended Wage Growth in Australia.

Source (Reserve Bank of Australia, 2017)

Australian wage rates have been stagnant as the rate of growth has continuously slowed since

2007. Despite this, retail has seen an increase in consumption. Some if this could be accorded to

the increase in population while a part of the increase may be due to the fact that inflation rates

in Australia have remained remarkably low following the Global Financial Crisis, which has led

to an availability of cheap credit for the consumers to spend on. However, if the wages remain

further stagnant, then retail consumption may slow down. However, forecasts for the future

expect the domestic consumption to remain high, especially since the Australian economy is

expected to grow at 3%. A proposed rise in the minimum wage under the Fair Wages Act will

further boost the domestic spending (Reserve Bank of Australia, 2017)

7. The Expansion of Castle Hill Towers and Future Deveopment

The Castle Towers project, therefore started the process of expansion in 2015, given the changed

outlook and the easy availability of funds.

The expansion will increase the total floor space to 193, 458 square metres. A total of 7959 car

park spaces will be provided and additional space for motorcycles and bicycles. The

development will make it possible to link the property to the Castle Hill Railway Station

increasing the accessibility of the property. The under works completely automated rapid rail

Feb-2008

Jan-2009

Dec-2009

Nov-2010

Oct-2011

Sep-2012

Aug-2013

Jul-2014

Jun-2015

May-2016

Apr-2017

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Year Ended Wage Growth in

Australia

Year Ended Wage Growth

in Australia

Graph 2 Year Ended Wage Growth in Australia.

Source (Reserve Bank of Australia, 2017)

Australian wage rates have been stagnant as the rate of growth has continuously slowed since

2007. Despite this, retail has seen an increase in consumption. Some if this could be accorded to

the increase in population while a part of the increase may be due to the fact that inflation rates

in Australia have remained remarkably low following the Global Financial Crisis, which has led

to an availability of cheap credit for the consumers to spend on. However, if the wages remain

further stagnant, then retail consumption may slow down. However, forecasts for the future

expect the domestic consumption to remain high, especially since the Australian economy is

expected to grow at 3%. A proposed rise in the minimum wage under the Fair Wages Act will

further boost the domestic spending (Reserve Bank of Australia, 2017)

7. The Expansion of Castle Hill Towers and Future Deveopment

The Castle Towers project, therefore started the process of expansion in 2015, given the changed

outlook and the easy availability of funds.

The expansion will increase the total floor space to 193, 458 square metres. A total of 7959 car

park spaces will be provided and additional space for motorcycles and bicycles. The

development will make it possible to link the property to the Castle Hill Railway Station

increasing the accessibility of the property. The under works completely automated rapid rail

system Au $8.3 billion North West Rail Link is also, expected to increase the accessibility of the

region. It is expected to be Australia’s largest mass transit infrastructure project and a priority

project announced by the New South Wales Government. It will be the first fully-automated

rapid transit rail system in Australia. The project will include a 23km railway link Cudgegong

Road at Rouse Hill to Epping. The project includes eight new train stations along the line,

including the Castle Hill Station. This will increase the accessibility of Castle Hill station with

respect to the surround residential areas. (Colliers International, 2018)

8 Competition and Coping Up Strategies

It is expected that there will be competition from online markets. However, the growth rates in

the rentals of malls suggest otherwise. The outlook still remains positive for shopping centers,

although data suggests that shopping centers that focus more on dining, hospitality and leisure

activities like gaming would expect to fare better.

There are plenty of other shopping centers that are cropping up in the periphery of the mall.

Plenty of these are backed by capital investors with deep pockets:

The Home Hub Castle Hill is an example of such a competition. The mall has similar facilities to

the Castle Towers and is likely to take away from the customers at Castle Towers.

There is still rising liquidity and low interest rates. Hence, liquidity crunch is not expected soon.

Retail spending is Sydney is expected to be strong, especially is the given region of Castle

Towers. Australia has, a after a long time, witnessed a GDP forecast of approximately 3%. Some

of this GDP growth is expected to have returns for the real estate sector. (Cromwell Funds

Management, 2017) The hub has a floor space of over 10,000square meters and 1213 car parks.

Although it is a much smaller estate, the mall is competitive and sees plenty of foot fall.

9 Outlook for the Future

The Castle Towers is surrounded by residential areas and its main customers are expected to be

working professional and some university students. The availability of a professional talent pool

with high spending powers in the vicinity, ensures that Castle Towers are in fact, a viable

commercial property and will remain so. Apparently, the negative effects of the global financial

region. It is expected to be Australia’s largest mass transit infrastructure project and a priority

project announced by the New South Wales Government. It will be the first fully-automated

rapid transit rail system in Australia. The project will include a 23km railway link Cudgegong

Road at Rouse Hill to Epping. The project includes eight new train stations along the line,

including the Castle Hill Station. This will increase the accessibility of Castle Hill station with

respect to the surround residential areas. (Colliers International, 2018)

8 Competition and Coping Up Strategies

It is expected that there will be competition from online markets. However, the growth rates in

the rentals of malls suggest otherwise. The outlook still remains positive for shopping centers,

although data suggests that shopping centers that focus more on dining, hospitality and leisure

activities like gaming would expect to fare better.

There are plenty of other shopping centers that are cropping up in the periphery of the mall.

Plenty of these are backed by capital investors with deep pockets:

The Home Hub Castle Hill is an example of such a competition. The mall has similar facilities to

the Castle Towers and is likely to take away from the customers at Castle Towers.

There is still rising liquidity and low interest rates. Hence, liquidity crunch is not expected soon.

Retail spending is Sydney is expected to be strong, especially is the given region of Castle

Towers. Australia has, a after a long time, witnessed a GDP forecast of approximately 3%. Some

of this GDP growth is expected to have returns for the real estate sector. (Cromwell Funds

Management, 2017) The hub has a floor space of over 10,000square meters and 1213 car parks.

Although it is a much smaller estate, the mall is competitive and sees plenty of foot fall.

9 Outlook for the Future

The Castle Towers is surrounded by residential areas and its main customers are expected to be

working professional and some university students. The availability of a professional talent pool

with high spending powers in the vicinity, ensures that Castle Towers are in fact, a viable

commercial property and will remain so. Apparently, the negative effects of the global financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

crisis are left in the past and the market for retail is picking up once again. (Cushman and

Wakefield Capital Markets) The expansion of the Castle Towers may not only help it achieve

better economies of scale but also, possible, help increase it’s accessibility. The Reserve Bank of

Australia has had a target inflation of around 2% , and this may keep bond yields low. If inflation

remains low, consumer spending would be expected to remain high. Additionally, a rise in the

minimum wage may help in the retail turn over at the mall due to increased spending. Low bond

yields will ensure the availability of cheap credit which in turn could boost investment in retail

space such as the Castle Towers. The Sydney market is saturated in the Central Business district

and the stock of properties of investment is not great. However, capital markets are only

investing in properties that have quality. Sydney being a commercial and tourism hub , is

expected to lose less value as compared to tier II and tier III cities, in case the retail property

market experiences a down turn. This “Flight to Quality” is diverting funds to the Sydney market

which may further lead to a rise in the returns on investment in expansion. (Knight Frank LLP,

2017)

10 Conclusion

The outlook for the Castle Towers is positive. However, commercial property manager must

focus on maximizing profitability by choosing the right tenant mix. The property can also, add to

this mix by allowing office spaces. The Sydney Central Business District is losing stock and it is

possible that firms may be looking for office spaces in the suburban and sub regional areas where

rents are low.

Bibliography

Besser, L. (2007, March 9). Will Castle Hill get Australia's biggest mall? Retrieved from The Sydney

Morning Herald.: https://www.smh.com.au/articles/2007/03/08/1173166897954.html

Colliers International. (2017). Experts in Propert Data and Insights. Australia: Colliers International.

Colliers International. (2018). Atmosphere, Castle Hill. Retrieved from Benefit Property Group :

http://benefitpropertygroup.com.au/eBrochure_pdf/Castle%20Hill

%20Brochure1485718934.pdf

Cromwell Funds Management. (2017). The 2017 Australian Commercial Property Outlook. Retrieved

from Cromwell Funds Management: https://www.cromwell.com.au/insights/news/the-2017-

australian-commercial-property-outlook

Wakefield Capital Markets) The expansion of the Castle Towers may not only help it achieve

better economies of scale but also, possible, help increase it’s accessibility. The Reserve Bank of

Australia has had a target inflation of around 2% , and this may keep bond yields low. If inflation

remains low, consumer spending would be expected to remain high. Additionally, a rise in the

minimum wage may help in the retail turn over at the mall due to increased spending. Low bond

yields will ensure the availability of cheap credit which in turn could boost investment in retail

space such as the Castle Towers. The Sydney market is saturated in the Central Business district

and the stock of properties of investment is not great. However, capital markets are only

investing in properties that have quality. Sydney being a commercial and tourism hub , is

expected to lose less value as compared to tier II and tier III cities, in case the retail property

market experiences a down turn. This “Flight to Quality” is diverting funds to the Sydney market

which may further lead to a rise in the returns on investment in expansion. (Knight Frank LLP,

2017)

10 Conclusion

The outlook for the Castle Towers is positive. However, commercial property manager must

focus on maximizing profitability by choosing the right tenant mix. The property can also, add to

this mix by allowing office spaces. The Sydney Central Business District is losing stock and it is

possible that firms may be looking for office spaces in the suburban and sub regional areas where

rents are low.

Bibliography

Besser, L. (2007, March 9). Will Castle Hill get Australia's biggest mall? Retrieved from The Sydney

Morning Herald.: https://www.smh.com.au/articles/2007/03/08/1173166897954.html

Colliers International. (2017). Experts in Propert Data and Insights. Australia: Colliers International.

Colliers International. (2018). Atmosphere, Castle Hill. Retrieved from Benefit Property Group :

http://benefitpropertygroup.com.au/eBrochure_pdf/Castle%20Hill

%20Brochure1485718934.pdf

Cromwell Funds Management. (2017). The 2017 Australian Commercial Property Outlook. Retrieved

from Cromwell Funds Management: https://www.cromwell.com.au/insights/news/the-2017-

australian-commercial-property-outlook

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cromwell Property Group. (2018, March 20). North Sydney's "go-to destination" open for business.

Retrieved from Cromwell Property Group:

https://www.cromwellpropertygroup.com/news/north-sydneys-go-to-destination-open-for-

business

Cushman and Wakefield Capital Markets. (n.d.). Winning in Growth Cities.

Ellis, L., & Naughtin, C. (2010). Commercial Property and Financial Stability – An International

Perspective. Canberra: Reserve Bank of Australia.

Facility Management. (2017, January 9). NSW property: the year that was and what to expect in 2017.

Retrieved from Facility Management: https://www.fmmagazine.com.au/sectors/nsw-property-

year-expect-2017/

Housing supply in Australia : the impact of the availability of development finance . (2010). 2010

International Conference on Construction and Real Estate Management, China (pp. 386-391).

Brisbane: s, Queensland University of Technology.

Jones Lang LaSalle. (2012, March). Australia: What next for property? Retrieved from JLL:

http://www.jll.com.au/australia/en-au/Research/Australia_What_next_for_property.pdf

Knight Frank LLP. (2017, February 03). Australian Office Market Commnetary. Retrieved from Knight

Frank: http://www.knightfrank.com.au/news/australian-office-market-commentary-

010268.aspx

Reserve Bank of Australia. (2017, August). Statement on Monetary Policy – August 2017 Box C Minimum

Wage Decision. Retrieved April 23, 2018, from Reserve Bank of Australia:

https://www.rba.gov.au/publications/smp/2017/aug/box-c-minimum-wage-decision.html

Reserve Bank of Australia. (2017). Statement on Monetary Policy August 2017. Melbourne: Reserve Bank

of Australia.

Reserve Bank of Australia. (2017, July 27). Statistical Tables. Retrieved April 23, 2018, from Reserve

Bank of Australia: http://www.rba.gov.au/statistics/tables/

Retrieved from Cromwell Property Group:

https://www.cromwellpropertygroup.com/news/north-sydneys-go-to-destination-open-for-

business

Cushman and Wakefield Capital Markets. (n.d.). Winning in Growth Cities.

Ellis, L., & Naughtin, C. (2010). Commercial Property and Financial Stability – An International

Perspective. Canberra: Reserve Bank of Australia.

Facility Management. (2017, January 9). NSW property: the year that was and what to expect in 2017.

Retrieved from Facility Management: https://www.fmmagazine.com.au/sectors/nsw-property-

year-expect-2017/

Housing supply in Australia : the impact of the availability of development finance . (2010). 2010

International Conference on Construction and Real Estate Management, China (pp. 386-391).

Brisbane: s, Queensland University of Technology.

Jones Lang LaSalle. (2012, March). Australia: What next for property? Retrieved from JLL:

http://www.jll.com.au/australia/en-au/Research/Australia_What_next_for_property.pdf

Knight Frank LLP. (2017, February 03). Australian Office Market Commnetary. Retrieved from Knight

Frank: http://www.knightfrank.com.au/news/australian-office-market-commentary-

010268.aspx

Reserve Bank of Australia. (2017, August). Statement on Monetary Policy – August 2017 Box C Minimum

Wage Decision. Retrieved April 23, 2018, from Reserve Bank of Australia:

https://www.rba.gov.au/publications/smp/2017/aug/box-c-minimum-wage-decision.html

Reserve Bank of Australia. (2017). Statement on Monetary Policy August 2017. Melbourne: Reserve Bank

of Australia.

Reserve Bank of Australia. (2017, July 27). Statistical Tables. Retrieved April 23, 2018, from Reserve

Bank of Australia: http://www.rba.gov.au/statistics/tables/

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.