MBA403 Financial and Economic Interpretation Case Study Analysis

VerifiedAdded on 2022/10/02

|4

|1043

|27

Case Study

AI Summary

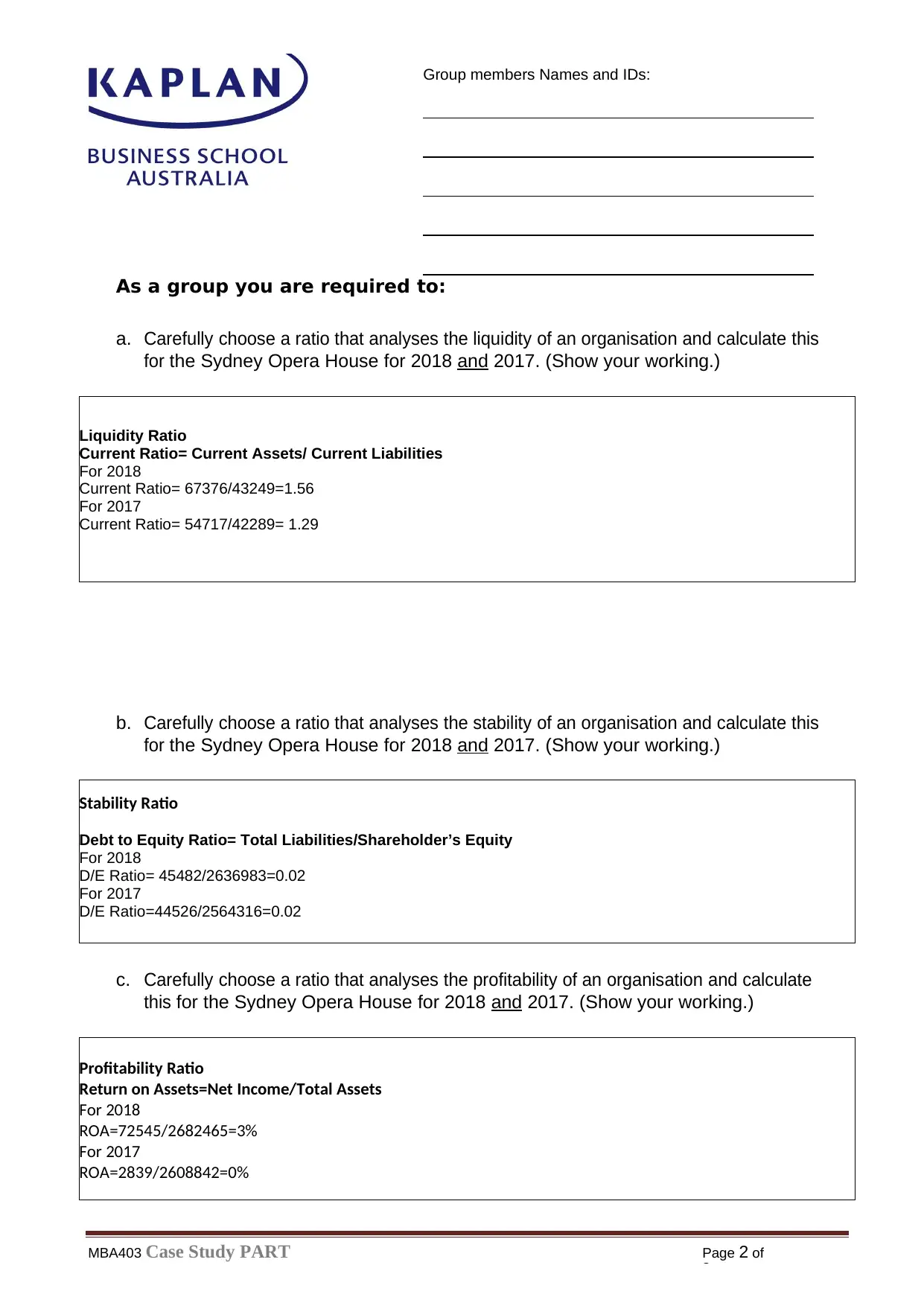

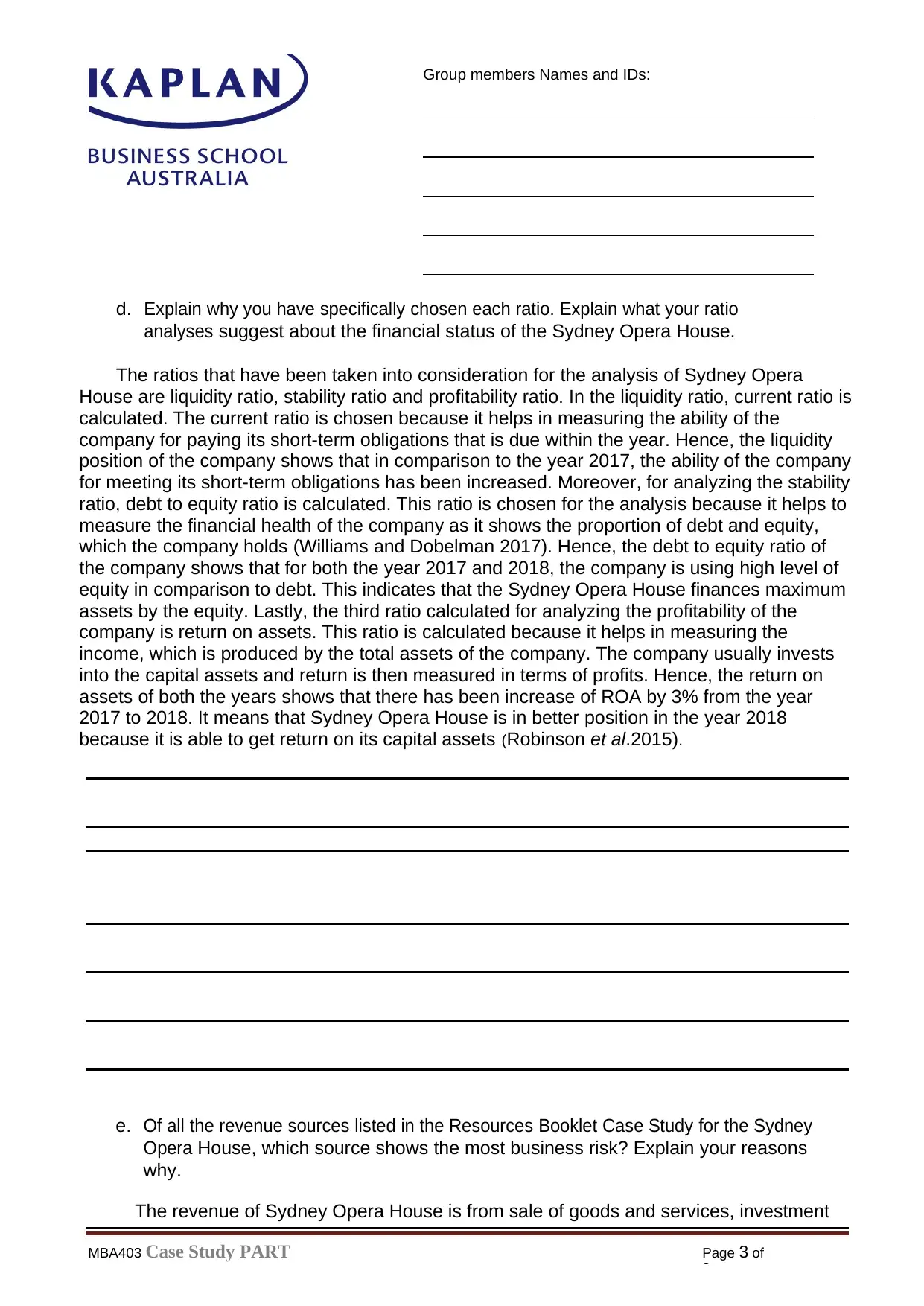

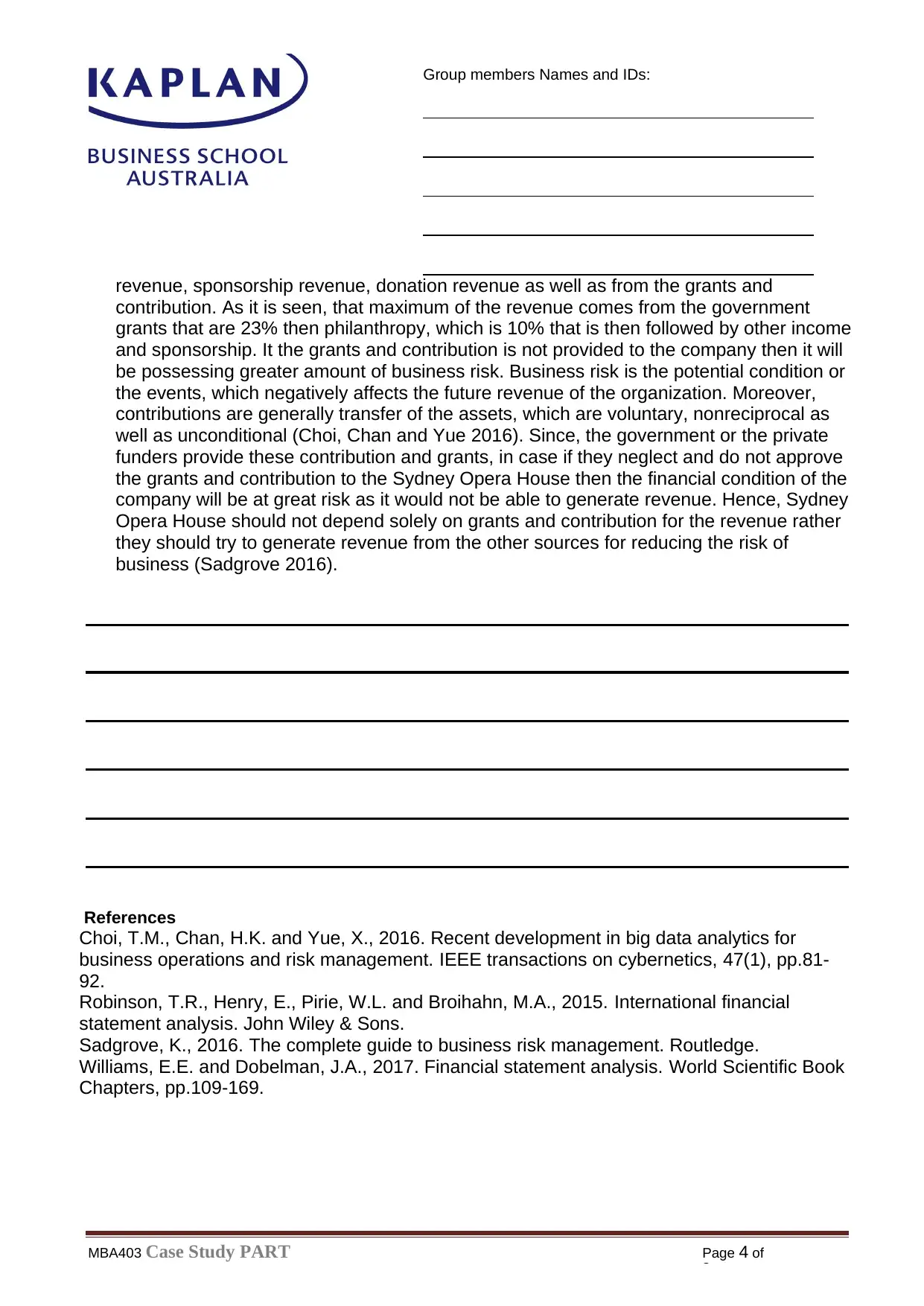

This case study analyzes the financial performance of the Sydney Opera House, focusing on the years 2017 and 2018. The analysis includes the calculation and interpretation of key financial ratios such as the current ratio (liquidity), debt-to-equity ratio (stability), and return on assets (profitability). The solution demonstrates the calculations, explains the choice of each ratio, and interprets the financial health of the organization based on the calculated values. Additionally, the case study identifies and explains the source of revenue that poses the most significant business risk to the Sydney Opera House, which is government grants and contributions. The student highlights the importance of diversifying revenue streams to mitigate this risk. The document also includes references to relevant financial literature used to support the analysis.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.