Syngenta: Strategic Financial Management and Investment Decisions

VerifiedAdded on 2023/06/18

|17

|5933

|201

Report

AI Summary

This report provides a comprehensive analysis of Syngenta's strategic financial management, covering various aspects such as sources of finance, ratio analysis for performance evaluation, potential investment decisions, and the impact of the global environment. It examines different sources of finance available to Syngenta, including retained earnings, debt capital, and equity capital, along with their associated risks. The report uses ratio analysis, including profitability and liquidity ratios, to assess Syngenta's financial performance and recommends improvements through new investments. It also evaluates potential investment decisions using payback period and accounting rate of return techniques. Furthermore, the report delves into the nature and types of costs incurred by Syngenta, appropriate costing techniques, the role of accounting in decision-making, risks involved in financial decisions, budgetary techniques, and investment evaluation techniques. The analysis concludes with recommendations for Syngenta to enhance its financial performance and manage risks effectively.

STRATEGIC FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1............................................................................................................................................3

1. Sources of finance available to Syngenta and associated risks...............................................3

2. Using ratios to analyse the performance of Syngenta.............................................................4

Recommendations on how new investment will improve the current financial performance of

Syngenta......................................................................................................................................6

3. Analysis of potential investment decisions and strategies......................................................6

4. Global environment decisions and strategies affecting Syngenta...........................................8

PART B..........................................................................................................................................10

TASK 1..........................................................................................................................................10

Nature and type of costs Syngenta and its impact on the company's financial position...........10

Appropriate costing techniques.................................................................................................11

Role of accounting to support decision making........................................................................11

Risk involve in financial decision making................................................................................13

Budgetary techniques................................................................................................................14

Investment evaluation techniques.............................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

PART 1............................................................................................................................................3

1. Sources of finance available to Syngenta and associated risks...............................................3

2. Using ratios to analyse the performance of Syngenta.............................................................4

Recommendations on how new investment will improve the current financial performance of

Syngenta......................................................................................................................................6

3. Analysis of potential investment decisions and strategies......................................................6

4. Global environment decisions and strategies affecting Syngenta...........................................8

PART B..........................................................................................................................................10

TASK 1..........................................................................................................................................10

Nature and type of costs Syngenta and its impact on the company's financial position...........10

Appropriate costing techniques.................................................................................................11

Role of accounting to support decision making........................................................................11

Risk involve in financial decision making................................................................................13

Budgetary techniques................................................................................................................14

Investment evaluation techniques.............................................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Financial management is defined as managing the financial resources associated with the

business venture and also to channelise the use of the respective financial resources in process to

maximise the business objectives. This report will talk about the different sources of finance

which company could use to mange its financial requirement in business. Performance of the

business will be discussed with the use of ratio analysis technique. Potential investment decision

will be discussed in respect to the organisation. Global environment and its impact over the

company will also discuss in this project. Furthermore, this report will discuss nature and type of

cost company is utilising in the business. Various costing technique will also be a part of

discussion. All different budgetary technique will be discussed under this project. Investment

evaluation technique will also be a part of discussion in this report.

MAIN BODY

PART 1

1. Sources of finance available to Syngenta and associated risks

Sources of finance for a concern are many but majorly company chooses to use debt, equity,

retained earnings, debentures and term loans for financing its expansion and growth purpose.

Syngenta has a need of long term sources to finance its Grangemouth expansion project. The

need of funds for the investment is identified as £150 million. The various sources of finance that

Syngenta could have used and their associated risks are explained as follows:

Retained earnings: This source of finance is available with the business internally which has

been generated through earning profit from year to year by selling their products and services.

The source is considered as a primary source of funding investment proposals (Tretyak and et.al.,

2020). There are no costs to the company for utilizing this source for financing their investments.

It gets created out of the profit remains after distributing dividends to the shareholders. Risk

involved in using retained earnings as a source of finance is that it deprived the existing

shareholders of the company from enjoying the benefits resulting from the actual earnings which

creates dissatisfaction among them and accordingly, the market value of the company's share

gets adversely affected.

Debt capital: Debt financing can be availed through external sources which can be for both short

term and long term. Generally, banks, financial institutions and individual who subscribes for the

Financial management is defined as managing the financial resources associated with the

business venture and also to channelise the use of the respective financial resources in process to

maximise the business objectives. This report will talk about the different sources of finance

which company could use to mange its financial requirement in business. Performance of the

business will be discussed with the use of ratio analysis technique. Potential investment decision

will be discussed in respect to the organisation. Global environment and its impact over the

company will also discuss in this project. Furthermore, this report will discuss nature and type of

cost company is utilising in the business. Various costing technique will also be a part of

discussion. All different budgetary technique will be discussed under this project. Investment

evaluation technique will also be a part of discussion in this report.

MAIN BODY

PART 1

1. Sources of finance available to Syngenta and associated risks

Sources of finance for a concern are many but majorly company chooses to use debt, equity,

retained earnings, debentures and term loans for financing its expansion and growth purpose.

Syngenta has a need of long term sources to finance its Grangemouth expansion project. The

need of funds for the investment is identified as £150 million. The various sources of finance that

Syngenta could have used and their associated risks are explained as follows:

Retained earnings: This source of finance is available with the business internally which has

been generated through earning profit from year to year by selling their products and services.

The source is considered as a primary source of funding investment proposals (Tretyak and et.al.,

2020). There are no costs to the company for utilizing this source for financing their investments.

It gets created out of the profit remains after distributing dividends to the shareholders. Risk

involved in using retained earnings as a source of finance is that it deprived the existing

shareholders of the company from enjoying the benefits resulting from the actual earnings which

creates dissatisfaction among them and accordingly, the market value of the company's share

gets adversely affected.

Debt capital: Debt financing can be availed through external sources which can be for both short

term and long term. Generally, banks, financial institutions and individual who subscribes for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company's debentures to provide debt capital (Mazouni, 2018). Debt capital can be availed at any

stage of the business through issuing debt securities such as debentures, promissory notes and

corporate bonds. Companies issuing debt instruments are called as borrowers as they are getting

funds in the form of cash for accomplishing their respective objectives. By using this source for

funding, companies need to pay back the principal amount along with the interest amount paid

regularly. In this way, there is cost to the company in choosing this source of finance in terms of

fixed rate of interest that is needed to be paid regularly (Kumar, 2017). Risk involved in sourcing

funds through debt securities is that company is under obligation to make payments of interest

and principal on time failing which leads to the bankruptcy and operation seizure for the

company. Therefore, a financial risk is present in this source of finance.

Equity capital: With the issue of equity shares and preference shares huge amount of funds can

be obtained and in return ownership stake has been provided to those subscribing for shares.

There is no requirement of making regular payments to the shareholders in the form of interest as

they got dividend payments when the company desires or make profits (Levchaev and Khezazna,

2020). Also, the principal amount of capital obtained is not necessary to be repaid in the

condition where the company's assets are not sufficient for making payments and thus they are

paid in last. The bad side of this source of finance is that whatever profit has been earned by the

company needs to be shared with the shareholders of the company. Risk involved in equity

financing is that there is an ownership loss when businesses use too much equity capital. The

control of the company also goes into the hands of shareholder and the investor owning huge

stake in the company can influence its operations.

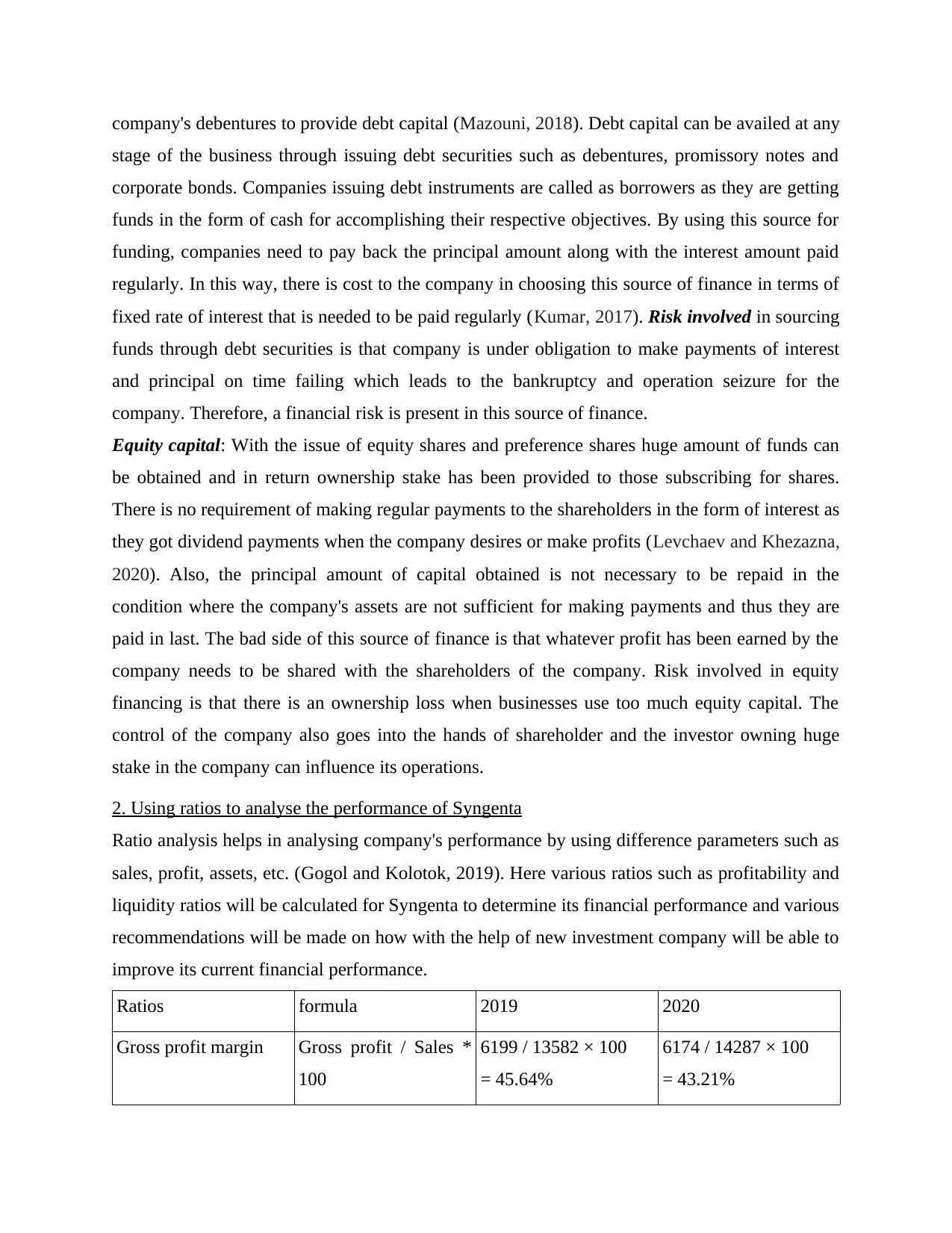

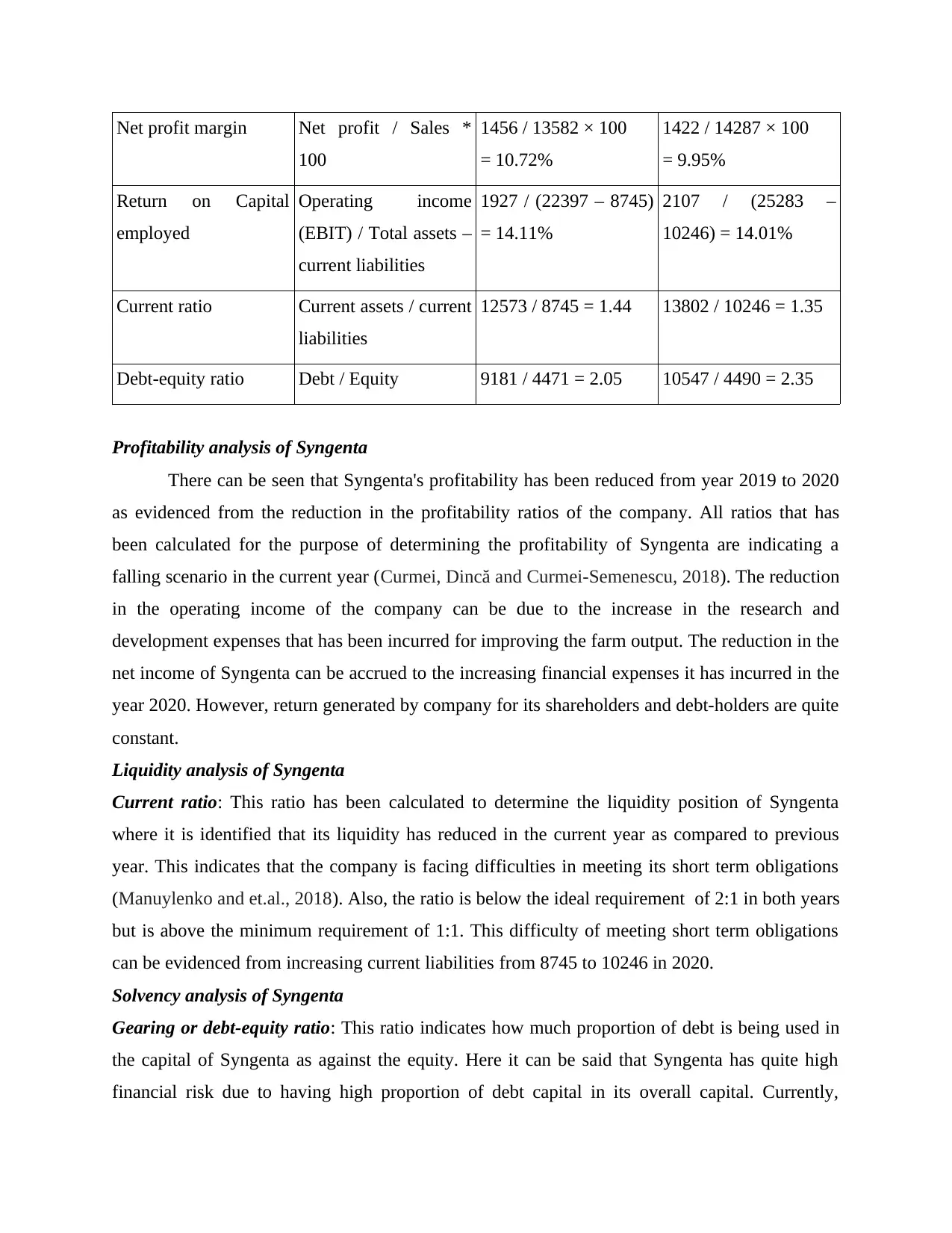

2. Using ratios to analyse the performance of Syngenta

Ratio analysis helps in analysing company's performance by using difference parameters such as

sales, profit, assets, etc. (Gogol and Kolotok, 2019). Here various ratios such as profitability and

liquidity ratios will be calculated for Syngenta to determine its financial performance and various

recommendations will be made on how with the help of new investment company will be able to

improve its current financial performance.

Ratios formula 2019 2020

Gross profit margin Gross profit / Sales *

100

6199 / 13582 × 100

= 45.64%

6174 / 14287 × 100

= 43.21%

stage of the business through issuing debt securities such as debentures, promissory notes and

corporate bonds. Companies issuing debt instruments are called as borrowers as they are getting

funds in the form of cash for accomplishing their respective objectives. By using this source for

funding, companies need to pay back the principal amount along with the interest amount paid

regularly. In this way, there is cost to the company in choosing this source of finance in terms of

fixed rate of interest that is needed to be paid regularly (Kumar, 2017). Risk involved in sourcing

funds through debt securities is that company is under obligation to make payments of interest

and principal on time failing which leads to the bankruptcy and operation seizure for the

company. Therefore, a financial risk is present in this source of finance.

Equity capital: With the issue of equity shares and preference shares huge amount of funds can

be obtained and in return ownership stake has been provided to those subscribing for shares.

There is no requirement of making regular payments to the shareholders in the form of interest as

they got dividend payments when the company desires or make profits (Levchaev and Khezazna,

2020). Also, the principal amount of capital obtained is not necessary to be repaid in the

condition where the company's assets are not sufficient for making payments and thus they are

paid in last. The bad side of this source of finance is that whatever profit has been earned by the

company needs to be shared with the shareholders of the company. Risk involved in equity

financing is that there is an ownership loss when businesses use too much equity capital. The

control of the company also goes into the hands of shareholder and the investor owning huge

stake in the company can influence its operations.

2. Using ratios to analyse the performance of Syngenta

Ratio analysis helps in analysing company's performance by using difference parameters such as

sales, profit, assets, etc. (Gogol and Kolotok, 2019). Here various ratios such as profitability and

liquidity ratios will be calculated for Syngenta to determine its financial performance and various

recommendations will be made on how with the help of new investment company will be able to

improve its current financial performance.

Ratios formula 2019 2020

Gross profit margin Gross profit / Sales *

100

6199 / 13582 × 100

= 45.64%

6174 / 14287 × 100

= 43.21%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net profit margin Net profit / Sales *

100

1456 / 13582 × 100

= 10.72%

1422 / 14287 × 100

= 9.95%

Return on Capital

employed

Operating income

(EBIT) / Total assets –

current liabilities

1927 / (22397 – 8745)

= 14.11%

2107 / (25283 –

10246) = 14.01%

Current ratio Current assets / current

liabilities

12573 / 8745 = 1.44 13802 / 10246 = 1.35

Debt-equity ratio Debt / Equity 9181 / 4471 = 2.05 10547 / 4490 = 2.35

Profitability analysis of Syngenta

There can be seen that Syngenta's profitability has been reduced from year 2019 to 2020

as evidenced from the reduction in the profitability ratios of the company. All ratios that has

been calculated for the purpose of determining the profitability of Syngenta are indicating a

falling scenario in the current year (Curmei, Dincă and Curmei-Semenescu, 2018). The reduction

in the operating income of the company can be due to the increase in the research and

development expenses that has been incurred for improving the farm output. The reduction in the

net income of Syngenta can be accrued to the increasing financial expenses it has incurred in the

year 2020. However, return generated by company for its shareholders and debt-holders are quite

constant.

Liquidity analysis of Syngenta

Current ratio: This ratio has been calculated to determine the liquidity position of Syngenta

where it is identified that its liquidity has reduced in the current year as compared to previous

year. This indicates that the company is facing difficulties in meeting its short term obligations

(Manuylenko and et.al., 2018). Also, the ratio is below the ideal requirement of 2:1 in both years

but is above the minimum requirement of 1:1. This difficulty of meeting short term obligations

can be evidenced from increasing current liabilities from 8745 to 10246 in 2020.

Solvency analysis of Syngenta

Gearing or debt-equity ratio: This ratio indicates how much proportion of debt is being used in

the capital of Syngenta as against the equity. Here it can be said that Syngenta has quite high

financial risk due to having high proportion of debt capital in its overall capital. Currently,

100

1456 / 13582 × 100

= 10.72%

1422 / 14287 × 100

= 9.95%

Return on Capital

employed

Operating income

(EBIT) / Total assets –

current liabilities

1927 / (22397 – 8745)

= 14.11%

2107 / (25283 –

10246) = 14.01%

Current ratio Current assets / current

liabilities

12573 / 8745 = 1.44 13802 / 10246 = 1.35

Debt-equity ratio Debt / Equity 9181 / 4471 = 2.05 10547 / 4490 = 2.35

Profitability analysis of Syngenta

There can be seen that Syngenta's profitability has been reduced from year 2019 to 2020

as evidenced from the reduction in the profitability ratios of the company. All ratios that has

been calculated for the purpose of determining the profitability of Syngenta are indicating a

falling scenario in the current year (Curmei, Dincă and Curmei-Semenescu, 2018). The reduction

in the operating income of the company can be due to the increase in the research and

development expenses that has been incurred for improving the farm output. The reduction in the

net income of Syngenta can be accrued to the increasing financial expenses it has incurred in the

year 2020. However, return generated by company for its shareholders and debt-holders are quite

constant.

Liquidity analysis of Syngenta

Current ratio: This ratio has been calculated to determine the liquidity position of Syngenta

where it is identified that its liquidity has reduced in the current year as compared to previous

year. This indicates that the company is facing difficulties in meeting its short term obligations

(Manuylenko and et.al., 2018). Also, the ratio is below the ideal requirement of 2:1 in both years

but is above the minimum requirement of 1:1. This difficulty of meeting short term obligations

can be evidenced from increasing current liabilities from 8745 to 10246 in 2020.

Solvency analysis of Syngenta

Gearing or debt-equity ratio: This ratio indicates how much proportion of debt is being used in

the capital of Syngenta as against the equity. Here it can be said that Syngenta has quite high

financial risk due to having high proportion of debt capital in its overall capital. Currently,

company has 2.35 debt-equity ratio which has increased from 2.05 which is higher than the ideal

ratio of 1:1. Accordingly, Syngenta is facing high financial risk (Samygin and et.al., 2019).

Recommendations on how new investment will improve the current financial performance of

Syngenta

As there is a positive net cash flow resulting from the new investment indicating the net

income that could be earned from this proposed expansion in all the upcoming years, so

the profitability of Syngenta would get improved. Also, the expenses are just 50% of the

sales that means there is a 50% profitability which would definitely be helpful in

increasing current profitability level (Gachuhi and Awuor, 2019).

Positive cash flows from the new investment that Syngenta is planning to make will be

helpful in liquidity position of the company and accordingly, ideal requirement can be

met. Expenses being just 50% indicates that the remaining 50% gets added to the

liquidity of the company that helps it in meeting its short term obligations on time.

Currently, gearing ratio of the company is too much high indicating high financial risk

for Syngenta (Alhusseinawi, 2017). So it would be recommended to the management that

it should go for making additional investment of £150 million through equity financing

which would result in lower debt-equity ratio and accordingly, financial risk of the

company will get reduced. Also, from the books of the company it has been identified

that it has huge amount of $3427 million in its balance sheet which can be used for the

purpose of making new investment which results in no additional cost for the company

and the debt-equity ratio will also get improved.

3. Analysis of potential investment decisions and strategies

To analyse various investment opportunities, there are many techniques available to evaluate

whether the investment decision and strategies framed are financially viable and the investment

is worthwhile or not. The two techniques that will be used here to evaluate the performance of

investment made in the Grangemouth expansion project are payback period method and

accounting rate of return technique.

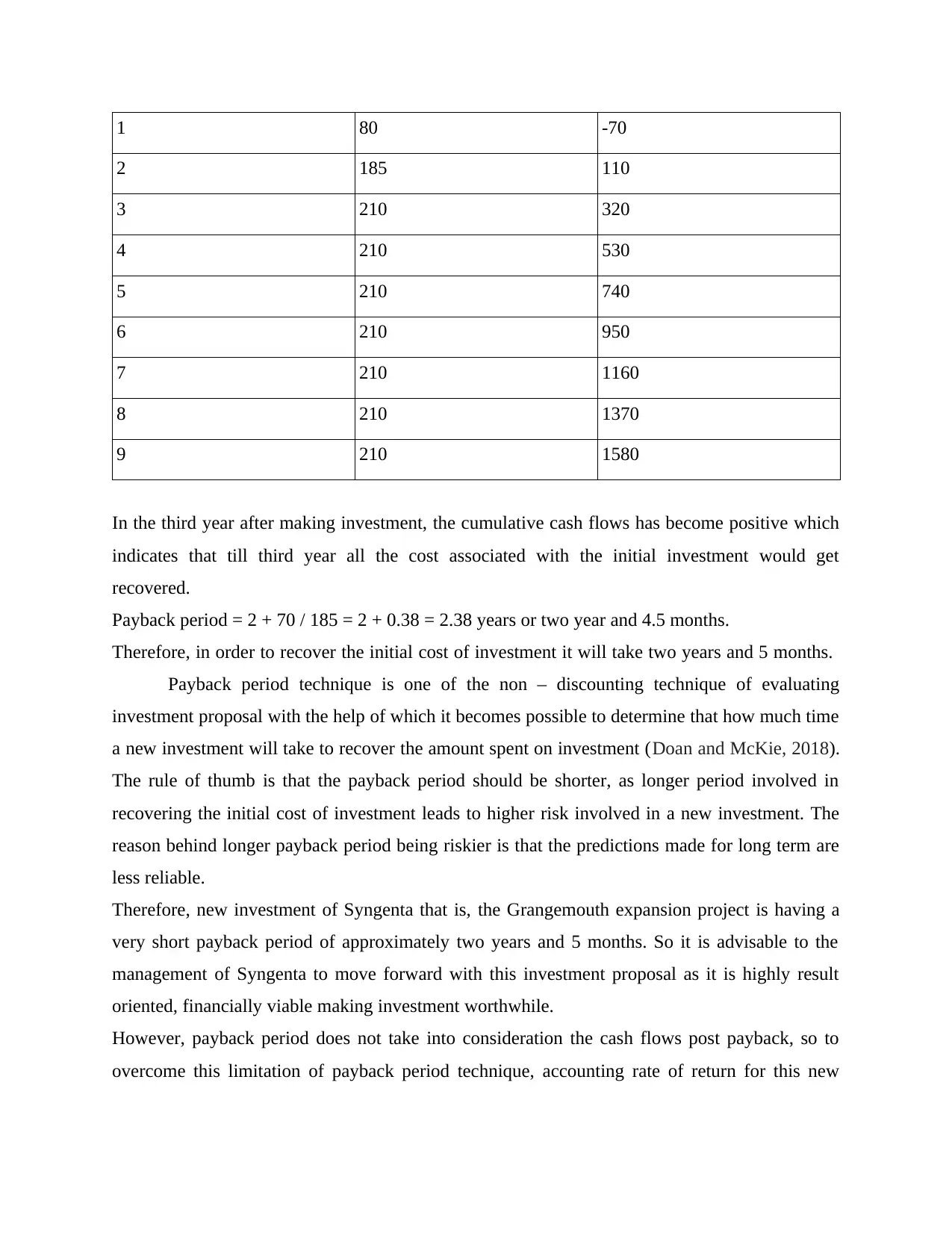

Calculation of payback period for the Grangemouth expansion project

Year Net cash flows Cumulative cash flows

0 -150 -150

ratio of 1:1. Accordingly, Syngenta is facing high financial risk (Samygin and et.al., 2019).

Recommendations on how new investment will improve the current financial performance of

Syngenta

As there is a positive net cash flow resulting from the new investment indicating the net

income that could be earned from this proposed expansion in all the upcoming years, so

the profitability of Syngenta would get improved. Also, the expenses are just 50% of the

sales that means there is a 50% profitability which would definitely be helpful in

increasing current profitability level (Gachuhi and Awuor, 2019).

Positive cash flows from the new investment that Syngenta is planning to make will be

helpful in liquidity position of the company and accordingly, ideal requirement can be

met. Expenses being just 50% indicates that the remaining 50% gets added to the

liquidity of the company that helps it in meeting its short term obligations on time.

Currently, gearing ratio of the company is too much high indicating high financial risk

for Syngenta (Alhusseinawi, 2017). So it would be recommended to the management that

it should go for making additional investment of £150 million through equity financing

which would result in lower debt-equity ratio and accordingly, financial risk of the

company will get reduced. Also, from the books of the company it has been identified

that it has huge amount of $3427 million in its balance sheet which can be used for the

purpose of making new investment which results in no additional cost for the company

and the debt-equity ratio will also get improved.

3. Analysis of potential investment decisions and strategies

To analyse various investment opportunities, there are many techniques available to evaluate

whether the investment decision and strategies framed are financially viable and the investment

is worthwhile or not. The two techniques that will be used here to evaluate the performance of

investment made in the Grangemouth expansion project are payback period method and

accounting rate of return technique.

Calculation of payback period for the Grangemouth expansion project

Year Net cash flows Cumulative cash flows

0 -150 -150

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 80 -70

2 185 110

3 210 320

4 210 530

5 210 740

6 210 950

7 210 1160

8 210 1370

9 210 1580

In the third year after making investment, the cumulative cash flows has become positive which

indicates that till third year all the cost associated with the initial investment would get

recovered.

Payback period = 2 + 70 / 185 = 2 + 0.38 = 2.38 years or two year and 4.5 months.

Therefore, in order to recover the initial cost of investment it will take two years and 5 months.

Payback period technique is one of the non – discounting technique of evaluating

investment proposal with the help of which it becomes possible to determine that how much time

a new investment will take to recover the amount spent on investment (Doan and McKie, 2018).

The rule of thumb is that the payback period should be shorter, as longer period involved in

recovering the initial cost of investment leads to higher risk involved in a new investment. The

reason behind longer payback period being riskier is that the predictions made for long term are

less reliable.

Therefore, new investment of Syngenta that is, the Grangemouth expansion project is having a

very short payback period of approximately two years and 5 months. So it is advisable to the

management of Syngenta to move forward with this investment proposal as it is highly result

oriented, financially viable making investment worthwhile.

However, payback period does not take into consideration the cash flows post payback, so to

overcome this limitation of payback period technique, accounting rate of return for this new

2 185 110

3 210 320

4 210 530

5 210 740

6 210 950

7 210 1160

8 210 1370

9 210 1580

In the third year after making investment, the cumulative cash flows has become positive which

indicates that till third year all the cost associated with the initial investment would get

recovered.

Payback period = 2 + 70 / 185 = 2 + 0.38 = 2.38 years or two year and 4.5 months.

Therefore, in order to recover the initial cost of investment it will take two years and 5 months.

Payback period technique is one of the non – discounting technique of evaluating

investment proposal with the help of which it becomes possible to determine that how much time

a new investment will take to recover the amount spent on investment (Doan and McKie, 2018).

The rule of thumb is that the payback period should be shorter, as longer period involved in

recovering the initial cost of investment leads to higher risk involved in a new investment. The

reason behind longer payback period being riskier is that the predictions made for long term are

less reliable.

Therefore, new investment of Syngenta that is, the Grangemouth expansion project is having a

very short payback period of approximately two years and 5 months. So it is advisable to the

management of Syngenta to move forward with this investment proposal as it is highly result

oriented, financially viable making investment worthwhile.

However, payback period does not take into consideration the cash flows post payback, so to

overcome this limitation of payback period technique, accounting rate of return for this new

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

investment that is, the Grangemouth expansion project will be calculated in the next section of

the report (Ivanova and et.al., 2019).

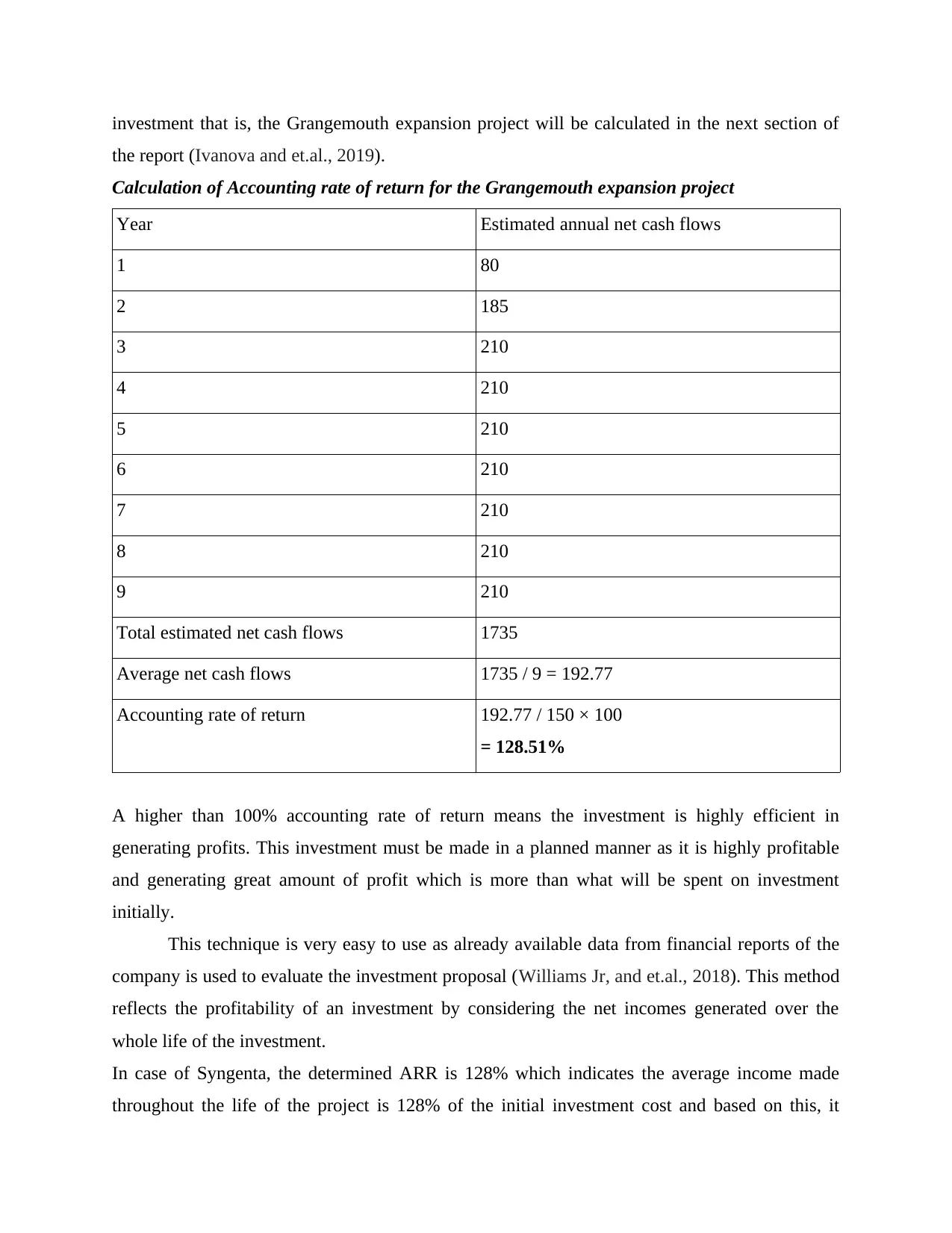

Calculation of Accounting rate of return for the Grangemouth expansion project

Year Estimated annual net cash flows

1 80

2 185

3 210

4 210

5 210

6 210

7 210

8 210

9 210

Total estimated net cash flows 1735

Average net cash flows 1735 / 9 = 192.77

Accounting rate of return 192.77 / 150 × 100

= 128.51%

A higher than 100% accounting rate of return means the investment is highly efficient in

generating profits. This investment must be made in a planned manner as it is highly profitable

and generating great amount of profit which is more than what will be spent on investment

initially.

This technique is very easy to use as already available data from financial reports of the

company is used to evaluate the investment proposal (Williams Jr, and et.al., 2018). This method

reflects the profitability of an investment by considering the net incomes generated over the

whole life of the investment.

In case of Syngenta, the determined ARR is 128% which indicates the average income made

throughout the life of the project is 128% of the initial investment cost and based on this, it

the report (Ivanova and et.al., 2019).

Calculation of Accounting rate of return for the Grangemouth expansion project

Year Estimated annual net cash flows

1 80

2 185

3 210

4 210

5 210

6 210

7 210

8 210

9 210

Total estimated net cash flows 1735

Average net cash flows 1735 / 9 = 192.77

Accounting rate of return 192.77 / 150 × 100

= 128.51%

A higher than 100% accounting rate of return means the investment is highly efficient in

generating profits. This investment must be made in a planned manner as it is highly profitable

and generating great amount of profit which is more than what will be spent on investment

initially.

This technique is very easy to use as already available data from financial reports of the

company is used to evaluate the investment proposal (Williams Jr, and et.al., 2018). This method

reflects the profitability of an investment by considering the net incomes generated over the

whole life of the investment.

In case of Syngenta, the determined ARR is 128% which indicates the average income made

throughout the life of the project is 128% of the initial investment cost and based on this, it

would be recommended to the management of Syngenta to must go for this investment

opportunity in order to enhance its profitability.

4. Global environment decisions and strategies affecting Syngenta

The global environment decisions and strategies can be assessed on the basis of six different

factors such as the following:

Political factors: Syngenta is operating in agricultural chemical industry in many countries of the

world (Janošková, Csikósová and Čulková, 2018). There are many decisions and strategies

associated with the political environment of different countries which may affect the company

such as the following:

Decisions related to labelling agricultural chemical products

Compulsory benefits for the employees

Taxation of agricultural chemical business affect the profitability of Syngenta

Pricing regulations applicable on agricultural chemical products

Intellectual property protection provided on new products developed will provide an

opportunity to Syngenta to get their new product patented. Interference of government in agricultural chemical industry will affect the operations of

Syngenta because it has to face difficulties in implementing new decisions and strategies.

Economic factors: Many decisions associated with interest rate, inflation rate and foreign

exchange rate may affect companies like Syngenta adversely. The company can utilize various

economic indicators such as growth rate of agricultural chemical industry to forecast their

organizational growth (Wiraeus and Creelman, 2019). Decisions and strategies that may affect

Syngenta are as follows:

Capital market efficiency affect the capital raising ability of Syngenta in local market.

Inflation rate will affect the pricing of the agricultural chemical product of Syngenta. Labour costs related regulations may affect the wages and salaries that Syngenta is

paying and accordingly, their profitability gets affected.

Social factors: There is a great impact of society's culture on the organizational culture in a given

environment. Beliefs and attitudes of individuals forming part of the organizational environment

affect Syngenta's marketers in understanding the customers of that market (Tretyak and et.al.,

2020). Also, they efforts towards designing marketing message for promoting their agricultural

chemical products. Decisions associated with this factor affecting Syngenta are as follows:

opportunity in order to enhance its profitability.

4. Global environment decisions and strategies affecting Syngenta

The global environment decisions and strategies can be assessed on the basis of six different

factors such as the following:

Political factors: Syngenta is operating in agricultural chemical industry in many countries of the

world (Janošková, Csikósová and Čulková, 2018). There are many decisions and strategies

associated with the political environment of different countries which may affect the company

such as the following:

Decisions related to labelling agricultural chemical products

Compulsory benefits for the employees

Taxation of agricultural chemical business affect the profitability of Syngenta

Pricing regulations applicable on agricultural chemical products

Intellectual property protection provided on new products developed will provide an

opportunity to Syngenta to get their new product patented. Interference of government in agricultural chemical industry will affect the operations of

Syngenta because it has to face difficulties in implementing new decisions and strategies.

Economic factors: Many decisions associated with interest rate, inflation rate and foreign

exchange rate may affect companies like Syngenta adversely. The company can utilize various

economic indicators such as growth rate of agricultural chemical industry to forecast their

organizational growth (Wiraeus and Creelman, 2019). Decisions and strategies that may affect

Syngenta are as follows:

Capital market efficiency affect the capital raising ability of Syngenta in local market.

Inflation rate will affect the pricing of the agricultural chemical product of Syngenta. Labour costs related regulations may affect the wages and salaries that Syngenta is

paying and accordingly, their profitability gets affected.

Social factors: There is a great impact of society's culture on the organizational culture in a given

environment. Beliefs and attitudes of individuals forming part of the organizational environment

affect Syngenta's marketers in understanding the customers of that market (Tretyak and et.al.,

2020). Also, they efforts towards designing marketing message for promoting their agricultural

chemical products. Decisions associated with this factor affecting Syngenta are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Being environmentally and health conscious affects Syngenta to ensure the quality of

their agricultural chemical products.

Society's attempt to encourage entrepreneurship Decisions for enhancing the skill level of the population.

Technological factors: This factor has the ability to affect the performance of Syngenta in great

way. With the decision of making current technology outdated, Syngenta may suffer a huge loss

and even lost its competitiveness in the market (Mazouni, 2018). Also, with the adoption of new

technology which is considered to be energy – wise and economically efficient, Syngenta can

become cost efficient and accordingly, their profitability gets enhanced. Likewise, in the given

case their production capacity has become inefficient to produce any more due to the

introduction of new technology in the agricultural chemical industry it becomes compulsory for

the company to make new investment. Decisions such as adoption of new technology by

Syngenta's competitors and its impact on product offering may greatly affect Syngenta.

Environmental factors: Norms and environmental standards applicable on agricultural chemical

industry have a huge impact on the operations of the company. With the applicability of new

laws and regulations such as associated with environmental pollution, air and water pollution,

recycling and waste management has a great impact on Syngenta policies and decisions (Kumar,

2017). Syngenta must take into consideration the society's attitude towards ecological products

and renewable energy while making new investment decisions.

Legal factors: Many countries are not having robust legal framework to protect the intellectual

property right of Syngenta. Therefore, its management needs to evaluate such country's market

before entering it because in the event of losses due to theft of their product design or any

intellectual property, they may not get the protective shield to safeguard their position in that

market (Gogol and Kolotok, 20190. Decisions that may affect Syngenta are changes in anti-trust

law in agricultural chemical industry, changes in intellectual property law, health and safety law

and consumer protection law.

their agricultural chemical products.

Society's attempt to encourage entrepreneurship Decisions for enhancing the skill level of the population.

Technological factors: This factor has the ability to affect the performance of Syngenta in great

way. With the decision of making current technology outdated, Syngenta may suffer a huge loss

and even lost its competitiveness in the market (Mazouni, 2018). Also, with the adoption of new

technology which is considered to be energy – wise and economically efficient, Syngenta can

become cost efficient and accordingly, their profitability gets enhanced. Likewise, in the given

case their production capacity has become inefficient to produce any more due to the

introduction of new technology in the agricultural chemical industry it becomes compulsory for

the company to make new investment. Decisions such as adoption of new technology by

Syngenta's competitors and its impact on product offering may greatly affect Syngenta.

Environmental factors: Norms and environmental standards applicable on agricultural chemical

industry have a huge impact on the operations of the company. With the applicability of new

laws and regulations such as associated with environmental pollution, air and water pollution,

recycling and waste management has a great impact on Syngenta policies and decisions (Kumar,

2017). Syngenta must take into consideration the society's attitude towards ecological products

and renewable energy while making new investment decisions.

Legal factors: Many countries are not having robust legal framework to protect the intellectual

property right of Syngenta. Therefore, its management needs to evaluate such country's market

before entering it because in the event of losses due to theft of their product design or any

intellectual property, they may not get the protective shield to safeguard their position in that

market (Gogol and Kolotok, 20190. Decisions that may affect Syngenta are changes in anti-trust

law in agricultural chemical industry, changes in intellectual property law, health and safety law

and consumer protection law.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART B

TASK 1

Nature and type of costs Syngenta and its impact on the company's financial position

From the financial reports and estimations made for the new investment, there are three types of

cost that has been identified with reference to Syngenta, such as the following:

Direct costs: These are cost included in the cost of sales and are directly linked to product

manufactured and changes in these costs greatly affect the gross profit margin of Syngenta as it

is an indicator of company's efficiency in managing its operations (Manuylenko and et.al., 2018).

Example of this type of cost is manufacturing cost.

Indirect or operating cost: These costs are those that incurred in a day to day business operations

which if gets high may affect the operating profit margin of the company and there will be less

profit available to make payment for financial cost and dividends which in turn may affect the

value of the company in the market. Example are selling and marketing costs.

Financial or non-operating costs: Such costs include interest expenses and other compulsory

payments which if gets higher than the optimum level then there will be higher financial risk for

the company (Samygin and et.al., 2019). Higher financial risk leads to bankruptcy and poor

image of the company in the financial market.

Appropriate costing techniques

Costing is defined as recording the overall cost that is associated with providing the

operation. There are various techniques which Syngenta adopt in order to identify the overall

cost of operations. The techniques adopted by the organisational involve the marginal costing

technique, absorption costing technique, batch costing and such like of techniques. All these are

the different methods and techniques that will support the business venture for understand the

need of the business venture and formulate and design all its operational requirement. The role of

the costing technique is to assess the overall cost incurred by the organisation in process to

deliver the business operation (Xu and et.al., 2018). The role all these technique play is to

identify and determine the overall cost that has incurred for delivering all different operations of

the firm. Methods and technique of accounting become the basis to determine the sales price of

the produce and service deliver by the company along with identify the sale price that company

seek to incurred in order to channelises the business operation. The further profit margin

TASK 1

Nature and type of costs Syngenta and its impact on the company's financial position

From the financial reports and estimations made for the new investment, there are three types of

cost that has been identified with reference to Syngenta, such as the following:

Direct costs: These are cost included in the cost of sales and are directly linked to product

manufactured and changes in these costs greatly affect the gross profit margin of Syngenta as it

is an indicator of company's efficiency in managing its operations (Manuylenko and et.al., 2018).

Example of this type of cost is manufacturing cost.

Indirect or operating cost: These costs are those that incurred in a day to day business operations

which if gets high may affect the operating profit margin of the company and there will be less

profit available to make payment for financial cost and dividends which in turn may affect the

value of the company in the market. Example are selling and marketing costs.

Financial or non-operating costs: Such costs include interest expenses and other compulsory

payments which if gets higher than the optimum level then there will be higher financial risk for

the company (Samygin and et.al., 2019). Higher financial risk leads to bankruptcy and poor

image of the company in the financial market.

Appropriate costing techniques

Costing is defined as recording the overall cost that is associated with providing the

operation. There are various techniques which Syngenta adopt in order to identify the overall

cost of operations. The techniques adopted by the organisational involve the marginal costing

technique, absorption costing technique, batch costing and such like of techniques. All these are

the different methods and techniques that will support the business venture for understand the

need of the business venture and formulate and design all its operational requirement. The role of

the costing technique is to assess the overall cost incurred by the organisation in process to

deliver the business operation (Xu and et.al., 2018). The role all these technique play is to

identify and determine the overall cost that has incurred for delivering all different operations of

the firm. Methods and technique of accounting become the basis to determine the sales price of

the produce and service deliver by the company along with identify the sale price that company

seek to incurred in order to channelises the business operation. The further profit margin

en65ertain and hold by the company is also a significant aspect that is determine don the basis of

the suitable costing technique has been adopted by the organisation.

Role of accounting to support decision making

Accounting is the practice involve recording the business transaction under accounting

books prepare by the organisation. Accounting play a crucial role for the company to take on the

best suitable business decisions. In the overall business situation accounting is the one core

technique that drive ad guide the organisation to take decisions on the basis of the records found

and identified by the venture. Decision making in business is highly supportive with support of

accounting transactions and books. Accounting provide the suitable basis to the management of

Syngenta for taking all important decision in business. Every strategy that is design and frame by

the venture would have some financial implication (Uğur and Leblebici, 2018). Decision making

in business would highly rate with the accounting figure and values that may support the

business venture to deliver the business objectives. In business world ever decision company

take is based on the financial return and outcome that such decision would be able to generate. In

such a process this is significant for the organisation to identify the financial implication of every

single business decision making process. The role of accounting is to support the business

venture for taking the best suitable decision on the basis of the need and requirement of the

business venture. Accounting not only drive the business to take important decision in business

but also to analysis the decision making taken by the company. Accounting play the fundamental

role for the business venture that will further support the venture for addressing all its various

need and requirement in the company. Counting will support the organisation to measure the

overall performance of the venture in respective target market.

Accounting is a crucial functional area associated with the organisation as to cover all the

costing related areas of the organisation which further allow the business venture to mitigate all

its different business objectives. The role of accounting is to suggest the company about the level

of expected profit against delivering the certain functional activity of the organisation. The role

of accounting is very crucial in the organisation as it improve the decision making ability of the

organisation along with supporting the suitable areas of operation tat would empower right

business venture for entertain and channelising all its various operations in he organisation. Cost

control is another significant role which accounting play for the Syngenta. The business venture

is associate with the multiple operation and functional areas that needed to overlook by the

the suitable costing technique has been adopted by the organisation.

Role of accounting to support decision making

Accounting is the practice involve recording the business transaction under accounting

books prepare by the organisation. Accounting play a crucial role for the company to take on the

best suitable business decisions. In the overall business situation accounting is the one core

technique that drive ad guide the organisation to take decisions on the basis of the records found

and identified by the venture. Decision making in business is highly supportive with support of

accounting transactions and books. Accounting provide the suitable basis to the management of

Syngenta for taking all important decision in business. Every strategy that is design and frame by

the venture would have some financial implication (Uğur and Leblebici, 2018). Decision making

in business would highly rate with the accounting figure and values that may support the

business venture to deliver the business objectives. In business world ever decision company

take is based on the financial return and outcome that such decision would be able to generate. In

such a process this is significant for the organisation to identify the financial implication of every

single business decision making process. The role of accounting is to support the business

venture for taking the best suitable decision on the basis of the need and requirement of the

business venture. Accounting not only drive the business to take important decision in business

but also to analysis the decision making taken by the company. Accounting play the fundamental

role for the business venture that will further support the venture for addressing all its various

need and requirement in the company. Counting will support the organisation to measure the

overall performance of the venture in respective target market.

Accounting is a crucial functional area associated with the organisation as to cover all the

costing related areas of the organisation which further allow the business venture to mitigate all

its different business objectives. The role of accounting is to suggest the company about the level

of expected profit against delivering the certain functional activity of the organisation. The role

of accounting is very crucial in the organisation as it improve the decision making ability of the

organisation along with supporting the suitable areas of operation tat would empower right

business venture for entertain and channelising all its various operations in he organisation. Cost

control is another significant role which accounting play for the Syngenta. The business venture

is associate with the multiple operation and functional areas that needed to overlook by the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.