Mobile Payment: A Systematic Literature Review on Mobile Payment

VerifiedAdded on 2022/08/12

|20

|6714

|36

Report

AI Summary

This report presents a systematic literature review on mobile payment, exploring its evolution, functionality, and benefits. The research investigates mobile payment's core concepts, technological underpinnings, and advantages. It delves into the gaps within the technology and provides recommendations for future research and development. The study employs a comprehensive methodology, analyzing various databases and sources, including EBSCO and Scopus, to gather relevant articles and data. The analysis encompasses the definition of mobile payment, its operational mechanisms, and its impact across different sectors. The report also highlights the benefits of mobile payments, such as enhanced transaction security and convenience, while also identifying existing limitations and areas for improvement. The report also discusses the research questions and the methodology, including the databases searched and the keywords used. Furthermore, it summarizes the findings of the research, including the conceptualization of mobile payment, the payment methods, and the benefits and gaps identified. The conclusion and recommendations provide insights for enhancing the future of mobile payment.

Running Head: MOBILE PAYMENT 1

Mobile Payment

Tutor

Institution

Date

A systematic literature review on Mobile Payment

Mobile Payment

Tutor

Institution

Date

A systematic literature review on Mobile Payment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MOBILE PAYMENT 2

Abstract

This review paper aims at assessing on mobile payment research. It provides its

understanding, how it works, the possible gaps that are or have been there over years as well as

its benefits. A number of research sources have been analyzed to explore on this topic as with the

evolution there is an accumulation of new knowledge and ideas. A general review on the

frequently asked question concerning mobile payments is also analyzed. This review paper

majorly requires a research on mobile payment using the EBSCO database and the Scopus

database as they provide a number of library database services that are of high quality as well as

they are easy to navigate despite having a wide coverage. A conclusion as well as suggested

recommendations are also analyzed to provide a variety of ideas that can enhance the future of

mobile payment.

Keywords: Mobile payment, mobile money, digital mobility technologies, frameworks.

Paper type: a systematic Literature review research paper.

Introduction

A new system of payment has emerged due to the recent evolution of Technology in the

wireless and telecommunication sector. This system is believed to solve inefficiencies and the

shortcomings of the conventional payment systems as PayPal debit card, visa card and master

card making it easy to perform transactions at any given time from any place. This system is the

mobile payment or mobile money that makes it possible to transfer money, buy goods as well as

pay for services among other services. It involves use of wireless devices such as the personal

digital assistant (PDA), a mobile phone and several relevant digital devices. Majorly there is

initiation of transactions using the mobile device or the phone that are the online banking

website, sending of text messages, web browser and online payment website. A good number of

banks have adopted this new system into their apps of banking to allow their customers to send

money directly from their bank accounts. The mobile payments were first known in Asia and

Europe that later spread to several parts of the continent that advanced from sending a text

message to having the capabilities for banking apps (Bailey, Pentina, Mishra & Mimoun, 2017).

A number of authors have defined mobile payments to their understanding and focused on

technology and consumer adoption. According to Yan L. et al (2011), they state it to be a kind of

service that ensure users have the permit to use its mobile terminal which is the mobile phone to

Abstract

This review paper aims at assessing on mobile payment research. It provides its

understanding, how it works, the possible gaps that are or have been there over years as well as

its benefits. A number of research sources have been analyzed to explore on this topic as with the

evolution there is an accumulation of new knowledge and ideas. A general review on the

frequently asked question concerning mobile payments is also analyzed. This review paper

majorly requires a research on mobile payment using the EBSCO database and the Scopus

database as they provide a number of library database services that are of high quality as well as

they are easy to navigate despite having a wide coverage. A conclusion as well as suggested

recommendations are also analyzed to provide a variety of ideas that can enhance the future of

mobile payment.

Keywords: Mobile payment, mobile money, digital mobility technologies, frameworks.

Paper type: a systematic Literature review research paper.

Introduction

A new system of payment has emerged due to the recent evolution of Technology in the

wireless and telecommunication sector. This system is believed to solve inefficiencies and the

shortcomings of the conventional payment systems as PayPal debit card, visa card and master

card making it easy to perform transactions at any given time from any place. This system is the

mobile payment or mobile money that makes it possible to transfer money, buy goods as well as

pay for services among other services. It involves use of wireless devices such as the personal

digital assistant (PDA), a mobile phone and several relevant digital devices. Majorly there is

initiation of transactions using the mobile device or the phone that are the online banking

website, sending of text messages, web browser and online payment website. A good number of

banks have adopted this new system into their apps of banking to allow their customers to send

money directly from their bank accounts. The mobile payments were first known in Asia and

Europe that later spread to several parts of the continent that advanced from sending a text

message to having the capabilities for banking apps (Bailey, Pentina, Mishra & Mimoun, 2017).

A number of authors have defined mobile payments to their understanding and focused on

technology and consumer adoption. According to Yan L. et al (2011), they state it to be a kind of

service that ensure users have the permit to use its mobile terminal which is the mobile phone to

MOBILE PAYMENT 3

pay for goods and services required for their consumption. Back then, a small number of

customers managed to experience the mobile payments and quite a big number of the initiatives

regarding mobile payments were never a success way before reaching the intended end users.

The complexity of the phenomenon leads to an investigation of the adoption of consumers to

provide quite an understanding of mobile payments.

In this systematic review paper, it is shown that mobile payments were differentiated

from any kind of electronic or mobile money, use of mobile devices and electronic banking. A

framework consisting of mobile payment service that is based on the Porter’s Five-Forces model

on its market and the contingent factors that influence the market in regard to the contingency

theory were crafted. After a number of publications, there has been a motivation on new critical

review of the literature. There has been performance of systematic literature research that lead to

the identification of a good number of articles that were major conferences that had a huge

impact that has been over 1.0. It is clear that trust and security are crucial in the adoption process

and the use of mobile payments. The purpose of this review is to analyze mobile payment

research that has been conducted after the publication of previous literature review. The

objective is to compare the volume, methods used to research, the themes of research and

provide other findings regarding mobile payments. There is also an overview of the

recommendations from the previous literature that have been beneficial in the mobile payment

research. An updated list of recommendations is also provided so as to improve on the future

research of mobile payments.

Research Questions

In this research paper, we are going to consider four research questions. By using these

questions, we will be able to get an understanding of what mobile payments is.

Q1: What is mobile payment?

This question seeks to find out the meaning of mobile payments. When we talk to mobile

payment, what do we mean? It seeks to explain the concept behind mobile payments and all that

is involved during the process.

Q2: How does mobile payments work?

This research question is particularly interested in the technology behind mobile paying. What

technologies are needed to make the process complete? Which technology is used to ensure that

the transaction is secure?

pay for goods and services required for their consumption. Back then, a small number of

customers managed to experience the mobile payments and quite a big number of the initiatives

regarding mobile payments were never a success way before reaching the intended end users.

The complexity of the phenomenon leads to an investigation of the adoption of consumers to

provide quite an understanding of mobile payments.

In this systematic review paper, it is shown that mobile payments were differentiated

from any kind of electronic or mobile money, use of mobile devices and electronic banking. A

framework consisting of mobile payment service that is based on the Porter’s Five-Forces model

on its market and the contingent factors that influence the market in regard to the contingency

theory were crafted. After a number of publications, there has been a motivation on new critical

review of the literature. There has been performance of systematic literature research that lead to

the identification of a good number of articles that were major conferences that had a huge

impact that has been over 1.0. It is clear that trust and security are crucial in the adoption process

and the use of mobile payments. The purpose of this review is to analyze mobile payment

research that has been conducted after the publication of previous literature review. The

objective is to compare the volume, methods used to research, the themes of research and

provide other findings regarding mobile payments. There is also an overview of the

recommendations from the previous literature that have been beneficial in the mobile payment

research. An updated list of recommendations is also provided so as to improve on the future

research of mobile payments.

Research Questions

In this research paper, we are going to consider four research questions. By using these

questions, we will be able to get an understanding of what mobile payments is.

Q1: What is mobile payment?

This question seeks to find out the meaning of mobile payments. When we talk to mobile

payment, what do we mean? It seeks to explain the concept behind mobile payments and all that

is involved during the process.

Q2: How does mobile payments work?

This research question is particularly interested in the technology behind mobile paying. What

technologies are needed to make the process complete? Which technology is used to ensure that

the transaction is secure?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MOBILE PAYMENT 4

Q3: What are the benefits of mobile payments?

In this research question, we find out the benefits and the advantages of this technology. Does it

help make the payment process easier? If it does, how does it do that? Are the people accepting

the technology and embracing it? These are some of the answers that the question as a whole

seeks to answer.

Q4: What are the gaps identified in mobile payments?

This is the final question and it involves identifying the gaps that are found within this

technology. It identifies areas that need improvement. This is the question that leads to

recommendations, which are meant to make this technology better and more helpful to human

beings.

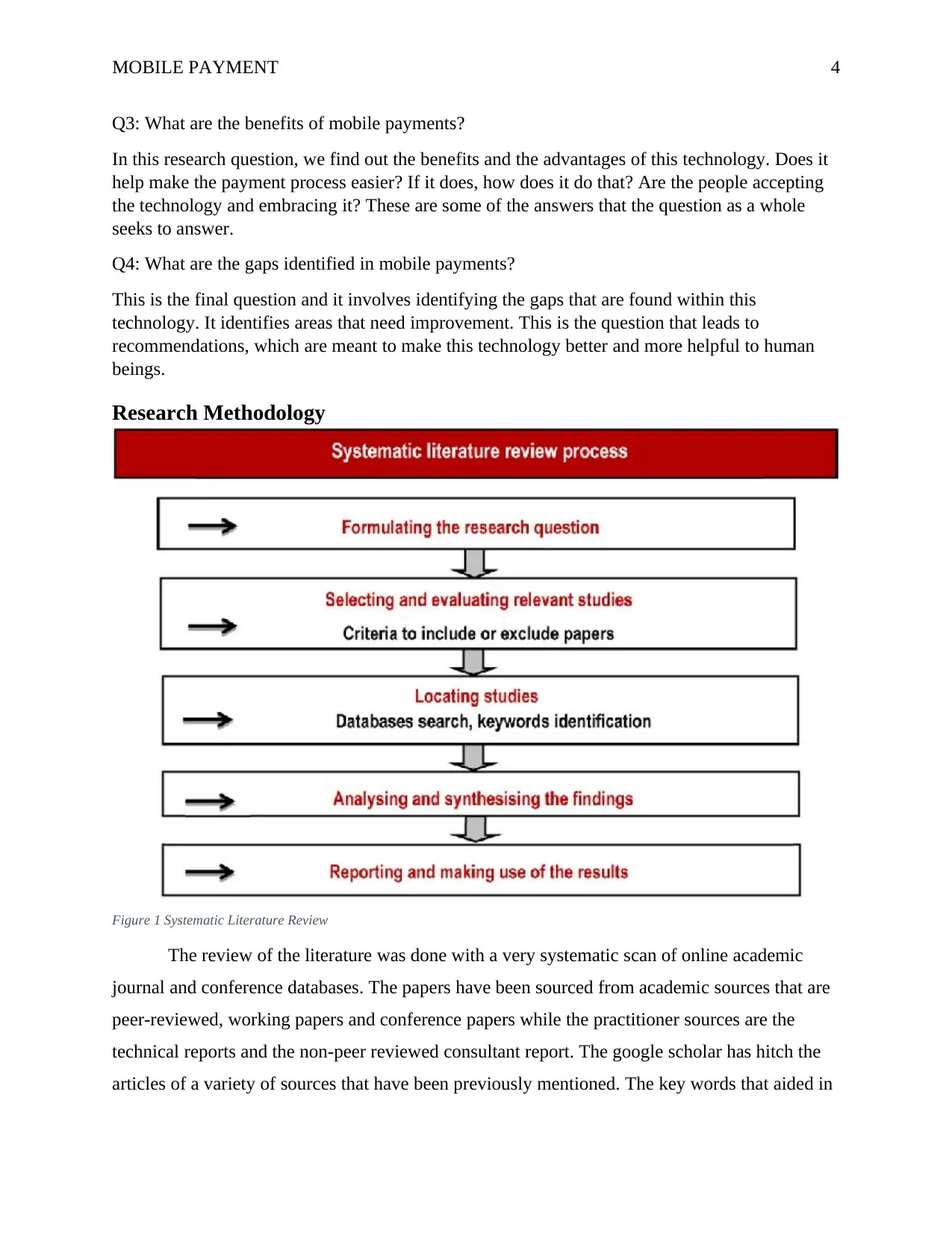

Research Methodology

Figure 1 Systematic Literature Review

The review of the literature was done with a very systematic scan of online academic

journal and conference databases. The papers have been sourced from academic sources that are

peer-reviewed, working papers and conference papers while the practitioner sources are the

technical reports and the non-peer reviewed consultant report. The google scholar has hitch the

articles of a variety of sources that have been previously mentioned. The key words that aided in

Q3: What are the benefits of mobile payments?

In this research question, we find out the benefits and the advantages of this technology. Does it

help make the payment process easier? If it does, how does it do that? Are the people accepting

the technology and embracing it? These are some of the answers that the question as a whole

seeks to answer.

Q4: What are the gaps identified in mobile payments?

This is the final question and it involves identifying the gaps that are found within this

technology. It identifies areas that need improvement. This is the question that leads to

recommendations, which are meant to make this technology better and more helpful to human

beings.

Research Methodology

Figure 1 Systematic Literature Review

The review of the literature was done with a very systematic scan of online academic

journal and conference databases. The papers have been sourced from academic sources that are

peer-reviewed, working papers and conference papers while the practitioner sources are the

technical reports and the non-peer reviewed consultant report. The google scholar has hitch the

articles of a variety of sources that have been previously mentioned. The key words that aided in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

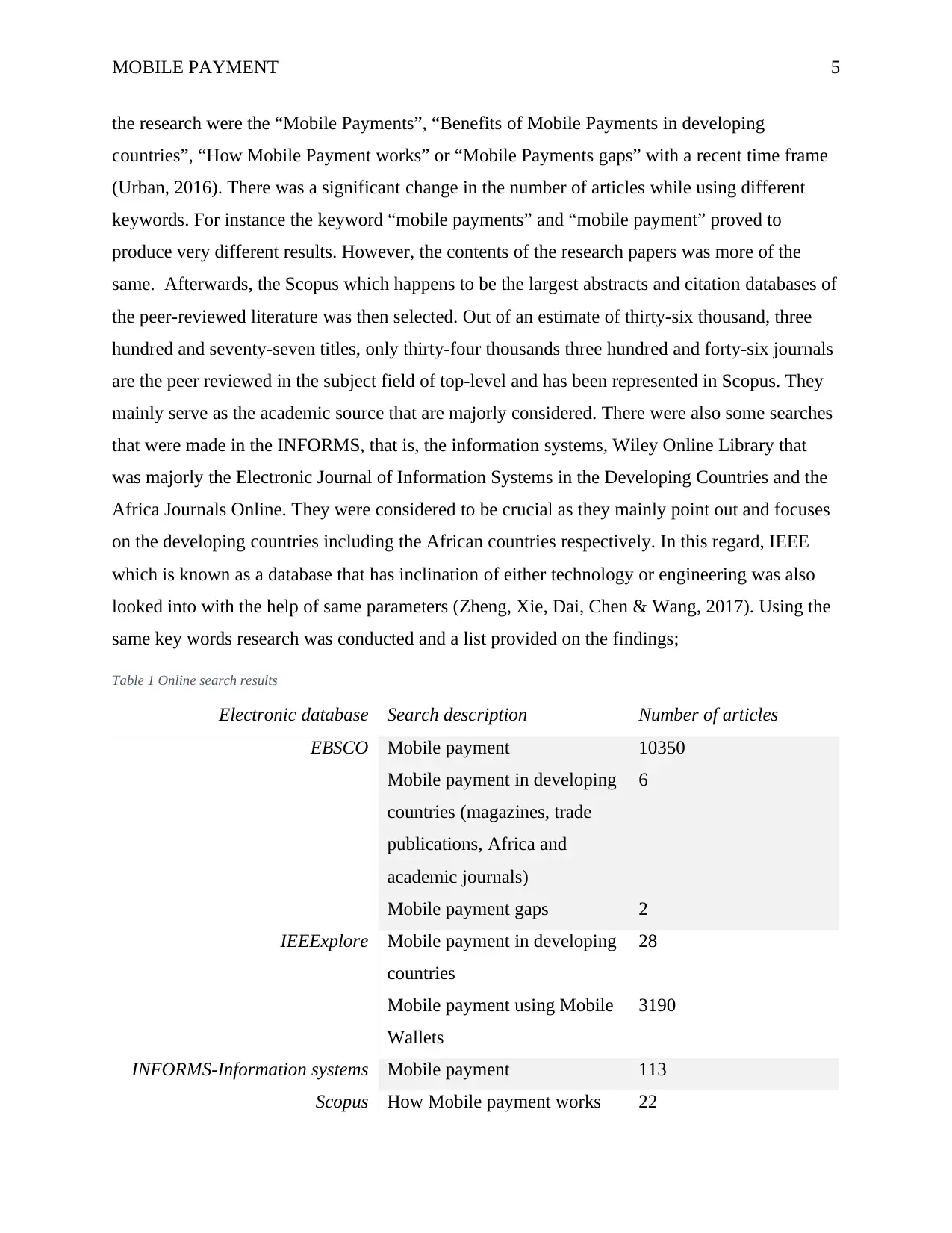

MOBILE PAYMENT 5

the research were the “Mobile Payments”, “Benefits of Mobile Payments in developing

countries”, “How Mobile Payment works” or “Mobile Payments gaps” with a recent time frame

(Urban, 2016). There was a significant change in the number of articles while using different

keywords. For instance the keyword “mobile payments” and “mobile payment” proved to

produce very different results. However, the contents of the research papers was more of the

same. Afterwards, the Scopus which happens to be the largest abstracts and citation databases of

the peer-reviewed literature was then selected. Out of an estimate of thirty-six thousand, three

hundred and seventy-seven titles, only thirty-four thousands three hundred and forty-six journals

are the peer reviewed in the subject field of top-level and has been represented in Scopus. They

mainly serve as the academic source that are majorly considered. There were also some searches

that were made in the INFORMS, that is, the information systems, Wiley Online Library that

was majorly the Electronic Journal of Information Systems in the Developing Countries and the

Africa Journals Online. They were considered to be crucial as they mainly point out and focuses

on the developing countries including the African countries respectively. In this regard, IEEE

which is known as a database that has inclination of either technology or engineering was also

looked into with the help of same parameters (Zheng, Xie, Dai, Chen & Wang, 2017). Using the

same key words research was conducted and a list provided on the findings;

Table 1 Online search results

Electronic database Search description Number of articles

EBSCO Mobile payment

Mobile payment in developing

countries (magazines, trade

publications, Africa and

academic journals)

Mobile payment gaps

10350

6

2

IEEExplore Mobile payment in developing

countries

Mobile payment using Mobile

Wallets

28

3190

INFORMS-Information systems Mobile payment 113

Scopus How Mobile payment works 22

the research were the “Mobile Payments”, “Benefits of Mobile Payments in developing

countries”, “How Mobile Payment works” or “Mobile Payments gaps” with a recent time frame

(Urban, 2016). There was a significant change in the number of articles while using different

keywords. For instance the keyword “mobile payments” and “mobile payment” proved to

produce very different results. However, the contents of the research papers was more of the

same. Afterwards, the Scopus which happens to be the largest abstracts and citation databases of

the peer-reviewed literature was then selected. Out of an estimate of thirty-six thousand, three

hundred and seventy-seven titles, only thirty-four thousands three hundred and forty-six journals

are the peer reviewed in the subject field of top-level and has been represented in Scopus. They

mainly serve as the academic source that are majorly considered. There were also some searches

that were made in the INFORMS, that is, the information systems, Wiley Online Library that

was majorly the Electronic Journal of Information Systems in the Developing Countries and the

Africa Journals Online. They were considered to be crucial as they mainly point out and focuses

on the developing countries including the African countries respectively. In this regard, IEEE

which is known as a database that has inclination of either technology or engineering was also

looked into with the help of same parameters (Zheng, Xie, Dai, Chen & Wang, 2017). Using the

same key words research was conducted and a list provided on the findings;

Table 1 Online search results

Electronic database Search description Number of articles

EBSCO Mobile payment

Mobile payment in developing

countries (magazines, trade

publications, Africa and

academic journals)

Mobile payment gaps

10350

6

2

IEEExplore Mobile payment in developing

countries

Mobile payment using Mobile

Wallets

28

3190

INFORMS-Information systems Mobile payment 113

Scopus How Mobile payment works 22

MOBILE PAYMENT 6

Mobile payment

43

African journals online(AJOL) Mobile payment 1

Google Scholar How mobile payment works

Mobile payment

Mobile payment gaps

Benefits of mobile payments

2

20

1

2

Wiley online Library(EJISDC) Mobile payment

Mobile payment gaps

160

25

A number of articles found from the research were examined and a number of them eliminated.

This elimination was done through focusing on mobile payment, its benefits and the present

gaps. The trade and news articles were filtered making it possible to access and have the

capability of dealing with the key research papers only for provision of the required information.

Thirty sources were chosen for the expected literature review.

Table 2 Filtered online search results

Electronic database Number of articles

EBSCO 14

IEEExplore 1

Scopus 12

Google scholar 3

Wiley online library 1

African journals online 1

After the thorough article research, it was clear the research papers that were relevant to

this study. Using these papers, a study was done and the research questions were well answered

and documented.

Mobile payment

43

African journals online(AJOL) Mobile payment 1

Google Scholar How mobile payment works

Mobile payment

Mobile payment gaps

Benefits of mobile payments

2

20

1

2

Wiley online Library(EJISDC) Mobile payment

Mobile payment gaps

160

25

A number of articles found from the research were examined and a number of them eliminated.

This elimination was done through focusing on mobile payment, its benefits and the present

gaps. The trade and news articles were filtered making it possible to access and have the

capability of dealing with the key research papers only for provision of the required information.

Thirty sources were chosen for the expected literature review.

Table 2 Filtered online search results

Electronic database Number of articles

EBSCO 14

IEEExplore 1

Scopus 12

Google scholar 3

Wiley online library 1

African journals online 1

After the thorough article research, it was clear the research papers that were relevant to

this study. Using these papers, a study was done and the research questions were well answered

and documented.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MOBILE PAYMENT 7

Results and Analysis

Mobile payment is conceptualized as payment that involves a mobile device to initiate,

activate as well as confirm this process of payment whereby this device has the capabilities of a

mobile phone such as a smartphone. It may involve payments of bills, acquisition or transfer of

money between agents dealing with finances. In this paper, mobile payments can be noted to

focus on digital mobility technologies that are used to help in transactions aside the networks of

telecommunication. The methods of payments are classified according to certain standards that

are analyzed for a proper framework. This framework entails different layers; load bearing, a

core application, network interface, a business and decision making layers. Being a killer

application, two processes are adopted to aid in mobile payments which are account based and

pre-pay. Throughout this process of mobile payment electronic money that is portable and has

the mobility is used to help in their systems that are majorly multi-sided platforms. These

platforms have high technology components that are stabilized and other components that are the

merchants and consumers who are linked by a buyer-to-seller connection. In regard to supply,

there are several dilemma as resources are shared in a big number as well as mobile payments

platforms presented to the consumers making them want to use mobile phones to pay as well as

be paid. The main clients in mobile payments services are the consumers, the merchants,

financial institutions, software, vendors of the handsets, Mobile Network Operators (MNO) as

well as networks that ensure there is positivity from the external forces. Findings from other

sources are;

News Articles

What is mobile payment?

Using a phone or a tablet to pay for a service or a product is referred to as mobile

payment (Collinge, Thompson, Smets, Roberts, & Ward, 2019). Using mobile payment, it is also

possible to transfer funds to family and friends. Examples of mobile payments include services

such as PayPal and Venmo (Morosan & DeFranco, 2016). Recently, majority of the banks have

adopted this technology and by doing so, customers can be able to instantly transfer funds to

family and friends directly from their banks accounts without having to visit the bank. On the

other hand, it is possible to make a mobile payment on site by simply scanning a barcode using

mobile apps or even accepting payments in a convenience store. These charges are deducted

from a preloaded card for that specific store or from a debit or credit card. Mobile payment uses

Results and Analysis

Mobile payment is conceptualized as payment that involves a mobile device to initiate,

activate as well as confirm this process of payment whereby this device has the capabilities of a

mobile phone such as a smartphone. It may involve payments of bills, acquisition or transfer of

money between agents dealing with finances. In this paper, mobile payments can be noted to

focus on digital mobility technologies that are used to help in transactions aside the networks of

telecommunication. The methods of payments are classified according to certain standards that

are analyzed for a proper framework. This framework entails different layers; load bearing, a

core application, network interface, a business and decision making layers. Being a killer

application, two processes are adopted to aid in mobile payments which are account based and

pre-pay. Throughout this process of mobile payment electronic money that is portable and has

the mobility is used to help in their systems that are majorly multi-sided platforms. These

platforms have high technology components that are stabilized and other components that are the

merchants and consumers who are linked by a buyer-to-seller connection. In regard to supply,

there are several dilemma as resources are shared in a big number as well as mobile payments

platforms presented to the consumers making them want to use mobile phones to pay as well as

be paid. The main clients in mobile payments services are the consumers, the merchants,

financial institutions, software, vendors of the handsets, Mobile Network Operators (MNO) as

well as networks that ensure there is positivity from the external forces. Findings from other

sources are;

News Articles

What is mobile payment?

Using a phone or a tablet to pay for a service or a product is referred to as mobile

payment (Collinge, Thompson, Smets, Roberts, & Ward, 2019). Using mobile payment, it is also

possible to transfer funds to family and friends. Examples of mobile payments include services

such as PayPal and Venmo (Morosan & DeFranco, 2016). Recently, majority of the banks have

adopted this technology and by doing so, customers can be able to instantly transfer funds to

family and friends directly from their banks accounts without having to visit the bank. On the

other hand, it is possible to make a mobile payment on site by simply scanning a barcode using

mobile apps or even accepting payments in a convenience store. These charges are deducted

from a preloaded card for that specific store or from a debit or credit card. Mobile payment uses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MOBILE PAYMENT 8

encrypted transfer of information and this makes it much safe compared to direct payment using

debit or credit cards (Dorsey, McCauley, Cummins, Monica, Quigley, & McKelvey, 2017).

Mobile payments were initially more popular in Asia and Europe and then later it was adopted in

United States (Bailey, Pentina, Mishra & Mimoun, 2017). As the technology was being

introduced, it involved sending of text messages only but later it was upgraded to incorporate

sending of check pictures that were taken using cell phones.

Figure 2 A depiction of two devices using mobile payment

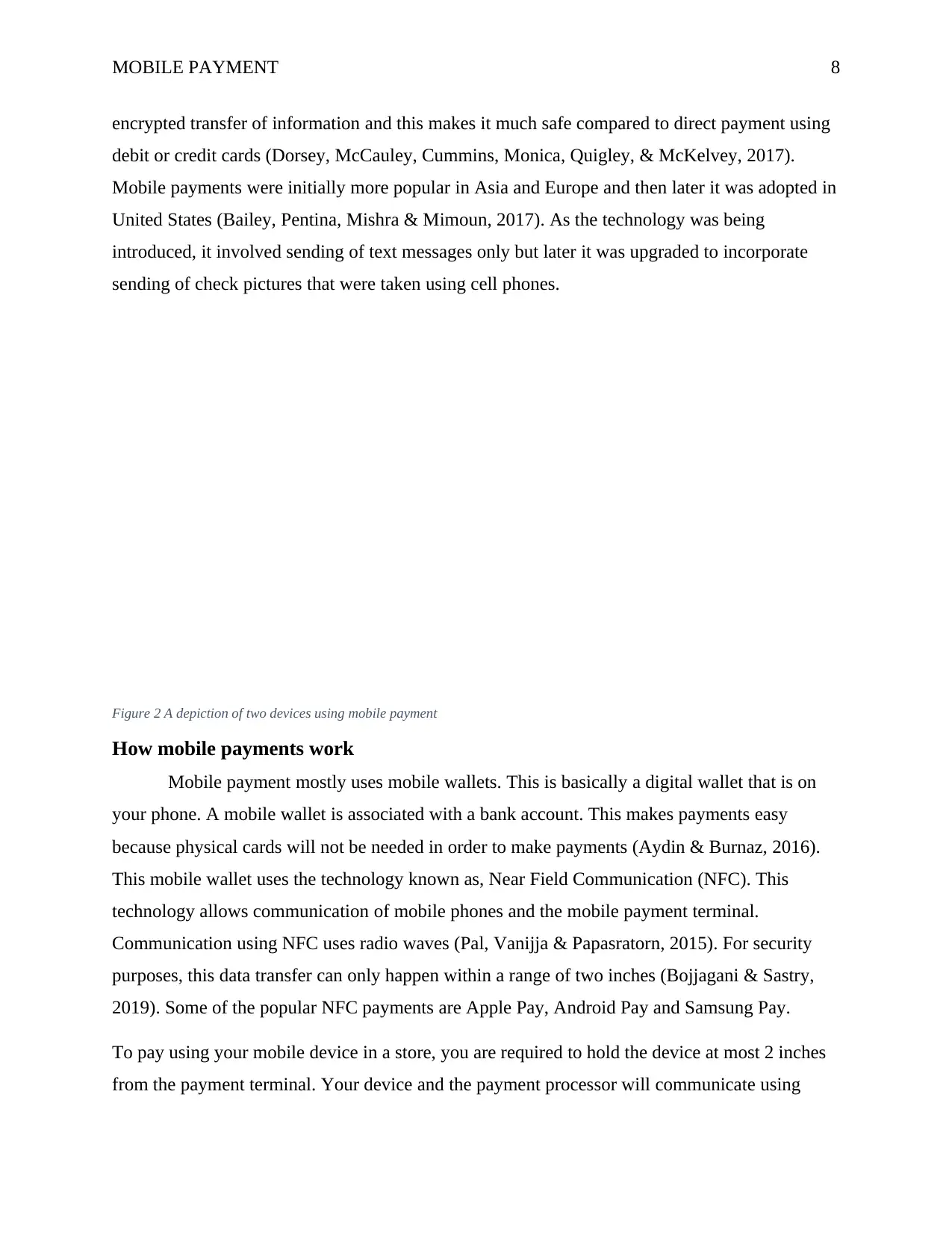

How mobile payments work

Mobile payment mostly uses mobile wallets. This is basically a digital wallet that is on

your phone. A mobile wallet is associated with a bank account. This makes payments easy

because physical cards will not be needed in order to make payments (Aydin & Burnaz, 2016).

This mobile wallet uses the technology known as, Near Field Communication (NFC). This

technology allows communication of mobile phones and the mobile payment terminal.

Communication using NFC uses radio waves (Pal, Vanijja & Papasratorn, 2015). For security

purposes, this data transfer can only happen within a range of two inches (Bojjagani & Sastry,

2019). Some of the popular NFC payments are Apple Pay, Android Pay and Samsung Pay.

To pay using your mobile device in a store, you are required to hold the device at most 2 inches

from the payment terminal. Your device and the payment processor will communicate using

encrypted transfer of information and this makes it much safe compared to direct payment using

debit or credit cards (Dorsey, McCauley, Cummins, Monica, Quigley, & McKelvey, 2017).

Mobile payments were initially more popular in Asia and Europe and then later it was adopted in

United States (Bailey, Pentina, Mishra & Mimoun, 2017). As the technology was being

introduced, it involved sending of text messages only but later it was upgraded to incorporate

sending of check pictures that were taken using cell phones.

Figure 2 A depiction of two devices using mobile payment

How mobile payments work

Mobile payment mostly uses mobile wallets. This is basically a digital wallet that is on

your phone. A mobile wallet is associated with a bank account. This makes payments easy

because physical cards will not be needed in order to make payments (Aydin & Burnaz, 2016).

This mobile wallet uses the technology known as, Near Field Communication (NFC). This

technology allows communication of mobile phones and the mobile payment terminal.

Communication using NFC uses radio waves (Pal, Vanijja & Papasratorn, 2015). For security

purposes, this data transfer can only happen within a range of two inches (Bojjagani & Sastry,

2019). Some of the popular NFC payments are Apple Pay, Android Pay and Samsung Pay.

To pay using your mobile device in a store, you are required to hold the device at most 2 inches

from the payment terminal. Your device and the payment processor will communicate using

MOBILE PAYMENT 9

NFC. The payment is processed through passing of information between the two devices using

radio waves. The whole process is executed in seconds and hence it is one of the fastest means of

payment. This kind of payment is often referred to as contactless payment since there is no

physical contact involved (Cocosila & Trabelsi, 2016). With its ability to function most

developing countries, have highly increased the systems of mobile payments facilitating

efficiency in transactions. A good number of consumers have been able to accelerate with the

booming mobile payment market, introducing several mobile payment platforms.

Figure 3 NFC mobile payment

Benefits of mobile payment

Mobile payments are very fast. This is probably the fastest way to make payments for

anything. Roughly, a mobile payment transaction takes about a second to complete. They are

slightly faster than the swipe payment methods, which is used to charge credit and debit cards.

This speed is convenient for stores and it even attracts customers as the queues move faster as a

result of fast check out. On the other hand, they are convenient. It is possible to walk around

cashless and be able to pay for everything as long as you have your mobile phone. The

NFC. The payment is processed through passing of information between the two devices using

radio waves. The whole process is executed in seconds and hence it is one of the fastest means of

payment. This kind of payment is often referred to as contactless payment since there is no

physical contact involved (Cocosila & Trabelsi, 2016). With its ability to function most

developing countries, have highly increased the systems of mobile payments facilitating

efficiency in transactions. A good number of consumers have been able to accelerate with the

booming mobile payment market, introducing several mobile payment platforms.

Figure 3 NFC mobile payment

Benefits of mobile payment

Mobile payments are very fast. This is probably the fastest way to make payments for

anything. Roughly, a mobile payment transaction takes about a second to complete. They are

slightly faster than the swipe payment methods, which is used to charge credit and debit cards.

This speed is convenient for stores and it even attracts customers as the queues move faster as a

result of fast check out. On the other hand, they are convenient. It is possible to walk around

cashless and be able to pay for everything as long as you have your mobile phone. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MOBILE PAYMENT 10

convenience that comes with mobile payments is nothing like we have seen in the past.

Additionally, the transactions are very secure. Mobile payments use multiple layers of dynamic

data encryption to make sure that the information for payment is extremely secure. Considering

business owners. Mobile payment draws a lot of customers. This is because customers love the

convenience that comes with this kind of payment (Zhang & Mao, 2020). By integrating this to

the business, customers note that you are keeping up with current trends and this could increase

trust and engagement from customers. On top of it all, as people embrace the mobile payment

technology and fully prefer it over cash payment, this step will be a determinant of which store a

customer is likely to visit (Ma & Fildes, 2020). According to research, it is true to say that,

customers who adopted mobile wallets early have spent almost twice in payment in relation to

those who pay in cash. Considering this aspect, it is clear that a business accepting electronic

payments in much likely to make more profit considered to the other stores which use cash

payment systems (Taylor, 2016).

Gaps in mobile payments

Mobile payment is associated with issues that are dragging down its adoption. From its

design and capabilities to user registration and logins, there is a lot of inconsistency within the

platforms for mobile payments. These inconsistencies are the reason why its adoption is sluggish

(Chavda, 2018). Customers have always had issues with sharing confidential information.

Moreover, as discussed, mobile payments require a lot of financial and personal information to

get started with them (Urban, 2016). This is one of the main reason why customers opt not to

enroll for mobile payments. Most people feel that their private information is at stake and hence

they choose not to share it.

Recommendations

Finding a way to keep the customer information private and confidential is important.

Additionally, it is important to find a way to convince the customers that their information is

very secure so as to increase the number of people signing up for this service. In order to reduce

the concerns regarding security of information, providers of mobile payments must find a way to

ensure that the customer’s data is secure and safe (Yeh, 2018). To make safer the front end,

adoption of biometric and touch ID is very key (Pal, Khethavath, Chen & Zhang, 2017). In

addition to that, encryption of data is also another way to ensure the safety of information.

convenience that comes with mobile payments is nothing like we have seen in the past.

Additionally, the transactions are very secure. Mobile payments use multiple layers of dynamic

data encryption to make sure that the information for payment is extremely secure. Considering

business owners. Mobile payment draws a lot of customers. This is because customers love the

convenience that comes with this kind of payment (Zhang & Mao, 2020). By integrating this to

the business, customers note that you are keeping up with current trends and this could increase

trust and engagement from customers. On top of it all, as people embrace the mobile payment

technology and fully prefer it over cash payment, this step will be a determinant of which store a

customer is likely to visit (Ma & Fildes, 2020). According to research, it is true to say that,

customers who adopted mobile wallets early have spent almost twice in payment in relation to

those who pay in cash. Considering this aspect, it is clear that a business accepting electronic

payments in much likely to make more profit considered to the other stores which use cash

payment systems (Taylor, 2016).

Gaps in mobile payments

Mobile payment is associated with issues that are dragging down its adoption. From its

design and capabilities to user registration and logins, there is a lot of inconsistency within the

platforms for mobile payments. These inconsistencies are the reason why its adoption is sluggish

(Chavda, 2018). Customers have always had issues with sharing confidential information.

Moreover, as discussed, mobile payments require a lot of financial and personal information to

get started with them (Urban, 2016). This is one of the main reason why customers opt not to

enroll for mobile payments. Most people feel that their private information is at stake and hence

they choose not to share it.

Recommendations

Finding a way to keep the customer information private and confidential is important.

Additionally, it is important to find a way to convince the customers that their information is

very secure so as to increase the number of people signing up for this service. In order to reduce

the concerns regarding security of information, providers of mobile payments must find a way to

ensure that the customer’s data is secure and safe (Yeh, 2018). To make safer the front end,

adoption of biometric and touch ID is very key (Pal, Khethavath, Chen & Zhang, 2017). In

addition to that, encryption of data is also another way to ensure the safety of information.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MOBILE PAYMENT 11

Encryption is more concerned with protecting the back end from unauthorized access. Adoption

of other ideas such as tokenization would also be a good way to reduce customer concerns. This

is true because, adopting tokenization would eliminate the use of debit and credit card during the

authorization of a transaction. In this method, a rand combination of number and letter is

generated and used to authorize the transaction (Hagan, Roberts, Wysocki & Logsdon, 2018).

Such measure will ensure that even in the event that hackers gain access to the system, it is still

not possible to access customer information. It is important for customers to feel safe before they

can adopt this method of payment.

Scientific articles

What is mobile payments

Mobile payment includes mobile wallets and mobile money transfers. Mobile payments

can therefore be defined as transaction, which are conducted using mobile phones and are

regulated. Mobile payments eliminate the use of checks, cash and physical credit card when

purchasing or paying bills. Through mobile payment, it is possible to perform these transactions

digitally. Mobile payments ate used widely in peer-to-peer context and even in brick and mortar

businesses. In the case of peer-to-peer, it allows you to send funds to friends or family while in

the context of brick and mortar it allows for payment of services and products (Kalinić, Liébana-

Cabanillas, Muñoz-Leiva & Marinković, 2019).

How mobile payments works

The current world has invested in technologies, which are much secure and safer in

regard to traditional methods. Due to this factor, many people are embracing electronic payment

such as mobile payments. There are several technologies behind the mobile payments. The first

technology is blockchain technology. Most companies are continually adopting this technology

to ensure that their services are modernized and swift (de Luna, Liébana-Cabanillas, Sánchez-

Fernández & Muñoz-Leiva, 2019). Mobile payments largely use this technology because of its

decentralized nature. This feature provides a very strong and almost impossible to crack

protection layer for all transactions. Blockchain technology incorporate the use of encryption and

distribution of ledgers (Zheng, Xie, Dai, Chen & Wang, 2017). These two techniques eliminate

the security risks and ensure that the mobile payment process is safe and secure. The other

technology is the use of digital wallets and POS technologies. Major mobile payment apps like

Encryption is more concerned with protecting the back end from unauthorized access. Adoption

of other ideas such as tokenization would also be a good way to reduce customer concerns. This

is true because, adopting tokenization would eliminate the use of debit and credit card during the

authorization of a transaction. In this method, a rand combination of number and letter is

generated and used to authorize the transaction (Hagan, Roberts, Wysocki & Logsdon, 2018).

Such measure will ensure that even in the event that hackers gain access to the system, it is still

not possible to access customer information. It is important for customers to feel safe before they

can adopt this method of payment.

Scientific articles

What is mobile payments

Mobile payment includes mobile wallets and mobile money transfers. Mobile payments

can therefore be defined as transaction, which are conducted using mobile phones and are

regulated. Mobile payments eliminate the use of checks, cash and physical credit card when

purchasing or paying bills. Through mobile payment, it is possible to perform these transactions

digitally. Mobile payments ate used widely in peer-to-peer context and even in brick and mortar

businesses. In the case of peer-to-peer, it allows you to send funds to friends or family while in

the context of brick and mortar it allows for payment of services and products (Kalinić, Liébana-

Cabanillas, Muñoz-Leiva & Marinković, 2019).

How mobile payments works

The current world has invested in technologies, which are much secure and safer in

regard to traditional methods. Due to this factor, many people are embracing electronic payment

such as mobile payments. There are several technologies behind the mobile payments. The first

technology is blockchain technology. Most companies are continually adopting this technology

to ensure that their services are modernized and swift (de Luna, Liébana-Cabanillas, Sánchez-

Fernández & Muñoz-Leiva, 2019). Mobile payments largely use this technology because of its

decentralized nature. This feature provides a very strong and almost impossible to crack

protection layer for all transactions. Blockchain technology incorporate the use of encryption and

distribution of ledgers (Zheng, Xie, Dai, Chen & Wang, 2017). These two techniques eliminate

the security risks and ensure that the mobile payment process is safe and secure. The other

technology is the use of digital wallets and POS technologies. Major mobile payment apps like

MOBILE PAYMENT 12

Samsung Pay and Apple Pay are working tirelessly to create a society that is cashless. Money is

therefore stored in digital wallets and to make any transactions, the phone’s access controls are

used (Kudesia & Pradhan, 2018). These access controls include fingerprints, passwords and

facial recognition. Digital wallets work in conjunction with NFC- Near Field Communication.

Using NFC the mobile device is able to communicate with the payment processer terminals,

which are installed in the stores. After authorization, the amount is charged from the digital

wallet within a second (Badra & Badra, 2016).

Figure 4 Block chain technology

Benefits of mobile payments

`The benefits of mobile payments include the speed, efficiency and security of the

payment process. Mobile payments have multiple layers of security, which ensures that the

transaction is secure. On the front end, some mobile payments are equipped with biometrics

readers, which helps in the authentication process. This means that no transaction can be

conducted without proper authentication (Himaga & Ogata, 2020). In the back end, mobile

payments use data encryption to make sure that the information being transferred between the

involved parties is safe and secure. The encryption makes sure that any leaked information is not

Samsung Pay and Apple Pay are working tirelessly to create a society that is cashless. Money is

therefore stored in digital wallets and to make any transactions, the phone’s access controls are

used (Kudesia & Pradhan, 2018). These access controls include fingerprints, passwords and

facial recognition. Digital wallets work in conjunction with NFC- Near Field Communication.

Using NFC the mobile device is able to communicate with the payment processer terminals,

which are installed in the stores. After authorization, the amount is charged from the digital

wallet within a second (Badra & Badra, 2016).

Figure 4 Block chain technology

Benefits of mobile payments

`The benefits of mobile payments include the speed, efficiency and security of the

payment process. Mobile payments have multiple layers of security, which ensures that the

transaction is secure. On the front end, some mobile payments are equipped with biometrics

readers, which helps in the authentication process. This means that no transaction can be

conducted without proper authentication (Himaga & Ogata, 2020). In the back end, mobile

payments use data encryption to make sure that the information being transferred between the

involved parties is safe and secure. The encryption makes sure that any leaked information is not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.