Management Accounting Systems, Reporting & Budgetary Control

VerifiedAdded on 2023/01/23

|16

|3606

|67

Report

AI Summary

This report provides a comprehensive overview of management accounting systems, reporting methodologies, and budgetary control within an organizational context, using Mazars and Airdri Ltd as examples. It explores various management accounting systems such as inventory management, job costing, and cost accounting, detailing their importance in business decision-making. The report also examines different management accounting reports, including inventory management, cost accounting, and performance reports, highlighting their role in providing internal insights and improving organizational efficiency. Furthermore, it delves into cost calculation techniques like marginal and absorption costing, comparing their impact on income statements. The analysis extends to budgetary control, assessing the advantages and disadvantages of planning tools like cash budgets, operating budgets, and master budgets, emphasizing their role in financial planning and control. Finally, it touches on how organizations adapt their management accounting systems to address financial challenges, providing a holistic view of management accounting practices and their practical applications.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK 1..........................................................................................................................................................3

P1. Management accounting systems.....................................................................................................3

P2 Different methodologies used in management accounting reporting................................................4

TASK 2..........................................................................................................................................................4

P3 Calculations of costs using appropriate techniques to prepare income statement............................4

TASK 3........................................................................................................................................................12

P4 Advantage and disadvantage of different types of planning tools used for budgetary control........12

TASK 4........................................................................................................................................................13

P5 Compare how organisations are adapting management accounting systems to respond to financial

problems...............................................................................................................................................13

CONCLUSION.............................................................................................................................................14

REFERENCES..............................................................................................................................................15

TASK 1..........................................................................................................................................................3

P1. Management accounting systems.....................................................................................................3

P2 Different methodologies used in management accounting reporting................................................4

TASK 2..........................................................................................................................................................4

P3 Calculations of costs using appropriate techniques to prepare income statement............................4

TASK 3........................................................................................................................................................12

P4 Advantage and disadvantage of different types of planning tools used for budgetary control........12

TASK 4........................................................................................................................................................13

P5 Compare how organisations are adapting management accounting systems to respond to financial

problems...............................................................................................................................................13

CONCLUSION.............................................................................................................................................14

REFERENCES..............................................................................................................................................15

INTRODUCTION

Management accounting is the set of Management and accounts that help to know about business and it's

transactions. It is used to maintain the proper accounts with organization. The main purpose of

Management accounting is to give true and fair vies for increasing the profits in a firm (Bloomfield,

2015). To understand the importance of Management accounting Mazars has been taken that provides

consultants services to different companies and help to make correct business decision. Airdri Ltd is one

of its client which get suggestions to run a business and the report is based on this organization. This

report will cover different topics like management accounting system, reports and planning tools that can

be used to control the budget in a company. Moreover, report will discusses about financial problem

which can be occur in an organization while using system.

TASK 1

P1. Management accounting systems

Management accounting system is the systematics process of identifying and making business decision

within organization. It is helpful for all company by maintaining the proper records and transaction in

entire company. Management accounting comprehends various methods and concepts which are

necessary for set up a business with controlling the business activities. It help to evaluate the data and

interpretation in order to make profitable company. Moreover, it gives financial and non-financial

information that help to take right action. Such as Airdri is the hand drier manufacturer company which is

using different types of management accounting system for making right business decision

(Abdelmoneim Mohamed and Jones, 2014). The different types of management accounting system

are follows by Airdri company that are:

Inventory management system: This is a system which is used to keeping records of inventory like raw

material, finished goods or unfinished goods. This is mainly used in manufacturing company to maintain

the records of stock which are available in a organization. It helps in stock forecasting, automatic

reordering, , materials tracking inventory alerts and many more for keeping records within organization. It

is essential required in Airdri as it help to keep and maintain the records of inventory

(Bagautdinova,Kundakchyan and Malakhov,2013). The manager of Airdri track the inventory and

make further decision for placing next order. It considers various method to use the stock like:

LIFO: It means last in first out which can be used by company to sell the products.

FIFO: It mean sell first in first out that can be used by company to sell the first ordered products.

Average: It means combination of price and units produced to sell the products within organization.

Job costing system: This means a specific contract, assignment or work which is needed to complete as

per customer’s requirement. This is the form of particular order costing which help to ascertain

the cost of individuals or jobs. It is required to maintain the records of specific jobs or contracts.

The manager of Airdri Ltd are using this system to make estimation of individual unit cost or

assignment in order to deliver hand driers. The essential requirement of such system in Airdri is

that it contains specialized rules which are applicable to all types of jobs and helps in estimation

of costs for ascertaining the jobs (Collis and Hussey, 2017).

Management accounting is the set of Management and accounts that help to know about business and it's

transactions. It is used to maintain the proper accounts with organization. The main purpose of

Management accounting is to give true and fair vies for increasing the profits in a firm (Bloomfield,

2015). To understand the importance of Management accounting Mazars has been taken that provides

consultants services to different companies and help to make correct business decision. Airdri Ltd is one

of its client which get suggestions to run a business and the report is based on this organization. This

report will cover different topics like management accounting system, reports and planning tools that can

be used to control the budget in a company. Moreover, report will discusses about financial problem

which can be occur in an organization while using system.

TASK 1

P1. Management accounting systems

Management accounting system is the systematics process of identifying and making business decision

within organization. It is helpful for all company by maintaining the proper records and transaction in

entire company. Management accounting comprehends various methods and concepts which are

necessary for set up a business with controlling the business activities. It help to evaluate the data and

interpretation in order to make profitable company. Moreover, it gives financial and non-financial

information that help to take right action. Such as Airdri is the hand drier manufacturer company which is

using different types of management accounting system for making right business decision

(Abdelmoneim Mohamed and Jones, 2014). The different types of management accounting system

are follows by Airdri company that are:

Inventory management system: This is a system which is used to keeping records of inventory like raw

material, finished goods or unfinished goods. This is mainly used in manufacturing company to maintain

the records of stock which are available in a organization. It helps in stock forecasting, automatic

reordering, , materials tracking inventory alerts and many more for keeping records within organization. It

is essential required in Airdri as it help to keep and maintain the records of inventory

(Bagautdinova,Kundakchyan and Malakhov,2013). The manager of Airdri track the inventory and

make further decision for placing next order. It considers various method to use the stock like:

LIFO: It means last in first out which can be used by company to sell the products.

FIFO: It mean sell first in first out that can be used by company to sell the first ordered products.

Average: It means combination of price and units produced to sell the products within organization.

Job costing system: This means a specific contract, assignment or work which is needed to complete as

per customer’s requirement. This is the form of particular order costing which help to ascertain

the cost of individuals or jobs. It is required to maintain the records of specific jobs or contracts.

The manager of Airdri Ltd are using this system to make estimation of individual unit cost or

assignment in order to deliver hand driers. The essential requirement of such system in Airdri is

that it contains specialized rules which are applicable to all types of jobs and helps in estimation

of costs for ascertaining the jobs (Collis and Hussey, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting system: This system is used to estimate the cost of products and services for the

valuation of stock, analyzing the cost and maintaining the profitability. It is very important for

organization to maintain the cost of organization as well as products. It is essential required for

Airdri and other organization to manage the cost in order to increase the profitability. The

manager of Airdri uses such system to is to estimate as well as record the costs like variable cost

and fixed cost (Demski, 2013).

P2 Different methodologies used in management accounting reporting

Management accounting reports means reports which are prepared by the manager of the organization in

order to make business decision. The main purpose of this reports is to give the inside

information which is received through financial accounting. In Airdri, managers prepares

different types of reports which is described below:

Inventory Management Report: Inventory means goods which is manufactured by organization

in order to sale the products and services. the main aim of preparing this report is to generate more

income with the help to preparing inventory management reports. In Airdri, managers prepare these

reports by containing all information which relates to maintenance and recording of inventory. Managers

also maintains proper records of inventory by using advanced technology. Ths report help to maintain the

proper records of all stock such as raw material finished goods etc and prepare inventory reports

(Kanellou and Spathis, 2013).

Cost accounting report: This means a report that can be used to collect, classify, analysis and

reporting the data for ascertaining the cost of products and services. It helps to calculate the cost

efficiently and manage the cost within industry. In Airdri, managers prepares cost accounting reports for

allocating the cost in to various cost centers and maintaining the cost trend within company. This report is

useful to calculate the cost of products and help to make further business transactions (Maher, M. W.,

Stickney and Weil, 2012).

Performance Report: This report is prepared by managers to analysis the performance of

company as well as employees who help to accomplish the goals. It is mainly used for evaluating the

efficiency of industry and improve the performance that help to make profitable organization. In Airdri,

managers build such type of report that help to maintain the performance of activities and make

improvements as per requirement. Moreover, this report helps to control the cost and managing the

workforce in order to increase the productivity (Malinić and Todorović, 2012).

TASK 2

P3 Calculations of costs using appropriate techniques to prepare income statement

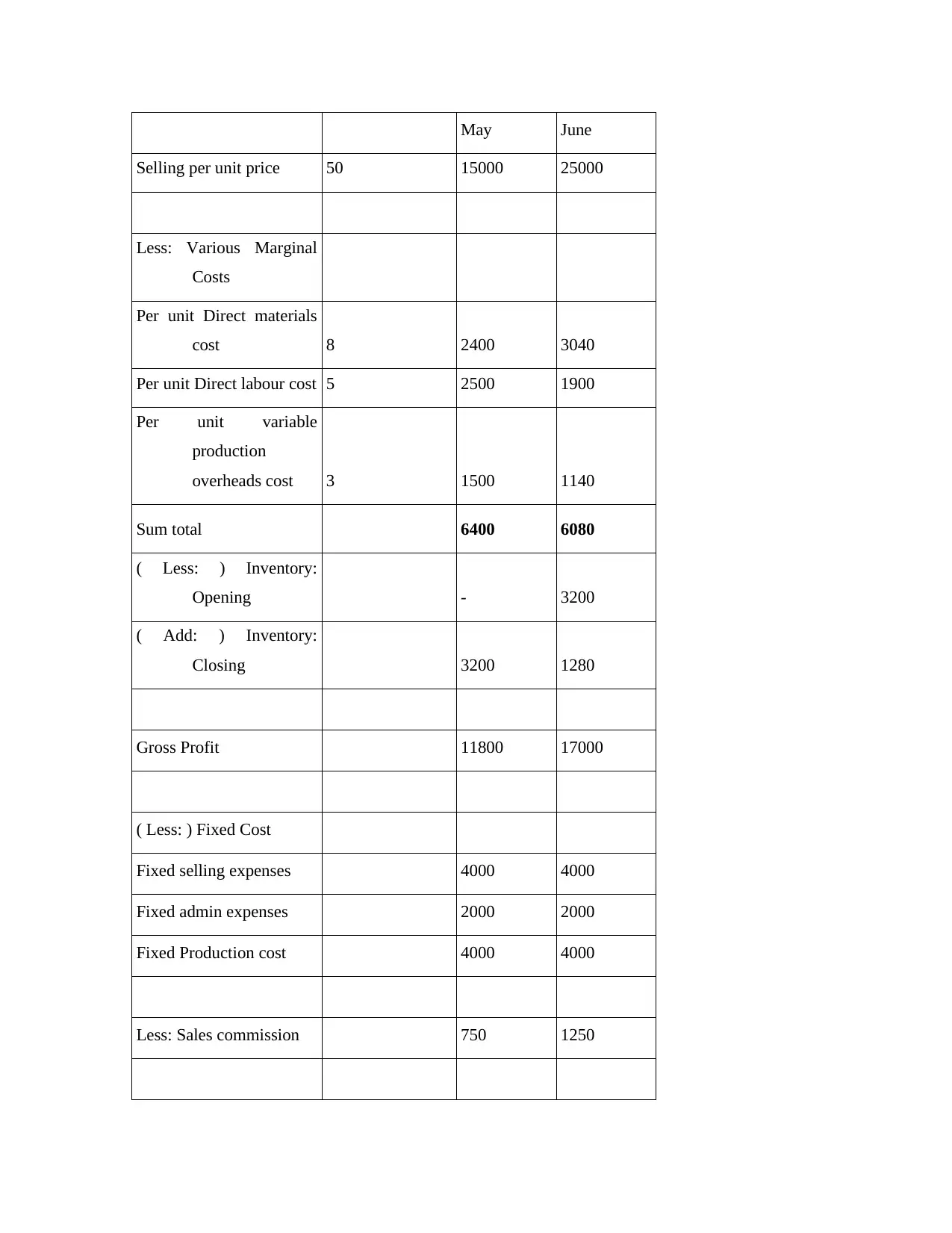

Marginal Costing: This is a costing method which can be used to know the profits of a organization. It

involves a systematic classification of expenses and cost a fixed and variable contribution per

unit.

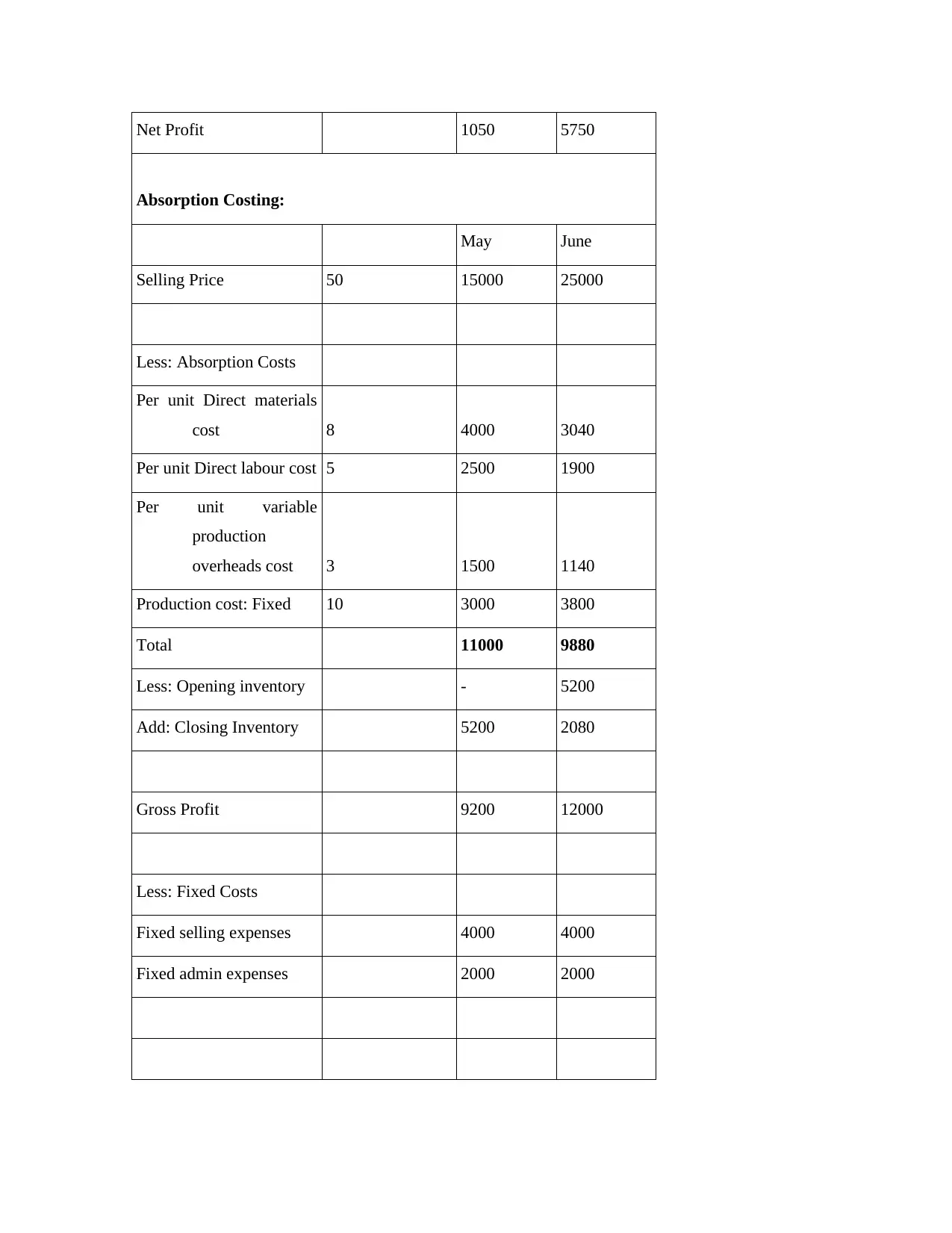

Absorption Costing: This is another method that defines profits of the organization after analyzing the

cost. In this method, all overheads are relates with production or unit cost of products. Herein, no

classification of expenses is needed in fixed and variable cost (Bargate, 2012).

valuation of stock, analyzing the cost and maintaining the profitability. It is very important for

organization to maintain the cost of organization as well as products. It is essential required for

Airdri and other organization to manage the cost in order to increase the profitability. The

manager of Airdri uses such system to is to estimate as well as record the costs like variable cost

and fixed cost (Demski, 2013).

P2 Different methodologies used in management accounting reporting

Management accounting reports means reports which are prepared by the manager of the organization in

order to make business decision. The main purpose of this reports is to give the inside

information which is received through financial accounting. In Airdri, managers prepares

different types of reports which is described below:

Inventory Management Report: Inventory means goods which is manufactured by organization

in order to sale the products and services. the main aim of preparing this report is to generate more

income with the help to preparing inventory management reports. In Airdri, managers prepare these

reports by containing all information which relates to maintenance and recording of inventory. Managers

also maintains proper records of inventory by using advanced technology. Ths report help to maintain the

proper records of all stock such as raw material finished goods etc and prepare inventory reports

(Kanellou and Spathis, 2013).

Cost accounting report: This means a report that can be used to collect, classify, analysis and

reporting the data for ascertaining the cost of products and services. It helps to calculate the cost

efficiently and manage the cost within industry. In Airdri, managers prepares cost accounting reports for

allocating the cost in to various cost centers and maintaining the cost trend within company. This report is

useful to calculate the cost of products and help to make further business transactions (Maher, M. W.,

Stickney and Weil, 2012).

Performance Report: This report is prepared by managers to analysis the performance of

company as well as employees who help to accomplish the goals. It is mainly used for evaluating the

efficiency of industry and improve the performance that help to make profitable organization. In Airdri,

managers build such type of report that help to maintain the performance of activities and make

improvements as per requirement. Moreover, this report helps to control the cost and managing the

workforce in order to increase the productivity (Malinić and Todorović, 2012).

TASK 2

P3 Calculations of costs using appropriate techniques to prepare income statement

Marginal Costing: This is a costing method which can be used to know the profits of a organization. It

involves a systematic classification of expenses and cost a fixed and variable contribution per

unit.

Absorption Costing: This is another method that defines profits of the organization after analyzing the

cost. In this method, all overheads are relates with production or unit cost of products. Herein, no

classification of expenses is needed in fixed and variable cost (Bargate, 2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

May June

Selling per unit price 50 15000 25000

Less: Various Marginal

Costs

Per unit Direct materials

cost 8 2400 3040

Per unit Direct labour cost 5 2500 1900

Per unit variable

production

overheads cost 3 1500 1140

Sum total 6400 6080

( Less: ) Inventory:

Opening - 3200

( Add: ) Inventory:

Closing 3200 1280

Gross Profit 11800 17000

( Less: ) Fixed Cost

Fixed selling expenses 4000 4000

Fixed admin expenses 2000 2000

Fixed Production cost 4000 4000

Less: Sales commission 750 1250

Selling per unit price 50 15000 25000

Less: Various Marginal

Costs

Per unit Direct materials

cost 8 2400 3040

Per unit Direct labour cost 5 2500 1900

Per unit variable

production

overheads cost 3 1500 1140

Sum total 6400 6080

( Less: ) Inventory:

Opening - 3200

( Add: ) Inventory:

Closing 3200 1280

Gross Profit 11800 17000

( Less: ) Fixed Cost

Fixed selling expenses 4000 4000

Fixed admin expenses 2000 2000

Fixed Production cost 4000 4000

Less: Sales commission 750 1250

Net Profit 1050 5750

Absorption Costing:

May June

Selling Price 50 15000 25000

Less: Absorption Costs

Per unit Direct materials

cost 8 4000 3040

Per unit Direct labour cost 5 2500 1900

Per unit variable

production

overheads cost 3 1500 1140

Production cost: Fixed 10 3000 3800

Total 11000 9880

Less: Opening inventory - 5200

Add: Closing Inventory 5200 2080

Gross Profit 9200 12000

Less: Fixed Costs

Fixed selling expenses 4000 4000

Fixed admin expenses 2000 2000

Absorption Costing:

May June

Selling Price 50 15000 25000

Less: Absorption Costs

Per unit Direct materials

cost 8 4000 3040

Per unit Direct labour cost 5 2500 1900

Per unit variable

production

overheads cost 3 1500 1140

Production cost: Fixed 10 3000 3800

Total 11000 9880

Less: Opening inventory - 5200

Add: Closing Inventory 5200 2080

Gross Profit 9200 12000

Less: Fixed Costs

Fixed selling expenses 4000 4000

Fixed admin expenses 2000 2000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Sales commission 750 1250

Net Profit 2450 4750

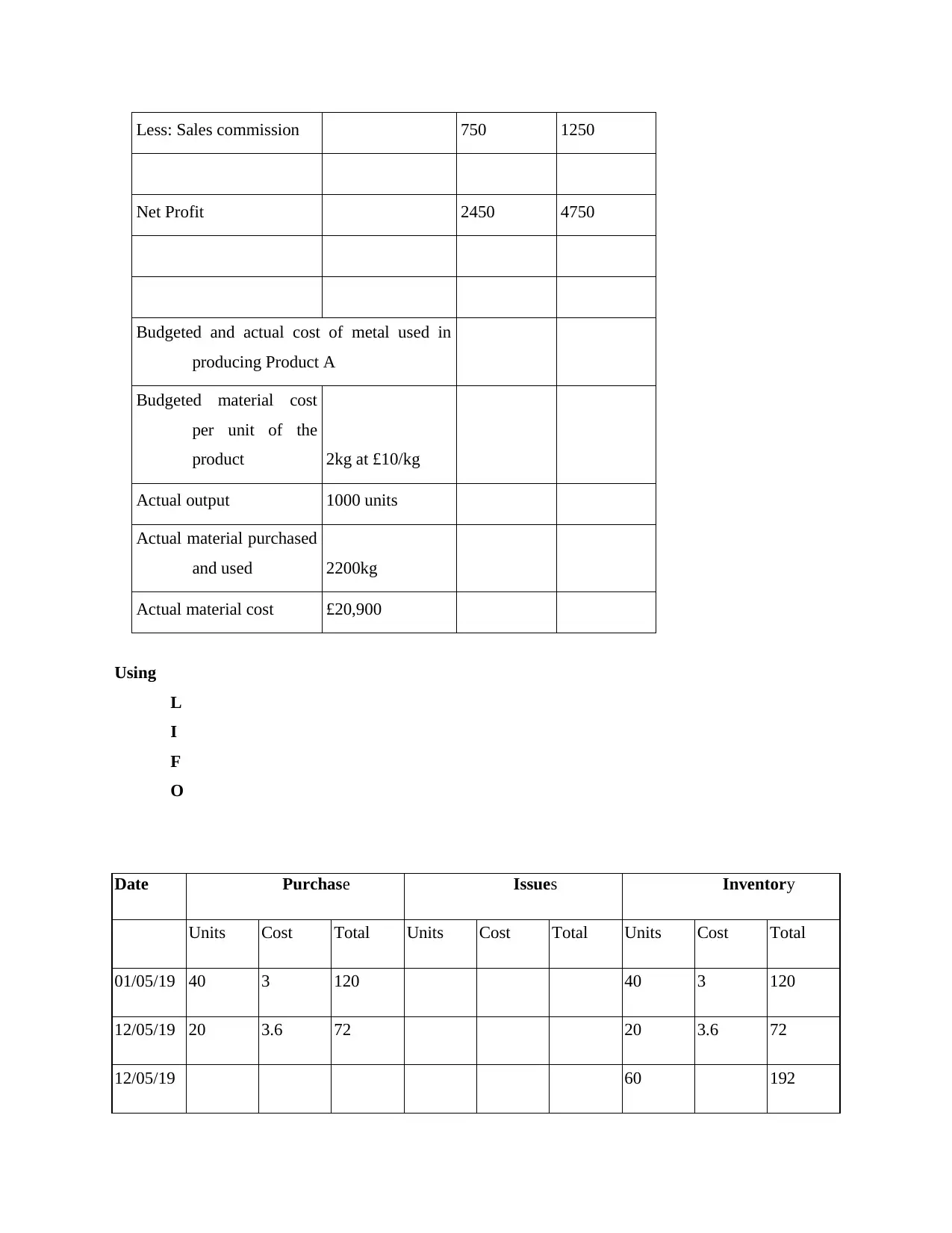

Budgeted and actual cost of metal used in

producing Product A

Budgeted material cost

per unit of the

product 2kg at £10/kg

Actual output 1000 units

Actual material purchased

and used 2200kg

Actual material cost £20,900

Using

L

I

F

O

Date Purchase Issues Inventory

Units Cost Total Units Cost Total Units Cost Total

01/05/19 40 3 120 40 3 120

12/05/19 20 3.6 72 20 3.6 72

12/05/19 60 192

Net Profit 2450 4750

Budgeted and actual cost of metal used in

producing Product A

Budgeted material cost

per unit of the

product 2kg at £10/kg

Actual output 1000 units

Actual material purchased

and used 2200kg

Actual material cost £20,900

Using

L

I

F

O

Date Purchase Issues Inventory

Units Cost Total Units Cost Total Units Cost Total

01/05/19 40 3 120 40 3 120

12/05/19 20 3.6 72 20 3.6 72

12/05/19 60 192

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

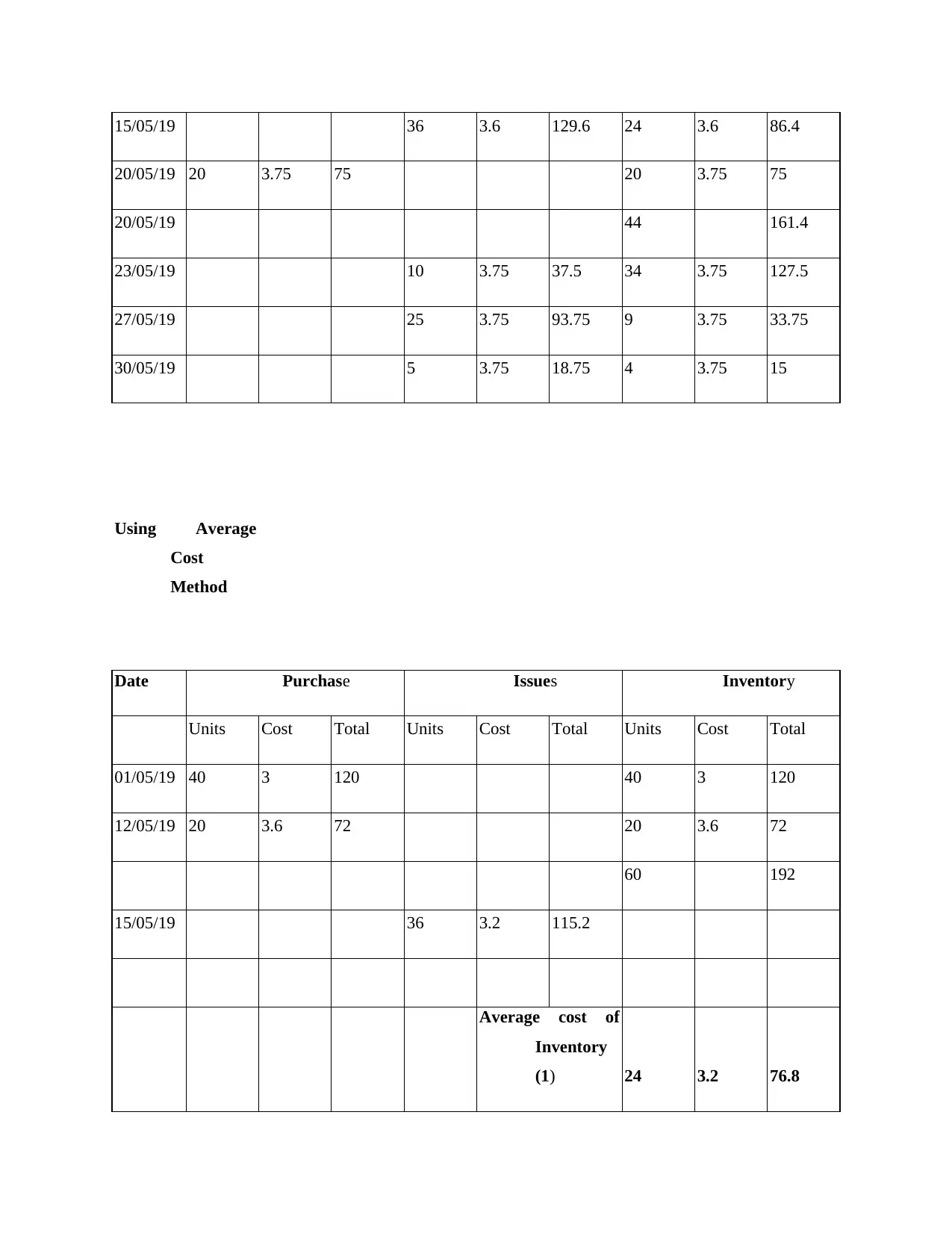

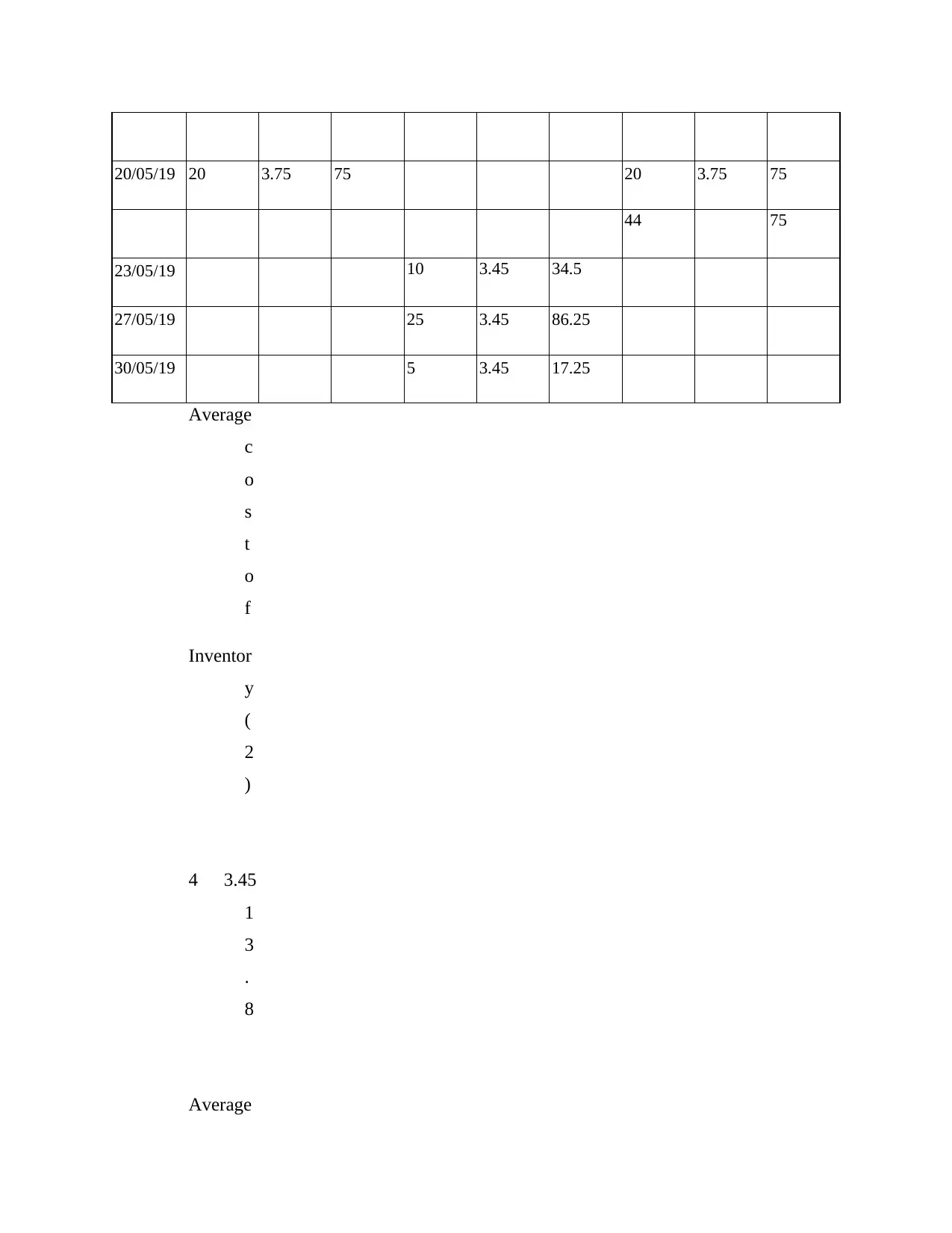

15/05/19 36 3.6 129.6 24 3.6 86.4

20/05/19 20 3.75 75 20 3.75 75

20/05/19 44 161.4

23/05/19 10 3.75 37.5 34 3.75 127.5

27/05/19 25 3.75 93.75 9 3.75 33.75

30/05/19 5 3.75 18.75 4 3.75 15

Using Average

Cost

Method

Date Purchase Issues Inventory

Units Cost Total Units Cost Total Units Cost Total

01/05/19 40 3 120 40 3 120

12/05/19 20 3.6 72 20 3.6 72

60 192

15/05/19 36 3.2 115.2

Average cost of

Inventory

(1) 24 3.2 76.8

20/05/19 20 3.75 75 20 3.75 75

20/05/19 44 161.4

23/05/19 10 3.75 37.5 34 3.75 127.5

27/05/19 25 3.75 93.75 9 3.75 33.75

30/05/19 5 3.75 18.75 4 3.75 15

Using Average

Cost

Method

Date Purchase Issues Inventory

Units Cost Total Units Cost Total Units Cost Total

01/05/19 40 3 120 40 3 120

12/05/19 20 3.6 72 20 3.6 72

60 192

15/05/19 36 3.2 115.2

Average cost of

Inventory

(1) 24 3.2 76.8

20/05/19 20 3.75 75 20 3.75 75

44 75

23/05/19 10 3.45 34.5

27/05/19 25 3.45 86.25

30/05/19 5 3.45 17.25

Average

c

o

s

t

o

f

Inventor

y

(

2

)

4 3.45

1

3

.

8

Average

44 75

23/05/19 10 3.45 34.5

27/05/19 25 3.45 86.25

30/05/19 5 3.45 17.25

Average

c

o

s

t

o

f

Inventor

y

(

2

)

4 3.45

1

3

.

8

Average

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

c

o

s

t

o

f

inventor

y

(

1

)

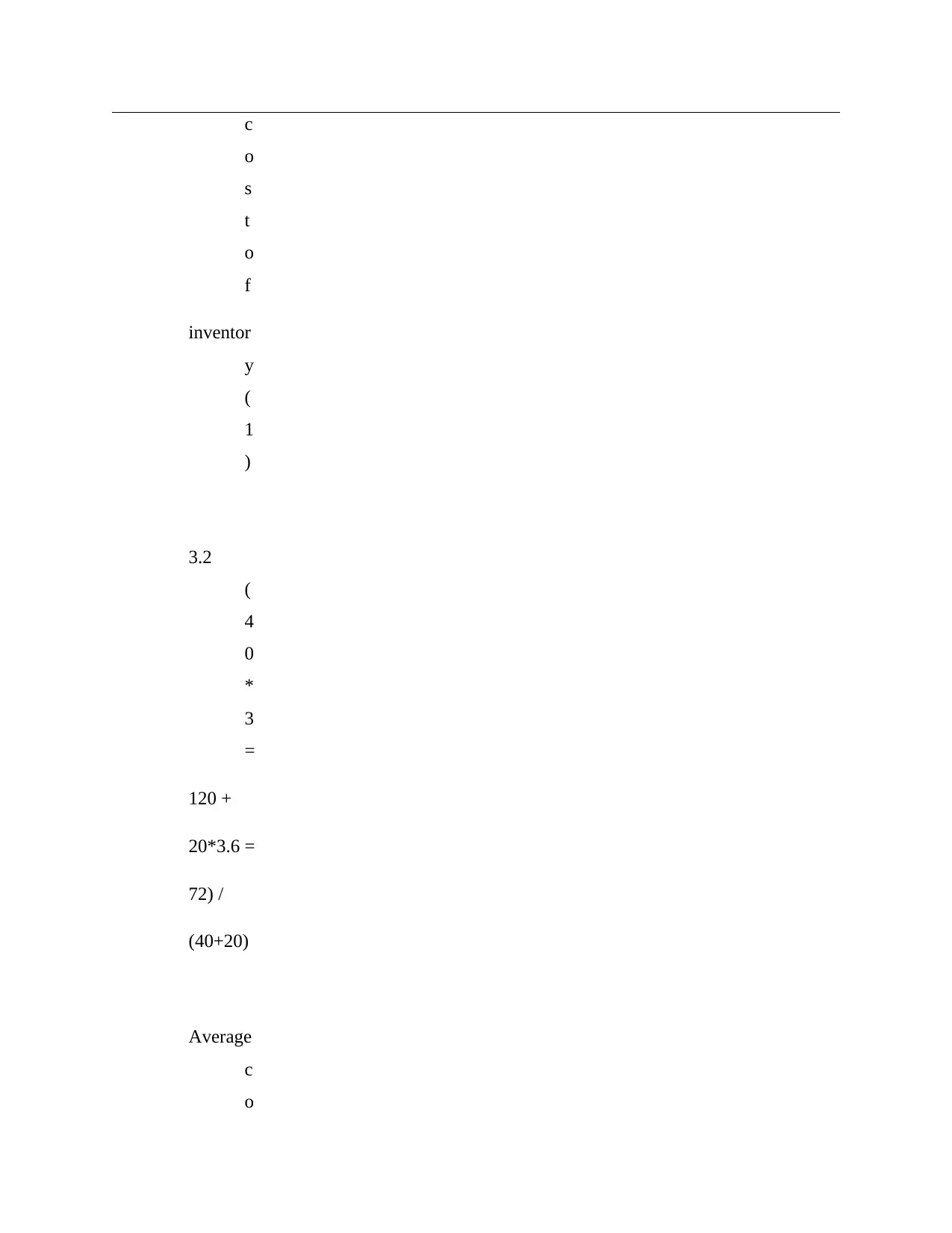

3.2

(

4

0

*

3

=

120 +

20*3.6 =

72) /

(40+20)

Average

c

o

o

s

t

o

f

inventor

y

(

1

)

3.2

(

4

0

*

3

=

120 +

20*3.6 =

72) /

(40+20)

Average

c

o

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

s

t

o

f

inventor

y

(

2

)

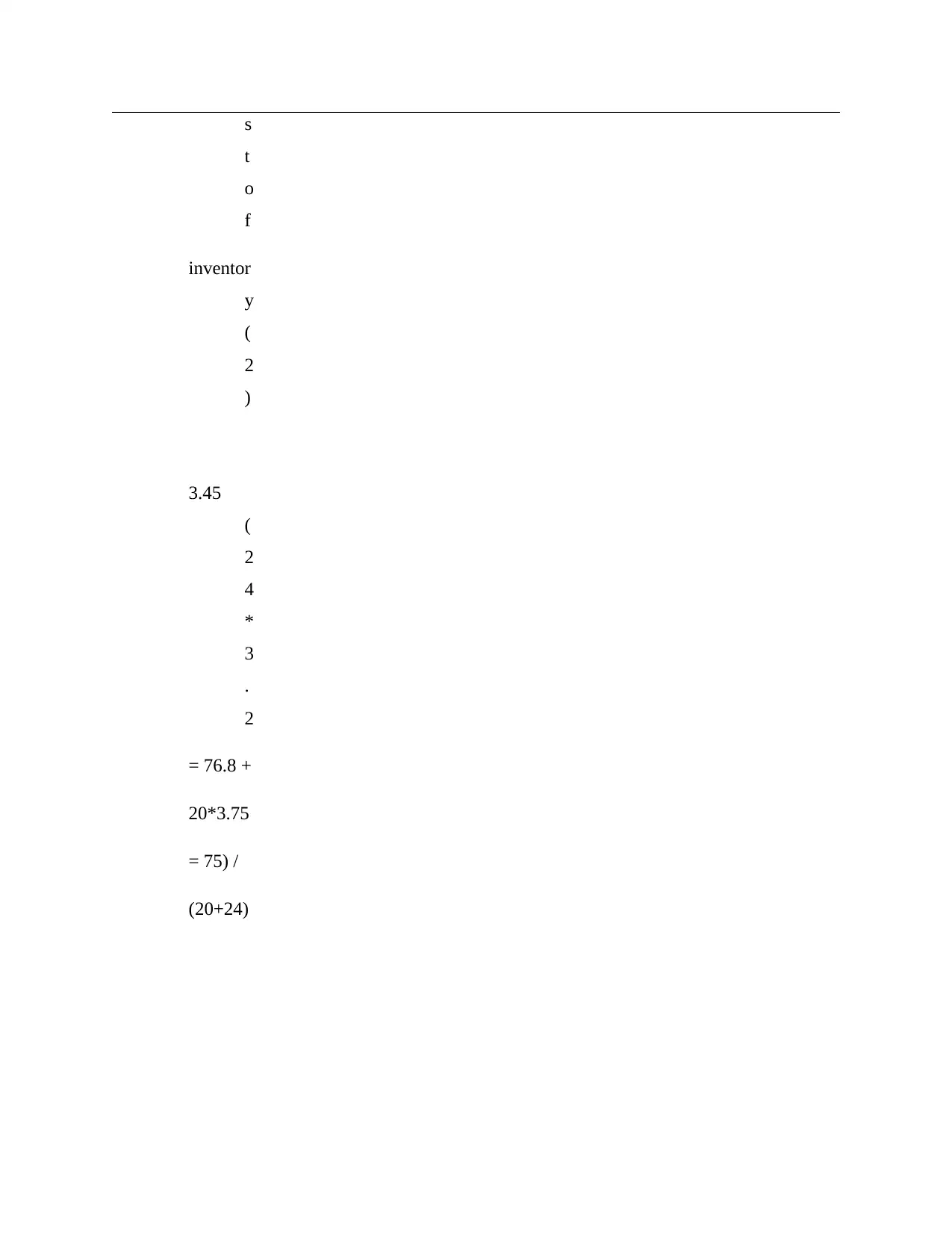

3.45

(

2

4

*

3

.

2

= 76.8 +

20*3.75

= 75) /

(20+24)

t

o

f

inventor

y

(

2

)

3.45

(

2

4

*

3

.

2

= 76.8 +

20*3.75

= 75) /

(20+24)

TASK 3

P4 Advantage and disadvantage of different types of planning tools used for budgetary control

Budget- Budget is the estimation of cost which is required in all industry. It is prepared by

business entity to evaluate the performance and set the budget within organization. The main

purpose of budget is to evaluate the actual performance of company for ascertaining the future

and take further actions. In Airdri, accountants analysis the past trends in order to increase

reliability and accuracy of budgets. It helps to build a strategy and formulate a actions plan for

increasing the profits margin. The manager of Airdri uses different planning tools to control over

budget and maintain the profits (Morden, 2016). The planning tools and it's merits or demerits

are follows as:

Cash budget: This means a budget which covers all cash transaction and information is consider

as cash budget. It is prepared by accountant or mangers to compute the real cash availability

within organization. It mainly focus on cash and its equivalent item that shows cash information.

In Airdri, managers uses this tool that helps to identify and improve the weak area that leads to

negative cash flow. This also help to handle the cash and provide information (Gullkvist, 2013).

Advantage: It helps Airdri to track the movement and flow of cash or it's equal items. Moreover,

it is helpful to increase the cash availability by monitoring the performance.

Disadvantage: It may be costly for company because it need to maintain the high cost. It may

be fail sometimes due to fraud which can be through accountant or managers of Airdri.

Operating budget: This budget is prepared by business entities while considering only

operational expenses and income incurred. It involves estimation of income and expenses which

are arises within industry due to monitoring on expenses. In Airdri, the manager firstly collects

all information and prepares different small budget. After making small budget managers

prepares operational budget that help to evaluate the operational efficiencies and capabilities of

entity. Such as Airdri is Manufacturer Company who prepares production budget, purchase and

sale budget that help to make a complete budget (Zoni, Dossi and Morelli, 2012). It help to

define the define the operational efficiencies of Airdri while using small budgets.

Advantage: It assist company to allocate the weak operational area and provide a basis for

removing the weakness. The manager of Airdri organise and control day to day activities

by focusing on operational budget.

Disadvantage: It maybe complex and time consuming budget because it involves numerous

budgets and information. Moreover, Airdri cannot control over weakness due to time

consuming procedure.

Master budget: This is more relevant and useful budget which is prepared by managers to focus

on financial statement of business entities. It is used to assess the combined and total

performance of organization. Such as manager of Airdri is using master budget to make

manufacturing and other business decision. Managers make plan for future by analysing

P4 Advantage and disadvantage of different types of planning tools used for budgetary control

Budget- Budget is the estimation of cost which is required in all industry. It is prepared by

business entity to evaluate the performance and set the budget within organization. The main

purpose of budget is to evaluate the actual performance of company for ascertaining the future

and take further actions. In Airdri, accountants analysis the past trends in order to increase

reliability and accuracy of budgets. It helps to build a strategy and formulate a actions plan for

increasing the profits margin. The manager of Airdri uses different planning tools to control over

budget and maintain the profits (Morden, 2016). The planning tools and it's merits or demerits

are follows as:

Cash budget: This means a budget which covers all cash transaction and information is consider

as cash budget. It is prepared by accountant or mangers to compute the real cash availability

within organization. It mainly focus on cash and its equivalent item that shows cash information.

In Airdri, managers uses this tool that helps to identify and improve the weak area that leads to

negative cash flow. This also help to handle the cash and provide information (Gullkvist, 2013).

Advantage: It helps Airdri to track the movement and flow of cash or it's equal items. Moreover,

it is helpful to increase the cash availability by monitoring the performance.

Disadvantage: It may be costly for company because it need to maintain the high cost. It may

be fail sometimes due to fraud which can be through accountant or managers of Airdri.

Operating budget: This budget is prepared by business entities while considering only

operational expenses and income incurred. It involves estimation of income and expenses which

are arises within industry due to monitoring on expenses. In Airdri, the manager firstly collects

all information and prepares different small budget. After making small budget managers

prepares operational budget that help to evaluate the operational efficiencies and capabilities of

entity. Such as Airdri is Manufacturer Company who prepares production budget, purchase and

sale budget that help to make a complete budget (Zoni, Dossi and Morelli, 2012). It help to

define the define the operational efficiencies of Airdri while using small budgets.

Advantage: It assist company to allocate the weak operational area and provide a basis for

removing the weakness. The manager of Airdri organise and control day to day activities

by focusing on operational budget.

Disadvantage: It maybe complex and time consuming budget because it involves numerous

budgets and information. Moreover, Airdri cannot control over weakness due to time

consuming procedure.

Master budget: This is more relevant and useful budget which is prepared by managers to focus

on financial statement of business entities. It is used to assess the combined and total

performance of organization. Such as manager of Airdri is using master budget to make

manufacturing and other business decision. Managers make plan for future by analysing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.