Comprehensive Business Report: Analysis of T-Shirt Ltd's Performance

VerifiedAdded on 2023/01/05

|12

|3284

|22

Report

AI Summary

This report offers a comprehensive analysis of T-Shirt Ltd's financial performance. It begins with an examination of the statement of profit or loss and the statement of financial position, including a detailed ratio analysis of key metrics such as current ratio, quick ratio, gross profit margin, and return on assets, highlighting the company's declining financial health. The report then delves into understanding financial information, contrasting accrual and cash accounting, and differentiating between profit and cash flow. Furthermore, it explores budget techniques, the purpose of budgeting, and the advantages of forming a limited company and listing it on a stock exchange. The analysis reveals significant financial challenges for T-Shirt Ltd, including declining revenues, increasing costs, and a shift from profitability to losses, emphasizing the need for immediate strategic interventions to improve financial performance and avoid potential bankruptcy.

Business report analysis and

business advice

business advice

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PART 1: BUSINESS PERFORMANCE ANALYSIS..............................................................3

1.1 Statement of Profit or Loss..............................................................................................3

1.2 Statement of Financial Position.......................................................................................5

PART 2: UNDERSTANDING FINANCIAL INFORMATION & MANAGEMENT OF

CASH.........................................................................................................................................6

2.1 Understanding the concept of accrual accounting vs cash accounting............................6

2.2 Meaning and differences between the profit and cash flow.............................................7

PART3: BUDGET TECHNIQUES AND COMPANY FINANCE..........................................8

3.1 Budget and purpose of preparing it..................................................................................8

3.2 Benefits of forming a limited company and listing it on a stock exchange.....................8

REFERENCES.........................................................................................................................10

APPENDIX..............................................................................................................................11

PART 1: BUSINESS PERFORMANCE ANALYSIS..............................................................3

1.1 Statement of Profit or Loss..............................................................................................3

1.2 Statement of Financial Position.......................................................................................5

PART 2: UNDERSTANDING FINANCIAL INFORMATION & MANAGEMENT OF

CASH.........................................................................................................................................6

2.1 Understanding the concept of accrual accounting vs cash accounting............................6

2.2 Meaning and differences between the profit and cash flow.............................................7

PART3: BUDGET TECHNIQUES AND COMPANY FINANCE..........................................8

3.1 Budget and purpose of preparing it..................................................................................8

3.2 Benefits of forming a limited company and listing it on a stock exchange.....................8

REFERENCES.........................................................................................................................10

APPENDIX..............................................................................................................................11

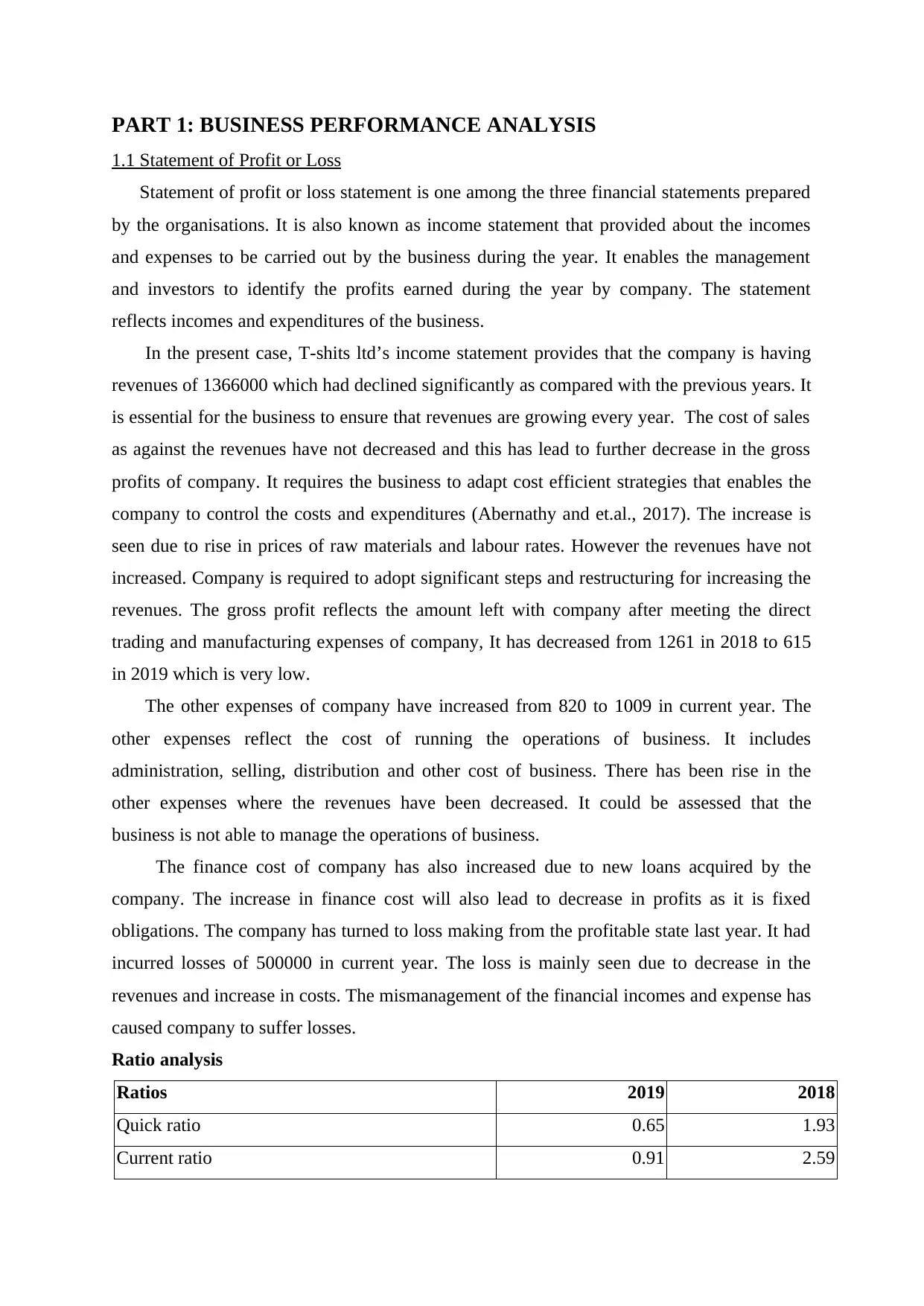

PART 1: BUSINESS PERFORMANCE ANALYSIS

1.1 Statement of Profit or Loss

Statement of profit or loss statement is one among the three financial statements prepared

by the organisations. It is also known as income statement that provided about the incomes

and expenses to be carried out by the business during the year. It enables the management

and investors to identify the profits earned during the year by company. The statement

reflects incomes and expenditures of the business.

In the present case, T-shits ltd’s income statement provides that the company is having

revenues of 1366000 which had declined significantly as compared with the previous years. It

is essential for the business to ensure that revenues are growing every year. The cost of sales

as against the revenues have not decreased and this has lead to further decrease in the gross

profits of company. It requires the business to adapt cost efficient strategies that enables the

company to control the costs and expenditures (Abernathy and et.al., 2017). The increase is

seen due to rise in prices of raw materials and labour rates. However the revenues have not

increased. Company is required to adopt significant steps and restructuring for increasing the

revenues. The gross profit reflects the amount left with company after meeting the direct

trading and manufacturing expenses of company, It has decreased from 1261 in 2018 to 615

in 2019 which is very low.

The other expenses of company have increased from 820 to 1009 in current year. The

other expenses reflect the cost of running the operations of business. It includes

administration, selling, distribution and other cost of business. There has been rise in the

other expenses where the revenues have been decreased. It could be assessed that the

business is not able to manage the operations of business.

The finance cost of company has also increased due to new loans acquired by the

company. The increase in finance cost will also lead to decrease in profits as it is fixed

obligations. The company has turned to loss making from the profitable state last year. It had

incurred losses of 500000 in current year. The loss is mainly seen due to decrease in the

revenues and increase in costs. The mismanagement of the financial incomes and expense has

caused company to suffer losses.

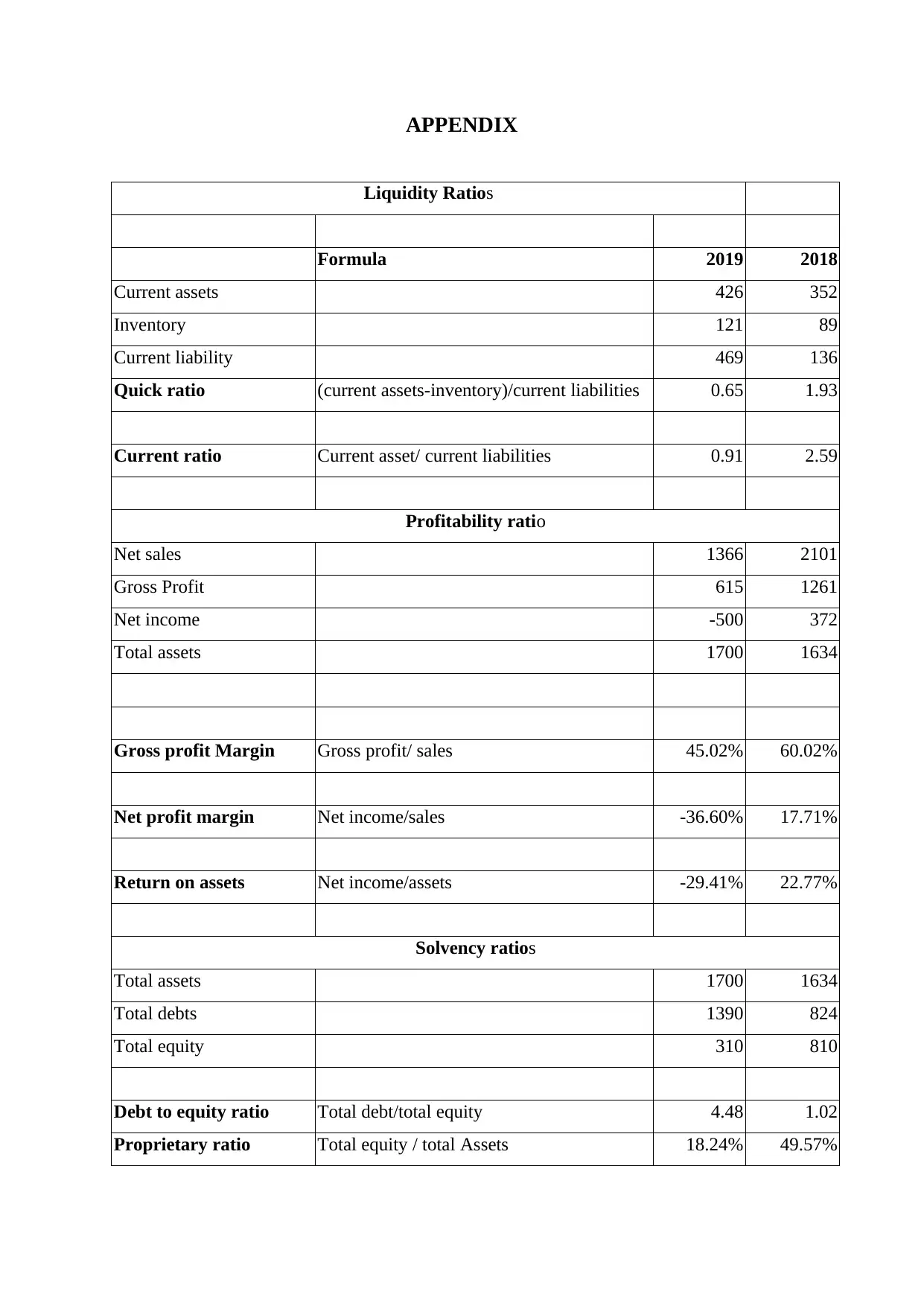

Ratio analysis

Ratios 2019 2018

Quick ratio 0.65 1.93

Current ratio 0.91 2.59

1.1 Statement of Profit or Loss

Statement of profit or loss statement is one among the three financial statements prepared

by the organisations. It is also known as income statement that provided about the incomes

and expenses to be carried out by the business during the year. It enables the management

and investors to identify the profits earned during the year by company. The statement

reflects incomes and expenditures of the business.

In the present case, T-shits ltd’s income statement provides that the company is having

revenues of 1366000 which had declined significantly as compared with the previous years. It

is essential for the business to ensure that revenues are growing every year. The cost of sales

as against the revenues have not decreased and this has lead to further decrease in the gross

profits of company. It requires the business to adapt cost efficient strategies that enables the

company to control the costs and expenditures (Abernathy and et.al., 2017). The increase is

seen due to rise in prices of raw materials and labour rates. However the revenues have not

increased. Company is required to adopt significant steps and restructuring for increasing the

revenues. The gross profit reflects the amount left with company after meeting the direct

trading and manufacturing expenses of company, It has decreased from 1261 in 2018 to 615

in 2019 which is very low.

The other expenses of company have increased from 820 to 1009 in current year. The

other expenses reflect the cost of running the operations of business. It includes

administration, selling, distribution and other cost of business. There has been rise in the

other expenses where the revenues have been decreased. It could be assessed that the

business is not able to manage the operations of business.

The finance cost of company has also increased due to new loans acquired by the

company. The increase in finance cost will also lead to decrease in profits as it is fixed

obligations. The company has turned to loss making from the profitable state last year. It had

incurred losses of 500000 in current year. The loss is mainly seen due to decrease in the

revenues and increase in costs. The mismanagement of the financial incomes and expense has

caused company to suffer losses.

Ratio analysis

Ratios 2019 2018

Quick ratio 0.65 1.93

Current ratio 0.91 2.59

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

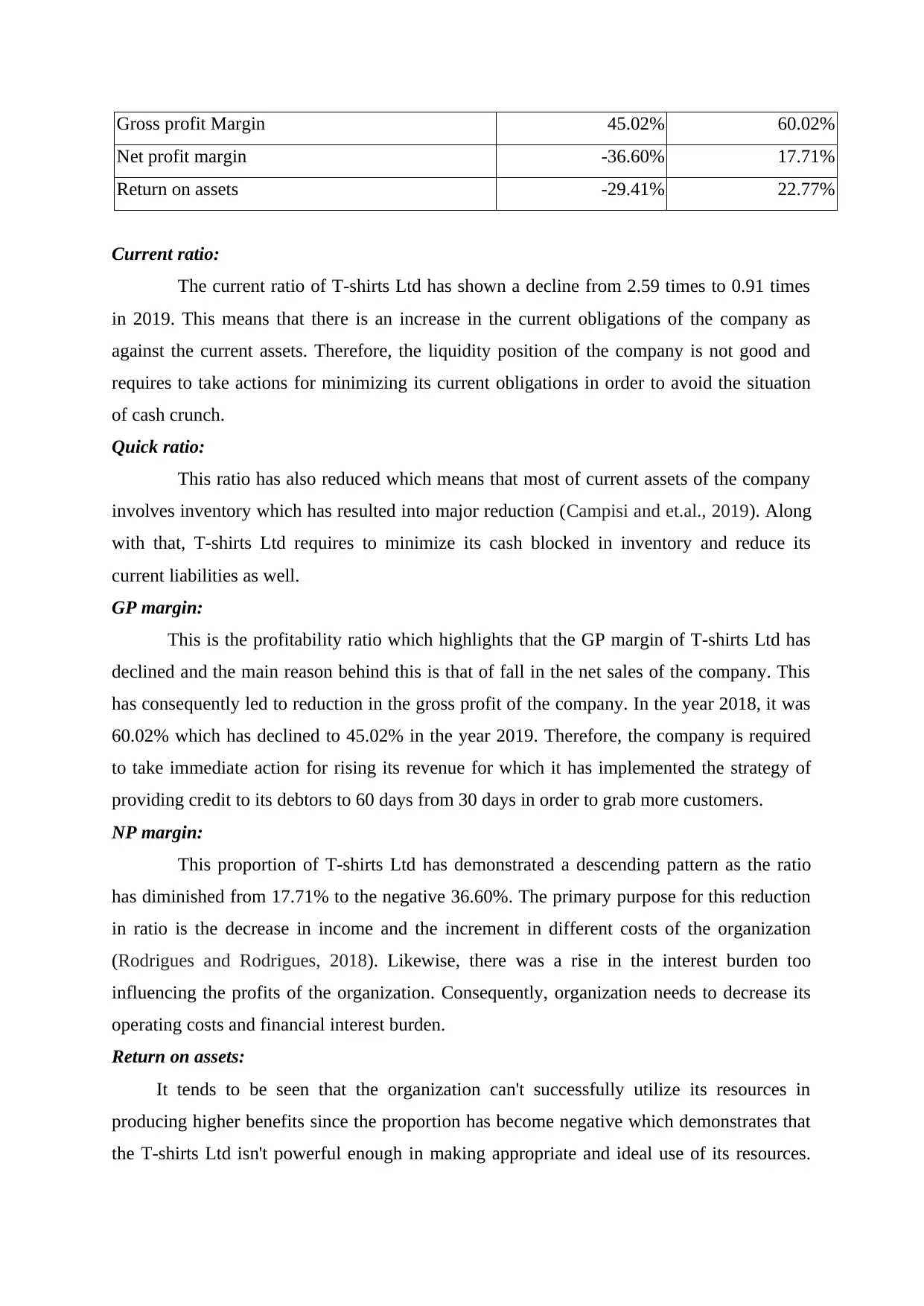

Gross profit Margin 45.02% 60.02%

Net profit margin -36.60% 17.71%

Return on assets -29.41% 22.77%

Current ratio:

The current ratio of T-shirts Ltd has shown a decline from 2.59 times to 0.91 times

in 2019. This means that there is an increase in the current obligations of the company as

against the current assets. Therefore, the liquidity position of the company is not good and

requires to take actions for minimizing its current obligations in order to avoid the situation

of cash crunch.

Quick ratio:

This ratio has also reduced which means that most of current assets of the company

involves inventory which has resulted into major reduction (Campisi and et.al., 2019). Along

with that, T-shirts Ltd requires to minimize its cash blocked in inventory and reduce its

current liabilities as well.

GP margin:

This is the profitability ratio which highlights that the GP margin of T-shirts Ltd has

declined and the main reason behind this is that of fall in the net sales of the company. This

has consequently led to reduction in the gross profit of the company. In the year 2018, it was

60.02% which has declined to 45.02% in the year 2019. Therefore, the company is required

to take immediate action for rising its revenue for which it has implemented the strategy of

providing credit to its debtors to 60 days from 30 days in order to grab more customers.

NP margin:

This proportion of T-shirts Ltd has demonstrated a descending pattern as the ratio

has diminished from 17.71% to the negative 36.60%. The primary purpose for this reduction

in ratio is the decrease in income and the increment in different costs of the organization

(Rodrigues and Rodrigues, 2018). Likewise, there was a rise in the interest burden too

influencing the profits of the organization. Consequently, organization needs to decrease its

operating costs and financial interest burden.

Return on assets:

It tends to be seen that the organization can't successfully utilize its resources in

producing higher benefits since the proportion has become negative which demonstrates that

the T-shirts Ltd isn't powerful enough in making appropriate and ideal use of its resources.

Net profit margin -36.60% 17.71%

Return on assets -29.41% 22.77%

Current ratio:

The current ratio of T-shirts Ltd has shown a decline from 2.59 times to 0.91 times

in 2019. This means that there is an increase in the current obligations of the company as

against the current assets. Therefore, the liquidity position of the company is not good and

requires to take actions for minimizing its current obligations in order to avoid the situation

of cash crunch.

Quick ratio:

This ratio has also reduced which means that most of current assets of the company

involves inventory which has resulted into major reduction (Campisi and et.al., 2019). Along

with that, T-shirts Ltd requires to minimize its cash blocked in inventory and reduce its

current liabilities as well.

GP margin:

This is the profitability ratio which highlights that the GP margin of T-shirts Ltd has

declined and the main reason behind this is that of fall in the net sales of the company. This

has consequently led to reduction in the gross profit of the company. In the year 2018, it was

60.02% which has declined to 45.02% in the year 2019. Therefore, the company is required

to take immediate action for rising its revenue for which it has implemented the strategy of

providing credit to its debtors to 60 days from 30 days in order to grab more customers.

NP margin:

This proportion of T-shirts Ltd has demonstrated a descending pattern as the ratio

has diminished from 17.71% to the negative 36.60%. The primary purpose for this reduction

in ratio is the decrease in income and the increment in different costs of the organization

(Rodrigues and Rodrigues, 2018). Likewise, there was a rise in the interest burden too

influencing the profits of the organization. Consequently, organization needs to decrease its

operating costs and financial interest burden.

Return on assets:

It tends to be seen that the organization can't successfully utilize its resources in

producing higher benefits since the proportion has become negative which demonstrates that

the T-shirts Ltd isn't powerful enough in making appropriate and ideal use of its resources.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

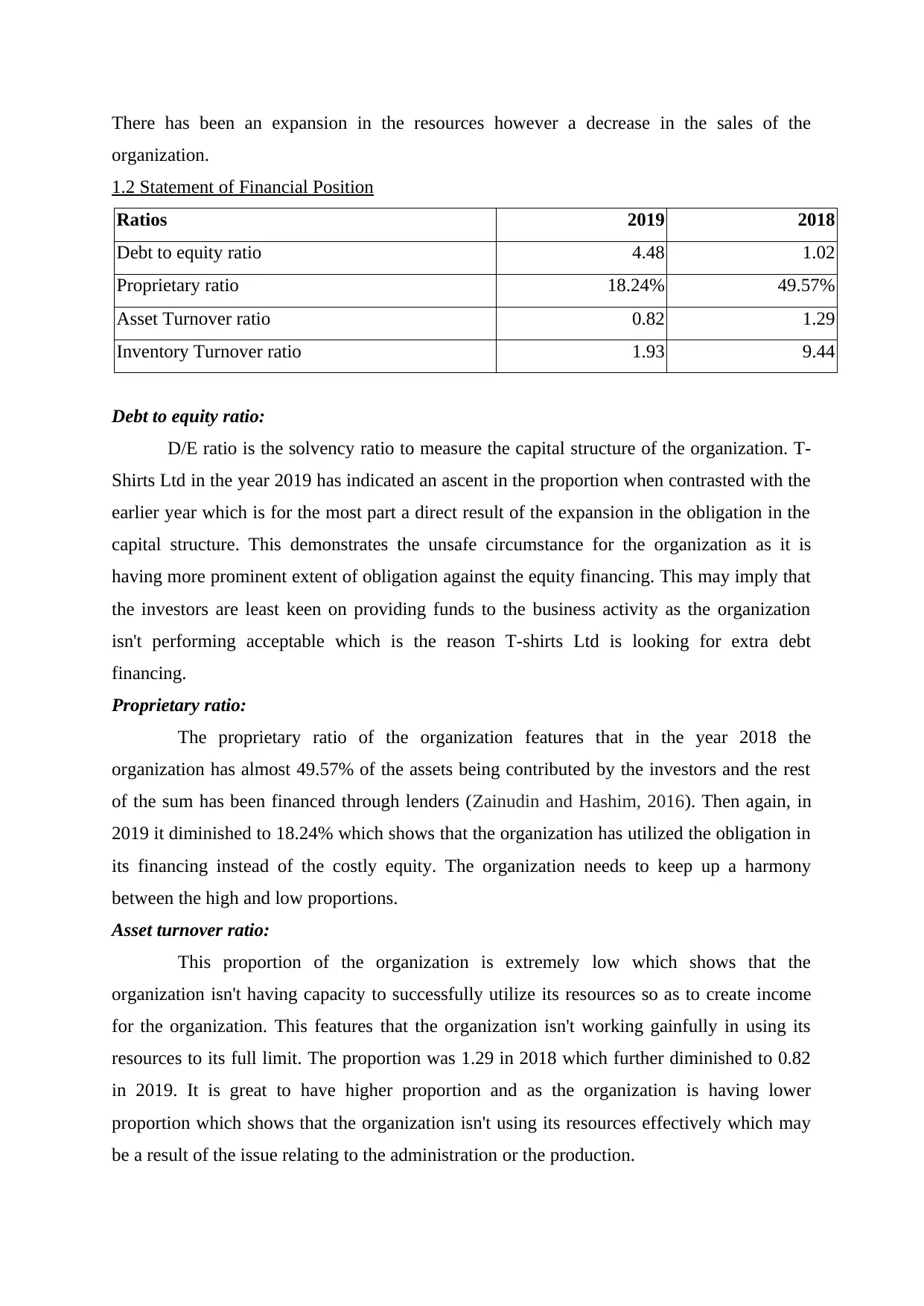

There has been an expansion in the resources however a decrease in the sales of the

organization.

1.2 Statement of Financial Position

Ratios 2019 2018

Debt to equity ratio 4.48 1.02

Proprietary ratio 18.24% 49.57%

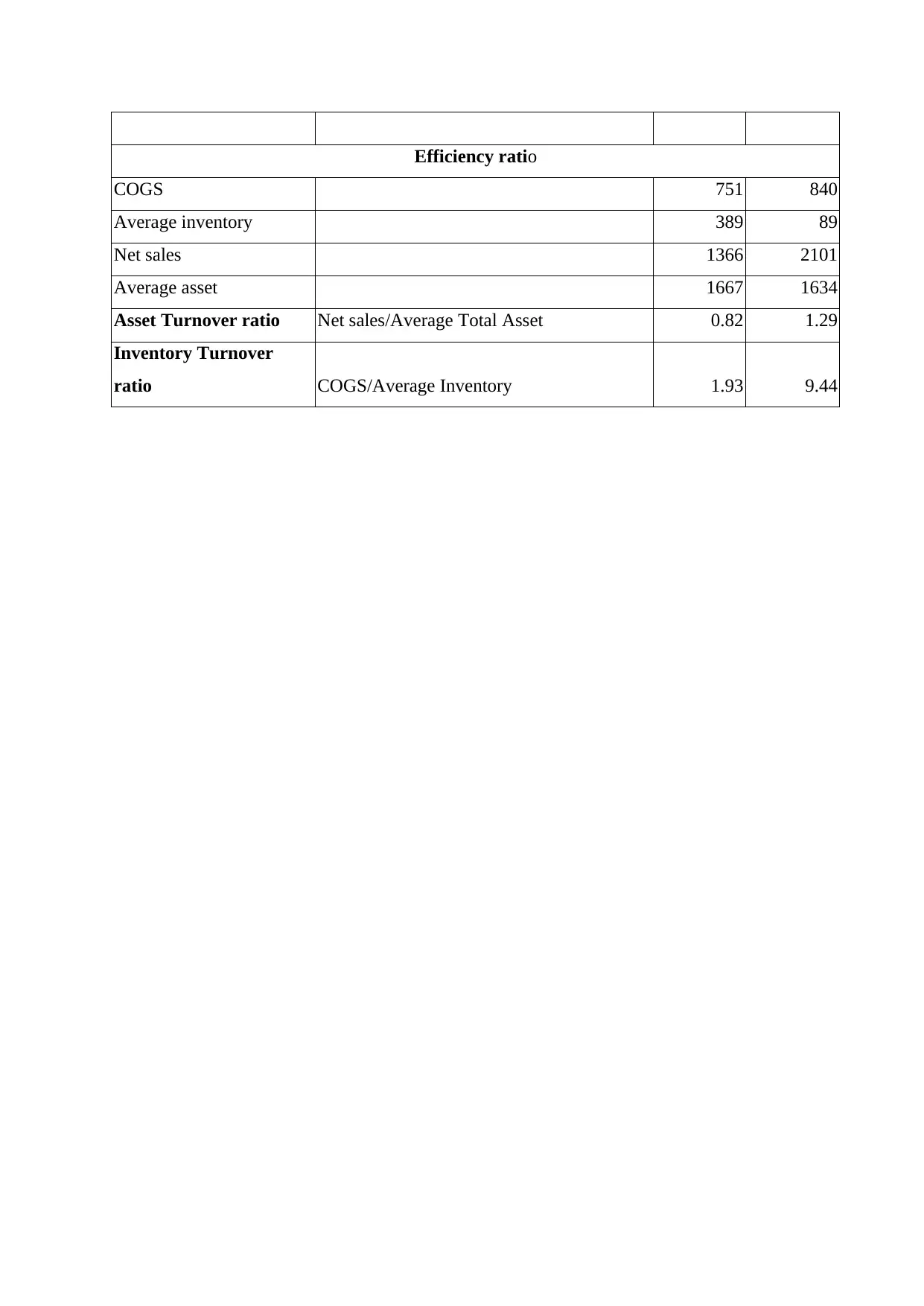

Asset Turnover ratio 0.82 1.29

Inventory Turnover ratio 1.93 9.44

Debt to equity ratio:

D/E ratio is the solvency ratio to measure the capital structure of the organization. T-

Shirts Ltd in the year 2019 has indicated an ascent in the proportion when contrasted with the

earlier year which is for the most part a direct result of the expansion in the obligation in the

capital structure. This demonstrates the unsafe circumstance for the organization as it is

having more prominent extent of obligation against the equity financing. This may imply that

the investors are least keen on providing funds to the business activity as the organization

isn't performing acceptable which is the reason T-shirts Ltd is looking for extra debt

financing.

Proprietary ratio:

The proprietary ratio of the organization features that in the year 2018 the

organization has almost 49.57% of the assets being contributed by the investors and the rest

of the sum has been financed through lenders (Zainudin and Hashim, 2016). Then again, in

2019 it diminished to 18.24% which shows that the organization has utilized the obligation in

its financing instead of the costly equity. The organization needs to keep up a harmony

between the high and low proportions.

Asset turnover ratio:

This proportion of the organization is extremely low which shows that the

organization isn't having capacity to successfully utilize its resources so as to create income

for the organization. This features that the organization isn't working gainfully in using its

resources to its full limit. The proportion was 1.29 in 2018 which further diminished to 0.82

in 2019. It is great to have higher proportion and as the organization is having lower

proportion which shows that the organization isn't using its resources effectively which may

be a result of the issue relating to the administration or the production.

organization.

1.2 Statement of Financial Position

Ratios 2019 2018

Debt to equity ratio 4.48 1.02

Proprietary ratio 18.24% 49.57%

Asset Turnover ratio 0.82 1.29

Inventory Turnover ratio 1.93 9.44

Debt to equity ratio:

D/E ratio is the solvency ratio to measure the capital structure of the organization. T-

Shirts Ltd in the year 2019 has indicated an ascent in the proportion when contrasted with the

earlier year which is for the most part a direct result of the expansion in the obligation in the

capital structure. This demonstrates the unsafe circumstance for the organization as it is

having more prominent extent of obligation against the equity financing. This may imply that

the investors are least keen on providing funds to the business activity as the organization

isn't performing acceptable which is the reason T-shirts Ltd is looking for extra debt

financing.

Proprietary ratio:

The proprietary ratio of the organization features that in the year 2018 the

organization has almost 49.57% of the assets being contributed by the investors and the rest

of the sum has been financed through lenders (Zainudin and Hashim, 2016). Then again, in

2019 it diminished to 18.24% which shows that the organization has utilized the obligation in

its financing instead of the costly equity. The organization needs to keep up a harmony

between the high and low proportions.

Asset turnover ratio:

This proportion of the organization is extremely low which shows that the

organization isn't having capacity to successfully utilize its resources so as to create income

for the organization. This features that the organization isn't working gainfully in using its

resources to its full limit. The proportion was 1.29 in 2018 which further diminished to 0.82

in 2019. It is great to have higher proportion and as the organization is having lower

proportion which shows that the organization isn't using its resources effectively which may

be a result of the issue relating to the administration or the production.

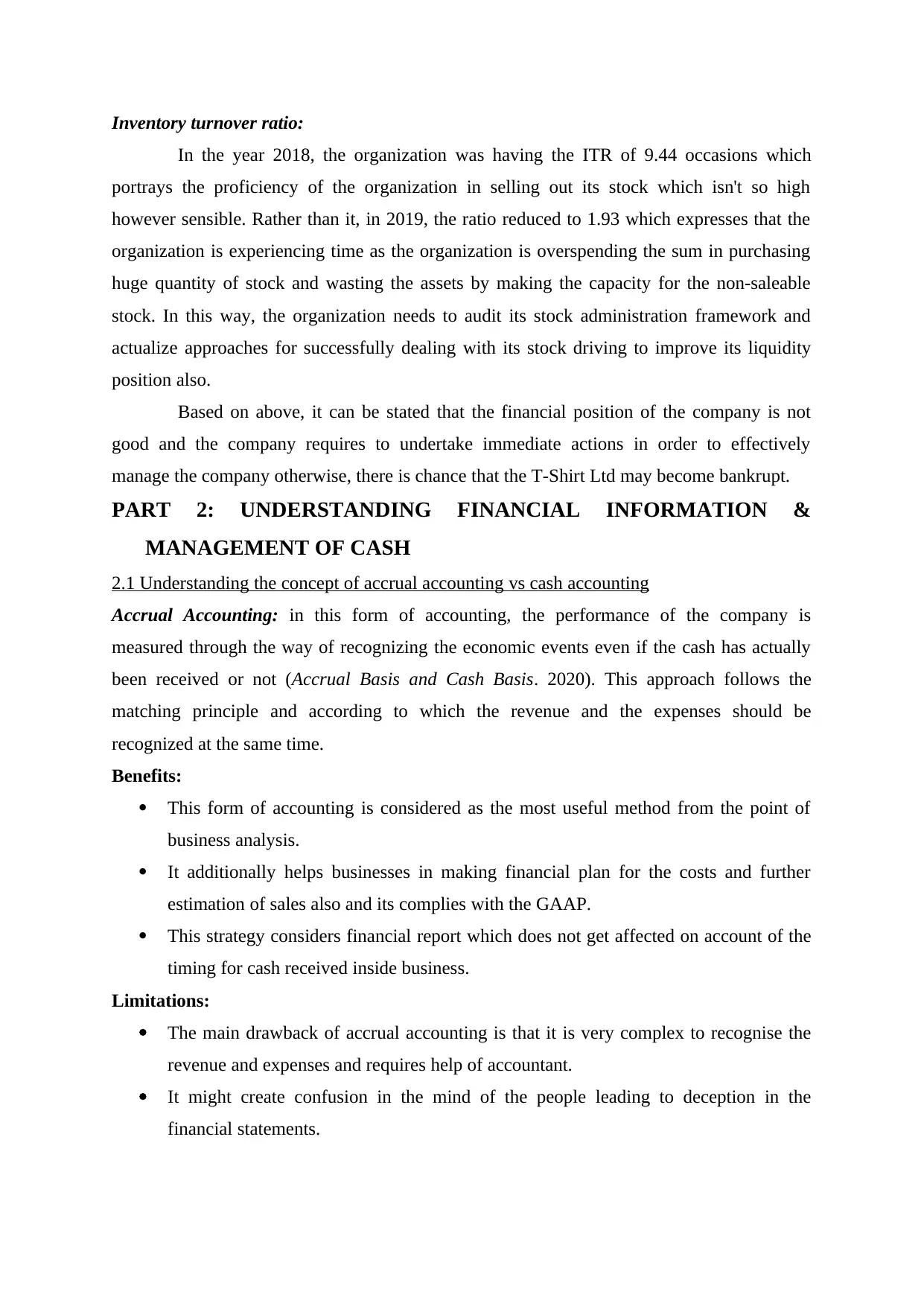

Inventory turnover ratio:

In the year 2018, the organization was having the ITR of 9.44 occasions which

portrays the proficiency of the organization in selling out its stock which isn't so high

however sensible. Rather than it, in 2019, the ratio reduced to 1.93 which expresses that the

organization is experiencing time as the organization is overspending the sum in purchasing

huge quantity of stock and wasting the assets by making the capacity for the non-saleable

stock. In this way, the organization needs to audit its stock administration framework and

actualize approaches for successfully dealing with its stock driving to improve its liquidity

position also.

Based on above, it can be stated that the financial position of the company is not

good and the company requires to undertake immediate actions in order to effectively

manage the company otherwise, there is chance that the T-Shirt Ltd may become bankrupt.

PART 2: UNDERSTANDING FINANCIAL INFORMATION &

MANAGEMENT OF CASH

2.1 Understanding the concept of accrual accounting vs cash accounting

Accrual Accounting: in this form of accounting, the performance of the company is

measured through the way of recognizing the economic events even if the cash has actually

been received or not (Accrual Basis and Cash Basis. 2020). This approach follows the

matching principle and according to which the revenue and the expenses should be

recognized at the same time.

Benefits:

This form of accounting is considered as the most useful method from the point of

business analysis.

It additionally helps businesses in making financial plan for the costs and further

estimation of sales also and its complies with the GAAP.

This strategy considers financial report which does not get affected on account of the

timing for cash received inside business.

Limitations:

The main drawback of accrual accounting is that it is very complex to recognise the

revenue and expenses and requires help of accountant.

It might create confusion in the mind of the people leading to deception in the

financial statements.

In the year 2018, the organization was having the ITR of 9.44 occasions which

portrays the proficiency of the organization in selling out its stock which isn't so high

however sensible. Rather than it, in 2019, the ratio reduced to 1.93 which expresses that the

organization is experiencing time as the organization is overspending the sum in purchasing

huge quantity of stock and wasting the assets by making the capacity for the non-saleable

stock. In this way, the organization needs to audit its stock administration framework and

actualize approaches for successfully dealing with its stock driving to improve its liquidity

position also.

Based on above, it can be stated that the financial position of the company is not

good and the company requires to undertake immediate actions in order to effectively

manage the company otherwise, there is chance that the T-Shirt Ltd may become bankrupt.

PART 2: UNDERSTANDING FINANCIAL INFORMATION &

MANAGEMENT OF CASH

2.1 Understanding the concept of accrual accounting vs cash accounting

Accrual Accounting: in this form of accounting, the performance of the company is

measured through the way of recognizing the economic events even if the cash has actually

been received or not (Accrual Basis and Cash Basis. 2020). This approach follows the

matching principle and according to which the revenue and the expenses should be

recognized at the same time.

Benefits:

This form of accounting is considered as the most useful method from the point of

business analysis.

It additionally helps businesses in making financial plan for the costs and further

estimation of sales also and its complies with the GAAP.

This strategy considers financial report which does not get affected on account of the

timing for cash received inside business.

Limitations:

The main drawback of accrual accounting is that it is very complex to recognise the

revenue and expenses and requires help of accountant.

It might create confusion in the mind of the people leading to deception in the

financial statements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

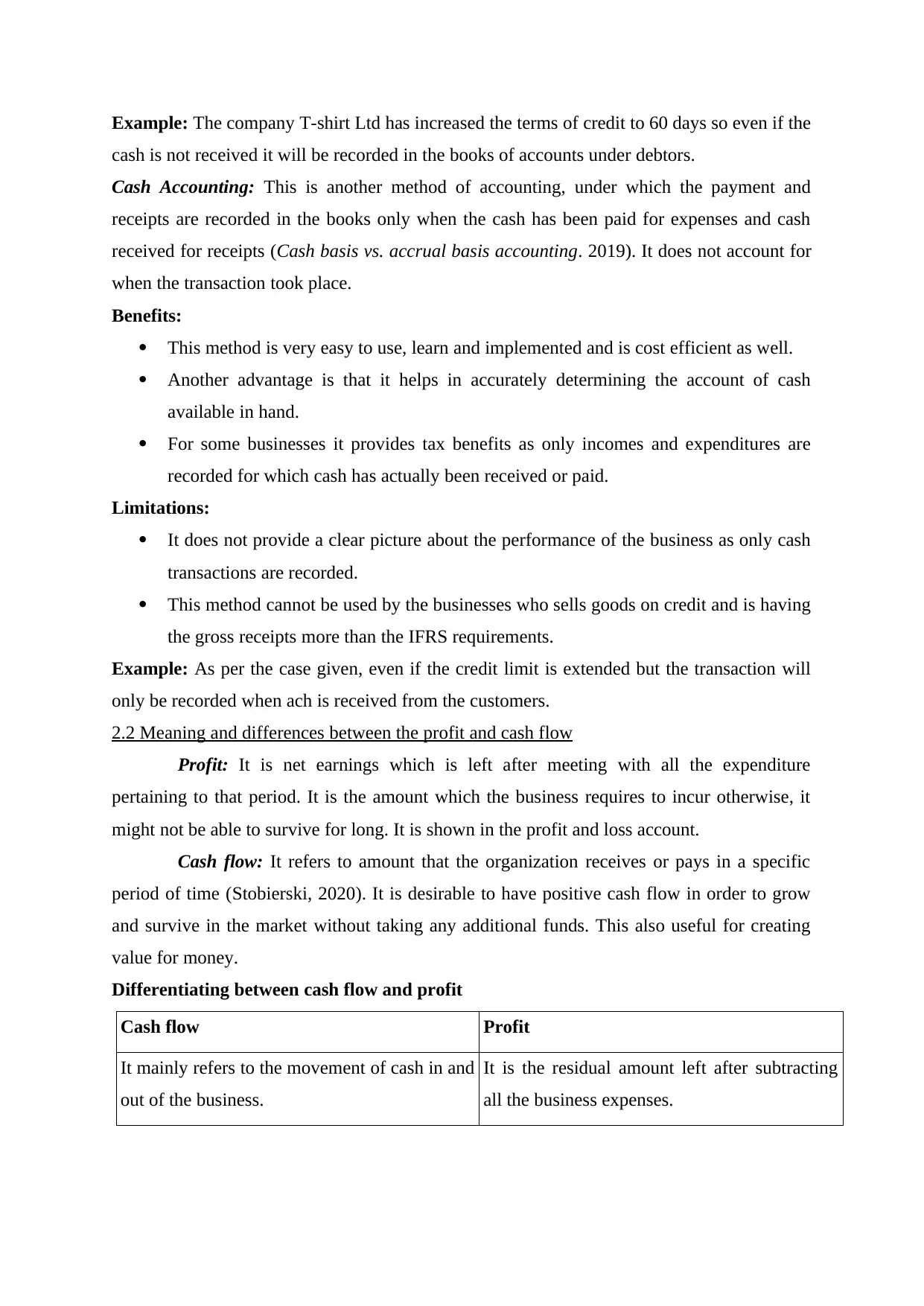

Example: The company T-shirt Ltd has increased the terms of credit to 60 days so even if the

cash is not received it will be recorded in the books of accounts under debtors.

Cash Accounting: This is another method of accounting, under which the payment and

receipts are recorded in the books only when the cash has been paid for expenses and cash

received for receipts (Cash basis vs. accrual basis accounting. 2019). It does not account for

when the transaction took place.

Benefits:

This method is very easy to use, learn and implemented and is cost efficient as well.

Another advantage is that it helps in accurately determining the account of cash

available in hand.

For some businesses it provides tax benefits as only incomes and expenditures are

recorded for which cash has actually been received or paid.

Limitations:

It does not provide a clear picture about the performance of the business as only cash

transactions are recorded.

This method cannot be used by the businesses who sells goods on credit and is having

the gross receipts more than the IFRS requirements.

Example: As per the case given, even if the credit limit is extended but the transaction will

only be recorded when ach is received from the customers.

2.2 Meaning and differences between the profit and cash flow

Profit: It is net earnings which is left after meeting with all the expenditure

pertaining to that period. It is the amount which the business requires to incur otherwise, it

might not be able to survive for long. It is shown in the profit and loss account.

Cash flow: It refers to amount that the organization receives or pays in a specific

period of time (Stobierski, 2020). It is desirable to have positive cash flow in order to grow

and survive in the market without taking any additional funds. This also useful for creating

value for money.

Differentiating between cash flow and profit

Cash flow Profit

It mainly refers to the movement of cash in and

out of the business.

It is the residual amount left after subtracting

all the business expenses.

cash is not received it will be recorded in the books of accounts under debtors.

Cash Accounting: This is another method of accounting, under which the payment and

receipts are recorded in the books only when the cash has been paid for expenses and cash

received for receipts (Cash basis vs. accrual basis accounting. 2019). It does not account for

when the transaction took place.

Benefits:

This method is very easy to use, learn and implemented and is cost efficient as well.

Another advantage is that it helps in accurately determining the account of cash

available in hand.

For some businesses it provides tax benefits as only incomes and expenditures are

recorded for which cash has actually been received or paid.

Limitations:

It does not provide a clear picture about the performance of the business as only cash

transactions are recorded.

This method cannot be used by the businesses who sells goods on credit and is having

the gross receipts more than the IFRS requirements.

Example: As per the case given, even if the credit limit is extended but the transaction will

only be recorded when ach is received from the customers.

2.2 Meaning and differences between the profit and cash flow

Profit: It is net earnings which is left after meeting with all the expenditure

pertaining to that period. It is the amount which the business requires to incur otherwise, it

might not be able to survive for long. It is shown in the profit and loss account.

Cash flow: It refers to amount that the organization receives or pays in a specific

period of time (Stobierski, 2020). It is desirable to have positive cash flow in order to grow

and survive in the market without taking any additional funds. This also useful for creating

value for money.

Differentiating between cash flow and profit

Cash flow Profit

It mainly refers to the movement of cash in and

out of the business.

It is the residual amount left after subtracting

all the business expenses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

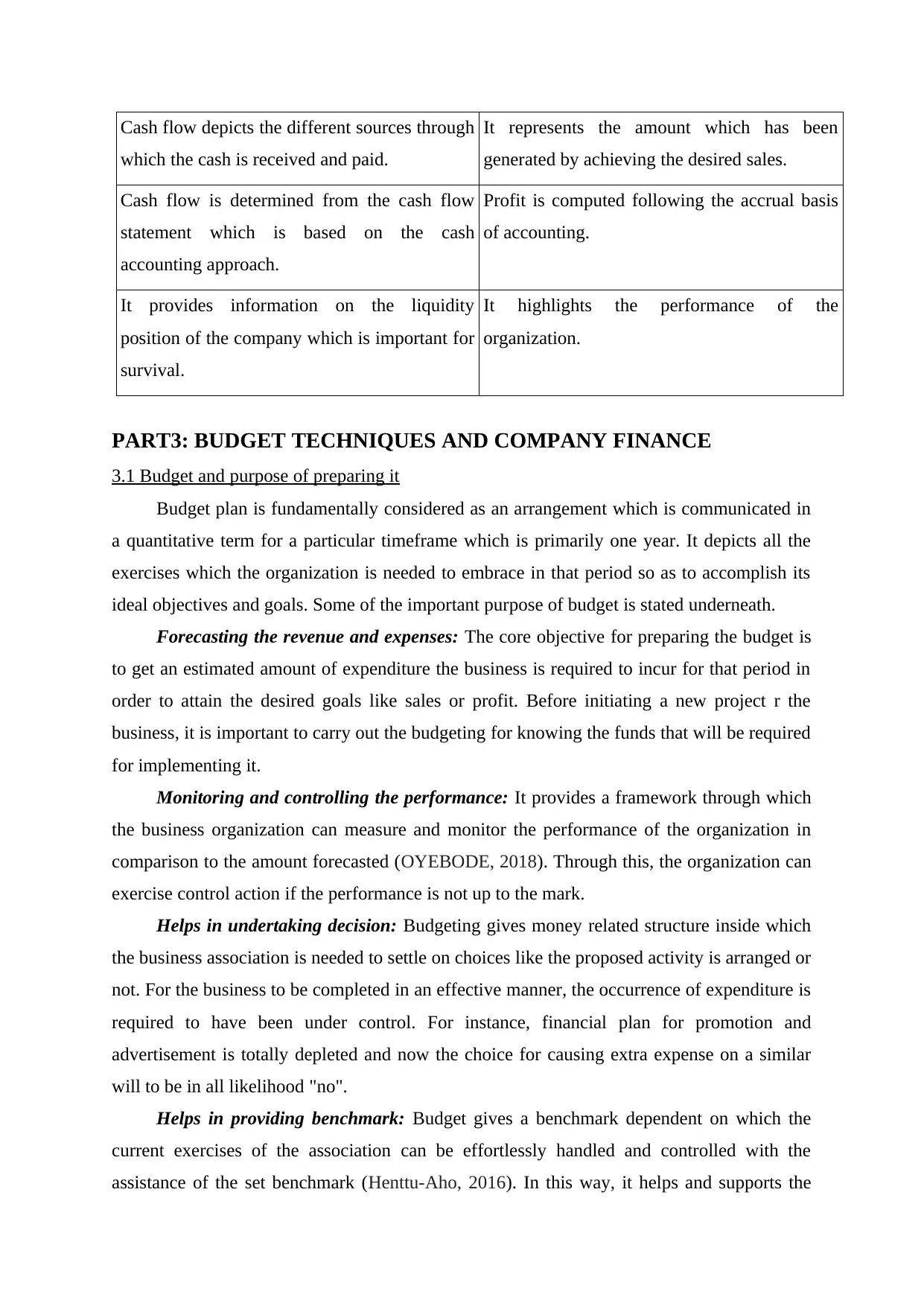

Cash flow depicts the different sources through

which the cash is received and paid.

It represents the amount which has been

generated by achieving the desired sales.

Cash flow is determined from the cash flow

statement which is based on the cash

accounting approach.

Profit is computed following the accrual basis

of accounting.

It provides information on the liquidity

position of the company which is important for

survival.

It highlights the performance of the

organization.

PART3: BUDGET TECHNIQUES AND COMPANY FINANCE

3.1 Budget and purpose of preparing it

Budget plan is fundamentally considered as an arrangement which is communicated in

a quantitative term for a particular timeframe which is primarily one year. It depicts all the

exercises which the organization is needed to embrace in that period so as to accomplish its

ideal objectives and goals. Some of the important purpose of budget is stated underneath.

Forecasting the revenue and expenses: The core objective for preparing the budget is

to get an estimated amount of expenditure the business is required to incur for that period in

order to attain the desired goals like sales or profit. Before initiating a new project r the

business, it is important to carry out the budgeting for knowing the funds that will be required

for implementing it.

Monitoring and controlling the performance: It provides a framework through which

the business organization can measure and monitor the performance of the organization in

comparison to the amount forecasted (OYEBODE, 2018). Through this, the organization can

exercise control action if the performance is not up to the mark.

Helps in undertaking decision: Budgeting gives money related structure inside which

the business association is needed to settle on choices like the proposed activity is arranged or

not. For the business to be completed in an effective manner, the occurrence of expenditure is

required to have been under control. For instance, financial plan for promotion and

advertisement is totally depleted and now the choice for causing extra expense on a similar

will to be in all likelihood "no".

Helps in providing benchmark: Budget gives a benchmark dependent on which the

current exercises of the association can be effortlessly handled and controlled with the

assistance of the set benchmark (Henttu-Aho, 2016). In this way, it helps and supports the

which the cash is received and paid.

It represents the amount which has been

generated by achieving the desired sales.

Cash flow is determined from the cash flow

statement which is based on the cash

accounting approach.

Profit is computed following the accrual basis

of accounting.

It provides information on the liquidity

position of the company which is important for

survival.

It highlights the performance of the

organization.

PART3: BUDGET TECHNIQUES AND COMPANY FINANCE

3.1 Budget and purpose of preparing it

Budget plan is fundamentally considered as an arrangement which is communicated in

a quantitative term for a particular timeframe which is primarily one year. It depicts all the

exercises which the organization is needed to embrace in that period so as to accomplish its

ideal objectives and goals. Some of the important purpose of budget is stated underneath.

Forecasting the revenue and expenses: The core objective for preparing the budget is

to get an estimated amount of expenditure the business is required to incur for that period in

order to attain the desired goals like sales or profit. Before initiating a new project r the

business, it is important to carry out the budgeting for knowing the funds that will be required

for implementing it.

Monitoring and controlling the performance: It provides a framework through which

the business organization can measure and monitor the performance of the organization in

comparison to the amount forecasted (OYEBODE, 2018). Through this, the organization can

exercise control action if the performance is not up to the mark.

Helps in undertaking decision: Budgeting gives money related structure inside which

the business association is needed to settle on choices like the proposed activity is arranged or

not. For the business to be completed in an effective manner, the occurrence of expenditure is

required to have been under control. For instance, financial plan for promotion and

advertisement is totally depleted and now the choice for causing extra expense on a similar

will to be in all likelihood "no".

Helps in providing benchmark: Budget gives a benchmark dependent on which the

current exercises of the association can be effortlessly handled and controlled with the

assistance of the set benchmark (Henttu-Aho, 2016). In this way, it helps and supports the

organization in taking right and improved decision which consequently results into

accomplishing the desired goals.

3.2 Benefits of forming a limited company and listing it on a stock exchange

A limited organization builds the methods of procuring funds and contributing

towards the development and improvement of the association. Listing an organization on a

stock trade empowers it to raise capital from the public which will help in additional

reinforcing of the authoritative structure and brand image. Listing encourages in offering

liquidity to the various providers of funds and in guaranteeing viable consistence with the

issuer and working in light of a legitimate concern for the investors. There are different

advantages related with the listing an organization on a stock trade which are expressed

underneath.

Procuring capital for additional growth: Companies arrives at a level where the extra

capital is needed to be infused which helps in organization's development and business

extension plans (Public Limited Companies. 2020). Hence, opening up to the world (going

public) is a path through which these limitations can be handily relieved. In this, the

organization builds the investors base and upgrades its credibility.

Increasing the organization’s visibility: This will help in improving the organization's

perceivability and validity all over different foundations and the public who are eager to

contribute which is a result of consenting to the various regulatory requirements and

guaranteeing straightforwardness while undertaking the business activities.

Liquidity: Going public animates liquidity giving the investors the opportunity to

understanding the worth they have put resources into the organization. It gives chance to the

investors or financial specialists to transact in the shares of the association and sharing

dangers and alongside the equivalent profiting the speculators with the expansion in the

company’s worth.

Enhancement in the employee morale and confidence: Listing of the organization

builds the perceivability and improves the impression of the general population towards the

business association, consequently, coming about into increment in the worker worth and

boosting of their spirit. There are odds of enlisting new staff and giving them the stock-based

payments like ESOPs and so on.

accomplishing the desired goals.

3.2 Benefits of forming a limited company and listing it on a stock exchange

A limited organization builds the methods of procuring funds and contributing

towards the development and improvement of the association. Listing an organization on a

stock trade empowers it to raise capital from the public which will help in additional

reinforcing of the authoritative structure and brand image. Listing encourages in offering

liquidity to the various providers of funds and in guaranteeing viable consistence with the

issuer and working in light of a legitimate concern for the investors. There are different

advantages related with the listing an organization on a stock trade which are expressed

underneath.

Procuring capital for additional growth: Companies arrives at a level where the extra

capital is needed to be infused which helps in organization's development and business

extension plans (Public Limited Companies. 2020). Hence, opening up to the world (going

public) is a path through which these limitations can be handily relieved. In this, the

organization builds the investors base and upgrades its credibility.

Increasing the organization’s visibility: This will help in improving the organization's

perceivability and validity all over different foundations and the public who are eager to

contribute which is a result of consenting to the various regulatory requirements and

guaranteeing straightforwardness while undertaking the business activities.

Liquidity: Going public animates liquidity giving the investors the opportunity to

understanding the worth they have put resources into the organization. It gives chance to the

investors or financial specialists to transact in the shares of the association and sharing

dangers and alongside the equivalent profiting the speculators with the expansion in the

company’s worth.

Enhancement in the employee morale and confidence: Listing of the organization

builds the perceivability and improves the impression of the general population towards the

business association, consequently, coming about into increment in the worker worth and

boosting of their spirit. There are odds of enlisting new staff and giving them the stock-based

payments like ESOPs and so on.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Abernathy, J.L., and et.al., 2017. Income statement reporting discretion allowed by FIN 48:

Interest and penalty expense classification. The Journal of the American Taxation

Association. 39(1). pp.45-66.

Campisi, D. and et.al., 2019. Efficiency assessment of knowledge intensive business services

industry in Italy: data envelopment analysis (DEA) and financial ratio

analysis. Measuring Business Excellence.

Henttu-Aho, T., 2016. Enabling characteristics of new budgeting practice and the role of

controller. Qualitative Research in Accounting & Management.

OYEBODE, O. J., 2018. Budget and Budgetary Control: A pragmatic approach to the

Nigerian infrastructure dilemma. World Journal of Research and Review. 7(3).

Rodrigues, L. and Rodrigues, L., 2018. Economic-financial performance of the Brazilian

sugarcane energy industry: An empirical evaluation using financial ratio, cluster and

discriminant analysis. Biomass and bioenergy. 108. pp.289-296.

Zainudin, E. F. and Hashim, H. A., 2016. Detecting fraudulent financial reporting using

financial ratio. Journal of Financial Reporting and Accounting.

Online

Accrual Basis and Cash Basis. 2020. [Online]. Available Through:<

https://www.toppr.com/guides/fundamentals-of-accounting/accounting-process/

accrual-basis-and-cash-basis/>.

Cash basis vs. accrual basis accounting. 2019. [Online]. Available Through:<

https://www.accountingtools.com/articles/cash-basis-vs-accrual-basis-

accounting.html>.

Public Limited Companies. 2020. [Online]. Available Through:<

https://www.tutor2u.net/business/reference/public-limited-companies >.

Stobierski, T., 2020. CASH FLOW VS. PROFIT: WHAT'S THE DIFFERENCE? [Online].

Available Through :< https://online.hbs.edu/blog/post/cash-flow-vs-profit>.

Books and Journals

Abernathy, J.L., and et.al., 2017. Income statement reporting discretion allowed by FIN 48:

Interest and penalty expense classification. The Journal of the American Taxation

Association. 39(1). pp.45-66.

Campisi, D. and et.al., 2019. Efficiency assessment of knowledge intensive business services

industry in Italy: data envelopment analysis (DEA) and financial ratio

analysis. Measuring Business Excellence.

Henttu-Aho, T., 2016. Enabling characteristics of new budgeting practice and the role of

controller. Qualitative Research in Accounting & Management.

OYEBODE, O. J., 2018. Budget and Budgetary Control: A pragmatic approach to the

Nigerian infrastructure dilemma. World Journal of Research and Review. 7(3).

Rodrigues, L. and Rodrigues, L., 2018. Economic-financial performance of the Brazilian

sugarcane energy industry: An empirical evaluation using financial ratio, cluster and

discriminant analysis. Biomass and bioenergy. 108. pp.289-296.

Zainudin, E. F. and Hashim, H. A., 2016. Detecting fraudulent financial reporting using

financial ratio. Journal of Financial Reporting and Accounting.

Online

Accrual Basis and Cash Basis. 2020. [Online]. Available Through:<

https://www.toppr.com/guides/fundamentals-of-accounting/accounting-process/

accrual-basis-and-cash-basis/>.

Cash basis vs. accrual basis accounting. 2019. [Online]. Available Through:<

https://www.accountingtools.com/articles/cash-basis-vs-accrual-basis-

accounting.html>.

Public Limited Companies. 2020. [Online]. Available Through:<

https://www.tutor2u.net/business/reference/public-limited-companies >.

Stobierski, T., 2020. CASH FLOW VS. PROFIT: WHAT'S THE DIFFERENCE? [Online].

Available Through :< https://online.hbs.edu/blog/post/cash-flow-vs-profit>.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

Liquidity Ratios

Formula 2019 2018

Current assets 426 352

Inventory 121 89

Current liability 469 136

Quick ratio (current assets-inventory)/current liabilities 0.65 1.93

Current ratio Current asset/ current liabilities 0.91 2.59

Profitability ratio

Net sales 1366 2101

Gross Profit 615 1261

Net income -500 372

Total assets 1700 1634

Gross profit Margin Gross profit/ sales 45.02% 60.02%

Net profit margin Net income/sales -36.60% 17.71%

Return on assets Net income/assets -29.41% 22.77%

Solvency ratios

Total assets 1700 1634

Total debts 1390 824

Total equity 310 810

Debt to equity ratio Total debt/total equity 4.48 1.02

Proprietary ratio Total equity / total Assets 18.24% 49.57%

Liquidity Ratios

Formula 2019 2018

Current assets 426 352

Inventory 121 89

Current liability 469 136

Quick ratio (current assets-inventory)/current liabilities 0.65 1.93

Current ratio Current asset/ current liabilities 0.91 2.59

Profitability ratio

Net sales 1366 2101

Gross Profit 615 1261

Net income -500 372

Total assets 1700 1634

Gross profit Margin Gross profit/ sales 45.02% 60.02%

Net profit margin Net income/sales -36.60% 17.71%

Return on assets Net income/assets -29.41% 22.77%

Solvency ratios

Total assets 1700 1634

Total debts 1390 824

Total equity 310 810

Debt to equity ratio Total debt/total equity 4.48 1.02

Proprietary ratio Total equity / total Assets 18.24% 49.57%

Efficiency ratio

COGS 751 840

Average inventory 389 89

Net sales 1366 2101

Average asset 1667 1634

Asset Turnover ratio Net sales/Average Total Asset 0.82 1.29

Inventory Turnover

ratio COGS/Average Inventory 1.93 9.44

COGS 751 840

Average inventory 389 89

Net sales 1366 2101

Average asset 1667 1634

Asset Turnover ratio Net sales/Average Total Asset 0.82 1.29

Inventory Turnover

ratio COGS/Average Inventory 1.93 9.44

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.