ACC-ACF2100 Take-home Test Solution: Financial Accounting, 2020

VerifiedAdded on 2023/01/11

|5

|570

|31

Homework Assignment

AI Summary

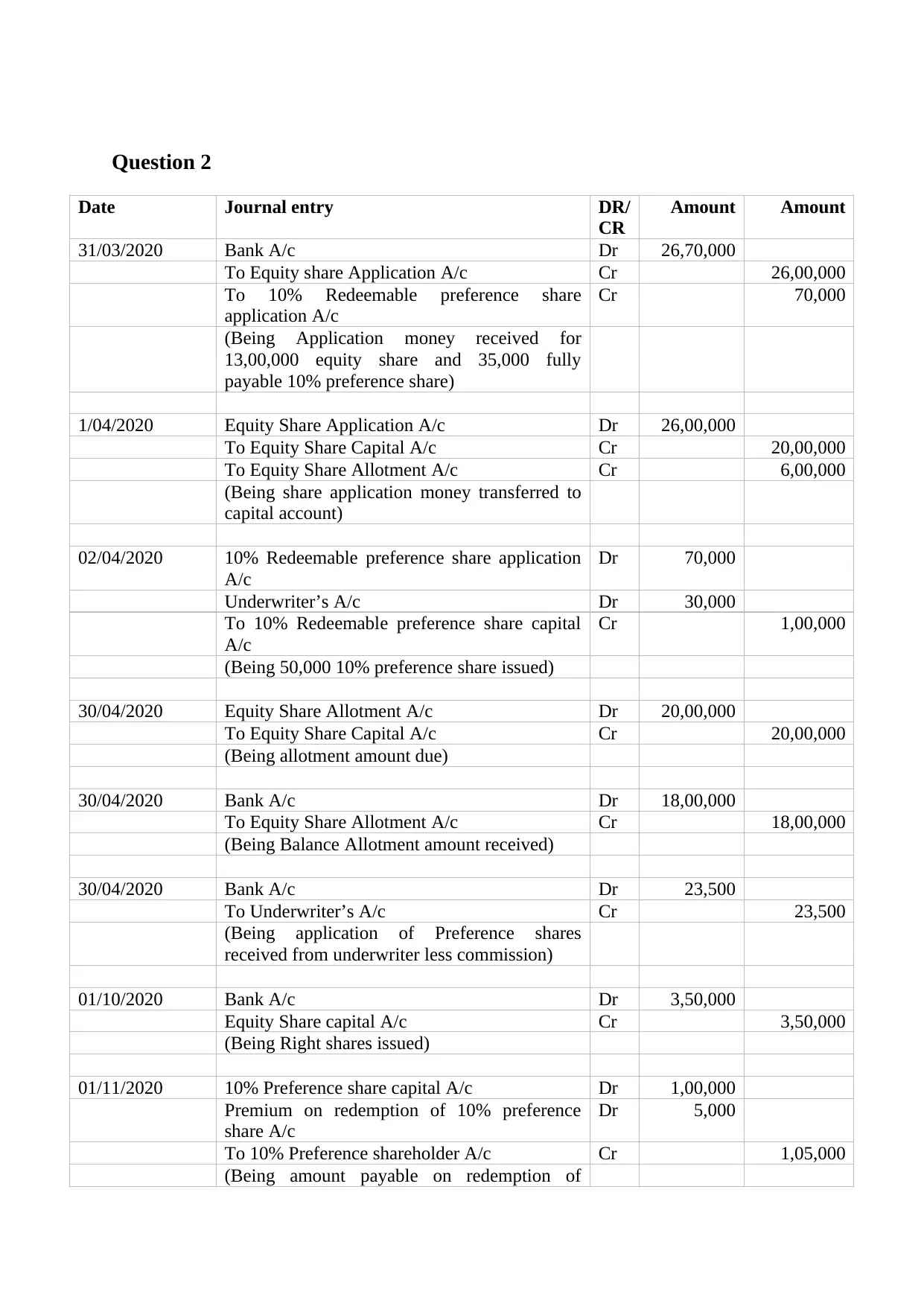

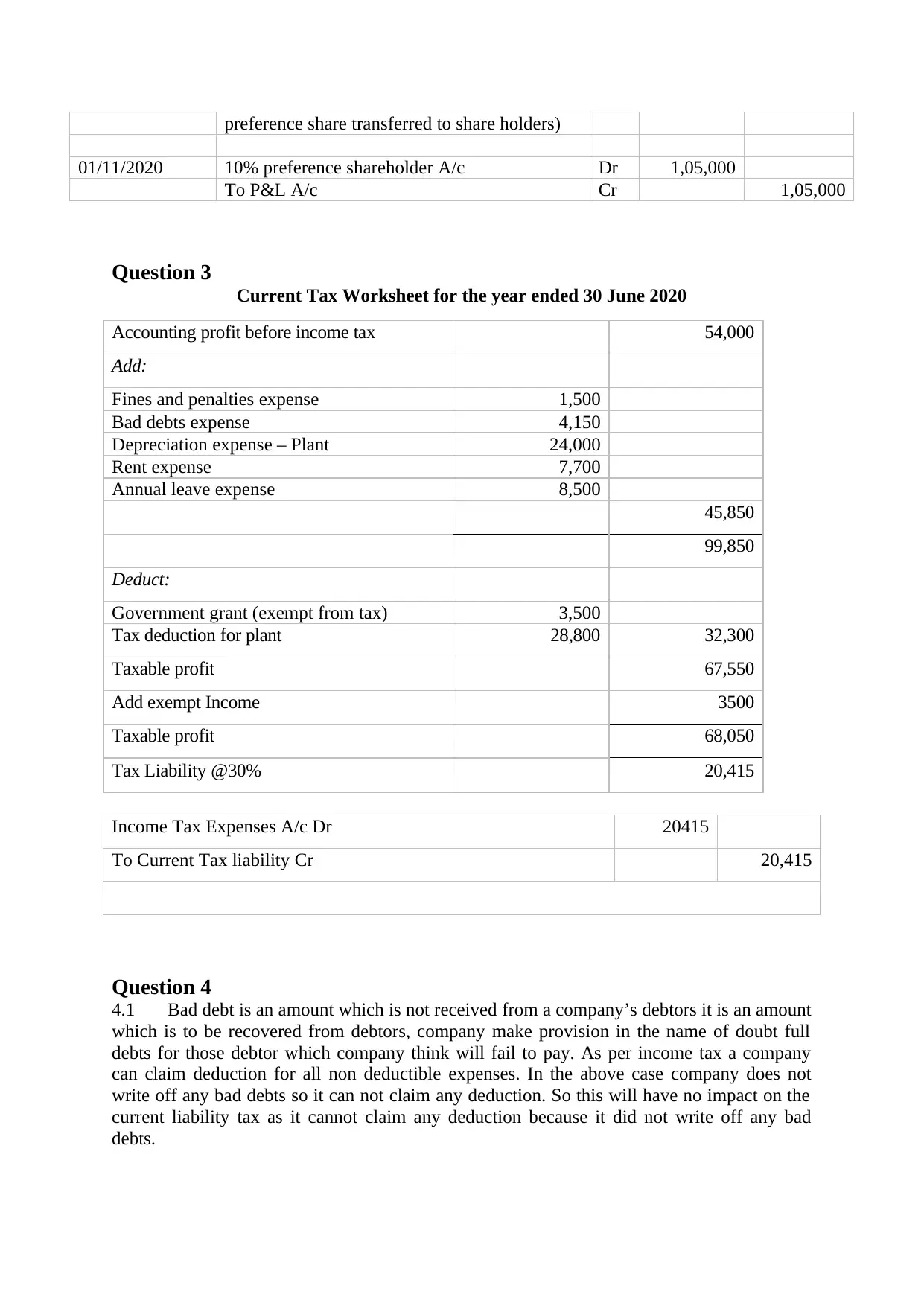

This document presents a comprehensive solution to the ACC-ACF2100 take-home test, focusing on financial accounting principles and their application. The solution includes detailed journal entries for various transactions, such as share applications, allotments, and preference share redemptions. It also features a current tax worksheet, calculating taxable profit and tax liability based on accounting profit and relevant adjustments. Furthermore, the document addresses deferred tax implications, explaining the impact of bad debts and providing journal entries for tax adjustments. The solution incorporates analysis of financial statements and addresses key accounting concepts like bad debts and deferred tax, offering a thorough understanding of the financial accounting principles examined in the take-home test.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.