Corporate Takeover Decision Making and Consolidation Accounting

VerifiedAdded on 2020/10/23

|12

|3069

|144

Report

AI Summary

This report provides a comprehensive overview of corporate takeovers and their impact on financial reporting, focusing on consolidation accounting. The report is structured into three key parts. Part A details the two primary methods of corporate acquisition: consolidation accounting and equity accounting, outlining their methodologies and key differences. Part B examines intra-group transactions, explaining their treatment within consolidated financial statements, and referencing relevant accounting standards. Part C addresses the requirements for disclosing non-controlling interests (NCI) as per Australian Accounting Standards Board (AASB) guidelines. The report uses examples to illustrate the concepts, providing a clear understanding of the accounting implications of corporate takeovers and the importance of accurate financial reporting. The report aims to provide a good understanding of the corporate takeover and consolidation accounting.

Corporate Takeover

Decision Making and the

Effects on Consolidation

Accounting

Decision Making and the

Effects on Consolidation

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This report concise about the decisions which are made during corporate take over and

methodology which is to be used by company to take over any other business. In this report two

corporate acquisition methods are discussed Consolidation Accounting and Equity Accounting,

and reason that why company should opt one of these methods. In the second part of the report it

summarises about the transaction happened between the subsidiary and parent company. The

third part of the report concise about the various requirements as per the AASB to disclose the

non controlling interest (NCI).

This report concise about the decisions which are made during corporate take over and

methodology which is to be used by company to take over any other business. In this report two

corporate acquisition methods are discussed Consolidation Accounting and Equity Accounting,

and reason that why company should opt one of these methods. In the second part of the report it

summarises about the transaction happened between the subsidiary and parent company. The

third part of the report concise about the various requirements as per the AASB to disclose the

non controlling interest (NCI).

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

PART B............................................................................................................................................4

PART C............................................................................................................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

PART B............................................................................................................................................4

PART C............................................................................................................................................5

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Corporate take over is the acquisition of one business by another business, in this all the

assets and liabilities are purchased by another business and that company is owned and managed

by the purchasing company (Shroff, Verdi and Yu, 2013). The Following report talks about the

corporate take and the effects which it can have on the consolidated financial statements. This

report is divided into three part, Part A talks about the different types of methods through which

one company can acquire another company, in this report key difference in methodology of

Consolidation Accounting and equity accounting. Part B talks about the intra group transactions

and its treatment and Part C talks about the requirements of NCI disclosure.

PART A

Consolidation method accounting: Consolidation method accounting is an investment

accounting method used by companies to consolidate financial statements of the company

holding majority of shares. This method is only used by the companies which owns more than

50.1% shares in the subsidiary company. This methods works after the reporting of subsidiary

company's balance of its financial statements in a combined financial statements of Parent

company. Under this method total revenue generated by a parent company from its business

operations are combined with the total revenue generated by its subsidiary company.

Equity method accounting: Equity method accounting is an accounting method used by

company when it holds a significant influence over the company which it is acquiring, but it does

not have a full control over it. In order to use this method of accounting company has to have a

significant influence over investee company. In order to have a significant control investor

company must own between 20% to 50% shares in the investee company or have voting rights.

If in any case investor has less than 20% shares but have a significant influence over its business

operations, investor company must use equity cost methods.

Key difference in methodology in both accounting methods

As per Australian Accounting Standard Board 3 business combination, parent company's

investment in subsidiary is shown as an assets, with subsidiary reporting which states the

equivalent equity that are owned by parent company are shown in its own accounts (Chiu, 2013).

During consolidation of statements an elimination adjustment are added in order to adjust the

amount of consolidated statements it is necessary to adjust elimination adjustment so that this

1

Corporate take over is the acquisition of one business by another business, in this all the

assets and liabilities are purchased by another business and that company is owned and managed

by the purchasing company (Shroff, Verdi and Yu, 2013). The Following report talks about the

corporate take and the effects which it can have on the consolidated financial statements. This

report is divided into three part, Part A talks about the different types of methods through which

one company can acquire another company, in this report key difference in methodology of

Consolidation Accounting and equity accounting. Part B talks about the intra group transactions

and its treatment and Part C talks about the requirements of NCI disclosure.

PART A

Consolidation method accounting: Consolidation method accounting is an investment

accounting method used by companies to consolidate financial statements of the company

holding majority of shares. This method is only used by the companies which owns more than

50.1% shares in the subsidiary company. This methods works after the reporting of subsidiary

company's balance of its financial statements in a combined financial statements of Parent

company. Under this method total revenue generated by a parent company from its business

operations are combined with the total revenue generated by its subsidiary company.

Equity method accounting: Equity method accounting is an accounting method used by

company when it holds a significant influence over the company which it is acquiring, but it does

not have a full control over it. In order to use this method of accounting company has to have a

significant influence over investee company. In order to have a significant control investor

company must own between 20% to 50% shares in the investee company or have voting rights.

If in any case investor has less than 20% shares but have a significant influence over its business

operations, investor company must use equity cost methods.

Key difference in methodology in both accounting methods

As per Australian Accounting Standard Board 3 business combination, parent company's

investment in subsidiary is shown as an assets, with subsidiary reporting which states the

equivalent equity that are owned by parent company are shown in its own accounts (Chiu, 2013).

During consolidation of statements an elimination adjustment are added in order to adjust the

amount of consolidated statements it is necessary to adjust elimination adjustment so that this

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

statement is not overstated by amount of equity which are held in the parent company. The

elimination adjustments are made with the intention to offset the inter company transactions, so

that the values are not counted twice during consolidation level.

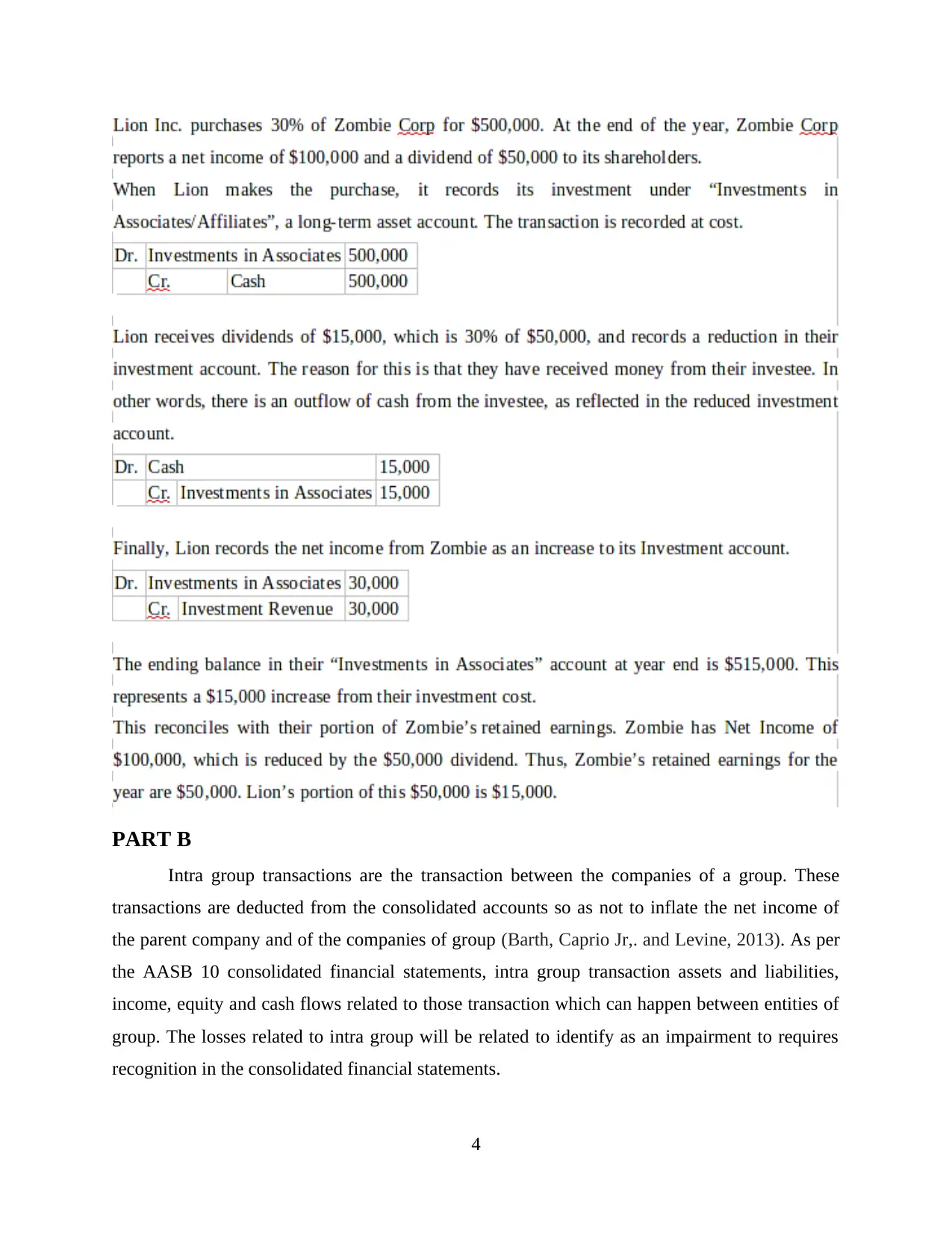

As per Australian Accounting Standard Boards 128 Investments in Associates and joint

venture, the investor company will not use consolidation and elimination adjustments in

preparing their financial statements (Younge, Tong and Fleming, 2015). In this method investor

company will report its share proportionately of the investee company's equity shares as an

investment on the assets side at cost. Any profit or loss from the investee company will increase

the investment account in the investor company with the proportional amount to which the

investee company has earned profit and number of share held in the investee. Any dividend on

investment which is paid by investee are deducted from investor's investment account.

Following are the examples which justify the key difference mentioned above:

Consolidation Accounting Method:

ABC Ltd recently began its operation and, has a simple financial structure, it injects $30M cash

into his business. Following is the journal entry.

Dr. Cash 30000000

Cr. Shareholder’s Equity 30000000

As such, ABC Lt d's balances are now 30M in assets and 30M in equity. In next month, ABC

Ltd sets up XYZ Inc., a new subsidiary. In which ABC Ltd invests $15M in the company for

100% of its equity. In Parent’s books, it shows as under:

Dr. Investments in Subsidiary 15000000

Cr. Cash 15000000

ABC Ltd cash is reduced by $15M, but still has a total of $30M in assets.

In XYZ Inc's books, the same transaction would be as follows.

Dr. Cash 15000000

Cr. Shareholder’s Equity 15000000

2

elimination adjustments are made with the intention to offset the inter company transactions, so

that the values are not counted twice during consolidation level.

As per Australian Accounting Standard Boards 128 Investments in Associates and joint

venture, the investor company will not use consolidation and elimination adjustments in

preparing their financial statements (Younge, Tong and Fleming, 2015). In this method investor

company will report its share proportionately of the investee company's equity shares as an

investment on the assets side at cost. Any profit or loss from the investee company will increase

the investment account in the investor company with the proportional amount to which the

investee company has earned profit and number of share held in the investee. Any dividend on

investment which is paid by investee are deducted from investor's investment account.

Following are the examples which justify the key difference mentioned above:

Consolidation Accounting Method:

ABC Ltd recently began its operation and, has a simple financial structure, it injects $30M cash

into his business. Following is the journal entry.

Dr. Cash 30000000

Cr. Shareholder’s Equity 30000000

As such, ABC Lt d's balances are now 30M in assets and 30M in equity. In next month, ABC

Ltd sets up XYZ Inc., a new subsidiary. In which ABC Ltd invests $15M in the company for

100% of its equity. In Parent’s books, it shows as under:

Dr. Investments in Subsidiary 15000000

Cr. Cash 15000000

ABC Ltd cash is reduced by $15M, but still has a total of $30M in assets.

In XYZ Inc's books, the same transaction would be as follows.

Dr. Cash 15000000

Cr. Shareholder’s Equity 15000000

2

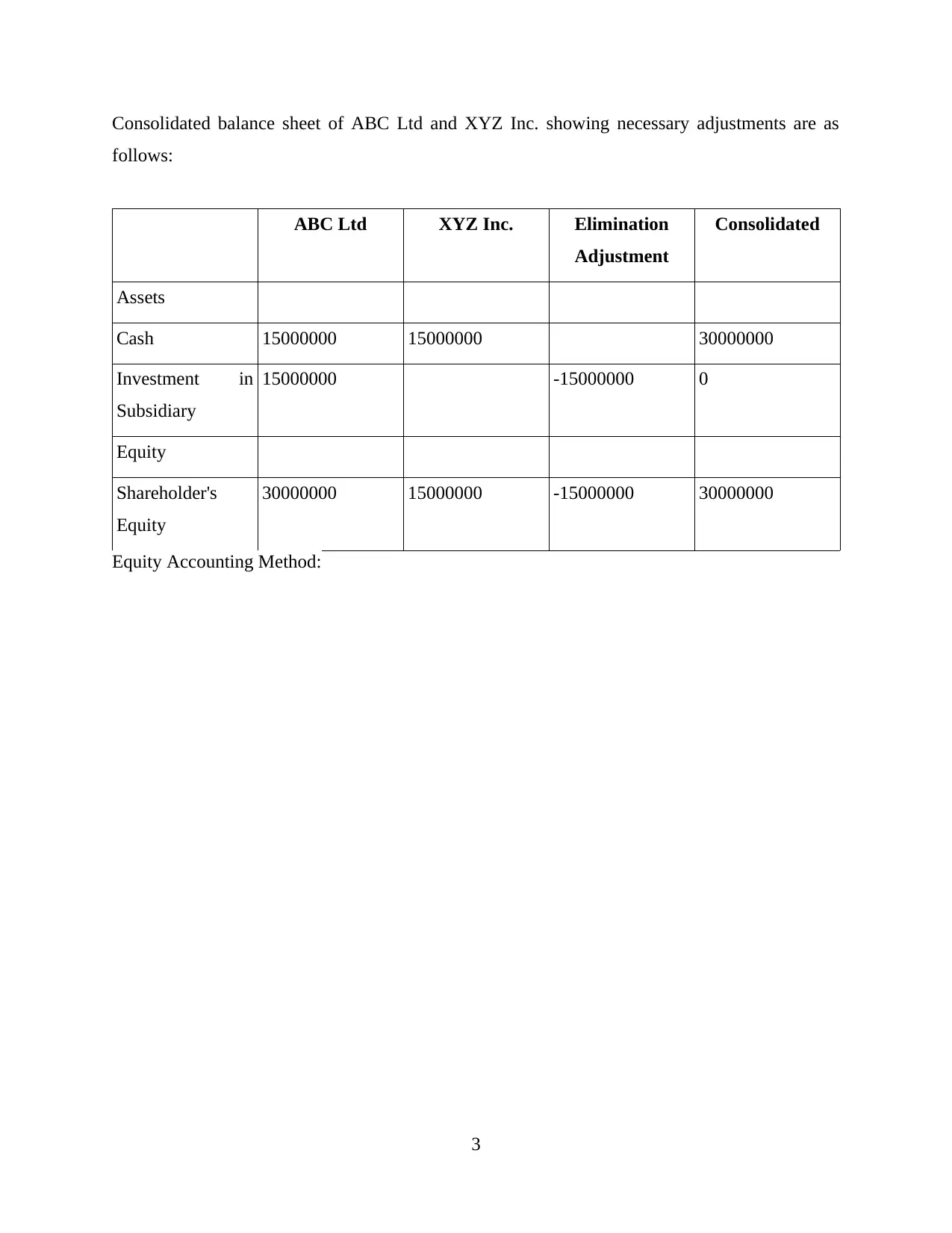

Consolidated balance sheet of ABC Ltd and XYZ Inc. showing necessary adjustments are as

follows:

ABC Ltd XYZ Inc. Elimination

Adjustment

Consolidated

Assets

Cash 15000000 15000000 30000000

Investment in

Subsidiary

15000000 -15000000 0

Equity

Shareholder's

Equity

30000000 15000000 -15000000 30000000

Equity Accounting Method:

3

follows:

ABC Ltd XYZ Inc. Elimination

Adjustment

Consolidated

Assets

Cash 15000000 15000000 30000000

Investment in

Subsidiary

15000000 -15000000 0

Equity

Shareholder's

Equity

30000000 15000000 -15000000 30000000

Equity Accounting Method:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PART B

Intra group transactions are the transaction between the companies of a group. These

transactions are deducted from the consolidated accounts so as not to inflate the net income of

the parent company and of the companies of group (Barth, Caprio Jr,. and Levine, 2013). As per

the AASB 10 consolidated financial statements, intra group transaction assets and liabilities,

income, equity and cash flows related to those transaction which can happen between entities of

group. The losses related to intra group will be related to identify as an impairment to requires

recognition in the consolidated financial statements.

4

Intra group transactions are the transaction between the companies of a group. These

transactions are deducted from the consolidated accounts so as not to inflate the net income of

the parent company and of the companies of group (Barth, Caprio Jr,. and Levine, 2013). As per

the AASB 10 consolidated financial statements, intra group transaction assets and liabilities,

income, equity and cash flows related to those transaction which can happen between entities of

group. The losses related to intra group will be related to identify as an impairment to requires

recognition in the consolidated financial statements.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As per AASB 127 Consolidated and separate financial statements intra-group

transactions and balances where including income, expenses and dividends. These are obviated

in full in reference to profits and losses as a result of intra group transaction. There are consisting

of different assets like inventory and fixed assets which are eliminated in full. It can be treated in

one unit of an entity and incudes in a transaction with other unit of the same entity. These

transaction can happen for a variety of reason, they mostly happen in the normal business.

As per Consolidate and separate financial statements of Australian Accounting Standards

Boards 127, there are basically two principles related to intra group transactions which are states

as under:

The main principle which states that the supervisors should take necessary steps, directly

or through various other regulated entities, in order to provide that conglomerates must have an

adequate risk management, including those transactions which pertain to intra group

transactions. Supervisor should take an appropriate measure where necessary such as reinforcing

these various process using supervisory limits (Beach, 2014). Second principle which provides

supervisors to monitor the intra group transactions related to material of various regulated

financial entities on a specific time. It is important for financial entities to reports these

transactions to help under stand the intra group transactions of these financial conglomerate.

Supervisors should maintain the amount of communication and communicate on a regular basis

in order to find out the problems of its subsidiary. It is a responsibility of supervisors to maintain

and ascertain each others concerns and coordinates properly and take necessary actions to over

come the problems which are related to intra group transactions within the group. Supervisors

should deal in an effective and efficient and in a very appropriate manner with intra group

transactions involving materials which have a detrimental effect on the entities which are

regulated directly or through various detrimental effect. Following is the example which shows

the treatment of Unrealised profit in inventories :

Unrealised profit in inventories

ABC Ltd has two subsidiaries: XYZ Ltd, in which it has 70 % interest; and PQR Ltd, in

which it has a 65 % interest. During an accounting period, XYZ Ltd sold goods to PQR Ltd for

$110,000. The goods had been manufactured by XYZ Ltd at a cost of $75,000. Of these goods,

PQR Ltd had sold 50 per cent by the end of an accounting period.

5

transactions and balances where including income, expenses and dividends. These are obviated

in full in reference to profits and losses as a result of intra group transaction. There are consisting

of different assets like inventory and fixed assets which are eliminated in full. It can be treated in

one unit of an entity and incudes in a transaction with other unit of the same entity. These

transaction can happen for a variety of reason, they mostly happen in the normal business.

As per Consolidate and separate financial statements of Australian Accounting Standards

Boards 127, there are basically two principles related to intra group transactions which are states

as under:

The main principle which states that the supervisors should take necessary steps, directly

or through various other regulated entities, in order to provide that conglomerates must have an

adequate risk management, including those transactions which pertain to intra group

transactions. Supervisor should take an appropriate measure where necessary such as reinforcing

these various process using supervisory limits (Beach, 2014). Second principle which provides

supervisors to monitor the intra group transactions related to material of various regulated

financial entities on a specific time. It is important for financial entities to reports these

transactions to help under stand the intra group transactions of these financial conglomerate.

Supervisors should maintain the amount of communication and communicate on a regular basis

in order to find out the problems of its subsidiary. It is a responsibility of supervisors to maintain

and ascertain each others concerns and coordinates properly and take necessary actions to over

come the problems which are related to intra group transactions within the group. Supervisors

should deal in an effective and efficient and in a very appropriate manner with intra group

transactions involving materials which have a detrimental effect on the entities which are

regulated directly or through various detrimental effect. Following is the example which shows

the treatment of Unrealised profit in inventories :

Unrealised profit in inventories

ABC Ltd has two subsidiaries: XYZ Ltd, in which it has 70 % interest; and PQR Ltd, in

which it has a 65 % interest. During an accounting period, XYZ Ltd sold goods to PQR Ltd for

$110,000. The goods had been manufactured by XYZ Ltd at a cost of $75,000. Of these goods,

PQR Ltd had sold 50 per cent by the end of an accounting period.

5

In the preparation of ABC Limited consolidated financial statements, the profit which was

unrealised on remaining inventories are still held by PQR Ltd will be eliminated in the

consolidated statements. These inventories were transferred from XYZ Ltd to PQR Ltd at a value

of $50,000, and their cost to the group which was $35,000. The intra group profit has to be

eliminated from inventories, therefore, is $15,000. The proportion which is attributed to non-

controlling interests, assuming if the first method described above is adopted, it is determined by

reference to group’s proportionate interest in selling company, XYZ Ltd, of which ABC Ltd

owns 70 per cent and the non-controlling interests own 30 per cent. The amount is therefore

$15,000 × 30 per cent = $4,500.

PART C

According to Australian Accounting Standard Board 127 Consolidated and Separate

Financial Statements and Australian Accounting Standard Board 101 Presentation of Financial

statements states that it is mandatory for the parent company to show the non controlling interest

to be shown separately in the consolidated financial statements (Nichols, Street and Tarca, 2013).

Following are the changes which parent company has to follow in order to clearly represent its

financial statements:

In accordance with paragraphs 4(a), Aus4.1 and Aus4.2 of AASB 10 any parent company

who does not want to prepare the consolidated financial statements can elect not to prepare the

financial statements consolidated to parent company instead can prepare separate financial

statements but has to disclose it in separate financial statements:

(a) the fact that financial statements are prepared are separate from the parent

company, and the separate name, principle place of business is being used and

exemption are also given from the consolidated statements separately. It is

important for the companies to disclose the nature of business and principle place

of business if separate from the company whose consolidated financial statements

which complies with the International Financial Reporting Standards have been

produced by the company for the use of general public, and the address where

these consolidated financial statements can be obtained.

(b) It should disclose list which shows a significant investments in various other

subsidiaries, associates and joint venture which should include:

The name of those Investee.

6

unrealised on remaining inventories are still held by PQR Ltd will be eliminated in the

consolidated statements. These inventories were transferred from XYZ Ltd to PQR Ltd at a value

of $50,000, and their cost to the group which was $35,000. The intra group profit has to be

eliminated from inventories, therefore, is $15,000. The proportion which is attributed to non-

controlling interests, assuming if the first method described above is adopted, it is determined by

reference to group’s proportionate interest in selling company, XYZ Ltd, of which ABC Ltd

owns 70 per cent and the non-controlling interests own 30 per cent. The amount is therefore

$15,000 × 30 per cent = $4,500.

PART C

According to Australian Accounting Standard Board 127 Consolidated and Separate

Financial Statements and Australian Accounting Standard Board 101 Presentation of Financial

statements states that it is mandatory for the parent company to show the non controlling interest

to be shown separately in the consolidated financial statements (Nichols, Street and Tarca, 2013).

Following are the changes which parent company has to follow in order to clearly represent its

financial statements:

In accordance with paragraphs 4(a), Aus4.1 and Aus4.2 of AASB 10 any parent company

who does not want to prepare the consolidated financial statements can elect not to prepare the

financial statements consolidated to parent company instead can prepare separate financial

statements but has to disclose it in separate financial statements:

(a) the fact that financial statements are prepared are separate from the parent

company, and the separate name, principle place of business is being used and

exemption are also given from the consolidated statements separately. It is

important for the companies to disclose the nature of business and principle place

of business if separate from the company whose consolidated financial statements

which complies with the International Financial Reporting Standards have been

produced by the company for the use of general public, and the address where

these consolidated financial statements can be obtained.

(b) It should disclose list which shows a significant investments in various other

subsidiaries, associates and joint venture which should include:

The name of those Investee.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The place where the business of the various investee's are located.

Its portion of interest of ownership interest which a investor company has

in its investee company's and the right to vote in the general meetings.

(c) It should also disclose a description of methods which are used in order to account

for various investments which are listed under (b).

A parent company other than parent companies mentioned above in the paragraphs 4(a),

Aus4.1 and Aus4.2 of AASB 10 or any investors who have a joint control of, or have a

significant influence over an investee who intend to prepare the separate statement of their

financial positions, the parent company or an investor shall recognize and identify the financial

statements which are prepared in with the accordance with AASB 10, AASB 11 or AASB 128

in which they all are related (Spieth, Schneckenberg and Ricart, 2014). The parent company and

the investors also have to disclose in their separate financial statements the followings:

(a) The fact which states that the financial statements of investee are separate from

financial statements of parent and investor, it should also include the reasons that

why these statements are need to be prepared even if it is not required by law.

(b) It should also list the various significant investments in all subsidiaries, associates

and joints ventures which should include:

◦ Name of those various investments.

◦ The place in which the business is operated of these various investees

◦ the proportion in which the investors has the controlling interest in the

ownership and voting rights held in the investee companies

(c) a description of methods which is used by the investor company to account for the

investments which are listed under point (b)

The Australian Accounting Standard Board 127 is applicable to the entities as under:

entities which are required by the Corporation Act 2001 are required to prepare the

financial reports.

Governments which are preparing the financial statements for General Government

Sectors and the whole of government.

Entities which are private or public by its nature for profit or not for profit sectors are

required to prepare the financial statements for general purpose.

7

Its portion of interest of ownership interest which a investor company has

in its investee company's and the right to vote in the general meetings.

(c) It should also disclose a description of methods which are used in order to account

for various investments which are listed under (b).

A parent company other than parent companies mentioned above in the paragraphs 4(a),

Aus4.1 and Aus4.2 of AASB 10 or any investors who have a joint control of, or have a

significant influence over an investee who intend to prepare the separate statement of their

financial positions, the parent company or an investor shall recognize and identify the financial

statements which are prepared in with the accordance with AASB 10, AASB 11 or AASB 128

in which they all are related (Spieth, Schneckenberg and Ricart, 2014). The parent company and

the investors also have to disclose in their separate financial statements the followings:

(a) The fact which states that the financial statements of investee are separate from

financial statements of parent and investor, it should also include the reasons that

why these statements are need to be prepared even if it is not required by law.

(b) It should also list the various significant investments in all subsidiaries, associates

and joints ventures which should include:

◦ Name of those various investments.

◦ The place in which the business is operated of these various investees

◦ the proportion in which the investors has the controlling interest in the

ownership and voting rights held in the investee companies

(c) a description of methods which is used by the investor company to account for the

investments which are listed under point (b)

The Australian Accounting Standard Board 127 is applicable to the entities as under:

entities which are required by the Corporation Act 2001 are required to prepare the

financial reports.

Governments which are preparing the financial statements for General Government

Sectors and the whole of government.

Entities which are private or public by its nature for profit or not for profit sectors are

required to prepare the financial statements for general purpose.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As per Australian Accounting Standard Board 1053 Application of Tiers of Australian

Accounting Standards establishes various reporting framework which consists of two tiers of

reporting requirements such as Tier 1: Australian Accounting Standards and Tier 2: Australian

Accounting Standards Reduced Disclosure Requirements (Weil, Schipper and Francis, 2013).

Tier 2 requirements states the recognition, presentation and measurement requirements of

Tier 1 and substantially reduced disclosure requirements as compared to requirements of Tier 1.

It also includes the various requirements which are specific to the Australian entities. The

disclosure requirement which are required under Tier 2 are determined through separate due

process with various amendments which are being made subsequently (Maroun and van Zijl,

2016). As per Australian Accounting Standards Board 127 separate Financial Statements which

incorporates IAS 27 Separate Financial Statements which are issued by International Accounting

Standards Board (IASB). As per the Australian Accounting Standard Board 127 presentation of

financial statements it is important for the companies to present the following item along with

their non comprehensive income in addition with Profit and Loss for the period:

a) Profit or loss which is attributable to :

i. non controlling interests

ii. Owners of the parent companies

b) Comprehensive income for the period which is to be attributed

i. non controlling interest

ii. owners of the parent companies (van Essen, Van Oosterhout and Heugens, 2013).

CONCLUSION

From above project report it has been concluded that corporate and financial accounting

is very crucial for all the financial companies. Eventually, the corporate takeover decisions are

made by reviewing different factors. Additionally, the report concludes about the basic

requirement of the legislation for formation of the company as well as it contains about the

various method by which a company can raise their fund or capital. Though, companies have

many option to expand their funding but all have some drawbacks and advantages. So it is

necessary to choose a right option. Apart from these, the project report concludes about the

process of preparation of financial statements.

8

Accounting Standards establishes various reporting framework which consists of two tiers of

reporting requirements such as Tier 1: Australian Accounting Standards and Tier 2: Australian

Accounting Standards Reduced Disclosure Requirements (Weil, Schipper and Francis, 2013).

Tier 2 requirements states the recognition, presentation and measurement requirements of

Tier 1 and substantially reduced disclosure requirements as compared to requirements of Tier 1.

It also includes the various requirements which are specific to the Australian entities. The

disclosure requirement which are required under Tier 2 are determined through separate due

process with various amendments which are being made subsequently (Maroun and van Zijl,

2016). As per Australian Accounting Standards Board 127 separate Financial Statements which

incorporates IAS 27 Separate Financial Statements which are issued by International Accounting

Standards Board (IASB). As per the Australian Accounting Standard Board 127 presentation of

financial statements it is important for the companies to present the following item along with

their non comprehensive income in addition with Profit and Loss for the period:

a) Profit or loss which is attributable to :

i. non controlling interests

ii. Owners of the parent companies

b) Comprehensive income for the period which is to be attributed

i. non controlling interest

ii. owners of the parent companies (van Essen, Van Oosterhout and Heugens, 2013).

CONCLUSION

From above project report it has been concluded that corporate and financial accounting

is very crucial for all the financial companies. Eventually, the corporate takeover decisions are

made by reviewing different factors. Additionally, the report concludes about the basic

requirement of the legislation for formation of the company as well as it contains about the

various method by which a company can raise their fund or capital. Though, companies have

many option to expand their funding but all have some drawbacks and advantages. So it is

necessary to choose a right option. Apart from these, the project report concludes about the

process of preparation of financial statements.

8

REFERENCES

Books and Journals

Shroff, N., Verdi, R. S. and Yu, G., 2013. Information environment and the investment decisions

of multinational corporations. The Accounting Review. 89(2). pp.759-790.

Chiu, I. H., 2013. Reviving shareholder stewardship: critically examining the impact of corporate

transparency reforms in the UK. Del. J. Corp. L. 38. p.983.

Younge, K. A., Tong, T. W. and Fleming, L., 2015. How anticipated employee mobility affects

acquisition likelihood: Evidence from a natural experiment. Strategic Management

Journal. 36(5). pp.686-708.

Barth, J. R., Caprio Jr, G. and Levine, R., 2013. Bank regulation and supervision in 180 countries

from 1999 to 2011. Journal of Financial Economic Policy. 5(2). pp.111-219.

Beach, L. R., 2014. Decision making in the workplace: A unified perspective. Psychology Press.

Nichols, N. B., Street, D. L. and Tarca, A., 2013. The impact of segment reporting under the

IFRS 8 and SFAS 131 management approach: A research review. Journal of

International Financial Management & Accounting. 24(3). pp.261-312.

Spieth, P., Schneckenberg, D. and Ricart, J. E., 2014. Business model innovation–state of the art

and future challenges for the field. R&d Management. 44(3). pp.237-247.

Weil, R. L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Maroun, W. and van Zijl, W., 2016. Isomorphism and resistance in implementing IFRS 10 and

IFRS 12. The British Accounting Review. 48(2). pp.220-239.

van Essen, M., Van Oosterhout, J. and Heugens, P. P., 2013. Competition and cooperation in

corporate governance: The effects of labor institutions on blockholder effectiveness in

23 European countries. Organization Science. 24(2). pp.530-551.

9

Books and Journals

Shroff, N., Verdi, R. S. and Yu, G., 2013. Information environment and the investment decisions

of multinational corporations. The Accounting Review. 89(2). pp.759-790.

Chiu, I. H., 2013. Reviving shareholder stewardship: critically examining the impact of corporate

transparency reforms in the UK. Del. J. Corp. L. 38. p.983.

Younge, K. A., Tong, T. W. and Fleming, L., 2015. How anticipated employee mobility affects

acquisition likelihood: Evidence from a natural experiment. Strategic Management

Journal. 36(5). pp.686-708.

Barth, J. R., Caprio Jr, G. and Levine, R., 2013. Bank regulation and supervision in 180 countries

from 1999 to 2011. Journal of Financial Economic Policy. 5(2). pp.111-219.

Beach, L. R., 2014. Decision making in the workplace: A unified perspective. Psychology Press.

Nichols, N. B., Street, D. L. and Tarca, A., 2013. The impact of segment reporting under the

IFRS 8 and SFAS 131 management approach: A research review. Journal of

International Financial Management & Accounting. 24(3). pp.261-312.

Spieth, P., Schneckenberg, D. and Ricart, J. E., 2014. Business model innovation–state of the art

and future challenges for the field. R&d Management. 44(3). pp.237-247.

Weil, R. L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Maroun, W. and van Zijl, W., 2016. Isomorphism and resistance in implementing IFRS 10 and

IFRS 12. The British Accounting Review. 48(2). pp.220-239.

van Essen, M., Van Oosterhout, J. and Heugens, P. P., 2013. Competition and cooperation in

corporate governance: The effects of labor institutions on blockholder effectiveness in

23 European countries. Organization Science. 24(2). pp.530-551.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.