Case Analysis: Talbros Automotive Components Limited - Valuation

VerifiedAdded on 2020/11/02

|31

|5852

|1085

Case Study

AI Summary

This case study analyzes Talbros Automotive Components Limited, focusing on relative valuation for mergers and acquisitions. It explores comparable company analysis and precedent transaction analysis to determine the implied share price and total company value. The study uses financial data from the case and industry sources, employing EV/Sales, EV/EBITDA, and P/E multiples. The report outlines the valuation process, including selecting comparable companies, determining metrics, calculating multiples, and applying them to estimate equity and enterprise value. It also discusses the limitations of the study, such as time constraints and data availability. The analysis aims to provide insights into the valuation of the company, considering factors like geography, industry, and financial size, while acknowledging the differences in sales volume compared to other companies in the industry.

Case Analysis on:Talbros Automotive

Components Limited: Relative valuation

Components Limited: Relative valuation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

F- 506

Cases in Financial Decision Making

A Case Study on

Case Analysis on Talbros Automotive

Components Limited: Relative Valuation

Submitted To

Dr. Gazi Mohammad HasanJamil

Associate Professor

Department of Finance

University of Dhaka

Submitted By: Group 15

Serial No Name Roll Number

1. Md. Ashiqul Islam 21-817

2. Santa Mazumder 21-913

3. Christina Madhubi Palma 21-914

Date of Submission: 20 August, 2020

Cases in Financial Decision Making

A Case Study on

Case Analysis on Talbros Automotive

Components Limited: Relative Valuation

Submitted To

Dr. Gazi Mohammad HasanJamil

Associate Professor

Department of Finance

University of Dhaka

Submitted By: Group 15

Serial No Name Roll Number

1. Md. Ashiqul Islam 21-817

2. Santa Mazumder 21-913

3. Christina Madhubi Palma 21-914

Date of Submission: 20 August, 2020

Letter of Transmittal

20 August, 2020.

Dr. Gazi Mohammad HasanJamil

Associate Professor

Department of Finance

University of Dhaka

Subject: Submission of Case Analysis Report on “Case Analysis on Talbros Automotive

Components Limited: Relative Valuation”

Sir,

With due respect, we submit here our report on “Talbros Automotive Components Limited:

Relative Valuation” for your kind evaluation that we prepare as a part of requirement of our

MBA Program “Cases in Financial Decision Making” course. During the preparation of the

report we have given our best effort to make it effective. We have tried our best to present our

ideas and findings as clearly as we could within the time and resource available. We express our

gratitude to you for providing us the opportunity to learn about the case analysis. We have

devoted our best effort to make the ultimate solution of our prescribed case.

During preparing this report we have enforced our best effort. Surely, it enriches our knowledge

and promotes our study. Thanks for giving us such an opportunity for working on the topic. We

hope you will find the report in appropriate manner. We are looking forward to your feedback.

Sincerely yours,

Christina Madhubi Palma

Sec: A, Roll Num:21-914

On behalf of Group 15

Department of Finance

University of Dhaka

20 August, 2020.

Dr. Gazi Mohammad HasanJamil

Associate Professor

Department of Finance

University of Dhaka

Subject: Submission of Case Analysis Report on “Case Analysis on Talbros Automotive

Components Limited: Relative Valuation”

Sir,

With due respect, we submit here our report on “Talbros Automotive Components Limited:

Relative Valuation” for your kind evaluation that we prepare as a part of requirement of our

MBA Program “Cases in Financial Decision Making” course. During the preparation of the

report we have given our best effort to make it effective. We have tried our best to present our

ideas and findings as clearly as we could within the time and resource available. We express our

gratitude to you for providing us the opportunity to learn about the case analysis. We have

devoted our best effort to make the ultimate solution of our prescribed case.

During preparing this report we have enforced our best effort. Surely, it enriches our knowledge

and promotes our study. Thanks for giving us such an opportunity for working on the topic. We

hope you will find the report in appropriate manner. We are looking forward to your feedback.

Sincerely yours,

Christina Madhubi Palma

Sec: A, Roll Num:21-914

On behalf of Group 15

Department of Finance

University of Dhaka

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Acknowledgement

At first, we would like to express our deepest gratitude the Almighty who gave us energy and the

composure to finish this case study within the scheduled time.

This report is an outcome of our effort, but its successful completion would have been

impossible without the sincere effort and helping attitude of our course instructor. We would like

to thank our honorable course teacher Dr. Gazi Mohammad Hasan Jamil, Associate Professor,

Department of Finance, University of Dhaka for providing us such an important and challenging

case to analyze. We would also like to thank him for giving us excellent guideline about how to

analyze a case and solve it using different techniques.

We would like to express our heartiest gratitude to our team members who shared their expertise

and struggled with difficulties to put meaningful effort in accumulation of solid & complete

information and analysis. Thanks to all the members of our group for working as a team and

participate in brain storming process to solve the case.

At first, we would like to express our deepest gratitude the Almighty who gave us energy and the

composure to finish this case study within the scheduled time.

This report is an outcome of our effort, but its successful completion would have been

impossible without the sincere effort and helping attitude of our course instructor. We would like

to thank our honorable course teacher Dr. Gazi Mohammad Hasan Jamil, Associate Professor,

Department of Finance, University of Dhaka for providing us such an important and challenging

case to analyze. We would also like to thank him for giving us excellent guideline about how to

analyze a case and solve it using different techniques.

We would like to express our heartiest gratitude to our team members who shared their expertise

and struggled with difficulties to put meaningful effort in accumulation of solid & complete

information and analysis. Thanks to all the members of our group for working as a team and

participate in brain storming process to solve the case.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

Chapter – 01

Introduction

1.1. Background of the Report

This report has been undertaken as a part of course F-506 (Cases in Financial Decisions Making)

under the MBA program. Our course instructor Dr. Gazi Mohammad HasanJamil has assigned

us this task to implement our academic knowledge in the real scenario of business. This really

provides us the opportunity to explore and confront the reality about financial analysis.

1.2. Objective of the Study

The main objective of the study is to fulfill the requirement of our course on Cases in Financial

Decision Making and to apply our theoretical knowledge in solving business cases. The other

objectives behind conducting this study are as follows:

To understand the valuation process for merger and acquisition.

To determine the implied share price of Talbros automotive components limited under

comparable company analysis and comparable transaction analysis.

To find out the total value of the company including control premium that the acquire

company should provide in the merger and acquisition process.

1.3. Scope of the Study

The study topic allows us to do comparable company analysis and comparable transaction

analysis in Talbros automotive components limited. We analyzed the financial condition of this

company and tried to find out the best implied share price of the company. Mean, median,

maximum mad minimum multiples have been considered while doing valuation.

1.4. Methodology of the Report

The data used in this report have been gathered from the case. Relevant industry data has been

collected from secondary sources that are not provided in the case.

The theoretical part of this report has been collected from the case and text provided by our

honorable course teacher.

Required assumptions have been made in consistent with the industry practice.

Introduction

1.1. Background of the Report

This report has been undertaken as a part of course F-506 (Cases in Financial Decisions Making)

under the MBA program. Our course instructor Dr. Gazi Mohammad HasanJamil has assigned

us this task to implement our academic knowledge in the real scenario of business. This really

provides us the opportunity to explore and confront the reality about financial analysis.

1.2. Objective of the Study

The main objective of the study is to fulfill the requirement of our course on Cases in Financial

Decision Making and to apply our theoretical knowledge in solving business cases. The other

objectives behind conducting this study are as follows:

To understand the valuation process for merger and acquisition.

To determine the implied share price of Talbros automotive components limited under

comparable company analysis and comparable transaction analysis.

To find out the total value of the company including control premium that the acquire

company should provide in the merger and acquisition process.

1.3. Scope of the Study

The study topic allows us to do comparable company analysis and comparable transaction

analysis in Talbros automotive components limited. We analyzed the financial condition of this

company and tried to find out the best implied share price of the company. Mean, median,

maximum mad minimum multiples have been considered while doing valuation.

1.4. Methodology of the Report

The data used in this report have been gathered from the case. Relevant industry data has been

collected from secondary sources that are not provided in the case.

The theoretical part of this report has been collected from the case and text provided by our

honorable course teacher.

Required assumptions have been made in consistent with the industry practice.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.5. Data Analysis

To analyze and solve the problems we have used valuation techniques in MS Excel.

1.6. Limitations of the Study

Learning all functions, moods of business, risk factors were quite tough within specified

timeframe.

Time constraint is a major issue for solving this huge case.

Data provided in the case were not sufficient.

To analyze and solve the problems we have used valuation techniques in MS Excel.

1.6. Limitations of the Study

Learning all functions, moods of business, risk factors were quite tough within specified

timeframe.

Time constraint is a major issue for solving this huge case.

Data provided in the case were not sufficient.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Chapter – 03

Valuation for Merger and Acquisition

3.1Valuation for Merger and acquisition:

When valuing a company as a going concern, there are three main valuation methods used by

industry practitioners: (1) DCF analysis, (2) comparable company analysis, and (3) precedent

transactions. These are the most common methods of valuation used in investment banking,

equity research, private equity, corporate development, mergers & acquisitions (M&A),

leveraged buyouts (LBO), and most areas of finance. When valuing a business or asset, there are

three broad categories that each contains their own methods. The Cost Approach looks at what it

costs to build something and this method is not frequently used by finance professionals to value

a company as a going concern. Next is the Market Approach, this is a form of relative

valuation and frequently used in the industry. It includes Comparable Analysis, Precedent

Transactions. Finally, the discounted cash flow (DCF) approach is a form of intrinsic

valuation and is the most detailed and thorough approach to valuation modeling.

Method 1: Comparable Analysis

Comparable company analysis (also called “trading multiples” or “peer group analysis” or

“equity comps” or “public market multiples”) is a relative valuation method in which you

compare the current value of a business to other similar businesses by looking at trading

multiples like P/E, EV/EBITDA, or other ratios. Multiples of EBITDA are the most common

valuation method. The “comps” valuation method provides an observable value for the business,

based on what companies are currently worth. Comps are the most widely used approach, as they

are easy to calculate and always current.

Method 2: Precedent Transactions

Precedent transactions analysis is another form of relative valuation where we compare the

company in question to other businesses that have recently been sold or acquired in the same

industry. These transaction values include the take-over premium included in the price for which

they were acquired. These values represent the value of a business. They are useful for M&A

transactions, but can easily become stale-dated and no longer reflective of the current market as

time passes. They are less commonly used than Comps or market trading multiples.

Valuation for Merger and Acquisition

3.1Valuation for Merger and acquisition:

When valuing a company as a going concern, there are three main valuation methods used by

industry practitioners: (1) DCF analysis, (2) comparable company analysis, and (3) precedent

transactions. These are the most common methods of valuation used in investment banking,

equity research, private equity, corporate development, mergers & acquisitions (M&A),

leveraged buyouts (LBO), and most areas of finance. When valuing a business or asset, there are

three broad categories that each contains their own methods. The Cost Approach looks at what it

costs to build something and this method is not frequently used by finance professionals to value

a company as a going concern. Next is the Market Approach, this is a form of relative

valuation and frequently used in the industry. It includes Comparable Analysis, Precedent

Transactions. Finally, the discounted cash flow (DCF) approach is a form of intrinsic

valuation and is the most detailed and thorough approach to valuation modeling.

Method 1: Comparable Analysis

Comparable company analysis (also called “trading multiples” or “peer group analysis” or

“equity comps” or “public market multiples”) is a relative valuation method in which you

compare the current value of a business to other similar businesses by looking at trading

multiples like P/E, EV/EBITDA, or other ratios. Multiples of EBITDA are the most common

valuation method. The “comps” valuation method provides an observable value for the business,

based on what companies are currently worth. Comps are the most widely used approach, as they

are easy to calculate and always current.

Method 2: Precedent Transactions

Precedent transactions analysis is another form of relative valuation where we compare the

company in question to other businesses that have recently been sold or acquired in the same

industry. These transaction values include the take-over premium included in the price for which

they were acquired. These values represent the value of a business. They are useful for M&A

transactions, but can easily become stale-dated and no longer reflective of the current market as

time passes. They are less commonly used than Comps or market trading multiples.

Method 3: DCF Analysis

Discounted Cash Flow (DCF) analysis is an intrinsic value approach where an analyst forecasts

the business’ unlevered free cash flow into the future and discounts it back to today at the firm’s

Weighted Average Cost of Capital (WACC).A DCF analysis is performed by building a financial

model in Excel and requires an extensive amount of detail and analysis. It is the most detailed of

the three approaches, requires the most assumptions, and often produces the highest value.

However, the effort required for preparing a DCF model will also often result in the most

accurate valuation. A DCF model allows the analyst to forecast value based on different

scenarios, and even perform a sensitivity analysis. For larger businesses, the DCF value is

commonly a sum-of-the-parts analysis, where different business units are modeled individually

and added together.

3.2 Steps in Comparable company analysis

To value a company with CCA, follow these steps:

Step 1: Select an appropriate set of comparable public companies.

Step 2: Determine the metrics and multiples.

Step 3: Calculate the metrics and multiples for all the companies.

Step 4: Apply the median or mean multiples to estimate Implied Equity Value and Enterprise

Value.

3.2.1 Step 1: Select an Appropriate Set of Comparable Public Companies

We normally can screen companies by geography, industry, and financial “size.” The first step in

this method was finding a set of comparable firms. Agarwal searched for publicly traded firms

whose primary industry classification was auto parts and equipment, which yielded a list of four

firms. He used the following screen for Talbros Automotive Components limited.

Geography:

Talbros Automotive Components limited is india based company. The Company has

manufacturing facilities situated in over nine locations across approximately three states in India.

Its gaskets manufacturing facilities are located in Faridabad, Haryana; Pune, Maharashtra, and

Sitarganj, Uttarakhand. Its forging manufacturing facilities are located in Bawal, Haryana.

Munjal Showa Limited was established in 1985. It was started as a technical joint venture

between Showa Corporation, Japan, and Hero Group. The company’s manufacturing operations

were spread across the states of Haryana and Uttarakhand.

15, 2020 to May 14, 2020.

Discounted Cash Flow (DCF) analysis is an intrinsic value approach where an analyst forecasts

the business’ unlevered free cash flow into the future and discounts it back to today at the firm’s

Weighted Average Cost of Capital (WACC).A DCF analysis is performed by building a financial

model in Excel and requires an extensive amount of detail and analysis. It is the most detailed of

the three approaches, requires the most assumptions, and often produces the highest value.

However, the effort required for preparing a DCF model will also often result in the most

accurate valuation. A DCF model allows the analyst to forecast value based on different

scenarios, and even perform a sensitivity analysis. For larger businesses, the DCF value is

commonly a sum-of-the-parts analysis, where different business units are modeled individually

and added together.

3.2 Steps in Comparable company analysis

To value a company with CCA, follow these steps:

Step 1: Select an appropriate set of comparable public companies.

Step 2: Determine the metrics and multiples.

Step 3: Calculate the metrics and multiples for all the companies.

Step 4: Apply the median or mean multiples to estimate Implied Equity Value and Enterprise

Value.

3.2.1 Step 1: Select an Appropriate Set of Comparable Public Companies

We normally can screen companies by geography, industry, and financial “size.” The first step in

this method was finding a set of comparable firms. Agarwal searched for publicly traded firms

whose primary industry classification was auto parts and equipment, which yielded a list of four

firms. He used the following screen for Talbros Automotive Components limited.

Geography:

Talbros Automotive Components limited is india based company. The Company has

manufacturing facilities situated in over nine locations across approximately three states in India.

Its gaskets manufacturing facilities are located in Faridabad, Haryana; Pune, Maharashtra, and

Sitarganj, Uttarakhand. Its forging manufacturing facilities are located in Bawal, Haryana.

Munjal Showa Limited was established in 1985. It was started as a technical joint venture

between Showa Corporation, Japan, and Hero Group. The company’s manufacturing operations

were spread across the states of Haryana and Uttarakhand.

15, 2020 to May 14, 2020.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Established in 1961, Gabriel India Limited had partnered with Maremont Corporation to

manufacture shock absorbers. The company had six manufacturing facilities (Pune, Khandsa,

Nashik, Hosur,Dewas, and Parwanoo) and three satellite plants (Sanand, Malur, and

Aurangabad).

Minda Industries Limited was established in 1992 as the flagship company of the UNO Minda

Group. It was the largest manufacturer of automotive switches for two-wheelers, three-wheelers,

and off-road vehicles in India. It is also an India based comapny.

Sona Koyo Steering Systems Limited, established in 1985, was the flagship company of Sona

Group and the largest manufacturer of steering systems in India, catering to passenger cars,

utility vehicles, and light commercial vehicles. .it is also an India based comapny.

Industry:

Talbros’s major products were gaskets and heat shields, forgings, suspension systems and

modules, anti-vibration components, and hoses. The company’s manufactured product lines

catered to various segments, including passenger vehicles, commercial vehicles, two-wheelers,

three-wheelers, and farm equipment

Munjal Showa Limited manufactured auto components for two-wheelers and four-wheelers. Its

product range consisted of front forks, shock absorbers, struts, gas springs, and window

balancers for sale in the domestic market.

Gabriel India Limited product line included front forks and rear shock absorbers (for two-

wheelers), McPherson struts and shock absorbers (for passenger cars), axles, cabin and seat

dampers, suspension shock absorbers (for commercial vehicles), and shock absorbers (for

railway coaches).

Minda industries limited was the largest manufacturer of automotive switches for two-wheelers,

three-wheelers, and off-road vehicles in India. Sales to OEMs formed the largest revenue

segment for the company, followed by the after-market and exports.

Sona Koyo Steering Systems Limited, established in 1985, was the flagship company of Sona

Group and the largest manufacturer of steering systems in India, catering to passenger cars,

utility vehicles, and light commercial vehicles. Consider their product lines, we can conclude

that these companies belong to auto parts and equipment.

Authorized for use only by Hossain Fahad in Cases in Financial Decision Making at University of Dhaka from

manufacture shock absorbers. The company had six manufacturing facilities (Pune, Khandsa,

Nashik, Hosur,Dewas, and Parwanoo) and three satellite plants (Sanand, Malur, and

Aurangabad).

Minda Industries Limited was established in 1992 as the flagship company of the UNO Minda

Group. It was the largest manufacturer of automotive switches for two-wheelers, three-wheelers,

and off-road vehicles in India. It is also an India based comapny.

Sona Koyo Steering Systems Limited, established in 1985, was the flagship company of Sona

Group and the largest manufacturer of steering systems in India, catering to passenger cars,

utility vehicles, and light commercial vehicles. .it is also an India based comapny.

Industry:

Talbros’s major products were gaskets and heat shields, forgings, suspension systems and

modules, anti-vibration components, and hoses. The company’s manufactured product lines

catered to various segments, including passenger vehicles, commercial vehicles, two-wheelers,

three-wheelers, and farm equipment

Munjal Showa Limited manufactured auto components for two-wheelers and four-wheelers. Its

product range consisted of front forks, shock absorbers, struts, gas springs, and window

balancers for sale in the domestic market.

Gabriel India Limited product line included front forks and rear shock absorbers (for two-

wheelers), McPherson struts and shock absorbers (for passenger cars), axles, cabin and seat

dampers, suspension shock absorbers (for commercial vehicles), and shock absorbers (for

railway coaches).

Minda industries limited was the largest manufacturer of automotive switches for two-wheelers,

three-wheelers, and off-road vehicles in India. Sales to OEMs formed the largest revenue

segment for the company, followed by the after-market and exports.

Sona Koyo Steering Systems Limited, established in 1985, was the flagship company of Sona

Group and the largest manufacturer of steering systems in India, catering to passenger cars,

utility vehicles, and light commercial vehicles. Consider their product lines, we can conclude

that these companies belong to auto parts and equipment.

Authorized for use only by Hossain Fahad in Cases in Financial Decision Making at University of Dhaka from

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

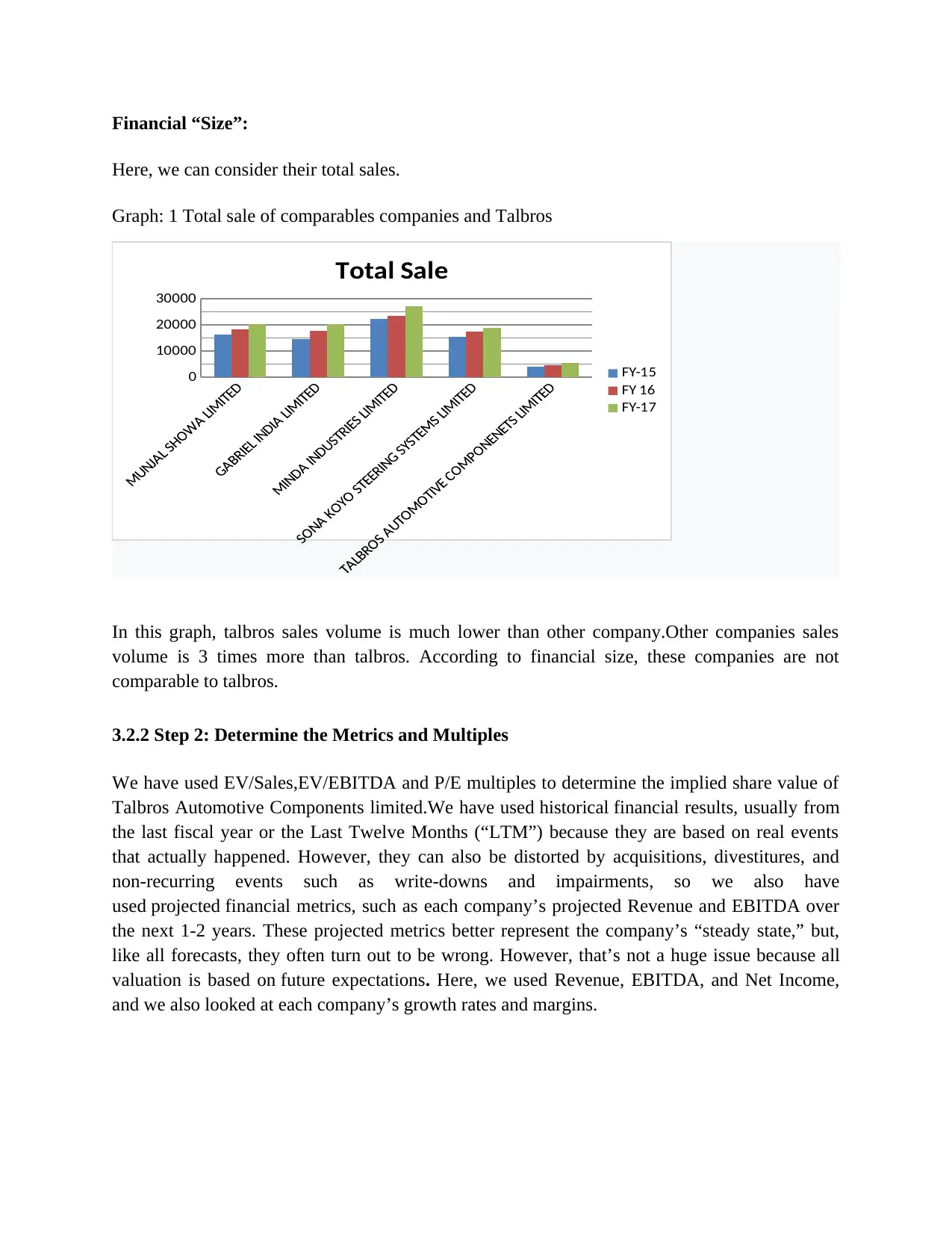

Financial “Size”:

Here, we can consider their total sales.

Graph: 1 Total sale of comparables companies and Talbros

0

10000

20000

30000

Total Sale

FY-15

FY 16

FY-17

In this graph, talbros sales volume is much lower than other company.Other companies sales

volume is 3 times more than talbros. According to financial size, these companies are not

comparable to talbros.

3.2.2 Step 2: Determine the Metrics and Multiples

We have used EV/Sales,EV/EBITDA and P/E multiples to determine the implied share value of

Talbros Automotive Components limited.We have used historical financial results, usually from

the last fiscal year or the Last Twelve Months (“LTM”) because they are based on real events

that actually happened. However, they can also be distorted by acquisitions, divestitures, and

non-recurring events such as write-downs and impairments, so we also have

used projected financial metrics, such as each company’s projected Revenue and EBITDA over

the next 1-2 years. These projected metrics better represent the company’s “steady state,” but,

like all forecasts, they often turn out to be wrong. However, that’s not a huge issue because all

valuation is based on future expectations. Here, we used Revenue, EBITDA, and Net Income,

and we also looked at each company’s growth rates and margins.

Here, we can consider their total sales.

Graph: 1 Total sale of comparables companies and Talbros

0

10000

20000

30000

Total Sale

FY-15

FY 16

FY-17

In this graph, talbros sales volume is much lower than other company.Other companies sales

volume is 3 times more than talbros. According to financial size, these companies are not

comparable to talbros.

3.2.2 Step 2: Determine the Metrics and Multiples

We have used EV/Sales,EV/EBITDA and P/E multiples to determine the implied share value of

Talbros Automotive Components limited.We have used historical financial results, usually from

the last fiscal year or the Last Twelve Months (“LTM”) because they are based on real events

that actually happened. However, they can also be distorted by acquisitions, divestitures, and

non-recurring events such as write-downs and impairments, so we also have

used projected financial metrics, such as each company’s projected Revenue and EBITDA over

the next 1-2 years. These projected metrics better represent the company’s “steady state,” but,

like all forecasts, they often turn out to be wrong. However, that’s not a huge issue because all

valuation is based on future expectations. Here, we used Revenue, EBITDA, and Net Income,

and we also looked at each company’s growth rates and margins.

3.2.3 Step 3: Calculate the Metrics and Multiples for the Comparable Public Companies

We have calculated each company’s Equity Value and Enterprise Value first, get the historical

figures from annual and quarterly reports, and get the projected figures from the case. The

historical financial metrics come directly from the company’s financial statements.

We have calculated each company’s Equity Value and Enterprise Value first, get the historical

figures from annual and quarterly reports, and get the projected figures from the case. The

historical financial metrics come directly from the company’s financial statements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 31

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.