University Finance Report: Performance of Tas Foods Ltd

VerifiedAdded on 2020/05/16

|13

|2932

|432

Report

AI Summary

This report presents a comprehensive financial analysis of Tas Foods Ltd. It begins with a description of the company and its organizational structure, followed by the computation and trend analysis of key performance ratios, including ROA, ROE, and debt ratios, from 2013 to 2016. The report includes a graphical representation of the company's stock price movement and identifies significant factors influencing its share price. It also calculates the company's beta and required rate of return, providing a rationale for conservative investment. Furthermore, the report assesses the weighted average cost of capital (WACC) and its implications on prospective investment projects. Debt and gearing ratios are analyzed, and the company's dividend policy is discussed. The report concludes with a letter of recommendation, summarizing the findings and providing investment advice. This report is a valuable resource for understanding Tas Foods Ltd's financial health and investment potential.

Running head: FINANCE

Finance

Name of the Student

Name of the University

Authors Note

Course ID

Finance

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE

Table of Contents

Description of the Company:.....................................................................................................2

Organization structure of ownership and governance:...............................................................2

Computation of the Performance Ratios:...................................................................................3

Graphical representation of the results:......................................................................................4

Significant factor influencing the share price of Tas Food Ltd:................................................5

Computation of Beta and required rate of return:......................................................................5

Rationale for Conservative Investment:.....................................................................................6

Weighted average of cost of capital:..........................................................................................6

Implication of the WACC on Prospective investment projects:................................................7

Debt ratios for the last two years:..............................................................................................7

Gearing ratio:.............................................................................................................................8

Dividend policy:.........................................................................................................................8

Letter of recommendation:.........................................................................................................8

Reference List:.........................................................................................................................10

Table of Contents

Description of the Company:.....................................................................................................2

Organization structure of ownership and governance:...............................................................2

Computation of the Performance Ratios:...................................................................................3

Graphical representation of the results:......................................................................................4

Significant factor influencing the share price of Tas Food Ltd:................................................5

Computation of Beta and required rate of return:......................................................................5

Rationale for Conservative Investment:.....................................................................................6

Weighted average of cost of capital:..........................................................................................6

Implication of the WACC on Prospective investment projects:................................................7

Debt ratios for the last two years:..............................................................................................7

Gearing ratio:.............................................................................................................................8

Dividend policy:.........................................................................................................................8

Letter of recommendation:.........................................................................................................8

Reference List:.........................................................................................................................10

2FINANCE

Description of the Company:

The Tasmania food company is regarded as the brand endorser with the help of which

the artisan of the company promotes the brand to the wider group of audience. The

Tasmanian food company endorses those brands that falls within the business meeting the

promise of brand and value that is represented by the company (TasFoods Ltd 2018). The

sub-brands under the Tasmanian Food Company will have their effect on their own set of the

unique attributes which would meet the needs of the target market. This would enable the

Tasmania food company to tell the story of the provenance of their products. It enables the

company in developing the new and exciting range of goods categories namely the ethical

free range chicken which meet the changing anticipations of the customers.

Tasmania usually commands the premium brand in the form of place of origin for the

food and beverage products (TasFoods Ltd 2018). Tas food limited has positioned the

company having head office in Tasmania with senior management team that is connected

with the Tasmanian agricultural and food industry in order to obtain the advantage of the

brand.

Organization structure of ownership and governance:

The management team of the Tas Food Ltd is accountable for the strategic direction

of the organization. The organization structure is so designed that the team works closely to

make sure that the Tas Food Ltd meets the demand of the shareholders however provides the

positive, innovative and better working environment for the employees (TasFoods Ltd 2018).

The organization structure of the Tas Food Ltd comprises of the non-executive chairman,

managing director, non-executive director, chief operating officer, chief financial officer and

company secretary. Additionally, the new food production business of the company has the

strong quality assurance team responsible for quality assurance management system that

Description of the Company:

The Tasmania food company is regarded as the brand endorser with the help of which

the artisan of the company promotes the brand to the wider group of audience. The

Tasmanian food company endorses those brands that falls within the business meeting the

promise of brand and value that is represented by the company (TasFoods Ltd 2018). The

sub-brands under the Tasmanian Food Company will have their effect on their own set of the

unique attributes which would meet the needs of the target market. This would enable the

Tasmania food company to tell the story of the provenance of their products. It enables the

company in developing the new and exciting range of goods categories namely the ethical

free range chicken which meet the changing anticipations of the customers.

Tasmania usually commands the premium brand in the form of place of origin for the

food and beverage products (TasFoods Ltd 2018). Tas food limited has positioned the

company having head office in Tasmania with senior management team that is connected

with the Tasmanian agricultural and food industry in order to obtain the advantage of the

brand.

Organization structure of ownership and governance:

The management team of the Tas Food Ltd is accountable for the strategic direction

of the organization. The organization structure is so designed that the team works closely to

make sure that the Tas Food Ltd meets the demand of the shareholders however provides the

positive, innovative and better working environment for the employees (TasFoods Ltd 2018).

The organization structure of the Tas Food Ltd comprises of the non-executive chairman,

managing director, non-executive director, chief operating officer, chief financial officer and

company secretary. Additionally, the new food production business of the company has the

strong quality assurance team responsible for quality assurance management system that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE

provides consistency of system and procedure across the business. Additionally, the

organizational structure comprises of the food and quality assurance management system that

are subjected to numerous regular audits by the independent certification bodies and

regulations.

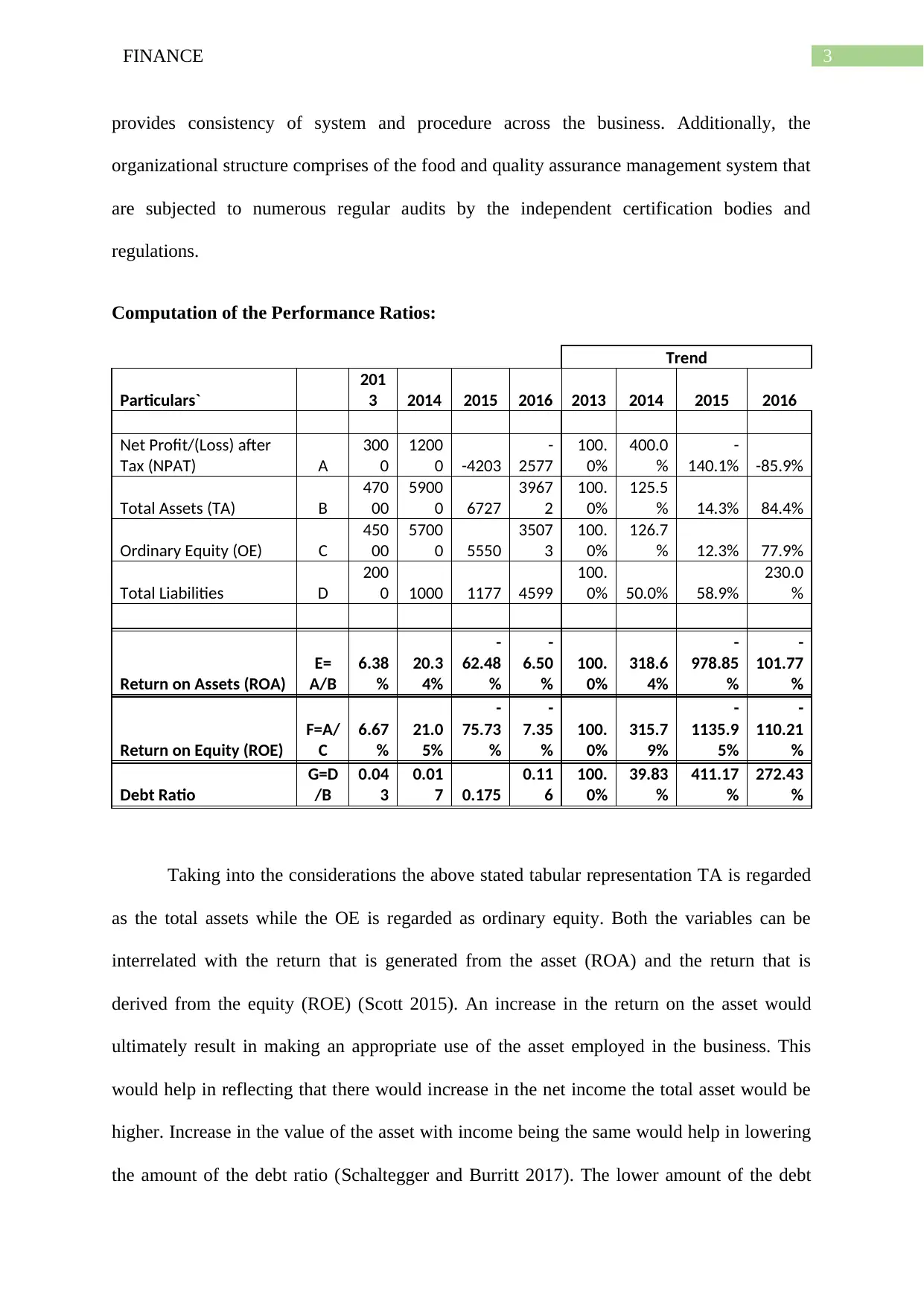

Computation of the Performance Ratios:

Trend

Particulars`

201

3 2014 2015 2016 2013 2014 2015 2016

Net Profit/(Loss) after

Tax (NPAT) A

300

0

1200

0 -4203

-

2577

100.

0%

400.0

%

-

140.1% -85.9%

Total Assets (TA) B

470

00

5900

0 6727

3967

2

100.

0%

125.5

% 14.3% 84.4%

Ordinary Equity (OE) C

450

00

5700

0 5550

3507

3

100.

0%

126.7

% 12.3% 77.9%

Total Liabilities D

200

0 1000 1177 4599

100.

0% 50.0% 58.9%

230.0

%

Return on Assets (ROA)

E=

A/B

6.38

%

20.3

4%

-

62.48

%

-

6.50

%

100.

0%

318.6

4%

-

978.85

%

-

101.77

%

Return on Equity (ROE)

F=A/

C

6.67

%

21.0

5%

-

75.73

%

-

7.35

%

100.

0%

315.7

9%

-

1135.9

5%

-

110.21

%

Debt Ratio

G=D

/B

0.04

3

0.01

7 0.175

0.11

6

100.

0%

39.83

%

411.17

%

272.43

%

Taking into the considerations the above stated tabular representation TA is regarded

as the total assets while the OE is regarded as ordinary equity. Both the variables can be

interrelated with the return that is generated from the asset (ROA) and the return that is

derived from the equity (ROE) (Scott 2015). An increase in the return on the asset would

ultimately result in making an appropriate use of the asset employed in the business. This

would help in reflecting that there would increase in the net income the total asset would be

higher. Increase in the value of the asset with income being the same would help in lowering

the amount of the debt ratio (Schaltegger and Burritt 2017). The lower amount of the debt

provides consistency of system and procedure across the business. Additionally, the

organizational structure comprises of the food and quality assurance management system that

are subjected to numerous regular audits by the independent certification bodies and

regulations.

Computation of the Performance Ratios:

Trend

Particulars`

201

3 2014 2015 2016 2013 2014 2015 2016

Net Profit/(Loss) after

Tax (NPAT) A

300

0

1200

0 -4203

-

2577

100.

0%

400.0

%

-

140.1% -85.9%

Total Assets (TA) B

470

00

5900

0 6727

3967

2

100.

0%

125.5

% 14.3% 84.4%

Ordinary Equity (OE) C

450

00

5700

0 5550

3507

3

100.

0%

126.7

% 12.3% 77.9%

Total Liabilities D

200

0 1000 1177 4599

100.

0% 50.0% 58.9%

230.0

%

Return on Assets (ROA)

E=

A/B

6.38

%

20.3

4%

-

62.48

%

-

6.50

%

100.

0%

318.6

4%

-

978.85

%

-

101.77

%

Return on Equity (ROE)

F=A/

C

6.67

%

21.0

5%

-

75.73

%

-

7.35

%

100.

0%

315.7

9%

-

1135.9

5%

-

110.21

%

Debt Ratio

G=D

/B

0.04

3

0.01

7 0.175

0.11

6

100.

0%

39.83

%

411.17

%

272.43

%

Taking into the considerations the above stated tabular representation TA is regarded

as the total assets while the OE is regarded as ordinary equity. Both the variables can be

interrelated with the return that is generated from the asset (ROA) and the return that is

derived from the equity (ROE) (Scott 2015). An increase in the return on the asset would

ultimately result in making an appropriate use of the asset employed in the business. This

would help in reflecting that there would increase in the net income the total asset would be

higher. Increase in the value of the asset with income being the same would help in lowering

the amount of the debt ratio (Schaltegger and Burritt 2017). The lower amount of the debt

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE

ratio would help in higher amount of return on equity. Therefore, the value of the return on

equity and return on asset is determined with the help of total amount of asset and equity.

The computation that has been done above represents that the return on equity that is

reported during the year 2014 stood 315.79% while in the subsequent year of 2015 and 2016

have declined significantly with -1135.95 and -110.21% respectively. This helps in reflecting

that the proficiency of the firm has declined significantly and insufficient use of the asset

employed in the firm (Warren and Jones 2018). For a healthy organization the amount of the

total assets generally continues to remain higher than the total amount of equity. This is

because the value of the assets that is reported by the firm is higher than the amount of equity

when the liabilities of the firm have declined significantly (Robson, Young and Power 2017).

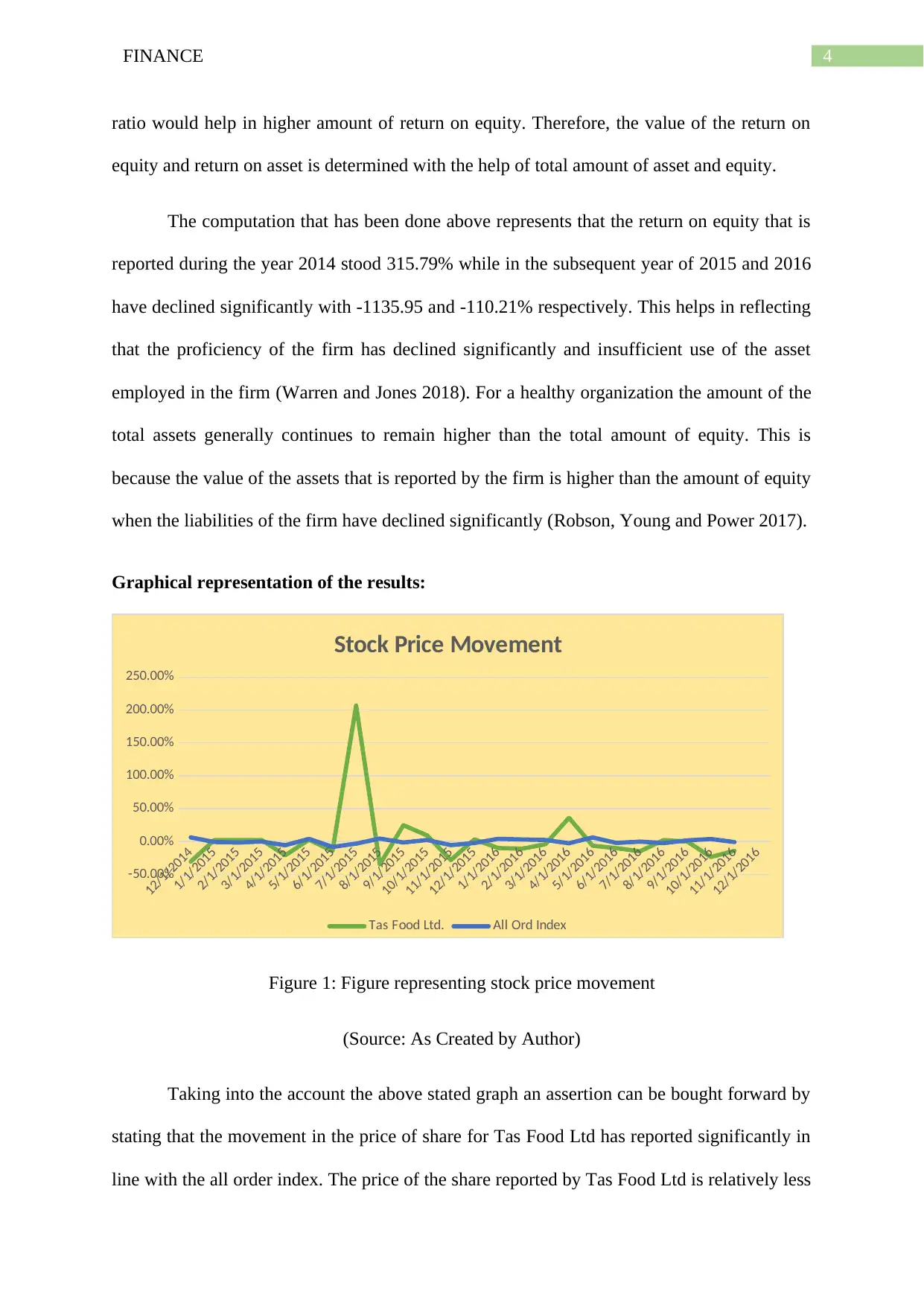

Graphical representation of the results:

12/1/2014

1/1/2015

2/1/2015

3/1/2015

4/1/2015

5/1/2015

6/1/2015

7/1/2015

8/1/2015

9/1/2015

10/1/2015

11/1/2015

12/1/2015

1/1/2016

2/1/2016

3/1/2016

4/1/2016

5/1/2016

6/1/2016

7/1/2016

8/1/2016

9/1/2016

10/1/2016

11/1/2016

12/1/2016

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

Stock Price Movement

Tas Food Ltd. All Ord Index

Figure 1: Figure representing stock price movement

(Source: As Created by Author)

Taking into the account the above stated graph an assertion can be bought forward by

stating that the movement in the price of share for Tas Food Ltd has reported significantly in

line with the all order index. The price of the share reported by Tas Food Ltd is relatively less

ratio would help in higher amount of return on equity. Therefore, the value of the return on

equity and return on asset is determined with the help of total amount of asset and equity.

The computation that has been done above represents that the return on equity that is

reported during the year 2014 stood 315.79% while in the subsequent year of 2015 and 2016

have declined significantly with -1135.95 and -110.21% respectively. This helps in reflecting

that the proficiency of the firm has declined significantly and insufficient use of the asset

employed in the firm (Warren and Jones 2018). For a healthy organization the amount of the

total assets generally continues to remain higher than the total amount of equity. This is

because the value of the assets that is reported by the firm is higher than the amount of equity

when the liabilities of the firm have declined significantly (Robson, Young and Power 2017).

Graphical representation of the results:

12/1/2014

1/1/2015

2/1/2015

3/1/2015

4/1/2015

5/1/2015

6/1/2015

7/1/2015

8/1/2015

9/1/2015

10/1/2015

11/1/2015

12/1/2015

1/1/2016

2/1/2016

3/1/2016

4/1/2016

5/1/2016

6/1/2016

7/1/2016

8/1/2016

9/1/2016

10/1/2016

11/1/2016

12/1/2016

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

Stock Price Movement

Tas Food Ltd. All Ord Index

Figure 1: Figure representing stock price movement

(Source: As Created by Author)

Taking into the account the above stated graph an assertion can be bought forward by

stating that the movement in the price of share for Tas Food Ltd has reported significantly in

line with the all order index. The price of the share reported by Tas Food Ltd is relatively less

5FINANCE

volatile except during the month of June and July where the company reported higher stock

price movement (Beatty and Liao 2014). The evidences that has been presented from the

stock price of Tas Food Ltd suggest that stock price on most of the circumstances have been

moderate. Opposing the higher amount of stock price there has been circumstances where the

company has reported fall in the stock price and at times it has declined below the all

ordinary index (Mullinova 2016).

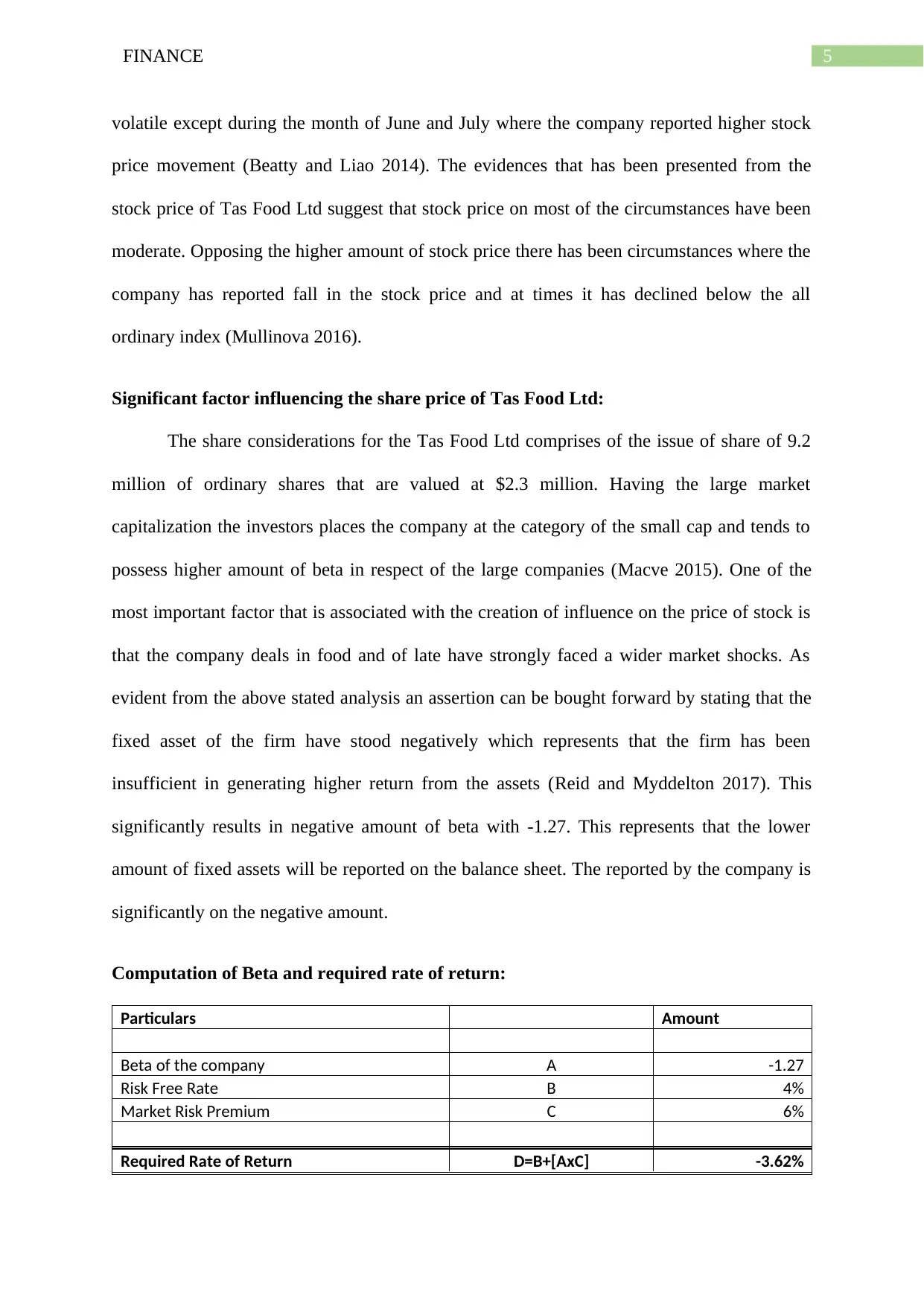

Significant factor influencing the share price of Tas Food Ltd:

The share considerations for the Tas Food Ltd comprises of the issue of share of 9.2

million of ordinary shares that are valued at $2.3 million. Having the large market

capitalization the investors places the company at the category of the small cap and tends to

possess higher amount of beta in respect of the large companies (Macve 2015). One of the

most important factor that is associated with the creation of influence on the price of stock is

that the company deals in food and of late have strongly faced a wider market shocks. As

evident from the above stated analysis an assertion can be bought forward by stating that the

fixed asset of the firm have stood negatively which represents that the firm has been

insufficient in generating higher return from the assets (Reid and Myddelton 2017). This

significantly results in negative amount of beta with -1.27. This represents that the lower

amount of fixed assets will be reported on the balance sheet. The reported by the company is

significantly on the negative amount.

Computation of Beta and required rate of return:

Particulars Amount

Beta of the company A -1.27

Risk Free Rate B 4%

Market Risk Premium C 6%

Required Rate of Return D=B+[AxC] -3.62%

volatile except during the month of June and July where the company reported higher stock

price movement (Beatty and Liao 2014). The evidences that has been presented from the

stock price of Tas Food Ltd suggest that stock price on most of the circumstances have been

moderate. Opposing the higher amount of stock price there has been circumstances where the

company has reported fall in the stock price and at times it has declined below the all

ordinary index (Mullinova 2016).

Significant factor influencing the share price of Tas Food Ltd:

The share considerations for the Tas Food Ltd comprises of the issue of share of 9.2

million of ordinary shares that are valued at $2.3 million. Having the large market

capitalization the investors places the company at the category of the small cap and tends to

possess higher amount of beta in respect of the large companies (Macve 2015). One of the

most important factor that is associated with the creation of influence on the price of stock is

that the company deals in food and of late have strongly faced a wider market shocks. As

evident from the above stated analysis an assertion can be bought forward by stating that the

fixed asset of the firm have stood negatively which represents that the firm has been

insufficient in generating higher return from the assets (Reid and Myddelton 2017). This

significantly results in negative amount of beta with -1.27. This represents that the lower

amount of fixed assets will be reported on the balance sheet. The reported by the company is

significantly on the negative amount.

Computation of Beta and required rate of return:

Particulars Amount

Beta of the company A -1.27

Risk Free Rate B 4%

Market Risk Premium C 6%

Required Rate of Return D=B+[AxC] -3.62%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE

Trend

Particulars`

201

3

201

4 2015

201

6 2013 2014 2015 2016

EBIT A

300

0

180

00

-

2096

-

261

1

100.0

0%

600.0

0%

-

69.87

%

-

87.03

%

Total Assets B

470

00

590

00 6727

396

72

100.0

0%

125.5

3%

14.31

%

84.41

%

Net Profit/(Loss) after

Tax (NPAT) C

300

0

120

00

-

4203

-

257

7

100.0

0%

400.0

0%

-

140.10

%

-

85.90

%

Owner's Equity D

450

00

570

00 5550

350

73

100.0

0%

126.6

7%

12.33

%

77.94

%

Return on Equity

E=(A/

B)x(C/A)x

(B/D)

6.6

7%

21.0

5%

-

75.7

3%

-

7.35

%

100.0

0%

315.7

9%

-

1135.9

5%

-

110.2

1%

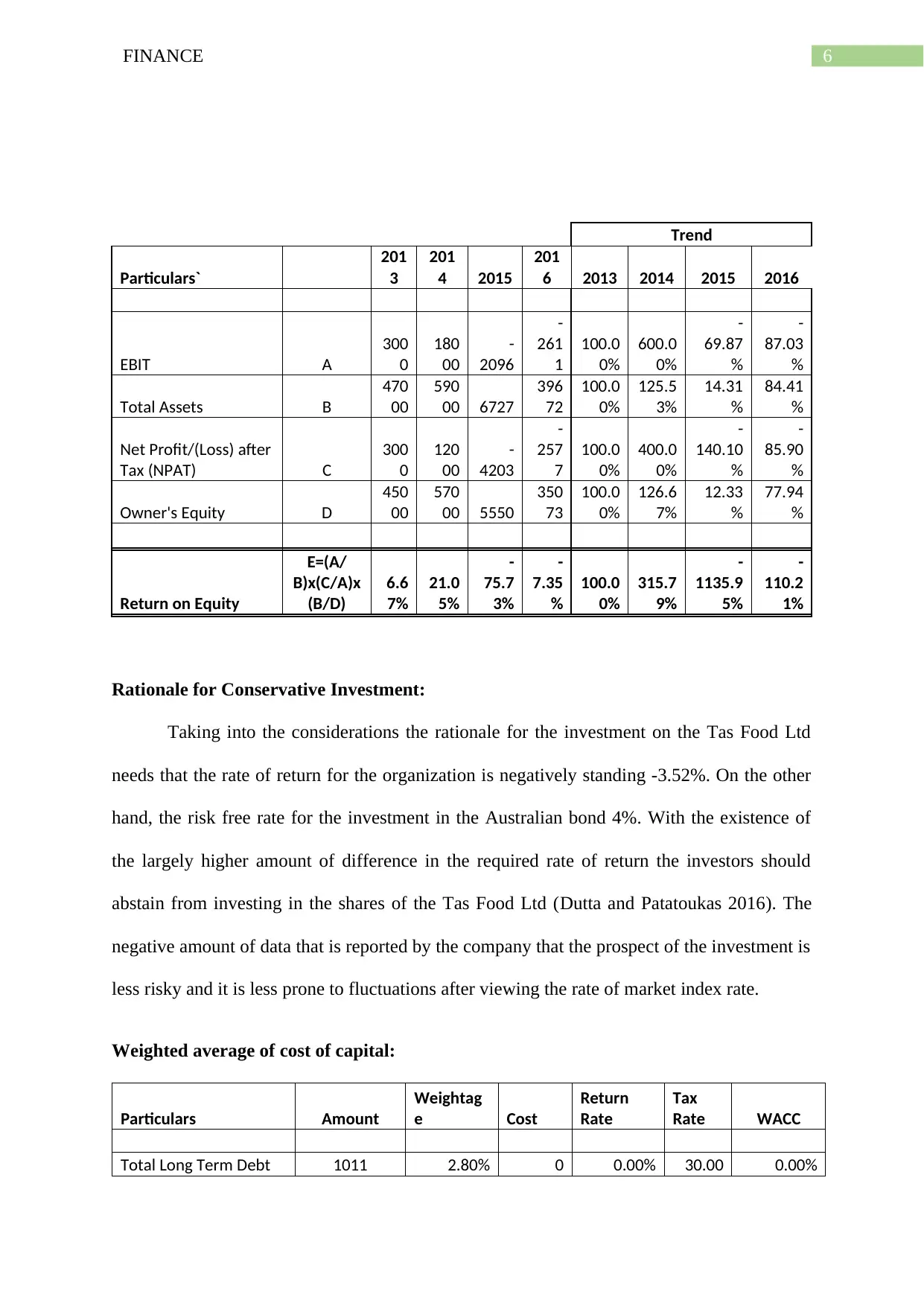

Rationale for Conservative Investment:

Taking into the considerations the rationale for the investment on the Tas Food Ltd

needs that the rate of return for the organization is negatively standing -3.52%. On the other

hand, the risk free rate for the investment in the Australian bond 4%. With the existence of

the largely higher amount of difference in the required rate of return the investors should

abstain from investing in the shares of the Tas Food Ltd (Dutta and Patatoukas 2016). The

negative amount of data that is reported by the company that the prospect of the investment is

less risky and it is less prone to fluctuations after viewing the rate of market index rate.

Weighted average of cost of capital:

Particulars Amount

Weightag

e Cost

Return

Rate

Tax

Rate WACC

Total Long Term Debt 1011 2.80% 0 0.00% 30.00 0.00%

Trend

Particulars`

201

3

201

4 2015

201

6 2013 2014 2015 2016

EBIT A

300

0

180

00

-

2096

-

261

1

100.0

0%

600.0

0%

-

69.87

%

-

87.03

%

Total Assets B

470

00

590

00 6727

396

72

100.0

0%

125.5

3%

14.31

%

84.41

%

Net Profit/(Loss) after

Tax (NPAT) C

300

0

120

00

-

4203

-

257

7

100.0

0%

400.0

0%

-

140.10

%

-

85.90

%

Owner's Equity D

450

00

570

00 5550

350

73

100.0

0%

126.6

7%

12.33

%

77.94

%

Return on Equity

E=(A/

B)x(C/A)x

(B/D)

6.6

7%

21.0

5%

-

75.7

3%

-

7.35

%

100.0

0%

315.7

9%

-

1135.9

5%

-

110.2

1%

Rationale for Conservative Investment:

Taking into the considerations the rationale for the investment on the Tas Food Ltd

needs that the rate of return for the organization is negatively standing -3.52%. On the other

hand, the risk free rate for the investment in the Australian bond 4%. With the existence of

the largely higher amount of difference in the required rate of return the investors should

abstain from investing in the shares of the Tas Food Ltd (Dutta and Patatoukas 2016). The

negative amount of data that is reported by the company that the prospect of the investment is

less risky and it is less prone to fluctuations after viewing the rate of market index rate.

Weighted average of cost of capital:

Particulars Amount

Weightag

e Cost

Return

Rate

Tax

Rate WACC

Total Long Term Debt 1011 2.80% 0 0.00% 30.00 0.00%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE

%

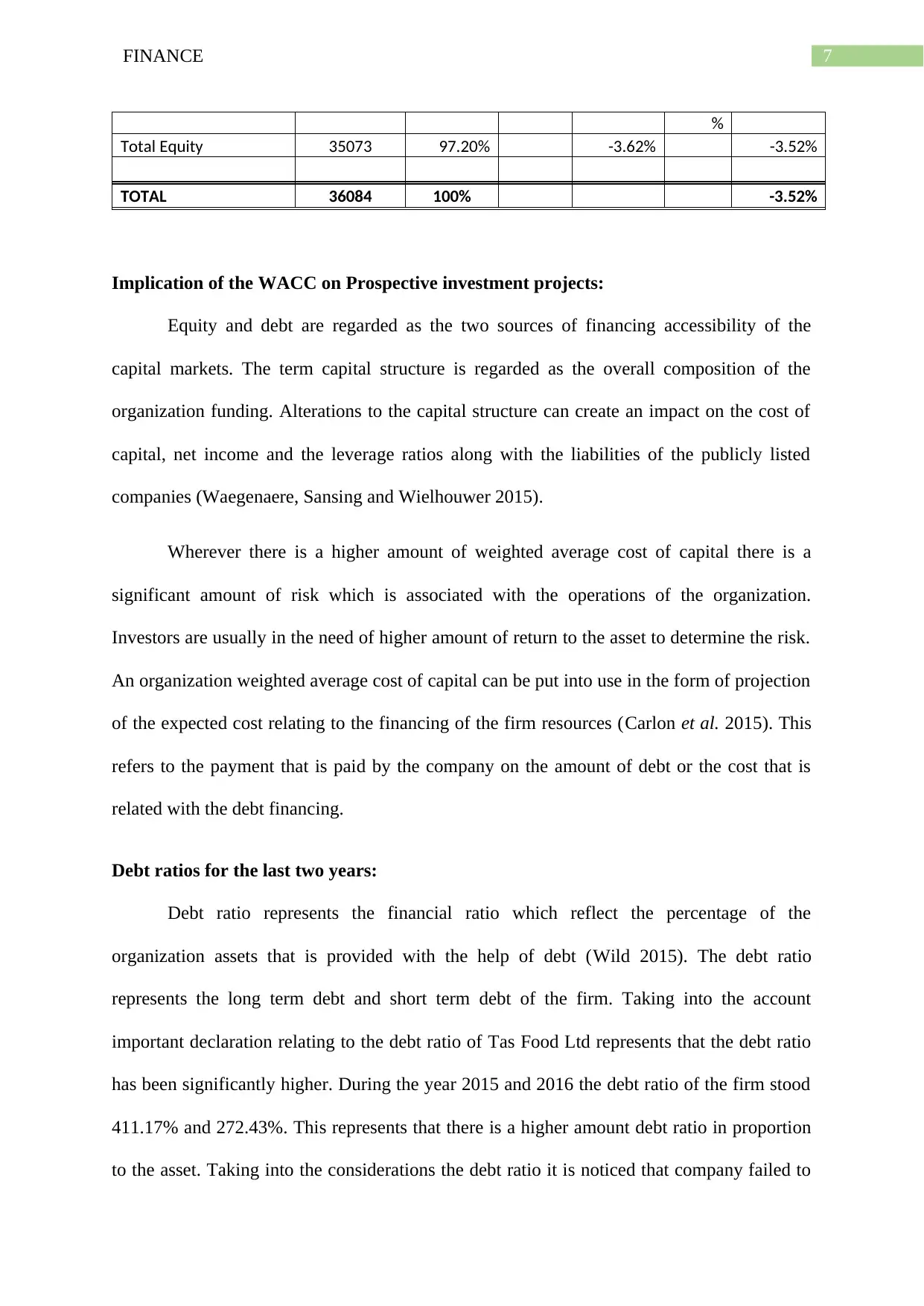

Total Equity 35073 97.20% -3.62% -3.52%

TOTAL 36084 100% -3.52%

Implication of the WACC on Prospective investment projects:

Equity and debt are regarded as the two sources of financing accessibility of the

capital markets. The term capital structure is regarded as the overall composition of the

organization funding. Alterations to the capital structure can create an impact on the cost of

capital, net income and the leverage ratios along with the liabilities of the publicly listed

companies (Waegenaere, Sansing and Wielhouwer 2015).

Wherever there is a higher amount of weighted average cost of capital there is a

significant amount of risk which is associated with the operations of the organization.

Investors are usually in the need of higher amount of return to the asset to determine the risk.

An organization weighted average cost of capital can be put into use in the form of projection

of the expected cost relating to the financing of the firm resources (Carlon et al. 2015). This

refers to the payment that is paid by the company on the amount of debt or the cost that is

related with the debt financing.

Debt ratios for the last two years:

Debt ratio represents the financial ratio which reflect the percentage of the

organization assets that is provided with the help of debt (Wild 2015). The debt ratio

represents the long term debt and short term debt of the firm. Taking into the account

important declaration relating to the debt ratio of Tas Food Ltd represents that the debt ratio

has been significantly higher. During the year 2015 and 2016 the debt ratio of the firm stood

411.17% and 272.43%. This represents that there is a higher amount debt ratio in proportion

to the asset. Taking into the considerations the debt ratio it is noticed that company failed to

%

Total Equity 35073 97.20% -3.62% -3.52%

TOTAL 36084 100% -3.52%

Implication of the WACC on Prospective investment projects:

Equity and debt are regarded as the two sources of financing accessibility of the

capital markets. The term capital structure is regarded as the overall composition of the

organization funding. Alterations to the capital structure can create an impact on the cost of

capital, net income and the leverage ratios along with the liabilities of the publicly listed

companies (Waegenaere, Sansing and Wielhouwer 2015).

Wherever there is a higher amount of weighted average cost of capital there is a

significant amount of risk which is associated with the operations of the organization.

Investors are usually in the need of higher amount of return to the asset to determine the risk.

An organization weighted average cost of capital can be put into use in the form of projection

of the expected cost relating to the financing of the firm resources (Carlon et al. 2015). This

refers to the payment that is paid by the company on the amount of debt or the cost that is

related with the debt financing.

Debt ratios for the last two years:

Debt ratio represents the financial ratio which reflect the percentage of the

organization assets that is provided with the help of debt (Wild 2015). The debt ratio

represents the long term debt and short term debt of the firm. Taking into the account

important declaration relating to the debt ratio of Tas Food Ltd represents that the debt ratio

has been significantly higher. During the year 2015 and 2016 the debt ratio of the firm stood

411.17% and 272.43%. This represents that there is a higher amount debt ratio in proportion

to the asset. Taking into the considerations the debt ratio it is noticed that company failed to

8FINANCE

take any positive initiative of lowering its debt and as a result of this the debt ratio reported

by the firm stood on the higher side (Barberis, et al. 2015).

Gearing ratio:

During the year 2016 in the month of February Tas food ltd issued 22,232,000

ordinary shares at $0.25 per share to the investors. Additionally, taking into the account the

gearing ratio for the Tas food ltd it can be stated that the company during the year 2016

reported a gearing ratio of 11.8%. Based on the gearing ratio of the firm an important

assertion can be stated that large portion of the capital for the firm comprises of the debt and

share capital (Ghosh, Julliard and Taylor 2016). As a result of this there is a higher amount of

debt ratio for the firm.

Dividend policy:

During the financial year of 2016 the company did not report any dividend to its

shareholders.

Letter of recommendation:

Dear ABC,

Queensland

Australia

Respected Sir,

I would like to draw your kind attention towards my recommendations that the

performance of the Tas food limited has been very poor in the financial year of 2016.

Additionally, it has been understood from the analysis that the company has reported a

negative figures of beta this represents that investing in this firm would result the investor

suffer losses. The beta of the company stood -1.27 with negative amount of required rate of

take any positive initiative of lowering its debt and as a result of this the debt ratio reported

by the firm stood on the higher side (Barberis, et al. 2015).

Gearing ratio:

During the year 2016 in the month of February Tas food ltd issued 22,232,000

ordinary shares at $0.25 per share to the investors. Additionally, taking into the account the

gearing ratio for the Tas food ltd it can be stated that the company during the year 2016

reported a gearing ratio of 11.8%. Based on the gearing ratio of the firm an important

assertion can be stated that large portion of the capital for the firm comprises of the debt and

share capital (Ghosh, Julliard and Taylor 2016). As a result of this there is a higher amount of

debt ratio for the firm.

Dividend policy:

During the financial year of 2016 the company did not report any dividend to its

shareholders.

Letter of recommendation:

Dear ABC,

Queensland

Australia

Respected Sir,

I would like to draw your kind attention towards my recommendations that the

performance of the Tas food limited has been very poor in the financial year of 2016.

Additionally, it has been understood from the analysis that the company has reported a

negative figures of beta this represents that investing in this firm would result the investor

suffer losses. The beta of the company stood -1.27 with negative amount of required rate of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE

return standing -3.62. The company reported downturn in the price of share and with highly

risky profile the investors faces the risk of suffering heavy amount of loss. The prices of the

shares have been on the declining trend and this might not yield a higher return for the

investors.

I hope that the above stated analysis and recommendations has been successful in providing

the required information to the investors. It would be wise for the investors for abstaining

from making an investment in the Tas Food Ltd. I hope that the information that is provided

has helped in serving you with the required information relating to the investment decision.

Thanking you,

ABC

Investment Company

return standing -3.62. The company reported downturn in the price of share and with highly

risky profile the investors faces the risk of suffering heavy amount of loss. The prices of the

shares have been on the declining trend and this might not yield a higher return for the

investors.

I hope that the above stated analysis and recommendations has been successful in providing

the required information to the investors. It would be wise for the investors for abstaining

from making an investment in the Tas Food Ltd. I hope that the information that is provided

has helped in serving you with the required information relating to the investment decision.

Thanking you,

ABC

Investment Company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE

Reference List:

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., 2015. X-CAPM: An extrapolative

capital asset pricing model. Journal of financial economics, 115(1), pp.1-24.

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Callen, J.L., 2015. A selective critical review of financial accounting research. Critical

Perspectives on Accounting, 26, pp.157-167.

Campbell, J.Y., Giglio, S., Polk, C. and Turley, R., 2016. Appendix to an intertemporal

CAPM with stochastic volatility.

Carlon, S., McAlpine-Mladenovic, R., Palm, C., Mitrione, L., Kirk, N. and Wong, L.,

2015. Financial Accounting: Reporting, Analysis and Decision Making. John Wiley and Sons

Australia.

Dufour, J.M., 2017. Time series and financial econometrics Multivariate linear linear

regression and CAPM Exercises.

Dutta, S. and Patatoukas, P.N., 2016. Identifying Conditional Conservatism in Financial

Accounting Data: Theory and Evidence. The Accounting Review, 92(4), pp.191-216.

Editorial, R. (2018). Market Indices | Reuters.com. [online] U.S. Available at:

https://www.reuters.com/finance/markets/indices [Accessed 30 Jan. 2018].

Fernandez, P., 2015. CAPM: an absurd model. Business Valuation Review, 34(1), pp.4-23.

Fernandez, P., 2017. CAPM: The Model and 307 Comments About It.

Reference List:

Barberis, N., Greenwood, R., Jin, L. and Shleifer, A., 2015. X-CAPM: An extrapolative

capital asset pricing model. Journal of financial economics, 115(1), pp.1-24.

Beatty, A. and Liao, S., 2014. Financial accounting in the banking industry: A review of the

empirical literature. Journal of Accounting and Economics, 58(2-3), pp.339-383.

Callen, J.L., 2015. A selective critical review of financial accounting research. Critical

Perspectives on Accounting, 26, pp.157-167.

Campbell, J.Y., Giglio, S., Polk, C. and Turley, R., 2016. Appendix to an intertemporal

CAPM with stochastic volatility.

Carlon, S., McAlpine-Mladenovic, R., Palm, C., Mitrione, L., Kirk, N. and Wong, L.,

2015. Financial Accounting: Reporting, Analysis and Decision Making. John Wiley and Sons

Australia.

Dufour, J.M., 2017. Time series and financial econometrics Multivariate linear linear

regression and CAPM Exercises.

Dutta, S. and Patatoukas, P.N., 2016. Identifying Conditional Conservatism in Financial

Accounting Data: Theory and Evidence. The Accounting Review, 92(4), pp.191-216.

Editorial, R. (2018). Market Indices | Reuters.com. [online] U.S. Available at:

https://www.reuters.com/finance/markets/indices [Accessed 30 Jan. 2018].

Fernandez, P., 2015. CAPM: an absurd model. Business Valuation Review, 34(1), pp.4-23.

Fernandez, P., 2017. CAPM: The Model and 307 Comments About It.

11FINANCE

Ghosh, A., Julliard, C. and Taylor, A.P., 2016. What is the consumption-CAPM missing? An

information-theoretic framework for the analysis of asset pricing models. The Review of

Financial Studies, 30(2), pp.442-504.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Mullinova, S., 2016. Use of the principles of IFRS (IAS) 39" Financial instruments:

recognition and assessment" for bank financial accounting. Modern European Researches,

(1), pp.60-64.

Reid, W. and Myddelton, D.R., 2017. The meaning of company accounts. Routledge.

Robson, K., Young, J. and Power, M., 2017. Themed section on financial accounting as

social and organizational practice: exploring the work of financial reporting. Accounting,

Organizations and Society, 56, pp.35-37.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

TasFoods Ltd. (2018). Home. [online] Available at: http://www.tasfoods.com.au/ [Accessed

30 Jan. 2018].

Waegenaere, A., Sansing, R. and Wielhouwer, J.L., 2015. Financial accounting effects of tax

aggressiveness: Contracting and measurement. Contemporary Accounting Research, 32(1),

pp.223-242.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Wild, J., 2015. Financial accounting fundamentals. McGraw-Hill Higher Education.

Ghosh, A., Julliard, C. and Taylor, A.P., 2016. What is the consumption-CAPM missing? An

information-theoretic framework for the analysis of asset pricing models. The Review of

Financial Studies, 30(2), pp.442-504.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Mullinova, S., 2016. Use of the principles of IFRS (IAS) 39" Financial instruments:

recognition and assessment" for bank financial accounting. Modern European Researches,

(1), pp.60-64.

Reid, W. and Myddelton, D.R., 2017. The meaning of company accounts. Routledge.

Robson, K., Young, J. and Power, M., 2017. Themed section on financial accounting as

social and organizational practice: exploring the work of financial reporting. Accounting,

Organizations and Society, 56, pp.35-37.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Scott, W.R., 2015. Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

TasFoods Ltd. (2018). Home. [online] Available at: http://www.tasfoods.com.au/ [Accessed

30 Jan. 2018].

Waegenaere, A., Sansing, R. and Wielhouwer, J.L., 2015. Financial accounting effects of tax

aggressiveness: Contracting and measurement. Contemporary Accounting Research, 32(1),

pp.223-242.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Wild, J., 2015. Financial accounting fundamentals. McGraw-Hill Higher Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

![Strategic Management Analysis of Bellamy's Organic - [University]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fdx%2F9ae26af63ac84162bd7d7d39e54e2da9.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.