Detailed Taxation Report: CGT, FBT, and Business Transactions Analysis

VerifiedAdded on 2023/06/04

|13

|3932

|212

Report

AI Summary

This report provides a detailed analysis of the tax implications, specifically Capital Gains Tax (CGT) and Fringe Benefits Tax (FBT), arising from various business transactions. It examines Amber's sale of a chocolate shop, including the tax treatment of goodwill, equipment, and stock, as well as the implications of a restrictive covenant. The report also covers the CGT implications of selling an inherited inner-city apartment, focusing on the main residence exemption. Furthermore, it addresses the tax implications for both employer (House R Us) and employee (Jamie) concerning salary, commission, car benefits, and low-interest loans, determining assessable income, tax deductions, and FBT liabilities. The analysis is supported by relevant sections of the ITAA 1997 and FBTAA 1986, along with case law and tax rulings.

TAXATION

Student Name

[Pick the date]

Student Name

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

Issue

Taking into consideration, the transaction enacted by Amber, the potential tax implications need

to be highlighted with special reference to CGT (Capital Gains Tax) but not limiting the purview

to only CGT. The key issues pertaining to the transactions that Amber has enacted are mentioned

as follows.

1) The tax implications of the various assets which comprise the shop particularly in relation to

potential CGT liabilities.

2) Another key issue is to highlight if the receipts on account of restrictive covenant would be

revenue or capital in nature.

3) The potential tax implications in relation to the proceeds obtained from liquidation of

apartment in inner city which was inherited after Amber’s uncle died in 2013.

Law

The applicable law in relation to the key assets has been presented below.

Sale of Shop

A key question which arises is whether goodwill would be a capital asset or not. This can be

answered using s.108-5 ITAA 1997 which besides listing other capital assets also highlights

goodwill as a capital asset. This is critical since proceeds from the sale of capital assets are

capital proceeds which are not subject to taxation. Only the capital gains that are derived by the

taxpayer on account of disposal of these assets may be put to tax in the form of CGT. One

exception in this regards is trading stock which as per s. 118-25 ITAA 1997 would not consider

the underlying capital gains (Barkoczy, 2017).

For CGT implications to arise, it is required that as per s. 104-5, capital event has to happen. The

capital event that related to the capital asset disposal is termed as A1 event. Each of the events

listed in s. 104-5 ITAA 1997 tend to also highlight the respective mechanism for computation of

capital gains (Coleman, 2015). For event A1, this involves deduction of the cost base of the asset

1

Issue

Taking into consideration, the transaction enacted by Amber, the potential tax implications need

to be highlighted with special reference to CGT (Capital Gains Tax) but not limiting the purview

to only CGT. The key issues pertaining to the transactions that Amber has enacted are mentioned

as follows.

1) The tax implications of the various assets which comprise the shop particularly in relation to

potential CGT liabilities.

2) Another key issue is to highlight if the receipts on account of restrictive covenant would be

revenue or capital in nature.

3) The potential tax implications in relation to the proceeds obtained from liquidation of

apartment in inner city which was inherited after Amber’s uncle died in 2013.

Law

The applicable law in relation to the key assets has been presented below.

Sale of Shop

A key question which arises is whether goodwill would be a capital asset or not. This can be

answered using s.108-5 ITAA 1997 which besides listing other capital assets also highlights

goodwill as a capital asset. This is critical since proceeds from the sale of capital assets are

capital proceeds which are not subject to taxation. Only the capital gains that are derived by the

taxpayer on account of disposal of these assets may be put to tax in the form of CGT. One

exception in this regards is trading stock which as per s. 118-25 ITAA 1997 would not consider

the underlying capital gains (Barkoczy, 2017).

For CGT implications to arise, it is required that as per s. 104-5, capital event has to happen. The

capital event that related to the capital asset disposal is termed as A1 event. Each of the events

listed in s. 104-5 ITAA 1997 tend to also highlight the respective mechanism for computation of

capital gains (Coleman, 2015). For event A1, this involves deduction of the cost base of the asset

1

under consideration from the proceeds derived from selling the asset. Once this capital gains is

computed, it can be reduced using either the indexation method or discount method whichever

provides a lower taxable value. Rebate to the extent of 50% is available under s. 115-25 ITAA

1997 if the underlying capital gains are long term in nature (Krever, 2017). The indexation

method relies on reducing capital gains by increasing the cost base by multiplying it by the

inflation index adjustment factor. The more common of the two methods is discount method

which is particularly useful when the capital gains are quite high.

Restrictive Covenant

The most important issue that needs to be answered in context of restrictive covenant is to decide

the nature of the proceeds. This is critical as no tax is levied on the capital receipts but the same

is not true for revenue receipts. Revenue receipts would be reflected in the assessable income of

the taxpayer. In case of proceeds being capital, potential impact would be in form of CGT on any

capital gains that are derived. To highlight the nature of proceeds, a case that merits discussion is

Reuter v. FC of T 93 ATC 4037; (1993) 24 ATR 527 (Reuters, 2017). In this case, compensation

was given to the party which allowed not exercising the right to sue. It was highlighted during

the case discussion that putting restrictions on available legal rights for proceeds would result in

proceeds being capital. This is because the right is essentially a legal asset which can potentially

bring future inflows for the individual. The concept in the above case can also be replicated for

restrictive covenant. This is because the business seller has the right to establish business without

any restrictions in terms of time and geography and this new business can provide future profits.

Hence, by restrictions on setting up business, right is being curtailed resulting in capital proceeds

for the taxpayer. The above treatment also is supported by TR 95/35 which also terms these

proceeds as capital (Nethercott, Richardson & Devos, 2016).

Inner City apartment-

CGT exemption is available for any asset which has been acquired by the taxpayer in the pre-

CGT era i.e. when there was no capital gains tax. This period corresponds to the time before the

threshold date of September 20, 1985. This is as per s.149-10 ITAA. Also, it is essential to note

that death does not result in capital gains or tax computed on the asset since it is not a capital

event in accordance with s. 104-5 ITAA 1997 (Wilmot, 2016). However, the CGT implications

2

computed, it can be reduced using either the indexation method or discount method whichever

provides a lower taxable value. Rebate to the extent of 50% is available under s. 115-25 ITAA

1997 if the underlying capital gains are long term in nature (Krever, 2017). The indexation

method relies on reducing capital gains by increasing the cost base by multiplying it by the

inflation index adjustment factor. The more common of the two methods is discount method

which is particularly useful when the capital gains are quite high.

Restrictive Covenant

The most important issue that needs to be answered in context of restrictive covenant is to decide

the nature of the proceeds. This is critical as no tax is levied on the capital receipts but the same

is not true for revenue receipts. Revenue receipts would be reflected in the assessable income of

the taxpayer. In case of proceeds being capital, potential impact would be in form of CGT on any

capital gains that are derived. To highlight the nature of proceeds, a case that merits discussion is

Reuter v. FC of T 93 ATC 4037; (1993) 24 ATR 527 (Reuters, 2017). In this case, compensation

was given to the party which allowed not exercising the right to sue. It was highlighted during

the case discussion that putting restrictions on available legal rights for proceeds would result in

proceeds being capital. This is because the right is essentially a legal asset which can potentially

bring future inflows for the individual. The concept in the above case can also be replicated for

restrictive covenant. This is because the business seller has the right to establish business without

any restrictions in terms of time and geography and this new business can provide future profits.

Hence, by restrictions on setting up business, right is being curtailed resulting in capital proceeds

for the taxpayer. The above treatment also is supported by TR 95/35 which also terms these

proceeds as capital (Nethercott, Richardson & Devos, 2016).

Inner City apartment-

CGT exemption is available for any asset which has been acquired by the taxpayer in the pre-

CGT era i.e. when there was no capital gains tax. This period corresponds to the time before the

threshold date of September 20, 1985. This is as per s.149-10 ITAA. Also, it is essential to note

that death does not result in capital gains or tax computed on the asset since it is not a capital

event in accordance with s. 104-5 ITAA 1997 (Wilmot, 2016). However, the CGT implications

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

would arise for the legal heir who would dispose the asset which would lead to an A1 event. It is

noticeable that the cost base of asset for the legal heir is the asset’s market value when the asset

is transferred in the name of legal heir. Additionally, in capital asset sale especially involving

property owing to larger denomination involved, there tends to be a time lag between signing of

the sale contract and settlement of the same. This time difference can result in the two events

being present in different tax years and thereby posing a dilemma for the taxpayer (Sadiq, et. al.,

2015). TR 94/29 provides help in this regards, since it states that CGT related liability ought to

be levied on the taxpayer in the same year when the property sale is concluded in terms of

agreement and does not depend on the actual cash being received. Besides, in case f residential

properties, a particular CGT exemption worth discussing is the main residence exemption

(Wilmot, 2016). This exemption arises when the taxpayer has used the property as permanent

residence and not for income generation. This is in accordance with subdivision 118-B ITAA

1997. Further, partial exemption under main residence clause can also be availed depending on

the income derived, years of main residence and other factors (Nethercott, Richardson & Devos,

2016).

Application

Sale of shop

The shop comprises of various assets which are capital assets and therefore the underlying

proceeds derived would be capital and hence non-taxable. Therefore, the potential tax

implications would arise owing to any capital gains that are realised on sale of shop. The shop in

the given case is an asset which is comprised of several assets and hence the treatment of these

individual assets needs to be considered.

A pertinent asset is goodwill whose disposal would lead to enactment of A1 event and the

resultant capital gains computation. The respective cost price and sale proceeds related to

goodwill have been offered in the question which can be used for finding the capital gains.

Besides, discount method would be applicable to reduce the capital gains which are subject to

CGT as these are long term capital gains.

With regards to the equipment, the underlying capital gains computation would consider the

sales proceeds and the asset book value. This would be considered since depreciation has been

3

noticeable that the cost base of asset for the legal heir is the asset’s market value when the asset

is transferred in the name of legal heir. Additionally, in capital asset sale especially involving

property owing to larger denomination involved, there tends to be a time lag between signing of

the sale contract and settlement of the same. This time difference can result in the two events

being present in different tax years and thereby posing a dilemma for the taxpayer (Sadiq, et. al.,

2015). TR 94/29 provides help in this regards, since it states that CGT related liability ought to

be levied on the taxpayer in the same year when the property sale is concluded in terms of

agreement and does not depend on the actual cash being received. Besides, in case f residential

properties, a particular CGT exemption worth discussing is the main residence exemption

(Wilmot, 2016). This exemption arises when the taxpayer has used the property as permanent

residence and not for income generation. This is in accordance with subdivision 118-B ITAA

1997. Further, partial exemption under main residence clause can also be availed depending on

the income derived, years of main residence and other factors (Nethercott, Richardson & Devos,

2016).

Application

Sale of shop

The shop comprises of various assets which are capital assets and therefore the underlying

proceeds derived would be capital and hence non-taxable. Therefore, the potential tax

implications would arise owing to any capital gains that are realised on sale of shop. The shop in

the given case is an asset which is comprised of several assets and hence the treatment of these

individual assets needs to be considered.

A pertinent asset is goodwill whose disposal would lead to enactment of A1 event and the

resultant capital gains computation. The respective cost price and sale proceeds related to

goodwill have been offered in the question which can be used for finding the capital gains.

Besides, discount method would be applicable to reduce the capital gains which are subject to

CGT as these are long term capital gains.

With regards to the equipment, the underlying capital gains computation would consider the

sales proceeds and the asset book value. This would be considered since depreciation has been

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

charged by the company with regards to equipment thereby reducing the book value. Hence,

capital gains would arise only if the sale value would exceed the book value. However, in

relation with the stock available, no CGT implications would arise since any capital gains or

losses on this asset are not considered for application of CGT.

Restrictive Covenant

It is apparent that restrictions have been put on Amber with regards to geography and time for

which business cannot be opened. This clearly impairs her earning capability and imposes

constraints on the same thus causing loss of potential cash inflows in the future. As a result, the

underlying proceeds that have been derived from this contract enactment would be considered as

proceeds of capital nature and would not be subject to any taxation. However, it is possible that

capital gains can result from restrictive covenant on which CGT could be applied.

Inner City apartment-

The given apartment has not been purchased by Amber but infact is a deceased estate which has

been inherited owing to death of uncle. Amber’s uncle had used the apartment as main residence

from the time of purchase in 1992 till the time of death in 2013. This apartment since the time of

inheritance has been used by Amber as her permanent residence. This can be concluded since no

income producing activity has been related to the apartment and also the taxpayer has used it for

staying during the period of ownership. As a result, the main residence exemption which Sub

Division 118-B provides would apply in this case and full exemption on CGT related liability

would be available. Since apartment is a capital asset, hence the proceeds from sale would be

capital and therefore non-taxable. The other issues are not significant in the case of this

apartment as it is a CGT exempt property.

Conclusion\

On the basis of the discussion carried out in the previous section, it has been found that Amber

would have to pay CGT on any capital gains realised from the sale of equipment and goodwill.

However, the treatment extended to stock would be different where no CGT would be applied

irrespective of gains or losses. In case of restrictive covenant, the proceeds would be capital and

hence non –taxable. But these may be subject to CGT if there are some capital gains realised.

4

capital gains would arise only if the sale value would exceed the book value. However, in

relation with the stock available, no CGT implications would arise since any capital gains or

losses on this asset are not considered for application of CGT.

Restrictive Covenant

It is apparent that restrictions have been put on Amber with regards to geography and time for

which business cannot be opened. This clearly impairs her earning capability and imposes

constraints on the same thus causing loss of potential cash inflows in the future. As a result, the

underlying proceeds that have been derived from this contract enactment would be considered as

proceeds of capital nature and would not be subject to any taxation. However, it is possible that

capital gains can result from restrictive covenant on which CGT could be applied.

Inner City apartment-

The given apartment has not been purchased by Amber but infact is a deceased estate which has

been inherited owing to death of uncle. Amber’s uncle had used the apartment as main residence

from the time of purchase in 1992 till the time of death in 2013. This apartment since the time of

inheritance has been used by Amber as her permanent residence. This can be concluded since no

income producing activity has been related to the apartment and also the taxpayer has used it for

staying during the period of ownership. As a result, the main residence exemption which Sub

Division 118-B provides would apply in this case and full exemption on CGT related liability

would be available. Since apartment is a capital asset, hence the proceeds from sale would be

capital and therefore non-taxable. The other issues are not significant in the case of this

apartment as it is a CGT exempt property.

Conclusion\

On the basis of the discussion carried out in the previous section, it has been found that Amber

would have to pay CGT on any capital gains realised from the sale of equipment and goodwill.

However, the treatment extended to stock would be different where no CGT would be applied

irrespective of gains or losses. In case of restrictive covenant, the proceeds would be capital and

hence non –taxable. But these may be subject to CGT if there are some capital gains realised.

4

The sale of deceased estate would not result in any tax liability for Amber as the proceeds from

sale are capital in nature while in accordance to main residence exemption, no CGT would apply

to any possible capital gains or losses.

Question 2

Issue

The issue is to determine tax implications for employer House R Us and employee Jamie for

various transactions incurred during the tax year. The main aspects in relation to the transactions

are given below.

1) Whether amount provided by House R Us to its employee Jamie will be considered as

assessable income for him as per s.6-5 or s.6-10, ITAA 1997.

2) Whether Jamie would get tax deductions on interest payments.

3) Whether tax deduction will be available on the account of payment made by House R Us as

per s. 8-1

4) Computation of Fringe Benefit Tax (FBT) levied on Jamie and House R Us on the account of

extended benefits in the form of car and low interest rate loan.

Law & Application

Salary and Commission

In accordance of s. 6-5, ITAA 1997 income received by employee from ordinary sources such as

personal exertion (salary, commission) would be termed as assessable income from ordinary

sources. This assessable income would be taken for tax treatment and personal tax would be

levied on the taxpayer. Further, any cash outflow of revenue nature would be categorised for tax

deductions only if it has been incurred in regards to derive assessable income under s. 8-1 ITAA

1997. Further, capital expenses that are used to derive assessable income would not be

considered for any tax deduction under ss. 8-1(2) ITAA 1997 (Barkoczy, 2017).

5

sale are capital in nature while in accordance to main residence exemption, no CGT would apply

to any possible capital gains or losses.

Question 2

Issue

The issue is to determine tax implications for employer House R Us and employee Jamie for

various transactions incurred during the tax year. The main aspects in relation to the transactions

are given below.

1) Whether amount provided by House R Us to its employee Jamie will be considered as

assessable income for him as per s.6-5 or s.6-10, ITAA 1997.

2) Whether Jamie would get tax deductions on interest payments.

3) Whether tax deduction will be available on the account of payment made by House R Us as

per s. 8-1

4) Computation of Fringe Benefit Tax (FBT) levied on Jamie and House R Us on the account of

extended benefits in the form of car and low interest rate loan.

Law & Application

Salary and Commission

In accordance of s. 6-5, ITAA 1997 income received by employee from ordinary sources such as

personal exertion (salary, commission) would be termed as assessable income from ordinary

sources. This assessable income would be taken for tax treatment and personal tax would be

levied on the taxpayer. Further, any cash outflow of revenue nature would be categorised for tax

deductions only if it has been incurred in regards to derive assessable income under s. 8-1 ITAA

1997. Further, capital expenses that are used to derive assessable income would not be

considered for any tax deduction under ss. 8-1(2) ITAA 1997 (Barkoczy, 2017).

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Employee (Jamie): He has received a monthly salary along with 10% commission on the sales as

per his employment contract with House R Us. Therefore, the amount contributes to the

assessable income of Jamie from ordinary sources as per s. 6 (5) ITAA 1997.

Employer (House R Us): They have given salary and commission amount to employee that

contributes to the generation of assessable income and therefore, the expenses would be revenue

expenditure and would be considered for tax deductions under s. 8-1 ITAA 1997.

Car benefit

According to Division 2, Part III Fringe Benefit Tax Assessment Act 1986, when an employer

makes a car available to employee for personal use, then it will be termed as car fringe benefits.

Further, the employee does not need to pay any FBT tax on the received benefits and hence,

would not be liable for FBT liabilities. Also, the employer who has provided car to employee

would be held accountable for FBT liabilities under s. 9 FBTAA 1986 (Coleman, 2015).

Employee (Jamie): He has received a Toyota Kluger car from House R Us that he can use for

personal work along with the office work and hence, it can be concluded that House R Us has

extended a car fringe benefit to Jamie. Further, no FBT liability will be imposed on Jamie for car

fringe benefit.

Employer (House R Us): They have provided car fringe benefit to Jamie and thus, FBT liability

will be imposed on House R Us. Three steps would be used to find the FBT liability for car

fringe benefit.

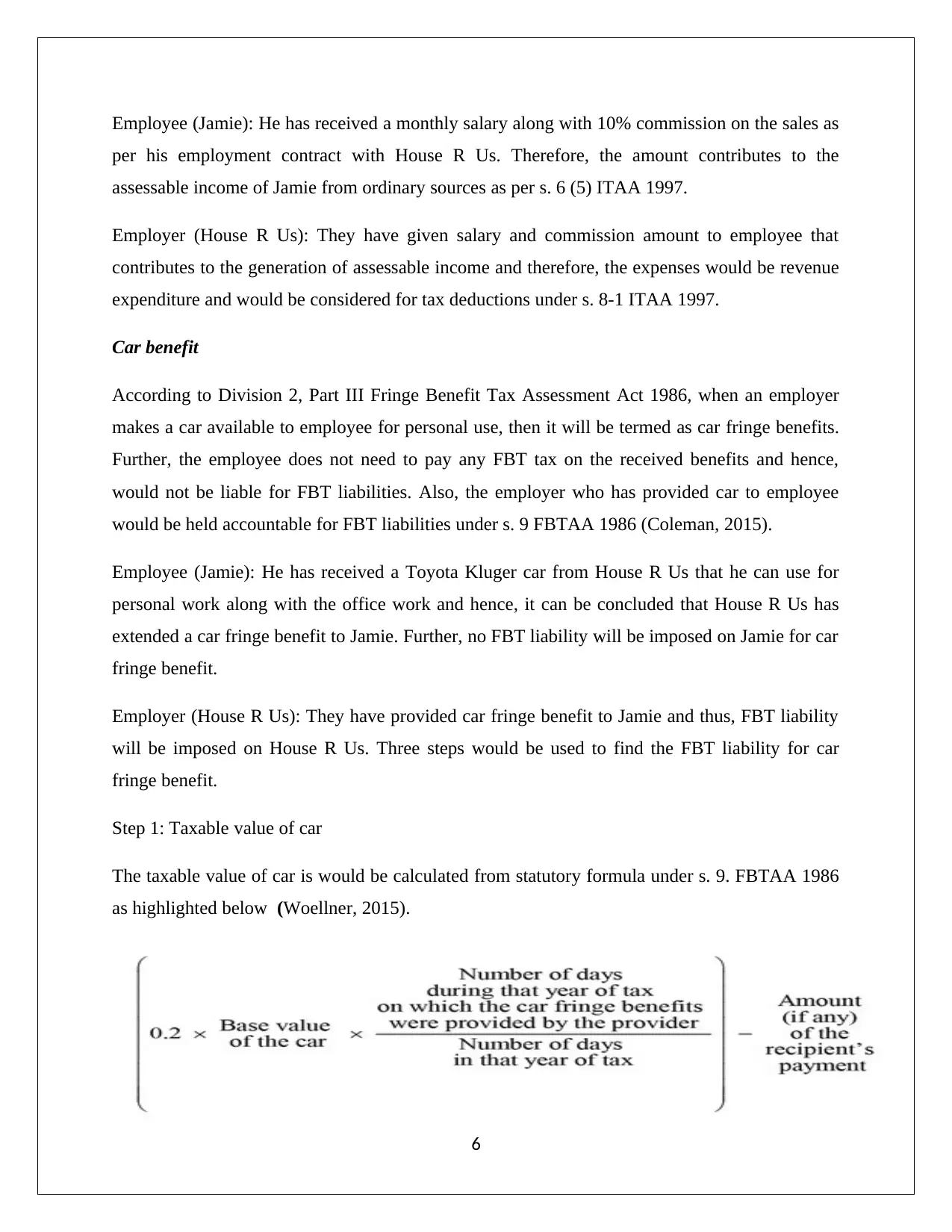

Step 1: Taxable value of car

The taxable value of car is would be calculated from statutory formula under s. 9. FBTAA 1986

as highlighted below (Woellner, 2015).

6

per his employment contract with House R Us. Therefore, the amount contributes to the

assessable income of Jamie from ordinary sources as per s. 6 (5) ITAA 1997.

Employer (House R Us): They have given salary and commission amount to employee that

contributes to the generation of assessable income and therefore, the expenses would be revenue

expenditure and would be considered for tax deductions under s. 8-1 ITAA 1997.

Car benefit

According to Division 2, Part III Fringe Benefit Tax Assessment Act 1986, when an employer

makes a car available to employee for personal use, then it will be termed as car fringe benefits.

Further, the employee does not need to pay any FBT tax on the received benefits and hence,

would not be liable for FBT liabilities. Also, the employer who has provided car to employee

would be held accountable for FBT liabilities under s. 9 FBTAA 1986 (Coleman, 2015).

Employee (Jamie): He has received a Toyota Kluger car from House R Us that he can use for

personal work along with the office work and hence, it can be concluded that House R Us has

extended a car fringe benefit to Jamie. Further, no FBT liability will be imposed on Jamie for car

fringe benefit.

Employer (House R Us): They have provided car fringe benefit to Jamie and thus, FBT liability

will be imposed on House R Us. Three steps would be used to find the FBT liability for car

fringe benefit.

Step 1: Taxable value of car

The taxable value of car is would be calculated from statutory formula under s. 9. FBTAA 1986

as highlighted below (Woellner, 2015).

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Step 2: Grossed up value of car

Grossed up value=Taxable value of car∗Grossup rate

Gross up rate depends on the type of goods under GST Act 1999.

Step 3: FBT liability for car fringe benefit

FBT liability=FBT rate∗Grossed up value

FBT rate would be 47% for TD 2017/3 and would change as per the respective FBT year.

House R US will also claim for the deductions on the account of given car fringe benefits and

extent of car used for personal purpose or business purpose under s. 8-1, FBTAA 1986.

Laptop & Mobile

Any electronic portable items such as laptop, mobile and so forth provided by employer to their

employees for office work purpose during the employment period will be exempted from FBT

implications under FBTAA 1986 (Hodgson, Mortimer & Butler, 2016).

Employee (Jamie): Jamie is using mobile phone and laptop only for office work and not for

personal work and hence, no fringe benefit has been extended to Jamie from employer. No FBT

liability will be raised on Jamie.

Employer (House R Us): House R Us has provided mobile phone and laptop to Jamie only for

office work and hence, no FBT liability will be raised on House R Us. Further, the expenditure

incurred in buying these devices will be capital expenses and therefore, s. 8-1 will not be applied

here and no deduction will be availed under this section. Further, the deduction can be claimed

by House R Us for the decline in value of the depreciating devices.

Annual Professional Subscription

7

Grossed up value=Taxable value of car∗Grossup rate

Gross up rate depends on the type of goods under GST Act 1999.

Step 3: FBT liability for car fringe benefit

FBT liability=FBT rate∗Grossed up value

FBT rate would be 47% for TD 2017/3 and would change as per the respective FBT year.

House R US will also claim for the deductions on the account of given car fringe benefits and

extent of car used for personal purpose or business purpose under s. 8-1, FBTAA 1986.

Laptop & Mobile

Any electronic portable items such as laptop, mobile and so forth provided by employer to their

employees for office work purpose during the employment period will be exempted from FBT

implications under FBTAA 1986 (Hodgson, Mortimer & Butler, 2016).

Employee (Jamie): Jamie is using mobile phone and laptop only for office work and not for

personal work and hence, no fringe benefit has been extended to Jamie from employer. No FBT

liability will be raised on Jamie.

Employer (House R Us): House R Us has provided mobile phone and laptop to Jamie only for

office work and hence, no FBT liability will be raised on House R Us. Further, the expenditure

incurred in buying these devices will be capital expenses and therefore, s. 8-1 will not be applied

here and no deduction will be availed under this section. Further, the deduction can be claimed

by House R Us for the decline in value of the depreciating devices.

Annual Professional Subscription

7

Employee must derive significant economic profit to derive assessable income under TR 92/15.

Tax deduction will be applicable on the expenditure incurred in subscription fees under s. 8-1,

ITAA 1997 for employer owing to nexus with assessable income production (Coleman, 2015).

Employee (Jamie): Jamie is not getting any monetary benefit due to the subscription of

professional magazine. This is because the amount actually paid has been reimbursed hence, no

tax liability will be raised on Jamie.

Employer (House R Us): Annual professional subscription of magazine is an expense for House

R Us which contributes to the assessable income generations. Hence, tax deduction will be

applicable for House R Us under s. 8-1, ITAA 1997.

Entertainment Allowance

This entertainment allowance is a type of expense that would be provided to the employees on

the part of employer irrespective of the scenario the concerned employees are using the

allowance for entertainment or not as per TR 92/15 (Wilmot, 2016).

Employee (Jamie): The entertainment allowance provided to employee is $2000 p.a. This

amount would be the part of the assessable income of Jamie as he will get this allowance per

years irrespective of the scenario that whether he is using it for entertainment or not. Therefore,

the economic benefit is derived and hence this allowance would be taken for tax implication for

Jamie.

Employer (House R Us): Providing entertainment allowance to employees is a type of revenue

expense and also, is contributes to the assessable income of employees and therefore, the

deduction can be requested by House R Us as per s. 8-1, ITAA 1997.

Home Entertainment System

Statutory income is a part of assessable income under s.6-10, ITAA 1997. The non-cash benefits

will be termed as statutory income only when they are directly connected with the income

8

Tax deduction will be applicable on the expenditure incurred in subscription fees under s. 8-1,

ITAA 1997 for employer owing to nexus with assessable income production (Coleman, 2015).

Employee (Jamie): Jamie is not getting any monetary benefit due to the subscription of

professional magazine. This is because the amount actually paid has been reimbursed hence, no

tax liability will be raised on Jamie.

Employer (House R Us): Annual professional subscription of magazine is an expense for House

R Us which contributes to the assessable income generations. Hence, tax deduction will be

applicable for House R Us under s. 8-1, ITAA 1997.

Entertainment Allowance

This entertainment allowance is a type of expense that would be provided to the employees on

the part of employer irrespective of the scenario the concerned employees are using the

allowance for entertainment or not as per TR 92/15 (Wilmot, 2016).

Employee (Jamie): The entertainment allowance provided to employee is $2000 p.a. This

amount would be the part of the assessable income of Jamie as he will get this allowance per

years irrespective of the scenario that whether he is using it for entertainment or not. Therefore,

the economic benefit is derived and hence this allowance would be taken for tax implication for

Jamie.

Employer (House R Us): Providing entertainment allowance to employees is a type of revenue

expense and also, is contributes to the assessable income of employees and therefore, the

deduction can be requested by House R Us as per s. 8-1, ITAA 1997.

Home Entertainment System

Statutory income is a part of assessable income under s.6-10, ITAA 1997. The non-cash benefits

will be termed as statutory income only when they are directly connected with the income

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

generation of the taxpayer. According to s. 21 A, ITAA 1997 these non-cash benefit will not be

cash convertible but it has been presumed that they can be converted to cash and thus, will

contribute to assessable income of taxpayer in the form of statutory income (Woellner, 2015).

Employee (Jamie): Jamie has received home entertainment system from House R Us as a part of

his professional work as he has recorded sales among the other employees. Therefore, it would

be assumed to be cash –convertible and hence, would be assessable income in terms of statutory

income.

Employer (House R Us): House R Us has provided home entertainment system to Jamie and

thus, expenses occurred while purchasing home entertainment system would be considered for

tax deductions as per s. 8-1, ITAA 1997 as it contributes in the assessable income of employer.

Loan to employee

Employer issues loan to employees in regards to extend financial help. Any loan which is issued

to employee at concessional rates inferior than the rates decided by the Reserve Bank of

Australia (RBA) would result in loan fringe benefit. There are numerous factors associated with

the calculation of loan FBT implications for employer. Further, no liability would be raised on

employee in scenario of loan fringe benefit. Further, tax deduction would be claimed by

employer taxpayer only if the loan payment given to employee would be used for assessable

income production (Hodgson, Mortimer & Butler, 2016).

Employee (Jamie): Jamie has received a loan of $100,000 with a rate of interest 4% per annum

from House R Us. Further, the rate of interest decided by RBA is 5.25% as per TD 2017/3. It can

be shown that House R Us has used inferior interest rate (4.0% << 5.25%) and therefore, it can

be said that House R Us is issuing loan fringe benefits to Jamie. Hence, there will be no FBT

implication that will be levied on Jamie for loan fringe benefit.

Employer (House R Us): As highlighted above, House R Us has chosen inferior interest rate as

compared with the rate decided by RBA for the FY2017/18 and hence, the loan fringe benefit is

offered to Jamie. Therefore, House R Us would have to bear the FBT liability raised due to the

loan fringe benefits to Jamie. Further, the interest payment paid to House R Us will be

considered for tax deduction by Jamie only if the house purchased from loan will derive

9

cash convertible but it has been presumed that they can be converted to cash and thus, will

contribute to assessable income of taxpayer in the form of statutory income (Woellner, 2015).

Employee (Jamie): Jamie has received home entertainment system from House R Us as a part of

his professional work as he has recorded sales among the other employees. Therefore, it would

be assumed to be cash –convertible and hence, would be assessable income in terms of statutory

income.

Employer (House R Us): House R Us has provided home entertainment system to Jamie and

thus, expenses occurred while purchasing home entertainment system would be considered for

tax deductions as per s. 8-1, ITAA 1997 as it contributes in the assessable income of employer.

Loan to employee

Employer issues loan to employees in regards to extend financial help. Any loan which is issued

to employee at concessional rates inferior than the rates decided by the Reserve Bank of

Australia (RBA) would result in loan fringe benefit. There are numerous factors associated with

the calculation of loan FBT implications for employer. Further, no liability would be raised on

employee in scenario of loan fringe benefit. Further, tax deduction would be claimed by

employer taxpayer only if the loan payment given to employee would be used for assessable

income production (Hodgson, Mortimer & Butler, 2016).

Employee (Jamie): Jamie has received a loan of $100,000 with a rate of interest 4% per annum

from House R Us. Further, the rate of interest decided by RBA is 5.25% as per TD 2017/3. It can

be shown that House R Us has used inferior interest rate (4.0% << 5.25%) and therefore, it can

be said that House R Us is issuing loan fringe benefits to Jamie. Hence, there will be no FBT

implication that will be levied on Jamie for loan fringe benefit.

Employer (House R Us): As highlighted above, House R Us has chosen inferior interest rate as

compared with the rate decided by RBA for the FY2017/18 and hence, the loan fringe benefit is

offered to Jamie. Therefore, House R Us would have to bear the FBT liability raised due to the

loan fringe benefits to Jamie. Further, the interest payment paid to House R Us will be

considered for tax deduction by Jamie only if the house purchased from loan will derive

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

assessable income in terms of rent amount. Further, it has been pre-assumed that Jamie is not

renting the home and uses it for her own dwelling and therefore, the deduction would not be

present for House R Us on the account of received interest amount as per s. 8-1, ITAA 1997

(Woellner, 2015) .

Conclusion

The following conclusions would be made based on the above analysis.

Base salary and

commission

Assessable income of Jamie as

per s. 6-5, ITAA 1997

Deduction will be available for House

R Us as per s. 8-1, ITAA1997

Car benefit Car fringe benefits,

No FBT liability on Jamie

FB liability on House R Us and

deduction will be available for House

R Us as per s. 8-1, ITAA1997

Mobile phone and

laptop

FBT will not be applied as

devices are used for office

(professional) work only

Deduction will be available on the

depreciation on the assets

Annual subscription

reimbursement

No tax liability on Jamie Deduction will be available for House

R Us as per s. 8-1, ITAA1997

Entertainment

allowance

Assessable income of Jamie as

per s. 6-5, ITAA 1997

Deduction will be available for House

R Us as per s. 8-1, ITAA1997

Home entertainment

system

Assessable income of Jamie as

per s. 6-5, ITAA 1997

Deduction will be available for House

R Us as per s. 8-1, ITAA1997

Loan fringe benefits No FBT liability on Jamie FBT liability on House R Us

No deduction will be available as

Jamie is using home for self-dwelling

not deriving assessable income.

10

renting the home and uses it for her own dwelling and therefore, the deduction would not be

present for House R Us on the account of received interest amount as per s. 8-1, ITAA 1997

(Woellner, 2015) .

Conclusion

The following conclusions would be made based on the above analysis.

Base salary and

commission

Assessable income of Jamie as

per s. 6-5, ITAA 1997

Deduction will be available for House

R Us as per s. 8-1, ITAA1997

Car benefit Car fringe benefits,

No FBT liability on Jamie

FB liability on House R Us and

deduction will be available for House

R Us as per s. 8-1, ITAA1997

Mobile phone and

laptop

FBT will not be applied as

devices are used for office

(professional) work only

Deduction will be available on the

depreciation on the assets

Annual subscription

reimbursement

No tax liability on Jamie Deduction will be available for House

R Us as per s. 8-1, ITAA1997

Entertainment

allowance

Assessable income of Jamie as

per s. 6-5, ITAA 1997

Deduction will be available for House

R Us as per s. 8-1, ITAA1997

Home entertainment

system

Assessable income of Jamie as

per s. 6-5, ITAA 1997

Deduction will be available for House

R Us as per s. 8-1, ITAA1997

Loan fringe benefits No FBT liability on Jamie FBT liability on House R Us

No deduction will be available as

Jamie is using home for self-dwelling

not deriving assessable income.

10

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.