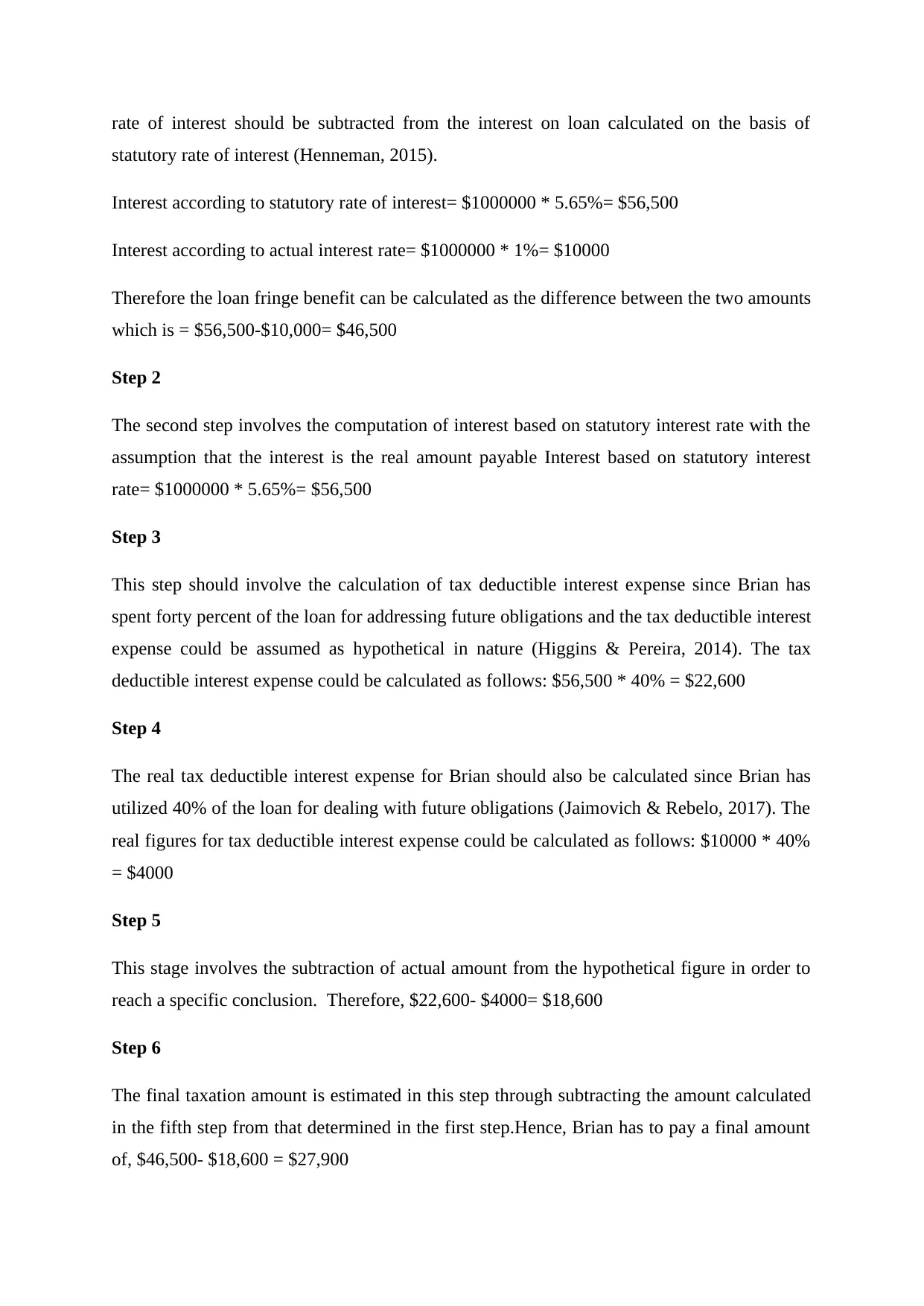

TAXATION: Analysis of Capital Gains, Fringe Benefits, and Tax Law

VerifiedAdded on 2020/03/28

|9

|3009

|41

Homework Assignment

AI Summary

This TAXATION assignment solution analyzes five different scenarios related to tax implications. The first scenario calculates annual net capital profit or loss, considering the acquisition and disposal of various assets, including personal use assets and collectibles, and determining tax liabilities. The second scenario focuses on fringe benefits, specifically a low-interest loan provided by an employer, calculating the loan fringe benefit and the tax implications. The third scenario examines property rental income between a husband and wife, detailing the allocation of profits and losses and the associated tax responsibilities. The fourth scenario discusses the legal principle from the case of IRC v Duke of Westminster, emphasizing an individual's right to minimize their tax liability through legal means. The fifth and final scenario assesses the tax implications for an individual who sells timber from their land, determining whether the income is considered a revenue receipt or capital gain. This assignment provides detailed calculations and considerations for each scenario, making it a valuable resource for students studying taxation.

TAXATION

<Student ID>

<Student Name>

<University Name>

<Student ID>

<Student Name>

<University Name>

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

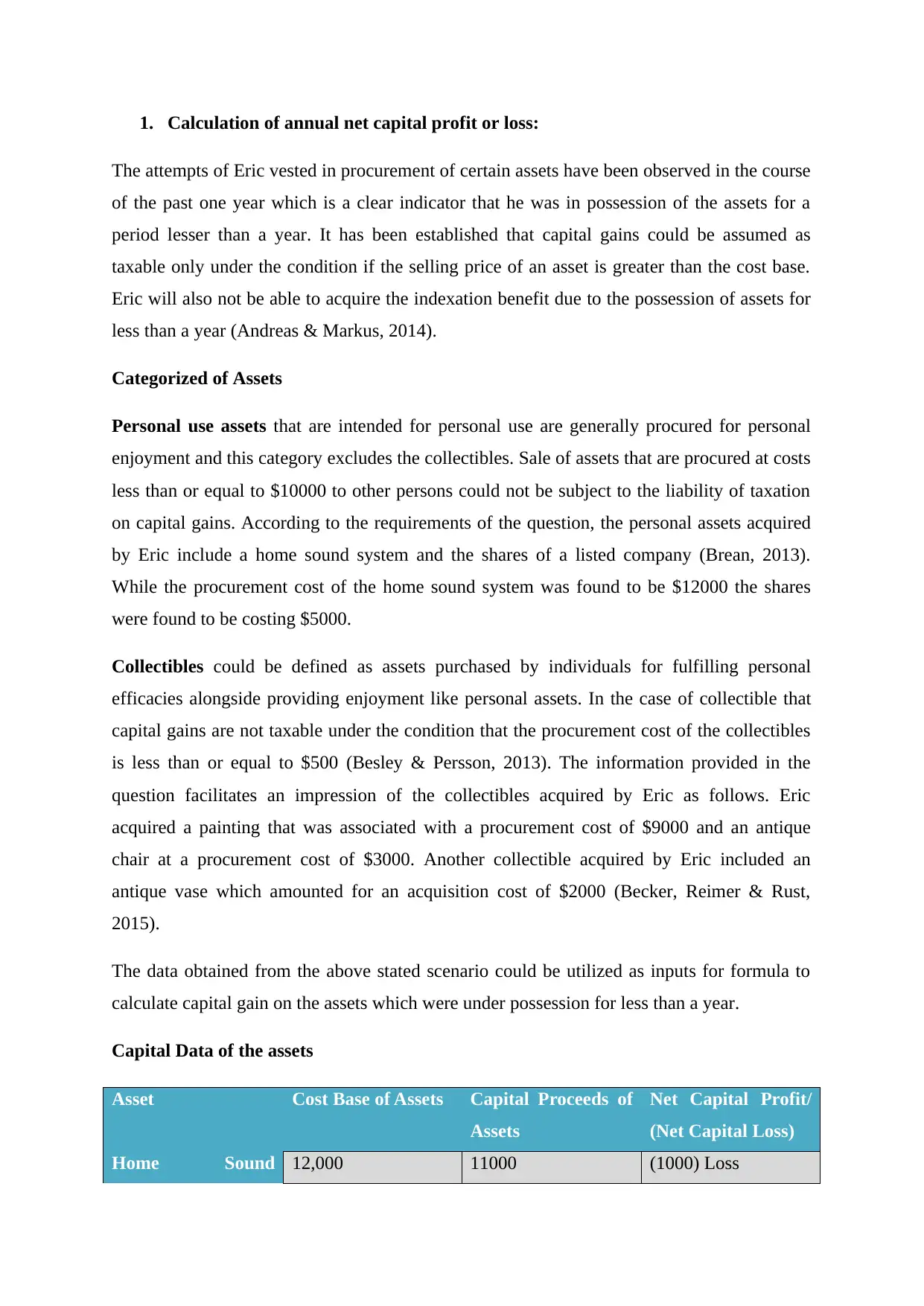

1. Calculation of annual net capital profit or loss:

The attempts of Eric vested in procurement of certain assets have been observed in the course

of the past one year which is a clear indicator that he was in possession of the assets for a

period lesser than a year. It has been established that capital gains could be assumed as

taxable only under the condition if the selling price of an asset is greater than the cost base.

Eric will also not be able to acquire the indexation benefit due to the possession of assets for

less than a year (Andreas & Markus, 2014).

Categorized of Assets

Personal use assets that are intended for personal use are generally procured for personal

enjoyment and this category excludes the collectibles. Sale of assets that are procured at costs

less than or equal to $10000 to other persons could not be subject to the liability of taxation

on capital gains. According to the requirements of the question, the personal assets acquired

by Eric include a home sound system and the shares of a listed company (Brean, 2013).

While the procurement cost of the home sound system was found to be $12000 the shares

were found to be costing $5000.

Collectibles could be defined as assets purchased by individuals for fulfilling personal

efficacies alongside providing enjoyment like personal assets. In the case of collectible that

capital gains are not taxable under the condition that the procurement cost of the collectibles

is less than or equal to $500 (Besley & Persson, 2013). The information provided in the

question facilitates an impression of the collectibles acquired by Eric as follows. Eric

acquired a painting that was associated with a procurement cost of $9000 and an antique

chair at a procurement cost of $3000. Another collectible acquired by Eric included an

antique vase which amounted for an acquisition cost of $2000 (Becker, Reimer & Rust,

2015).

The data obtained from the above stated scenario could be utilized as inputs for formula to

calculate capital gain on the assets which were under possession for less than a year.

Capital Data of the assets

Asset Cost Base of Assets Capital Proceeds of

Assets

Net Capital Profit/

(Net Capital Loss)

Home Sound 12,000 11000 (1000) Loss

The attempts of Eric vested in procurement of certain assets have been observed in the course

of the past one year which is a clear indicator that he was in possession of the assets for a

period lesser than a year. It has been established that capital gains could be assumed as

taxable only under the condition if the selling price of an asset is greater than the cost base.

Eric will also not be able to acquire the indexation benefit due to the possession of assets for

less than a year (Andreas & Markus, 2014).

Categorized of Assets

Personal use assets that are intended for personal use are generally procured for personal

enjoyment and this category excludes the collectibles. Sale of assets that are procured at costs

less than or equal to $10000 to other persons could not be subject to the liability of taxation

on capital gains. According to the requirements of the question, the personal assets acquired

by Eric include a home sound system and the shares of a listed company (Brean, 2013).

While the procurement cost of the home sound system was found to be $12000 the shares

were found to be costing $5000.

Collectibles could be defined as assets purchased by individuals for fulfilling personal

efficacies alongside providing enjoyment like personal assets. In the case of collectible that

capital gains are not taxable under the condition that the procurement cost of the collectibles

is less than or equal to $500 (Besley & Persson, 2013). The information provided in the

question facilitates an impression of the collectibles acquired by Eric as follows. Eric

acquired a painting that was associated with a procurement cost of $9000 and an antique

chair at a procurement cost of $3000. Another collectible acquired by Eric included an

antique vase which amounted for an acquisition cost of $2000 (Becker, Reimer & Rust,

2015).

The data obtained from the above stated scenario could be utilized as inputs for formula to

calculate capital gain on the assets which were under possession for less than a year.

Capital Data of the assets

Asset Cost Base of Assets Capital Proceeds of

Assets

Net Capital Profit/

(Net Capital Loss)

Home Sound 12,000 11000 (1000) Loss

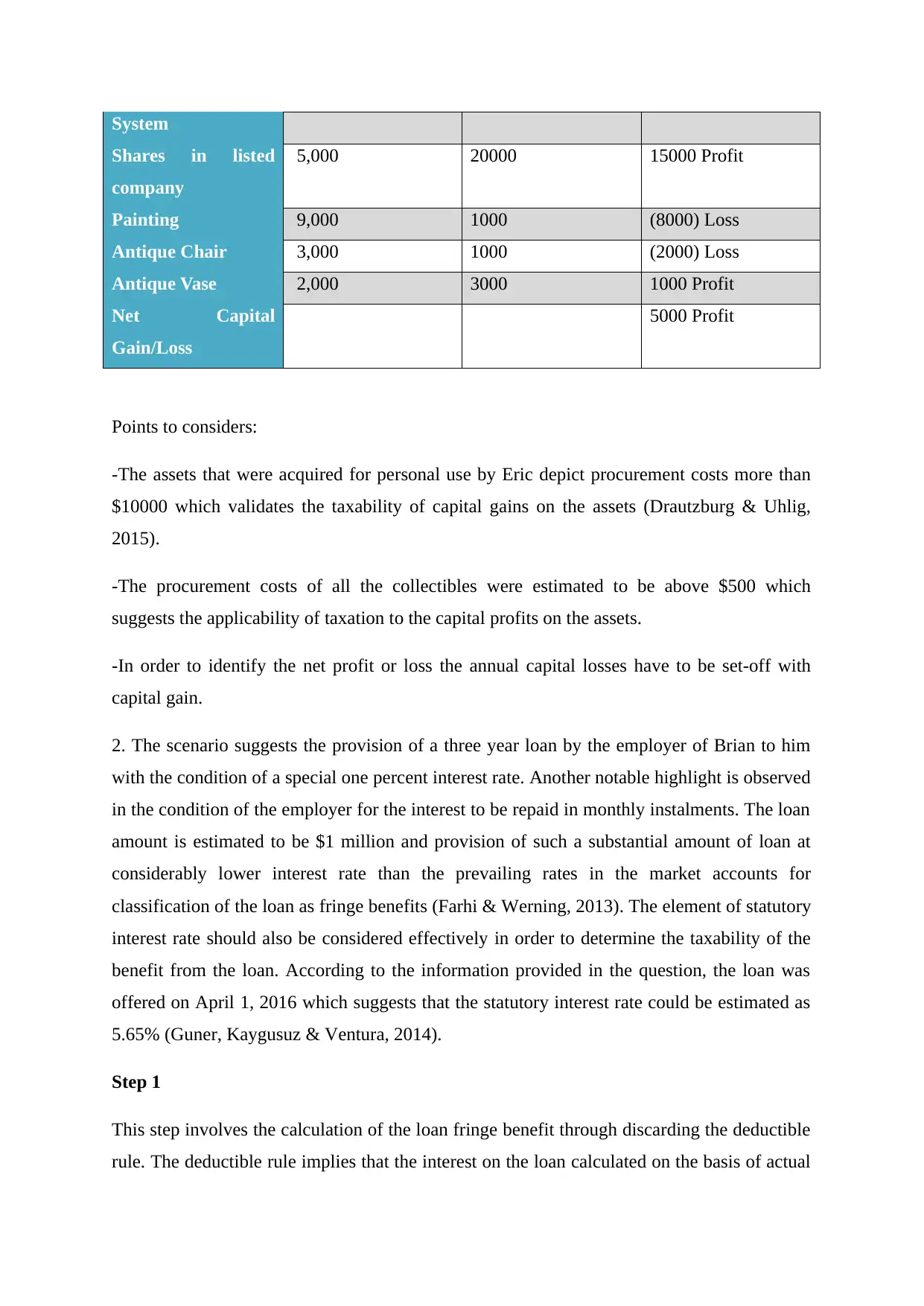

System

Shares in listed

company

5,000 20000 15000 Profit

Painting 9,000 1000 (8000) Loss

Antique Chair 3,000 1000 (2000) Loss

Antique Vase 2,000 3000 1000 Profit

Net Capital

Gain/Loss

5000 Profit

Points to considers:

-The assets that were acquired for personal use by Eric depict procurement costs more than

$10000 which validates the taxability of capital gains on the assets (Drautzburg & Uhlig,

2015).

-The procurement costs of all the collectibles were estimated to be above $500 which

suggests the applicability of taxation to the capital profits on the assets.

-In order to identify the net profit or loss the annual capital losses have to be set-off with

capital gain.

2. The scenario suggests the provision of a three year loan by the employer of Brian to him

with the condition of a special one percent interest rate. Another notable highlight is observed

in the condition of the employer for the interest to be repaid in monthly instalments. The loan

amount is estimated to be $1 million and provision of such a substantial amount of loan at

considerably lower interest rate than the prevailing rates in the market accounts for

classification of the loan as fringe benefits (Farhi & Werning, 2013). The element of statutory

interest rate should also be considered effectively in order to determine the taxability of the

benefit from the loan. According to the information provided in the question, the loan was

offered on April 1, 2016 which suggests that the statutory interest rate could be estimated as

5.65% (Guner, Kaygusuz & Ventura, 2014).

Step 1

This step involves the calculation of the loan fringe benefit through discarding the deductible

rule. The deductible rule implies that the interest on the loan calculated on the basis of actual

Shares in listed

company

5,000 20000 15000 Profit

Painting 9,000 1000 (8000) Loss

Antique Chair 3,000 1000 (2000) Loss

Antique Vase 2,000 3000 1000 Profit

Net Capital

Gain/Loss

5000 Profit

Points to considers:

-The assets that were acquired for personal use by Eric depict procurement costs more than

$10000 which validates the taxability of capital gains on the assets (Drautzburg & Uhlig,

2015).

-The procurement costs of all the collectibles were estimated to be above $500 which

suggests the applicability of taxation to the capital profits on the assets.

-In order to identify the net profit or loss the annual capital losses have to be set-off with

capital gain.

2. The scenario suggests the provision of a three year loan by the employer of Brian to him

with the condition of a special one percent interest rate. Another notable highlight is observed

in the condition of the employer for the interest to be repaid in monthly instalments. The loan

amount is estimated to be $1 million and provision of such a substantial amount of loan at

considerably lower interest rate than the prevailing rates in the market accounts for

classification of the loan as fringe benefits (Farhi & Werning, 2013). The element of statutory

interest rate should also be considered effectively in order to determine the taxability of the

benefit from the loan. According to the information provided in the question, the loan was

offered on April 1, 2016 which suggests that the statutory interest rate could be estimated as

5.65% (Guner, Kaygusuz & Ventura, 2014).

Step 1

This step involves the calculation of the loan fringe benefit through discarding the deductible

rule. The deductible rule implies that the interest on the loan calculated on the basis of actual

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

rate of interest should be subtracted from the interest on loan calculated on the basis of

statutory rate of interest (Henneman, 2015).

Interest according to statutory rate of interest= $1000000 * 5.65%= $56,500

Interest according to actual interest rate= $1000000 * 1%= $10000

Therefore the loan fringe benefit can be calculated as the difference between the two amounts

which is = $56,500-$10,000= $46,500

Step 2

The second step involves the computation of interest based on statutory interest rate with the

assumption that the interest is the real amount payable Interest based on statutory interest

rate= $1000000 * 5.65%= $56,500

Step 3

This step should involve the calculation of tax deductible interest expense since Brian has

spent forty percent of the loan for addressing future obligations and the tax deductible interest

expense could be assumed as hypothetical in nature (Higgins & Pereira, 2014). The tax

deductible interest expense could be calculated as follows: $56,500 * 40% = $22,600

Step 4

The real tax deductible interest expense for Brian should also be calculated since Brian has

utilized 40% of the loan for dealing with future obligations (Jaimovich & Rebelo, 2017). The

real figures for tax deductible interest expense could be calculated as follows: $10000 * 40%

= $4000

Step 5

This stage involves the subtraction of actual amount from the hypothetical figure in order to

reach a specific conclusion. Therefore, $22,600- $4000= $18,600

Step 6

The final taxation amount is estimated in this step through subtracting the amount calculated

in the fifth step from that determined in the first step.Hence, Brian has to pay a final amount

of, $46,500- $18,600 = $27,900

statutory rate of interest (Henneman, 2015).

Interest according to statutory rate of interest= $1000000 * 5.65%= $56,500

Interest according to actual interest rate= $1000000 * 1%= $10000

Therefore the loan fringe benefit can be calculated as the difference between the two amounts

which is = $56,500-$10,000= $46,500

Step 2

The second step involves the computation of interest based on statutory interest rate with the

assumption that the interest is the real amount payable Interest based on statutory interest

rate= $1000000 * 5.65%= $56,500

Step 3

This step should involve the calculation of tax deductible interest expense since Brian has

spent forty percent of the loan for addressing future obligations and the tax deductible interest

expense could be assumed as hypothetical in nature (Higgins & Pereira, 2014). The tax

deductible interest expense could be calculated as follows: $56,500 * 40% = $22,600

Step 4

The real tax deductible interest expense for Brian should also be calculated since Brian has

utilized 40% of the loan for dealing with future obligations (Jaimovich & Rebelo, 2017). The

real figures for tax deductible interest expense could be calculated as follows: $10000 * 40%

= $4000

Step 5

This stage involves the subtraction of actual amount from the hypothetical figure in order to

reach a specific conclusion. Therefore, $22,600- $4000= $18,600

Step 6

The final taxation amount is estimated in this step through subtracting the amount calculated

in the fifth step from that determined in the first step.Hence, Brian has to pay a final amount

of, $46,500- $18,600 = $27,900

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The conditions in which interest is paid at the termination of the loan rather than in monthly

instalments, the deemed period in case of the loan would have to be calculated from the time

when the interest becomes payable (Mellon, 2016). In the case of monthly repayments the

deemed period is assumed from the time when the interests are paid respectively. On the

other hand, it is necessary to emphasize on the case if Brian is not obliged to repay the

interests then the computation has to follow the similar approach only with the assumption of

zero actual interest rate (Matter, 2016).

3.The scenario depicts the agreement between Jack and Jill who are husband and wife to rent

a property under the condition that Jack would be eligible for 10% of the profits earned from

the property while the wife, Jill, would be eligible for 90% of profits. Furthermore, the

agreement also involved Jack’s consent to bear complete responsibilities of any sort of losses

thereby relieving Jill of the burden (Maurer, 2016). Hence it can be stated that the loss of

$10000 observed last year becomes the sole liability of Jack without any responsibility of Jill

in the case. On the other hand, Jack also has the opportunities of offsetting the loss of $10000

through his other incomes thereby reaching on a final estimation of net profit or loss for the

concerned year. Jack also has the option to carry forward the losses for subsequent years until

the point where the property has to be sold which can lead to either profits or losses for Jack

and Jill (Piketty & Saez, 2013).

In event of a loss, the responsibility for the entire amount is vested in Jack who has the

privilege to carry forward the losses or implement them for determination of net profit or

losses in the concerned year or upcoming years (Thomson, 2015). On the contrary, if an event

of profit is encountered then the amount must be distributed in the agreed shares of 10% of

Jack and 90% for Jill respectively. Jack also has the privilege of offsetting the loss of $10000

incurred last year with the profits acquired from sale of property. Therefore, it can be

concluded that Jack can offset the losses of the past year in the present year through income

that can be acquired as profits from the sale of the property (Wallace, 2015). However, if

there are no observed profits in the current year, then Jack is responsible for the losses with

the exclusion of Jill from such undertakings. Hence it can be concluded that Jill would not be

subject to any consequences in context of tax treatment while Jack is obliged to be

responsible for the losses in his accounts.

4. The case of IRC v Duke of Westminster [1936] AC 1 provided insights into the fact that an

individual is rightfully entitled to utilize legal strategies and resources for decreasing total

instalments, the deemed period in case of the loan would have to be calculated from the time

when the interest becomes payable (Mellon, 2016). In the case of monthly repayments the

deemed period is assumed from the time when the interests are paid respectively. On the

other hand, it is necessary to emphasize on the case if Brian is not obliged to repay the

interests then the computation has to follow the similar approach only with the assumption of

zero actual interest rate (Matter, 2016).

3.The scenario depicts the agreement between Jack and Jill who are husband and wife to rent

a property under the condition that Jack would be eligible for 10% of the profits earned from

the property while the wife, Jill, would be eligible for 90% of profits. Furthermore, the

agreement also involved Jack’s consent to bear complete responsibilities of any sort of losses

thereby relieving Jill of the burden (Maurer, 2016). Hence it can be stated that the loss of

$10000 observed last year becomes the sole liability of Jack without any responsibility of Jill

in the case. On the other hand, Jack also has the opportunities of offsetting the loss of $10000

through his other incomes thereby reaching on a final estimation of net profit or loss for the

concerned year. Jack also has the option to carry forward the losses for subsequent years until

the point where the property has to be sold which can lead to either profits or losses for Jack

and Jill (Piketty & Saez, 2013).

In event of a loss, the responsibility for the entire amount is vested in Jack who has the

privilege to carry forward the losses or implement them for determination of net profit or

losses in the concerned year or upcoming years (Thomson, 2015). On the contrary, if an event

of profit is encountered then the amount must be distributed in the agreed shares of 10% of

Jack and 90% for Jill respectively. Jack also has the privilege of offsetting the loss of $10000

incurred last year with the profits acquired from sale of property. Therefore, it can be

concluded that Jack can offset the losses of the past year in the present year through income

that can be acquired as profits from the sale of the property (Wallace, 2015). However, if

there are no observed profits in the current year, then Jack is responsible for the losses with

the exclusion of Jill from such undertakings. Hence it can be concluded that Jill would not be

subject to any consequences in context of tax treatment while Jack is obliged to be

responsible for the losses in his accounts.

4. The case of IRC v Duke of Westminster [1936] AC 1 provided insights into the fact that an

individual is rightfully entitled to utilize legal strategies and resources for decreasing total

income at the end of a year. Therefore, it can be imperatively observed that in cases where an

individual decreases their total income at the end of the year, the Commissioners of Inland

Revenue are not authorized for inquiry into the matter or pressurizing the individual to

increase their payable tax (Thomson, 2015). However, it is necessary to consider that such

rule is applicable only in cases where an individual utilizes authentic measures for decreasing

total income at the end to the year helping them in reducing the total payable tax.

The notable principles that can be apprehended from the case include the following:

Every individual is rightfully eligible to implement strategic measures in account

management leading to depreciation in their total income

An individual is not liable to pay additional taxes if the procedures adopted for decreasing

income are ethical and moral.

Adoption of legal means to decrease the total payable tax amount also indicates that an

individual cannot be questioned for validity. The individual is also exempted from any sort of

pressure to pay an increased amount of tax.

However, the validity of the above mentioned rule could be questioned on the grounds of

inferences drawn from new case laws in the contemporary scenario (Jaimovich & Rebelo,

2017). The prominent difference could be observed in the reforms in ideologies underlying

review of accounts and their management. In the current scenario, the rule can be presented

as follows:

The rule mentioned previously holds significance in the contemporary environment in order

to prevent organizations from utilizing unscrupulous means for modification of accounts to

accomplish superior advantage. The rule is also reflective of the legal right for businesses to

execute their operations feasibly (Higgins & Pereira, 2014). An example of the application of

the rule can be observed in a company which is encountering losses and is unable to fulfil its

obligations. This type of organization could prefer alteration of balance sheet amounts

alongside writing off their fixed assets according to the intended values. The organization

should also emphasize on the significance of authenticity of the documents that are used to

justify the transactions (Henneman, 2015). On the other hand, the organization is liable to

experience backlash in event of adopting unethical means for management of accounts due to

the rule. Therefore, it can be concluded that transactions which facilitate effective operations

individual decreases their total income at the end of the year, the Commissioners of Inland

Revenue are not authorized for inquiry into the matter or pressurizing the individual to

increase their payable tax (Thomson, 2015). However, it is necessary to consider that such

rule is applicable only in cases where an individual utilizes authentic measures for decreasing

total income at the end to the year helping them in reducing the total payable tax.

The notable principles that can be apprehended from the case include the following:

Every individual is rightfully eligible to implement strategic measures in account

management leading to depreciation in their total income

An individual is not liable to pay additional taxes if the procedures adopted for decreasing

income are ethical and moral.

Adoption of legal means to decrease the total payable tax amount also indicates that an

individual cannot be questioned for validity. The individual is also exempted from any sort of

pressure to pay an increased amount of tax.

However, the validity of the above mentioned rule could be questioned on the grounds of

inferences drawn from new case laws in the contemporary scenario (Jaimovich & Rebelo,

2017). The prominent difference could be observed in the reforms in ideologies underlying

review of accounts and their management. In the current scenario, the rule can be presented

as follows:

The rule mentioned previously holds significance in the contemporary environment in order

to prevent organizations from utilizing unscrupulous means for modification of accounts to

accomplish superior advantage. The rule is also reflective of the legal right for businesses to

execute their operations feasibly (Higgins & Pereira, 2014). An example of the application of

the rule can be observed in a company which is encountering losses and is unable to fulfil its

obligations. This type of organization could prefer alteration of balance sheet amounts

alongside writing off their fixed assets according to the intended values. The organization

should also emphasize on the significance of authenticity of the documents that are used to

justify the transactions (Henneman, 2015). On the other hand, the organization is liable to

experience backlash in event of adopting unethical means for management of accounts due to

the rule. Therefore, it can be concluded that transactions which facilitate effective operations

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of an enterprise could be considered valid from a legal perspective without any concerns of

questioning by legal authorities.

5. The scenario indicates the abundance of big pine trees in the piece of land owned by Bill

which in turn is intended by him to be used as grazing grounds for sheep. In order to

accomplish this feat, Bill has to ensure that the trees are cut from the property. Hence, Bill

hired the services of a logging company which agreed to reimburse Bill with $1000 for every

100 meters of timber (Guner, Kaygusuz & Ventura, 2014). The question that needs to be

addressed in this context is the applicability of the tax on Bill for the amount of profits earned

by the logging company. The question does not provide clear insights into the exact amount

of receipts for clearing of trees which implies the assumption that is a revenue receipt in

hands of Bill. Therefore, Bill is not liable to pay the capital gains tax.

The lump sum amount attained by Bill can be considered as a capital receipt in his hands. For

example, if Bill receives $50000 from the logging company for removing the timber from his

property then that amount can be ascertained as capital receipt for Bill. Considering the

payment as capital receipt could be validated on the grounds of the lump sum nature of the

payment alongside the zero presence of recurring receipts (Farhi & Werning, 2013). Another

characteristic that should be noted in this context is that the transaction is underlined by the

provision of rights to another party for removal of trees from the property. Hence it can be

observed that since the receipt in the hands of bill is a lump sum amount and has been

considered as capital receipt, the amount is taxable according to the rules of capital gains tax.

The scenarios depicted above provide an illustration of the fact that Bill is acquiring money

in either case. The first case suggests that Bill receives payments in recurring receipts which

are also small in nature while in the second case Bill receives a capital receipt in the form of a

lump sum amount of $50000 which is not recurring in nature. The concern of providing the

right to the logging company for clearing of trees from the property is also liable for

classifying the lump sum amount eligible for capital gains tax (Farhi & Werning, 2013). The

receipt in the second case is larger in amount and can be estimated as one-time in nature

owing to the considerable period of time required for regrowth of the trees after cutting them

down. Hence the second case indicates that Bill is engaged in the sale of an asset to another

company for a considerable amount alongside providing rights to the company. According to

the precedents of taxation law, sale of assets for consideration by one party to another implies

consideration of capital receipt and taxability for the seller (Farhi & Werning, 2013). On the

contrary, the first case depicts formidable implications towards recurring receipts which in

questioning by legal authorities.

5. The scenario indicates the abundance of big pine trees in the piece of land owned by Bill

which in turn is intended by him to be used as grazing grounds for sheep. In order to

accomplish this feat, Bill has to ensure that the trees are cut from the property. Hence, Bill

hired the services of a logging company which agreed to reimburse Bill with $1000 for every

100 meters of timber (Guner, Kaygusuz & Ventura, 2014). The question that needs to be

addressed in this context is the applicability of the tax on Bill for the amount of profits earned

by the logging company. The question does not provide clear insights into the exact amount

of receipts for clearing of trees which implies the assumption that is a revenue receipt in

hands of Bill. Therefore, Bill is not liable to pay the capital gains tax.

The lump sum amount attained by Bill can be considered as a capital receipt in his hands. For

example, if Bill receives $50000 from the logging company for removing the timber from his

property then that amount can be ascertained as capital receipt for Bill. Considering the

payment as capital receipt could be validated on the grounds of the lump sum nature of the

payment alongside the zero presence of recurring receipts (Farhi & Werning, 2013). Another

characteristic that should be noted in this context is that the transaction is underlined by the

provision of rights to another party for removal of trees from the property. Hence it can be

observed that since the receipt in the hands of bill is a lump sum amount and has been

considered as capital receipt, the amount is taxable according to the rules of capital gains tax.

The scenarios depicted above provide an illustration of the fact that Bill is acquiring money

in either case. The first case suggests that Bill receives payments in recurring receipts which

are also small in nature while in the second case Bill receives a capital receipt in the form of a

lump sum amount of $50000 which is not recurring in nature. The concern of providing the

right to the logging company for clearing of trees from the property is also liable for

classifying the lump sum amount eligible for capital gains tax (Farhi & Werning, 2013). The

receipt in the second case is larger in amount and can be estimated as one-time in nature

owing to the considerable period of time required for regrowth of the trees after cutting them

down. Hence the second case indicates that Bill is engaged in the sale of an asset to another

company for a considerable amount alongside providing rights to the company. According to

the precedents of taxation law, sale of assets for consideration by one party to another implies

consideration of capital receipt and taxability for the seller (Farhi & Werning, 2013). On the

contrary, the first case depicts formidable implications towards recurring receipts which in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

turn limit the prospects for acquiring capital gain tax. Therefore the scenario in the first case

should be addressed through normal taxation rates rather than subjecting the profits to capital

gains tax.

References

Andreas, O. and Markus, H., 2014. Taxation of income from domestic and cross-border

collective investment.

Brean, D.J., 2013. Taxation in modern China. Routledge.

Besley, T.J. and Persson, T., 2013. Taxation and development.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International.

Drautzburg, T. and Uhlig, H., 2015. Fiscal stimulus and distortionary taxation. Review of

Economic Dynamics, 18(4), pp.894-920.

Farhi, E. and Werning, I., 2013. Insurance and taxation over the life cycle. Review of

Economic Studies, 80(2), pp.596-635.

Guner, N., Kaygusuz, R. and Ventura, G., 2014. Income taxation of US households: Facts

and parametric estimates. Review of Economic Dynamics, 17(4), pp.559-581.

Henneman, J.B., 2015. Royal Taxation in Fourteenth-Century France: The Development of

War Financing, 1322-1359. Princeton University Press.

Higgins, S. and Pereira, C., 2014. The effects of Brazil’s taxation and social spending on the

distribution of household income. Public Finance Review, 42(3), pp.346-367.

should be addressed through normal taxation rates rather than subjecting the profits to capital

gains tax.

References

Andreas, O. and Markus, H., 2014. Taxation of income from domestic and cross-border

collective investment.

Brean, D.J., 2013. Taxation in modern China. Routledge.

Besley, T.J. and Persson, T., 2013. Taxation and development.

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International.

Drautzburg, T. and Uhlig, H., 2015. Fiscal stimulus and distortionary taxation. Review of

Economic Dynamics, 18(4), pp.894-920.

Farhi, E. and Werning, I., 2013. Insurance and taxation over the life cycle. Review of

Economic Studies, 80(2), pp.596-635.

Guner, N., Kaygusuz, R. and Ventura, G., 2014. Income taxation of US households: Facts

and parametric estimates. Review of Economic Dynamics, 17(4), pp.559-581.

Henneman, J.B., 2015. Royal Taxation in Fourteenth-Century France: The Development of

War Financing, 1322-1359. Princeton University Press.

Higgins, S. and Pereira, C., 2014. The effects of Brazil’s taxation and social spending on the

distribution of household income. Public Finance Review, 42(3), pp.346-367.

Jaimovich, N. and Rebelo, S., 2017. Nonlinear effects of taxation on growth. Journal of

Political Economy, 125(1), pp.265-291.

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Matter, P., 2016. Green taxation in question.

Maurer, J., 2016. Sharing Economy. Regulatory Approaches for Combating Airbnb's

Controversy Regarding Taxation and Regulation.

Piketty, T. and Saez, E., 2013. A theory of optimal inheritance taxation. Econometrica, 81(5),

pp.1851-1886.

Thomson, W., 2015. Axiomatic and game-theoretic analysis of bankruptcy and taxation

problems: an update. Mathematical Social Sciences, 74, pp.41-59.

Wallace, S.L., 2015. Taxation in Egypt from Augustus to Diocletian. Princeton University

Press.

Political Economy, 125(1), pp.265-291.

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Matter, P., 2016. Green taxation in question.

Maurer, J., 2016. Sharing Economy. Regulatory Approaches for Combating Airbnb's

Controversy Regarding Taxation and Regulation.

Piketty, T. and Saez, E., 2013. A theory of optimal inheritance taxation. Econometrica, 81(5),

pp.1851-1886.

Thomson, W., 2015. Axiomatic and game-theoretic analysis of bankruptcy and taxation

problems: an update. Mathematical Social Sciences, 74, pp.41-59.

Wallace, S.L., 2015. Taxation in Egypt from Augustus to Diocletian. Princeton University

Press.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.