HA3042 Taxation Law Assignment: Fringe Benefits Tax and CGT

VerifiedAdded on 2022/11/14

|9

|2360

|71

Homework Assignment

AI Summary

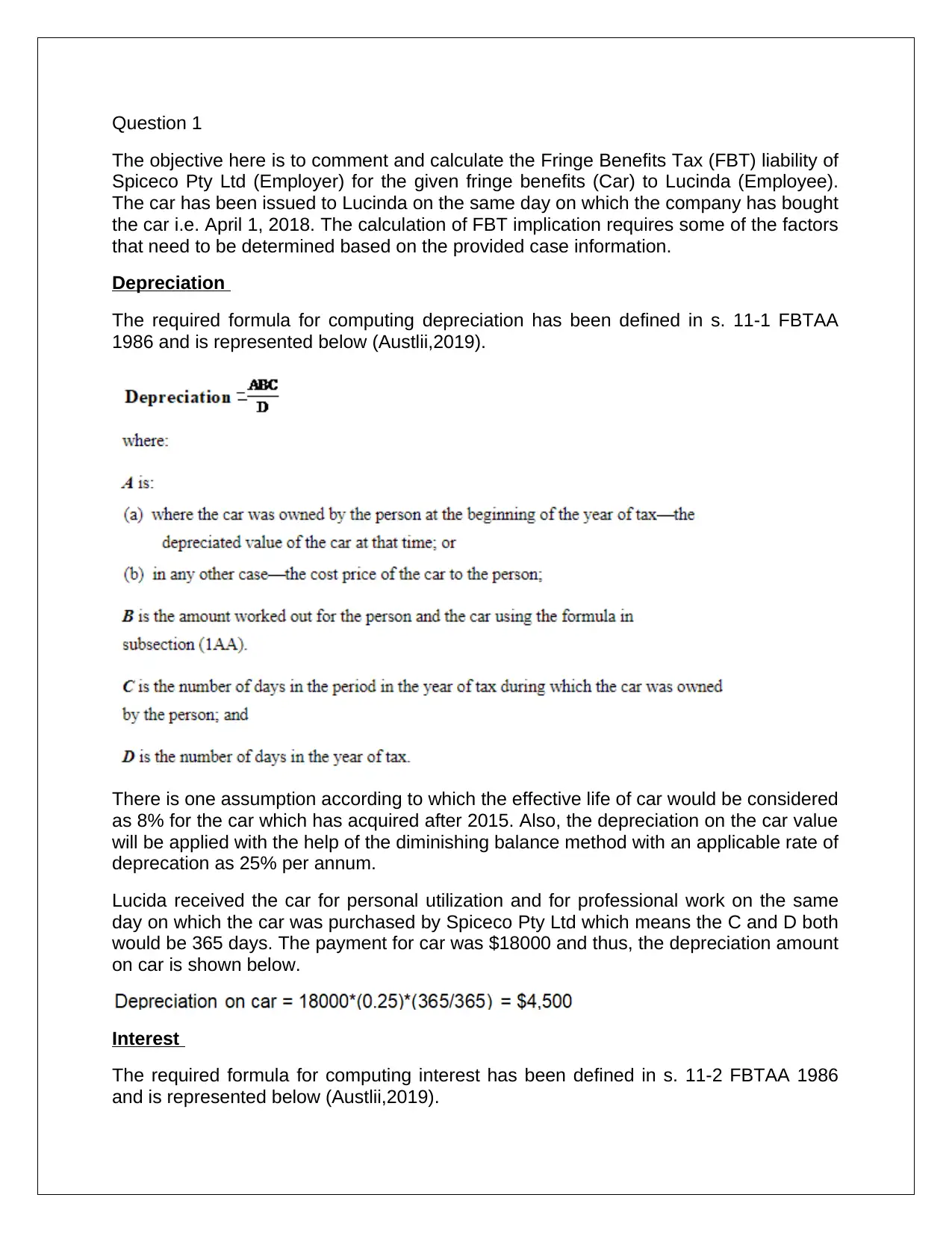

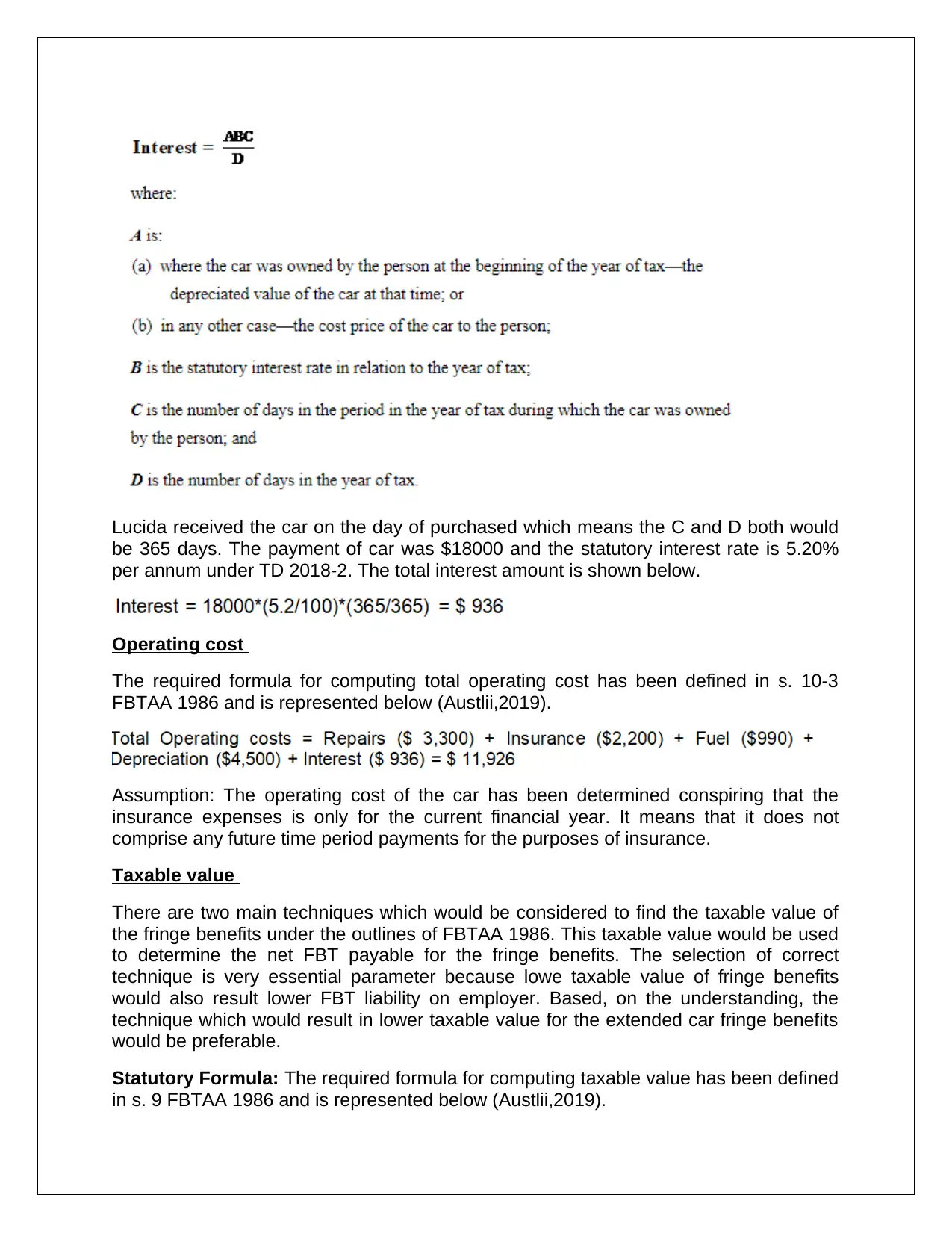

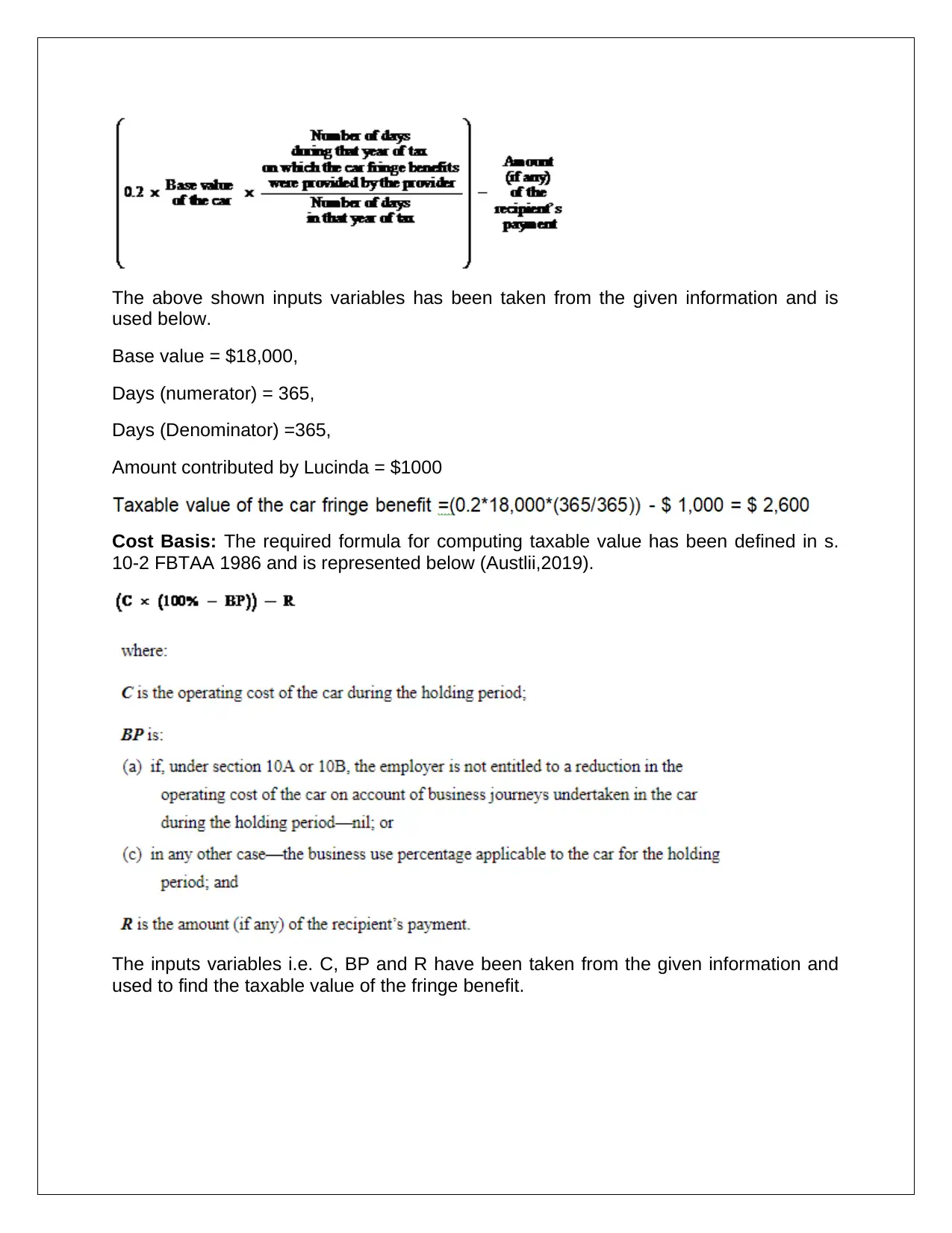

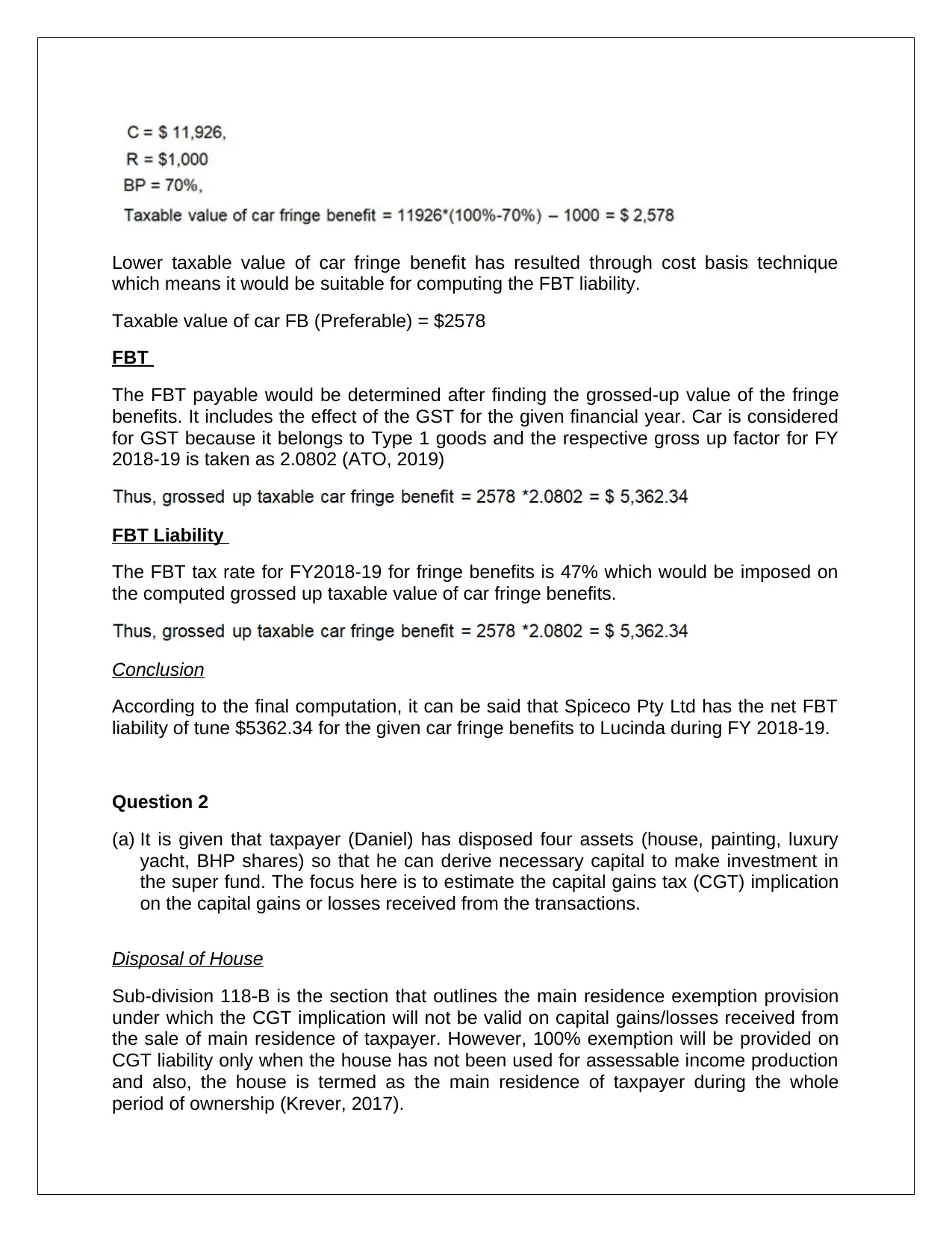

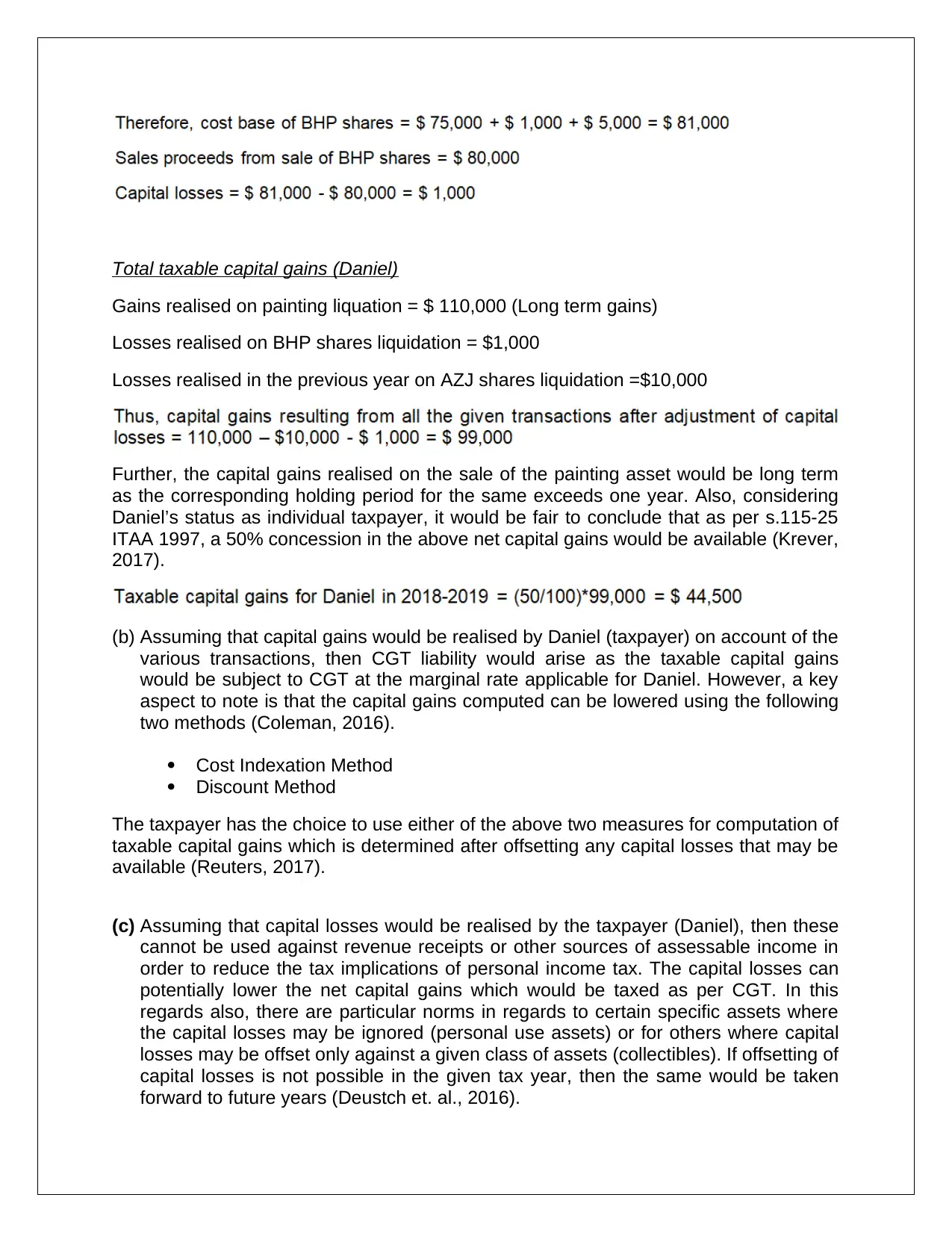

This taxation law assignment, prepared by a student, addresses two key areas of Australian tax law: Fringe Benefits Tax (FBT) and Capital Gains Tax (CGT). The first part focuses on calculating the FBT liability for Spiceco Pty Ltd concerning a car fringe benefit provided to an employee, Lucinda. The calculation involves determining depreciation, interest, operating costs, and taxable value using statutory formulas and cost basis techniques. The final FBT liability is computed after considering the grossed-up value and applicable tax rates. The second part of the assignment examines the Capital Gains Tax (CGT) implications for Daniel, who disposed of several assets, including a house, painting, luxury yacht, and BHP shares. The analysis covers the main residence exemption, treatment of collectibles, personal use assets, and shares, including cost base calculations. The assignment concludes with a discussion of potential capital gains or losses, the 50% discount method, and the application of CGT at the marginal rate, along with the possibility of offsetting capital losses and carrying them forward. References to relevant sections of the FBTAA 1986 and ITAA 1997 are included.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.