Australian Taxation Law Assignment - [University Name]

VerifiedAdded on 2022/08/18

|5

|649

|13

Homework Assignment

AI Summary

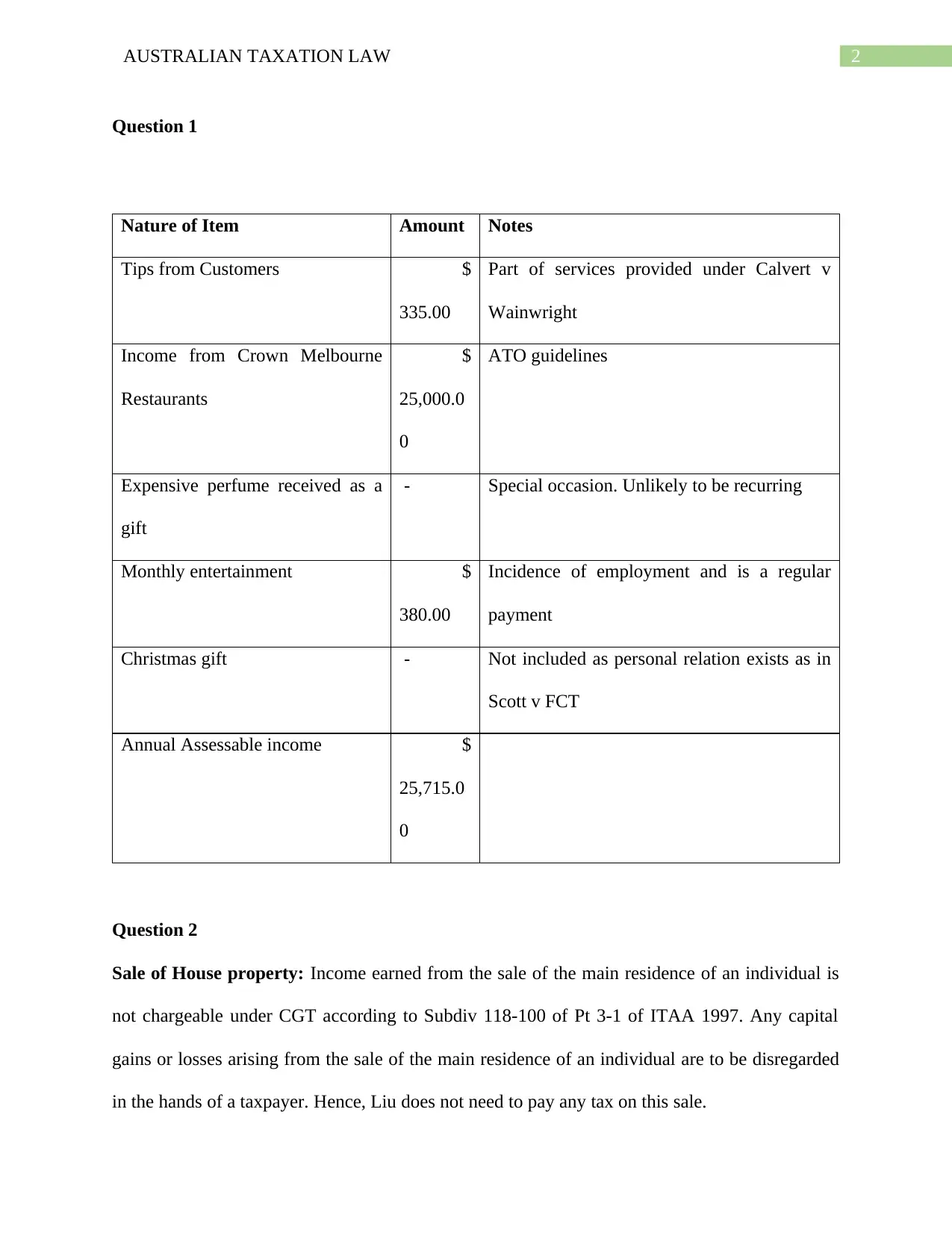

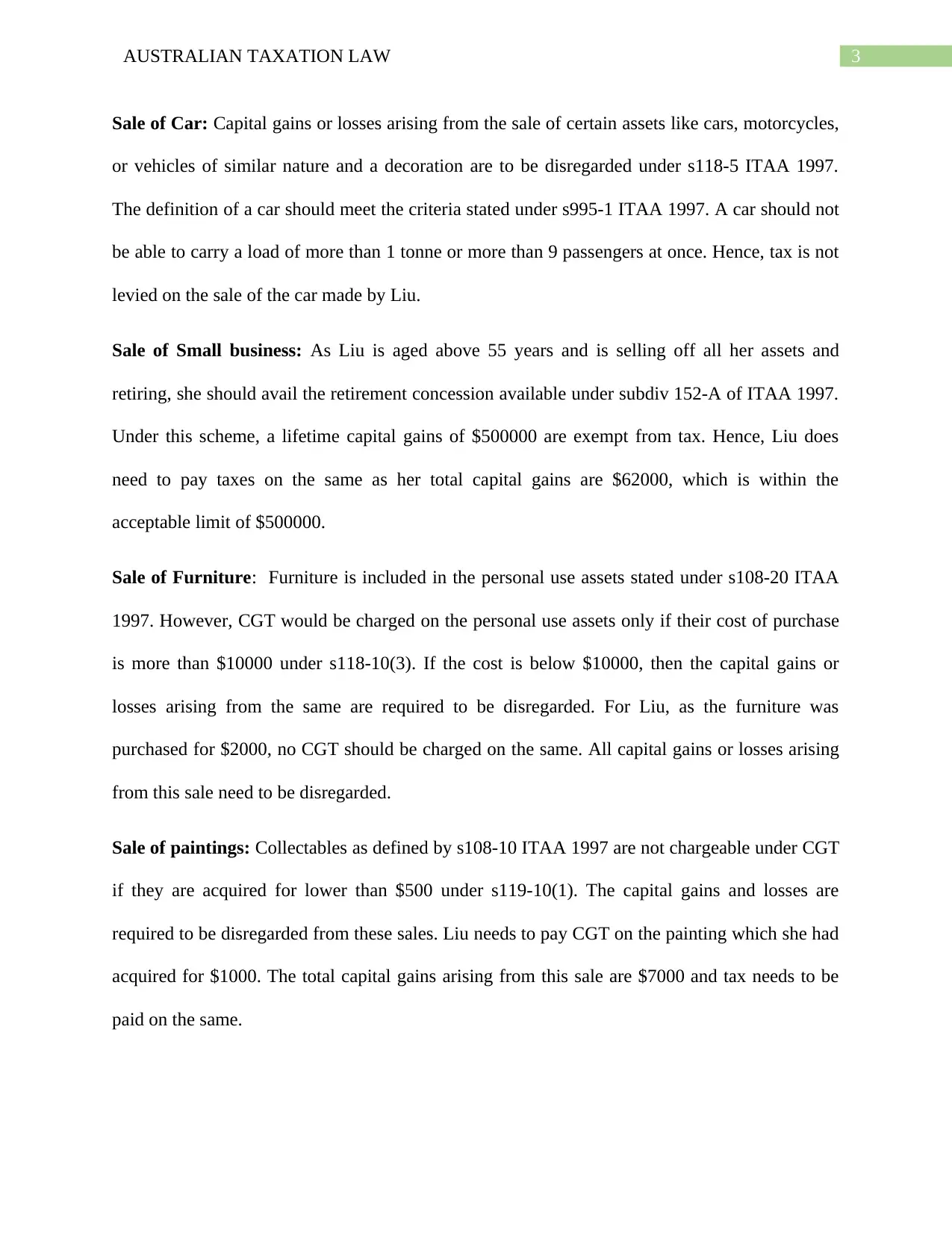

This Australian Taxation Law assignment addresses two key questions related to taxation. Question 1 focuses on determining assessable income, analyzing various income sources like tips, restaurant income, and gifts, applying relevant ATO guidelines and legal precedents. Question 2 delves into capital gains tax (CGT) implications for the sale of different assets, including a house, car, small business, furniture, and paintings. The analysis considers specific provisions of the ITAA 1997, such as Subdiv 118-100, s118-5, s995-1, subdiv 152-A, s108-20, and s118-10(3), to determine tax liabilities, including the application of retirement concessions and the treatment of personal use assets and collectables. The assignment concludes with a bibliography citing relevant sources from ATO and other governmental websites.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.