TAX TAX 13 Assignment Solution - Finance Module, Semester 1

VerifiedAdded on 2020/02/23

|14

|3471

|34

Homework Assignment

AI Summary

This document presents a comprehensive solution to a TAX assignment, addressing various aspects of Australian tax law. It begins with answers to specific questions regarding taxation powers, sources of tax law, residential status, Medicare levy, misleading conduct, theft losses, repair deductions, stock valuation, and PAYG. The assignment then delves into the deductibility of expenses, specifically focusing on the general and specific deductions under the Income Tax Assessment Act 1997. The solution provides a detailed breakdown of allowable deductions, including tax agent fees and solicitor fees. Furthermore, the document examines the concept of residential status, outlining the different tests used to determine residency for tax purposes. Finally, the assignment addresses the calculation of taxable income, distinguishing between ordinary and statutory income, and providing examples of taxable income sources, such as employment income and tips. The document also addresses the taxability of different income sources.

Running head: TAX

Tax

Name of the Student:

Name of the University:

Authors Note:

Tax

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAX

Table of Contents

PART – A...................................................................................................................................2

Answer to question 1..................................................................................................................2

Answer to Question 3.................................................................................................................2

Answer to Question 6.................................................................................................................4

Answer to Question 7.................................................................................................................4

Answer to Question 8.................................................................................................................4

Answer to Question 9.................................................................................................................5

Answer to Question 10...............................................................................................................5

Part B..........................................................................................................................................5

Part C..........................................................................................................................................7

Part D.........................................................................................................................................8

Part E........................................................................................................................................10

Reference..................................................................................................................................11

Table of Contents

PART – A...................................................................................................................................2

Answer to question 1..................................................................................................................2

Answer to Question 3.................................................................................................................2

Answer to Question 6.................................................................................................................4

Answer to Question 7.................................................................................................................4

Answer to Question 8.................................................................................................................4

Answer to Question 9.................................................................................................................5

Answer to Question 10...............................................................................................................5

Part B..........................................................................................................................................5

Part C..........................................................................................................................................7

Part D.........................................................................................................................................8

Part E........................................................................................................................................10

Reference..................................................................................................................................11

2TAX

PART – A

Answer to question 1.

In accordance with the Constitution of Australia, the primary source of the

Commonwealth Parliament’s taxation power is mostly comes from Sections 51(ii), 53, 55, 90

and 96.

According to Section 51(ii) of Australian Constitution, the power to create laws in

regard to taxation is given to the Commonwealth Parliament (Gitman et al. 2015). However,

there are certain conditions that those laws do not differentiate between states or parts of any

states.

Answer to question 2.

It is observed that Acts mainly create Tax Laws in Australia. Therefore, the primary

source of Australian Tax Laws comes from Legislation that are various Parliamentary Acts

and Regulations that are delegated legislation. Thus legislation is the primary or main or first

source of Australian Tax Laws. The second source of Tax Laws in Australia are the Cases

which interpret the legislation such as decisions of court, tribunals, etc. Third source of tax

laws in practise in Australia is the Tax Rulings by the Commissioner of Taxation (Katic &

Leigh 2016).

Answer to Question 3

According to the Australian Taxation Office, Taxation Ruling TR 98/17 discusses

about the residential status of any individual who is entering Australia (Braithwaite 2017).

According to TR 98/17, this ruling is applicable to most of the individuals those who are

entering Australia which includes the followings:

PART – A

Answer to question 1.

In accordance with the Constitution of Australia, the primary source of the

Commonwealth Parliament’s taxation power is mostly comes from Sections 51(ii), 53, 55, 90

and 96.

According to Section 51(ii) of Australian Constitution, the power to create laws in

regard to taxation is given to the Commonwealth Parliament (Gitman et al. 2015). However,

there are certain conditions that those laws do not differentiate between states or parts of any

states.

Answer to question 2.

It is observed that Acts mainly create Tax Laws in Australia. Therefore, the primary

source of Australian Tax Laws comes from Legislation that are various Parliamentary Acts

and Regulations that are delegated legislation. Thus legislation is the primary or main or first

source of Australian Tax Laws. The second source of Tax Laws in Australia are the Cases

which interpret the legislation such as decisions of court, tribunals, etc. Third source of tax

laws in practise in Australia is the Tax Rulings by the Commissioner of Taxation (Katic &

Leigh 2016).

Answer to Question 3

According to the Australian Taxation Office, Taxation Ruling TR 98/17 discusses

about the residential status of any individual who is entering Australia (Braithwaite 2017).

According to TR 98/17, this ruling is applicable to most of the individuals those who are

entering Australia which includes the followings:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAX

a. Any migrants,

b. Any student who is studying in Australia,

c. Any person who came to visit Australia i.e. a Visitor,

d. Any worker(s) who came along with planned contracts of employment.

Answer to question 4.

In Australia, Medicare gives the residents of Australia health care access. Medicare

Levy of 2% has to be paid by the taxpayers in Australia which is partly funded by them. If

one’s taxable income is below a certain limit then that person’s Medicare levy might get

reduced or might not have to pay any levy at all (Kucukvar et al. 2014). On the other hand,

one might need to pay Medicare levy surcharge (ML S) if he/ she have health insurance of a

private hospital. The individual meets some medical requirements or a resident of other

country are not entitled to Medicare Benefits then he/ she might be exempted from paying the

Medicare Levy.

Answer to Question 5

According to Australian Law, misleading or dishonest conduct is a principle. As per

Schedule 2 of the Competition and Consumer Act 2010, any conduct by companies in trade

and commerce that is misleading or false or like to misguide is prohibited under Section 18 of

the Australian Consumer Law (Taylor & Richardson 2013). Moreover, prohibition of

misguiding, false, or deceptive conduct in terms of financial services is clearly stated under

Section 12DA of the Australian Securities and Investment Commission Act 2001.

The main objective of this principle is to provide security and safety to the consumers

from being misguided by businesses.

a. Any migrants,

b. Any student who is studying in Australia,

c. Any person who came to visit Australia i.e. a Visitor,

d. Any worker(s) who came along with planned contracts of employment.

Answer to question 4.

In Australia, Medicare gives the residents of Australia health care access. Medicare

Levy of 2% has to be paid by the taxpayers in Australia which is partly funded by them. If

one’s taxable income is below a certain limit then that person’s Medicare levy might get

reduced or might not have to pay any levy at all (Kucukvar et al. 2014). On the other hand,

one might need to pay Medicare levy surcharge (ML S) if he/ she have health insurance of a

private hospital. The individual meets some medical requirements or a resident of other

country are not entitled to Medicare Benefits then he/ she might be exempted from paying the

Medicare Levy.

Answer to Question 5

According to Australian Law, misleading or dishonest conduct is a principle. As per

Schedule 2 of the Competition and Consumer Act 2010, any conduct by companies in trade

and commerce that is misleading or false or like to misguide is prohibited under Section 18 of

the Australian Consumer Law (Taylor & Richardson 2013). Moreover, prohibition of

misguiding, false, or deceptive conduct in terms of financial services is clearly stated under

Section 12DA of the Australian Securities and Investment Commission Act 2001.

The main objective of this principle is to provide security and safety to the consumers

from being misguided by businesses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAX

Answer to Question 6

The Section 25-45 of the Income Tax Assessment Act 1997 states about the lost by theft.

As per the section, it is clearly mentioned that loss in respect of money cannot be deducted by

one if:

a. One ascertains the loss in the year of income,

b. The loss so ascertained was the result of activities such as theft, stealing, larceny,

defalcation,

c. In the assessable income for the year of income of that person, the amount was

involved, or may be an earlier year of income.

Answer to Question 7

The Case W Thomas & Co Pty Ltd v FC of T (1965), deals with deduction to a claim

of a taxpayer for undertaking a repair. In the case a taxpayer who was a flour miller and grain

merchant purchased a building whose some parts were in a state of broken down. The person

then undertook extensive repair work which include repair of roof, guttering, walls and floor

of the building (Richardson et al. 2013). Then the person pursued deduction for the cost of

work as repair. However, the amount was not deductible under section 53 of the ITAA 1997

as the expenses for the repair for the house was not needed for producing assessable income

of the taxpayer.

Answer to Question 8

A taxpayer can opt for one of the following method for valuation of each stock item at the

end of the year of income (Forsyth et al. 2014).

a. The method of cost price which includes all cost relating to brining the stock at its

current location and situation,

Answer to Question 6

The Section 25-45 of the Income Tax Assessment Act 1997 states about the lost by theft.

As per the section, it is clearly mentioned that loss in respect of money cannot be deducted by

one if:

a. One ascertains the loss in the year of income,

b. The loss so ascertained was the result of activities such as theft, stealing, larceny,

defalcation,

c. In the assessable income for the year of income of that person, the amount was

involved, or may be an earlier year of income.

Answer to Question 7

The Case W Thomas & Co Pty Ltd v FC of T (1965), deals with deduction to a claim

of a taxpayer for undertaking a repair. In the case a taxpayer who was a flour miller and grain

merchant purchased a building whose some parts were in a state of broken down. The person

then undertook extensive repair work which include repair of roof, guttering, walls and floor

of the building (Richardson et al. 2013). Then the person pursued deduction for the cost of

work as repair. However, the amount was not deductible under section 53 of the ITAA 1997

as the expenses for the repair for the house was not needed for producing assessable income

of the taxpayer.

Answer to Question 8

A taxpayer can opt for one of the following method for valuation of each stock item at the

end of the year of income (Forsyth et al. 2014).

a. The method of cost price which includes all cost relating to brining the stock at its

current location and situation,

5TAX

b. The method of Market selling value which makes use of the stock’s current value if

sold during the normal course of business,

c. Method of Replacement Value where cost to acquire nearly same item is used.

Answer to Question 9

The person having a taxable income of $45,000 in 2016/17 is liable to pay tax of

amount $3752 and in addition to this, the person also needs to pay 32.5c for every $1 over

$37,000.

Answer to Question 10

The PAYG refers to Pay As You Go income tax instalment system that comprises of

payments that are made regularly by the employers and other taxpayers. Here instalment

system is used to collect income tax. It is a system of instalments in order to make regular

payments towards one’s expected income tax liability for the year. If an individual pays

PAYG instalments, still he/ she will be required to file a tax return for the year (Richardson

et al. 2015).

Part B

The Division 8 of the Income Tax Assessment Act 1997 provides rules that describes

the deductibility of outgoings and losses. The division makes a distinction between the

general deduction as discussed under section 8-1 of the Income Tax Assessment Act 1997

and the specific deduction as provided under section 8-5 of the Income tax Assessment Act

1997.

The section 8-1 of the Income Tax Assessment Act 1997 states that an individual is

allowed to claim deduction for the loss or outgoing that has been incurred for:

producing or gaining assessable income;

b. The method of Market selling value which makes use of the stock’s current value if

sold during the normal course of business,

c. Method of Replacement Value where cost to acquire nearly same item is used.

Answer to Question 9

The person having a taxable income of $45,000 in 2016/17 is liable to pay tax of

amount $3752 and in addition to this, the person also needs to pay 32.5c for every $1 over

$37,000.

Answer to Question 10

The PAYG refers to Pay As You Go income tax instalment system that comprises of

payments that are made regularly by the employers and other taxpayers. Here instalment

system is used to collect income tax. It is a system of instalments in order to make regular

payments towards one’s expected income tax liability for the year. If an individual pays

PAYG instalments, still he/ she will be required to file a tax return for the year (Richardson

et al. 2015).

Part B

The Division 8 of the Income Tax Assessment Act 1997 provides rules that describes

the deductibility of outgoings and losses. The division makes a distinction between the

general deduction as discussed under section 8-1 of the Income Tax Assessment Act 1997

and the specific deduction as provided under section 8-5 of the Income tax Assessment Act

1997.

The section 8-1 of the Income Tax Assessment Act 1997 states that an individual is

allowed to claim deduction for the loss or outgoing that has been incurred for:

producing or gaining assessable income;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAX

the expenses that are incurred for carrying on the activity related to business;

The section 8-5 of the Income tax Assessment Act 1997 states that a taxpayer is allowed

to claim specific deductions from the assessable income. The specific deduction is loss or

outgoing that is deductible from assessable under specific provisions of the tax act (Borowski

2013).

In this case, Ram has incurred three types of expense the deductibility of these expenses

are determined in this section of the explanation. The section 25-5 of the Income Tax

Assessment Act 1997 states that expenses that have been incurred for managing the tax affair

is allowed as deduction. That means the cost of accounting and the tax agent fees will be

allowed as deduction under this section.

It can be seen that Ram has incurred solicitor expenses for drafting an objection against

the assessment of ATO. The Para 11 of the Taxation Ruling 2011/5 states that if a tax payer

is not satisfied with the assessment then the taxpayer can raise an objection in the procedure

as provided under section 175A(1) of the Income Tax Assessment Act 1936. The ATO

Interpretive Decision 2002/814 deals with the issue of deductibility of legal or accounting

expenses for dispute with the tax authorities (McLachlan 2013). The decision provided in the

interpretive decision states that expenses incurred for appealing in the court for tax dispute is

allowed as deduction under section 8-1 of the Income Tax Assessment Act 1997. Therefore,

it can be said that the expenses incurred by Ram for objecting to the assessment of ATO is

allowed as deduction.

The amount that is incurred for payment of income tax is not allowed as deduction under

section 8-1 of the Income Tax Assessment Act 1997. Therefore, the computation of allowable

deductions are given below:

Computation of Allowable Deduction

the expenses that are incurred for carrying on the activity related to business;

The section 8-5 of the Income tax Assessment Act 1997 states that a taxpayer is allowed

to claim specific deductions from the assessable income. The specific deduction is loss or

outgoing that is deductible from assessable under specific provisions of the tax act (Borowski

2013).

In this case, Ram has incurred three types of expense the deductibility of these expenses

are determined in this section of the explanation. The section 25-5 of the Income Tax

Assessment Act 1997 states that expenses that have been incurred for managing the tax affair

is allowed as deduction. That means the cost of accounting and the tax agent fees will be

allowed as deduction under this section.

It can be seen that Ram has incurred solicitor expenses for drafting an objection against

the assessment of ATO. The Para 11 of the Taxation Ruling 2011/5 states that if a tax payer

is not satisfied with the assessment then the taxpayer can raise an objection in the procedure

as provided under section 175A(1) of the Income Tax Assessment Act 1936. The ATO

Interpretive Decision 2002/814 deals with the issue of deductibility of legal or accounting

expenses for dispute with the tax authorities (McLachlan 2013). The decision provided in the

interpretive decision states that expenses incurred for appealing in the court for tax dispute is

allowed as deduction under section 8-1 of the Income Tax Assessment Act 1997. Therefore,

it can be said that the expenses incurred by Ram for objecting to the assessment of ATO is

allowed as deduction.

The amount that is incurred for payment of income tax is not allowed as deduction under

section 8-1 of the Income Tax Assessment Act 1997. Therefore, the computation of allowable

deductions are given below:

Computation of Allowable Deduction

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAX

Particulars Amount Reason

Tax Agent fees $ 1,000.00 Section 25-5 of ITAA 97

Solicitor Fees $ 2,000.00 ATO ID 2002/814

Allowable Deduction $ 3,000.00

Table 1: Allowable Deduction

(Source: Created by Author)

Part C

The residential status of an individual is a question of fact and it is an important

criteria for determining the income tax liability of the individual. The term resident defined

under section 995-1 of the Income Tax Assessment Act 1997 indicates a person resident of

Australia for the purpose of tax. The section 6-1 of the Income Tax Assessment Act 1936

provides the definition of resident and highlights the primary test for deciding the residential

status of the individual (Hawkes et al. 2015). The Para 32 of the Taxation Ruling 98/17

states that the definition of resident provided under section 6-1 of the Income tax

Assessment Act 1936 provides four test of residency indicated below:

residential status according to the ordinary concept;

test for permanent place of abode;

183 days test; and

Superannuation fund test;

The taxpayer born and living in Australia is considered as resident for the purpose of tax

according to the ordinary concept. If an individual is not resident according to the ordinary

concept then the statutory test is applied for determining the residential status and if the

individual satisfied any one of primary test then the individual is regarded as resident. In

accordance with the domicile test if the individual has a permanent place of abode in

Particulars Amount Reason

Tax Agent fees $ 1,000.00 Section 25-5 of ITAA 97

Solicitor Fees $ 2,000.00 ATO ID 2002/814

Allowable Deduction $ 3,000.00

Table 1: Allowable Deduction

(Source: Created by Author)

Part C

The residential status of an individual is a question of fact and it is an important

criteria for determining the income tax liability of the individual. The term resident defined

under section 995-1 of the Income Tax Assessment Act 1997 indicates a person resident of

Australia for the purpose of tax. The section 6-1 of the Income Tax Assessment Act 1936

provides the definition of resident and highlights the primary test for deciding the residential

status of the individual (Hawkes et al. 2015). The Para 32 of the Taxation Ruling 98/17

states that the definition of resident provided under section 6-1 of the Income tax

Assessment Act 1936 provides four test of residency indicated below:

residential status according to the ordinary concept;

test for permanent place of abode;

183 days test; and

Superannuation fund test;

The taxpayer born and living in Australia is considered as resident for the purpose of tax

according to the ordinary concept. If an individual is not resident according to the ordinary

concept then the statutory test is applied for determining the residential status and if the

individual satisfied any one of primary test then the individual is regarded as resident. In

accordance with the domicile test if the individual has a permanent place of abode in

8TAX

Australia, then the individual is considered as resident for the tax purpose. The 183 days rule

states that if an individual resides in Australia for 183 days or more in a year then the

individual is regarded as resident for tax purpose. The superannuation test is applicable for

Australian government employees working overseas (Snape & De Souza 2016). The law

further provides that if an individual enrols for a course that has duration six months or more

then the student enrolling in the course is generally regarded as resident for the purpose of

tax. That means the student will have to pay tax on the earning as a resident Australian and is

required to declare earning from all the sources. In this case, Tina has arrived in Australia for

study and has stayed until 30 June during the year. It can be seen that as she has stayed in

Australia for 183 days or more so she is regarded as resident of Australia for the tax purpose.

Therefore, the income of $12000 earned by Tina is taxable.

Part D

In Australia, an individual is liable to pay tax on taxable income. The section 4-15 of

the Income Tax Assessment Act 1997 provides that taxable income is calculated by

subtracting allowable deductions from the assessable income. The Income tax laws classifies

assessable income as ordinary income under section 6-5 of the Income tax Assessment Act

1997 and the statutory income under section 6-10 of the Income tax Assessment Act 1997.

The section 6-5 of the ITAA 97 states that income according to the ordinary concept should

be treated as an ordinary income (Picciotto 2015). On the other, hand the income that is not

as ordinary income is statutory income under section 6-10 of the ITAA 97. It is provided in

both the section that for a resident taxpayer income from all the sources are taxable. That

means income earned by Jimmy working in the restaurant as a taxpayer is an ordinary income

under section 6-5 of the ITAA 97 and it is taxable. The tips received from customer is an

incentive from customer that is directly related to employment hence it is also taxable. The

Australia, then the individual is considered as resident for the tax purpose. The 183 days rule

states that if an individual resides in Australia for 183 days or more in a year then the

individual is regarded as resident for tax purpose. The superannuation test is applicable for

Australian government employees working overseas (Snape & De Souza 2016). The law

further provides that if an individual enrols for a course that has duration six months or more

then the student enrolling in the course is generally regarded as resident for the purpose of

tax. That means the student will have to pay tax on the earning as a resident Australian and is

required to declare earning from all the sources. In this case, Tina has arrived in Australia for

study and has stayed until 30 June during the year. It can be seen that as she has stayed in

Australia for 183 days or more so she is regarded as resident of Australia for the tax purpose.

Therefore, the income of $12000 earned by Tina is taxable.

Part D

In Australia, an individual is liable to pay tax on taxable income. The section 4-15 of

the Income Tax Assessment Act 1997 provides that taxable income is calculated by

subtracting allowable deductions from the assessable income. The Income tax laws classifies

assessable income as ordinary income under section 6-5 of the Income tax Assessment Act

1997 and the statutory income under section 6-10 of the Income tax Assessment Act 1997.

The section 6-5 of the ITAA 97 states that income according to the ordinary concept should

be treated as an ordinary income (Picciotto 2015). On the other, hand the income that is not

as ordinary income is statutory income under section 6-10 of the ITAA 97. It is provided in

both the section that for a resident taxpayer income from all the sources are taxable. That

means income earned by Jimmy working in the restaurant as a taxpayer is an ordinary income

under section 6-5 of the ITAA 97 and it is taxable. The tips received from customer is an

incentive from customer that is directly related to employment hence it is also taxable. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAX

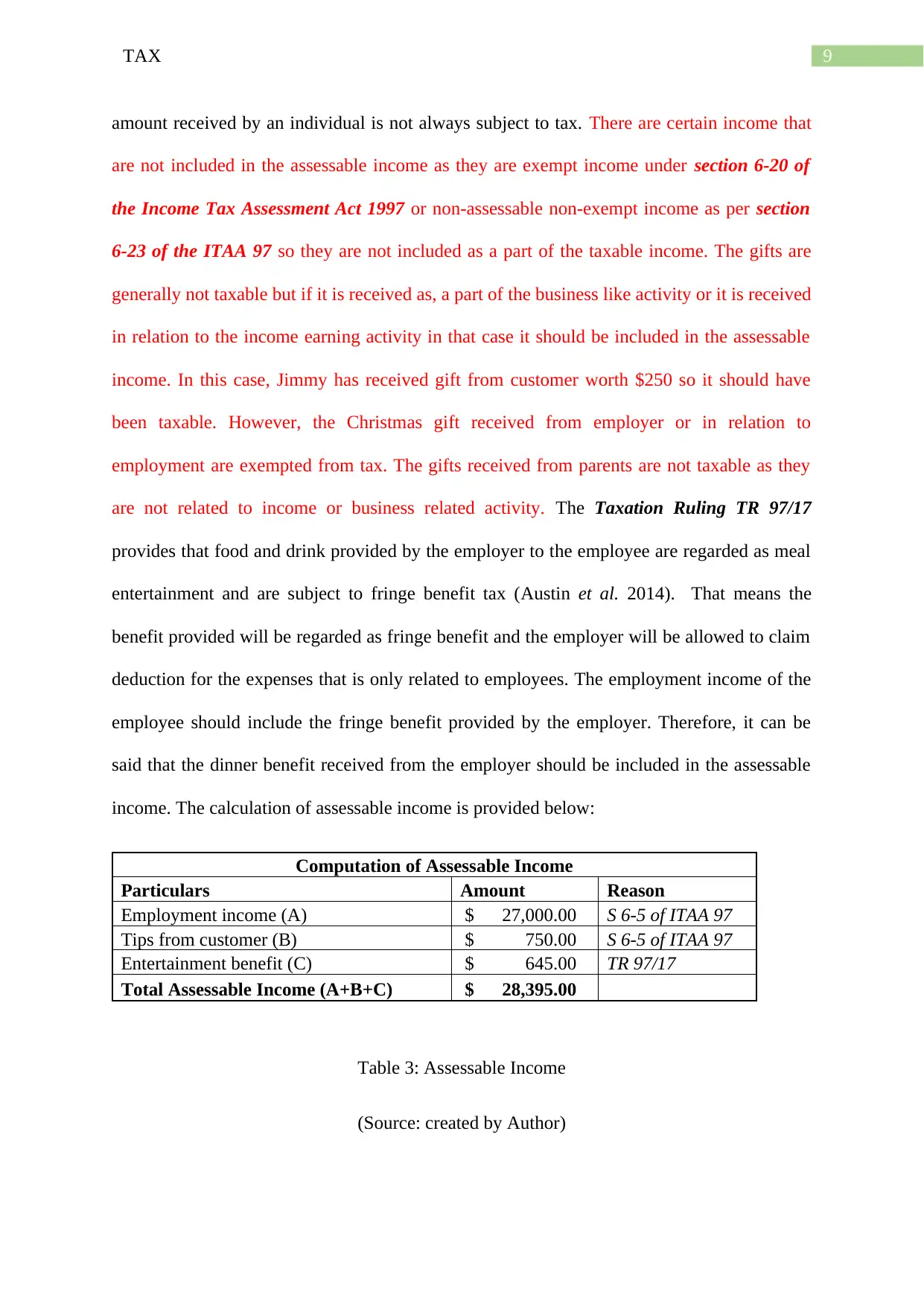

amount received by an individual is not always subject to tax. There are certain income that

are not included in the assessable income as they are exempt income under section 6-20 of

the Income Tax Assessment Act 1997 or non-assessable non-exempt income as per section

6-23 of the ITAA 97 so they are not included as a part of the taxable income. The gifts are

generally not taxable but if it is received as, a part of the business like activity or it is received

in relation to the income earning activity in that case it should be included in the assessable

income. In this case, Jimmy has received gift from customer worth $250 so it should have

been taxable. However, the Christmas gift received from employer or in relation to

employment are exempted from tax. The gifts received from parents are not taxable as they

are not related to income or business related activity. The Taxation Ruling TR 97/17

provides that food and drink provided by the employer to the employee are regarded as meal

entertainment and are subject to fringe benefit tax (Austin et al. 2014). That means the

benefit provided will be regarded as fringe benefit and the employer will be allowed to claim

deduction for the expenses that is only related to employees. The employment income of the

employee should include the fringe benefit provided by the employer. Therefore, it can be

said that the dinner benefit received from the employer should be included in the assessable

income. The calculation of assessable income is provided below:

Computation of Assessable Income

Particulars Amount Reason

Employment income (A) $ 27,000.00 S 6-5 of ITAA 97

Tips from customer (B) $ 750.00 S 6-5 of ITAA 97

Entertainment benefit (C) $ 645.00 TR 97/17

Total Assessable Income (A+B+C) $ 28,395.00

Table 3: Assessable Income

(Source: created by Author)

amount received by an individual is not always subject to tax. There are certain income that

are not included in the assessable income as they are exempt income under section 6-20 of

the Income Tax Assessment Act 1997 or non-assessable non-exempt income as per section

6-23 of the ITAA 97 so they are not included as a part of the taxable income. The gifts are

generally not taxable but if it is received as, a part of the business like activity or it is received

in relation to the income earning activity in that case it should be included in the assessable

income. In this case, Jimmy has received gift from customer worth $250 so it should have

been taxable. However, the Christmas gift received from employer or in relation to

employment are exempted from tax. The gifts received from parents are not taxable as they

are not related to income or business related activity. The Taxation Ruling TR 97/17

provides that food and drink provided by the employer to the employee are regarded as meal

entertainment and are subject to fringe benefit tax (Austin et al. 2014). That means the

benefit provided will be regarded as fringe benefit and the employer will be allowed to claim

deduction for the expenses that is only related to employees. The employment income of the

employee should include the fringe benefit provided by the employer. Therefore, it can be

said that the dinner benefit received from the employer should be included in the assessable

income. The calculation of assessable income is provided below:

Computation of Assessable Income

Particulars Amount Reason

Employment income (A) $ 27,000.00 S 6-5 of ITAA 97

Tips from customer (B) $ 750.00 S 6-5 of ITAA 97

Entertainment benefit (C) $ 645.00 TR 97/17

Total Assessable Income (A+B+C) $ 28,395.00

Table 3: Assessable Income

(Source: created by Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAX

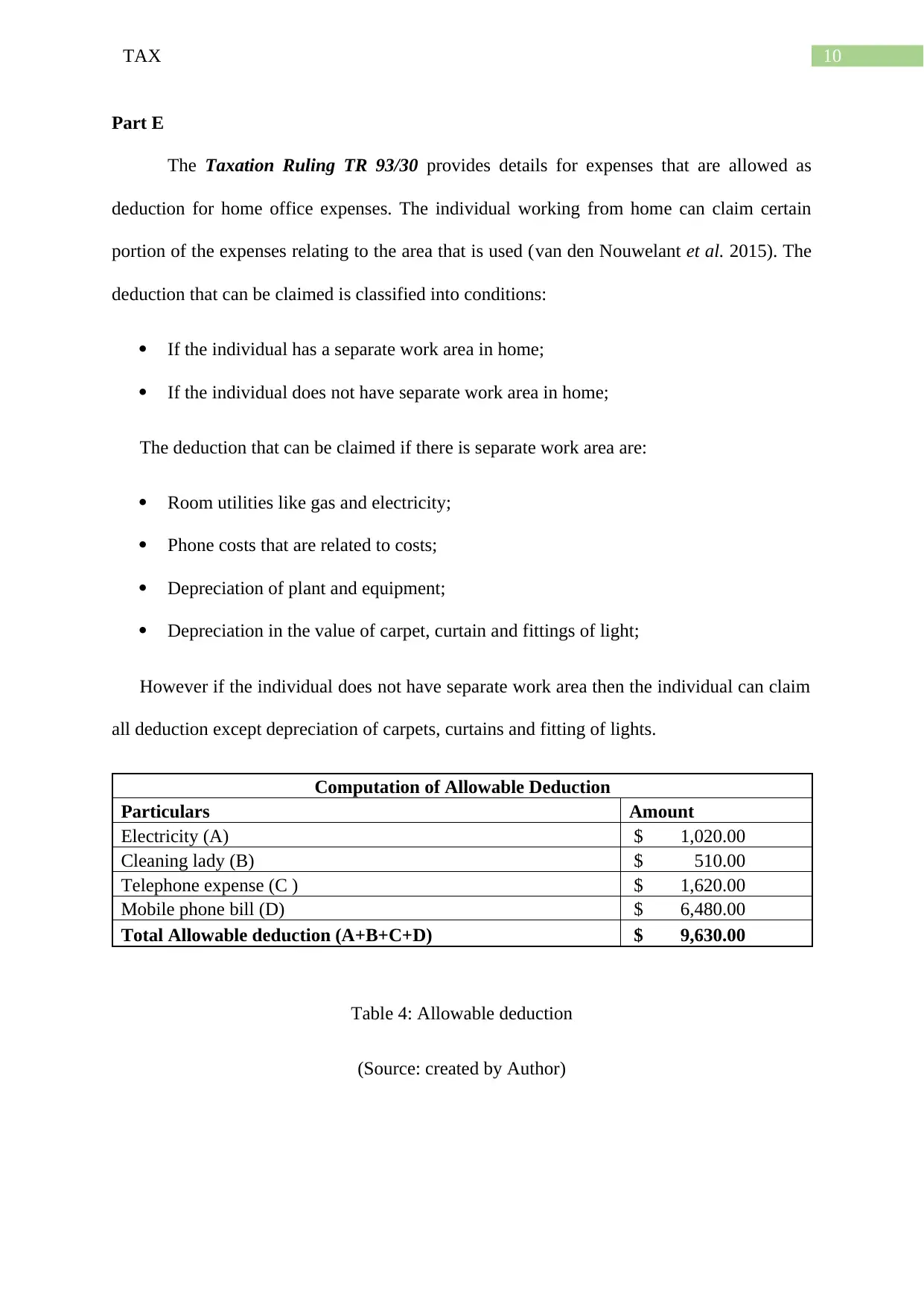

Part E

The Taxation Ruling TR 93/30 provides details for expenses that are allowed as

deduction for home office expenses. The individual working from home can claim certain

portion of the expenses relating to the area that is used (van den Nouwelant et al. 2015). The

deduction that can be claimed is classified into conditions:

If the individual has a separate work area in home;

If the individual does not have separate work area in home;

The deduction that can be claimed if there is separate work area are:

Room utilities like gas and electricity;

Phone costs that are related to costs;

Depreciation of plant and equipment;

Depreciation in the value of carpet, curtain and fittings of light;

However if the individual does not have separate work area then the individual can claim

all deduction except depreciation of carpets, curtains and fitting of lights.

Computation of Allowable Deduction

Particulars Amount

Electricity (A) $ 1,020.00

Cleaning lady (B) $ 510.00

Telephone expense (C ) $ 1,620.00

Mobile phone bill (D) $ 6,480.00

Total Allowable deduction (A+B+C+D) $ 9,630.00

Table 4: Allowable deduction

(Source: created by Author)

Part E

The Taxation Ruling TR 93/30 provides details for expenses that are allowed as

deduction for home office expenses. The individual working from home can claim certain

portion of the expenses relating to the area that is used (van den Nouwelant et al. 2015). The

deduction that can be claimed is classified into conditions:

If the individual has a separate work area in home;

If the individual does not have separate work area in home;

The deduction that can be claimed if there is separate work area are:

Room utilities like gas and electricity;

Phone costs that are related to costs;

Depreciation of plant and equipment;

Depreciation in the value of carpet, curtain and fittings of light;

However if the individual does not have separate work area then the individual can claim

all deduction except depreciation of carpets, curtains and fitting of lights.

Computation of Allowable Deduction

Particulars Amount

Electricity (A) $ 1,020.00

Cleaning lady (B) $ 510.00

Telephone expense (C ) $ 1,620.00

Mobile phone bill (D) $ 6,480.00

Total Allowable deduction (A+B+C+D) $ 9,630.00

Table 4: Allowable deduction

(Source: created by Author)

11TAX

Reference

Austin, P. M., Gurran, N., & Whitehead, C. M. (2014). Planning and affordable housing in

Australia, New Zealand and England: common culture; different mechanisms. Journal of

Housing and the Built Environment, 29(3), 455-472.

Borowski, A. (2013). Risky by design: The mandatory private pillar of Australia's retirement

income system. Social Policy & Administration, 47(6), 749-764.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cheshire, L., Everingham, J. A., & Lawrence, G. (2014). Governing the impacts of mining

and the impacts of mining governance: Challenges for rural and regional local governments

in Australia. Journal of Rural Studies, 36, 330-339.

Fitzsimons, J. A. (2015). Private protected areas in Australia: current status and future

directions. Nature Conservation, 10, 1.

Forsyth, P., Dwyer, L., Spurr, R., & Pham, T. (2014). The impacts of Australia's departure

tax: Tourism versus the economy?. Tourism Management, 40, 126-136.

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Hawkes, C., Smith, T. G., Jewell, J., Wardle, J., Hammond, R. A., Friel, S., ... & Kain, J.

(2015). Smart food policies for obesity prevention. The Lancet, 385(9985), 2410-2421.

Katic, P., & Leigh, A. (2016). Top wealth shares in Australia 1915–2012. Review of Income

and Wealth, 62(2), 209-222.

Reference

Austin, P. M., Gurran, N., & Whitehead, C. M. (2014). Planning and affordable housing in

Australia, New Zealand and England: common culture; different mechanisms. Journal of

Housing and the Built Environment, 29(3), 455-472.

Borowski, A. (2013). Risky by design: The mandatory private pillar of Australia's retirement

income system. Social Policy & Administration, 47(6), 749-764.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cheshire, L., Everingham, J. A., & Lawrence, G. (2014). Governing the impacts of mining

and the impacts of mining governance: Challenges for rural and regional local governments

in Australia. Journal of Rural Studies, 36, 330-339.

Fitzsimons, J. A. (2015). Private protected areas in Australia: current status and future

directions. Nature Conservation, 10, 1.

Forsyth, P., Dwyer, L., Spurr, R., & Pham, T. (2014). The impacts of Australia's departure

tax: Tourism versus the economy?. Tourism Management, 40, 126-136.

Gitman, L. J., Juchau, R., & Flanagan, J. (2015). Principles of managerial finance. Pearson

Higher Education AU.

Hawkes, C., Smith, T. G., Jewell, J., Wardle, J., Hammond, R. A., Friel, S., ... & Kain, J.

(2015). Smart food policies for obesity prevention. The Lancet, 385(9985), 2410-2421.

Katic, P., & Leigh, A. (2016). Top wealth shares in Australia 1915–2012. Review of Income

and Wealth, 62(2), 209-222.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.