King's Own Institute: BUS707 Article Review on Tax Avoidance in Trusts

VerifiedAdded on 2023/06/07

|10

|2556

|484

Report

AI Summary

This report presents a structured literature review on tax avoidance within family trusts, focusing on the Australian context. The analysis begins with a summary of the theory and the progression of the field, highlighting the historical development and current strategies used to minimize tax liabilities. The review then identifies and discusses common and differing themes across four academic articles, exploring topics such as the use of discretionary trusts, the impact of tax avoidance on revenue, and the role of family courts in asset distribution. The report also delves into managerial implications, such as how family companies strive to evade tax, and limitations of the research, including the unreliability of data and the complexity of tax laws. The report references articles that discuss the implications of tax avoidance, the role of trusts in estate planning, and government responses to tax avoidance, offering insights into the economic and social consequences of these practices. Finally, the report concludes with the analysis of the articles and their relation to the topic of tax avoidance and its impact on the Australian economy.

RUNNING HEADER: Applied business research

Applied business research

Name

Professor

Course

Date

1

Applied business research

Name

Professor

Course

Date

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RUNNING HEADER: Applied business research

Article review on tax avoidance in Family Trusts in Australia

Summary and progression of the field

Tax avoidance involves the legal utilization of tax in one territory to a person's benefit aimed art

decreasing the total amount of tax payable by methods which are within law jurisdictions.

Various forms of tax evasion are considered to be morally illegal. Many corporations, firms, and

business that participate in the practice are negatively impacted by active customers. Tax evasion

involves efforts by corporations, trusts, business and other entities to evade tax through the use

of illegal means. A business may decide to avoid theoretical means of paying taxes by

establishing the subsidiaries in an offshore trust (Amato 2012, p.637) Family tax evasion can be

done by creating a separate legal entity from the property or business owner. Assets are often

transferred to a new business so the t the gains realized or income generated can be within the

legal entity and not the individual owner. Tax avoidance assets back from 1696. However, over

the years, this theoretical approach has improved with governments coming up with strategies

and policies in order to curb tax avoidance techniques.

In this review the following four articles were extensively used to discuss the field in detail;

1. Bird, Robert, and Karie Davis-Nozemack. "Tax avoidance as a sustainability problem."

Journal of Business Ethics (2016): 1-17

2. Dowding, K. and Lewis, C., 2012. Newspaper reporting and changing perceptions of

ministerial accountability in Australia. Australian Journal of Politics & History, 58(2),

pp.236-250.

3. Mafrolla, E. and D'Amico, E., 2016. Tax aggressiveness in family firms and the non-

linear entrenchment effect. Journal of family business strategy, 7(3), pp.178-184.

4. Xynas, L., 2010. Tax planning, avoidance, and evasion in Australia 1970-2010: the

regulatory responses and taxpayer compliance. Revenue Law Journal, 20(2010), p.38.

Article Themes/findings

Over the years, People save money into self-managed super funds as a popular strategy used to

minimize tax, avoid tax and plan estates. Some of such particular options are shut down and the

2

Article review on tax avoidance in Family Trusts in Australia

Summary and progression of the field

Tax avoidance involves the legal utilization of tax in one territory to a person's benefit aimed art

decreasing the total amount of tax payable by methods which are within law jurisdictions.

Various forms of tax evasion are considered to be morally illegal. Many corporations, firms, and

business that participate in the practice are negatively impacted by active customers. Tax evasion

involves efforts by corporations, trusts, business and other entities to evade tax through the use

of illegal means. A business may decide to avoid theoretical means of paying taxes by

establishing the subsidiaries in an offshore trust (Amato 2012, p.637) Family tax evasion can be

done by creating a separate legal entity from the property or business owner. Assets are often

transferred to a new business so the t the gains realized or income generated can be within the

legal entity and not the individual owner. Tax avoidance assets back from 1696. However, over

the years, this theoretical approach has improved with governments coming up with strategies

and policies in order to curb tax avoidance techniques.

In this review the following four articles were extensively used to discuss the field in detail;

1. Bird, Robert, and Karie Davis-Nozemack. "Tax avoidance as a sustainability problem."

Journal of Business Ethics (2016): 1-17

2. Dowding, K. and Lewis, C., 2012. Newspaper reporting and changing perceptions of

ministerial accountability in Australia. Australian Journal of Politics & History, 58(2),

pp.236-250.

3. Mafrolla, E. and D'Amico, E., 2016. Tax aggressiveness in family firms and the non-

linear entrenchment effect. Journal of family business strategy, 7(3), pp.178-184.

4. Xynas, L., 2010. Tax planning, avoidance, and evasion in Australia 1970-2010: the

regulatory responses and taxpayer compliance. Revenue Law Journal, 20(2010), p.38.

Article Themes/findings

Over the years, People save money into self-managed super funds as a popular strategy used to

minimize tax, avoid tax and plan estates. Some of such particular options are shut down and the

2

RUNNING HEADER: Applied business research

Australian 2017 budget included various measures enacted to address some of the strategies and

challenges.

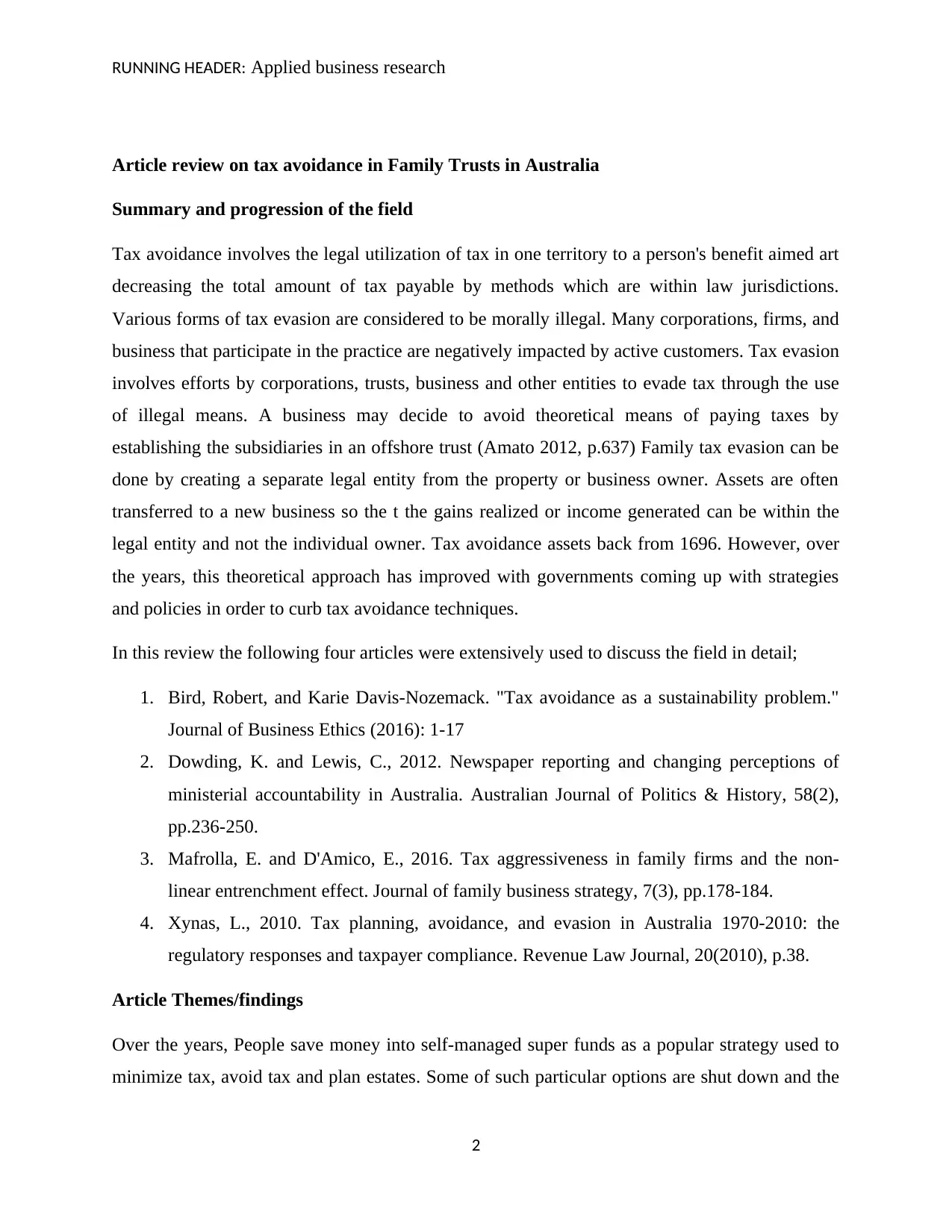

Fig 1.1 growth in trust

Various reason for setting up trusts include

Protection from divorce issues

High discretion in the case of trust capital and income being distributed to the available

beneficiaries. The latter involves the actual splitting between two trust beneficiaries. While

policies against avoidance are being applauded by the authorities in charge, it doesn't mean that

tax avoiders will find other channels of avoiding if not evading tax. The Australian Taxation

Office indicates a variety of arrangements that are aggressive towards the tax system

Avoidance of tax and other obligations completely.

Optimized rebates

A rise in the income deductions per month

Reduction of the family member's taxable income

Literally, there is little to do in commending discretionary trusts. The merits they bring are

minimal since many are limited by their existing destructive and damaging nature or features.

3

Australian 2017 budget included various measures enacted to address some of the strategies and

challenges.

Fig 1.1 growth in trust

Various reason for setting up trusts include

Protection from divorce issues

High discretion in the case of trust capital and income being distributed to the available

beneficiaries. The latter involves the actual splitting between two trust beneficiaries. While

policies against avoidance are being applauded by the authorities in charge, it doesn't mean that

tax avoiders will find other channels of avoiding if not evading tax. The Australian Taxation

Office indicates a variety of arrangements that are aggressive towards the tax system

Avoidance of tax and other obligations completely.

Optimized rebates

A rise in the income deductions per month

Reduction of the family member's taxable income

Literally, there is little to do in commending discretionary trusts. The merits they bring are

minimal since many are limited by their existing destructive and damaging nature or features.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RUNNING HEADER: Applied business research

According to the article by Bird, Robert, & Karie Davis (2016, p.2-3), trusts are typically utilized

to give money to members of a particular group, normally a family. Under a discretionary trust,

the only available channel a beneficiary will acquire capital or monthly income from the trust is

if the person who is a trustee decides to offer them something in return. Family organizations are

usually included as beneficiaries in order to optimize tax.

The labor party puts high consideration on trusts. This focus is overwhelmingly warranted since

the purpose of trusts is to reduce tax, avoid paying creditors and avoiding the fair share of

property after family relationships have broken down.

As a result of a lack of data, it is quite difficult to approximate the total amount of tax revenue

that is lost in the modern era. However, an estimate of simply losing a$2.1 billion annually in the

income tax through available discretionary trust can be ultimately done.

If a discretionary trust decides to a family trust under the new tax law, it can also lead easily

access various concessional tax rules. These do not exist in any other entities or taxpayers

(Dwyer 2010, p.23)

Discretionary family trust issued largely to frustrate creditors who are individuals that are owned

by the beneficiaries of a trust. A person who is owed money by a certain beneficiary of the trust

cannot make an effort to visit trust or tax authorities so as to settle the prevailing debt. Also even

if the beneficiary has gotten money from the trust initially and there is a high likelihood that

he/she can receive the money in the long run, after releasing from bankruptcy situation which

means not having paid any of their debts.

Unsecured creditors such as suppliers of a family business transacting with a trustee, cannot

settle their debts completely with a trust in case the trustee does not have enough funds in form

of assets. The trustee will mostly be a family company paid to coordinate the trust with less share

of income capital

According to Dowding, K. and Lewis, C., (2012, p.236) indicates reliable data from the

Australian Taxation office, shows that family wealth is held in existing discretionary trusts. Once

a family relationship breaks, one spouse will argue that since the asset funds are in discretionary

trust, nobody has prior claim over them and therefore it would be divided among the rest of the

4

According to the article by Bird, Robert, & Karie Davis (2016, p.2-3), trusts are typically utilized

to give money to members of a particular group, normally a family. Under a discretionary trust,

the only available channel a beneficiary will acquire capital or monthly income from the trust is

if the person who is a trustee decides to offer them something in return. Family organizations are

usually included as beneficiaries in order to optimize tax.

The labor party puts high consideration on trusts. This focus is overwhelmingly warranted since

the purpose of trusts is to reduce tax, avoid paying creditors and avoiding the fair share of

property after family relationships have broken down.

As a result of a lack of data, it is quite difficult to approximate the total amount of tax revenue

that is lost in the modern era. However, an estimate of simply losing a$2.1 billion annually in the

income tax through available discretionary trust can be ultimately done.

If a discretionary trust decides to a family trust under the new tax law, it can also lead easily

access various concessional tax rules. These do not exist in any other entities or taxpayers

(Dwyer 2010, p.23)

Discretionary family trust issued largely to frustrate creditors who are individuals that are owned

by the beneficiaries of a trust. A person who is owed money by a certain beneficiary of the trust

cannot make an effort to visit trust or tax authorities so as to settle the prevailing debt. Also even

if the beneficiary has gotten money from the trust initially and there is a high likelihood that

he/she can receive the money in the long run, after releasing from bankruptcy situation which

means not having paid any of their debts.

Unsecured creditors such as suppliers of a family business transacting with a trustee, cannot

settle their debts completely with a trust in case the trustee does not have enough funds in form

of assets. The trustee will mostly be a family company paid to coordinate the trust with less share

of income capital

According to Dowding, K. and Lewis, C., (2012, p.236) indicates reliable data from the

Australian Taxation office, shows that family wealth is held in existing discretionary trusts. Once

a family relationship breaks, one spouse will argue that since the asset funds are in discretionary

trust, nobody has prior claim over them and therefore it would be divided among the rest of the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RUNNING HEADER: Applied business research

other couples assets. This gives a way of avoiding paying taxes to the relevant Australian

authority.

The family court has more power to choose what can be shared and it normally includes assets

that represent in the discretionary trusts. This is done in case a specific spouse is capable of

appointing or removing a trustee. Conversely, in an instance where a spouse is expelled from the

trust funds, it becomes very problematic for the court to include assets to be shared and pay

taxes.

The trust can also be used in succession planning leading to tax avoidance. This is where an

individual has property to discard and needs flexibility over a given period of time. It permits the

payments to change with demand, needs, and circumstances. For instance, if a trust beneficiary

gets a well-paying job, they could be given less thus leading to tax evasion (Mafrolla & D'Amico

2016, p.178).

Also in the cases of death, putting assets into the discretionary trust of a deceased individual

makes the assets to be tied up for over a maximum of approximately 80years. This will make it

difficult for the assets to contribute to the countries tax.

Findings in Numbers

According to the articles in 2014, there existed approximately 823,447 trusts with assets

estimated to be $3.1 trilkion.78 percent of the trust were discretionary trusts that reused by the

individual who sets up the trust funds.

5

other couples assets. This gives a way of avoiding paying taxes to the relevant Australian

authority.

The family court has more power to choose what can be shared and it normally includes assets

that represent in the discretionary trusts. This is done in case a specific spouse is capable of

appointing or removing a trustee. Conversely, in an instance where a spouse is expelled from the

trust funds, it becomes very problematic for the court to include assets to be shared and pay

taxes.

The trust can also be used in succession planning leading to tax avoidance. This is where an

individual has property to discard and needs flexibility over a given period of time. It permits the

payments to change with demand, needs, and circumstances. For instance, if a trust beneficiary

gets a well-paying job, they could be given less thus leading to tax evasion (Mafrolla & D'Amico

2016, p.178).

Also in the cases of death, putting assets into the discretionary trust of a deceased individual

makes the assets to be tied up for over a maximum of approximately 80years. This will make it

difficult for the assets to contribute to the countries tax.

Findings in Numbers

According to the articles in 2014, there existed approximately 823,447 trusts with assets

estimated to be $3.1 trilkion.78 percent of the trust were discretionary trusts that reused by the

individual who sets up the trust funds.

5

RUNNING HEADER: Applied business research

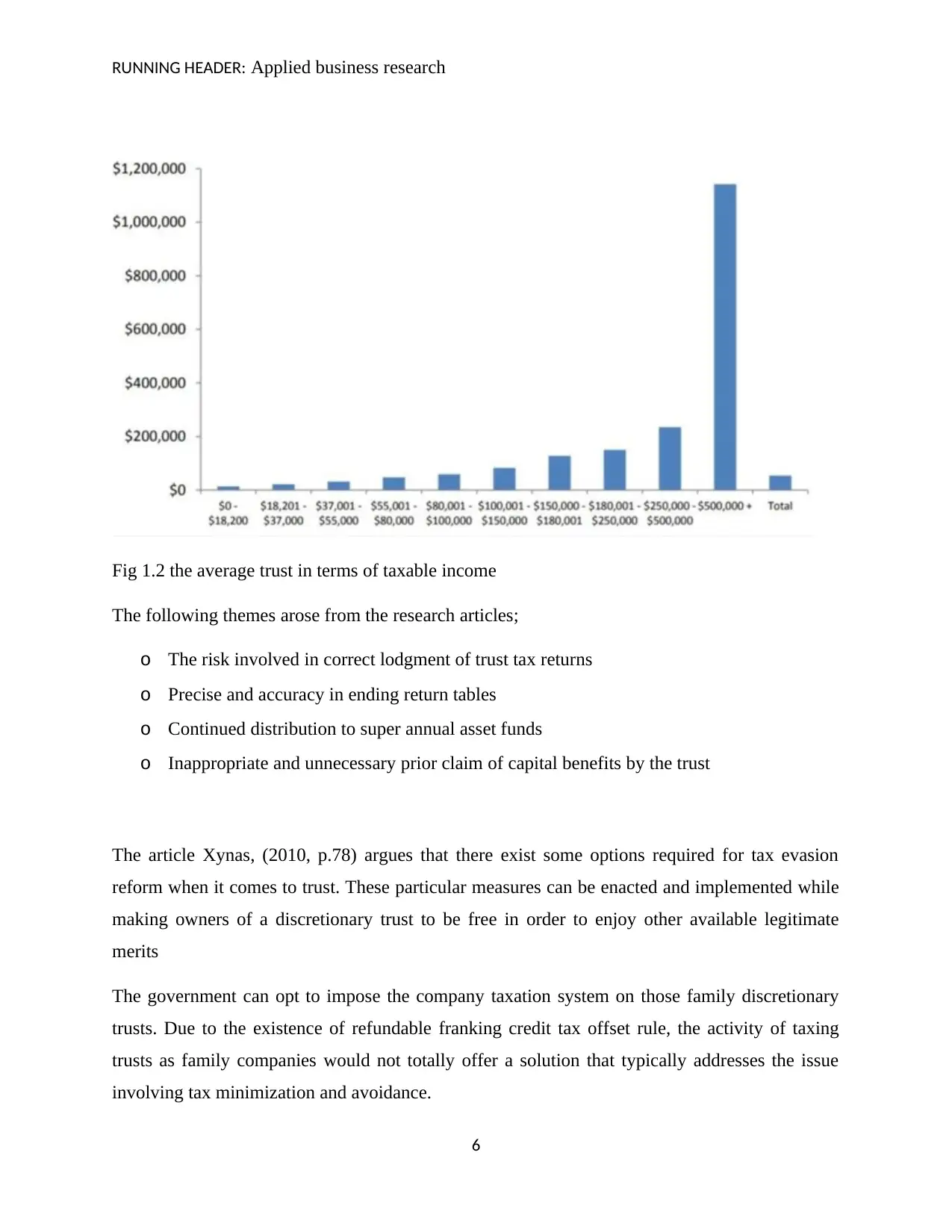

Fig 1.2 the average trust in terms of taxable income

The following themes arose from the research articles;

o The risk involved in correct lodgment of trust tax returns

o Precise and accuracy in ending return tables

o Continued distribution to super annual asset funds

o Inappropriate and unnecessary prior claim of capital benefits by the trust

The article Xynas, (2010, p.78) argues that there exist some options required for tax evasion

reform when it comes to trust. These particular measures can be enacted and implemented while

making owners of a discretionary trust to be free in order to enjoy other available legitimate

merits

The government can opt to impose the company taxation system on those family discretionary

trusts. Due to the existence of refundable franking credit tax offset rule, the activity of taxing

trusts as family companies would not totally offer a solution that typically addresses the issue

involving tax minimization and avoidance.

6

Fig 1.2 the average trust in terms of taxable income

The following themes arose from the research articles;

o The risk involved in correct lodgment of trust tax returns

o Precise and accuracy in ending return tables

o Continued distribution to super annual asset funds

o Inappropriate and unnecessary prior claim of capital benefits by the trust

The article Xynas, (2010, p.78) argues that there exist some options required for tax evasion

reform when it comes to trust. These particular measures can be enacted and implemented while

making owners of a discretionary trust to be free in order to enjoy other available legitimate

merits

The government can opt to impose the company taxation system on those family discretionary

trusts. Due to the existence of refundable franking credit tax offset rule, the activity of taxing

trusts as family companies would not totally offer a solution that typically addresses the issue

involving tax minimization and avoidance.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RUNNING HEADER: Applied business research

This is because trusts would still have the capability to offer manipulations in the allocations of

money between low-rate beneficiaries. They will be able to change allocations from time to time

and avoid paying tax annually (Richardson, Taylor, & Lanis 2015.,p.44)On the other hand it

would achieve a goal of removing the presence of the capital gains tax discount to the family

discretionary trust

The Australian government can utilize the attribution methodological approach to trust. This is

the same manner that social security systems do in effectively implementing the family law

(Amato 2012, p.637). Under this model, the family member who immensely contributes the asset

in the trust is seen to have ownership of the monthly income and asset funds. This perspective

would highly reflect typical law entitlements for all the spouses and thus reflect their economic

contributions in order to build upon assets. This would make the tax authority to keep track of

the taxable income.

Future research indicates that given the complexity of the laws in Australian income tax and the

prevailing enforcement rules that constitute the Australian Taxation office in various dimensions,

any challenges with this approach are simply solved. It forms the ideal sections of the social

security regime for available asset funds and income test that are needed for one to pay tax and

not evade (Prebble & Prebble, 2010, p.21).

The articles bring out the theme of negative gearing. Those individuals who are in the top

income brackets benefit from carrying out investment strategies like negative gearing. It works

efficiently where taxpayer gets in the high marginal tax bracket. Some individuals have the

ability to legally decrease their income under assessment by income diversion.

The articles also bring out the themes of tax reform, anti-avoidance provisions and tax

compliance aimed at promoting the payment of taxes

Managerial implications

Some of the managerial implications include how family companies dealing with high-quality

products strive to evade tax so as to save capital in order to promote their customer satisfaction.

However, this has been considered unethical behavior since it can lead to the downfall of the

7

This is because trusts would still have the capability to offer manipulations in the allocations of

money between low-rate beneficiaries. They will be able to change allocations from time to time

and avoid paying tax annually (Richardson, Taylor, & Lanis 2015.,p.44)On the other hand it

would achieve a goal of removing the presence of the capital gains tax discount to the family

discretionary trust

The Australian government can utilize the attribution methodological approach to trust. This is

the same manner that social security systems do in effectively implementing the family law

(Amato 2012, p.637). Under this model, the family member who immensely contributes the asset

in the trust is seen to have ownership of the monthly income and asset funds. This perspective

would highly reflect typical law entitlements for all the spouses and thus reflect their economic

contributions in order to build upon assets. This would make the tax authority to keep track of

the taxable income.

Future research indicates that given the complexity of the laws in Australian income tax and the

prevailing enforcement rules that constitute the Australian Taxation office in various dimensions,

any challenges with this approach are simply solved. It forms the ideal sections of the social

security regime for available asset funds and income test that are needed for one to pay tax and

not evade (Prebble & Prebble, 2010, p.21).

The articles bring out the theme of negative gearing. Those individuals who are in the top

income brackets benefit from carrying out investment strategies like negative gearing. It works

efficiently where taxpayer gets in the high marginal tax bracket. Some individuals have the

ability to legally decrease their income under assessment by income diversion.

The articles also bring out the themes of tax reform, anti-avoidance provisions and tax

compliance aimed at promoting the payment of taxes

Managerial implications

Some of the managerial implications include how family companies dealing with high-quality

products strive to evade tax so as to save capital in order to promote their customer satisfaction.

However, this has been considered unethical behavior since it can lead to the downfall of the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RUNNING HEADER: Applied business research

entire company management when the Australian law catches up with that behavior (Woellner,

Barkoczy, Murphy, Evans, Pinto, 2010, p.118).

Failure to pay taxes will lead to failure of business since government always support them with

subsidies and incentives. It will also have real-world negative implications in the entire

economy.

Limitations

The articles indicate that trust does not have the capability of capital distribution or revenue

losses to its beneficiaries. In case a trust leads to losses the beneficiaries will not be able to offset

the loss against any taxable income.

The articles indicate that from time to time concerns arise on if the tax avoidance rules apply to

all family trust that is used in taxable income splitting objectives. It is highly unlikely that anti-

tax avoidance rules will apply to commercial and family business dealings. Individuals involved

in business or investment operations will not be affected (Taylor & Richardson, 2013, p.12). A

larger percentage of researchers and advisors argue that trust arrangements are not within tax

avoidance rule, provided that there exist normal commercial reasons for instance asset fun

protection and maximal estate planning. The articles, therefore, indicate that future research is

limited to one dimension. Data and information regarding tax avoidance will be unreliable and

exaggerated. Future research does not account for offering the solutions for end of tax avoidance

8

entire company management when the Australian law catches up with that behavior (Woellner,

Barkoczy, Murphy, Evans, Pinto, 2010, p.118).

Failure to pay taxes will lead to failure of business since government always support them with

subsidies and incentives. It will also have real-world negative implications in the entire

economy.

Limitations

The articles indicate that trust does not have the capability of capital distribution or revenue

losses to its beneficiaries. In case a trust leads to losses the beneficiaries will not be able to offset

the loss against any taxable income.

The articles indicate that from time to time concerns arise on if the tax avoidance rules apply to

all family trust that is used in taxable income splitting objectives. It is highly unlikely that anti-

tax avoidance rules will apply to commercial and family business dealings. Individuals involved

in business or investment operations will not be affected (Taylor & Richardson, 2013, p.12). A

larger percentage of researchers and advisors argue that trust arrangements are not within tax

avoidance rule, provided that there exist normal commercial reasons for instance asset fun

protection and maximal estate planning. The articles, therefore, indicate that future research is

limited to one dimension. Data and information regarding tax avoidance will be unreliable and

exaggerated. Future research does not account for offering the solutions for end of tax avoidance

8

RUNNING HEADER: Applied business research

References

Amato, D.J., 2012. The Good, the Bad, and the Ugly: The Political Economy and Unintended

Consequences of Perpetual Trusts. S. Cal. L. Rev., 86, p.637.

Bird, Robert, and Karie Davis-Nozemack. "Tax avoidance as a sustainability problem." Journal

of Business Ethics (2016): 1-17.

Dowding, K. and Lewis, C., 2012. Newspaper reporting and changing perceptions of ministerial

accountability in Australia. Australian Journal of Politics & History, 58(2), pp.236-250.

Dwyer, T., 2010. The taxation of shared family incomes. About this issue, p.23.

Mafrolla, E. and D'Amico, E., 2016. Tax aggressiveness in family firms and the non-linear

entrenchment effect. Journal of family business strategy, 7(3), pp.178-184.

Prebble, R. and Prebble, J., 2010. Does the use of general anti-avoidance rules to combat tax

avoidance breach principles of the rule of law-a comparative study. Louis ULJ, 55, p.21.

Richardson, G., Taylor, G., and Lanis, R., 2015. The impact of financial distress on corporate tax

avoidance spanning the global financial crisis: Evidence from Australia. Economic Modelling,

44, pp.44-53.

Richardson, G., Taylor, G., and Lanis, R., 2015. The impact of financial distress on corporate tax

avoidance spanning the global financial crisis: Evidence from Australia. Economic Modelling,

44, pp.44-53.

Taylor, G. and Richardson, G., 2013. The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting, Auditing, and

Taxation, 22(1), pp.12-25.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2010. Australian taxation

law. CCH Australia.

9

References

Amato, D.J., 2012. The Good, the Bad, and the Ugly: The Political Economy and Unintended

Consequences of Perpetual Trusts. S. Cal. L. Rev., 86, p.637.

Bird, Robert, and Karie Davis-Nozemack. "Tax avoidance as a sustainability problem." Journal

of Business Ethics (2016): 1-17.

Dowding, K. and Lewis, C., 2012. Newspaper reporting and changing perceptions of ministerial

accountability in Australia. Australian Journal of Politics & History, 58(2), pp.236-250.

Dwyer, T., 2010. The taxation of shared family incomes. About this issue, p.23.

Mafrolla, E. and D'Amico, E., 2016. Tax aggressiveness in family firms and the non-linear

entrenchment effect. Journal of family business strategy, 7(3), pp.178-184.

Prebble, R. and Prebble, J., 2010. Does the use of general anti-avoidance rules to combat tax

avoidance breach principles of the rule of law-a comparative study. Louis ULJ, 55, p.21.

Richardson, G., Taylor, G., and Lanis, R., 2015. The impact of financial distress on corporate tax

avoidance spanning the global financial crisis: Evidence from Australia. Economic Modelling,

44, pp.44-53.

Richardson, G., Taylor, G., and Lanis, R., 2015. The impact of financial distress on corporate tax

avoidance spanning the global financial crisis: Evidence from Australia. Economic Modelling,

44, pp.44-53.

Taylor, G. and Richardson, G., 2013. The determinants of thinly capitalized tax avoidance

structures: Evidence from Australian firms. Journal of International Accounting, Auditing, and

Taxation, 22(1), pp.12-25.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2010. Australian taxation

law. CCH Australia.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RUNNING HEADER: Applied business research

Xynas, L., 2010. Tax planning, avoidance, and evasion in Australia 1970-2010: the regulatory

responses and taxpayer compliance. Revenue Law Journal, 20(2010), p.38.

Xynas, L., 2011. Tax Planning, Avoidance and Evasion in Australia 1970-2010: The Regulatory

Responses and Taxpayer Compliance. Revenue Law Journal, 20(1), p.2.

10

Xynas, L., 2010. Tax planning, avoidance, and evasion in Australia 1970-2010: the regulatory

responses and taxpayer compliance. Revenue Law Journal, 20(2010), p.38.

Xynas, L., 2011. Tax Planning, Avoidance and Evasion in Australia 1970-2010: The Regulatory

Responses and Taxpayer Compliance. Revenue Law Journal, 20(1), p.2.

10

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.