PTAX5037 Spring 2019: Principles of Taxation Report Analysis

VerifiedAdded on 2023/04/24

|14

|2680

|263

Report

AI Summary

This report provides a comprehensive overview of the principles of taxation, focusing on the UK tax system. It begins by comparing and contrasting progressive and regressive taxation systems, providing examples to illustrate their differences. The report then delves into the sources of tax law in the UK, identifying key legislation and the role of the HMRC. Furthermore, it examines the concepts of tax avoidance and tax evasion, differentiating between the two and providing practical examples to highlight their implications. The analysis includes a discussion of marginal tax rates, tax thresholds, and the application of different tax rates based on income levels. The report also touches upon the impact of EU membership and court precedents on UK tax law. Finally, it explores government initiatives aimed at preventing tax evasion and avoidance, such as the introduction of the Google tax and the criminalization of assisting tax evasion. The report provides a detailed understanding of the UK tax framework and its practical applications.

Running head: PRINCIPLES OF TAXATION

Principles of Taxation

Name of the Student

Name of the University

Author Note

Principles of Taxation

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PRINCIPLES OF TAXATION

Introduction

The tax laws in the UK comprises of payments of tax to the three levels of the

Government namely, the central Government, the Local Government and the devolved

Government. This paper will present a comparison and contrast of the progressive taxation

system and the regressive taxation system by providing examples. It will strive to analyse the

sources of tax law in the UK, considering that the basic rules of the UK tax system have been

established from several sources. This paper will also present a comparison and contrast with

respect to the tax avoidance and tax evasion by providing practical examples.

Introduction

The tax laws in the UK comprises of payments of tax to the three levels of the

Government namely, the central Government, the Local Government and the devolved

Government. This paper will present a comparison and contrast of the progressive taxation

system and the regressive taxation system by providing examples. It will strive to analyse the

sources of tax law in the UK, considering that the basic rules of the UK tax system have been

established from several sources. This paper will also present a comparison and contrast with

respect to the tax avoidance and tax evasion by providing practical examples.

2PRINCIPLES OF TAXATION

Main body

Progressive Taxation System and Regressive Taxation System

The tax in which the average rate of tax increases with the increase in the amount taxable

is referred to as a progressive tax (Pizer and Sexton 2019). Whereas, in case of regressive tax,

the average rate of tax decreases with an increase in the taxable amount. The computation of

the average tax rate is done by dividing the taxes paid by the personal income earned and

subjected to taxation. Regressive tax system is applied in a uniform manner in contrast with

the progressive tax system, which is not uniform in its application. The regressive tax system

imposes an increased rate of tax over the lower income group and a diminished rate of tax

over the higher income group. In case of regressive tax structure, the rate of tax and the

capacity of the taxpayers or the taxable income varies inversely with each other (Mahler and

Jesuit 2018). Whereas, the progressive tax structure presents a direct proportion of the rate of

tax with the capacity of the taxpayers or the taxable income (Atkinson et al. 2017).

Most of the tax regimes in the world follows the progressive aspect with respect to

taxation. This system imposes a higher percentage of tax upon an individual with the higher

income.

Main body

Progressive Taxation System and Regressive Taxation System

The tax in which the average rate of tax increases with the increase in the amount taxable

is referred to as a progressive tax (Pizer and Sexton 2019). Whereas, in case of regressive tax,

the average rate of tax decreases with an increase in the taxable amount. The computation of

the average tax rate is done by dividing the taxes paid by the personal income earned and

subjected to taxation. Regressive tax system is applied in a uniform manner in contrast with

the progressive tax system, which is not uniform in its application. The regressive tax system

imposes an increased rate of tax over the lower income group and a diminished rate of tax

over the higher income group. In case of regressive tax structure, the rate of tax and the

capacity of the taxpayers or the taxable income varies inversely with each other (Mahler and

Jesuit 2018). Whereas, the progressive tax structure presents a direct proportion of the rate of

tax with the capacity of the taxpayers or the taxable income (Atkinson et al. 2017).

Most of the tax regimes in the world follows the progressive aspect with respect to

taxation. This system imposes a higher percentage of tax upon an individual with the higher

income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PRINCIPLES OF TAXATION

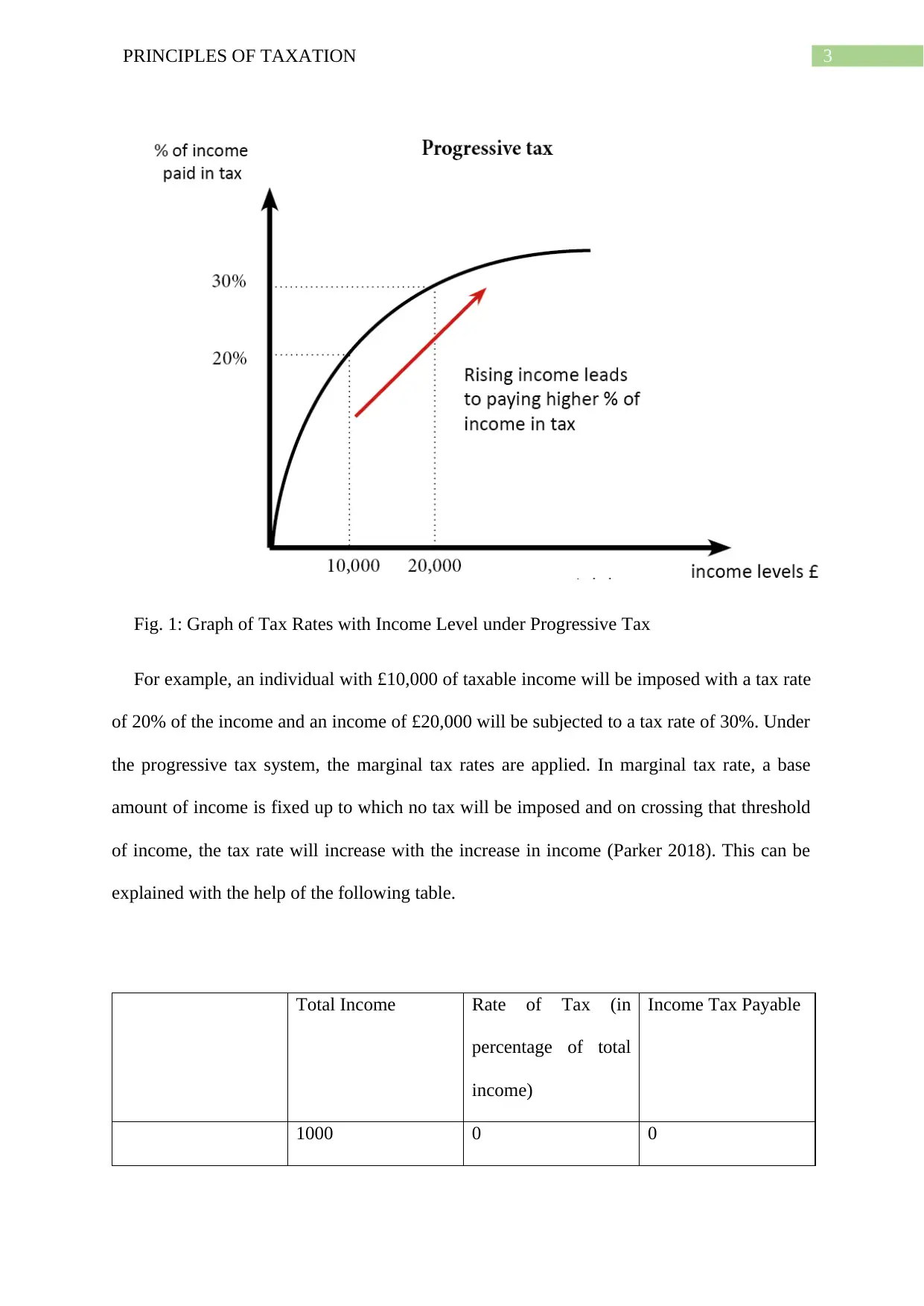

Fig. 1: Graph of Tax Rates with Income Level under Progressive Tax

For example, an individual with £10,000 of taxable income will be imposed with a tax rate

of 20% of the income and an income of £20,000 will be subjected to a tax rate of 30%. Under

the progressive tax system, the marginal tax rates are applied. In marginal tax rate, a base

amount of income is fixed up to which no tax will be imposed and on crossing that threshold

of income, the tax rate will increase with the increase in income (Parker 2018). This can be

explained with the help of the following table.

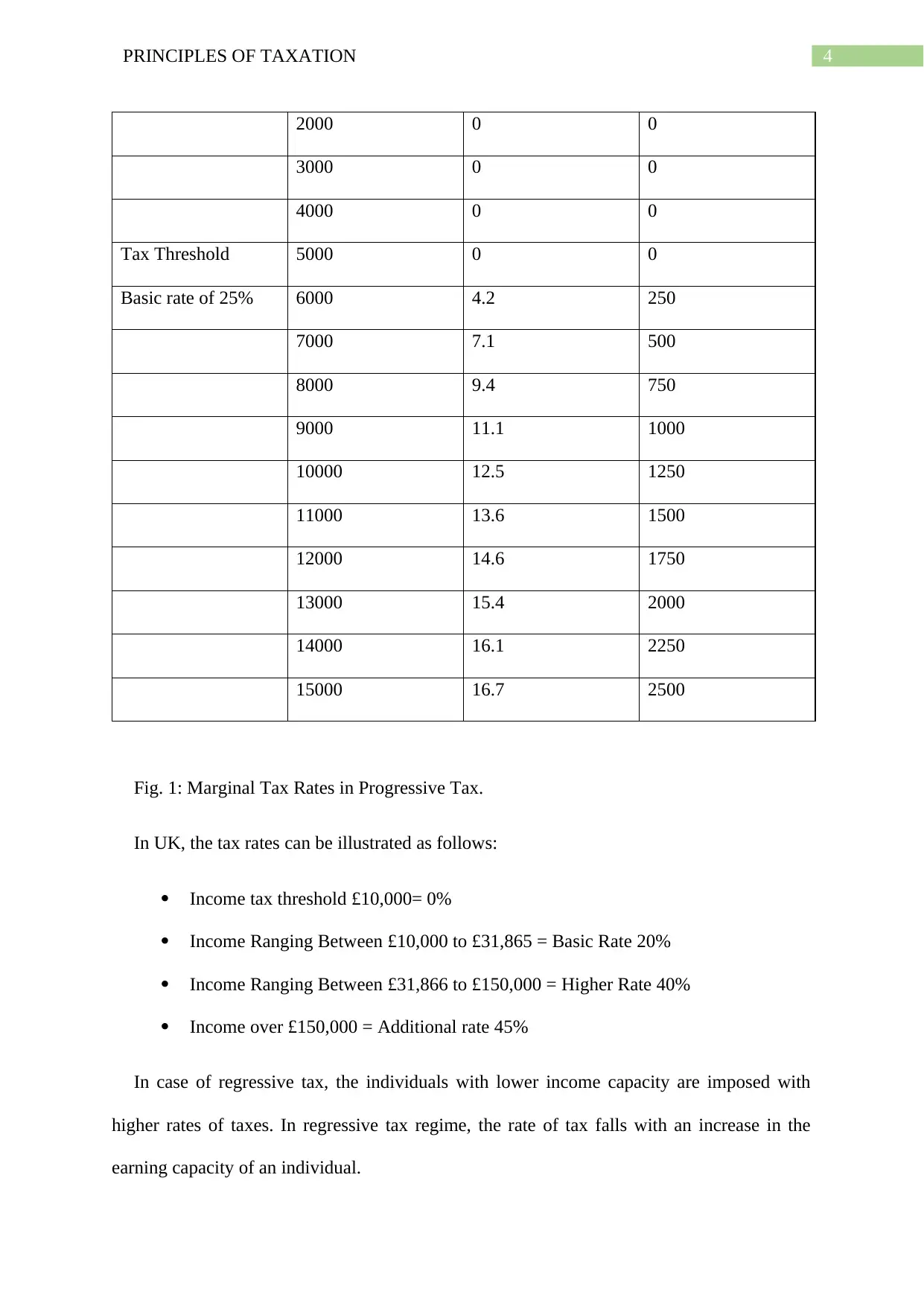

Total Income Rate of Tax (in

percentage of total

income)

Income Tax Payable

1000 0 0

Fig. 1: Graph of Tax Rates with Income Level under Progressive Tax

For example, an individual with £10,000 of taxable income will be imposed with a tax rate

of 20% of the income and an income of £20,000 will be subjected to a tax rate of 30%. Under

the progressive tax system, the marginal tax rates are applied. In marginal tax rate, a base

amount of income is fixed up to which no tax will be imposed and on crossing that threshold

of income, the tax rate will increase with the increase in income (Parker 2018). This can be

explained with the help of the following table.

Total Income Rate of Tax (in

percentage of total

income)

Income Tax Payable

1000 0 0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4PRINCIPLES OF TAXATION

2000 0 0

3000 0 0

4000 0 0

Tax Threshold 5000 0 0

Basic rate of 25% 6000 4.2 250

7000 7.1 500

8000 9.4 750

9000 11.1 1000

10000 12.5 1250

11000 13.6 1500

12000 14.6 1750

13000 15.4 2000

14000 16.1 2250

15000 16.7 2500

Fig. 1: Marginal Tax Rates in Progressive Tax.

In UK, the tax rates can be illustrated as follows:

Income tax threshold £10,000= 0%

Income Ranging Between £10,000 to £31,865 = Basic Rate 20%

Income Ranging Between £31,866 to £150,000 = Higher Rate 40%

Income over £150,000 = Additional rate 45%

In case of regressive tax, the individuals with lower income capacity are imposed with

higher rates of taxes. In regressive tax regime, the rate of tax falls with an increase in the

earning capacity of an individual.

2000 0 0

3000 0 0

4000 0 0

Tax Threshold 5000 0 0

Basic rate of 25% 6000 4.2 250

7000 7.1 500

8000 9.4 750

9000 11.1 1000

10000 12.5 1250

11000 13.6 1500

12000 14.6 1750

13000 15.4 2000

14000 16.1 2250

15000 16.7 2500

Fig. 1: Marginal Tax Rates in Progressive Tax.

In UK, the tax rates can be illustrated as follows:

Income tax threshold £10,000= 0%

Income Ranging Between £10,000 to £31,865 = Basic Rate 20%

Income Ranging Between £31,866 to £150,000 = Higher Rate 40%

Income over £150,000 = Additional rate 45%

In case of regressive tax, the individuals with lower income capacity are imposed with

higher rates of taxes. In regressive tax regime, the rate of tax falls with an increase in the

earning capacity of an individual.

5PRINCIPLES OF TAXATION

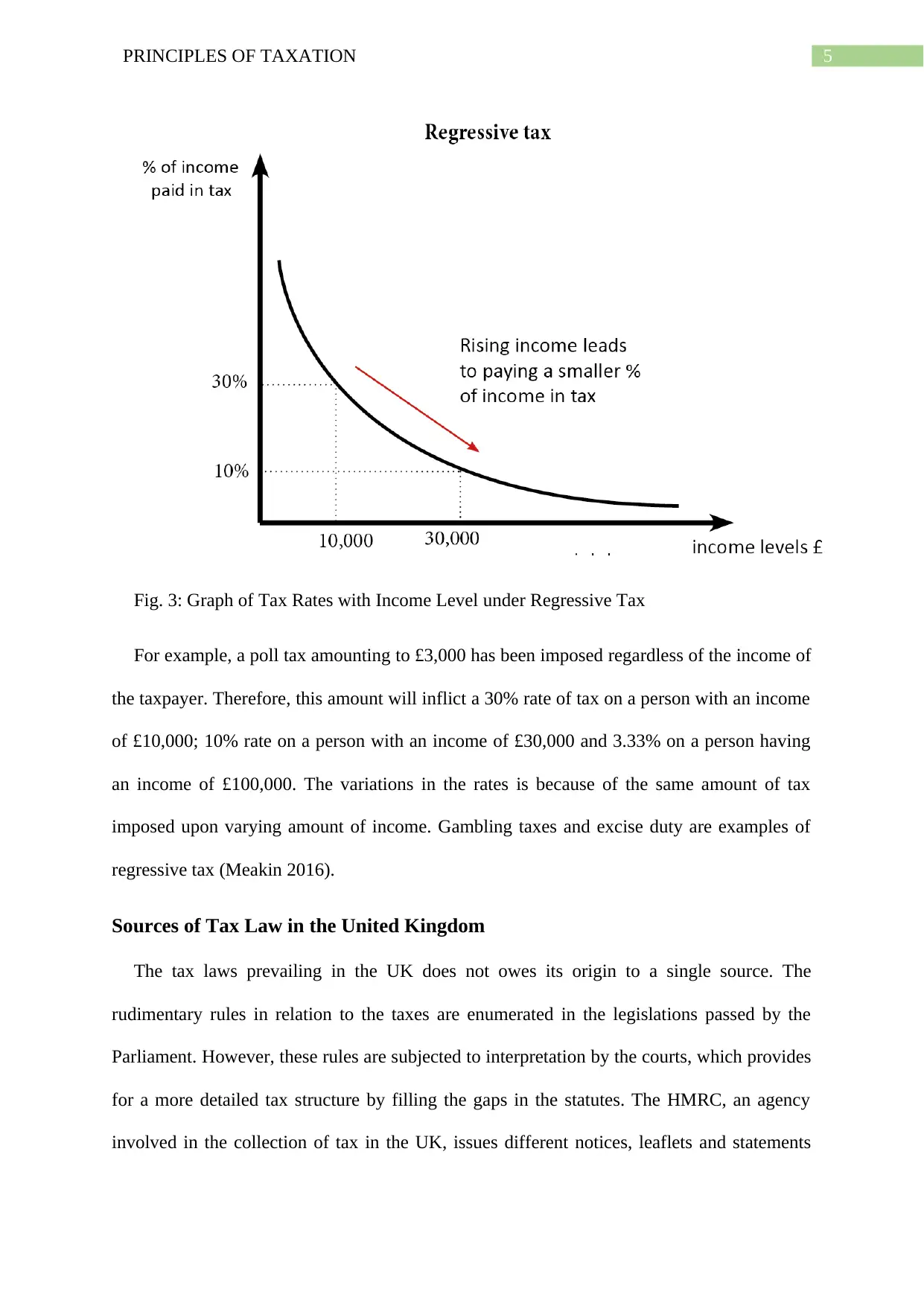

Fig. 3: Graph of Tax Rates with Income Level under Regressive Tax

For example, a poll tax amounting to £3,000 has been imposed regardless of the income of

the taxpayer. Therefore, this amount will inflict a 30% rate of tax on a person with an income

of £10,000; 10% rate on a person with an income of £30,000 and 3.33% on a person having

an income of £100,000. The variations in the rates is because of the same amount of tax

imposed upon varying amount of income. Gambling taxes and excise duty are examples of

regressive tax (Meakin 2016).

Sources of Tax Law in the United Kingdom

The tax laws prevailing in the UK does not owes its origin to a single source. The

rudimentary rules in relation to the taxes are enumerated in the legislations passed by the

Parliament. However, these rules are subjected to interpretation by the courts, which provides

for a more detailed tax structure by filling the gaps in the statutes. The HMRC, an agency

involved in the collection of tax in the UK, issues different notices, leaflets and statements

Fig. 3: Graph of Tax Rates with Income Level under Regressive Tax

For example, a poll tax amounting to £3,000 has been imposed regardless of the income of

the taxpayer. Therefore, this amount will inflict a 30% rate of tax on a person with an income

of £10,000; 10% rate on a person with an income of £30,000 and 3.33% on a person having

an income of £100,000. The variations in the rates is because of the same amount of tax

imposed upon varying amount of income. Gambling taxes and excise duty are examples of

regressive tax (Meakin 2016).

Sources of Tax Law in the United Kingdom

The tax laws prevailing in the UK does not owes its origin to a single source. The

rudimentary rules in relation to the taxes are enumerated in the legislations passed by the

Parliament. However, these rules are subjected to interpretation by the courts, which provides

for a more detailed tax structure by filling the gaps in the statutes. The HMRC, an agency

involved in the collection of tax in the UK, issues different notices, leaflets and statements

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6PRINCIPLES OF TAXATION

explaining the practical implementation of these laws. The statement issued by the HMRC

does not have any legal validity but are implemented to demonstrate the interpretation of the

tax authorities with respect to the enacted tax laws. However, these statements should be

complied with until the same has been challenged by the courts.

Therefore, it can be conceived that the Statute Laws are the main sources of tax in UK. It

includes the legislations enacted by the Parliament. The present legislations prevailing in UK

can be illustrated as follows:

explaining the practical implementation of these laws. The statement issued by the HMRC

does not have any legal validity but are implemented to demonstrate the interpretation of the

tax authorities with respect to the enacted tax laws. However, these statements should be

complied with until the same has been challenged by the courts.

Therefore, it can be conceived that the Statute Laws are the main sources of tax in UK. It

includes the legislations enacted by the Parliament. The present legislations prevailing in UK

can be illustrated as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PRINCIPLES OF TAXATION

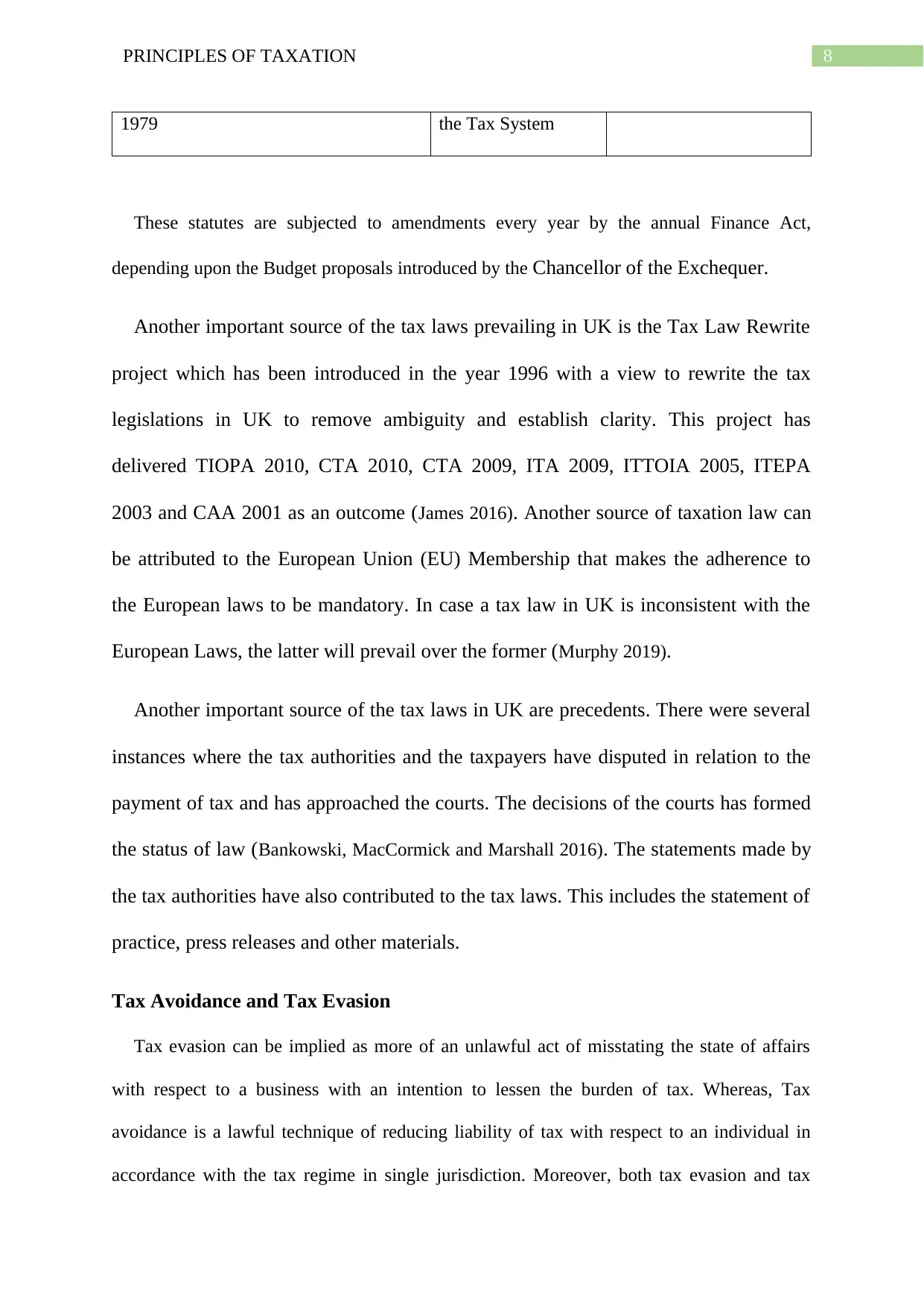

Statute Kind of Tax Abbreviation

Income and Corporation Taxes Act

1988

Income tax ICTA 1988

Capital Allowances Act 2001 Income tax CAA 2001

Income Tax (Earnings and Pensions)

Act 2003

Income tax ITEPA 2003

Income Tax (Trading and Other

Income) Act 2005

Income tax ITTOIA 2005

Income Tax Act 2007 Income tax ITA 2007

Social Security Contributions and

Benefits Act 1992

National Insurance SSCBA 1992

Taxation of Chargeable Gains Act 1992 Capital Gains Tax TCGA 1992

Inheritance Tax Act 1984 Inheritance Tax IHTA 1984

Income and Corporation Taxes Act

1988

Corporation tax ICTA 1988

Taxation of Chargeable Gains Act 1992 Corporation tax TCGA 1992

Capital Allowances Act 2001 Corporation tax CAA 2001

Corporation Tax Act 2009 Corporation tax CTA 2009

Corporation Tax Act 2010 Corporation tax CTA 2010

Taxation (International and Other

Provisions) Act 2010

Overseas aspects of

tax

TIOPA 2010

Value Added Tax Act 1994 Value added tax VATA 1994

Taxes Management Act 1970 TMA 1970

Customs and Excise Management Act Administration of CEMA 1979

Statute Kind of Tax Abbreviation

Income and Corporation Taxes Act

1988

Income tax ICTA 1988

Capital Allowances Act 2001 Income tax CAA 2001

Income Tax (Earnings and Pensions)

Act 2003

Income tax ITEPA 2003

Income Tax (Trading and Other

Income) Act 2005

Income tax ITTOIA 2005

Income Tax Act 2007 Income tax ITA 2007

Social Security Contributions and

Benefits Act 1992

National Insurance SSCBA 1992

Taxation of Chargeable Gains Act 1992 Capital Gains Tax TCGA 1992

Inheritance Tax Act 1984 Inheritance Tax IHTA 1984

Income and Corporation Taxes Act

1988

Corporation tax ICTA 1988

Taxation of Chargeable Gains Act 1992 Corporation tax TCGA 1992

Capital Allowances Act 2001 Corporation tax CAA 2001

Corporation Tax Act 2009 Corporation tax CTA 2009

Corporation Tax Act 2010 Corporation tax CTA 2010

Taxation (International and Other

Provisions) Act 2010

Overseas aspects of

tax

TIOPA 2010

Value Added Tax Act 1994 Value added tax VATA 1994

Taxes Management Act 1970 TMA 1970

Customs and Excise Management Act Administration of CEMA 1979

8PRINCIPLES OF TAXATION

1979 the Tax System

These statutes are subjected to amendments every year by the annual Finance Act,

depending upon the Budget proposals introduced by the Chancellor of the Exchequer.

Another important source of the tax laws prevailing in UK is the Tax Law Rewrite

project which has been introduced in the year 1996 with a view to rewrite the tax

legislations in UK to remove ambiguity and establish clarity. This project has

delivered TIOPA 2010, CTA 2010, CTA 2009, ITA 2009, ITTOIA 2005, ITEPA

2003 and CAA 2001 as an outcome (James 2016). Another source of taxation law can

be attributed to the European Union (EU) Membership that makes the adherence to

the European laws to be mandatory. In case a tax law in UK is inconsistent with the

European Laws, the latter will prevail over the former (Murphy 2019).

Another important source of the tax laws in UK are precedents. There were several

instances where the tax authorities and the taxpayers have disputed in relation to the

payment of tax and has approached the courts. The decisions of the courts has formed

the status of law (Bankowski, MacCormick and Marshall 2016). The statements made by

the tax authorities have also contributed to the tax laws. This includes the statement of

practice, press releases and other materials.

Tax Avoidance and Tax Evasion

Tax evasion can be implied as more of an unlawful act of misstating the state of affairs

with respect to a business with an intention to lessen the burden of tax. Whereas, Tax

avoidance is a lawful technique of reducing liability of tax with respect to an individual in

accordance with the tax regime in single jurisdiction. Moreover, both tax evasion and tax

1979 the Tax System

These statutes are subjected to amendments every year by the annual Finance Act,

depending upon the Budget proposals introduced by the Chancellor of the Exchequer.

Another important source of the tax laws prevailing in UK is the Tax Law Rewrite

project which has been introduced in the year 1996 with a view to rewrite the tax

legislations in UK to remove ambiguity and establish clarity. This project has

delivered TIOPA 2010, CTA 2010, CTA 2009, ITA 2009, ITTOIA 2005, ITEPA

2003 and CAA 2001 as an outcome (James 2016). Another source of taxation law can

be attributed to the European Union (EU) Membership that makes the adherence to

the European laws to be mandatory. In case a tax law in UK is inconsistent with the

European Laws, the latter will prevail over the former (Murphy 2019).

Another important source of the tax laws in UK are precedents. There were several

instances where the tax authorities and the taxpayers have disputed in relation to the

payment of tax and has approached the courts. The decisions of the courts has formed

the status of law (Bankowski, MacCormick and Marshall 2016). The statements made by

the tax authorities have also contributed to the tax laws. This includes the statement of

practice, press releases and other materials.

Tax Avoidance and Tax Evasion

Tax evasion can be implied as more of an unlawful act of misstating the state of affairs

with respect to a business with an intention to lessen the burden of tax. Whereas, Tax

avoidance is a lawful technique of reducing liability of tax with respect to an individual in

accordance with the tax regime in single jurisdiction. Moreover, both tax evasion and tax

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9PRINCIPLES OF TAXATION

avoidance are a way to reduce the tax liability of a taxpayer. However, tax evasion is an

unlawful way to effect the same while tax avoidance is more lawful in nature.

The tax regime with respect to the single jurisdiction provides for certain techniques to

assist tax avoidance. This form of usage of the tax laws to shrink the tax liability is permitted

under the law. For the reason of being covered by the laws, the techniques of tax avoidance is

generally regarded as legal. The aggressive tax avoidance although not considered to be

illegal but the same has always been treated to be unethical. This method of tax avoidance

employs a channelizing of profits from a high tax rate territory to a low tax rate territory to

lessen the tax payable on that specified portion of the profit so channelized.

The laws with respect to tax avoidance is more preventive in nature. The preventive

principles have evolved with the case of W. T. Ramsay Ltd. v. Inland Revenue

Commissioners, Eilbeck (Inspector of Taxes) v. Rawling [1982] A.C. 300, which renders a

transaction to be taxed nullifying the tax reduction as the same has been designed for the sole

purpose of reducing tax and does not have any economic purpose. This principle has been

further extended in the case of Furniss v. Dawson [1984] 1 All ER 530. However, later on,

this principle has been rejected by the courts. However, this principle has been extended to

the case Morrison 2002 Maintenance Trust, The Trustees of and Others v Revenue and

Customs [2016] UKFTT 250 (TC). Several schemes has been introduced by the UK

Government to prevent this, which includes Budget Note 66 (BN66) introducing the clause

55 of the Finance Bill 2008. The base erosion and profit shifting has also been provided for

with the initiative taken by the Organisation for Economic Co-operation and Development

(OECD), which further received the support of the UK Government. A tax has been imposed

on the diverted profit termed as Google tax by the Chancellor George Osborne during the

year 2015.

avoidance are a way to reduce the tax liability of a taxpayer. However, tax evasion is an

unlawful way to effect the same while tax avoidance is more lawful in nature.

The tax regime with respect to the single jurisdiction provides for certain techniques to

assist tax avoidance. This form of usage of the tax laws to shrink the tax liability is permitted

under the law. For the reason of being covered by the laws, the techniques of tax avoidance is

generally regarded as legal. The aggressive tax avoidance although not considered to be

illegal but the same has always been treated to be unethical. This method of tax avoidance

employs a channelizing of profits from a high tax rate territory to a low tax rate territory to

lessen the tax payable on that specified portion of the profit so channelized.

The laws with respect to tax avoidance is more preventive in nature. The preventive

principles have evolved with the case of W. T. Ramsay Ltd. v. Inland Revenue

Commissioners, Eilbeck (Inspector of Taxes) v. Rawling [1982] A.C. 300, which renders a

transaction to be taxed nullifying the tax reduction as the same has been designed for the sole

purpose of reducing tax and does not have any economic purpose. This principle has been

further extended in the case of Furniss v. Dawson [1984] 1 All ER 530. However, later on,

this principle has been rejected by the courts. However, this principle has been extended to

the case Morrison 2002 Maintenance Trust, The Trustees of and Others v Revenue and

Customs [2016] UKFTT 250 (TC). Several schemes has been introduced by the UK

Government to prevent this, which includes Budget Note 66 (BN66) introducing the clause

55 of the Finance Bill 2008. The base erosion and profit shifting has also been provided for

with the initiative taken by the Organisation for Economic Co-operation and Development

(OECD), which further received the support of the UK Government. A tax has been imposed

on the diverted profit termed as Google tax by the Chancellor George Osborne during the

year 2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10PRINCIPLES OF TAXATION

Tax evasion however, includes a misstatement of the true state of affairs in relation to a

business while making submission of the tax return by an individual to the authorities

concerned with the assessment of tax. Such misstatement is effected with a view to reduce tax

liability and includes false tax reporting, overstatement with respect to deductions,

understatement of profits and gains and a reduced declaration of income. This form of

evasion is visible in the informal kinds of economy where the government fails to monitor the

tax discrepancies adequately. Tax evasion can be calculated with respect to the unreported

taxable income that is the difference between the actual and the reported taxable income.

During the period of 2016-17, £5.3 billion of costs was accrued to the UK government

purely by way of tax evasion according to the estimation prepared by the HMRC. This

estimation excludes the criminal activities and hidden economy. This indicates a higher gap

of tax amounting to £33 billion incurring a liability of 5.7%. However, in this same period,

the estimated tax avoidance was £1.7 billion that excluded profit shifting, base erosion and

the international tax arrangement, which falls beyond the purview of the UK tax regime. The

Coalition Government has declared the assistance to tax evasion to be a criminal offence

during the year 2013 with the economic crime enforcement. In 2015, Chancellor George

Osborne aimed at the taxpayers owning offshore bank accounts with the help of the HMRC

and marked a doubled tax evasion prosecution. In this context, 27 cases of serious evasion of

tax have been opened by the HMRC and this included the top businesses operating in the UK

(Schneider, Raczkowski and Mróz 2015).

Tax evasion however, includes a misstatement of the true state of affairs in relation to a

business while making submission of the tax return by an individual to the authorities

concerned with the assessment of tax. Such misstatement is effected with a view to reduce tax

liability and includes false tax reporting, overstatement with respect to deductions,

understatement of profits and gains and a reduced declaration of income. This form of

evasion is visible in the informal kinds of economy where the government fails to monitor the

tax discrepancies adequately. Tax evasion can be calculated with respect to the unreported

taxable income that is the difference between the actual and the reported taxable income.

During the period of 2016-17, £5.3 billion of costs was accrued to the UK government

purely by way of tax evasion according to the estimation prepared by the HMRC. This

estimation excludes the criminal activities and hidden economy. This indicates a higher gap

of tax amounting to £33 billion incurring a liability of 5.7%. However, in this same period,

the estimated tax avoidance was £1.7 billion that excluded profit shifting, base erosion and

the international tax arrangement, which falls beyond the purview of the UK tax regime. The

Coalition Government has declared the assistance to tax evasion to be a criminal offence

during the year 2013 with the economic crime enforcement. In 2015, Chancellor George

Osborne aimed at the taxpayers owning offshore bank accounts with the help of the HMRC

and marked a doubled tax evasion prosecution. In this context, 27 cases of serious evasion of

tax have been opened by the HMRC and this included the top businesses operating in the UK

(Schneider, Raczkowski and Mróz 2015).

11PRINCIPLES OF TAXATION

Conclusion

Under the light of the above discussion, it can be concluded that the tax in which the

average rate of tax increases with the increase in the amount taxable is referred to as a

progressive tax whereas, in case of regressive tax, the average rate of tax decreases with an

increase in the taxable amount. The sources of tax laws in the UK includes the legislations,

precedents, statement of authorities and the European Laws. Tax evasion can be implied as

more of an unlawful act of misstating the state of affairs with respect to a business with an

intention to lessen the burden of tax whereas, Tax avoidance is a lawful technique of reducing

liability of tax with respect to an individual in accordance with the tax regime in single

jurisdiction.

Conclusion

Under the light of the above discussion, it can be concluded that the tax in which the

average rate of tax increases with the increase in the amount taxable is referred to as a

progressive tax whereas, in case of regressive tax, the average rate of tax decreases with an

increase in the taxable amount. The sources of tax laws in the UK includes the legislations,

precedents, statement of authorities and the European Laws. Tax evasion can be implied as

more of an unlawful act of misstating the state of affairs with respect to a business with an

intention to lessen the burden of tax whereas, Tax avoidance is a lawful technique of reducing

liability of tax with respect to an individual in accordance with the tax regime in single

jurisdiction.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.