Taxation Assignment: Income Tax Liability Calculations

VerifiedAdded on 2022/10/11

|7

|1213

|15

Homework Assignment

AI Summary

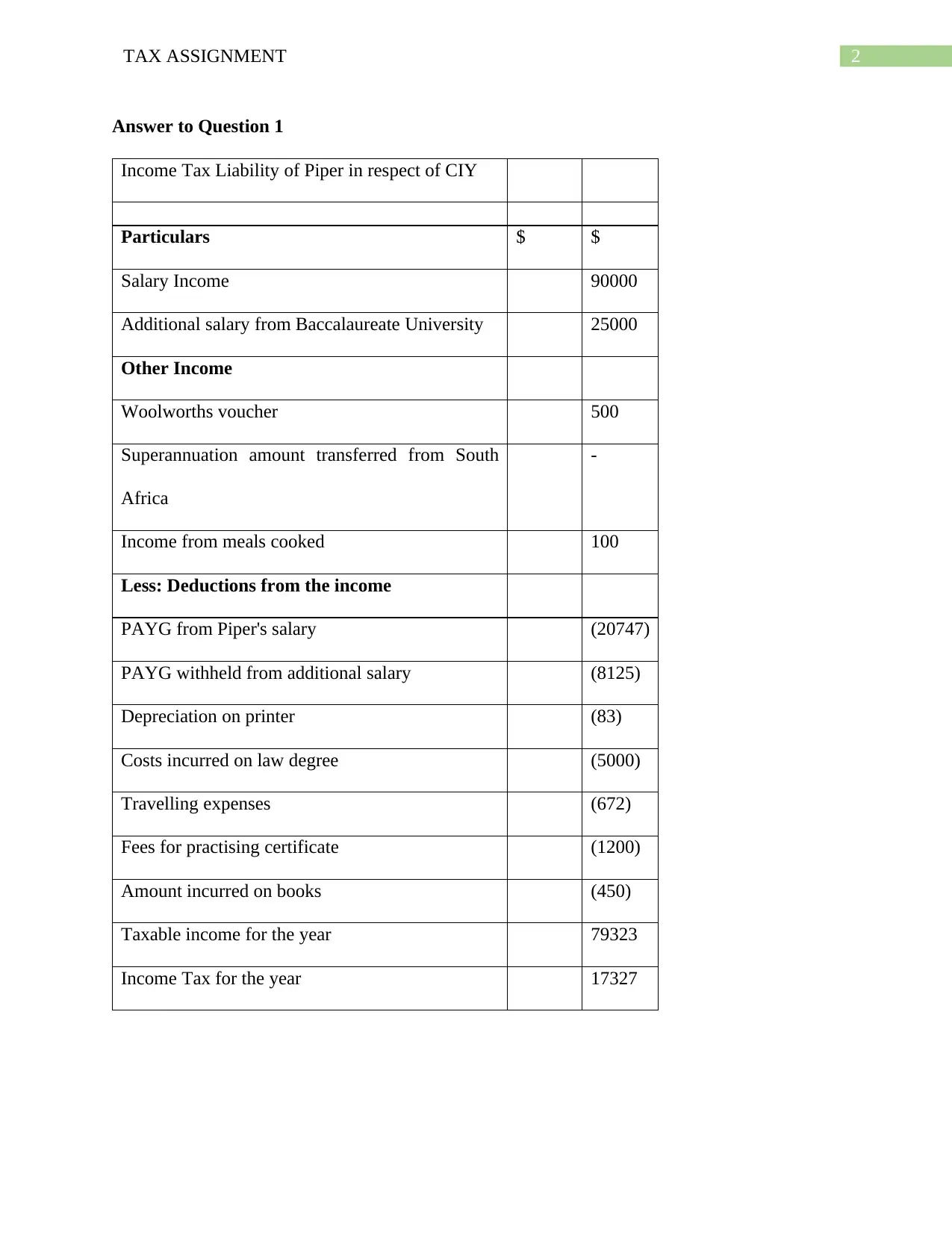

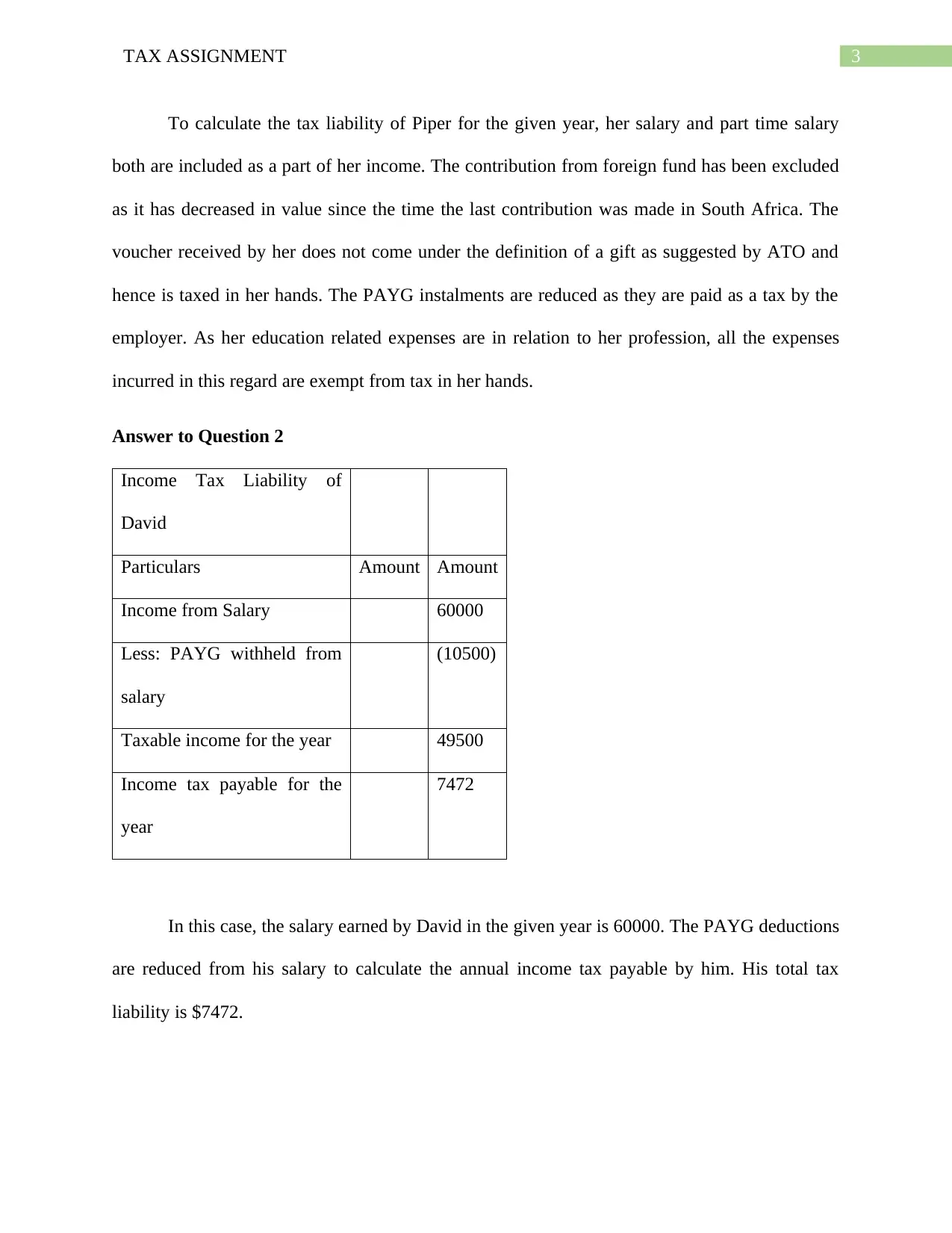

This assignment provides a detailed analysis of income tax liabilities for two individuals, Piper and David, covering various income sources, deductions, and tax calculations. The solution addresses specific scenarios, including salary income, additional income, and superannuation transfers from foreign funds. It explains the tax implications of Woolworths vouchers, depreciation, education expenses, and travel expenses. The assignment also examines the ATO guidelines regarding the transfer of superannuation funds from foreign countries to Australia, including the tax treatment of fund value changes. Additionally, it discusses the deductibility of expenses related to seminars, workshops, and educational courses, considering their connection to the individual's work and the allocation of travel expenses. The solution references ATO guidelines to support its conclusions and calculations.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.