TAX 12 Assignment: Analysis of Tax Laws on Income and Benefits

VerifiedAdded on 2021/05/31

|14

|1954

|20

Homework Assignment

AI Summary

This assignment analyzes a company's tax situation, focusing on ordinary income, capital gains, and fringe benefits. The company, involved in renovations and property leasing, generated income from rents (ordinary income) and asset sales (statutory income). The analysis examines relevant tax laws, including those related to capital assets and statutory income. The assignment then delves into fringe benefit tax calculations, including car fringe benefits, loan fringe benefits, and property fringe benefits. Calculations are provided for each type of benefit, determining taxable values and the overall fringe benefit tax amount. The assignment also includes references to relevant tax literature.

Running head: TAX

Tax

Name of the Student:

Name of the University:

Authors Note:

Tax

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAX

Table of Contents

Answer to Question 1.................................................................................................................2

Answer to Question 2.................................................................................................................7

Reference..................................................................................................................................10

Table of Contents

Answer to Question 1.................................................................................................................2

Answer to Question 2.................................................................................................................7

Reference..................................................................................................................................10

2TAX

Answer to Question 1

Issues:

In the present case, the company has been in the business of renovations for the last

30 years. After that, it was faced with a downturn in the market and sought to look for new

sources of income. Hence, it purchased old houses in the city, renovated them, and leased

them out for high rents. In the current year that is for the current tax year the company has

reinstated its old functions and sold the assets held by it. Due to the sale of the assets held by

the company, a huge profit was earned by the company1. Following is the analysis of the

virus laws and regulations relating to the ordinary income and the capital gain tax prevalent

in the country. After considering all the relevant provisions of the law applicable in the

present scenario a conclusion is given in respect of the tax treatment that has to be initiated in

respect to the present transaction of the company.

Laws:

Ordinary income 6(5)

The income according to the accounting concept is known as the ordinary income. The

meaning of the ordinary income is a lot dependent on the natural meaning of the words. In

1 Burkhauser, Richard V., Markus H. Hahn, and Roger Wilkins. "Measuring top incomes

using tax record data: A cautionary tale from Australia." The Journal of Economic

Inequality 13, no. 2 (2015): 181-205.

Answer to Question 1

Issues:

In the present case, the company has been in the business of renovations for the last

30 years. After that, it was faced with a downturn in the market and sought to look for new

sources of income. Hence, it purchased old houses in the city, renovated them, and leased

them out for high rents. In the current year that is for the current tax year the company has

reinstated its old functions and sold the assets held by it. Due to the sale of the assets held by

the company, a huge profit was earned by the company1. Following is the analysis of the

virus laws and regulations relating to the ordinary income and the capital gain tax prevalent

in the country. After considering all the relevant provisions of the law applicable in the

present scenario a conclusion is given in respect of the tax treatment that has to be initiated in

respect to the present transaction of the company.

Laws:

Ordinary income 6(5)

The income according to the accounting concept is known as the ordinary income. The

meaning of the ordinary income is a lot dependent on the natural meaning of the words. In

1 Burkhauser, Richard V., Markus H. Hahn, and Roger Wilkins. "Measuring top incomes

using tax record data: A cautionary tale from Australia." The Journal of Economic

Inequality 13, no. 2 (2015): 181-205.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAX

addition to that, it depends on the natural interpretation by the court2. The three attributes of

an ordinary income are as follows:

a) The amount or a part of the total amount being classified as accrued in respect of the

taxpayer due to the conduct of business by him.

b) The amount or part of the amount has accrued to the taxpayer from the services that

have been rendered by him to some other entity.

c) The income that is to be classified is received as a compensation for foregoing an item

that would have resulted to the inflow of income for the taxpayer presently or in the

future.

There are other parameters too in relation to which the amount is measures so as to establish

whether it is an income or not. They are as follows:

a) Is the amount to be classified has been actually received by the tax payer.\

b) Is the nature of the income is to occur regularly or periodically.

c) Has the income accrued from the use of any asset?

d) Is the income a result of the compensation received for the loss of income earned by

the taxpayer?

e) Is the amount or item received by the taxpayer convertible into cash or not.

Statutory income 6 (10):

As per the provisions of this section the income that are not ordinary income are termed as

statutory income.

2 Becker, Johannes, E. Reimer, and A. Rust. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International, 2015.

addition to that, it depends on the natural interpretation by the court2. The three attributes of

an ordinary income are as follows:

a) The amount or a part of the total amount being classified as accrued in respect of the

taxpayer due to the conduct of business by him.

b) The amount or part of the amount has accrued to the taxpayer from the services that

have been rendered by him to some other entity.

c) The income that is to be classified is received as a compensation for foregoing an item

that would have resulted to the inflow of income for the taxpayer presently or in the

future.

There are other parameters too in relation to which the amount is measures so as to establish

whether it is an income or not. They are as follows:

a) Is the amount to be classified has been actually received by the tax payer.\

b) Is the nature of the income is to occur regularly or periodically.

c) Has the income accrued from the use of any asset?

d) Is the income a result of the compensation received for the loss of income earned by

the taxpayer?

e) Is the amount or item received by the taxpayer convertible into cash or not.

Statutory income 6 (10):

As per the provisions of this section the income that are not ordinary income are termed as

statutory income.

2 Becker, Johannes, E. Reimer, and A. Rust. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International, 2015.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAX

Capital asset sect. 108.5

As per the provisions of this act, a CGT asset can be referred to as any kind of property

and any legal or equitable right that cannot be termed as property. The section further goes

onto kits out specific assets to avoid any sort of doubt in the future3. They are as follows:

a) A particular part of, or specific interest held in any asset that has been referred to in

the sub section 1.

b) The goodwill of any entity along with any interest in it.

c) The interest held by the entity in the in an asset of the partnership.

d) Any sort of other interest in the partnership that was skipped by the paragraph (c).

Some of the examples of the capital assets as listed out by the entity are as follows:

1) Land and buildings.

2) The shares of any company and the units in any unit trust.

3) The various options.

4) The debts owed to the taxpayer.

5) The right with the entity to enforce any contractual obligation.

6) Any sort of foreign currency.

In addition to this, it has been specifically stated out that no asset shall be considered as a

capital asset if the same has been acquired before 26th of June 1992 and was not

3 Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Capital asset sect. 108.5

As per the provisions of this act, a CGT asset can be referred to as any kind of property

and any legal or equitable right that cannot be termed as property. The section further goes

onto kits out specific assets to avoid any sort of doubt in the future3. They are as follows:

a) A particular part of, or specific interest held in any asset that has been referred to in

the sub section 1.

b) The goodwill of any entity along with any interest in it.

c) The interest held by the entity in the in an asset of the partnership.

d) Any sort of other interest in the partnership that was skipped by the paragraph (c).

Some of the examples of the capital assets as listed out by the entity are as follows:

1) Land and buildings.

2) The shares of any company and the units in any unit trust.

3) The various options.

4) The debts owed to the taxpayer.

5) The right with the entity to enforce any contractual obligation.

6) Any sort of foreign currency.

In addition to this, it has been specifically stated out that no asset shall be considered as a

capital asset if the same has been acquired before 26th of June 1992 and was not

3 Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

5TAX

considered an asset for the purpose of former Part III A of the Income Tax Assessment

Act 19364.

Application:

The income that is earned by the company in respect of the property acquired by it on lease

falls under the purview of the ordinary income. The reason being as follows:

a) The amount of that is earned by the company in respect of the high rent from the

properties is earned by the company by the conduct of a business5.

b) The company has been able to receive the amount accrued to it in respect of the use of

the asset by the lessee6.

c) The amount received by the company is recurring in nature. In other words, the

company receives the income from the source on a regular basis on not only during

the happening of a particular event7.

4 Richardson, G., Taylor, G., & Lanis, R. (2015). The impact of financial distress on

corporate tax avoidance spanning the global financial crisis: Evidence from

Australia. Economic Modelling, 44, 44-53.

5 Maurer, Ludmilla, Christian Port, Tom Roth, and John Walker. "A Brave New Post-BEPS

World: New Double Tax Treaty Between Germany and Australia Implements BEPS

Measures." Intertax 45, no. 4 (2017): 310-321.

6 Hodgson, Helen, and Prafula Pearce. "TravelSmart or travel tax breaks: is the fringe benefits

tax a barrier to active commuting in Australia? 1." eJournal of Tax Research 13, no. 3 (2015):

819.

considered an asset for the purpose of former Part III A of the Income Tax Assessment

Act 19364.

Application:

The income that is earned by the company in respect of the property acquired by it on lease

falls under the purview of the ordinary income. The reason being as follows:

a) The amount of that is earned by the company in respect of the high rent from the

properties is earned by the company by the conduct of a business5.

b) The company has been able to receive the amount accrued to it in respect of the use of

the asset by the lessee6.

c) The amount received by the company is recurring in nature. In other words, the

company receives the income from the source on a regular basis on not only during

the happening of a particular event7.

4 Richardson, G., Taylor, G., & Lanis, R. (2015). The impact of financial distress on

corporate tax avoidance spanning the global financial crisis: Evidence from

Australia. Economic Modelling, 44, 44-53.

5 Maurer, Ludmilla, Christian Port, Tom Roth, and John Walker. "A Brave New Post-BEPS

World: New Double Tax Treaty Between Germany and Australia Implements BEPS

Measures." Intertax 45, no. 4 (2017): 310-321.

6 Hodgson, Helen, and Prafula Pearce. "TravelSmart or travel tax breaks: is the fringe benefits

tax a barrier to active commuting in Australia? 1." eJournal of Tax Research 13, no. 3 (2015):

819.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAX

d) The income that is earned by the company in respect of the rent is accrued to it due to

the use of its assets by the lessee.

The profit that is earned by the company because of the sale of the houses owned by it

does not satisfy any of the condition of the ordinary income and hence it is categories as

statutory income8.

It can be said that the property held by the company can be termed as capital asset as pert

the provision of the section 108.5. The gain arising out of the sale of the capital assets held by

the entity is termed as capital gain9.

Conclusion:

It can be concluded from the analysis that has been undertaken above in respect of

this case that the rental income that was being previously earned by the company satisfies all

the conditions of an ordinary income while the income or the gain that is earned by the

company in respect of the sale of the asset held by the company does not fulfil any of the

condition of the ordinary income and hence is to be treated as statutory income. It has to be

noted that the assets held by the company has satisfied all the condition as specified in the

section. Hence can be termed as capital assets, which have been sold by the company.

7 King, Alexander. "Mid market focus: The new attribution tax regime for MITs: Part

1." Taxation in Australia 50, no. 10 (2016): 590.

8 James, Simon, Adrian Sawyer, and Ian Wallschutzky. "Tax simplification: A review of initiatives in Australia,

New Zealand and the United Kingdom." eJournal of Tax Research 13, no. 1 (2015): 280.

9 Gunnarsson, Åsa, and Eva-Maria Svensson. Exploiting the limits of law: Swedish feminism

and the challenge to pessimism. Routledge, 2016.

d) The income that is earned by the company in respect of the rent is accrued to it due to

the use of its assets by the lessee.

The profit that is earned by the company because of the sale of the houses owned by it

does not satisfy any of the condition of the ordinary income and hence it is categories as

statutory income8.

It can be said that the property held by the company can be termed as capital asset as pert

the provision of the section 108.5. The gain arising out of the sale of the capital assets held by

the entity is termed as capital gain9.

Conclusion:

It can be concluded from the analysis that has been undertaken above in respect of

this case that the rental income that was being previously earned by the company satisfies all

the conditions of an ordinary income while the income or the gain that is earned by the

company in respect of the sale of the asset held by the company does not fulfil any of the

condition of the ordinary income and hence is to be treated as statutory income. It has to be

noted that the assets held by the company has satisfied all the condition as specified in the

section. Hence can be termed as capital assets, which have been sold by the company.

7 King, Alexander. "Mid market focus: The new attribution tax regime for MITs: Part

1." Taxation in Australia 50, no. 10 (2016): 590.

8 James, Simon, Adrian Sawyer, and Ian Wallschutzky. "Tax simplification: A review of initiatives in Australia,

New Zealand and the United Kingdom." eJournal of Tax Research 13, no. 1 (2015): 280.

9 Gunnarsson, Åsa, and Eva-Maria Svensson. Exploiting the limits of law: Swedish feminism

and the challenge to pessimism. Routledge, 2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAX

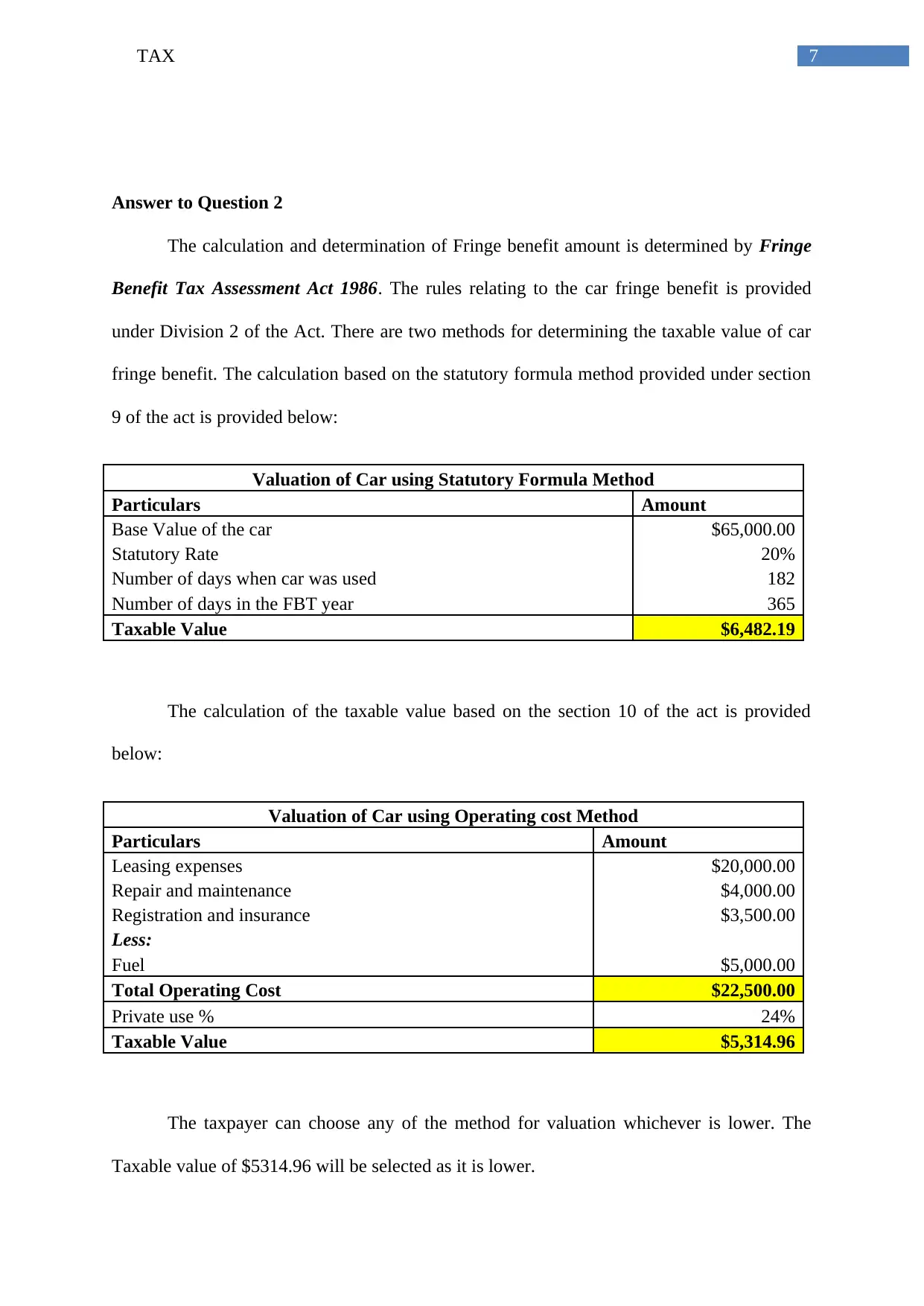

Answer to Question 2

The calculation and determination of Fringe benefit amount is determined by Fringe

Benefit Tax Assessment Act 1986. The rules relating to the car fringe benefit is provided

under Division 2 of the Act. There are two methods for determining the taxable value of car

fringe benefit. The calculation based on the statutory formula method provided under section

9 of the act is provided below:

Valuation of Car using Statutory Formula Method

Particulars Amount

Base Value of the car $65,000.00

Statutory Rate 20%

Number of days when car was used 182

Number of days in the FBT year 365

Taxable Value $6,482.19

The calculation of the taxable value based on the section 10 of the act is provided

below:

Valuation of Car using Operating cost Method

Particulars Amount

Leasing expenses $20,000.00

Repair and maintenance $4,000.00

Registration and insurance $3,500.00

Less:

Fuel $5,000.00

Total Operating Cost $22,500.00

Private use % 24%

Taxable Value $5,314.96

The taxpayer can choose any of the method for valuation whichever is lower. The

Taxable value of $5314.96 will be selected as it is lower.

Answer to Question 2

The calculation and determination of Fringe benefit amount is determined by Fringe

Benefit Tax Assessment Act 1986. The rules relating to the car fringe benefit is provided

under Division 2 of the Act. There are two methods for determining the taxable value of car

fringe benefit. The calculation based on the statutory formula method provided under section

9 of the act is provided below:

Valuation of Car using Statutory Formula Method

Particulars Amount

Base Value of the car $65,000.00

Statutory Rate 20%

Number of days when car was used 182

Number of days in the FBT year 365

Taxable Value $6,482.19

The calculation of the taxable value based on the section 10 of the act is provided

below:

Valuation of Car using Operating cost Method

Particulars Amount

Leasing expenses $20,000.00

Repair and maintenance $4,000.00

Registration and insurance $3,500.00

Less:

Fuel $5,000.00

Total Operating Cost $22,500.00

Private use % 24%

Taxable Value $5,314.96

The taxpayer can choose any of the method for valuation whichever is lower. The

Taxable value of $5314.96 will be selected as it is lower.

8TAX

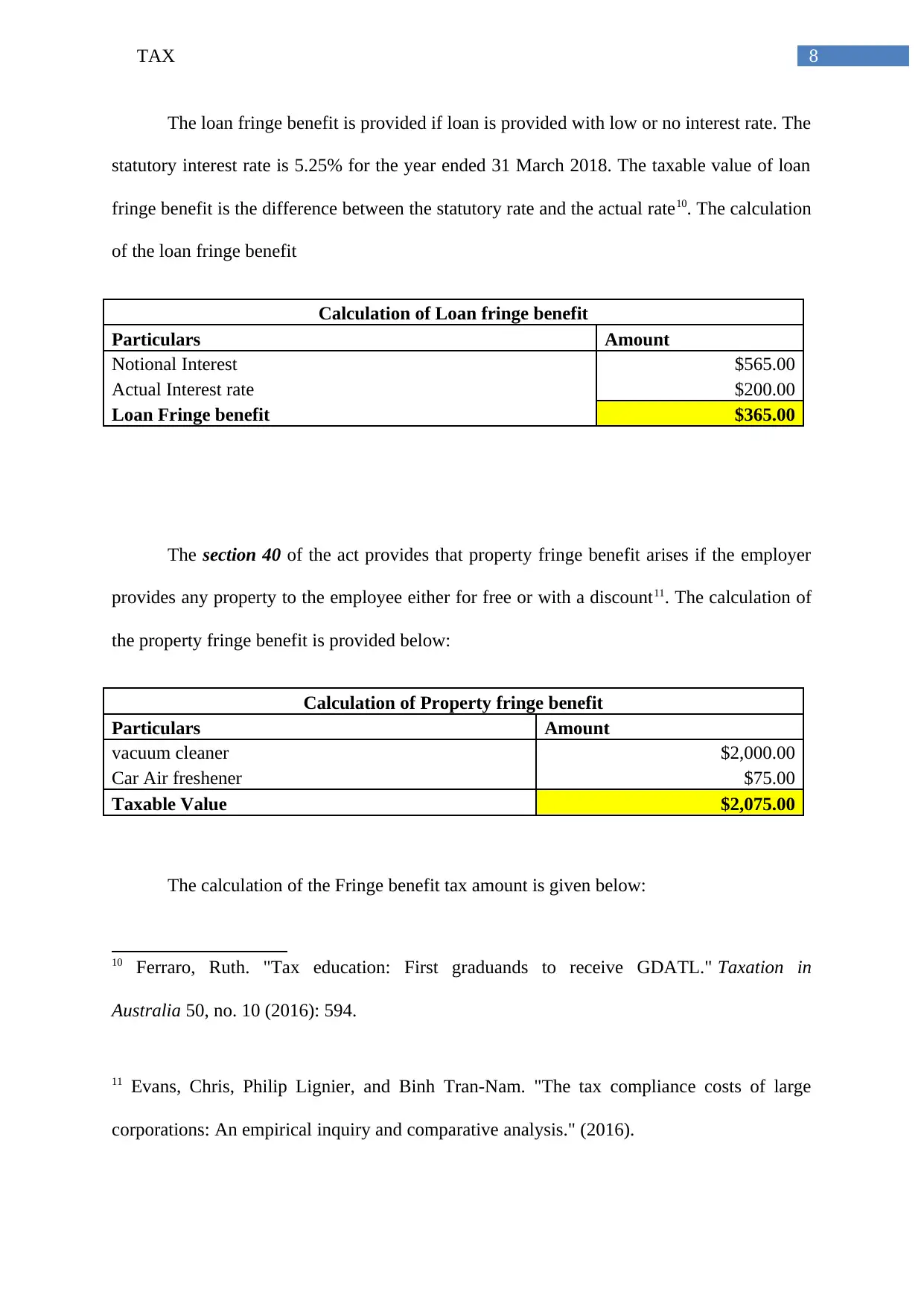

The loan fringe benefit is provided if loan is provided with low or no interest rate. The

statutory interest rate is 5.25% for the year ended 31 March 2018. The taxable value of loan

fringe benefit is the difference between the statutory rate and the actual rate10. The calculation

of the loan fringe benefit

Calculation of Loan fringe benefit

Particulars Amount

Notional Interest $565.00

Actual Interest rate $200.00

Loan Fringe benefit $365.00

The section 40 of the act provides that property fringe benefit arises if the employer

provides any property to the employee either for free or with a discount11. The calculation of

the property fringe benefit is provided below:

Calculation of Property fringe benefit

Particulars Amount

vacuum cleaner $2,000.00

Car Air freshener $75.00

Taxable Value $2,075.00

The calculation of the Fringe benefit tax amount is given below:

10 Ferraro, Ruth. "Tax education: First graduands to receive GDATL." Taxation in

Australia 50, no. 10 (2016): 594.

11 Evans, Chris, Philip Lignier, and Binh Tran-Nam. "The tax compliance costs of large

corporations: An empirical inquiry and comparative analysis." (2016).

The loan fringe benefit is provided if loan is provided with low or no interest rate. The

statutory interest rate is 5.25% for the year ended 31 March 2018. The taxable value of loan

fringe benefit is the difference between the statutory rate and the actual rate10. The calculation

of the loan fringe benefit

Calculation of Loan fringe benefit

Particulars Amount

Notional Interest $565.00

Actual Interest rate $200.00

Loan Fringe benefit $365.00

The section 40 of the act provides that property fringe benefit arises if the employer

provides any property to the employee either for free or with a discount11. The calculation of

the property fringe benefit is provided below:

Calculation of Property fringe benefit

Particulars Amount

vacuum cleaner $2,000.00

Car Air freshener $75.00

Taxable Value $2,075.00

The calculation of the Fringe benefit tax amount is given below:

10 Ferraro, Ruth. "Tax education: First graduands to receive GDATL." Taxation in

Australia 50, no. 10 (2016): 594.

11 Evans, Chris, Philip Lignier, and Binh Tran-Nam. "The tax compliance costs of large

corporations: An empirical inquiry and comparative analysis." (2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAX

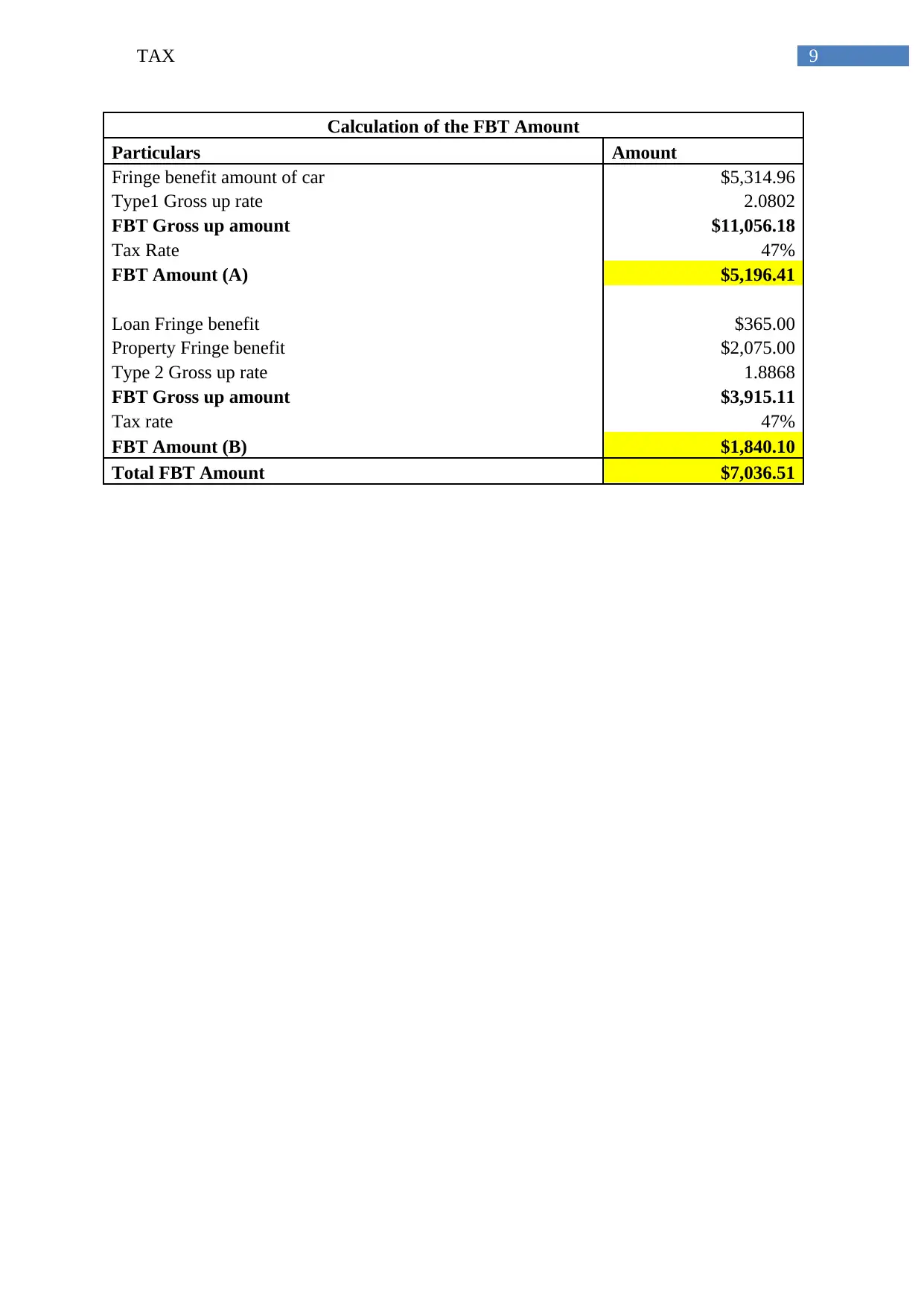

Calculation of the FBT Amount

Particulars Amount

Fringe benefit amount of car $5,314.96

Type1 Gross up rate 2.0802

FBT Gross up amount $11,056.18

Tax Rate 47%

FBT Amount (A) $5,196.41

Loan Fringe benefit $365.00

Property Fringe benefit $2,075.00

Type 2 Gross up rate 1.8868

FBT Gross up amount $3,915.11

Tax rate 47%

FBT Amount (B) $1,840.10

Total FBT Amount $7,036.51

Calculation of the FBT Amount

Particulars Amount

Fringe benefit amount of car $5,314.96

Type1 Gross up rate 2.0802

FBT Gross up amount $11,056.18

Tax Rate 47%

FBT Amount (A) $5,196.41

Loan Fringe benefit $365.00

Property Fringe benefit $2,075.00

Type 2 Gross up rate 1.8868

FBT Gross up amount $3,915.11

Tax rate 47%

FBT Amount (B) $1,840.10

Total FBT Amount $7,036.51

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAX

Reference

Becker, Johannes, E. Reimer, and A. Rust. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International, 2015.

Burkhauser, Richard V., Markus H. Hahn, and Roger Wilkins. "Measuring top incomes using

tax record data: A cautionary tale from Australia." The Journal of Economic Inequality 13,

no. 2 (2015): 181-205.

Evans, Chris, Philip Lignier, and Binh Tran-Nam. "The tax compliance costs of large

corporations: An empirical inquiry and comparative analysis." (2016).

Ferraro, Ruth. "Tax education: First graduands to receive GDATL." Taxation in Australia 50,

no. 10 (2016): 594.

Gunnarsson, Åsa, and Eva-Maria Svensson. Exploiting the limits of law: Swedish feminism

and the challenge to pessimism. Routledge, 2016.

Hodgson, Helen, and Prafula Pearce. "TravelSmart or travel tax breaks: is the fringe benefits

tax a barrier to active commuting in Australia? 1." eJournal of Tax Research 13, no. 3 (2015):

819.

James, Simon, Adrian Sawyer, and Ian Wallschutzky. "Tax simplification: A review of

initiatives in Australia, New Zealand and the United Kingdom." eJournal of Tax

Research 13, no. 1 (2015): 280.

King, Alexander. "Mid market focus: The new attribution tax regime for MITs: Part

1." Taxation in Australia 50, no. 10 (2016): 590.

Reference

Becker, Johannes, E. Reimer, and A. Rust. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International, 2015.

Burkhauser, Richard V., Markus H. Hahn, and Roger Wilkins. "Measuring top incomes using

tax record data: A cautionary tale from Australia." The Journal of Economic Inequality 13,

no. 2 (2015): 181-205.

Evans, Chris, Philip Lignier, and Binh Tran-Nam. "The tax compliance costs of large

corporations: An empirical inquiry and comparative analysis." (2016).

Ferraro, Ruth. "Tax education: First graduands to receive GDATL." Taxation in Australia 50,

no. 10 (2016): 594.

Gunnarsson, Åsa, and Eva-Maria Svensson. Exploiting the limits of law: Swedish feminism

and the challenge to pessimism. Routledge, 2016.

Hodgson, Helen, and Prafula Pearce. "TravelSmart or travel tax breaks: is the fringe benefits

tax a barrier to active commuting in Australia? 1." eJournal of Tax Research 13, no. 3 (2015):

819.

James, Simon, Adrian Sawyer, and Ian Wallschutzky. "Tax simplification: A review of

initiatives in Australia, New Zealand and the United Kingdom." eJournal of Tax

Research 13, no. 1 (2015): 280.

King, Alexander. "Mid market focus: The new attribution tax regime for MITs: Part

1." Taxation in Australia 50, no. 10 (2016): 590.

11TAX

Maurer, Ludmilla, Christian Port, Tom Roth, and John Walker. "A Brave New Post-BEPS

World: New Double Tax Treaty Between Germany and Australia Implements BEPS

Measures." Intertax 45, no. 4 (2017): 310-321.

Mumford, Ann. Taxing culture: towards a theory of tax collection law. Routledge, 2017.

Richardson, G., Taylor, G., & Lanis, R. (2015). The impact of financial distress on corporate

tax avoidance spanning the global financial crisis: Evidence from Australia. Economic

Modelling, 44, 44-53.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Maurer, Ludmilla, Christian Port, Tom Roth, and John Walker. "A Brave New Post-BEPS

World: New Double Tax Treaty Between Germany and Australia Implements BEPS

Measures." Intertax 45, no. 4 (2017): 310-321.

Mumford, Ann. Taxing culture: towards a theory of tax collection law. Routledge, 2017.

Richardson, G., Taylor, G., & Lanis, R. (2015). The impact of financial distress on corporate

tax avoidance spanning the global financial crisis: Evidence from Australia. Economic

Modelling, 44, 44-53.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.