University Taxation Assignment: Analysis of Tax Issues

VerifiedAdded on 2020/04/07

|8

|1309

|69

Homework Assignment

AI Summary

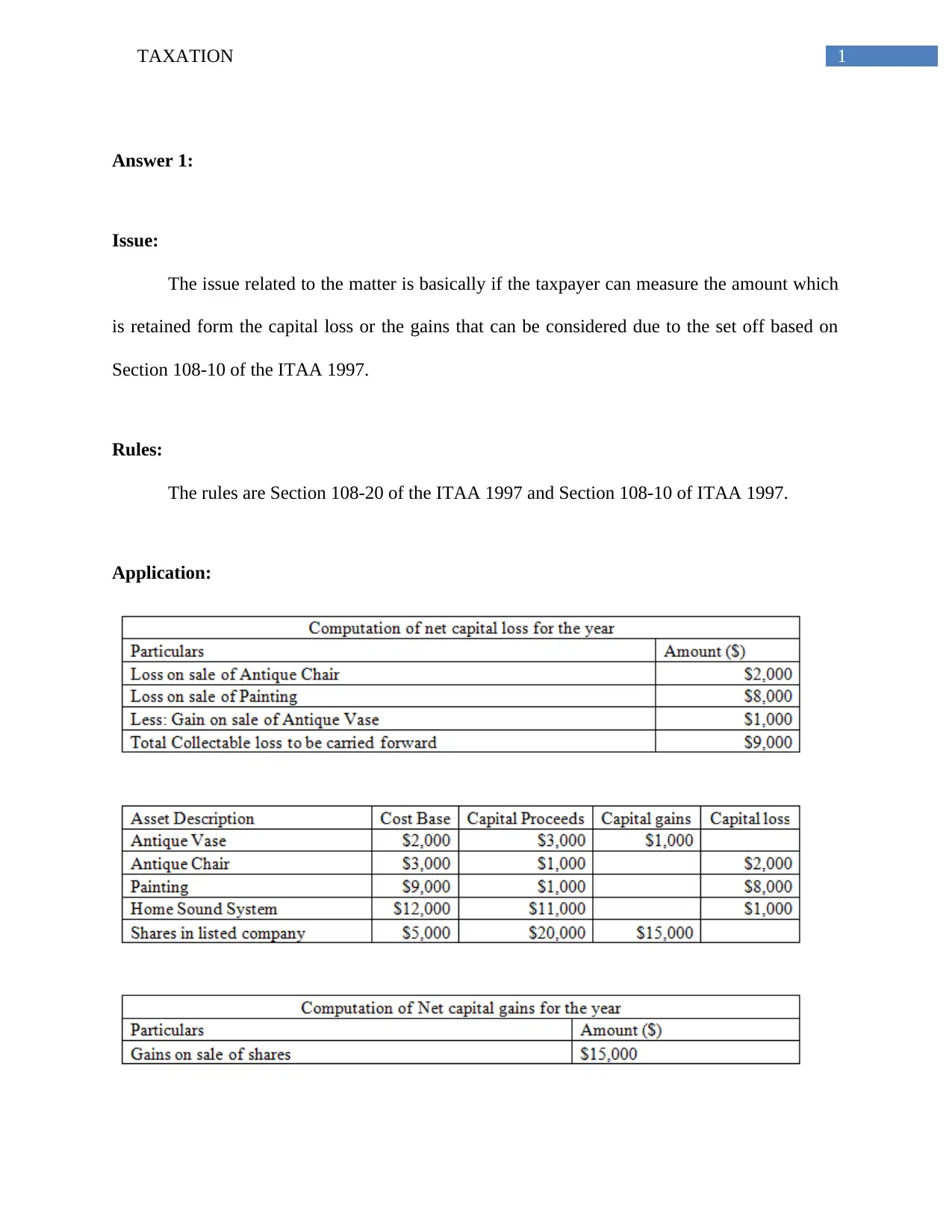

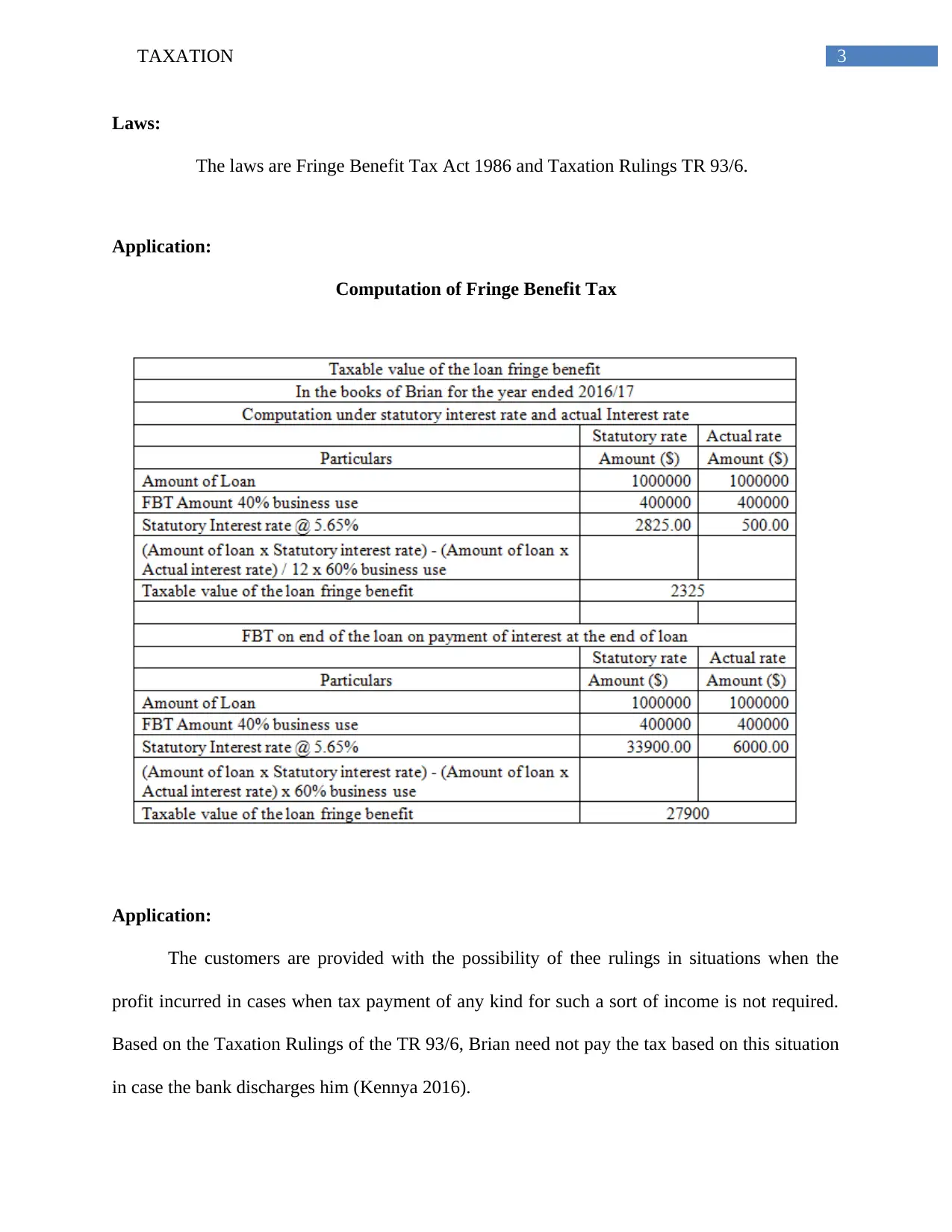

This document provides a comprehensive analysis of several taxation scenarios. It begins by addressing whether a taxpayer can offset capital losses against gains based on Section 108-10 of the ITAA 1997, concluding that losses from personal assets cannot be offset. The assignment then explores the calculation of Fringe Benefit Tax (FBT) according to the Fringe Benefit Tax Act 1986 and relevant taxation rulings, determining that, in the given scenario, no FBT is payable. Furthermore, the assignment examines loss distribution in joint ownership of rental properties, applying relevant laws and rulings to determine how losses should be shared. The document also discusses tax avoidance, referencing IRC v Duke of Westminster (1936). Finally, it analyzes the taxation of timber cutting, referencing Subsection 6 (1) of the ITAA 1936 and concluding that the income received from timber sales is taxable. The analysis is supported by references to relevant legal and academic sources.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.