Taxation Law Assignment: Capital Gains, Fringe Benefits, and Losses

VerifiedAdded on 2020/03/13

|11

|2896

|48

Homework Assignment

AI Summary

This taxation law assignment addresses several key aspects of taxation, including capital gains, fringe benefits, and the application of tax principles through case studies. The first part examines capital gains and losses arising from the acquisition and sale of assets, considering collectibles, personal use assets, and shares in a listed company, calculating the net capital gain. The second part focuses on fringe benefits tax (FBT) related to a bank executive's loan, analyzing the tax implications of different interest payment scenarios and loan forgiveness. The third part explores the tax treatment of losses in a rental property, considering the agreement between joint owners and the implications for capital gains or losses. The final part discusses the principle established in IRC v Duke of Westminster, the right to minimize tax liability legally, and its relevance in the present scenario. The assignment provides detailed calculations, legal analysis, and practical examples to illustrate complex tax concepts.

TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

Answer-1

Issue

Over the past 12 months Eric acquired and sold some of the assets. Will it lead to capital gain or

loss for the year?

Rule

It was held in the case of Californian Copper Syndicate (Limited) v. Harris (Surveyor of Taxes)

(1904) 5 TC 159 that those transactions held in the normal course of business will be subjected

to tax.

Application

Net Capital Gain or Loss computation -

In the past 12 months there has been various acquisitions by Eric. As the date has not been given,

it can be assumed that the assets have been held by Eric for less than 12 months.

Capital Gain tax arises where the sale consideration of the assets sold is more than the cost base

of the said assets (Hopewell, 2012). Here the benefit of indexation will not be available as the

assets have been held for less than 12 months period.

First of all the assets held should be classified under their respective heads as under:

Collectables- these are the items that are bought by the individual mostly for personal benefit or

enjoyment. No capital gain arises on the sale of such collectible assets if the acquisition costs of

these assets are $500 or less than that. In the given case, Eric has the following collectibles in

hand with the acquisition cost given:

Antique Vase- $ 2000

Antique Chair- $ 3000

Painting- $ 9000

Personal Use Assets- these are the assets which are used by an individual for his own use or

enjoyment but other than collectibles. Capital gain does not come into picture if there is a sale of

the personal assets and where the acquisition cost of these assets was $ 10,000 or below

(Nethercott et. al, 2013).

2

Answer-1

Issue

Over the past 12 months Eric acquired and sold some of the assets. Will it lead to capital gain or

loss for the year?

Rule

It was held in the case of Californian Copper Syndicate (Limited) v. Harris (Surveyor of Taxes)

(1904) 5 TC 159 that those transactions held in the normal course of business will be subjected

to tax.

Application

Net Capital Gain or Loss computation -

In the past 12 months there has been various acquisitions by Eric. As the date has not been given,

it can be assumed that the assets have been held by Eric for less than 12 months.

Capital Gain tax arises where the sale consideration of the assets sold is more than the cost base

of the said assets (Hopewell, 2012). Here the benefit of indexation will not be available as the

assets have been held for less than 12 months period.

First of all the assets held should be classified under their respective heads as under:

Collectables- these are the items that are bought by the individual mostly for personal benefit or

enjoyment. No capital gain arises on the sale of such collectible assets if the acquisition costs of

these assets are $500 or less than that. In the given case, Eric has the following collectibles in

hand with the acquisition cost given:

Antique Vase- $ 2000

Antique Chair- $ 3000

Painting- $ 9000

Personal Use Assets- these are the assets which are used by an individual for his own use or

enjoyment but other than collectibles. Capital gain does not come into picture if there is a sale of

the personal assets and where the acquisition cost of these assets was $ 10,000 or below

(Nethercott et. al, 2013).

2

Taxation

In the given case, Eric has the following personal use assets in hand with the acquisition cost

given :

A home sound system- $ 12,000

Other than the Collectibles and Personal Use Assets, Eric had purchased shares in a listed

company for $ 5,000 which come under the purview of capital gain tax.

Conclusion

It needs to be noted that as per Income Tax Assessment Act 1997, section 102-5 the income that

is assessable will contain net capital gain. For calculation of capital gain tax for the assets held

for less than 12 months, the following formula shall be used:

Capital Proceeds – Assets as per the base cost

(Amounts in dollars)

Particulars Cost Base of Assets Capital Proceeds of

Assets

Net Capital Gain/

(Net Capital Loss)

Antique Vase 2,000 3000 1000 Gain

Antique Chair 3,000 1000 (2000) Loss

Painting 9,000 1000 (8000) Loss

Home Sound System 12,000 11000 (1000) Loss

Shares in listed

company

5,000 20000 15000 Gain

Total 5000 Net Capital

Gain

Hence, the total taxable capital gain for Eric for the year comes to $5,000.

Working Notes:

i. The overall collectibles have been acquired on an individual basis (cost ranks higher

than $5000) therefore will attract capital gain

ii. All the Personal use assets individually have been purchased at a cost more than $

10,000, hence they are applicable for taxable capital gain.

3

In the given case, Eric has the following personal use assets in hand with the acquisition cost

given :

A home sound system- $ 12,000

Other than the Collectibles and Personal Use Assets, Eric had purchased shares in a listed

company for $ 5,000 which come under the purview of capital gain tax.

Conclusion

It needs to be noted that as per Income Tax Assessment Act 1997, section 102-5 the income that

is assessable will contain net capital gain. For calculation of capital gain tax for the assets held

for less than 12 months, the following formula shall be used:

Capital Proceeds – Assets as per the base cost

(Amounts in dollars)

Particulars Cost Base of Assets Capital Proceeds of

Assets

Net Capital Gain/

(Net Capital Loss)

Antique Vase 2,000 3000 1000 Gain

Antique Chair 3,000 1000 (2000) Loss

Painting 9,000 1000 (8000) Loss

Home Sound System 12,000 11000 (1000) Loss

Shares in listed

company

5,000 20000 15000 Gain

Total 5000 Net Capital

Gain

Hence, the total taxable capital gain for Eric for the year comes to $5,000.

Working Notes:

i. The overall collectibles have been acquired on an individual basis (cost ranks higher

than $5000) therefore will attract capital gain

ii. All the Personal use assets individually have been purchased at a cost more than $

10,000, hence they are applicable for taxable capital gain.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation

iii. Even the assets that are used personally are acquired at a cost that exceeds $10,000

and therefore capital gain is applicable

iv. The process of set off has occurred between the capital gain and the loss to determine

the net capital gain or loss (Hopewell, 2012).

4

iii. Even the assets that are used personally are acquired at a cost that exceeds $10,000

and therefore capital gain is applicable

iv. The process of set off has occurred between the capital gain and the loss to determine

the net capital gain or loss (Hopewell, 2012).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

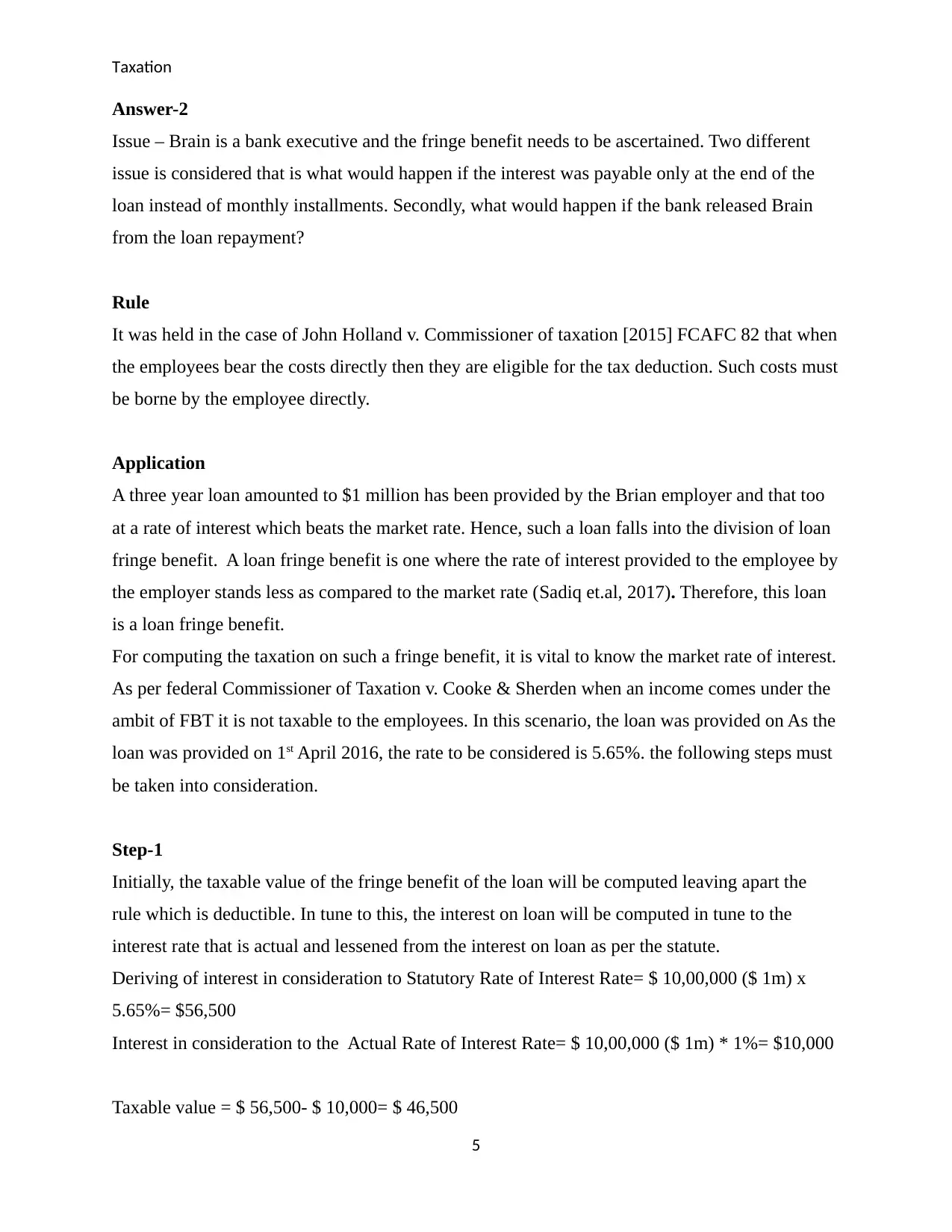

Answer-2

Issue – Brain is a bank executive and the fringe benefit needs to be ascertained. Two different

issue is considered that is what would happen if the interest was payable only at the end of the

loan instead of monthly installments. Secondly, what would happen if the bank released Brain

from the loan repayment?

Rule

It was held in the case of John Holland v. Commissioner of taxation [2015] FCAFC 82 that when

the employees bear the costs directly then they are eligible for the tax deduction. Such costs must

be borne by the employee directly.

Application

A three year loan amounted to $1 million has been provided by the Brian employer and that too

at a rate of interest which beats the market rate. Hence, such a loan falls into the division of loan

fringe benefit. A loan fringe benefit is one where the rate of interest provided to the employee by

the employer stands less as compared to the market rate (Sadiq et.al, 2017). Therefore, this loan

is a loan fringe benefit.

For computing the taxation on such a fringe benefit, it is vital to know the market rate of interest.

As per federal Commissioner of Taxation v. Cooke & Sherden when an income comes under the

ambit of FBT it is not taxable to the employees. In this scenario, the loan was provided on As the

loan was provided on 1st April 2016, the rate to be considered is 5.65%. the following steps must

be taken into consideration.

Step-1

Initially, the taxable value of the fringe benefit of the loan will be computed leaving apart the

rule which is deductible. In tune to this, the interest on loan will be computed in tune to the

interest rate that is actual and lessened from the interest on loan as per the statute.

Deriving of interest in consideration to Statutory Rate of Interest Rate= $ 10,00,000 ($ 1m) x

5.65%= $56,500

Interest in consideration to the Actual Rate of Interest Rate= $ 10,00,000 ($ 1m) * 1%= $10,000

Taxable value = $ 56,500- $ 10,000= $ 46,500

5

Answer-2

Issue – Brain is a bank executive and the fringe benefit needs to be ascertained. Two different

issue is considered that is what would happen if the interest was payable only at the end of the

loan instead of monthly installments. Secondly, what would happen if the bank released Brain

from the loan repayment?

Rule

It was held in the case of John Holland v. Commissioner of taxation [2015] FCAFC 82 that when

the employees bear the costs directly then they are eligible for the tax deduction. Such costs must

be borne by the employee directly.

Application

A three year loan amounted to $1 million has been provided by the Brian employer and that too

at a rate of interest which beats the market rate. Hence, such a loan falls into the division of loan

fringe benefit. A loan fringe benefit is one where the rate of interest provided to the employee by

the employer stands less as compared to the market rate (Sadiq et.al, 2017). Therefore, this loan

is a loan fringe benefit.

For computing the taxation on such a fringe benefit, it is vital to know the market rate of interest.

As per federal Commissioner of Taxation v. Cooke & Sherden when an income comes under the

ambit of FBT it is not taxable to the employees. In this scenario, the loan was provided on As the

loan was provided on 1st April 2016, the rate to be considered is 5.65%. the following steps must

be taken into consideration.

Step-1

Initially, the taxable value of the fringe benefit of the loan will be computed leaving apart the

rule which is deductible. In tune to this, the interest on loan will be computed in tune to the

interest rate that is actual and lessened from the interest on loan as per the statute.

Deriving of interest in consideration to Statutory Rate of Interest Rate= $ 10,00,000 ($ 1m) x

5.65%= $56,500

Interest in consideration to the Actual Rate of Interest Rate= $ 10,00,000 ($ 1m) * 1%= $10,000

Taxable value = $ 56,500- $ 10,000= $ 46,500

5

Taxation

Step-2

The computation of interest on loan in tune to the statutory interest rate will be done considering

that it was the only amount to be paid by Brian.

Statutory Rate of Interest Rate – interest = $ 10,00,000 ($ 1m) * 5.65%= $56,500

Step-3

The utilization of funds by Brian constitutes to 40% of the funds that is borrowed for the purpose

of income production and ensuring the interest payment are done properly. The figure of interest

expense that is subjected to tax deduction is as follows:

$ 56,500 * 40% = $ 22,600

Step-4

The borrowed funds are used to the capacity of 40% and this ensures the interest payments are

obliged. The tax deductible interest expense is as follows:

$ 10,000 * 40% = $ 4,000

Step- 5

Now, we shall deduct the actual deductible amount from the hypothetical deductible amount

$ 22,600 - $ 4,000= $18,600

Step-6

The final taxable amount shall be calculated by deducting amount in Step 5 from the amount in

Step 1

=$ 46,500 - $18,600= $27,900

Conclusion

If the interest was payable at the end of the loan rather than monthly installments then the

deemed period of this loan would have been treated from the period when interest will be paid or

will become payable.

In case the Bank released Brian from repaying the interest on the loan, the calculations will be

done as above mentioned steps keeping the actual interest rate as zero.

6

Step-2

The computation of interest on loan in tune to the statutory interest rate will be done considering

that it was the only amount to be paid by Brian.

Statutory Rate of Interest Rate – interest = $ 10,00,000 ($ 1m) * 5.65%= $56,500

Step-3

The utilization of funds by Brian constitutes to 40% of the funds that is borrowed for the purpose

of income production and ensuring the interest payment are done properly. The figure of interest

expense that is subjected to tax deduction is as follows:

$ 56,500 * 40% = $ 22,600

Step-4

The borrowed funds are used to the capacity of 40% and this ensures the interest payments are

obliged. The tax deductible interest expense is as follows:

$ 10,000 * 40% = $ 4,000

Step- 5

Now, we shall deduct the actual deductible amount from the hypothetical deductible amount

$ 22,600 - $ 4,000= $18,600

Step-6

The final taxable amount shall be calculated by deducting amount in Step 5 from the amount in

Step 1

=$ 46,500 - $18,600= $27,900

Conclusion

If the interest was payable at the end of the loan rather than monthly installments then the

deemed period of this loan would have been treated from the period when interest will be paid or

will become payable.

In case the Bank released Brian from repaying the interest on the loan, the calculations will be

done as above mentioned steps keeping the actual interest rate as zero.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation

Answer-3

Issue

Jack incurred loss in the property and the determination of tax will be done for the purpose of

tax. The case determines how capital gain or loss will come into the picture?

Rule

Money is being borrowed by Jack and Jill to purchase a rental property. As per the agreement

made between Jack & Jill to borrow money to purchase a rental property as joint tenants, the

agreement was that Jack shall be entitled to 10%of profits against 90% profits to his wife Jill. In

case loss took place, Jack agreed to bear the entire loss. As in last year, there has been a loss of

10000$ and as per the agreement agreed among Jack & Jill, the entire loss shall be borne by

Jack. Similar case was observed in the case of Bowden v Los and Ors [1998] NSWSC 216.

This loss shall be added along with Jack’s other income if any and shall help in reduction of total

income and tax as well. In case there is no other income this loss can also be allowed to be

carried forward (Thorpe, 2012).

Application

Two situations can crop up when there is a talk of selling the property. In case of a gain, the same

shall be distributed among Jack and Jill in the ratio of 10: 90 respectively. Jack shall be able to

set off his loss of $ 10,000 of last year against the gain arising out of selling of the property. On

the other hand, in case there is a loss by selling the property, the entire loss shall be born by Jack

and it shall be set off or allowed to be carried forward to next year to be adjusted with other

incomes (Kenny, et. al, 2017).

Conclusion

So, the net result is that Jack shall be able to set off his loss of last year in the current year only if

there is some gain against selling of the property but in case the selling of property does not

provide any gains as per their agreement, Jack shall bear the entire loss and Jill shall not be

required to bear any loss (Kobestky, 2005). Hence, tax treatment shall not affect Jill in any way

while Jack shall have to book the loss in his books of accounts.

7

Answer-3

Issue

Jack incurred loss in the property and the determination of tax will be done for the purpose of

tax. The case determines how capital gain or loss will come into the picture?

Rule

Money is being borrowed by Jack and Jill to purchase a rental property. As per the agreement

made between Jack & Jill to borrow money to purchase a rental property as joint tenants, the

agreement was that Jack shall be entitled to 10%of profits against 90% profits to his wife Jill. In

case loss took place, Jack agreed to bear the entire loss. As in last year, there has been a loss of

10000$ and as per the agreement agreed among Jack & Jill, the entire loss shall be borne by

Jack. Similar case was observed in the case of Bowden v Los and Ors [1998] NSWSC 216.

This loss shall be added along with Jack’s other income if any and shall help in reduction of total

income and tax as well. In case there is no other income this loss can also be allowed to be

carried forward (Thorpe, 2012).

Application

Two situations can crop up when there is a talk of selling the property. In case of a gain, the same

shall be distributed among Jack and Jill in the ratio of 10: 90 respectively. Jack shall be able to

set off his loss of $ 10,000 of last year against the gain arising out of selling of the property. On

the other hand, in case there is a loss by selling the property, the entire loss shall be born by Jack

and it shall be set off or allowed to be carried forward to next year to be adjusted with other

incomes (Kenny, et. al, 2017).

Conclusion

So, the net result is that Jack shall be able to set off his loss of last year in the current year only if

there is some gain against selling of the property but in case the selling of property does not

provide any gains as per their agreement, Jack shall bear the entire loss and Jill shall not be

required to bear any loss (Kobestky, 2005). Hence, tax treatment shall not affect Jill in any way

while Jack shall have to book the loss in his books of accounts.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

Answer- 4

Issue

Relevancy of the principle of IRC v Duke of Westminster [1936] AC 1

Rule

As per the case of IRC v Duke of Westminster [1936] AC 1, the principle that came into view is

as follows:

Every person has a right to manage his accounts and affairs in such a manner that the tax on his

total income can be minimized to the maximum possible. And if he succeeds in doing so legally

then no matter what the commissioners of the Inland Revenue may find inappropriate he cannot

be compelled to increase his tax amount payable (Saunders, 2015).

Application

This rule was only applicable if the taxpayer arranges his accounts and affairs in only such

manner which is compliant with the laws laid down in the income tax rules and by the courts.

And if the documents and transaction details provide by the taxpayer are genuine, then the courts

shall not go behind these details on the basis of some underlying substance.

It means that the case has given following principles:

i. Every person has the right to manage his books of accounts in every possible manner

in order to reduce the tax payable to the minimum.

ii. If no window dressing or fault is found from the accounts, then there will be no

additional tax (Renton, 2005).

iii. No one can question the transactions if these are legally effective on the ground that

the substance of the transaction is different from that interpreted by the taxpayer

(Fullerton et. al, 2017).

This rule was not overruled but with the passage of time and other new case laws coming into

effect, the said case lost its worth somehow. And now the perspective of viewing the accounts

has been differentiated.

Relevance of the rule in present scenario-

8

Answer- 4

Issue

Relevancy of the principle of IRC v Duke of Westminster [1936] AC 1

Rule

As per the case of IRC v Duke of Westminster [1936] AC 1, the principle that came into view is

as follows:

Every person has a right to manage his accounts and affairs in such a manner that the tax on his

total income can be minimized to the maximum possible. And if he succeeds in doing so legally

then no matter what the commissioners of the Inland Revenue may find inappropriate he cannot

be compelled to increase his tax amount payable (Saunders, 2015).

Application

This rule was only applicable if the taxpayer arranges his accounts and affairs in only such

manner which is compliant with the laws laid down in the income tax rules and by the courts.

And if the documents and transaction details provide by the taxpayer are genuine, then the courts

shall not go behind these details on the basis of some underlying substance.

It means that the case has given following principles:

i. Every person has the right to manage his books of accounts in every possible manner

in order to reduce the tax payable to the minimum.

ii. If no window dressing or fault is found from the accounts, then there will be no

additional tax (Renton, 2005).

iii. No one can question the transactions if these are legally effective on the ground that

the substance of the transaction is different from that interpreted by the taxpayer

(Fullerton et. al, 2017).

This rule was not overruled but with the passage of time and other new case laws coming into

effect, the said case lost its worth somehow. And now the perspective of viewing the accounts

has been differentiated.

Relevance of the rule in present scenario-

8

Taxation

Conclusion

In the present scenario, this rule holds true as it not only restricts businesses from manipulating

facts and figures but also gives them a right to legally do business genuinely. For example, if a

business is undergoing losses and not able to repay the debts, the business can alter the figures of

the balance sheet and the fixed assets can be written off to the extent of the carrying value.

In this case, even if the business does not have any valid document to prove this transaction,

continuous losses and inability to pay dues and debts, it will be appropriate and justified enough

to write off fixed assets, but in case of business tries to manipulate and hide substantial facts

from the stakeholders, the above law shall restrict the business to hide or manipulate things

(Fullerton et. al, 2017). Any decision or transaction which helps in running a business effectively

in a legalized manner not evading any taxes it shall be absolutely perfect to do so.

9

Conclusion

In the present scenario, this rule holds true as it not only restricts businesses from manipulating

facts and figures but also gives them a right to legally do business genuinely. For example, if a

business is undergoing losses and not able to repay the debts, the business can alter the figures of

the balance sheet and the fixed assets can be written off to the extent of the carrying value.

In this case, even if the business does not have any valid document to prove this transaction,

continuous losses and inability to pay dues and debts, it will be appropriate and justified enough

to write off fixed assets, but in case of business tries to manipulate and hide substantial facts

from the stakeholders, the above law shall restrict the business to hide or manipulate things

(Fullerton et. al, 2017). Any decision or transaction which helps in running a business effectively

in a legalized manner not evading any taxes it shall be absolutely perfect to do so.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation

Answer-5

Issue

Whether Bill will be assessable for the receipts received for the arrangement?

Rule

A piece of land is being owned where there are many tall pine trees. His intention is to use that

land for grazing sheep but for this, he has to clear the entire pine trees. He shall receive $ 1000

for every 100 meters of timber from a logging company. So now the question is that whether

there arises any tax on receipts from the logging company. As there is not mentioned in the

question that what is the total amount of receipts out of clearing of timber. We can treat this as a

revenue receipt and there shall not be any capital gain tax issue in this matter. These receipts

shall be treated as revenue receipts of the bill (Barcokzy, 2010). Similar instance was held in the

case of case of Hastle Group Limited v Commissioner of Taxation 2009 ATC

Application

If Bill paid a total sum of $50000 that grants a right to the logging company to eliminate timber

from the land, this can be treated as a capital receipt as it is an overall payment and there is no

receipt of a recurring nature. Lastly, it appears due to the fact that providing or selling timber is

from the own land hence, capital in nature. Moreover, in the second case, it will be considered as

lump sum receipt and put under the capital gain taxation (Pratt & Kulsrud, 2013).

Conclusion

In both the cases, Bill shall receive the sum of money. In the first case, the receipt shall be small

but recurring while in the second case, where he agrees to give his right to cut as much as timber

to the logging company against a lump sum of $ 50,000,it is a big but one time receipt because

once the timber has been removed, it shall take a long time to grow again. So as Bill is in receipt

of huge money against giving his right, this may be treated as selling of an asset to the company

and selling of asset incurred capital gain tax (Barcokzy, 2010). While in the first case it shall be

treated under normal tax rates.

10

Answer-5

Issue

Whether Bill will be assessable for the receipts received for the arrangement?

Rule

A piece of land is being owned where there are many tall pine trees. His intention is to use that

land for grazing sheep but for this, he has to clear the entire pine trees. He shall receive $ 1000

for every 100 meters of timber from a logging company. So now the question is that whether

there arises any tax on receipts from the logging company. As there is not mentioned in the

question that what is the total amount of receipts out of clearing of timber. We can treat this as a

revenue receipt and there shall not be any capital gain tax issue in this matter. These receipts

shall be treated as revenue receipts of the bill (Barcokzy, 2010). Similar instance was held in the

case of case of Hastle Group Limited v Commissioner of Taxation 2009 ATC

Application

If Bill paid a total sum of $50000 that grants a right to the logging company to eliminate timber

from the land, this can be treated as a capital receipt as it is an overall payment and there is no

receipt of a recurring nature. Lastly, it appears due to the fact that providing or selling timber is

from the own land hence, capital in nature. Moreover, in the second case, it will be considered as

lump sum receipt and put under the capital gain taxation (Pratt & Kulsrud, 2013).

Conclusion

In both the cases, Bill shall receive the sum of money. In the first case, the receipt shall be small

but recurring while in the second case, where he agrees to give his right to cut as much as timber

to the logging company against a lump sum of $ 50,000,it is a big but one time receipt because

once the timber has been removed, it shall take a long time to grow again. So as Bill is in receipt

of huge money against giving his right, this may be treated as selling of an asset to the company

and selling of asset incurred capital gain tax (Barcokzy, 2010). While in the first case it shall be

treated under normal tax rates.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

References

Barcokzy, S 2010, Australian Tax Casebook, CCH Australia Ltd

Fullerton,I.G, Deutsch, R, Friezer, M.L, Hanley,P & Snape, T 2017, The Australian Tax

Handbook Tax Return Edition 2017, Thomson Reuters: Australia

Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 27 August 2017,

www.zdnet.com.au.

Kenny, P, Blissenden, M, & Villios, S 2016, Australian Tax 2017, Thomson Reuters: Australia

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation

Press

Nethercott, L, Richardson, G & Devos,K. 2013, Australian Taxation Study Manual, Sydney.

Pratt, J. W & Kulsrud, W N 2013, Federal Taxation, Oxford university press.

Renton N.E 2005, Income Tax and Investment, 2nd edition, Sydney

Sadiq, K, Coleman, C , Hanegbi, R, Jogarajan,S, Krever, R, Obst, R, Teoh, J & Ting, A

2017, Principles of Taxation Law 2017, Law book Australia

Sadiq, K, Coleman, C, Hanegbi, R., Jogarajan,S, Krever, R.,Obst, W.,& Ting, A 2014,

Principles of Taxation Law, Sydney.

Saunders, C 2015, The Australian Constitution, Carlton: Constitutional Centenary Foundation

Thorpe, C 2012, Tax Pack dumped online returns encouraged ABC News, viewed 25 August

2017 http://www.abc.net.au/news/2012-07-09/tax-pack-dumped-online-returns-encouraged/

4117784

11

References

Barcokzy, S 2010, Australian Tax Casebook, CCH Australia Ltd

Fullerton,I.G, Deutsch, R, Friezer, M.L, Hanley,P & Snape, T 2017, The Australian Tax

Handbook Tax Return Edition 2017, Thomson Reuters: Australia

Hopewell, L 2012, Australia tax inquiry opens submissions, viewed 27 August 2017,

www.zdnet.com.au.

Kenny, P, Blissenden, M, & Villios, S 2016, Australian Tax 2017, Thomson Reuters: Australia

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation

Press

Nethercott, L, Richardson, G & Devos,K. 2013, Australian Taxation Study Manual, Sydney.

Pratt, J. W & Kulsrud, W N 2013, Federal Taxation, Oxford university press.

Renton N.E 2005, Income Tax and Investment, 2nd edition, Sydney

Sadiq, K, Coleman, C , Hanegbi, R, Jogarajan,S, Krever, R, Obst, R, Teoh, J & Ting, A

2017, Principles of Taxation Law 2017, Law book Australia

Sadiq, K, Coleman, C, Hanegbi, R., Jogarajan,S, Krever, R.,Obst, W.,& Ting, A 2014,

Principles of Taxation Law, Sydney.

Saunders, C 2015, The Australian Constitution, Carlton: Constitutional Centenary Foundation

Thorpe, C 2012, Tax Pack dumped online returns encouraged ABC News, viewed 25 August

2017 http://www.abc.net.au/news/2012-07-09/tax-pack-dumped-online-returns-encouraged/

4117784

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.