Taxation Report: Capital Gains, Losses and Tax Implications Analysis

VerifiedAdded on 2023/06/05

|10

|1676

|385

Report

AI Summary

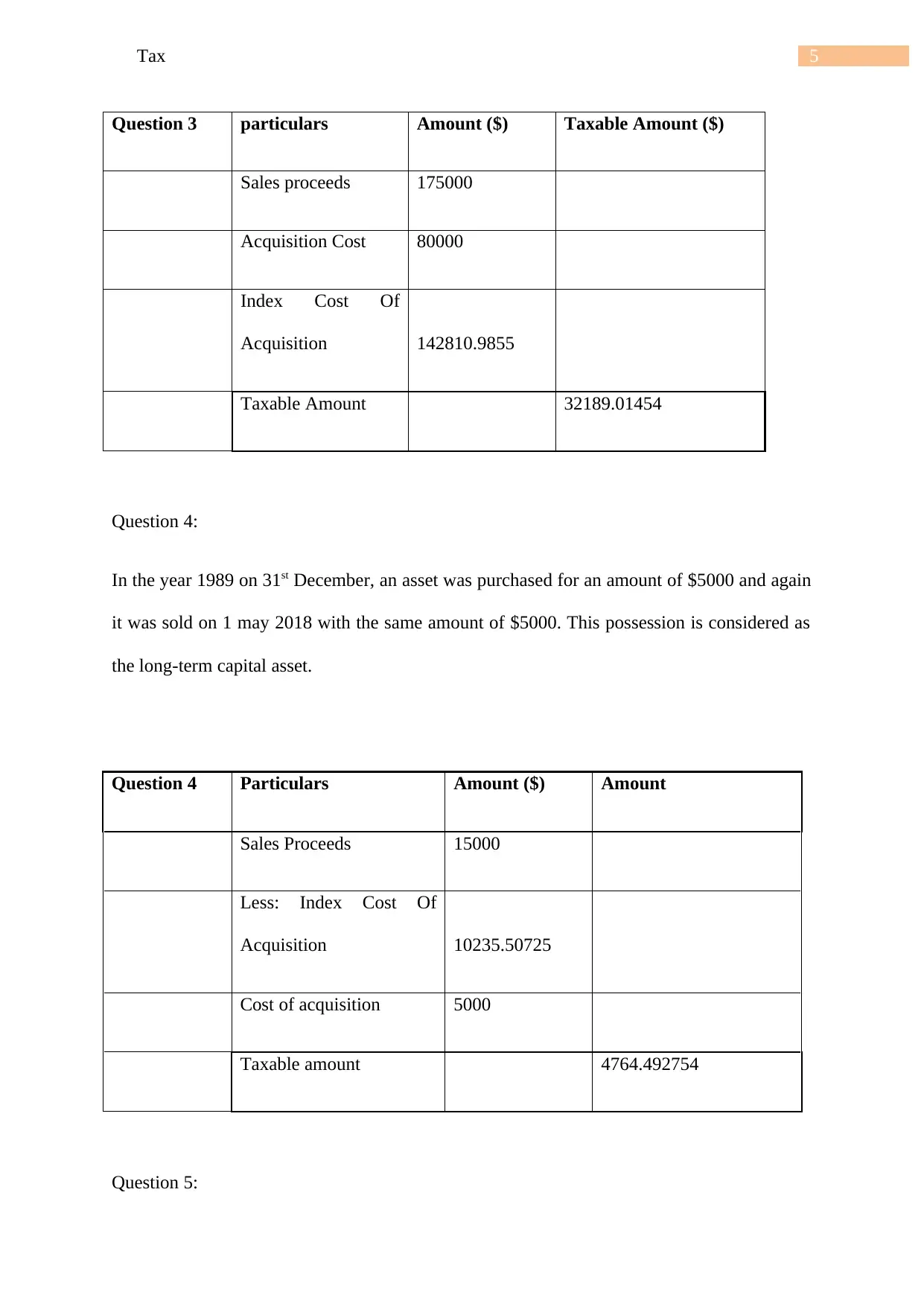

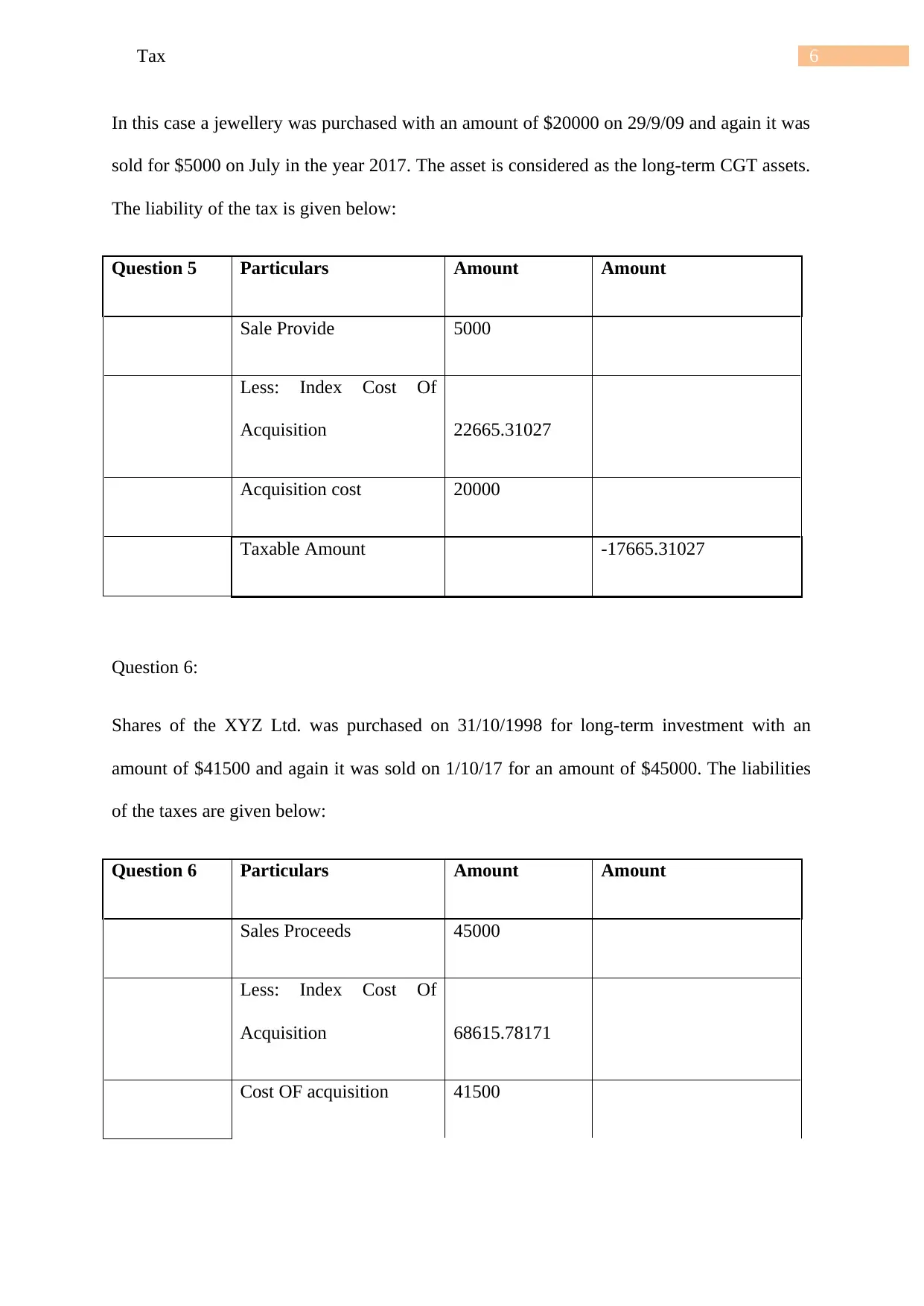

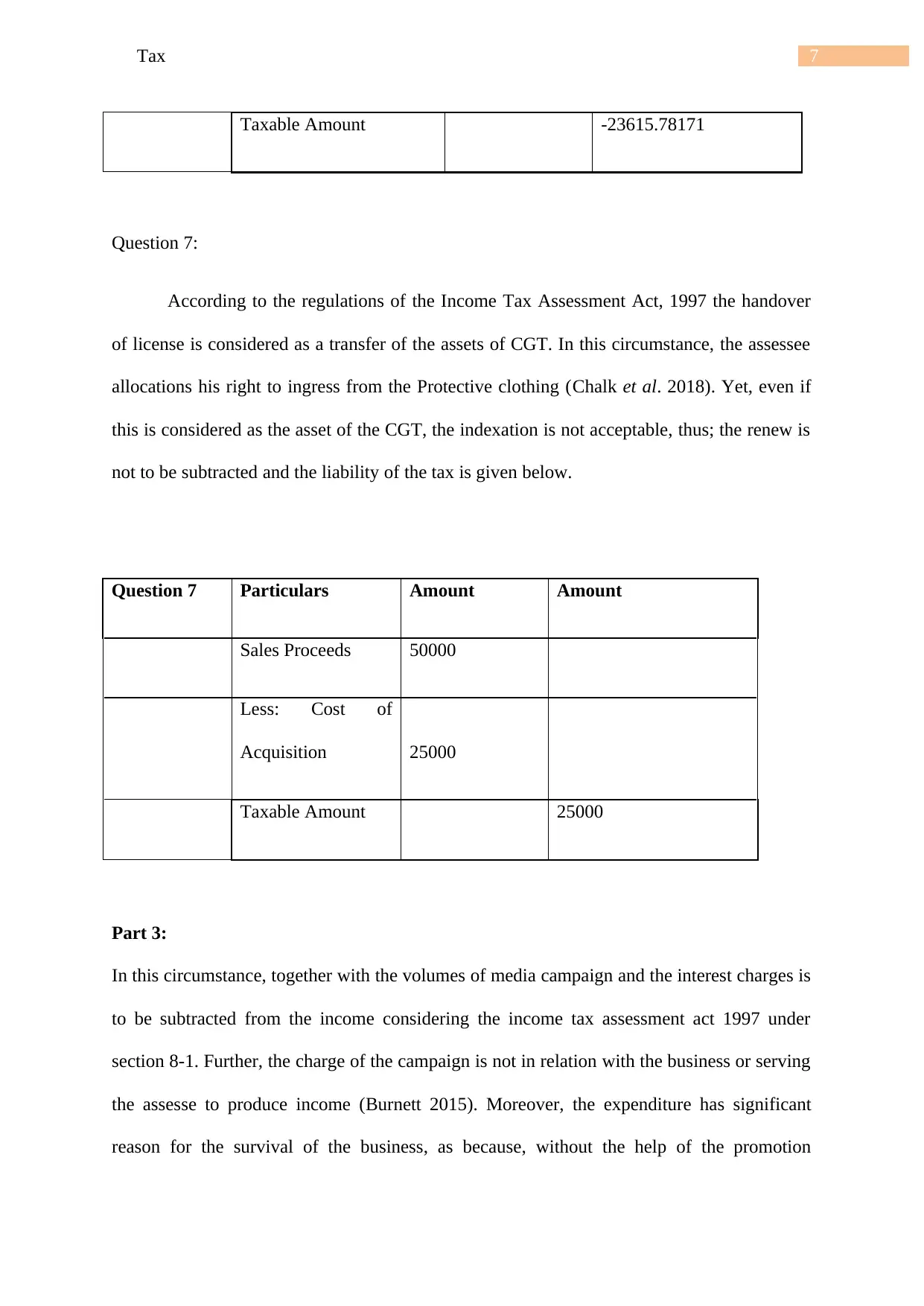

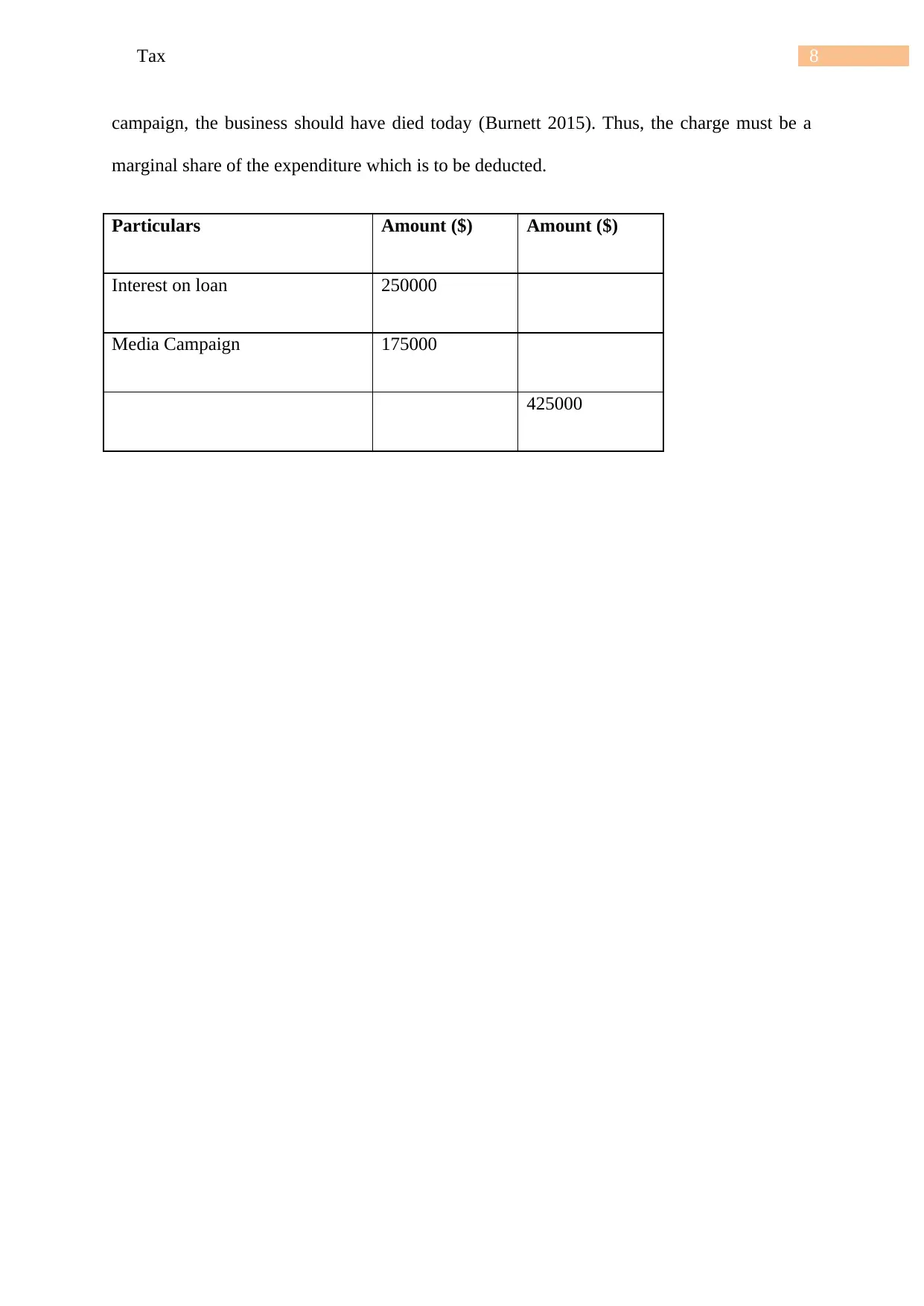

This tax report analyzes various scenarios involving capital gains and losses, offering insights into the Income Tax Assessment Act 1997. The report begins by outlining the residential position for taxation, considering factors like incorporation, control, and central management, referencing the case of Ors V Commissioner of Taxation and Baywater Investments Ltd. It then delves into calculating taxable amounts, including the impact of bad debts and indexation on capital gains. Several questions are addressed, examining the tax implications of different asset types, such as land, shares, and jewelry, and determining whether the assets are CGT assets. The report also discusses the treatment of various assets like shares and licenses, calculating the taxable amount and providing detailed calculations for each scenario, showcasing the application of relevant tax regulations. Finally, the report concludes by analyzing the deductibility of expenses, such as interest on loans and media campaigns, in relation to the Income Tax Assessment Act.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.