Tax Compliance Obligations and Analysis for Victorian Flight Academy

VerifiedAdded on 2020/10/05

|13

|4431

|248

Report

AI Summary

This report provides a comprehensive analysis of tax compliance for the Victorian Flight Academy (VFA). It begins with an introduction to Australian taxation and the role of the Australian Taxation Office (ATO). The main body of the report details the necessary documentation required for tax compliance, including financial records (receipts, invoices, bank statements), legal records (business registration, leases, contracts), and employee records (salaries, superannuation). It also covers the importance of policies and procedures related to taxation, such as workplace health and safety plans and GST applications. The report then analyzes tax issues faced by VFA, particularly concerning employee bonuses and their impact on the company's profitability, referencing a case study of Merrill Lynch International Australia Ltd V Commissioner of Taxation, discussing the timing of bonus payments and their deductibility. The report highlights the importance of accurate record-keeping, adherence to tax regulations, and the potential consequences of non-compliance. Finally, the report offers recommendations based on the analysis. The report aims to guide VFA in meeting its tax obligations and mitigating potential risks.

Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Necessary documentation to meet tax compliance obligations..............................................1

B. Analysing Tax Issues : .....................................................................................................5

Issue:.......................................................................................................................................5

Rule: ......................................................................................................................................6

Applications:...........................................................................................................................7

Conclusion:.............................................................................................................................8

Recommendations:...........................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Necessary documentation to meet tax compliance obligations..............................................1

B. Analysing Tax Issues : .....................................................................................................5

Issue:.......................................................................................................................................5

Rule: ......................................................................................................................................6

Applications:...........................................................................................................................7

Conclusion:.............................................................................................................................8

Recommendations:...........................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Australian taxation is a tax compliance which implies under the demography of

Australia. All rules, regulations, compliances and other matters related to tax are governed by

statutory body of Australian taxation office. In this project report, case scenario of Victorian

Flight Academy is analysed along with their strategic business transactions and key client

matters. Various documentation are prepared to meet the tax compliances in this report along

with suitable taxation laws and regulations. A letter of advice is also developed and presented to

VFA as a tax agent. This letter includes relevant tax issues, taxation treatment and more

moreover research on a case study of Merrill Lynch (Australia) Ltd. Vs commissioner of

taxation. The Merrill Lynch Ltd. was an American MNC continuing the business in several

countries the head office of Merrill lynch was in new york, the company had world wide region

relevant to this case was the “Asia pacific” or “Australian region”not only this other operations

also in form of “business group” or “business units”. the case study belong to the its Australian

branch and of year 1994. The Merrill Lynch International Ltd. had declared to paid bonuses to

their employees at the end of year 1994 . But the bonuses were not paid until late January 1995.

the case study regarding the Australian taxation.

MAIN BODY

Necessary documentation to meet tax compliance obligations

Case Scenario:

VFA is a flying school which usually earns reasonable amount of profit but due to recent

low admission of students they has faced losses and has incurred total tax loss of 190000 dollars.

In order to provide an understanding about their tax compliances, various documents are

prepared which are mandatory to be developed according to Australian tax.

Tax compliance and obligations :

Tax compliance means meeting the tax obligations as mentioned by the law wholly and .

Tax compliance refers to submitting a tax return within the specified period, correctly stating

income and deductions, pay taxes which are due date and payment of taxes. Moreover, tax

compliance refers to which a taxpayer complies with the tax rules of Australia or any other

country from which the organisation belongs to, for example by declaring income, filing income,

filling a return and paying the tax due on time. the organisation operating without required tax

1

Australian taxation is a tax compliance which implies under the demography of

Australia. All rules, regulations, compliances and other matters related to tax are governed by

statutory body of Australian taxation office. In this project report, case scenario of Victorian

Flight Academy is analysed along with their strategic business transactions and key client

matters. Various documentation are prepared to meet the tax compliances in this report along

with suitable taxation laws and regulations. A letter of advice is also developed and presented to

VFA as a tax agent. This letter includes relevant tax issues, taxation treatment and more

moreover research on a case study of Merrill Lynch (Australia) Ltd. Vs commissioner of

taxation. The Merrill Lynch Ltd. was an American MNC continuing the business in several

countries the head office of Merrill lynch was in new york, the company had world wide region

relevant to this case was the “Asia pacific” or “Australian region”not only this other operations

also in form of “business group” or “business units”. the case study belong to the its Australian

branch and of year 1994. The Merrill Lynch International Ltd. had declared to paid bonuses to

their employees at the end of year 1994 . But the bonuses were not paid until late January 1995.

the case study regarding the Australian taxation.

MAIN BODY

Necessary documentation to meet tax compliance obligations

Case Scenario:

VFA is a flying school which usually earns reasonable amount of profit but due to recent

low admission of students they has faced losses and has incurred total tax loss of 190000 dollars.

In order to provide an understanding about their tax compliances, various documents are

prepared which are mandatory to be developed according to Australian tax.

Tax compliance and obligations :

Tax compliance means meeting the tax obligations as mentioned by the law wholly and .

Tax compliance refers to submitting a tax return within the specified period, correctly stating

income and deductions, pay taxes which are due date and payment of taxes. Moreover, tax

compliance refers to which a taxpayer complies with the tax rules of Australia or any other

country from which the organisation belongs to, for example by declaring income, filing income,

filling a return and paying the tax due on time. the organisation operating without required tax

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

registrations (as made mandatory by Australian tax authority) or failing to file tax returns in

timely manner will potentially exposed the business to interest and penalties. Moreover,

regulatory and tax obligations vary according to the type of entity structure, means type of

business activities performed by business (Piketty, Saez and Stantcheva, 2014).

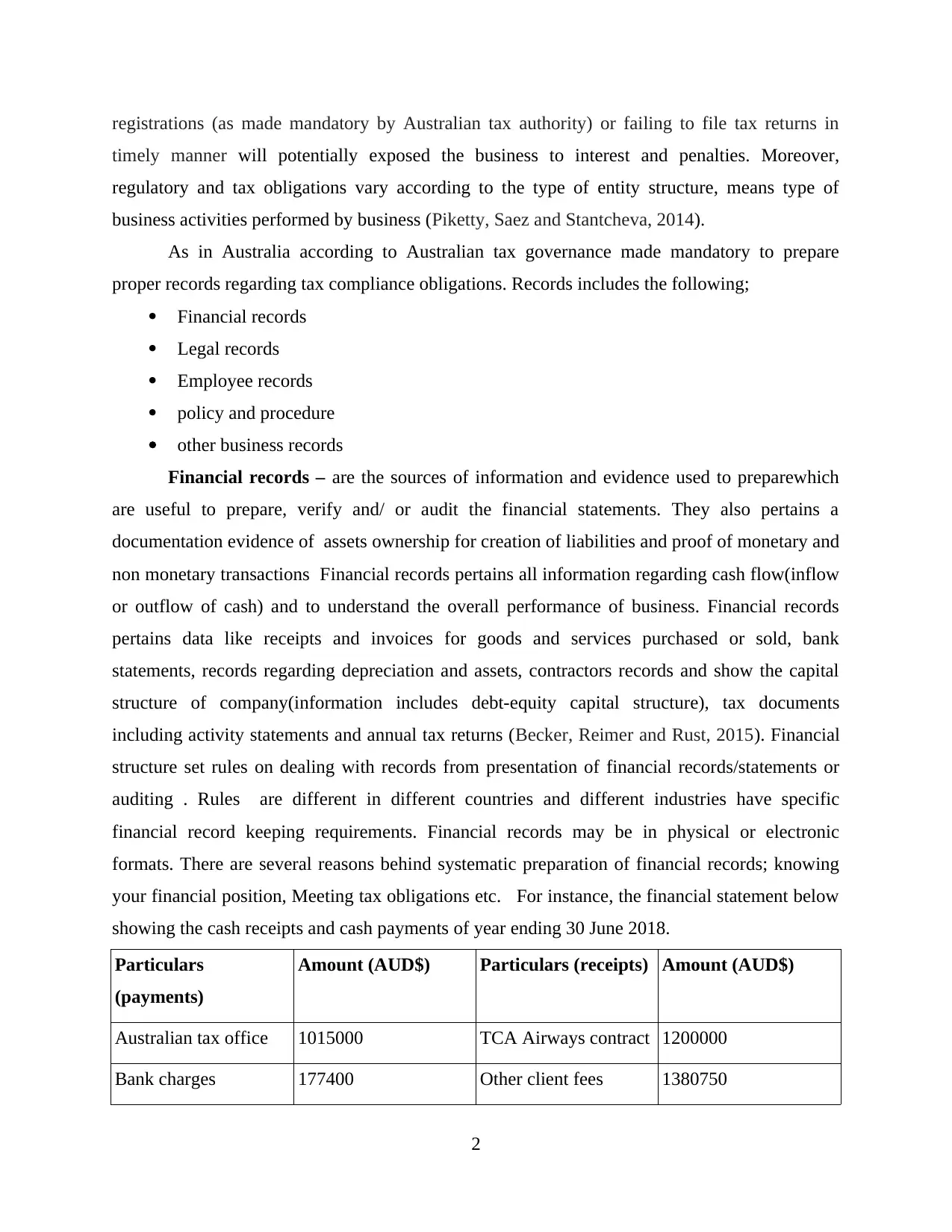

As in Australia according to Australian tax governance made mandatory to prepare

proper records regarding tax compliance obligations. Records includes the following;

Financial records

Legal records

Employee records

policy and procedure

other business records

Financial records – are the sources of information and evidence used to preparewhich

are useful to prepare, verify and/ or audit the financial statements. They also pertains a

documentation evidence of assets ownership for creation of liabilities and proof of monetary and

non monetary transactions Financial records pertains all information regarding cash flow(inflow

or outflow of cash) and to understand the overall performance of business. Financial records

pertains data like receipts and invoices for goods and services purchased or sold, bank

statements, records regarding depreciation and assets, contractors records and show the capital

structure of company(information includes debt-equity capital structure), tax documents

including activity statements and annual tax returns (Becker, Reimer and Rust, 2015). Financial

structure set rules on dealing with records from presentation of financial records/statements or

auditing . Rules are different in different countries and different industries have specific

financial record keeping requirements. Financial records may be in physical or electronic

formats. There are several reasons behind systematic preparation of financial records; knowing

your financial position, Meeting tax obligations etc. For instance, the financial statement below

showing the cash receipts and cash payments of year ending 30 June 2018.

Particulars

(payments)

Amount (AUD$) Particulars (receipts) Amount (AUD$)

Australian tax office 1015000 TCA Airways contract 1200000

Bank charges 177400 Other client fees 1380750

2

timely manner will potentially exposed the business to interest and penalties. Moreover,

regulatory and tax obligations vary according to the type of entity structure, means type of

business activities performed by business (Piketty, Saez and Stantcheva, 2014).

As in Australia according to Australian tax governance made mandatory to prepare

proper records regarding tax compliance obligations. Records includes the following;

Financial records

Legal records

Employee records

policy and procedure

other business records

Financial records – are the sources of information and evidence used to preparewhich

are useful to prepare, verify and/ or audit the financial statements. They also pertains a

documentation evidence of assets ownership for creation of liabilities and proof of monetary and

non monetary transactions Financial records pertains all information regarding cash flow(inflow

or outflow of cash) and to understand the overall performance of business. Financial records

pertains data like receipts and invoices for goods and services purchased or sold, bank

statements, records regarding depreciation and assets, contractors records and show the capital

structure of company(information includes debt-equity capital structure), tax documents

including activity statements and annual tax returns (Becker, Reimer and Rust, 2015). Financial

structure set rules on dealing with records from presentation of financial records/statements or

auditing . Rules are different in different countries and different industries have specific

financial record keeping requirements. Financial records may be in physical or electronic

formats. There are several reasons behind systematic preparation of financial records; knowing

your financial position, Meeting tax obligations etc. For instance, the financial statement below

showing the cash receipts and cash payments of year ending 30 June 2018.

Particulars

(payments)

Amount (AUD$) Particulars (receipts) Amount (AUD$)

Australian tax office 1015000 TCA Airways contract 1200000

Bank charges 177400 Other client fees 1380750

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

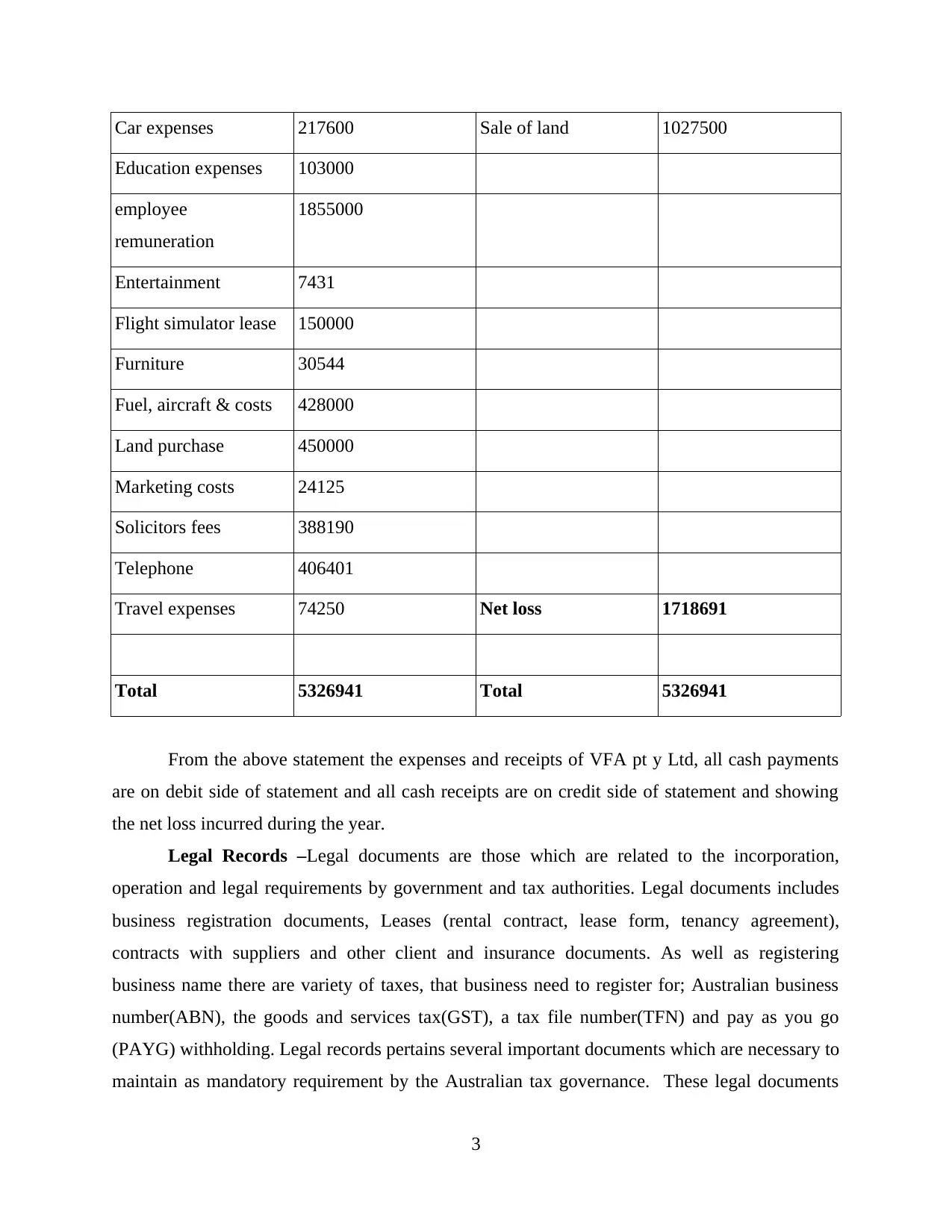

Car expenses 217600 Sale of land 1027500

Education expenses 103000

employee

remuneration

1855000

Entertainment 7431

Flight simulator lease 150000

Furniture 30544

Fuel, aircraft & costs 428000

Land purchase 450000

Marketing costs 24125

Solicitors fees 388190

Telephone 406401

Travel expenses 74250 Net loss 1718691

Total 5326941 Total 5326941

From the above statement the expenses and receipts of VFA pt y Ltd, all cash payments

are on debit side of statement and all cash receipts are on credit side of statement and showing

the net loss incurred during the year.

Legal Records –Legal documents are those which are related to the incorporation,

operation and legal requirements by government and tax authorities. Legal documents includes

business registration documents, Leases (rental contract, lease form, tenancy agreement),

contracts with suppliers and other client and insurance documents. As well as registering

business name there are variety of taxes, that business need to register for; Australian business

number(ABN), the goods and services tax(GST), a tax file number(TFN) and pay as you go

(PAYG) withholding. Legal records pertains several important documents which are necessary to

maintain as mandatory requirement by the Australian tax governance. These legal documents

3

Education expenses 103000

employee

remuneration

1855000

Entertainment 7431

Flight simulator lease 150000

Furniture 30544

Fuel, aircraft & costs 428000

Land purchase 450000

Marketing costs 24125

Solicitors fees 388190

Telephone 406401

Travel expenses 74250 Net loss 1718691

Total 5326941 Total 5326941

From the above statement the expenses and receipts of VFA pt y Ltd, all cash payments

are on debit side of statement and all cash receipts are on credit side of statement and showing

the net loss incurred during the year.

Legal Records –Legal documents are those which are related to the incorporation,

operation and legal requirements by government and tax authorities. Legal documents includes

business registration documents, Leases (rental contract, lease form, tenancy agreement),

contracts with suppliers and other client and insurance documents. As well as registering

business name there are variety of taxes, that business need to register for; Australian business

number(ABN), the goods and services tax(GST), a tax file number(TFN) and pay as you go

(PAYG) withholding. Legal records pertains several important documents which are necessary to

maintain as mandatory requirement by the Australian tax governance. These legal documents

3

not depicts the legal existence of the organisation but also helps in smooth functioning. These

legal documents shows that the organisation is a separate legal entity distinct from its members.

Means after the legal documentation the organisation works as an artificial person, created by or

under law, perpetual succession, legal personality and a common seal . Moreover legal

personality means company can make transactions by its own name and can sue or can be sued

by its own name. (Pomeranz, Wallace, Piketty 2015 )

In case VFA committed with a lease contract and perform all legal requirements, As mentioned

in given information VFA leased a special flight simulator from Flight Services Ltd. The lease

agreement contracted VFA for the period of five years for a cost of $150,000 per annum. And

also GST as included in all amounts mentioned above.

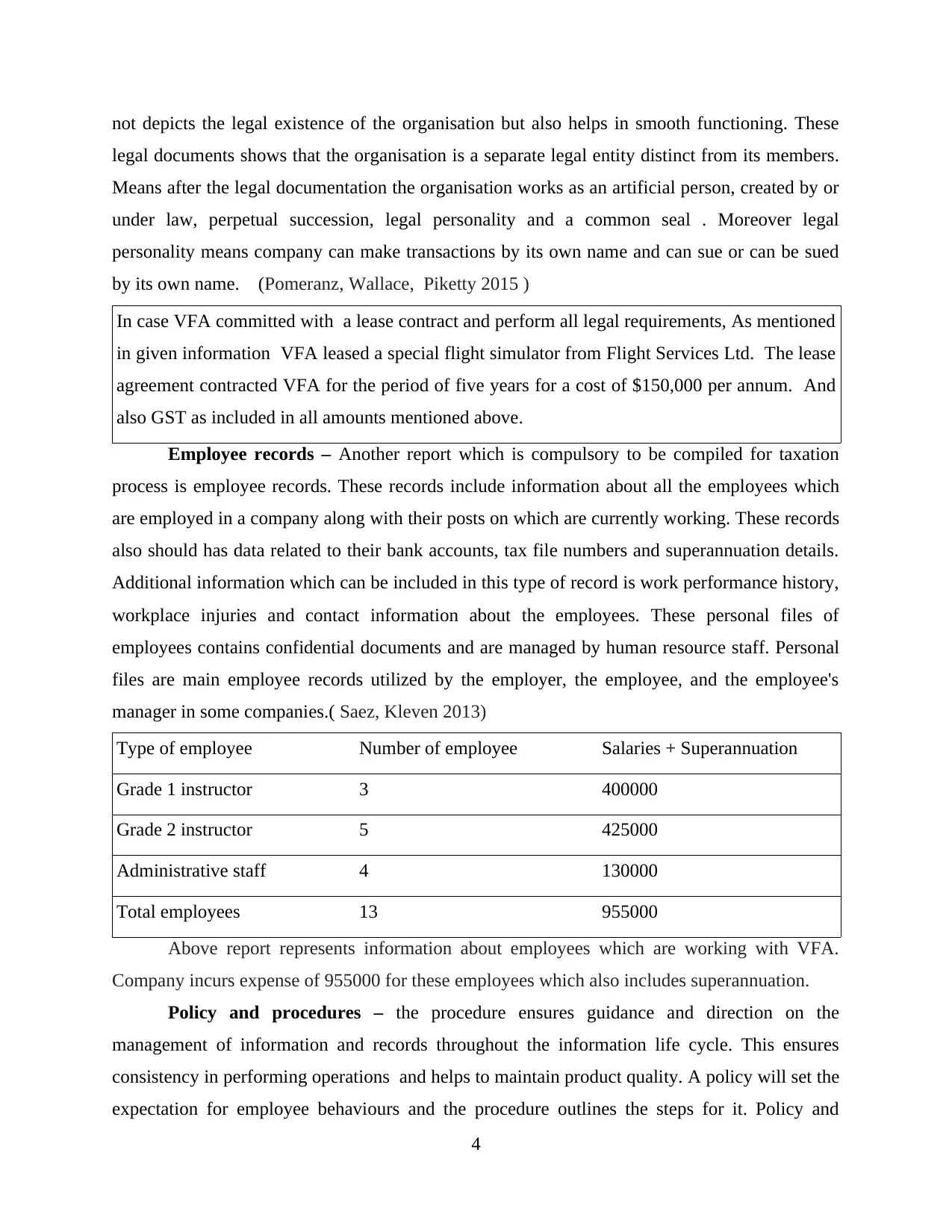

Employee records – Another report which is compulsory to be compiled for taxation

process is employee records. These records include information about all the employees which

are employed in a company along with their posts on which are currently working. These records

also should has data related to their bank accounts, tax file numbers and superannuation details.

Additional information which can be included in this type of record is work performance history,

workplace injuries and contact information about the employees. These personal files of

employees contains confidential documents and are managed by human resource staff. Personal

files are main employee records utilized by the employer, the employee, and the employee's

manager in some companies.( Saez, Kleven 2013)

Type of employee Number of employee Salaries + Superannuation

Grade 1 instructor 3 400000

Grade 2 instructor 5 425000

Administrative staff 4 130000

Total employees 13 955000

Above report represents information about employees which are working with VFA.

Company incurs expense of 955000 for these employees which also includes superannuation.

Policy and procedures – the procedure ensures guidance and direction on the

management of information and records throughout the information life cycle. This ensures

consistency in performing operations and helps to maintain product quality. A policy will set the

expectation for employee behaviours and the procedure outlines the steps for it. Policy and

4

legal documents shows that the organisation is a separate legal entity distinct from its members.

Means after the legal documentation the organisation works as an artificial person, created by or

under law, perpetual succession, legal personality and a common seal . Moreover legal

personality means company can make transactions by its own name and can sue or can be sued

by its own name. (Pomeranz, Wallace, Piketty 2015 )

In case VFA committed with a lease contract and perform all legal requirements, As mentioned

in given information VFA leased a special flight simulator from Flight Services Ltd. The lease

agreement contracted VFA for the period of five years for a cost of $150,000 per annum. And

also GST as included in all amounts mentioned above.

Employee records – Another report which is compulsory to be compiled for taxation

process is employee records. These records include information about all the employees which

are employed in a company along with their posts on which are currently working. These records

also should has data related to their bank accounts, tax file numbers and superannuation details.

Additional information which can be included in this type of record is work performance history,

workplace injuries and contact information about the employees. These personal files of

employees contains confidential documents and are managed by human resource staff. Personal

files are main employee records utilized by the employer, the employee, and the employee's

manager in some companies.( Saez, Kleven 2013)

Type of employee Number of employee Salaries + Superannuation

Grade 1 instructor 3 400000

Grade 2 instructor 5 425000

Administrative staff 4 130000

Total employees 13 955000

Above report represents information about employees which are working with VFA.

Company incurs expense of 955000 for these employees which also includes superannuation.

Policy and procedures – the procedure ensures guidance and direction on the

management of information and records throughout the information life cycle. This ensures

consistency in performing operations and helps to maintain product quality. A policy will set the

expectation for employee behaviours and the procedure outlines the steps for it. Policy and

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

procedures ensures articulation of required steps, performance measures, process consistency,

serve as a training tool, incorporates workers experience, training refreshers, foundation for

process improvement. Under this report, company has to mention all the policies and procedures

which are followed by their management and can affect their material information. All tax

related rules and regulations are mandatory to be filed to complete tax compliance method.

According to Australian Taxation Office, procedures and policies which are necessary to be

included in this report are work place health and safety plans, operation manuals, GST

applications and taxation rates. In order to develop necessary documentation for Victorian Flight

Academy, their policy and procedures report is prepared below:

Policy and procedures report

Victorian Flight Academy has a policy of providing benefits to their employees of free

flying time of 150 hours per year to any location in Australia.

VFA implies the procedure of maintaining minimum flight time requirement provided

by CAA.

This academy has a policy of doubtful debts to prepare a provision for them which are

equal to 1.5% of outstanding debtors at the end of a financial year.

Taxation is charged using GST in this organisation.

B. Analysing Tax Issues :

Issue:

In the mentioned case situation of VFS company, the biggest issues they are getting is

related with the bonus given to the employees in the beginning of the next year and the recorded

in the last year of the financial statements. This will directly have made impacts on the overall

profitability position of the company. The contract provides for the exclusive training for all new

Australian based and recruited crew. The another issues were associated with the risky nature of

loan the bank used to secure the title to Ross Mc kinnon and Dale wise personal homes. Because

of the heavy opposition from the Lysterfield airport together with the CAA. The council has

decided to reject the planning application. There are certain similar case issues which was related

with the VFS company is mentioned below:

CASE Example: Merrill Lynch International Australia Ltd V Commissioner of Taxation/ [2001]

FCA 1127.

5

serve as a training tool, incorporates workers experience, training refreshers, foundation for

process improvement. Under this report, company has to mention all the policies and procedures

which are followed by their management and can affect their material information. All tax

related rules and regulations are mandatory to be filed to complete tax compliance method.

According to Australian Taxation Office, procedures and policies which are necessary to be

included in this report are work place health and safety plans, operation manuals, GST

applications and taxation rates. In order to develop necessary documentation for Victorian Flight

Academy, their policy and procedures report is prepared below:

Policy and procedures report

Victorian Flight Academy has a policy of providing benefits to their employees of free

flying time of 150 hours per year to any location in Australia.

VFA implies the procedure of maintaining minimum flight time requirement provided

by CAA.

This academy has a policy of doubtful debts to prepare a provision for them which are

equal to 1.5% of outstanding debtors at the end of a financial year.

Taxation is charged using GST in this organisation.

B. Analysing Tax Issues :

Issue:

In the mentioned case situation of VFS company, the biggest issues they are getting is

related with the bonus given to the employees in the beginning of the next year and the recorded

in the last year of the financial statements. This will directly have made impacts on the overall

profitability position of the company. The contract provides for the exclusive training for all new

Australian based and recruited crew. The another issues were associated with the risky nature of

loan the bank used to secure the title to Ross Mc kinnon and Dale wise personal homes. Because

of the heavy opposition from the Lysterfield airport together with the CAA. The council has

decided to reject the planning application. There are certain similar case issues which was related

with the VFS company is mentioned below:

CASE Example: Merrill Lynch International Australia Ltd V Commissioner of Taxation/ [2001]

FCA 1127.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The bonuses were due till January mid 1995. and the issue was that all applicants were

entitled to get the advantage of reduction for amount then paid, mainly the issue was either it was

entitled to the advantage in its return of income for year 1994. that is, the dispute was the tax

commissioner stated that the outflow incurred by the bonuses paid was referable to year 1994

which was not at the end of that financial year. Also the commissioner concedes that the former

is needed by the authority and that an outgoing was incurred when if, a taxpayer becomes liable

to pay it in accordance with law. According to the commercial approach of income Tax

Assessment Act 1936 the applicant submit that “commercial” approach which states that the

representation of outgoing incurred in year 1994 in order to pay bonuses is not necessary and the

organisation had the obligation to pay the bonuses at the end of year. The applicants concedes

that they had obligated to pay the bonuses of year 1994. Moreover, the salaries of employees

were at average or below average level for the industry, means unfair compensation. The head

of executive compensation department was also the head of human resources for Merrill lynch

testified that competitive position of the company over the years with respect to base salaries as

well as bonus schemes at or below what would be required for competitive environment. But the

bonus had not the integral part of compensation of executive level employees. And in ending of

1994 year, the company avoided the documentary evidence that was letter of engagement and

perform unfair practice by refusing to pay bonuses . Not only this the company paid employees

the salaries which are below or at market remuneration rate, bonus payment criteria was also set

by , management of the company and critical.

Rule:

The applicants appeals against the dis allowance by the taxation commissioner of an

assessment to income tax for the year ended December 31, 1994. All applicants claimed a

deductions under section 51(1) of the Income Tax Assessment Act 1936. Moreover this section

states that in order to generate income or inflow or some assessable income the outgoings or

outflow incurred shall be allowable deductions except the losses or tax losses or outgoings of

capital, in order to attaining the production of exempt income the private or domestic nature

occurred. The Income Tax Assessment Act 1936 come in existence by act of the parliament of

Australia. Calculation of income tax is regulated by this act, under this section amount of

employee bonuses must be paid in respect of year 1994 ( Landais, Besley 2013).

6

entitled to get the advantage of reduction for amount then paid, mainly the issue was either it was

entitled to the advantage in its return of income for year 1994. that is, the dispute was the tax

commissioner stated that the outflow incurred by the bonuses paid was referable to year 1994

which was not at the end of that financial year. Also the commissioner concedes that the former

is needed by the authority and that an outgoing was incurred when if, a taxpayer becomes liable

to pay it in accordance with law. According to the commercial approach of income Tax

Assessment Act 1936 the applicant submit that “commercial” approach which states that the

representation of outgoing incurred in year 1994 in order to pay bonuses is not necessary and the

organisation had the obligation to pay the bonuses at the end of year. The applicants concedes

that they had obligated to pay the bonuses of year 1994. Moreover, the salaries of employees

were at average or below average level for the industry, means unfair compensation. The head

of executive compensation department was also the head of human resources for Merrill lynch

testified that competitive position of the company over the years with respect to base salaries as

well as bonus schemes at or below what would be required for competitive environment. But the

bonus had not the integral part of compensation of executive level employees. And in ending of

1994 year, the company avoided the documentary evidence that was letter of engagement and

perform unfair practice by refusing to pay bonuses . Not only this the company paid employees

the salaries which are below or at market remuneration rate, bonus payment criteria was also set

by , management of the company and critical.

Rule:

The applicants appeals against the dis allowance by the taxation commissioner of an

assessment to income tax for the year ended December 31, 1994. All applicants claimed a

deductions under section 51(1) of the Income Tax Assessment Act 1936. Moreover this section

states that in order to generate income or inflow or some assessable income the outgoings or

outflow incurred shall be allowable deductions except the losses or tax losses or outgoings of

capital, in order to attaining the production of exempt income the private or domestic nature

occurred. The Income Tax Assessment Act 1936 come in existence by act of the parliament of

Australia. Calculation of income tax is regulated by this act, under this section amount of

employee bonuses must be paid in respect of year 1994 ( Landais, Besley 2013).

6

Not only this law, Merrill lynch had three schemes regarding benefit of staff and bonus;

the first scheme was “Variable Incentive Compensation” (VICP), the second was “Key

Employees Incentive Plan”(KEICP) and the third- “Employees Incentive Plan” (EIP). The VICP

's participants are top level authority members, traders, and management staff. The top level

authority of company or administrative employees are entitled to participate in KEICP, and on

the other hand non administrative employees were entitled to participate in the EIP. The payment

of bonus was at the discretion of the employer as stipulated in terms employees appointment.

Many engagement letters were in form of documentary evidence but their terms and conditions

relating to bonus were not identical and were unfair. Moreover company breaks several rule that

breach of contract as company promised in contract with the employees to pay their all

remuneration and bonuses on time and their amounts would be equal to market remuneration

rate. But company fails to meet the facts of contract and not only this company also breaks the

accounting rules and concepts like “accrual concept” that is all accounting transactions of same

year must be made in entries in books of accounts in same year . But company paid bonuses in

year 1995 and recognised the expenses in in books of accounts in year 1994 while closing the

accounts they recognise bonus payment as expense in order to save the tax. Also company paid

bonus accordance with critical criteria set by the management of company. Moreover, the

company failed to meet requirements in contract with the employees that was in employment

contract the company promises to pay the complete remuneration and bonuses in time and

accordance with the market remuneration rate. But the salaries were paid to employees are below

average level and also below from market remuneration rate. That time company breaches the

contract and followed unfair trade and practices by violating the promises made in contract of

employment, accounting procedure, concepts and conventions but company failed to raise claim

on facts with the employees to pay their remuneration and bonuses on time.

Applications:

In this case states that in order to come within subsection 51(1) of Income Tax

Assessment act 1936, VFA become obligated legally to employees to pay them bonus

individually, and for an outflow or outgoings actually paid after the accounting era had been

incurred, must be payable in year which it belongs to its a legal liability of organisation. On the

other hand, the issue regarding the payment of outgoing as legal liability is different from a

liability in damages for breach of contracts. It means payment of bonus was in contract and was

7

the first scheme was “Variable Incentive Compensation” (VICP), the second was “Key

Employees Incentive Plan”(KEICP) and the third- “Employees Incentive Plan” (EIP). The VICP

's participants are top level authority members, traders, and management staff. The top level

authority of company or administrative employees are entitled to participate in KEICP, and on

the other hand non administrative employees were entitled to participate in the EIP. The payment

of bonus was at the discretion of the employer as stipulated in terms employees appointment.

Many engagement letters were in form of documentary evidence but their terms and conditions

relating to bonus were not identical and were unfair. Moreover company breaks several rule that

breach of contract as company promised in contract with the employees to pay their all

remuneration and bonuses on time and their amounts would be equal to market remuneration

rate. But company fails to meet the facts of contract and not only this company also breaks the

accounting rules and concepts like “accrual concept” that is all accounting transactions of same

year must be made in entries in books of accounts in same year . But company paid bonuses in

year 1995 and recognised the expenses in in books of accounts in year 1994 while closing the

accounts they recognise bonus payment as expense in order to save the tax. Also company paid

bonus accordance with critical criteria set by the management of company. Moreover, the

company failed to meet requirements in contract with the employees that was in employment

contract the company promises to pay the complete remuneration and bonuses in time and

accordance with the market remuneration rate. But the salaries were paid to employees are below

average level and also below from market remuneration rate. That time company breaches the

contract and followed unfair trade and practices by violating the promises made in contract of

employment, accounting procedure, concepts and conventions but company failed to raise claim

on facts with the employees to pay their remuneration and bonuses on time.

Applications:

In this case states that in order to come within subsection 51(1) of Income Tax

Assessment act 1936, VFA become obligated legally to employees to pay them bonus

individually, and for an outflow or outgoings actually paid after the accounting era had been

incurred, must be payable in year which it belongs to its a legal liability of organisation. On the

other hand, the issue regarding the payment of outgoing as legal liability is different from a

liability in damages for breach of contracts. It means payment of bonus was in contract and was

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the contractual promise “to pay bonus” is differ from the contractual promise perform

contractual discretion honestly, in a fair manner and in good faith. The applicants must

completely accepted to pay the outgoings sought to be deducted in present case.

According to the financial performance of company VICP, KEICP and EIP and

allocation of global pool for VICP and EIP were determined or approved by the board of

directors. The non administrative employees were the participants of bonus scheme plan

EIP(Employees Incentive Plan). The amount which is required to be payable to employees by

VFA is calculated from return on equity plan. According to which calculation of bonus is done

on the basis of job performance of employee, number of working days or working hours. It was

calculated each year after that there was a process of accrual accounting throughout the year in

order to get EIP. But the salaries of employees were at or below average level and bonus would

be at or above what were the competitive standards. In early January 1995 updated lists of

eligible employees and proposed bonuses are paid to them according to set criteria and other

measures of performance appraisal performed by the human resource manager of company.

No doubt in this statement that circumstances of the employees varied. According to the

bonus payment criteria of company, some newly joined employees would not received the bonus

the company failed to attain claim on fact regarding the payment of bonus of employees in same

preceding years. Some employees received the salaries according to market remuneration rate

being paid to person of that level and on other hand others had received salaries amount which

was below then the market remuneration rate. But the aggregate shortfalls in amount of salaries

could not be treated as equal to the amount paid by company in late January 1995.

According to subsection 51(1) of Income Tax Assessment act 1936, the qualifying employees of

company were informed regarding hedged of currency. Qualifying employees were informed

earlier so that they plan for their financial affairs. The VFA falsely recognised the payment of

bonus amount as expenses in their books of accounts in order to save tax and the payment made

in next year.

Conclusion:

According to the overall assessment of the case examples of VFS to make

analysis of the financial statements effectively so that overall impact can be minimise properly.

As it has been found that there are issues regarding the bonus amount adjustments. The bonuses

were due till January mid 1995 and the issue was that all applicants were entitled to get the

8

contractual discretion honestly, in a fair manner and in good faith. The applicants must

completely accepted to pay the outgoings sought to be deducted in present case.

According to the financial performance of company VICP, KEICP and EIP and

allocation of global pool for VICP and EIP were determined or approved by the board of

directors. The non administrative employees were the participants of bonus scheme plan

EIP(Employees Incentive Plan). The amount which is required to be payable to employees by

VFA is calculated from return on equity plan. According to which calculation of bonus is done

on the basis of job performance of employee, number of working days or working hours. It was

calculated each year after that there was a process of accrual accounting throughout the year in

order to get EIP. But the salaries of employees were at or below average level and bonus would

be at or above what were the competitive standards. In early January 1995 updated lists of

eligible employees and proposed bonuses are paid to them according to set criteria and other

measures of performance appraisal performed by the human resource manager of company.

No doubt in this statement that circumstances of the employees varied. According to the

bonus payment criteria of company, some newly joined employees would not received the bonus

the company failed to attain claim on fact regarding the payment of bonus of employees in same

preceding years. Some employees received the salaries according to market remuneration rate

being paid to person of that level and on other hand others had received salaries amount which

was below then the market remuneration rate. But the aggregate shortfalls in amount of salaries

could not be treated as equal to the amount paid by company in late January 1995.

According to subsection 51(1) of Income Tax Assessment act 1936, the qualifying employees of

company were informed regarding hedged of currency. Qualifying employees were informed

earlier so that they plan for their financial affairs. The VFA falsely recognised the payment of

bonus amount as expenses in their books of accounts in order to save tax and the payment made

in next year.

Conclusion:

According to the overall assessment of the case examples of VFS to make

analysis of the financial statements effectively so that overall impact can be minimise properly.

As it has been found that there are issues regarding the bonus amount adjustments. The bonuses

were due till January mid 1995 and the issue was that all applicants were entitled to get the

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

advantage of reduction for amount then paid, mainly the issue was either it was entitled to the

advantage in its return of income for year 1994. that is, the dispute was the tax commissioner

stated that the outflow incurred by the bonuses paid was referable to year 1994 which was not at

the end of that financial year. Also the commissioner concedes that the former is needed by the

authority and that an outgoing was incurred when if, a taxpayer becomes liable to pay it in

accordance with law. According to the commercial approach of income Tax Assessment Act

1936 the applicant Not only this legal and jurisprudential approach pursued by courts, means

jurisprudence seeks to analyse, explain, classify and criticize entire bodies of law. Merrill lynch

may be suggested to have made by the progressive accrual in its accounts of the reserves to meet

the bonuses. In my view, in order for an outgoing which is in fact paid after an accounting period

to have been “incurred” within it, exist by the end of that period a legal liability to pay it.

Company failed to meet the bonus requirement of bonus and breaches the contracts also.

Recommendations:

On the basis of the all the above case analysis, it has been suggested that the revenue

increasing would be related with concentrated on personal income that are assessed on

comprehensive basis, business income which is designed to be supported as economic growth. It

is specified additionally that only it is possible to make modification on social results or market

efficient in better rate. Such kind of taxes would basically use where they can attain the desire

number of outcomes that other policy instruments. The other recommendation is to progressivist

in the tax should be deliver from the individual tax rates scales and transfer payments. In case of

high tax-free threshold with a constant marginal rate for effective people that would be

introduced to make modification in order provide greater clearness and overall easiness. The

basic units in an individual unit in personal tax system would need to continue to be the

individual and subsidies for dependants through an effective system. It should be needed to

restricted certain rights of people so that changes of losses. There is another suggestion which

will be valuable for the company to remove the complexity and ensure that government

assistance is properly aimed, concessional offset would be overcome. The medical expenses tax

deduction need to be removed by following a review of the scope and overall structure of the

health safety and net valuation.

It is recommended that organisation should follow the required guidelines and the process

to asses the tax requirement for a particular period. It is analysed that organisational impact fall

9

advantage in its return of income for year 1994. that is, the dispute was the tax commissioner

stated that the outflow incurred by the bonuses paid was referable to year 1994 which was not at

the end of that financial year. Also the commissioner concedes that the former is needed by the

authority and that an outgoing was incurred when if, a taxpayer becomes liable to pay it in

accordance with law. According to the commercial approach of income Tax Assessment Act

1936 the applicant Not only this legal and jurisprudential approach pursued by courts, means

jurisprudence seeks to analyse, explain, classify and criticize entire bodies of law. Merrill lynch

may be suggested to have made by the progressive accrual in its accounts of the reserves to meet

the bonuses. In my view, in order for an outgoing which is in fact paid after an accounting period

to have been “incurred” within it, exist by the end of that period a legal liability to pay it.

Company failed to meet the bonus requirement of bonus and breaches the contracts also.

Recommendations:

On the basis of the all the above case analysis, it has been suggested that the revenue

increasing would be related with concentrated on personal income that are assessed on

comprehensive basis, business income which is designed to be supported as economic growth. It

is specified additionally that only it is possible to make modification on social results or market

efficient in better rate. Such kind of taxes would basically use where they can attain the desire

number of outcomes that other policy instruments. The other recommendation is to progressivist

in the tax should be deliver from the individual tax rates scales and transfer payments. In case of

high tax-free threshold with a constant marginal rate for effective people that would be

introduced to make modification in order provide greater clearness and overall easiness. The

basic units in an individual unit in personal tax system would need to continue to be the

individual and subsidies for dependants through an effective system. It should be needed to

restricted certain rights of people so that changes of losses. There is another suggestion which

will be valuable for the company to remove the complexity and ensure that government

assistance is properly aimed, concessional offset would be overcome. The medical expenses tax

deduction need to be removed by following a review of the scope and overall structure of the

health safety and net valuation.

It is recommended that organisation should follow the required guidelines and the process

to asses the tax requirement for a particular period. It is analysed that organisational impact fall

9

upon the significant chapter and evaluation for better evaluation and control. The rules and

regulations related to commercial taxes, central goods tax and changes are required to adhere. It

was estimated that most of the tax agents avoid the relevance while creating advanced tax

provisions which may lead organisation towards serious concerns and legal challenges. It is

required to determine the main challenges and affect for determining the tangible and intangible

tax liability. Such kind of avoidance must be prohibited in organisational context and should be

related with the assessment criteria for taxable year. There is a proper adjustment and recording

required to attain the interest of employees and the tangible structure of taxable assessment

criteria. The benefits given to employees are also required for better analysis and accurate

accessibility of tax for the particular year. VFA should follow all the rules and regulations which

are applicable to them in order to ascertain their fair tax liabilities. From these applied laws, VFA

can be benefited as they can determine their challenges are can find ways to tackle them.

10

regulations related to commercial taxes, central goods tax and changes are required to adhere. It

was estimated that most of the tax agents avoid the relevance while creating advanced tax

provisions which may lead organisation towards serious concerns and legal challenges. It is

required to determine the main challenges and affect for determining the tangible and intangible

tax liability. Such kind of avoidance must be prohibited in organisational context and should be

related with the assessment criteria for taxable year. There is a proper adjustment and recording

required to attain the interest of employees and the tangible structure of taxable assessment

criteria. The benefits given to employees are also required for better analysis and accurate

accessibility of tax for the particular year. VFA should follow all the rules and regulations which

are applicable to them in order to ascertain their fair tax liabilities. From these applied laws, VFA

can be benefited as they can determine their challenges are can find ways to tackle them.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.