Taxation Law Assignment: Brekkie and Lunch, OZ Bottle Shop Tax Return

VerifiedAdded on 2023/04/20

|10

|2114

|297

Homework Assignment

AI Summary

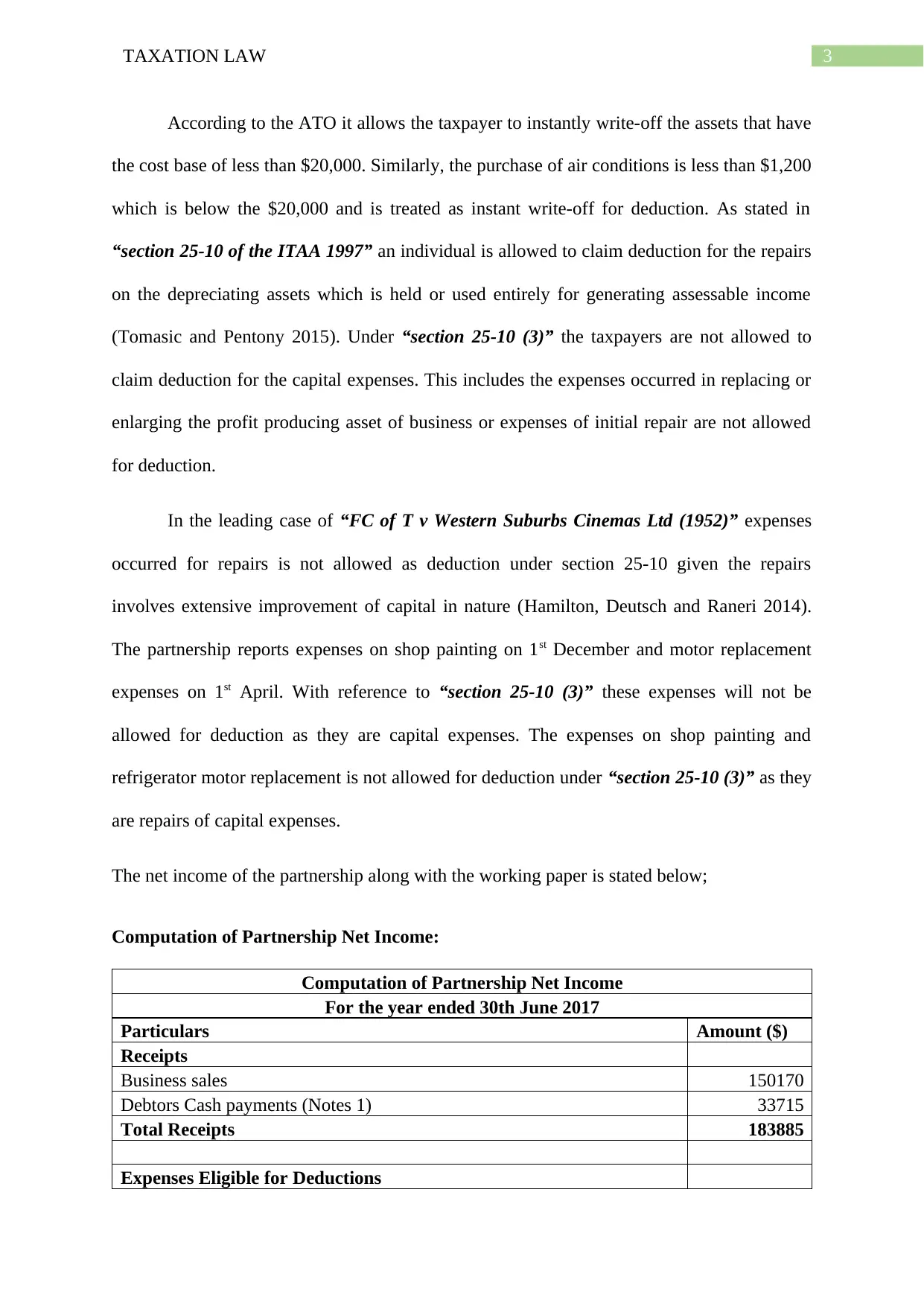

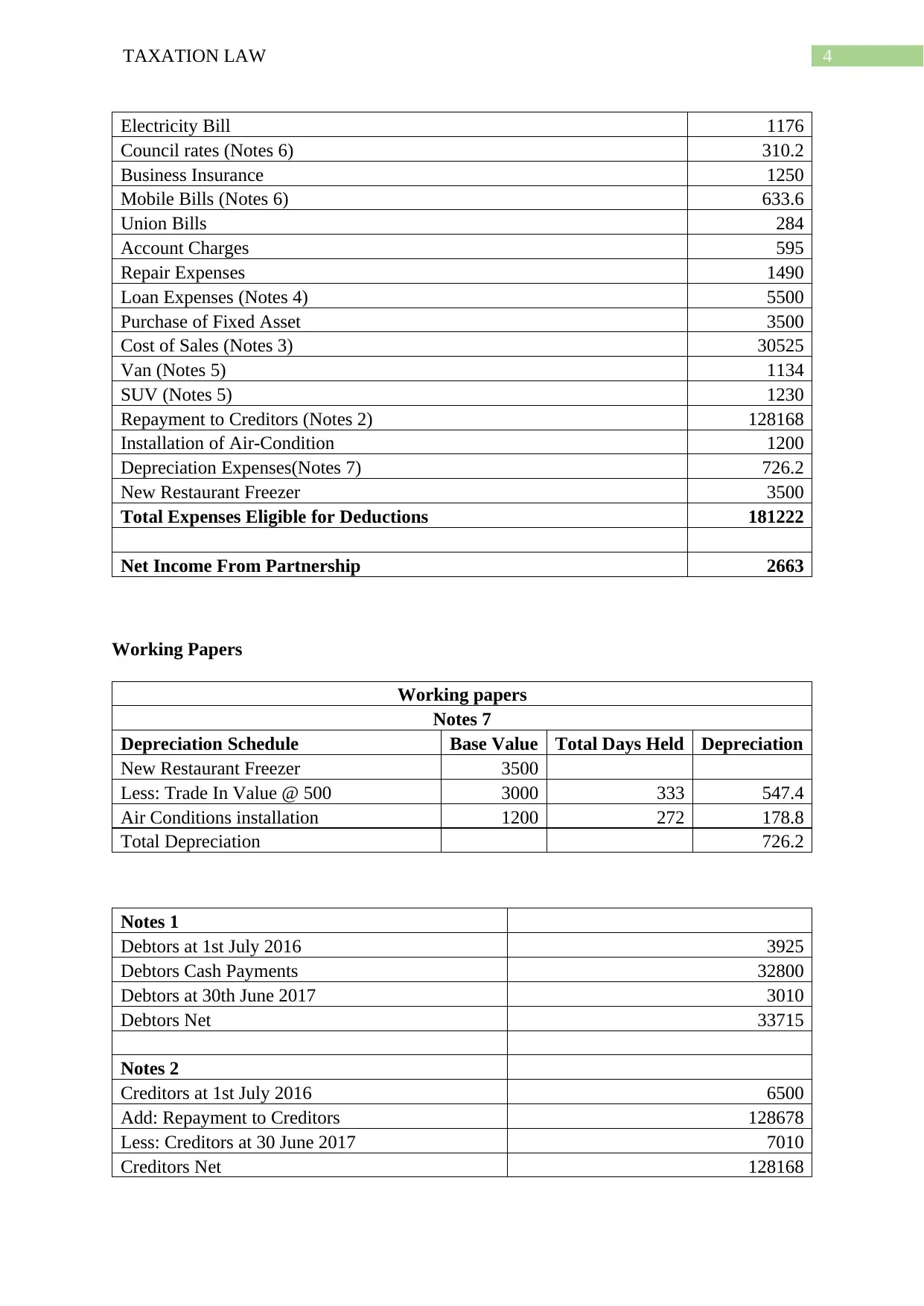

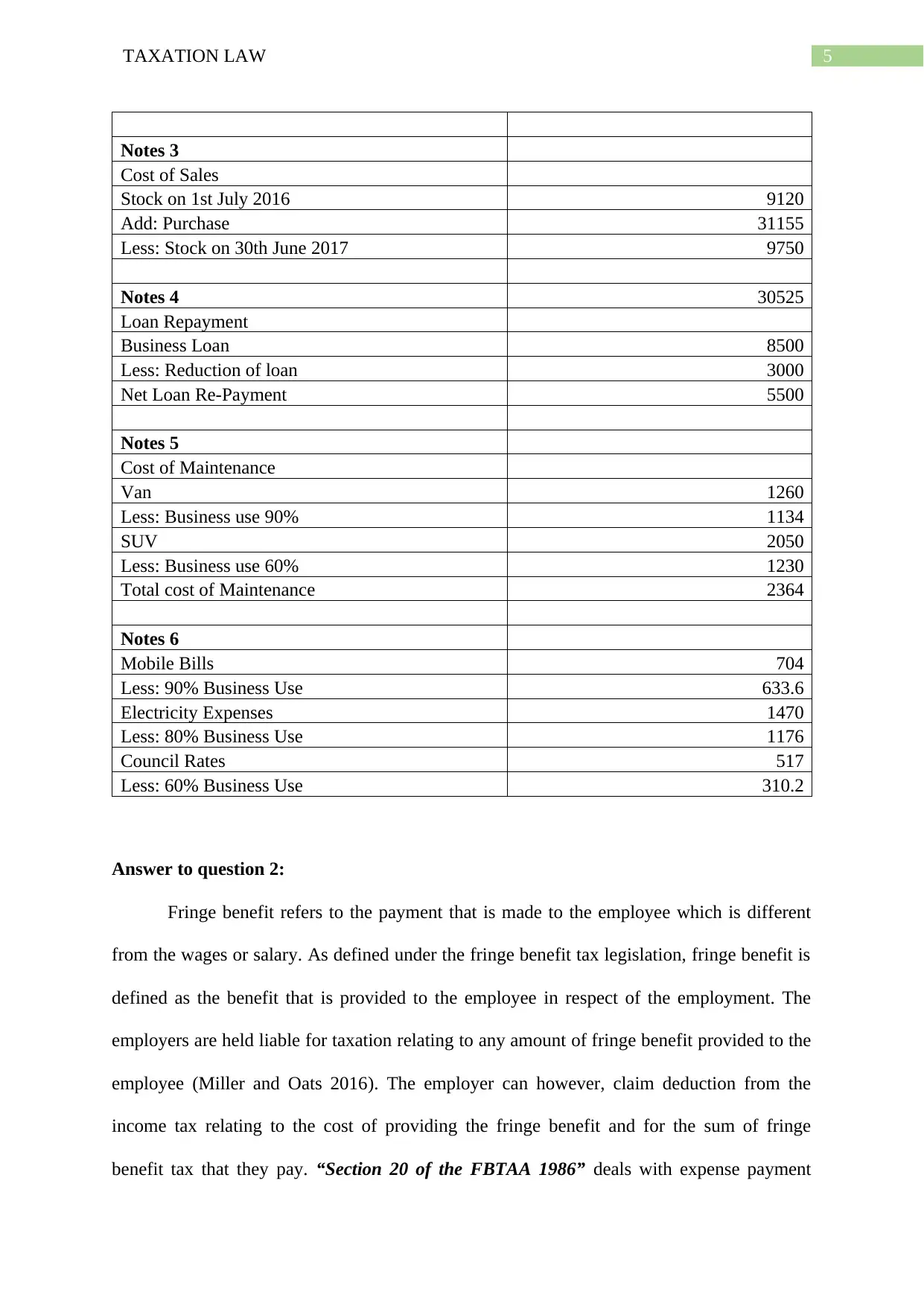

This assignment solution addresses a taxation law problem concerning Daniel and Olivia Smith's mixed business, Brekkie and Lunch and OZ Bottle Shop. The solution analyzes the partnership's net income calculation, considering business sales, debtor payments, and various expenses, including depreciation, repairs, and loan repayments. It references relevant sections of the ITAA 1936 and ITAA 1997, as well as ATO guidelines. The solution also covers fringe benefits tax (FBT), specifically addressing expense payment and accommodation fringe benefits provided to an employee, John. The analysis considers the tax implications of school fees paid for John's child and the market value of an apartment provided to John, referencing the FBTAA 1986 and relevant case law, such as J & G Knowles v Federal Commissioner of Taxation (2000).

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.