Taxation Law Report: Assessment of Jane's Tax Liability and Deductions

VerifiedAdded on 2021/04/24

|11

|2415

|44

Report

AI Summary

This report provides a detailed analysis of a taxpayer's tax liabilities and potential deductions based on the provided financial information. The report begins with a letter of advice to the taxpayer, Jane, outlining the assessable income from various sources, including salary, business profits, dividends, capital gains, and rental property income. It then discusses the application of relevant sections of the ITAA 1936 and ITAA 1997 to determine the tax implications of each income source. The report further examines allowable deductions, including car-related expenses, work-related expenses (uniforms, shoes), self-education expenses, and rental property expenses, referencing relevant case law and legislation. The report includes a summary table with the calculation of taxable income, tax payable, and Medicare levy. The report concludes by summarizing the key findings and providing a comprehensive overview of the taxpayer's tax position, offering valuable insights into the complexities of Australian taxation law.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Letter of Advice.........................................................................................................................2

Table of Contents

Letter of Advice.........................................................................................................................2

2TAXATION LAW

Letter of Advice

Dear Jane

I would like to draw your kind attention towards the letter that would be

providing you valuable advice regarding the tax liability and tax deductions of transactions

that has been provided by you. Initially it is necessary to understand that Section 6 of the

ITAA 1936 provides that income from the personal exertion or income that are derived from

the personal exertion represents income comprising of earnings, salaries, commissions, fees

bonus, pension or income from business would be considered for assessment.

Section 6-5 of the ITAA 1997 defines that most of the income to the taxpayer that

comes in is regarded as the ordinary income (Woellner et al. 2016). The court of “Law of

Scott v Federal Commissioner of Taxation (1935)” defined that the word income in

compliance with the ordinary concepts and use of mankind. The total amount of salary

reported by you shall be considered assessable under section 6-5 of the ITAA 1997 as the

income from personal exertion. Additionally, is also noted that you reported a business

profits of $2,000,000 during the income year of 2016. Therefore, for the assessment of year

2017 your business will be included the taxable return and the same will held be assessable.

An important consideration has been made for the income reported from the dividend

income reported by you. These dividends possess the character of income which is a gain for

you. Therefore, the dividend income will be considered for assessment under section 6-5 of

the ITAA 1997 as income from ordinary concepts (Barkoczy 2016). Section 102-5 of the

ITAA 1997 takes into the account the net capital gain for the year of income into the

assessable income year. It is noticed that you reported a capital gain of 500,000. A CGT

discount of 50% would be provided to you for the assets that are held for 12 months or more.

It is assumed that the asset has been held by you for a minimum period of 12 months and as a

Letter of Advice

Dear Jane

I would like to draw your kind attention towards the letter that would be

providing you valuable advice regarding the tax liability and tax deductions of transactions

that has been provided by you. Initially it is necessary to understand that Section 6 of the

ITAA 1936 provides that income from the personal exertion or income that are derived from

the personal exertion represents income comprising of earnings, salaries, commissions, fees

bonus, pension or income from business would be considered for assessment.

Section 6-5 of the ITAA 1997 defines that most of the income to the taxpayer that

comes in is regarded as the ordinary income (Woellner et al. 2016). The court of “Law of

Scott v Federal Commissioner of Taxation (1935)” defined that the word income in

compliance with the ordinary concepts and use of mankind. The total amount of salary

reported by you shall be considered assessable under section 6-5 of the ITAA 1997 as the

income from personal exertion. Additionally, is also noted that you reported a business

profits of $2,000,000 during the income year of 2016. Therefore, for the assessment of year

2017 your business will be included the taxable return and the same will held be assessable.

An important consideration has been made for the income reported from the dividend

income reported by you. These dividends possess the character of income which is a gain for

you. Therefore, the dividend income will be considered for assessment under section 6-5 of

the ITAA 1997 as income from ordinary concepts (Barkoczy 2016). Section 102-5 of the

ITAA 1997 takes into the account the net capital gain for the year of income into the

assessable income year. It is noticed that you reported a capital gain of 500,000. A CGT

discount of 50% would be provided to you for the assets that are held for 12 months or more.

It is assumed that the asset has been held by you for a minimum period of 12 months and as a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

result of this you would be entitled to 50% CGT discount for the total amount of capital gains

derived by you.

The commissioner in the case of “FCT v Dixon” has explained that income derived

from the personal receipts are regarded as taxable income (Cao et al. 2015). Similarly, the

receipt of $26,000 from the rental property income forms the part of the taxable income and

the same will be considered taxable.

The federal court in “Moore v Griffiths (1972)” explained that mere winning from

prize does not forms the part of income (Braithwaite 2017). Hence, the prize winning of

$8000 from a golf tournament is not held as income and the same will not be included in your

taxable income.

According to section 8-1 of the ITAA 1997 an individual is allowed to claim

deductions relating to the expenses or outgoing that directly related with the assessable

income. To claim a deduction, the expenditure must meet the deductibility test under positive

limbs of section 8-1 of the ITAA 1997 (Saad 2014). An expenses or outgoings that are of

private or domestic in nature might not be considered for deductions since it does not meet

the criteria of positive limbs or the it is not allowed for deductions under “section 8-1 (2) (b)

of the ITAA 1997”. The court of law in “Lunney v Federal Commissioner of taxation

(1958)” defined that an expenditure must have the necessary character of loss or outgoings in

the derivation of the taxable income.

The expenditure on car reported by you related to the work purpose will be considered

for deductions. However, under “Sub-section 136 (1)” you cannot claim the expenditure

relating to travel purpose or home and office purpose as these are expenditure constitute a

private expenditure that cannot be claimed as the allowable deductions (Miller and Oats

2016). By referring to the commissioner decisions in “Lunney v Federal Commissioner of

result of this you would be entitled to 50% CGT discount for the total amount of capital gains

derived by you.

The commissioner in the case of “FCT v Dixon” has explained that income derived

from the personal receipts are regarded as taxable income (Cao et al. 2015). Similarly, the

receipt of $26,000 from the rental property income forms the part of the taxable income and

the same will be considered taxable.

The federal court in “Moore v Griffiths (1972)” explained that mere winning from

prize does not forms the part of income (Braithwaite 2017). Hence, the prize winning of

$8000 from a golf tournament is not held as income and the same will not be included in your

taxable income.

According to section 8-1 of the ITAA 1997 an individual is allowed to claim

deductions relating to the expenses or outgoing that directly related with the assessable

income. To claim a deduction, the expenditure must meet the deductibility test under positive

limbs of section 8-1 of the ITAA 1997 (Saad 2014). An expenses or outgoings that are of

private or domestic in nature might not be considered for deductions since it does not meet

the criteria of positive limbs or the it is not allowed for deductions under “section 8-1 (2) (b)

of the ITAA 1997”. The court of law in “Lunney v Federal Commissioner of taxation

(1958)” defined that an expenditure must have the necessary character of loss or outgoings in

the derivation of the taxable income.

The expenditure on car reported by you related to the work purpose will be considered

for deductions. However, under “Sub-section 136 (1)” you cannot claim the expenditure

relating to travel purpose or home and office purpose as these are expenditure constitute a

private expenditure that cannot be claimed as the allowable deductions (Miller and Oats

2016). By referring to the commissioner decisions in “Lunney v Federal Commissioner of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Taxation” held that travel between an individual home or an individual usual place of work

is usually not held deductible. Therefore, the travel expenditure incurred by shall not be

considered as the allowable deductions.

Referring to the judgement in “Fullerton v Federal Commissioner of Taxation” the

commissioner did not allowed deductions to taxpayer for moving with his family to a new

home since these expenditures were entirely domestic or family arrangement (Barkoczy

2014).

According to the Australian taxation Law an individual is allowed to claim

expenditure of compulsory uniform, protective clothing or occupation related specific

clothing. According to the statement made by the commissioner in “Mansfield v Federal

Commissioner of Law” the court permitted the flight attendant to claim deductions relating

to cost of shoes along with the cost of stockings as these clothes were occupation specific

(Brokelind 2014). The expenditure reported by you relating to purchase of skirts and pair of

shoes will be considered as the allowable deductions. The primary reason for considering the

deductions allowable the expenses or outgoing is directly related with the assessable income.

Furthermore, the expenditure reported by you meets the deductibility test under positive

limbs of section 8-1 of the ITAA 1997.

On the other hand, occupation related self-education that are incurred by the taxpayer

are allowed for deductions. This is because the self-education expenditure are usually

considered for deductions because these expenditure are incurred in meeting or increasing the

taxpayer skills that are engaged in their occupation (Coleman and Sadiq 2013). Particularly,

these expenditure are related to improving the income earning prospects of the taxpayer.

Similarly, the examples of occupation related self-education includes an instances of cost

incurred in registering, travelling and accommodation at the professional conference will be

Taxation” held that travel between an individual home or an individual usual place of work

is usually not held deductible. Therefore, the travel expenditure incurred by shall not be

considered as the allowable deductions.

Referring to the judgement in “Fullerton v Federal Commissioner of Taxation” the

commissioner did not allowed deductions to taxpayer for moving with his family to a new

home since these expenditures were entirely domestic or family arrangement (Barkoczy

2014).

According to the Australian taxation Law an individual is allowed to claim

expenditure of compulsory uniform, protective clothing or occupation related specific

clothing. According to the statement made by the commissioner in “Mansfield v Federal

Commissioner of Law” the court permitted the flight attendant to claim deductions relating

to cost of shoes along with the cost of stockings as these clothes were occupation specific

(Brokelind 2014). The expenditure reported by you relating to purchase of skirts and pair of

shoes will be considered as the allowable deductions. The primary reason for considering the

deductions allowable the expenses or outgoing is directly related with the assessable income.

Furthermore, the expenditure reported by you meets the deductibility test under positive

limbs of section 8-1 of the ITAA 1997.

On the other hand, occupation related self-education that are incurred by the taxpayer

are allowed for deductions. This is because the self-education expenditure are usually

considered for deductions because these expenditure are incurred in meeting or increasing the

taxpayer skills that are engaged in their occupation (Coleman and Sadiq 2013). Particularly,

these expenditure are related to improving the income earning prospects of the taxpayer.

Similarly, the examples of occupation related self-education includes an instances of cost

incurred in registering, travelling and accommodation at the professional conference will be

5TAXATION LAW

held as an allowable deductions. As evident that you have reported a self-education

expenditure that are related to the attending of law conference in Melbourne.

The expenditure incurred by you on cost of registering, travel and accommodations

will be considered as the allowable deductions. According to the judgement made in

“Highfield v Federal Commissioner of Taxation” it was stated that the expenditure related

to travel, accommodations of undertaking the self-education shall be considered as the

allowable deductions (Grange et al. 2014). Therefore, the expenditure reported by you for

attending the conference in Melbourne will be considered as the allowable deductions under

section 8-1 of the ITAA 1997. The primary reason for claiming the deduction is that these

expenditure are related to improving the income earning prospects (Kenny 2013). The self-

education expenditure are typically allowed for deductions since these expenditure are

occurred in meeting or increasing your skills of your solicitor occupation.

An instances obtained from the case study suggest that you incurred expenditure on a

client in relation to the function of partnership with the client. As a result of this you regularly

engage with the client for lunch and dinner at outside (James 2014). The cost of meal

entertainment can be considered as the business related expenditure. In accordance with the

Australian taxation office you can claim an allowable deductions related to the expenditure

on the business entertainment meal purpose.

Other transactions include an expenditure incurred by you for purchase of golf clubs

since your old set was not usable anymore. In accordance to the negative limbs of “section 8-

1 (2) (b) of the ITAA 1997” an individual is barred from claiming an allowable deductions

relating to expenditure that are private or domestic in nature (Krever 2015). The court of law

in the “Lodge v Federal Commissioner of Taxation” denied a taxpayer with the private

related expenditure as the expenditure was considered neither relevant nor incidental in

held as an allowable deductions. As evident that you have reported a self-education

expenditure that are related to the attending of law conference in Melbourne.

The expenditure incurred by you on cost of registering, travel and accommodations

will be considered as the allowable deductions. According to the judgement made in

“Highfield v Federal Commissioner of Taxation” it was stated that the expenditure related

to travel, accommodations of undertaking the self-education shall be considered as the

allowable deductions (Grange et al. 2014). Therefore, the expenditure reported by you for

attending the conference in Melbourne will be considered as the allowable deductions under

section 8-1 of the ITAA 1997. The primary reason for claiming the deduction is that these

expenditure are related to improving the income earning prospects (Kenny 2013). The self-

education expenditure are typically allowed for deductions since these expenditure are

occurred in meeting or increasing your skills of your solicitor occupation.

An instances obtained from the case study suggest that you incurred expenditure on a

client in relation to the function of partnership with the client. As a result of this you regularly

engage with the client for lunch and dinner at outside (James 2014). The cost of meal

entertainment can be considered as the business related expenditure. In accordance with the

Australian taxation office you can claim an allowable deductions related to the expenditure

on the business entertainment meal purpose.

Other transactions include an expenditure incurred by you for purchase of golf clubs

since your old set was not usable anymore. In accordance to the negative limbs of “section 8-

1 (2) (b) of the ITAA 1997” an individual is barred from claiming an allowable deductions

relating to expenditure that are private or domestic in nature (Krever 2015). The court of law

in the “Lodge v Federal Commissioner of Taxation” denied a taxpayer with the private

related expenditure as the expenditure was considered neither relevant nor incidental in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

generation of assessable income. Therefore the expenditure on purchase of golf set will be

considered as entirely for private purpose. With respect to the provision of “section 8-1 (2)

(b) of the ITAA 1997” you would not be allowed to claim allowable deductions (Morgan,

Mortimer and Pinto 2013).

Section 25-10 of the ITAA 1997 allows an individual can claim expenditure related to

the rental property as long as the property has been rented out or available for rent.

Nevertheless, an exception to this rule is that an individual is barred from claiming

expenditure that is are having the nature of capital or having private nature (Sadiq et al.

2014). As evident you have reported a number of rental property expenditure that is related

solely with the objective of gaining taxable income. Therefore, with reference to section 25-

10 of the ITAA 1997 you can claim an allowable deductions for the expenditure incurred in

producing the rental income from your property.

According to the section 40-25 (1) an organization can deduct an amount from the

declining value of the depreciating asset that is held by the taxpayer during the income year

(Woellner 2013). As evident in the transactions provided you it is found that you have

purchased an asset of Air conditions, washing machines and microwave oven. These assess

entirely used for your private purpose and you can implement the diminishing method to

reduce the declining value for your depreciated assets.

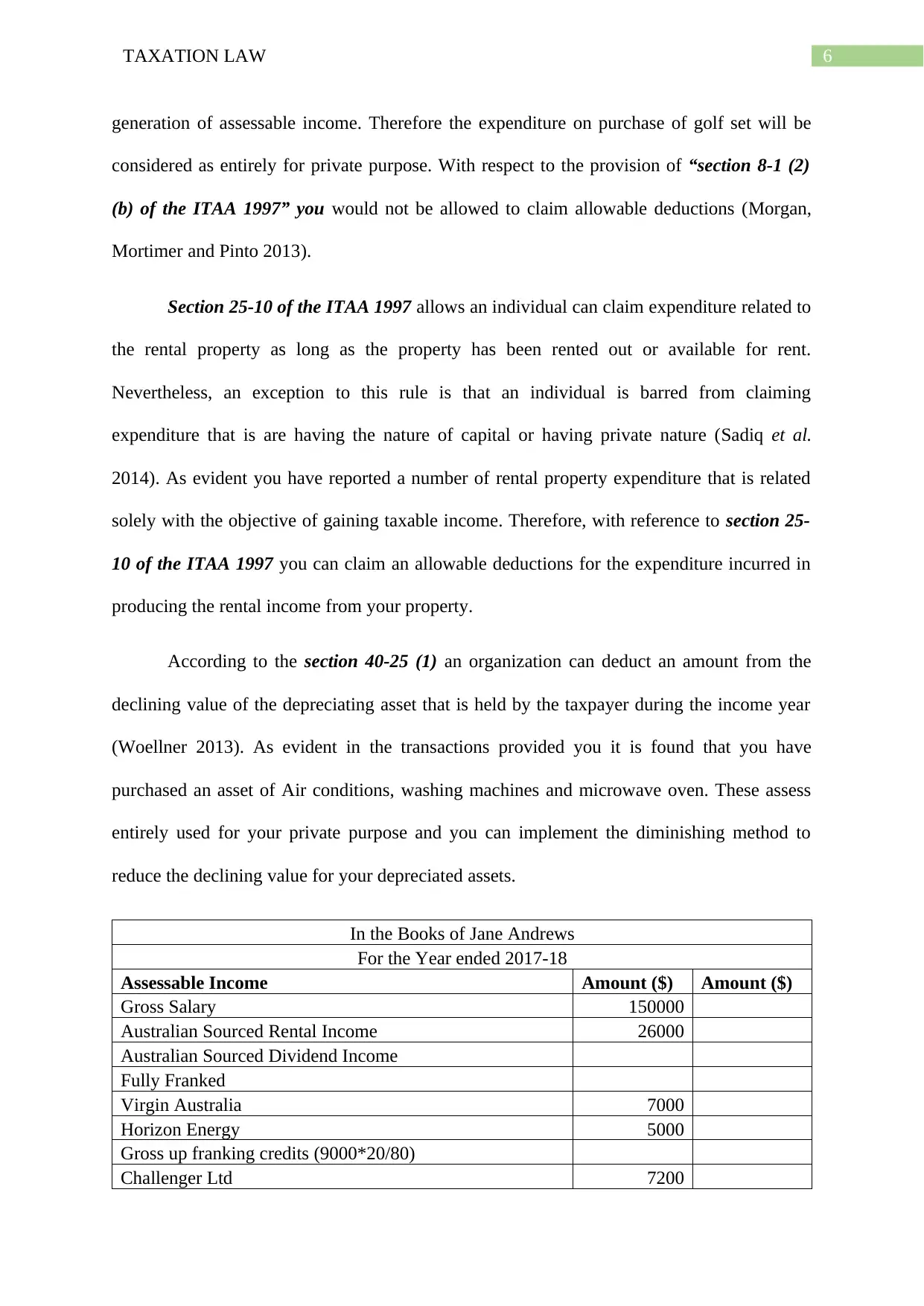

In the Books of Jane Andrews

For the Year ended 2017-18

Assessable Income Amount ($) Amount ($)

Gross Salary 150000

Australian Sourced Rental Income 26000

Australian Sourced Dividend Income

Fully Franked

Virgin Australia 7000

Horizon Energy 5000

Gross up franking credits (9000*20/80)

Challenger Ltd 7200

generation of assessable income. Therefore the expenditure on purchase of golf set will be

considered as entirely for private purpose. With respect to the provision of “section 8-1 (2)

(b) of the ITAA 1997” you would not be allowed to claim allowable deductions (Morgan,

Mortimer and Pinto 2013).

Section 25-10 of the ITAA 1997 allows an individual can claim expenditure related to

the rental property as long as the property has been rented out or available for rent.

Nevertheless, an exception to this rule is that an individual is barred from claiming

expenditure that is are having the nature of capital or having private nature (Sadiq et al.

2014). As evident you have reported a number of rental property expenditure that is related

solely with the objective of gaining taxable income. Therefore, with reference to section 25-

10 of the ITAA 1997 you can claim an allowable deductions for the expenditure incurred in

producing the rental income from your property.

According to the section 40-25 (1) an organization can deduct an amount from the

declining value of the depreciating asset that is held by the taxpayer during the income year

(Woellner 2013). As evident in the transactions provided you it is found that you have

purchased an asset of Air conditions, washing machines and microwave oven. These assess

entirely used for your private purpose and you can implement the diminishing method to

reduce the declining value for your depreciated assets.

In the Books of Jane Andrews

For the Year ended 2017-18

Assessable Income Amount ($) Amount ($)

Gross Salary 150000

Australian Sourced Rental Income 26000

Australian Sourced Dividend Income

Fully Franked

Virgin Australia 7000

Horizon Energy 5000

Gross up franking credits (9000*20/80)

Challenger Ltd 7200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

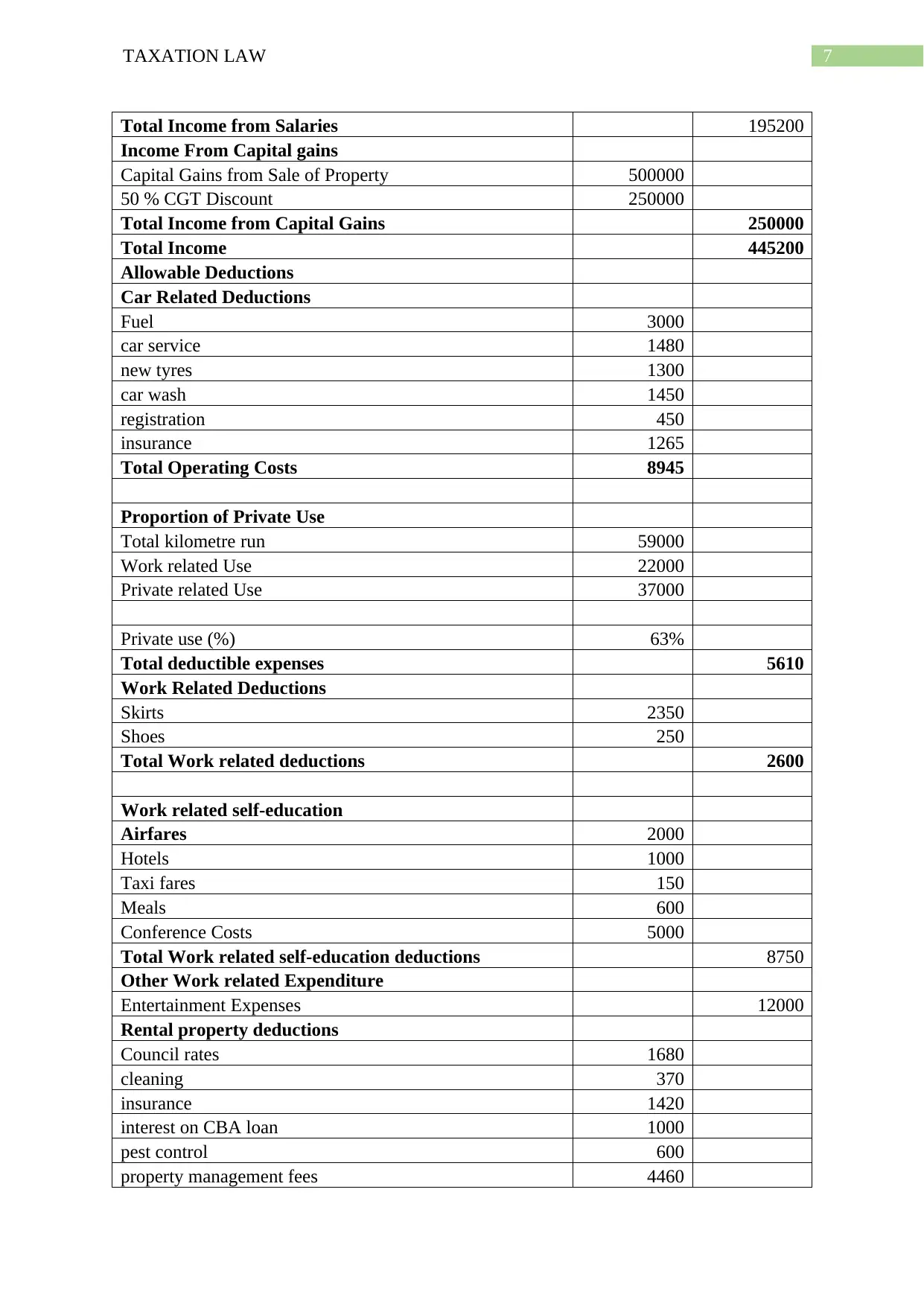

Total Income from Salaries 195200

Income From Capital gains

Capital Gains from Sale of Property 500000

50 % CGT Discount 250000

Total Income from Capital Gains 250000

Total Income 445200

Allowable Deductions

Car Related Deductions

Fuel 3000

car service 1480

new tyres 1300

car wash 1450

registration 450

insurance 1265

Total Operating Costs 8945

Proportion of Private Use

Total kilometre run 59000

Work related Use 22000

Private related Use 37000

Private use (%) 63%

Total deductible expenses 5610

Work Related Deductions

Skirts 2350

Shoes 250

Total Work related deductions 2600

Work related self-education

Airfares 2000

Hotels 1000

Taxi fares 150

Meals 600

Conference Costs 5000

Total Work related self-education deductions 8750

Other Work related Expenditure

Entertainment Expenses 12000

Rental property deductions

Council rates 1680

cleaning 370

insurance 1420

interest on CBA loan 1000

pest control 600

property management fees 4460

Total Income from Salaries 195200

Income From Capital gains

Capital Gains from Sale of Property 500000

50 % CGT Discount 250000

Total Income from Capital Gains 250000

Total Income 445200

Allowable Deductions

Car Related Deductions

Fuel 3000

car service 1480

new tyres 1300

car wash 1450

registration 450

insurance 1265

Total Operating Costs 8945

Proportion of Private Use

Total kilometre run 59000

Work related Use 22000

Private related Use 37000

Private use (%) 63%

Total deductible expenses 5610

Work Related Deductions

Skirts 2350

Shoes 250

Total Work related deductions 2600

Work related self-education

Airfares 2000

Hotels 1000

Taxi fares 150

Meals 600

Conference Costs 5000

Total Work related self-education deductions 8750

Other Work related Expenditure

Entertainment Expenses 12000

Rental property deductions

Council rates 1680

cleaning 370

insurance 1420

interest on CBA loan 1000

pest control 600

property management fees 4460

8TAXATION LAW

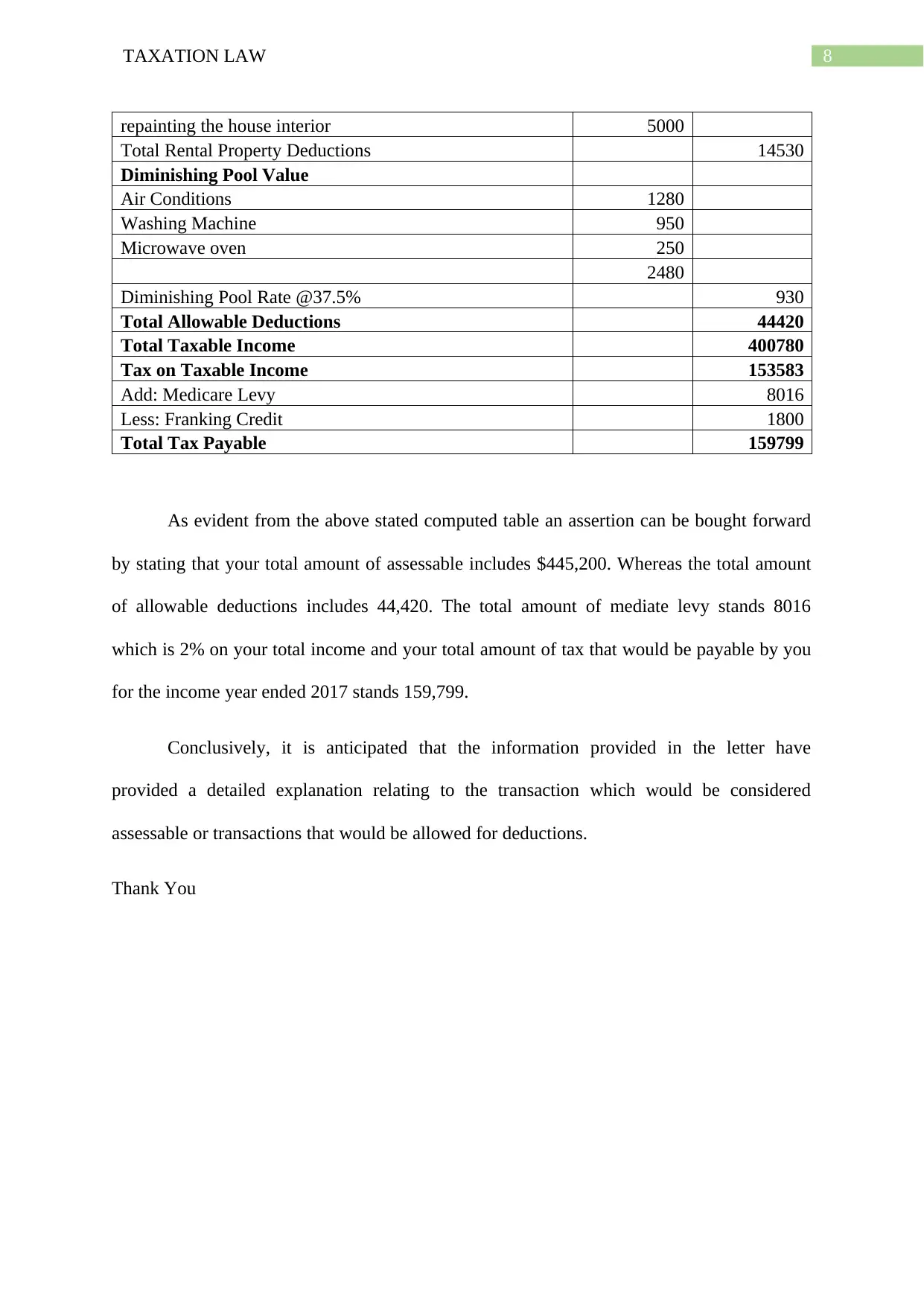

repainting the house interior 5000

Total Rental Property Deductions 14530

Diminishing Pool Value

Air Conditions 1280

Washing Machine 950

Microwave oven 250

2480

Diminishing Pool Rate @37.5% 930

Total Allowable Deductions 44420

Total Taxable Income 400780

Tax on Taxable Income 153583

Add: Medicare Levy 8016

Less: Franking Credit 1800

Total Tax Payable 159799

As evident from the above stated computed table an assertion can be bought forward

by stating that your total amount of assessable includes $445,200. Whereas the total amount

of allowable deductions includes 44,420. The total amount of mediate levy stands 8016

which is 2% on your total income and your total amount of tax that would be payable by you

for the income year ended 2017 stands 159,799.

Conclusively, it is anticipated that the information provided in the letter have

provided a detailed explanation relating to the transaction which would be considered

assessable or transactions that would be allowed for deductions.

Thank You

repainting the house interior 5000

Total Rental Property Deductions 14530

Diminishing Pool Value

Air Conditions 1280

Washing Machine 950

Microwave oven 250

2480

Diminishing Pool Rate @37.5% 930

Total Allowable Deductions 44420

Total Taxable Income 400780

Tax on Taxable Income 153583

Add: Medicare Levy 8016

Less: Franking Credit 1800

Total Tax Payable 159799

As evident from the above stated computed table an assertion can be bought forward

by stating that your total amount of assessable includes $445,200. Whereas the total amount

of allowable deductions includes 44,420. The total amount of mediate levy stands 8016

which is 2% on your total income and your total amount of tax that would be payable by you

for the income year ended 2017 stands 159,799.

Conclusively, it is anticipated that the information provided in the letter have

provided a detailed explanation relating to the transaction which would be considered

assessable or transactions that would be allowed for deductions.

Thank You

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Reference List:

Barkoczy, S 2014 Foundations of taxation law.

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Brokelind, C. 2014. Principles of law: function, status and impact in EU tax law.

Amsterdam: IBFD.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Coleman, C. and Sadiq, K. 2013. Principles of taxation law.

Grange, J., Jover-Ledesma, G. and Maydew, G. 2014. principles of business taxation.

James, M. 2014 Taxation of small businesses.

Kenny, P. 2013. Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths

Krever, R. 2015. Australian taxation law cases.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Morgan, A., Mortimer, C. and Pinto, D. 2013. A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Reference List:

Barkoczy, S 2014 Foundations of taxation law.

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Brokelind, C. 2014. Principles of law: function, status and impact in EU tax law.

Amsterdam: IBFD.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Coleman, C. and Sadiq, K. 2013. Principles of taxation law.

Grange, J., Jover-Ledesma, G. and Maydew, G. 2014. principles of business taxation.

James, M. 2014 Taxation of small businesses.

Kenny, P. 2013. Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths

Krever, R. 2015. Australian taxation law cases.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Morgan, A., Mortimer, C. and Pinto, D. 2013. A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W. and Ting, A.

2014. Principles of taxation law 2014.

Woellner, R. 2013. Australian taxation law select 2013. North Ryde, N.S.W.: CCH Australia.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W. and Ting, A.

2014. Principles of taxation law 2014.

Woellner, R. 2013. Australian taxation law select 2013. North Ryde, N.S.W.: CCH Australia.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.