Taxation Law Assignment: Exploring Deductions, GST, and Legal Expenses

VerifiedAdded on 2020/03/23

|12

|1998

|47

Homework Assignment

AI Summary

This taxation law assignment addresses several key issues related to income tax deductions and GST in the context of Australian tax law. The assignment begins by examining allowable deductions under section 8-1 of the ITAA 1997, focusing on the deductibility of costs associated with shifting machinery, asset revaluation for insurance cover, legal expenses related to business wind-up, and legal disbursements for various business operations. It analyzes these scenarios in light of relevant legislation and case law, such as the British Insulated & Helsby Cables case and the taxation ruling of TD 93/126. The second part of the assignment focuses on GST, specifically addressing the input tax credit for a financial institution's advertising expenditures, differentiating between expenses related to current services and new product launches. The assignment concludes with a calculation of the input tax credit allowed to the bank. The document provides a comprehensive analysis of taxation principles and their application to practical business scenarios.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to Question 1:................................................................................................................3

Answer to Requirement 1:.....................................................................................................3

Issue:..................................................................................................................................3

Legislations:.......................................................................................................................3

Application:........................................................................................................................3

Conclusion:........................................................................................................................4

Answer to Requirement 2:.....................................................................................................4

Issue:..................................................................................................................................4

Legislations:.......................................................................................................................4

Application:........................................................................................................................4

Conclusion:........................................................................................................................4

Answer to Requirement 3:.....................................................................................................4

Issue:..................................................................................................................................4

Legislations:.......................................................................................................................4

Application:........................................................................................................................5

Conclusion:........................................................................................................................5

Answer to Requirement 4:.....................................................................................................5

Issue:..................................................................................................................................5

Legislations:.......................................................................................................................5

Application:........................................................................................................................5

Table of Contents

Answer to Question 1:................................................................................................................3

Answer to Requirement 1:.....................................................................................................3

Issue:..................................................................................................................................3

Legislations:.......................................................................................................................3

Application:........................................................................................................................3

Conclusion:........................................................................................................................4

Answer to Requirement 2:.....................................................................................................4

Issue:..................................................................................................................................4

Legislations:.......................................................................................................................4

Application:........................................................................................................................4

Conclusion:........................................................................................................................4

Answer to Requirement 3:.....................................................................................................4

Issue:..................................................................................................................................4

Legislations:.......................................................................................................................4

Application:........................................................................................................................5

Conclusion:........................................................................................................................5

Answer to Requirement 4:.....................................................................................................5

Issue:..................................................................................................................................5

Legislations:.......................................................................................................................5

Application:........................................................................................................................5

2TAXATION LAW

Conclusion:........................................................................................................................5

Answer to Question 2:................................................................................................................5

Issue:......................................................................................................................................5

Legislations:...........................................................................................................................5

Application:............................................................................................................................5

Conclusion:............................................................................................................................6

Answer to Question 3:................................................................................................................6

Answer to Question 4:................................................................................................................6

References:.................................................................................................................................8

Conclusion:........................................................................................................................5

Answer to Question 2:................................................................................................................5

Issue:......................................................................................................................................5

Legislations:...........................................................................................................................5

Application:............................................................................................................................5

Conclusion:............................................................................................................................6

Answer to Question 3:................................................................................................................6

Answer to Question 4:................................................................................................................6

References:.................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to Question 1:

Answer to Requirement 1:

Issue:

The issue is related to ascertaining the deductions that would be allowed under

“section 8-1 of the ITAA 1997” with respect to the cost happened in the shifting of machine.

Legislations:

a. “Section 8-1 of the ITAA 1997”

b. “British Insulated &Helsby Cables”

Application:

The charge that has taken place for shifting the machine to new location signifies

capital expenditure and admissible deductions permitted under the “Section 8-1 of the

Income Tax Assessment Act 1997”. In case of depreciation, the shifting of machinery to new

site has raised the overall asset cost. The charge that has occurred for shifting the machine to

the new location signifies a charge followed from minor changes and means to be allowable

in the form of admissible deductions, as per the “section 8-1 of the ITAA 1997”. The sole

reason for considering the expenses for allowable deductions is that the cost is considered as

portion of the business expenditures arising from the daily business operations (Blakelock

and King 2017).

With special reference to the result obtained in the case of “British Insulated

&Helsby Cables”, the charge arising out of the carriage features a continuous benefit on the

trade-associated locations through location of the depreciable assets (Becker, Reimer and

Rust 2015). According to the “taxation rule of TD 93/126” in relation to the machinery

installation and initiation of the business operations, the occurrence of cost to shift the

Answer to Question 1:

Answer to Requirement 1:

Issue:

The issue is related to ascertaining the deductions that would be allowed under

“section 8-1 of the ITAA 1997” with respect to the cost happened in the shifting of machine.

Legislations:

a. “Section 8-1 of the ITAA 1997”

b. “British Insulated &Helsby Cables”

Application:

The charge that has taken place for shifting the machine to new location signifies

capital expenditure and admissible deductions permitted under the “Section 8-1 of the

Income Tax Assessment Act 1997”. In case of depreciation, the shifting of machinery to new

site has raised the overall asset cost. The charge that has occurred for shifting the machine to

the new location signifies a charge followed from minor changes and means to be allowable

in the form of admissible deductions, as per the “section 8-1 of the ITAA 1997”. The sole

reason for considering the expenses for allowable deductions is that the cost is considered as

portion of the business expenditures arising from the daily business operations (Blakelock

and King 2017).

With special reference to the result obtained in the case of “British Insulated

&Helsby Cables”, the charge arising out of the carriage features a continuous benefit on the

trade-associated locations through location of the depreciable assets (Becker, Reimer and

Rust 2015). According to the “taxation rule of TD 93/126” in relation to the machinery

installation and initiation of the business operations, the occurrence of cost to shift the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

machine in overall operation would be treated as revenue. It has been laid out under the

current incidence of state of charge in situating the machine to the new site features a nature

of the capital cost and this would be treated in the form of deductions, which are not allowed.

Conclusion:

From the above analysis, it has been found out that the relocation of machine

to the fresh destination is not permissible to deduct due to capital cost and it is restricted from

being taken into account as deductions in accordance with “section 8-1 of the ITAA 1997”.

Answer to Requirement 2:

Issue:

The existing state is familiar with whether or not the asset revaluation to influence the

insurance cover would be viewed in the form of permitted deductions, as per the “section 8-1

ITAA 1997” (Hill and Mancino 2014).

Legislations:

“Section 8 (1) of ITAA 1997”

Application:

As identified from the current scenario, the expense having relation with the non-

current asset to ascertain the deductions is crucial to ascertain whether such expenditures

have taken place in revaluation acquires in enhancing the revenue generation capacity. In

case of the second proposal consequences as profit of transitory nature, then it would be taken

as acceptable deductions according to “Section 8 (1) of ITAA 1997”. Evidence obtained from

the current state incidence of charge in asset revaluation as the insurance cover consequence

would be acceptable in the form of admissible tax deductions in accordance with section 8(1)

at the time the outflow occurred are primarily repeating cost.

machine in overall operation would be treated as revenue. It has been laid out under the

current incidence of state of charge in situating the machine to the new site features a nature

of the capital cost and this would be treated in the form of deductions, which are not allowed.

Conclusion:

From the above analysis, it has been found out that the relocation of machine

to the fresh destination is not permissible to deduct due to capital cost and it is restricted from

being taken into account as deductions in accordance with “section 8-1 of the ITAA 1997”.

Answer to Requirement 2:

Issue:

The existing state is familiar with whether or not the asset revaluation to influence the

insurance cover would be viewed in the form of permitted deductions, as per the “section 8-1

ITAA 1997” (Hill and Mancino 2014).

Legislations:

“Section 8 (1) of ITAA 1997”

Application:

As identified from the current scenario, the expense having relation with the non-

current asset to ascertain the deductions is crucial to ascertain whether such expenditures

have taken place in revaluation acquires in enhancing the revenue generation capacity. In

case of the second proposal consequences as profit of transitory nature, then it would be taken

as acceptable deductions according to “Section 8 (1) of ITAA 1997”. Evidence obtained from

the current state incidence of charge in asset revaluation as the insurance cover consequence

would be acceptable in the form of admissible tax deductions in accordance with section 8(1)

at the time the outflow occurred are primarily repeating cost.

5TAXATION LAW

Conclusion:

Based on the analysis in relation to the revaluing cost, it could be ascertained that the

insurance cover cost is identified as admissible deductions related to income tax.

Subsequently, it could be adjudged as periodic cost and it needs to be regarded as acceptable

deductions of income tax, as per the “8-1 of the ITAA 1997”.

Answer to Requirement 3:

Issue:

The statement initiates the circumstances, which carries with the question of whether

the legal expenditures that the taxpayer has incurred for opposing the requisition to wind up

would be observed for deductions of income tax allowable under the supervision of “section

8-1 of the ITAA 1997”.

Legislations:

a. “Section 8-1 of ITAA”

b. “FC of T v Snowden and Wilson Pty Ltd (1958)”

Application:

In relation to the above issue and under the supervision of “section 8-1 of the ITAA

1997”, the charge occurred in winding up the business and they are not observed in the form

of acceptable deductions of income tax. According to the “taxation ruling of ID 2004/367”,

the legal cost would be taken into account for deductions; in case, the cost is for conduction

of the business operation through which a person develops the taxable proceeds (Kingston

2015).

Conclusion:

Based on the analysis in relation to the revaluing cost, it could be ascertained that the

insurance cover cost is identified as admissible deductions related to income tax.

Subsequently, it could be adjudged as periodic cost and it needs to be regarded as acceptable

deductions of income tax, as per the “8-1 of the ITAA 1997”.

Answer to Requirement 3:

Issue:

The statement initiates the circumstances, which carries with the question of whether

the legal expenditures that the taxpayer has incurred for opposing the requisition to wind up

would be observed for deductions of income tax allowable under the supervision of “section

8-1 of the ITAA 1997”.

Legislations:

a. “Section 8-1 of ITAA”

b. “FC of T v Snowden and Wilson Pty Ltd (1958)”

Application:

In relation to the above issue and under the supervision of “section 8-1 of the ITAA

1997”, the charge occurred in winding up the business and they are not observed in the form

of acceptable deductions of income tax. According to the “taxation ruling of ID 2004/367”,

the legal cost would be taken into account for deductions; in case, the cost is for conduction

of the business operation through which a person develops the taxable proceeds (Kingston

2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

As observed from “FC of T v Snowden and Wilson Pty Ltd (1958)”, the unusual

expenses and the taxpayer in no previous occasion are crucial to start the lawful actions, as it

could not prevent the expense for qualifying as deductible expense (Lang 2014).

Conclusion:

With reference to the above analysis concerning the cost occurring in opposition to

the business wind up, it would be considered as non-permissible deductions of income tax, as

per the “section 8-1 of the ITAA 1997”.

Answer to Requirement 4:

Issue:

The statement conducts the issue of ascertaining whether or not the legal

disbursement to obtain the solicitor services for discharging different commercial processes

of the taxpayer would be considered as admissible deductions of income tax in accordance

with the “section 8-1 of the ITAA 1997”.

Legislations:

a. “section 8-1 of ITAA 1997”

Application:

Based on the primary statement developed within the context of “section 8-1 of the

Income Tax Assessment Act 1997”, when the taxpayer incurs legal expenditure with the

intention of obtaining various business functions for yielding profit, such type of outlay

would be considered in the form of income tax deductions. However, there are certain types

of exception to the norms of “section 8-1 of the ITAA”, in which the legal outlay occurrence

taken place denotes the capital character, private and domestic expense or the incurring of

expenditure to yield the exempted and non-chargeable non-exempt proceeds.

As observed from “FC of T v Snowden and Wilson Pty Ltd (1958)”, the unusual

expenses and the taxpayer in no previous occasion are crucial to start the lawful actions, as it

could not prevent the expense for qualifying as deductible expense (Lang 2014).

Conclusion:

With reference to the above analysis concerning the cost occurring in opposition to

the business wind up, it would be considered as non-permissible deductions of income tax, as

per the “section 8-1 of the ITAA 1997”.

Answer to Requirement 4:

Issue:

The statement conducts the issue of ascertaining whether or not the legal

disbursement to obtain the solicitor services for discharging different commercial processes

of the taxpayer would be considered as admissible deductions of income tax in accordance

with the “section 8-1 of the ITAA 1997”.

Legislations:

a. “section 8-1 of ITAA 1997”

Application:

Based on the primary statement developed within the context of “section 8-1 of the

Income Tax Assessment Act 1997”, when the taxpayer incurs legal expenditure with the

intention of obtaining various business functions for yielding profit, such type of outlay

would be considered in the form of income tax deductions. However, there are certain types

of exception to the norms of “section 8-1 of the ITAA”, in which the legal outlay occurrence

taken place denotes the capital character, private and domestic expense or the incurring of

expenditure to yield the exempted and non-chargeable non-exempt proceeds.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Conclusion:

In accordance with the above discussion, the occurrence of legal expense in relation to

the business operations for developing the taxable income needs to treated as allowable

deductions with reference to “section 8-1 of the ITAA 1997”.

Answer to Question 2:

Issue:

If a business organisation makes any purchase, the input credit of GST is permitted

only, in case; pertinent documents are stored properly in association with such transactions.

According to “GST Act 1999”, any organisation intending to make business income

possesses the right to obtain credit of input for payments related to GST involving material or

asset purchase (Peattie 2013). It has been identified from the provided case that Big Bank

Limited has incurred advertisement expenditure of $1,650,000 that includes GST as well. In

the current scenario, the bank intends to assure that the overall expenditures related to

advertisement would be permitted as credit of input or not, as the expenditures include GST.

Legislations:

As identified from the “Chapter 2 of the Goods and Services Act 1999”, input tax

credit including GST would be permitted to an organisation on the incurred expenditures at

the time of general course of the business. However, it is to be noted that such expenses

include the amount of GST.

Application:

Big Bank Limited is a financial organisation that provides services to the individuals

having more than 50 branches throughout the province of Australia. It has a 10-storied

apartment, in which its head office is situated. Along with, there has been the introduction of

Conclusion:

In accordance with the above discussion, the occurrence of legal expense in relation to

the business operations for developing the taxable income needs to treated as allowable

deductions with reference to “section 8-1 of the ITAA 1997”.

Answer to Question 2:

Issue:

If a business organisation makes any purchase, the input credit of GST is permitted

only, in case; pertinent documents are stored properly in association with such transactions.

According to “GST Act 1999”, any organisation intending to make business income

possesses the right to obtain credit of input for payments related to GST involving material or

asset purchase (Peattie 2013). It has been identified from the provided case that Big Bank

Limited has incurred advertisement expenditure of $1,650,000 that includes GST as well. In

the current scenario, the bank intends to assure that the overall expenditures related to

advertisement would be permitted as credit of input or not, as the expenditures include GST.

Legislations:

As identified from the “Chapter 2 of the Goods and Services Act 1999”, input tax

credit including GST would be permitted to an organisation on the incurred expenditures at

the time of general course of the business. However, it is to be noted that such expenses

include the amount of GST.

Application:

Big Bank Limited is a financial organisation that provides services to the individuals

having more than 50 branches throughout the province of Australia. It has a 10-storied

apartment, in which its head office is situated. Along with, there has been the introduction of

8TAXATION LAW

home content and insurance policy in Australian market coupled with loan and deposit

provisions of the customers over the years1. In order to carry out advertising work, the bank

has kept apart a budget amounting to $1,650,000 from which $550,000 is invested for house

advertisement and insurance products. With the help of such investment, the organisation has

managed to generate 2% of its overall revenues. The leftover amount of $1,100,000 is for

promoting the other services of the organisation and it takes into consideration the GST as

well (Saad 2014).

Therefore, it has been evaluated that $1,100,000 had been incurred for the promotion

of services for generation of maximum revenue, while the amount of $550,000 is to be

considered as capital expense. This is because the newly launched product would contribute

towards the income generation of the organisation (Wigmore 2016).

Conclusion:

From the above discussion, it is inherent that the sum of $1,100,000 that the

organisation has spent on advertising its current products and services would be allowed to

obtain credit input. On the contrary, the overall amount of $550,000 would not be restricted

to obtain credit of input, since 2% of such expense contributes towards the generation of

income of Big Bank Limited.

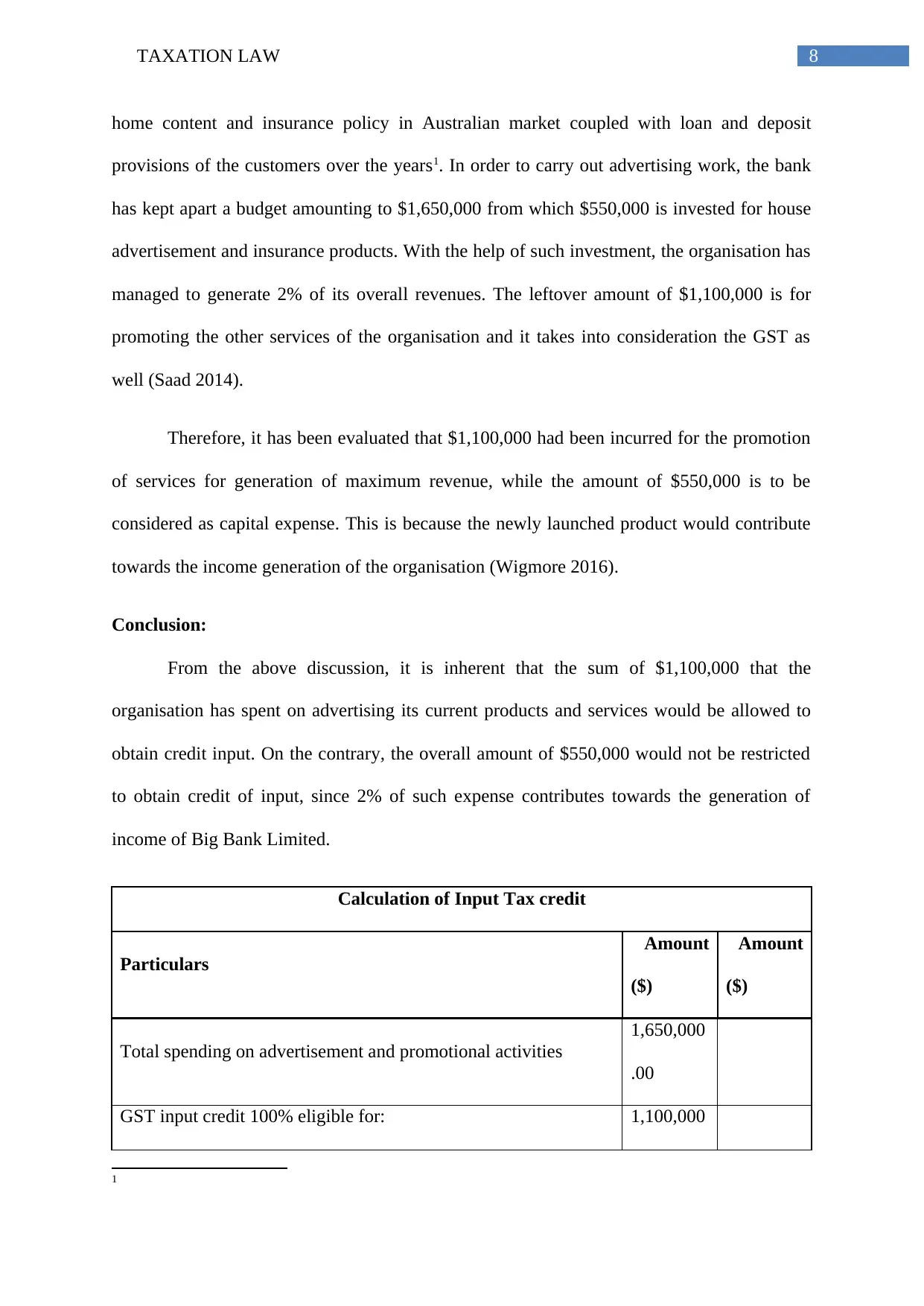

Calculation of Input Tax credit

Particulars

Amount

($)

Amount

($)

Total spending on advertisement and promotional activities

1,650,000

.00

GST input credit 100% eligible for: 1,100,000

1

home content and insurance policy in Australian market coupled with loan and deposit

provisions of the customers over the years1. In order to carry out advertising work, the bank

has kept apart a budget amounting to $1,650,000 from which $550,000 is invested for house

advertisement and insurance products. With the help of such investment, the organisation has

managed to generate 2% of its overall revenues. The leftover amount of $1,100,000 is for

promoting the other services of the organisation and it takes into consideration the GST as

well (Saad 2014).

Therefore, it has been evaluated that $1,100,000 had been incurred for the promotion

of services for generation of maximum revenue, while the amount of $550,000 is to be

considered as capital expense. This is because the newly launched product would contribute

towards the income generation of the organisation (Wigmore 2016).

Conclusion:

From the above discussion, it is inherent that the sum of $1,100,000 that the

organisation has spent on advertising its current products and services would be allowed to

obtain credit input. On the contrary, the overall amount of $550,000 would not be restricted

to obtain credit of input, since 2% of such expense contributes towards the generation of

income of Big Bank Limited.

Calculation of Input Tax credit

Particulars

Amount

($)

Amount

($)

Total spending on advertisement and promotional activities

1,650,000

.00

GST input credit 100% eligible for: 1,100,000

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

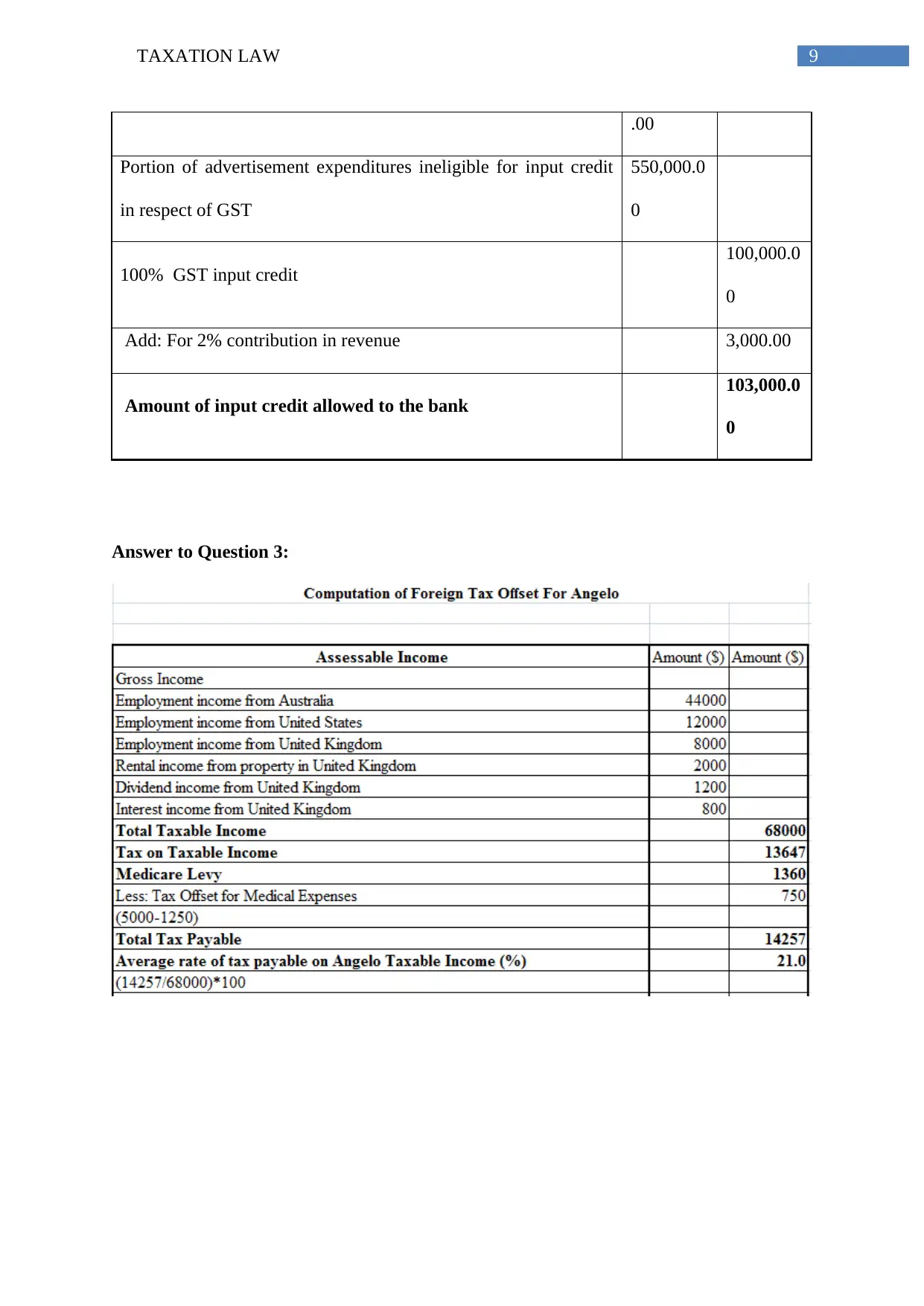

.00

Portion of advertisement expenditures ineligible for input credit

in respect of GST

550,000.0

0

100% GST input credit

100,000.0

0

Add: For 2% contribution in revenue 3,000.00

Amount of input credit allowed to the bank

103,000.0

0

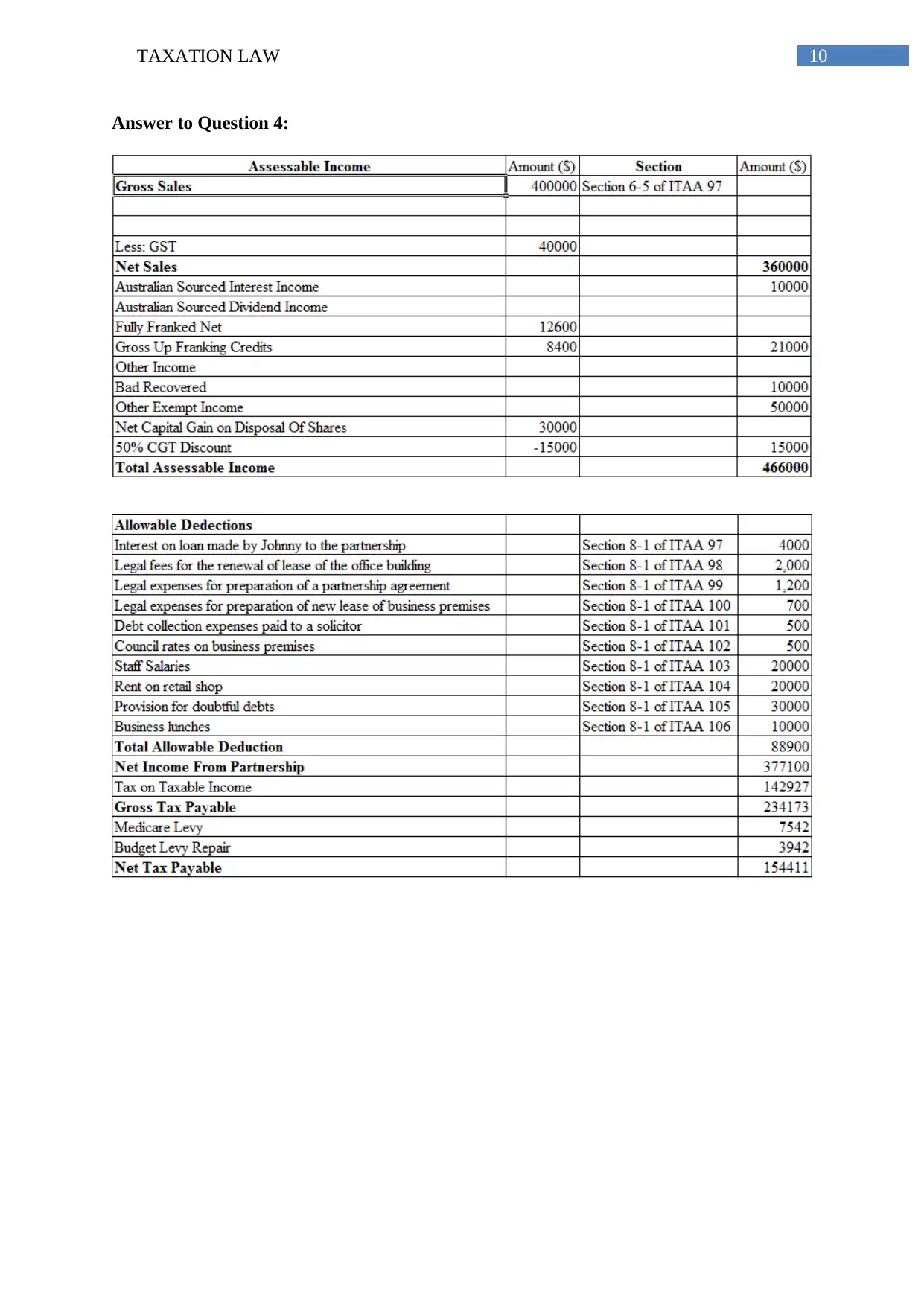

Answer to Question 3:

.00

Portion of advertisement expenditures ineligible for input credit

in respect of GST

550,000.0

0

100% GST input credit

100,000.0

0

Add: For 2% contribution in revenue 3,000.00

Amount of input credit allowed to the bank

103,000.0

0

Answer to Question 3:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

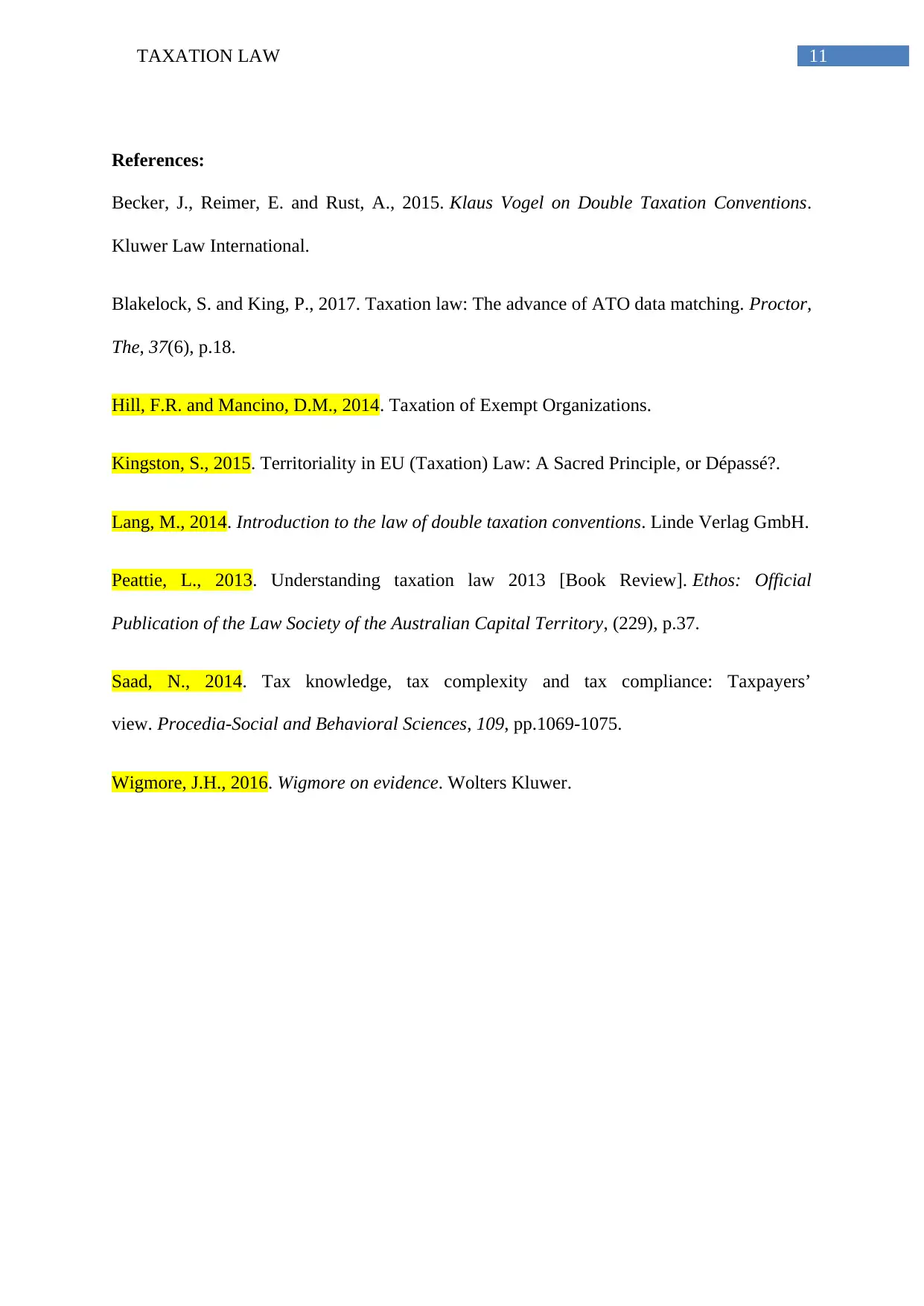

Answer to Question 4:

Answer to Question 4:

11TAXATION LAW

References:

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data matching. Proctor,

The, 37(6), p.18.

Hill, F.R. and Mancino, D.M., 2014. Taxation of Exempt Organizations.

Kingston, S., 2015. Territoriality in EU (Taxation) Law: A Sacred Principle, or Dépassé?.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Peattie, L., 2013. Understanding taxation law 2013 [Book Review]. Ethos: Official

Publication of the Law Society of the Australian Capital Territory, (229), p.37.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Wigmore, J.H., 2016. Wigmore on evidence. Wolters Kluwer.

References:

Becker, J., Reimer, E. and Rust, A., 2015. Klaus Vogel on Double Taxation Conventions.

Kluwer Law International.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data matching. Proctor,

The, 37(6), p.18.

Hill, F.R. and Mancino, D.M., 2014. Taxation of Exempt Organizations.

Kingston, S., 2015. Territoriality in EU (Taxation) Law: A Sacred Principle, or Dépassé?.

Lang, M., 2014. Introduction to the law of double taxation conventions. Linde Verlag GmbH.

Peattie, L., 2013. Understanding taxation law 2013 [Book Review]. Ethos: Official

Publication of the Law Society of the Australian Capital Territory, (229), p.37.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Wigmore, J.H., 2016. Wigmore on evidence. Wolters Kluwer.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.