TAXATION LAW 14: Deductions, GST, and Legal Expenditure Analysis

VerifiedAdded on 2020/04/07

|15

|2700

|49

Homework Assignment

AI Summary

This taxation law assignment solution analyzes several key issues related to Australian tax law. Question 1.1 examines whether the cost of moving a machine to a new site is an allowable deduction, concluding it is not, based on ITAA 1997 and relevant rulings. Question 1.2 assesses the deductibility of asset revaluation expenses for insurance, determining they are deductible due to their repetitive nature. Question 1.3 addresses the deductibility of legal expenses incurred to oppose a winding-up petition, concluding they are not deductible as they are capital in nature. Question 1.4 considers the deductibility of solicitor services for business functions, determining they are deductible. Question 2 focuses on input tax credits related to GST supplies, specifically advertising expenses, analyzing the applicability of the GST Act 1999 and relevant rulings like GSTR 2006/3 and case law such as Ronpibon Tin NL v FC of T, and detailing how Big Bank Ltd can claim input tax credits. The assignment provides thorough analysis of the issues, rules, and applications, and offers clear conclusions for each scenario.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to Question 1.1:.............................................................................................................3

Issue:..........................................................................................................................................3

Rule:...........................................................................................................................................3

Application:................................................................................................................................3

Conclusion:................................................................................................................................4

Answer to question 1.2:..............................................................................................................4

Issue:..........................................................................................................................................4

Rule:...........................................................................................................................................4

Application:................................................................................................................................4

Answer to question 1.3:..............................................................................................................5

Issue:..........................................................................................................................................5

Rule:...........................................................................................................................................5

Application:................................................................................................................................5

Answer to question 1.4:..............................................................................................................6

Issue:..........................................................................................................................................6

Rule:...........................................................................................................................................6

Applications:..............................................................................................................................6

Conclusion:................................................................................................................................7

Answer to question 2:.................................................................................................................7

Issue:..........................................................................................................................................7

Table of Contents

Answer to Question 1.1:.............................................................................................................3

Issue:..........................................................................................................................................3

Rule:...........................................................................................................................................3

Application:................................................................................................................................3

Conclusion:................................................................................................................................4

Answer to question 1.2:..............................................................................................................4

Issue:..........................................................................................................................................4

Rule:...........................................................................................................................................4

Application:................................................................................................................................4

Answer to question 1.3:..............................................................................................................5

Issue:..........................................................................................................................................5

Rule:...........................................................................................................................................5

Application:................................................................................................................................5

Answer to question 1.4:..............................................................................................................6

Issue:..........................................................................................................................................6

Rule:...........................................................................................................................................6

Applications:..............................................................................................................................6

Conclusion:................................................................................................................................7

Answer to question 2:.................................................................................................................7

Issue:..........................................................................................................................................7

2TAXATION LAW

Rule:...........................................................................................................................................7

Applications:..............................................................................................................................8

Conclusion:..............................................................................................................................10

Answer to question 3:...............................................................................................................10

Answer to question 4:...............................................................................................................12

Reference List..........................................................................................................................14

Rule:...........................................................................................................................................7

Applications:..............................................................................................................................8

Conclusion:..............................................................................................................................10

Answer to question 3:...............................................................................................................10

Answer to question 4:...............................................................................................................12

Reference List..........................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to Question 1.1:

Issue:

The issues relating to the study has been seen in terms of whether the cost involved

for moving the machine to the new site shall be considered for non-allowable or allowable

deductions.

Rule:

I. “Section 8-1 of the ITAA 1997”

II. “Britissh Insulated & Helsby Cables”

III. “Taxation ruling of TD 92/126”

Application:

Individual taxpayers shall be entitled for deductions in case the expenditure has been

seen to take place for the purpose of assessable income. As per “Section 8-1 of the ITAA”

the different expenses relating to moving the machine is seen to represent an additional

increase in the acid cost. Based on the present context it has been discerned that the cost of

moving the machine in the new site shall be not entitled for the purpose of allowable

deductions. The sole reason for this is due to the fact that these non-allowable entitlements

need to an increase in the cost of asset (Barkoczy 2016).

As signified in “British Insulated & Helsby Cables” the cost involved in the

transportation signifies that there is a persistent benefit for the business by allocating the

depreciable asset in a new location. As defined in “Taxation ruling of TD 92/126”,

installation of the machine and starting of the business process is viewed as a part of the

revenue. Henceforth, it can be suggested that the expense incurred in carrying the machine to

Answer to Question 1.1:

Issue:

The issues relating to the study has been seen in terms of whether the cost involved

for moving the machine to the new site shall be considered for non-allowable or allowable

deductions.

Rule:

I. “Section 8-1 of the ITAA 1997”

II. “Britissh Insulated & Helsby Cables”

III. “Taxation ruling of TD 92/126”

Application:

Individual taxpayers shall be entitled for deductions in case the expenditure has been

seen to take place for the purpose of assessable income. As per “Section 8-1 of the ITAA”

the different expenses relating to moving the machine is seen to represent an additional

increase in the acid cost. Based on the present context it has been discerned that the cost of

moving the machine in the new site shall be not entitled for the purpose of allowable

deductions. The sole reason for this is due to the fact that these non-allowable entitlements

need to an increase in the cost of asset (Barkoczy 2016).

As signified in “British Insulated & Helsby Cables” the cost involved in the

transportation signifies that there is a persistent benefit for the business by allocating the

depreciable asset in a new location. As defined in “Taxation ruling of TD 92/126”,

installation of the machine and starting of the business process is viewed as a part of the

revenue. Henceforth, it can be suggested that the expense incurred in carrying the machine to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

the new site location shall be treated as per cost of capital and not be entitled under allowable

portion of deductions (Datt et al. 2017).

Conclusion:

The consideration of the above explanation shows that the cost in moving the machine

is not entitled for the total allowable deductions from the time such costs are seen to be

portraying an outlay of the capital.

Answer to question 1.2:

Issue:

The main issue as per the present case has been subjected to the main concern

whether the revaluation of the asset expense with the effect of insurance cover shall be

entitled with “Section 8-1 of the ITAA 1997” for the purpose of allowable deductions.

Rule:

I. “Section 8-1 of ITAA 1997”

Application:

As for the given situation it can be clearly seen that the cost has taken place as a result

of revaluation of the assets for insurance cover which needs to be considered for allowable

deductions. With reference to “Section 8-1 of the ITAA 1997”, it has been discerned that the

expense needs to be treated under allowable deductions as it has outlaid the features which

are repetitive in nature. The outlay considered for asset evaluation is for the thing to be done

on a straight-line basis which is related to the assets which are fixed (Saad 2014). The

consideration of taxable return has been obligated to be determined for nature of deductibility

of expenditure and evaluate whether it can be considered during the evaluation stage due to

increase in the revenue generated from the activity or precaution of the asset. As evident with

the new site location shall be treated as per cost of capital and not be entitled under allowable

portion of deductions (Datt et al. 2017).

Conclusion:

The consideration of the above explanation shows that the cost in moving the machine

is not entitled for the total allowable deductions from the time such costs are seen to be

portraying an outlay of the capital.

Answer to question 1.2:

Issue:

The main issue as per the present case has been subjected to the main concern

whether the revaluation of the asset expense with the effect of insurance cover shall be

entitled with “Section 8-1 of the ITAA 1997” for the purpose of allowable deductions.

Rule:

I. “Section 8-1 of ITAA 1997”

Application:

As for the given situation it can be clearly seen that the cost has taken place as a result

of revaluation of the assets for insurance cover which needs to be considered for allowable

deductions. With reference to “Section 8-1 of the ITAA 1997”, it has been discerned that the

expense needs to be treated under allowable deductions as it has outlaid the features which

are repetitive in nature. The outlay considered for asset evaluation is for the thing to be done

on a straight-line basis which is related to the assets which are fixed (Saad 2014). The

consideration of taxable return has been obligated to be determined for nature of deductibility

of expenditure and evaluate whether it can be considered during the evaluation stage due to

increase in the revenue generated from the activity or precaution of the asset. As evident with

5TAXATION LAW

the cost, the impermanent nature of advantage and aspects of repetitive nature needs to be

entitled for the deductions under “Section 8-1 of the ITAA 1997” (Deutsch 2014).

Conclusion:

As inferred from the above explanation it can be said that the outlay encoding the

devaluation of asset is to be entitled for deductions as per “Section 8-1 of the ITAA 1997”

with the main reason being the nature of repetitiveness.

Answer to question 1.3:

Issue:

based on the current situation the main question has been raised whether the legal expenditure

incurred by an individual taxpayer for the purpose of opposing the petition winding up needs

to be considered for allowable deductions.

Rule:

I. “FC of T v Snowden and Wilson Pty Ltd (1958)”

II. “Section 8-1 of the ITAA 1997”

Application:

As per the given case study can be discerned that any winding up of business activity

needs to be normally treated under the outlay of the business functions and shall not be

regarded as entitlement for the allowable deductions under “Section 8-1 of the ITAA 1997”.

As stated under the “Taxation ruling of ID 2004/367” the main cost of carrying out of

business operations needs to be considered for allowable deductions. The main rationale for

this is due to the expenses which are delectable in nature as the cost is incurred by the

taxpayer for producing the visible income (Millar 2014).

the cost, the impermanent nature of advantage and aspects of repetitive nature needs to be

entitled for the deductions under “Section 8-1 of the ITAA 1997” (Deutsch 2014).

Conclusion:

As inferred from the above explanation it can be said that the outlay encoding the

devaluation of asset is to be entitled for deductions as per “Section 8-1 of the ITAA 1997”

with the main reason being the nature of repetitiveness.

Answer to question 1.3:

Issue:

based on the current situation the main question has been raised whether the legal expenditure

incurred by an individual taxpayer for the purpose of opposing the petition winding up needs

to be considered for allowable deductions.

Rule:

I. “FC of T v Snowden and Wilson Pty Ltd (1958)”

II. “Section 8-1 of the ITAA 1997”

Application:

As per the given case study can be discerned that any winding up of business activity

needs to be normally treated under the outlay of the business functions and shall not be

regarded as entitlement for the allowable deductions under “Section 8-1 of the ITAA 1997”.

As stated under the “Taxation ruling of ID 2004/367” the main cost of carrying out of

business operations needs to be considered for allowable deductions. The main rationale for

this is due to the expenses which are delectable in nature as the cost is incurred by the

taxpayer for producing the visible income (Millar 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

With reference to the case “FC of T v Snowden and Wilson Pty Ltd (1958)”,

the expense or the whole place are seen to be arising from ordinary course and the individual

taxpayer is required to held admissible for the allowable deductions.

The various types of legal expenses with the present context for opposing the

winding of the edition shall not be entitled for admissible deductions. Despite of the various

types of expenses which have been qualified and that the positive limbs, it shall not be

considered for allowable deductions as it is deep-rooted within the business structure.

Various incidence of the legal cost shall not be treated for admissible deductions as it is

owned by the features of capital (Fry 2017).

Conclusion:

as per the denoted assessments it can be inferred that the various types of cost for

opposing the petition for winding up of business needs to be barred from allowable

deductions as it owns the attributes of capital under “Section 8-1 of the ITAA 1997”.

Answer to question 1.4:

Issue:

The most significant issue has been held in consideration with whether expenses of

the services of solicitor for the business needs to be considered as for the deductions under

“Section 8-1 of the ITAA 1997”.

Rule:

I. “Section 8-1 of the ITAA 1997”

Applications:

As for the aforementioned ruling the legal expenditure associated to the trading

activities needs to be considered for admissible deductions. It has been further seen to be

With reference to the case “FC of T v Snowden and Wilson Pty Ltd (1958)”,

the expense or the whole place are seen to be arising from ordinary course and the individual

taxpayer is required to held admissible for the allowable deductions.

The various types of legal expenses with the present context for opposing the

winding of the edition shall not be entitled for admissible deductions. Despite of the various

types of expenses which have been qualified and that the positive limbs, it shall not be

considered for allowable deductions as it is deep-rooted within the business structure.

Various incidence of the legal cost shall not be treated for admissible deductions as it is

owned by the features of capital (Fry 2017).

Conclusion:

as per the denoted assessments it can be inferred that the various types of cost for

opposing the petition for winding up of business needs to be barred from allowable

deductions as it owns the attributes of capital under “Section 8-1 of the ITAA 1997”.

Answer to question 1.4:

Issue:

The most significant issue has been held in consideration with whether expenses of

the services of solicitor for the business needs to be considered as for the deductions under

“Section 8-1 of the ITAA 1997”.

Rule:

I. “Section 8-1 of the ITAA 1997”

Applications:

As for the aforementioned ruling the legal expenditure associated to the trading

activities needs to be considered for admissible deductions. It has been further seen to be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

worth noting that for the purpose of meeting the criteria of the legal expenditure trading

activities shall be directly linked to produce higher revenue. As per the rulings of “Section 8-

1 of the ITAA 1997” in case the various types of legal outlay seen to be of personal, capital

and domestic in nature then it cannot be regarded as a non-exemption, non-admissible and

non-assessable deductions. With relevance to the present issue, the individual taxpayers who

are seen to be incurring the legal expense, the solicitor responsible for discharging the

business functions needs to be treated as an exemption of the expenses as the individual will

qualify for the allowable deductions as per “Section 8-1 of the ITAA 1997”.

Conclusion:

Based on the conduction of interpretations of legal expenditure, various services of

the solicitor for discharging of business functions needs to be taken into consideration as per

the rulings of allowable deductions as stated under “Section 8-1 of the ITAA 1997”. The

main rationale for this is that the legal expenditure is considered as a liability reduction as it

has been incurred with the revenue generating activities.

Answer to question 2:

Issue:

The main form of existing issue has been seen in terms of data mining the input tax

credit associated to the GST supplies which has been made under “GST Act 1999”.

Rule:

I. “Ronpibon Tin NL v FC of T”

II. “Goods and Service Taxation Ruling of GSTR 2006/3”

III. “GST Act 1999”

worth noting that for the purpose of meeting the criteria of the legal expenditure trading

activities shall be directly linked to produce higher revenue. As per the rulings of “Section 8-

1 of the ITAA 1997” in case the various types of legal outlay seen to be of personal, capital

and domestic in nature then it cannot be regarded as a non-exemption, non-admissible and

non-assessable deductions. With relevance to the present issue, the individual taxpayers who

are seen to be incurring the legal expense, the solicitor responsible for discharging the

business functions needs to be treated as an exemption of the expenses as the individual will

qualify for the allowable deductions as per “Section 8-1 of the ITAA 1997”.

Conclusion:

Based on the conduction of interpretations of legal expenditure, various services of

the solicitor for discharging of business functions needs to be taken into consideration as per

the rulings of allowable deductions as stated under “Section 8-1 of the ITAA 1997”. The

main rationale for this is that the legal expenditure is considered as a liability reduction as it

has been incurred with the revenue generating activities.

Answer to question 2:

Issue:

The main form of existing issue has been seen in terms of data mining the input tax

credit associated to the GST supplies which has been made under “GST Act 1999”.

Rule:

I. “Ronpibon Tin NL v FC of T”

II. “Goods and Service Taxation Ruling of GSTR 2006/3”

III. “GST Act 1999”

8TAXATION LAW

Applications:

Based on the given case of the Big Bank is seen to be concerned for the determination

of GST supplies based on input tax credit as for the advertisement expenses. It is for the

noting that the second chapter of “GST Act 1999” has been able to provide vital

consideration for commercial units which needs to be permitted for claimed input tax

incurred by the organisation as for normal course of business operations. Despite of this, the

claiming process of input tax must be considered by adding of the GST amount. The given

case study of Big Bank Ltd has been able to bring about the various types of financial

services put forward to the customers in more than 50 branches in the country. Big Bank has

been further able to bring about the services associated to program of insurance and home

content into the market aside from providing various types of facilities of deposits and loans

to its customers. With reference to “Taxation Ruling of GSTR 2006/3” important rules and

regulations laid down in the process of tax computation has been observed (May 2016).

As per “division 11-15 and 129 of the GST Act 1999” the total creditable amount

for acquisition and imposition for the ruling has been previously mentioned. As per the

taxation rulings of “GSTR 2006/3” in organisation has exceeded the financial invitation for

acquisition in the purview of lower input tax credit.

It has been further evident from the case study of Big Bank Ltd that the organisation

has incurred its expenses based on the advertising and which is inclusive of the “Goods and

Service Tax”. As per the present issues brought forward by Big Bank Ltd it can be clearly

stated that the main rulings under “GSTR 2006/3” is applicable for the given situation. The

main reason for GST application is seen with “GSTR 2006/3” as Big Bank has been able to

successfully qualify self for tax credit claiming input. Based on the principle as per “GSTR

2006/3”, it is in discern that in case a commercial concern is registered under the ruling of

Applications:

Based on the given case of the Big Bank is seen to be concerned for the determination

of GST supplies based on input tax credit as for the advertisement expenses. It is for the

noting that the second chapter of “GST Act 1999” has been able to provide vital

consideration for commercial units which needs to be permitted for claimed input tax

incurred by the organisation as for normal course of business operations. Despite of this, the

claiming process of input tax must be considered by adding of the GST amount. The given

case study of Big Bank Ltd has been able to bring about the various types of financial

services put forward to the customers in more than 50 branches in the country. Big Bank has

been further able to bring about the services associated to program of insurance and home

content into the market aside from providing various types of facilities of deposits and loans

to its customers. With reference to “Taxation Ruling of GSTR 2006/3” important rules and

regulations laid down in the process of tax computation has been observed (May 2016).

As per “division 11-15 and 129 of the GST Act 1999” the total creditable amount

for acquisition and imposition for the ruling has been previously mentioned. As per the

taxation rulings of “GSTR 2006/3” in organisation has exceeded the financial invitation for

acquisition in the purview of lower input tax credit.

It has been further evident from the case study of Big Bank Ltd that the organisation

has incurred its expenses based on the advertising and which is inclusive of the “Goods and

Service Tax”. As per the present issues brought forward by Big Bank Ltd it can be clearly

stated that the main rulings under “GSTR 2006/3” is applicable for the given situation. The

main reason for GST application is seen with “GSTR 2006/3” as Big Bank has been able to

successfully qualify self for tax credit claiming input. Based on the principle as per “GSTR

2006/3”, it is in discern that in case a commercial concern is registered under the ruling of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

“GST Act 1999”, or it needs to get the registration, can be stated that such an concern needs

to make payment of GST with the amount of financial supplies available.

The total GST rulings as per “GSTR 2006/3” has been able to state that the various

types of commercial entities are able to claim for the input tax credit associated to supplies of

financial assistance including the GST amount. On the contrary, in case the commercial

entities goes beyond the financial acquisition limit then in such a case the taxable entity will

not be permitted to claim for the full amount of input tax credit. However, it will be eligible

for claiming of only a portion of the same.

As per the case denoted under the ruling of “Ronpibon Tin NL v FC of T” the most

significant feature of GST ruling of “GSTR 2006/3” has been determined in terms of

“extent” and “to the extent” for the total GST supplies made. As per this legislation, that is

meant of GST as the based on responsibility and fairness of the commercial entities. As noted

in the “para 11-5 and 15-5” the various types of GST rulings for “GSTR 2006/3” has been

based on a commercial entity and the financial acquisition is as been able to qualify for the

purpose of creditable acquisitions which has been made partially or fully (Coleman and Sadiq

2013) .

As a significant issue with respect to “para 11-5 and 15-5” of the GST rulings as per

“GSTR 2006/3” has been able to qualify for the creditable acquisition. On the contrary, on

assessing the acquisition which is partly eligible for creditable purpose, the degree of

creditable purpose needs to be ascertained.

“GST Act 1999”, or it needs to get the registration, can be stated that such an concern needs

to make payment of GST with the amount of financial supplies available.

The total GST rulings as per “GSTR 2006/3” has been able to state that the various

types of commercial entities are able to claim for the input tax credit associated to supplies of

financial assistance including the GST amount. On the contrary, in case the commercial

entities goes beyond the financial acquisition limit then in such a case the taxable entity will

not be permitted to claim for the full amount of input tax credit. However, it will be eligible

for claiming of only a portion of the same.

As per the case denoted under the ruling of “Ronpibon Tin NL v FC of T” the most

significant feature of GST ruling of “GSTR 2006/3” has been determined in terms of

“extent” and “to the extent” for the total GST supplies made. As per this legislation, that is

meant of GST as the based on responsibility and fairness of the commercial entities. As noted

in the “para 11-5 and 15-5” the various types of GST rulings for “GSTR 2006/3” has been

based on a commercial entity and the financial acquisition is as been able to qualify for the

purpose of creditable acquisitions which has been made partially or fully (Coleman and Sadiq

2013) .

As a significant issue with respect to “para 11-5 and 15-5” of the GST rulings as per

“GSTR 2006/3” has been able to qualify for the creditable acquisition. On the contrary, on

assessing the acquisition which is partly eligible for creditable purpose, the degree of

creditable purpose needs to be ascertained.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

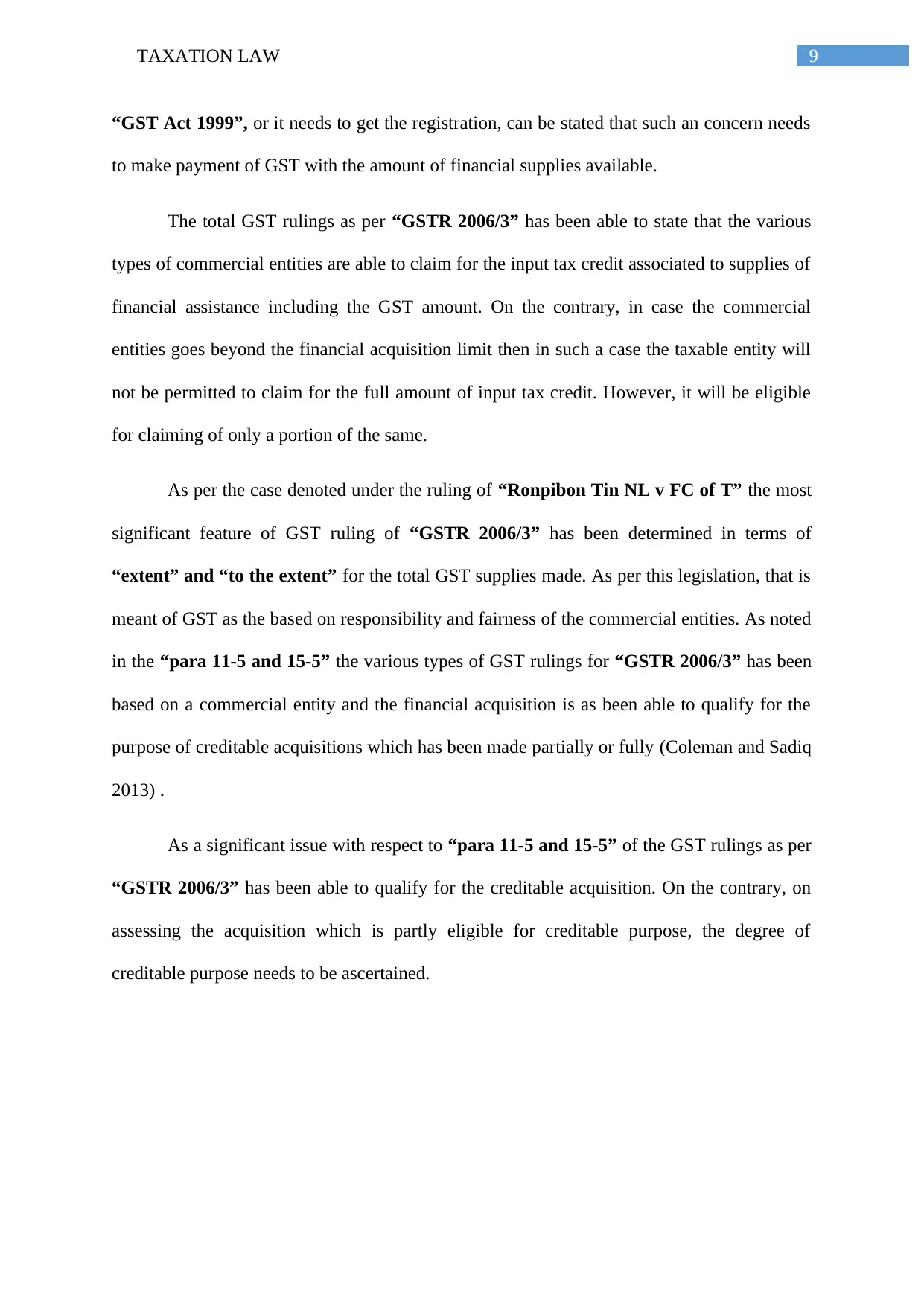

It has been further discern that as per “Section 11-5 and 15-10”, the appropriate GST

legislation of “GSTR 2006/3” will be levied on the various types of financial supplies which

has been made in the commercial entity inclusive of the sum of input tax and the tax which is

to be claimed (Cassidy 2017). It has been further evident with Big Bank Ltd that the financial

supplies are associated to the various types of creditable supplies. By consideration of the

present indications with Big Bank Ltd the GST ruling of “GSTR 2006/3” has exceeded its

limit of the financial acquisition and henceforth the concern needs to bring forward the input

claim for tax credit on the sum of GST supplies (Cao et al. 2015).

Conclusion:

Based on the aforementioned discussions it can be inferred that “GSTR 2006/3” is

mainly applicable for Big Bank Ltd as it has been able to qualify for the input tax credit based

on advertising expenditure.

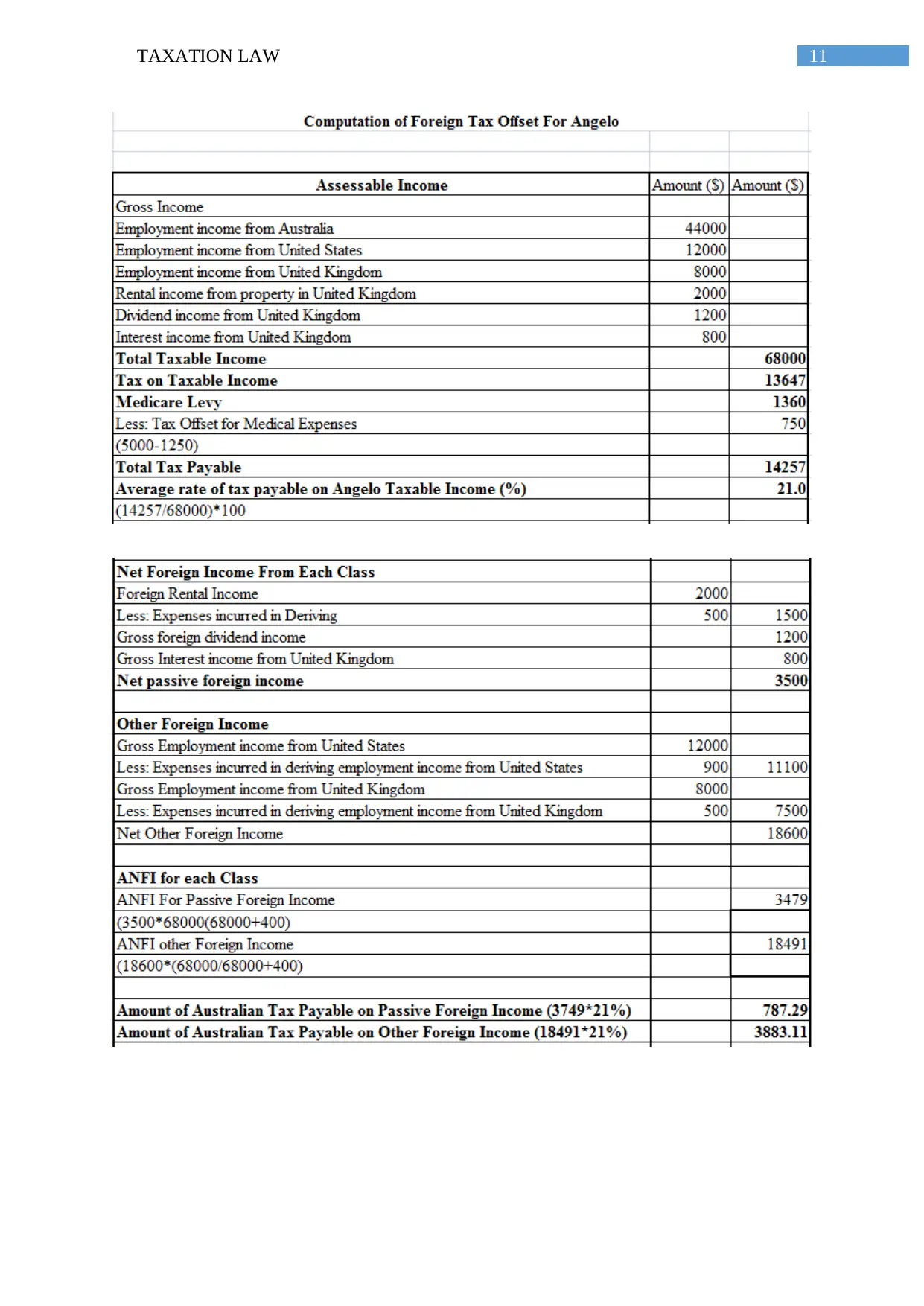

Answer to question 3:

Computation of Taxable Income of Angelo

It has been further discern that as per “Section 11-5 and 15-10”, the appropriate GST

legislation of “GSTR 2006/3” will be levied on the various types of financial supplies which

has been made in the commercial entity inclusive of the sum of input tax and the tax which is

to be claimed (Cassidy 2017). It has been further evident with Big Bank Ltd that the financial

supplies are associated to the various types of creditable supplies. By consideration of the

present indications with Big Bank Ltd the GST ruling of “GSTR 2006/3” has exceeded its

limit of the financial acquisition and henceforth the concern needs to bring forward the input

claim for tax credit on the sum of GST supplies (Cao et al. 2015).

Conclusion:

Based on the aforementioned discussions it can be inferred that “GSTR 2006/3” is

mainly applicable for Big Bank Ltd as it has been able to qualify for the input tax credit based

on advertising expenditure.

Answer to question 3:

Computation of Taxable Income of Angelo

11TAXATION LAW

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.