FNSACC512/FNSACC601: Tax Documentation Preparation and Administration

VerifiedAdded on 2023/06/18

|16

|2669

|298

Homework Assignment

AI Summary

This document provides a comprehensive solution to an assignment covering FNSACC512 and FNSACC601 units, focusing on preparing tax documentation for individuals and legal entities. It addresses various tasks including identifying tax avoidance schemes, understanding organizational policies and procedures related to tax, calculating superannuation contributions and related tax implications, determining partnership income and its allocation, managing tax administration and penalties, handling foreign source income for entities, dealing with trust income and tax obligations, and performing company reconciliations and franking account management. The solutions include detailed calculations and explanations for each task, providing a clear understanding of the concepts and practical application of tax principles.

FNSACC512 Prepare tax

documentation for individuals

FNSACC601 Prepare and administer tax

documentation for legal entities

Assessment 13

LA023800

Assessment Template

documentation for individuals

FNSACC601 Prepare and administer tax

documentation for legal entities

Assessment 13

LA023800

Assessment Template

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

What you have to do

This assessment consists of 9 tasks. Students are required to complete every question in each task in the

assessment. To achieve a satisfactory result in these topics they must achieve the following results for

each task:

Task Topics Satisfactory/Not

satisfactory

1 Tax Avoidance

2 Organisational policies and procedures

3 Superannuation contributions

4 Partnerships

5 Administration of tax

6 Foreign source income

7 Trusts

8 Company Reconciliations

9 Company Franking Accounts

Result Assessment result: Satisfactory (S) / Unsatisfactory (U) -

Note: The number of rows and columns in the tables are indicative only. Students are allowed to add

rows and columns according to their answers.

Task 1 – Tax avoidance

(a) Discuss whether Robert’s tax planning arrangement is a tax avoidance scheme or not.

This assessment consists of 9 tasks. Students are required to complete every question in each task in the

assessment. To achieve a satisfactory result in these topics they must achieve the following results for

each task:

Task Topics Satisfactory/Not

satisfactory

1 Tax Avoidance

2 Organisational policies and procedures

3 Superannuation contributions

4 Partnerships

5 Administration of tax

6 Foreign source income

7 Trusts

8 Company Reconciliations

9 Company Franking Accounts

Result Assessment result: Satisfactory (S) / Unsatisfactory (U) -

Note: The number of rows and columns in the tables are indicative only. Students are allowed to add

rows and columns according to their answers.

Task 1 – Tax avoidance

(a) Discuss whether Robert’s tax planning arrangement is a tax avoidance scheme or not.

Tax avoidance is an act of minimising tax liability by adopting legal methods. Although it is legal

method but not advisable because it is an activity of taking unfair advantage of loops which are

present in tax laws. It can be done by finding a different way to avoid the tax payment (within the limit

of law). Robert is implementing tax planning in such a way (within the boundaries of law) that will help

to reduce tax liability of David. As it come under the tax avoidance scheme which is also known as tax

exploitation. Tax avoidance is to be done by adjusting the accounts in such a manner where there is no

violation of tax law. Moreover, on the other hand by reducing the tax liability with the help of tax

avoidance, it is required to pay penalties (as per the law).

(b) Explain Robert how promoter penalty laws operate and the maximum penalties that the Federal Court

can impose on him.

_____Promoter penalties laws is to be made in order to determine the tax avoidance schemes. All those

advisers who take part in design, implementing and marketing of schemes which claim to provide

taxation benefits are to be considered under this law. The main element of this law is to monitor and

control an entity not to engage in prohibited conduct. Moreover, prohibited conduct is an act that

result in entity being (work as a) promoter of tax exploitation or avoidance scheme. The promoter

penalty laws is not formed to obstruct intermediaries and tax advisers in order to give useful advice to

their client. If any entity is caught by being a promoter of tax avoidance scheme then the legislation

enables in order to request the Federal court of Australia for imposing civil penalties. Maximum

penalty which can be imposed by Federal court is 5000 penalty unites for individuals whereas one unit

is equal to $222. Moreover, 25000 penalty units will be lea-vied for body corporate. A scheme can be

said tax avoidance or exploitation of tax, If at the stand point of promotion, has a dominant or sole

purpose of an entity to gain a scheme benefit which is not legally available. So as here, court will

charge 5000 penalty unites from Devid.

Task 2 – Organisational policies and procedures

(a) Decision making processes

method but not advisable because it is an activity of taking unfair advantage of loops which are

present in tax laws. It can be done by finding a different way to avoid the tax payment (within the limit

of law). Robert is implementing tax planning in such a way (within the boundaries of law) that will help

to reduce tax liability of David. As it come under the tax avoidance scheme which is also known as tax

exploitation. Tax avoidance is to be done by adjusting the accounts in such a manner where there is no

violation of tax law. Moreover, on the other hand by reducing the tax liability with the help of tax

avoidance, it is required to pay penalties (as per the law).

(b) Explain Robert how promoter penalty laws operate and the maximum penalties that the Federal Court

can impose on him.

_____Promoter penalties laws is to be made in order to determine the tax avoidance schemes. All those

advisers who take part in design, implementing and marketing of schemes which claim to provide

taxation benefits are to be considered under this law. The main element of this law is to monitor and

control an entity not to engage in prohibited conduct. Moreover, prohibited conduct is an act that

result in entity being (work as a) promoter of tax exploitation or avoidance scheme. The promoter

penalty laws is not formed to obstruct intermediaries and tax advisers in order to give useful advice to

their client. If any entity is caught by being a promoter of tax avoidance scheme then the legislation

enables in order to request the Federal court of Australia for imposing civil penalties. Maximum

penalty which can be imposed by Federal court is 5000 penalty unites for individuals whereas one unit

is equal to $222. Moreover, 25000 penalty units will be lea-vied for body corporate. A scheme can be

said tax avoidance or exploitation of tax, If at the stand point of promotion, has a dominant or sole

purpose of an entity to gain a scheme benefit which is not legally available. So as here, court will

charge 5000 penalty unites from Devid.

Task 2 – Organisational policies and procedures

(a) Decision making processes

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The decision making in respect to the good corporate governance practice will be__________

taken based on the need and situation. The aim of the decision making is to maximise the growth of

the business in respective target market. The________________________________________

organisation has planned to adopt a good corporate governance practice ________________

that can favour the business venture to approach all its various business__________________

objectives. The decision making process is for changing the structure is __________________

also involved all the key stakeholders associated with venture.

____________________________________________________________________________

(b) Getting proper advice

The decision of the Antonio is to convert the business into the company is ________________

very effective. This is to advice the organisation to get conversion into the________________

company business so that overall objective of operations can meet. In context_____________

to any business house this become important to convert the business type once___________

the scale of business become broad. The conversion of the business into the______________

company will facilitate the organisation to easily approach the funding.

____________________________________________________________________________

(c) Record keeping and documentation

The records and documentation related to every transaction need to be done _____________

by company. In context to the company this is a mandatory requirement that_____________

business house record every single business transaction. Record keeping is________________

happen with support of bill book and also over the financial statement such_______________

taken based on the need and situation. The aim of the decision making is to maximise the growth of

the business in respective target market. The________________________________________

organisation has planned to adopt a good corporate governance practice ________________

that can favour the business venture to approach all its various business__________________

objectives. The decision making process is for changing the structure is __________________

also involved all the key stakeholders associated with venture.

____________________________________________________________________________

(b) Getting proper advice

The decision of the Antonio is to convert the business into the company is ________________

very effective. This is to advice the organisation to get conversion into the________________

company business so that overall objective of operations can meet. In context_____________

to any business house this become important to convert the business type once___________

the scale of business become broad. The conversion of the business into the______________

company will facilitate the organisation to easily approach the funding.

____________________________________________________________________________

(c) Record keeping and documentation

The records and documentation related to every transaction need to be done _____________

by company. In context to the company this is a mandatory requirement that_____________

business house record every single business transaction. Record keeping is________________

happen with support of bill book and also over the financial statement such_______________

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

as trading account, profit and loss, balance sheet and also in cash flow statement__________

maintain by company. Record keeping and documentation is mandatory for_______________

the company and its business operations.

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

maintain by company. Record keeping and documentation is mandatory for_______________

the company and its business operations.

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

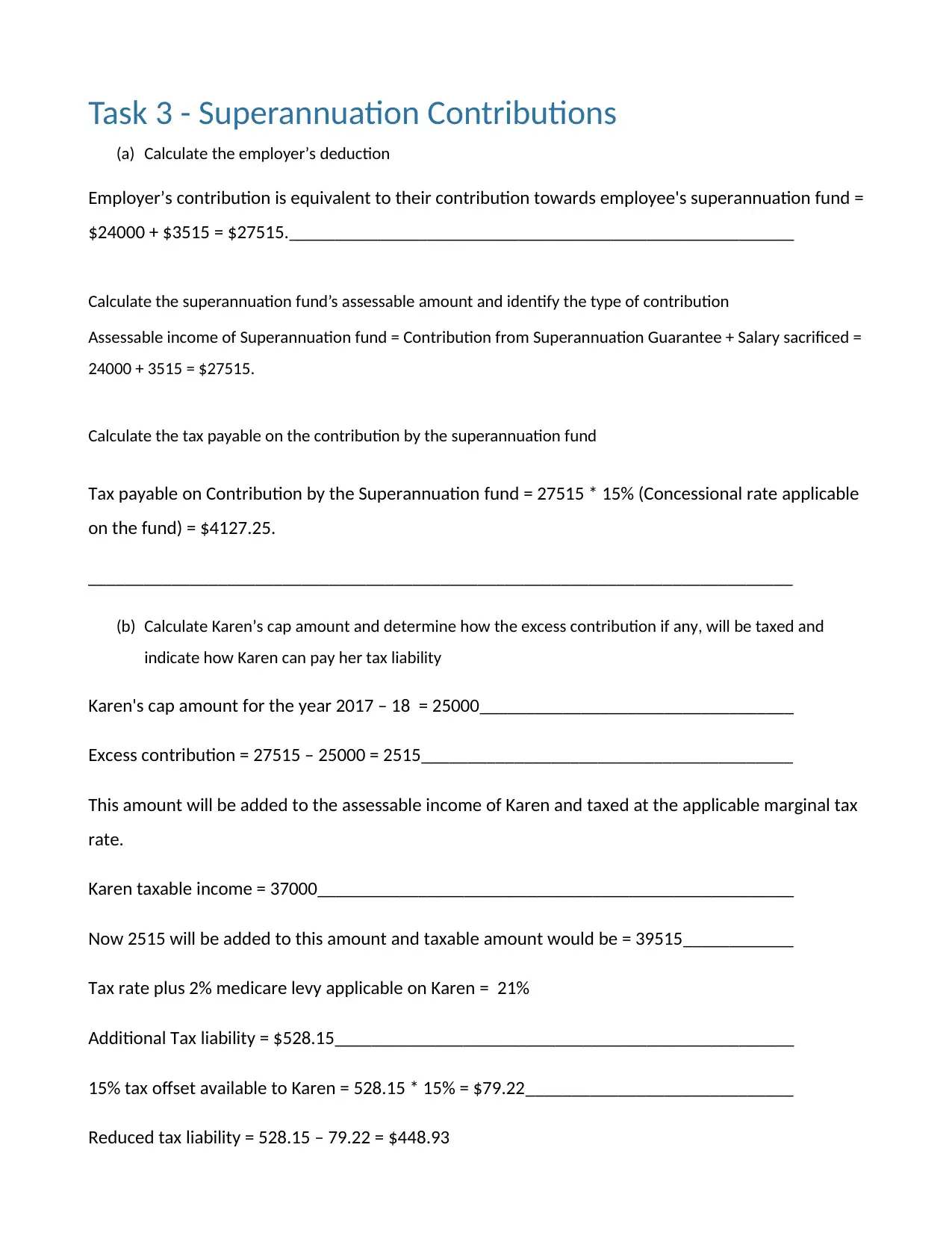

Task 3 - Superannuation Contributions

(a) Calculate the employer’s deduction

Employer’s contribution is equivalent to their contribution towards employee's superannuation fund =

$24000 + $3515 = $27515._______________________________________________________

Calculate the superannuation fund’s assessable amount and identify the type of contribution

Assessable income of Superannuation fund = Contribution from Superannuation Guarantee + Salary sacrificed =

24000 + 3515 = $27515.

Calculate the tax payable on the contribution by the superannuation fund

Tax payable on Contribution by the Superannuation fund = 27515 * 15% (Concessional rate applicable

on the fund) = $4127.25.

____________________________________________________________________________

(b) Calculate Karen’s cap amount and determine how the excess contribution if any, will be taxed and

indicate how Karen can pay her tax liability

Karen's cap amount for the year 2017 – 18 = 25000__________________________________

Excess contribution = 27515 – 25000 = 2515________________________________________

This amount will be added to the assessable income of Karen and taxed at the applicable marginal tax

rate.

Karen taxable income = 37000____________________________________________________

Now 2515 will be added to this amount and taxable amount would be = 39515____________

Tax rate plus 2% medicare levy applicable on Karen = 21%

Additional Tax liability = $528.15__________________________________________________

15% tax offset available to Karen = 528.15 * 15% = $79.22_____________________________

Reduced tax liability = 528.15 – 79.22 = $448.93

(a) Calculate the employer’s deduction

Employer’s contribution is equivalent to their contribution towards employee's superannuation fund =

$24000 + $3515 = $27515._______________________________________________________

Calculate the superannuation fund’s assessable amount and identify the type of contribution

Assessable income of Superannuation fund = Contribution from Superannuation Guarantee + Salary sacrificed =

24000 + 3515 = $27515.

Calculate the tax payable on the contribution by the superannuation fund

Tax payable on Contribution by the Superannuation fund = 27515 * 15% (Concessional rate applicable

on the fund) = $4127.25.

____________________________________________________________________________

(b) Calculate Karen’s cap amount and determine how the excess contribution if any, will be taxed and

indicate how Karen can pay her tax liability

Karen's cap amount for the year 2017 – 18 = 25000__________________________________

Excess contribution = 27515 – 25000 = 2515________________________________________

This amount will be added to the assessable income of Karen and taxed at the applicable marginal tax

rate.

Karen taxable income = 37000____________________________________________________

Now 2515 will be added to this amount and taxable amount would be = 39515____________

Tax rate plus 2% medicare levy applicable on Karen = 21%

Additional Tax liability = $528.15__________________________________________________

15% tax offset available to Karen = 528.15 * 15% = $79.22_____________________________

Reduced tax liability = 528.15 – 79.22 = $448.93

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

____________________________________________________________________________

(c) Explain if Karen’s eligible income for any of the tax offsets available in the superannuation system

Yes, Karen is eligible for the tax offset @ 15% of the additional tax liability that has been arises on the

ground of excess concessional contribution towards the complying superannuation fund. This tax

offset results in the reduction of the additional tax liability of Karen.

____________________________________________________________________________

(c) Explain if Karen’s eligible income for any of the tax offsets available in the superannuation system

Yes, Karen is eligible for the tax offset @ 15% of the additional tax liability that has been arises on the

ground of excess concessional contribution towards the complying superannuation fund. This tax

offset results in the reduction of the additional tax liability of Karen.

____________________________________________________________________________

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

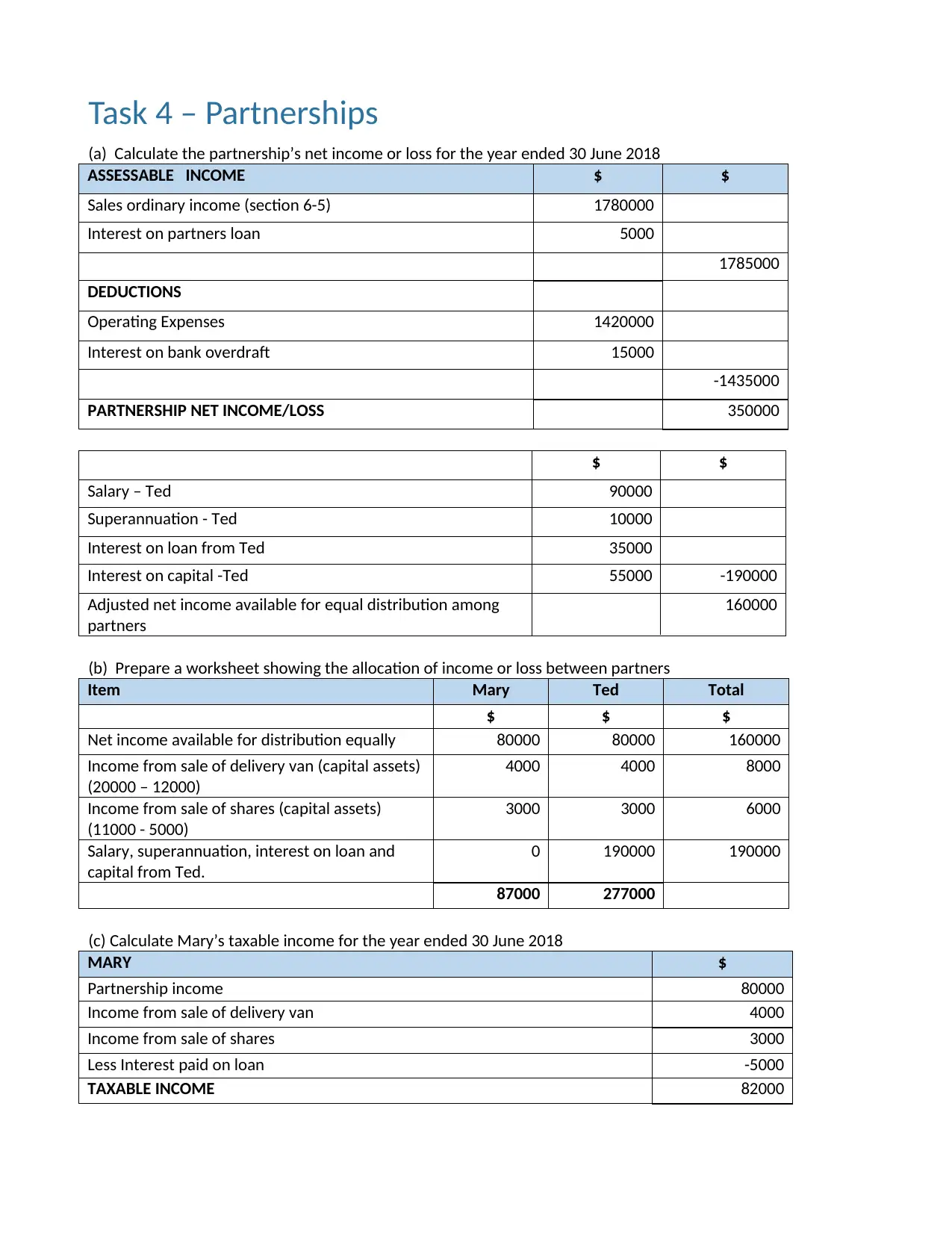

Task 4 – Partnerships

(a) Calculate the partnership’s net income or loss for the year ended 30 June 2018

ASSESSABLE INCOME $ $

Sales ordinary income (section 6-5) 1780000

Interest on partners loan 5000

1785000

DEDUCTIONS

Operating Expenses 1420000

Interest on bank overdraft 15000

-1435000

PARTNERSHIP NET INCOME/LOSS 350000

$ $

Salary – Ted 90000

Superannuation - Ted 10000

Interest on loan from Ted 35000

Interest on capital -Ted 55000 -190000

Adjusted net income available for equal distribution among

partners

160000

(b) Prepare a worksheet showing the allocation of income or loss between partners

Item Mary Ted Total

$ $ $

Net income available for distribution equally 80000 80000 160000

Income from sale of delivery van (capital assets)

(20000 – 12000)

4000 4000 8000

Income from sale of shares (capital assets)

(11000 - 5000)

3000 3000 6000

Salary, superannuation, interest on loan and

capital from Ted.

0 190000 190000

87000 277000

(c) Calculate Mary’s taxable income for the year ended 30 June 2018

MARY $

Partnership income 80000

Income from sale of delivery van 4000

Income from sale of shares 3000

Less Interest paid on loan -5000

TAXABLE INCOME 82000

(a) Calculate the partnership’s net income or loss for the year ended 30 June 2018

ASSESSABLE INCOME $ $

Sales ordinary income (section 6-5) 1780000

Interest on partners loan 5000

1785000

DEDUCTIONS

Operating Expenses 1420000

Interest on bank overdraft 15000

-1435000

PARTNERSHIP NET INCOME/LOSS 350000

$ $

Salary – Ted 90000

Superannuation - Ted 10000

Interest on loan from Ted 35000

Interest on capital -Ted 55000 -190000

Adjusted net income available for equal distribution among

partners

160000

(b) Prepare a worksheet showing the allocation of income or loss between partners

Item Mary Ted Total

$ $ $

Net income available for distribution equally 80000 80000 160000

Income from sale of delivery van (capital assets)

(20000 – 12000)

4000 4000 8000

Income from sale of shares (capital assets)

(11000 - 5000)

3000 3000 6000

Salary, superannuation, interest on loan and

capital from Ted.

0 190000 190000

87000 277000

(c) Calculate Mary’s taxable income for the year ended 30 June 2018

MARY $

Partnership income 80000

Income from sale of delivery van 4000

Income from sale of shares 3000

Less Interest paid on loan -5000

TAXABLE INCOME 82000

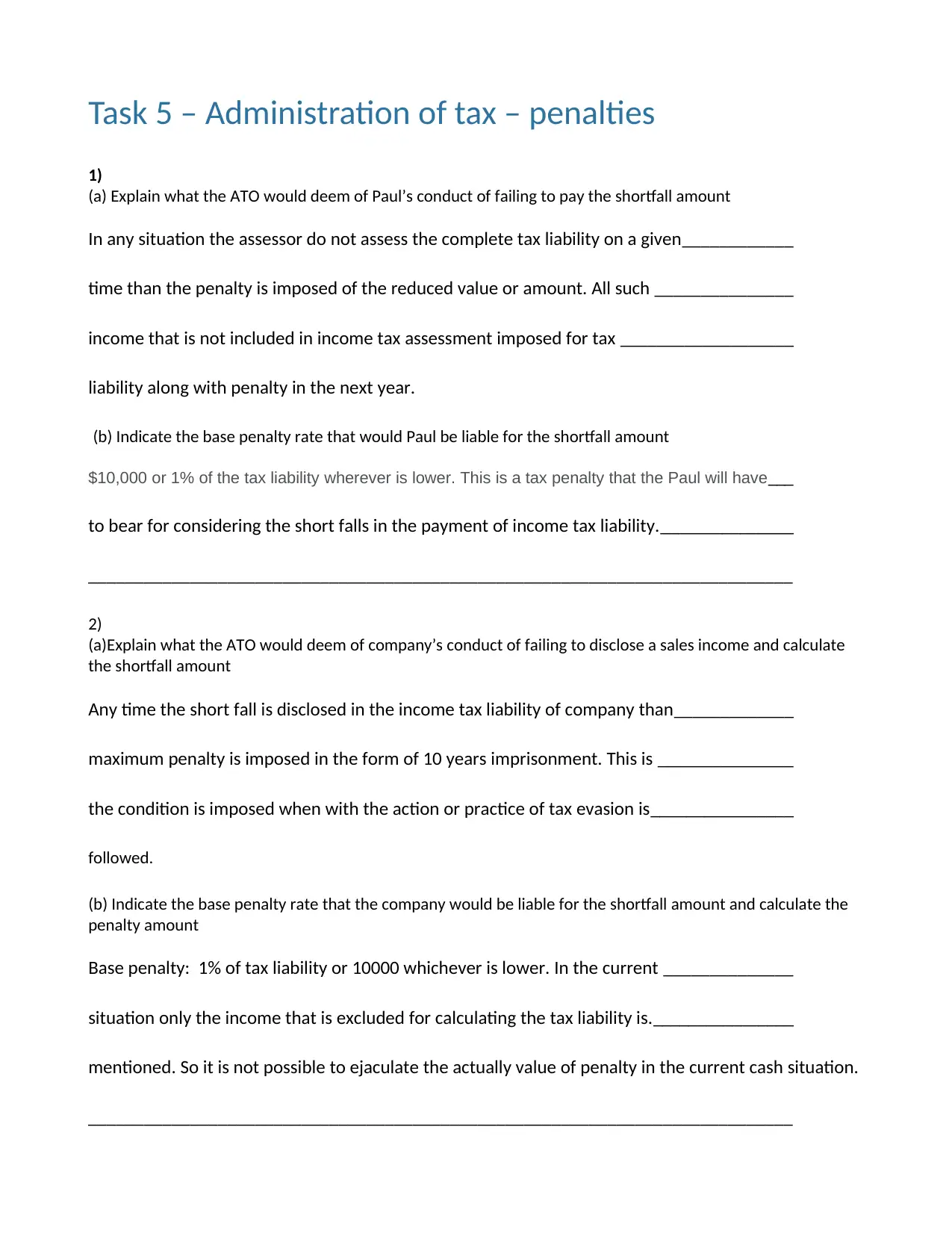

Task 5 – Administration of tax – penalties

1)

(a) Explain what the ATO would deem of Paul’s conduct of failing to pay the shortfall amount

In any situation the assessor do not assess the complete tax liability on a given____________

time than the penalty is imposed of the reduced value or amount. All such _______________

income that is not included in income tax assessment imposed for tax ___________________

liability along with penalty in the next year.

(b) Indicate the base penalty rate that would Paul be liable for the shortfall amount

$10,000 or 1% of the tax liability wherever is lower. This is a tax penalty that the Paul will have___

to bear for considering the short falls in the payment of income tax liability._______________

____________________________________________________________________________

2)

(a)Explain what the ATO would deem of company’s conduct of failing to disclose a sales income and calculate

the shortfall amount

Any time the short fall is disclosed in the income tax liability of company than_____________

maximum penalty is imposed in the form of 10 years imprisonment. This is _______________

the condition is imposed when with the action or practice of tax evasion is________________

followed.

(b) Indicate the base penalty rate that the company would be liable for the shortfall amount and calculate the

penalty amount

Base penalty: 1% of tax liability or 10000 whichever is lower. In the current ______________

situation only the income that is excluded for calculating the tax liability is.________________

mentioned. So it is not possible to ejaculate the actually value of penalty in the current cash situation.

____________________________________________________________________________

1)

(a) Explain what the ATO would deem of Paul’s conduct of failing to pay the shortfall amount

In any situation the assessor do not assess the complete tax liability on a given____________

time than the penalty is imposed of the reduced value or amount. All such _______________

income that is not included in income tax assessment imposed for tax ___________________

liability along with penalty in the next year.

(b) Indicate the base penalty rate that would Paul be liable for the shortfall amount

$10,000 or 1% of the tax liability wherever is lower. This is a tax penalty that the Paul will have___

to bear for considering the short falls in the payment of income tax liability._______________

____________________________________________________________________________

2)

(a)Explain what the ATO would deem of company’s conduct of failing to disclose a sales income and calculate

the shortfall amount

Any time the short fall is disclosed in the income tax liability of company than_____________

maximum penalty is imposed in the form of 10 years imprisonment. This is _______________

the condition is imposed when with the action or practice of tax evasion is________________

followed.

(b) Indicate the base penalty rate that the company would be liable for the shortfall amount and calculate the

penalty amount

Base penalty: 1% of tax liability or 10000 whichever is lower. In the current ______________

situation only the income that is excluded for calculating the tax liability is.________________

mentioned. So it is not possible to ejaculate the actually value of penalty in the current cash situation.

____________________________________________________________________________

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

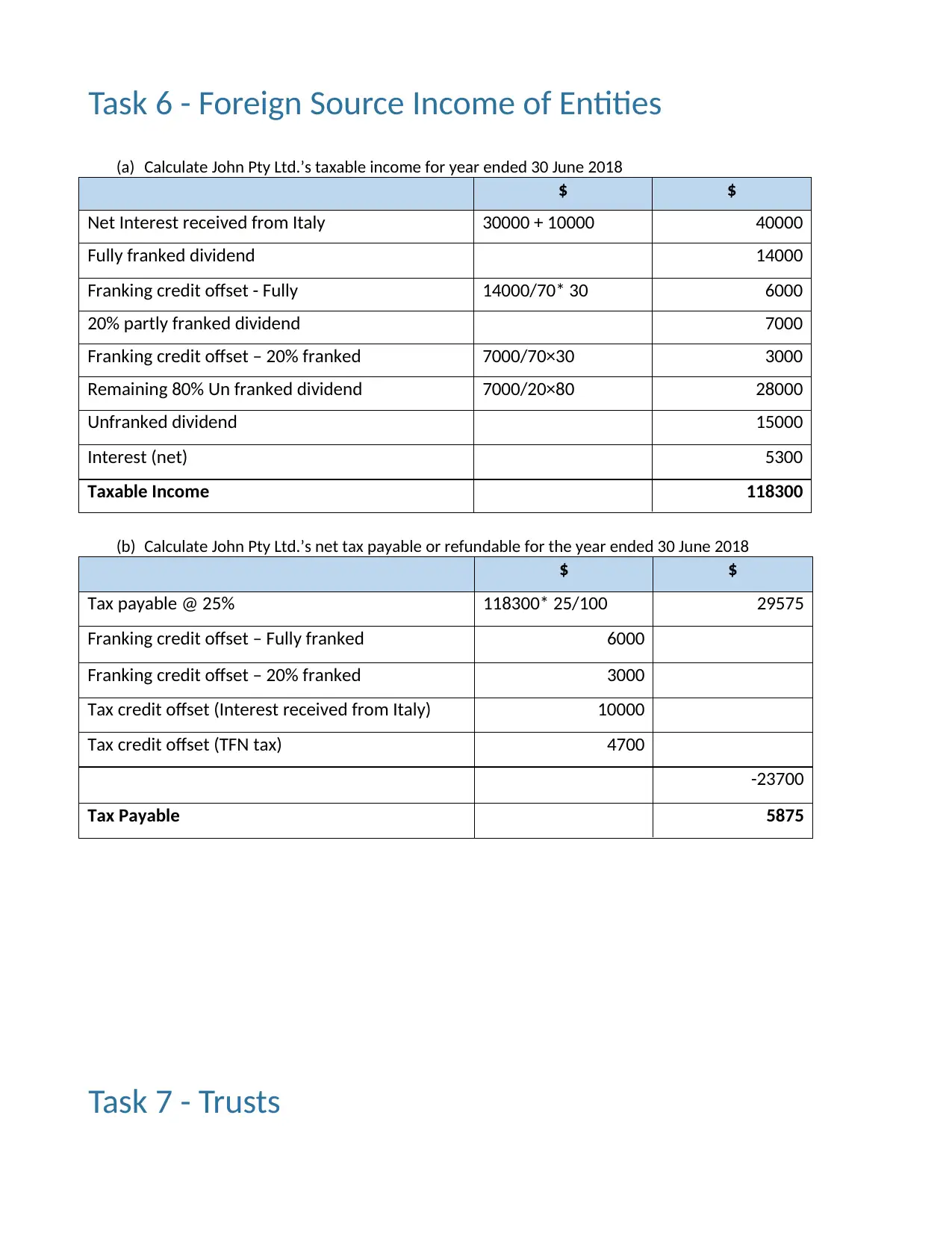

Task 6 - Foreign Source Income of Entities

(a) Calculate John Pty Ltd.’s taxable income for year ended 30 June 2018

$ $

Net Interest received from Italy 30000 + 10000 40000

Fully franked dividend 14000

Franking credit offset - Fully 14000/70* 30 6000

20% partly franked dividend 7000

Franking credit offset – 20% franked 7000/70×30 3000

Remaining 80% Un franked dividend 7000/20×80 28000

Unfranked dividend 15000

Interest (net) 5300

Taxable Income 118300

(b) Calculate John Pty Ltd.’s net tax payable or refundable for the year ended 30 June 2018

$ $

Tax payable @ 25% 118300* 25/100 29575

Franking credit offset – Fully franked 6000

Franking credit offset – 20% franked 3000

Tax credit offset (Interest received from Italy) 10000

Tax credit offset (TFN tax) 4700

-23700

Tax Payable 5875

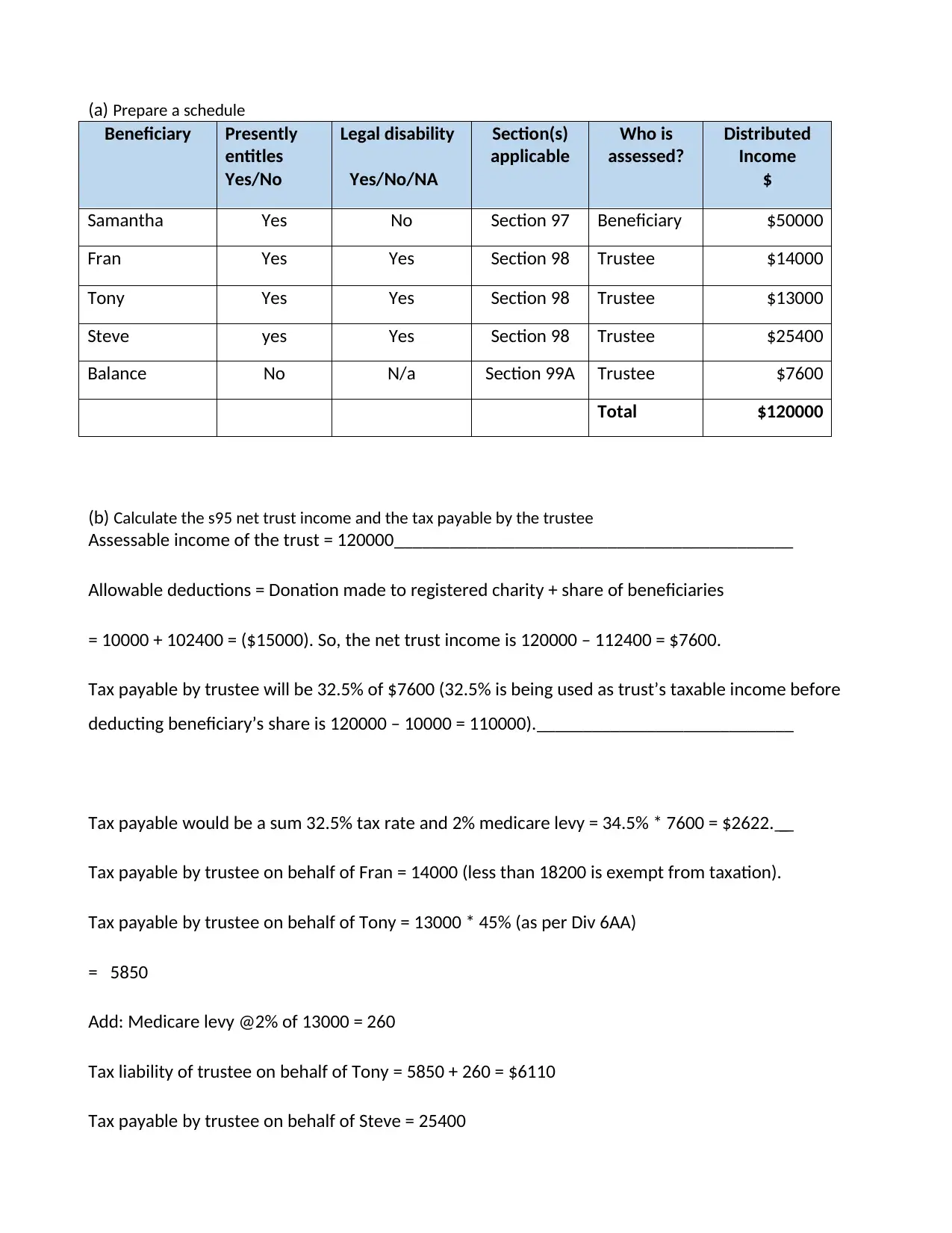

Task 7 - Trusts

(a) Calculate John Pty Ltd.’s taxable income for year ended 30 June 2018

$ $

Net Interest received from Italy 30000 + 10000 40000

Fully franked dividend 14000

Franking credit offset - Fully 14000/70* 30 6000

20% partly franked dividend 7000

Franking credit offset – 20% franked 7000/70×30 3000

Remaining 80% Un franked dividend 7000/20×80 28000

Unfranked dividend 15000

Interest (net) 5300

Taxable Income 118300

(b) Calculate John Pty Ltd.’s net tax payable or refundable for the year ended 30 June 2018

$ $

Tax payable @ 25% 118300* 25/100 29575

Franking credit offset – Fully franked 6000

Franking credit offset – 20% franked 3000

Tax credit offset (Interest received from Italy) 10000

Tax credit offset (TFN tax) 4700

-23700

Tax Payable 5875

Task 7 - Trusts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(a) Prepare a schedule

Beneficiary Presently

entitles

Yes/No

Legal disability

Yes/No/NA

Section(s)

applicable

Who is

assessed?

Distributed

Income

$

Samantha Yes No Section 97 Beneficiary $50000

Fran Yes Yes Section 98 Trustee $14000

Tony Yes Yes Section 98 Trustee $13000

Steve yes Yes Section 98 Trustee $25400

Balance No N/a Section 99A Trustee $7600

Total $120000

(b) Calculate the s95 net trust income and the tax payable by the trustee

Assessable income of the trust = 120000___________________________________________

Allowable deductions = Donation made to registered charity + share of beneficiaries

= 10000 + 102400 = ($15000). So, the net trust income is 120000 – 112400 = $7600.

Tax payable by trustee will be 32.5% of $7600 (32.5% is being used as trust’s taxable income before

deducting beneficiary’s share is 120000 – 10000 = 110000).____________________________

Tax payable would be a sum 32.5% tax rate and 2% medicare levy = 34.5% * 7600 = $2622.___

Tax payable by trustee on behalf of Fran = 14000 (less than 18200 is exempt from taxation).

Tax payable by trustee on behalf of Tony = 13000 * 45% (as per Div 6AA)

= 5850

Add: Medicare levy @2% of 13000 = 260

Tax liability of trustee on behalf of Tony = 5850 + 260 = $6110

Tax payable by trustee on behalf of Steve = 25400

Beneficiary Presently

entitles

Yes/No

Legal disability

Yes/No/NA

Section(s)

applicable

Who is

assessed?

Distributed

Income

$

Samantha Yes No Section 97 Beneficiary $50000

Fran Yes Yes Section 98 Trustee $14000

Tony Yes Yes Section 98 Trustee $13000

Steve yes Yes Section 98 Trustee $25400

Balance No N/a Section 99A Trustee $7600

Total $120000

(b) Calculate the s95 net trust income and the tax payable by the trustee

Assessable income of the trust = 120000___________________________________________

Allowable deductions = Donation made to registered charity + share of beneficiaries

= 10000 + 102400 = ($15000). So, the net trust income is 120000 – 112400 = $7600.

Tax payable by trustee will be 32.5% of $7600 (32.5% is being used as trust’s taxable income before

deducting beneficiary’s share is 120000 – 10000 = 110000).____________________________

Tax payable would be a sum 32.5% tax rate and 2% medicare levy = 34.5% * 7600 = $2622.___

Tax payable by trustee on behalf of Fran = 14000 (less than 18200 is exempt from taxation).

Tax payable by trustee on behalf of Tony = 13000 * 45% (as per Div 6AA)

= 5850

Add: Medicare levy @2% of 13000 = 260

Tax liability of trustee on behalf of Tony = 5850 + 260 = $6110

Tax payable by trustee on behalf of Steve = 25400

25400 * 45% = 11430___________________________________________________________

Add: medicare levy @2% of 25400 = 508

Tax liability of trustee on behalf of Steve = 11430 + 508 = $11938.

(c) Calculate the tax payable by Tony and Steve

Tax payable by Tony____________________________________________________________

Gross wages received = 30000____________________________________________________

Received from inter vivos trust = 4000_____________________________________________

Share of trust income = 13000____________________________________________________

Assessable income = 30000 + 4000 + 13000 = 47000__________________________________

Tax liability on 47000 = 3572 + 32.5% of (47000 - 37000)_______________________________

Tax payable= 3572 + 3250 = $6822

Add: Medicare levy = 2% of 47000 = $940

Tax liability = 6822 + 940 = $7762

Net tax liability of Tony = 7762 – 4500 (PAYG tax withheld) = $3262

Tax payable by Steve

5000 + 25400 = 30400

first 18200 exempt

Next (30400 – 18200) = $12200 * 19% = 2318.

Add: Medicare levy @2% of 12200 = 244

total tax payable by Steve = 2318 + 244 = $2562.

____________________________________________________________________________

Add: medicare levy @2% of 25400 = 508

Tax liability of trustee on behalf of Steve = 11430 + 508 = $11938.

(c) Calculate the tax payable by Tony and Steve

Tax payable by Tony____________________________________________________________

Gross wages received = 30000____________________________________________________

Received from inter vivos trust = 4000_____________________________________________

Share of trust income = 13000____________________________________________________

Assessable income = 30000 + 4000 + 13000 = 47000__________________________________

Tax liability on 47000 = 3572 + 32.5% of (47000 - 37000)_______________________________

Tax payable= 3572 + 3250 = $6822

Add: Medicare levy = 2% of 47000 = $940

Tax liability = 6822 + 940 = $7762

Net tax liability of Tony = 7762 – 4500 (PAYG tax withheld) = $3262

Tax payable by Steve

5000 + 25400 = 30400

first 18200 exempt

Next (30400 – 18200) = $12200 * 19% = 2318.

Add: Medicare levy @2% of 12200 = 244

total tax payable by Steve = 2318 + 244 = $2562.

____________________________________________________________________________

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.