Taxation Law Assignment: Income Tax, CGT, and Fringe Benefits

VerifiedAdded on 2021/05/31

|8

|1915

|44

Homework Assignment

AI Summary

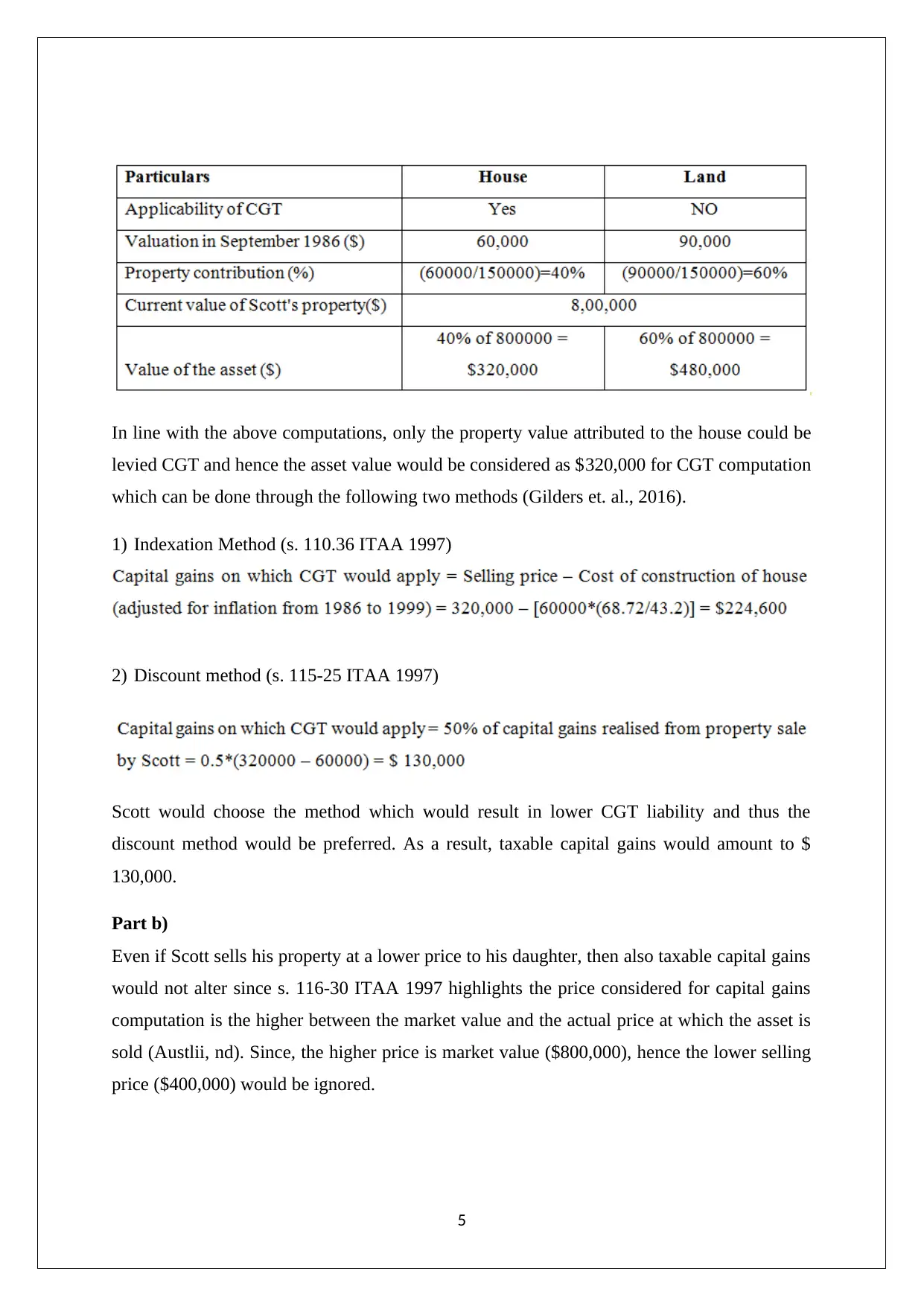

This taxation law assignment addresses several key issues, including whether payments received by Hilary are taxable income from personal exertion, the calculation of car fringe benefits, the tax implications of a loan and interest, and the application of capital gains tax (CGT). The solution analyzes these scenarios based on relevant sections of the ITAA 1997 and the Fringe Benefits Tax Assessment Act 1986, as well as case law such as Brent v. Federal Commissioner of Taxation. The assignment explores the distinction between capital receipts and income, the determination of taxable values for fringe benefits, and the tax treatment of loans and gifts. Furthermore, it covers CGT calculations, including the application of the indexation and discount methods, considering different scenarios such as the sale of property at market value and the implications of selling to a related party. The assignment provides detailed analysis and calculations, supported by references to relevant legislation and case law.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.