Taxation Analysis: Residency, Tax Calculation, and Fringe Benefits

VerifiedAdded on 2020/04/29

|12

|2612

|87

Homework Assignment

AI Summary

This taxation assignment addresses two main questions. The first question focuses on determining Daniel's residency status for the 2016/2017 tax year based on domicile, 183-day, and superannuation tests, subsequently calculating his tax payable using his income details, including salary, superannuation, interest, rental income, bonuses, and dividends. The second question analyzes various transactions involving Joyce, a marketing manager, to determine fringe benefit tax (FBT) or income tax implications. The analysis covers salary, superannuation, school fees, travel costs, professional memberships, car benefits, gym memberships, and loan and debt waiver benefits, calculating the FBT liability for the year, with detailed working notes on car fringe benefits, loan fringe benefits, debt waivers, and travel and professional membership expenses. The assignment highlights the difference between income tax and FBT obligations, providing a comprehensive overview of Australian taxation principles.

TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1.............................................................................................................................1

1) Determine the residency status of Daniel for tax purpose for 2016/2017..........................1

2) Calculate the tax payable by Daniel for 2016-17...............................................................2

QUESTION 2.............................................................................................................................3

1) Analyze the transactions in determining whether there any FBT or income tax

implications............................................................................................................................3

2) Calculate FBT liability for the year...................................................................................5

REFERENCES...........................................................................................................................9

QUESTION 1.............................................................................................................................1

1) Determine the residency status of Daniel for tax purpose for 2016/2017..........................1

2) Calculate the tax payable by Daniel for 2016-17...............................................................2

QUESTION 2.............................................................................................................................3

1) Analyze the transactions in determining whether there any FBT or income tax

implications............................................................................................................................3

2) Calculate FBT liability for the year...................................................................................5

REFERENCES...........................................................................................................................9

QUESTION 1

1) Determine the residency status of Daniel for tax purpose for 2016/2017

Residency status plays a significant role in determining the residency status of an

individual while assessing the tax liabilities incurred on an individual in a particular year.

There are three residency tests required to pass by a person to get the status of resident or

non-resident for taxation purpose in evaluating the tax liabilities in the Australia.1 Income

earned by Daniel in the current case is assessed on the basis of determined residency status of

him as different tax slabs are there for resident individual and non-resident individual in the

Australia.

Domicile tests- It is one of the tests used by the Australian taxation officer to assess

the tax obligation incurred on a person.2 This states that a person is an Australian

resident if they permanently reside in the Australia unless the permanent place of the

person is outside the Australia.

183 days tests- Another tests used to determine the residency status of a person for

analyzing the tax liabilities of an individual. This test helps in determining the

residency status of a person.3 If a person stays in the current country for 183 days or

half of the income year that is 6 months spent in the Australia is count as one of the

resident of this place. Relaxation has mentioned in the act and its tax determination

principles about the determination of the residency status of a person is that total

period of 183 days spent by a person in a country can be of complete 183 days or in

breaks.4 This checks the presence of a person in a country to provide all the benefit of

a resident of the country as compared o all the people living in this particular country.

Superannuation tests- Superannuation is a retirement fund held by all the employees

who are working in an Australia is an easy way to determine the residency of all the

employees.5 A person having legal superannuation funds account is treated as

Australian resident as they are living in this county for the working purpose in which

they leave their original country to accept the citizenship of the country in which they

are doing job counts under a legal resident individual.

1 Residency tests, 2017. Available through: <

https://www.ato.gov.au/individuals/international-tax-for-individuals/work-out-your-tax-

residency/residency-tests/> [Accessed on 27th October 2017].

2 Robertson, S., 2017.

3 Hedrick, K., 2017.

4 To, H., Grafton, R.Q. and Regan, S., 2017.

5 Walters, R. and Zeller, B., 2017.

1

1) Determine the residency status of Daniel for tax purpose for 2016/2017

Residency status plays a significant role in determining the residency status of an

individual while assessing the tax liabilities incurred on an individual in a particular year.

There are three residency tests required to pass by a person to get the status of resident or

non-resident for taxation purpose in evaluating the tax liabilities in the Australia.1 Income

earned by Daniel in the current case is assessed on the basis of determined residency status of

him as different tax slabs are there for resident individual and non-resident individual in the

Australia.

Domicile tests- It is one of the tests used by the Australian taxation officer to assess

the tax obligation incurred on a person.2 This states that a person is an Australian

resident if they permanently reside in the Australia unless the permanent place of the

person is outside the Australia.

183 days tests- Another tests used to determine the residency status of a person for

analyzing the tax liabilities of an individual. This test helps in determining the

residency status of a person.3 If a person stays in the current country for 183 days or

half of the income year that is 6 months spent in the Australia is count as one of the

resident of this place. Relaxation has mentioned in the act and its tax determination

principles about the determination of the residency status of a person is that total

period of 183 days spent by a person in a country can be of complete 183 days or in

breaks.4 This checks the presence of a person in a country to provide all the benefit of

a resident of the country as compared o all the people living in this particular country.

Superannuation tests- Superannuation is a retirement fund held by all the employees

who are working in an Australia is an easy way to determine the residency of all the

employees.5 A person having legal superannuation funds account is treated as

Australian resident as they are living in this county for the working purpose in which

they leave their original country to accept the citizenship of the country in which they

are doing job counts under a legal resident individual.

1 Residency tests, 2017. Available through: <

https://www.ato.gov.au/individuals/international-tax-for-individuals/work-out-your-tax-

residency/residency-tests/> [Accessed on 27th October 2017].

2 Robertson, S., 2017.

3 Hedrick, K., 2017.

4 To, H., Grafton, R.Q. and Regan, S., 2017.

5 Walters, R. and Zeller, B., 2017.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

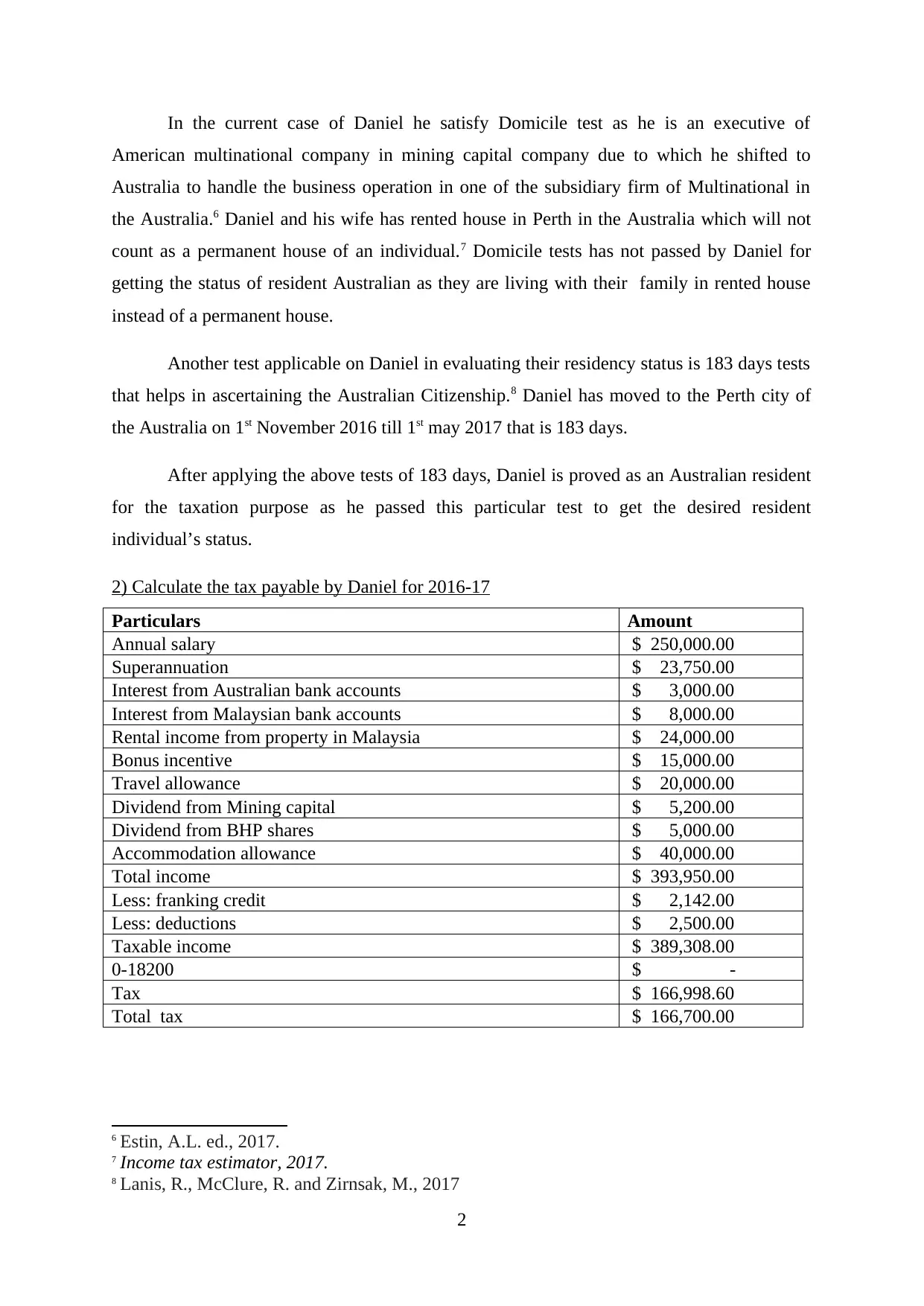

In the current case of Daniel he satisfy Domicile test as he is an executive of

American multinational company in mining capital company due to which he shifted to

Australia to handle the business operation in one of the subsidiary firm of Multinational in

the Australia.6 Daniel and his wife has rented house in Perth in the Australia which will not

count as a permanent house of an individual.7 Domicile tests has not passed by Daniel for

getting the status of resident Australian as they are living with their family in rented house

instead of a permanent house.

Another test applicable on Daniel in evaluating their residency status is 183 days tests

that helps in ascertaining the Australian Citizenship.8 Daniel has moved to the Perth city of

the Australia on 1st November 2016 till 1st may 2017 that is 183 days.

After applying the above tests of 183 days, Daniel is proved as an Australian resident

for the taxation purpose as he passed this particular test to get the desired resident

individual’s status.

2) Calculate the tax payable by Daniel for 2016-17

Particulars Amount

Annual salary $ 250,000.00

Superannuation $ 23,750.00

Interest from Australian bank accounts $ 3,000.00

Interest from Malaysian bank accounts $ 8,000.00

Rental income from property in Malaysia $ 24,000.00

Bonus incentive $ 15,000.00

Travel allowance $ 20,000.00

Dividend from Mining capital $ 5,200.00

Dividend from BHP shares $ 5,000.00

Accommodation allowance $ 40,000.00

Total income $ 393,950.00

Less: franking credit $ 2,142.00

Less: deductions $ 2,500.00

Taxable income $ 389,308.00

0-18200 $ -

Tax $ 166,998.60

Total tax $ 166,700.00

6 Estin, A.L. ed., 2017.

7 Income tax estimator, 2017.

8 Lanis, R., McClure, R. and Zirnsak, M., 2017

2

American multinational company in mining capital company due to which he shifted to

Australia to handle the business operation in one of the subsidiary firm of Multinational in

the Australia.6 Daniel and his wife has rented house in Perth in the Australia which will not

count as a permanent house of an individual.7 Domicile tests has not passed by Daniel for

getting the status of resident Australian as they are living with their family in rented house

instead of a permanent house.

Another test applicable on Daniel in evaluating their residency status is 183 days tests

that helps in ascertaining the Australian Citizenship.8 Daniel has moved to the Perth city of

the Australia on 1st November 2016 till 1st may 2017 that is 183 days.

After applying the above tests of 183 days, Daniel is proved as an Australian resident

for the taxation purpose as he passed this particular test to get the desired resident

individual’s status.

2) Calculate the tax payable by Daniel for 2016-17

Particulars Amount

Annual salary $ 250,000.00

Superannuation $ 23,750.00

Interest from Australian bank accounts $ 3,000.00

Interest from Malaysian bank accounts $ 8,000.00

Rental income from property in Malaysia $ 24,000.00

Bonus incentive $ 15,000.00

Travel allowance $ 20,000.00

Dividend from Mining capital $ 5,200.00

Dividend from BHP shares $ 5,000.00

Accommodation allowance $ 40,000.00

Total income $ 393,950.00

Less: franking credit $ 2,142.00

Less: deductions $ 2,500.00

Taxable income $ 389,308.00

0-18200 $ -

Tax $ 166,998.60

Total tax $ 166,700.00

6 Estin, A.L. ed., 2017.

7 Income tax estimator, 2017.

8 Lanis, R., McClure, R. and Zirnsak, M., 2017

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 2

1) Analyze the transactions in determining whether there any FBT or income tax implications

Fringe benefit liability incurred on an employer for providing all the benefits offer by

the business owner to sustain all the employees for long period of time in the business. It

includes various allowances such as mobile and laptop given by the owner to an employee,

travel allowances, car given by the firm, debt waived by the firm, business trips, loan offer by

the owner to its personnel.9 There are various transactions given below incurred by Joyce as a

marketing manager of escape vacations Pty Ltd in a particular financial year is mention

below:

Various transactions incurred by Joyce as a marketing manager of Escape vacations

Pty Ltd. Joyce is a family of four people with wife and two kids Zari and Luke. Several

transactions incurred by an individual have both income tax as well as fringe benefit tax

obligations which will be taxed in the hands of Joyce and not its employer.

Salary of $150000 plus superannuation benefit allowed by the employer of escape

vacations to its employee Joyce has income tax obligations instead of fringe benefit tax

liability. In the act of fringe benefit tax, salaries given to all the employees are not covered in

determining the fringe benefit liability for a particular year. Specifically exclusion of salary

and superannuation has mentioned in the act that helps an individual like Joyce to reduce

their overall fringe benefit tax liability incurred on all benefits provided by the employer to

facilitate all the needs of its employees.10 Superannuation benefit is also not consider as one

of the element included for determining the fringe benefit tax liability as this fund is regarded

as the secured fund of an individual which a person can redeem after a specific tenure in the

future and not before than that it helps I securing the wealth if an individual which also helps

in reducing the entire fringe benefit tax liability incurred on a person.

School fees pay by the Joyce for tow of their kids Zari and luke is also consider as a

legal fringe benefit emoluments taxed in the hands of an employee like Joyce as the

employer provided benefit to retain its employee for longer time period in a business

concern. This is also taxed under income tax obligations in which it is used as a deduction to

reduce the total income tax obligation of a person.

9 Braithwaite, V. ed., 2017.

10 Butler, C. and Calcott, P., 2017.

3

1) Analyze the transactions in determining whether there any FBT or income tax implications

Fringe benefit liability incurred on an employer for providing all the benefits offer by

the business owner to sustain all the employees for long period of time in the business. It

includes various allowances such as mobile and laptop given by the owner to an employee,

travel allowances, car given by the firm, debt waived by the firm, business trips, loan offer by

the owner to its personnel.9 There are various transactions given below incurred by Joyce as a

marketing manager of escape vacations Pty Ltd in a particular financial year is mention

below:

Various transactions incurred by Joyce as a marketing manager of Escape vacations

Pty Ltd. Joyce is a family of four people with wife and two kids Zari and Luke. Several

transactions incurred by an individual have both income tax as well as fringe benefit tax

obligations which will be taxed in the hands of Joyce and not its employer.

Salary of $150000 plus superannuation benefit allowed by the employer of escape

vacations to its employee Joyce has income tax obligations instead of fringe benefit tax

liability. In the act of fringe benefit tax, salaries given to all the employees are not covered in

determining the fringe benefit liability for a particular year. Specifically exclusion of salary

and superannuation has mentioned in the act that helps an individual like Joyce to reduce

their overall fringe benefit tax liability incurred on all benefits provided by the employer to

facilitate all the needs of its employees.10 Superannuation benefit is also not consider as one

of the element included for determining the fringe benefit tax liability as this fund is regarded

as the secured fund of an individual which a person can redeem after a specific tenure in the

future and not before than that it helps I securing the wealth if an individual which also helps

in reducing the entire fringe benefit tax liability incurred on a person.

School fees pay by the Joyce for tow of their kids Zari and luke is also consider as a

legal fringe benefit emoluments taxed in the hands of an employee like Joyce as the

employer provided benefit to retain its employee for longer time period in a business

concern. This is also taxed under income tax obligations in which it is used as a deduction to

reduce the total income tax obligation of a person.

9 Braithwaite, V. ed., 2017.

10 Butler, C. and Calcott, P., 2017.

3

Travel cost incurred by Escape vacations to afford the travel meetings of the

marketing manager for arranging meeting with the six potential clients have both income tax

as well as Fringe benefit liability obligations. The amount of GST has included in the total

amount of travel costs which is also deducted from the income tax liability of Joyce. After

excluding the amount of GST from the total travel expenses, 50% of the rest of expenses is

taken as travel fringe benefit cost in evaluating the FBT liability.11 Travel allowances given

by the firm to its employees has reduces from the taxable income of Joyce.

Professional membership expenses consider as legitimate fringe benefit element along

with the amount of GST which will be reduces from the total amount to determine the

exclusive GST amount in assessing the FBT obligations of a person.12 While determining

income tax obligations, this membership fee of gym is considered as personal expenses of an

individual which will get deducted from the total income of a person which indirectly reduces

the tax liability of a person.

Car given by the employer is considered as a fringe benefit tax element in which

personal and business use of the car is segregated to determine the taxable amount for income

tax as well as FBT tax purpose.13 All costs of operating associated with the car will be

included in ascertaining the amount of car allowance in the income tax and taxable value if

the car FBT. Including GST amount of the car and all other operating costs incurred for the

use of car is assessed by excluding the amount of GST from the total amount of the costs

incurred by a person to be taxed under income tax as well as Fringe tax liability.14 In

evaluating the tax, car allowances determine by an individual will get deducted from the total

cost of expenses incurred by a person on the car provided by the firm to its employee.

Gym membership fees is a personal expenses as per the income tax act in which an

individual will be assessed as a separate entity as compared to the firm or an entity in which a

person is working as all the expense incurred by a person will get deducted from the total

income earned by a person in a particular financial year. Similar expenses incurred by the

firm is taxed under FBT rules and regulations as providing additional facility for keeping

11 use. International Tax and Public Finance, pp.1-19.

12 Visser, A., 2017.

13 Temple, J. B., Rice, J. M. and McDonald, P. F., 2017.

14 Raftery, A., 2017

4

marketing manager for arranging meeting with the six potential clients have both income tax

as well as Fringe benefit liability obligations. The amount of GST has included in the total

amount of travel costs which is also deducted from the income tax liability of Joyce. After

excluding the amount of GST from the total travel expenses, 50% of the rest of expenses is

taken as travel fringe benefit cost in evaluating the FBT liability.11 Travel allowances given

by the firm to its employees has reduces from the taxable income of Joyce.

Professional membership expenses consider as legitimate fringe benefit element along

with the amount of GST which will be reduces from the total amount to determine the

exclusive GST amount in assessing the FBT obligations of a person.12 While determining

income tax obligations, this membership fee of gym is considered as personal expenses of an

individual which will get deducted from the total income of a person which indirectly reduces

the tax liability of a person.

Car given by the employer is considered as a fringe benefit tax element in which

personal and business use of the car is segregated to determine the taxable amount for income

tax as well as FBT tax purpose.13 All costs of operating associated with the car will be

included in ascertaining the amount of car allowance in the income tax and taxable value if

the car FBT. Including GST amount of the car and all other operating costs incurred for the

use of car is assessed by excluding the amount of GST from the total amount of the costs

incurred by a person to be taxed under income tax as well as Fringe tax liability.14 In

evaluating the tax, car allowances determine by an individual will get deducted from the total

cost of expenses incurred by a person on the car provided by the firm to its employee.

Gym membership fees is a personal expenses as per the income tax act in which an

individual will be assessed as a separate entity as compared to the firm or an entity in which a

person is working as all the expense incurred by a person will get deducted from the total

income earned by a person in a particular financial year. Similar expenses incurred by the

firm is taxed under FBT rules and regulations as providing additional facility for keeping

11 use. International Tax and Public Finance, pp.1-19.

12 Visser, A., 2017.

13 Temple, J. B., Rice, J. M. and McDonald, P. F., 2017.

14 Raftery, A., 2017

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

their body fit will further enhances its overall productivity which is also helpful for the firm

in generating higher output.15

2) Calculate FBT liability for the year

Particulars Amount

School fees 15000

Car fringe benefit(W.N.1) 15174

Loan Fringe benefit(W.N2) 10757

Debt waiver fringe benefit(W.N.3) 10000

Travel fringe benefit(W.N.5) 13500

Professional membership (W.N.6) 675

Gym membership(W.N8) 259.2

I pad 990

Mobile phone 67.5

Virgin Airline membership 99

Total taxable value of Fringe benefit 66521.7

Type 1 grossed up rate 2.1463

Taxable value 1427.755

Taxable value of fringe benefit on which no GST can be claim 24000

Type 2 Grossed up rate 1.9608

Taxable value 470.592

Total Fringe benefit taxable amount 1898.347

FBT liability 930.1902

Working notes

W.N.1 Car fringe benefit tax

Particulars Amount

Operating costs

Fuel per month 2400

Servicing 300

Registration 750

Insurance 700

Personal contribution amount 1800

Total operating costs 4150

Exclusive GST operating costs 3735

Leased cost 7200

Value of costs 31500

Total value of costs 42435

Private Km travelled by car 8000

Total km travelled 20000

Private % 40%

Employee contribution 1800

Car fringe benefit taxable value 15174

15

5

in generating higher output.15

2) Calculate FBT liability for the year

Particulars Amount

School fees 15000

Car fringe benefit(W.N.1) 15174

Loan Fringe benefit(W.N2) 10757

Debt waiver fringe benefit(W.N.3) 10000

Travel fringe benefit(W.N.5) 13500

Professional membership (W.N.6) 675

Gym membership(W.N8) 259.2

I pad 990

Mobile phone 67.5

Virgin Airline membership 99

Total taxable value of Fringe benefit 66521.7

Type 1 grossed up rate 2.1463

Taxable value 1427.755

Taxable value of fringe benefit on which no GST can be claim 24000

Type 2 Grossed up rate 1.9608

Taxable value 470.592

Total Fringe benefit taxable amount 1898.347

FBT liability 930.1902

Working notes

W.N.1 Car fringe benefit tax

Particulars Amount

Operating costs

Fuel per month 2400

Servicing 300

Registration 750

Insurance 700

Personal contribution amount 1800

Total operating costs 4150

Exclusive GST operating costs 3735

Leased cost 7200

Value of costs 31500

Total value of costs 42435

Private Km travelled by car 8000

Total km travelled 20000

Private % 40%

Employee contribution 1800

Car fringe benefit taxable value 15174

15

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

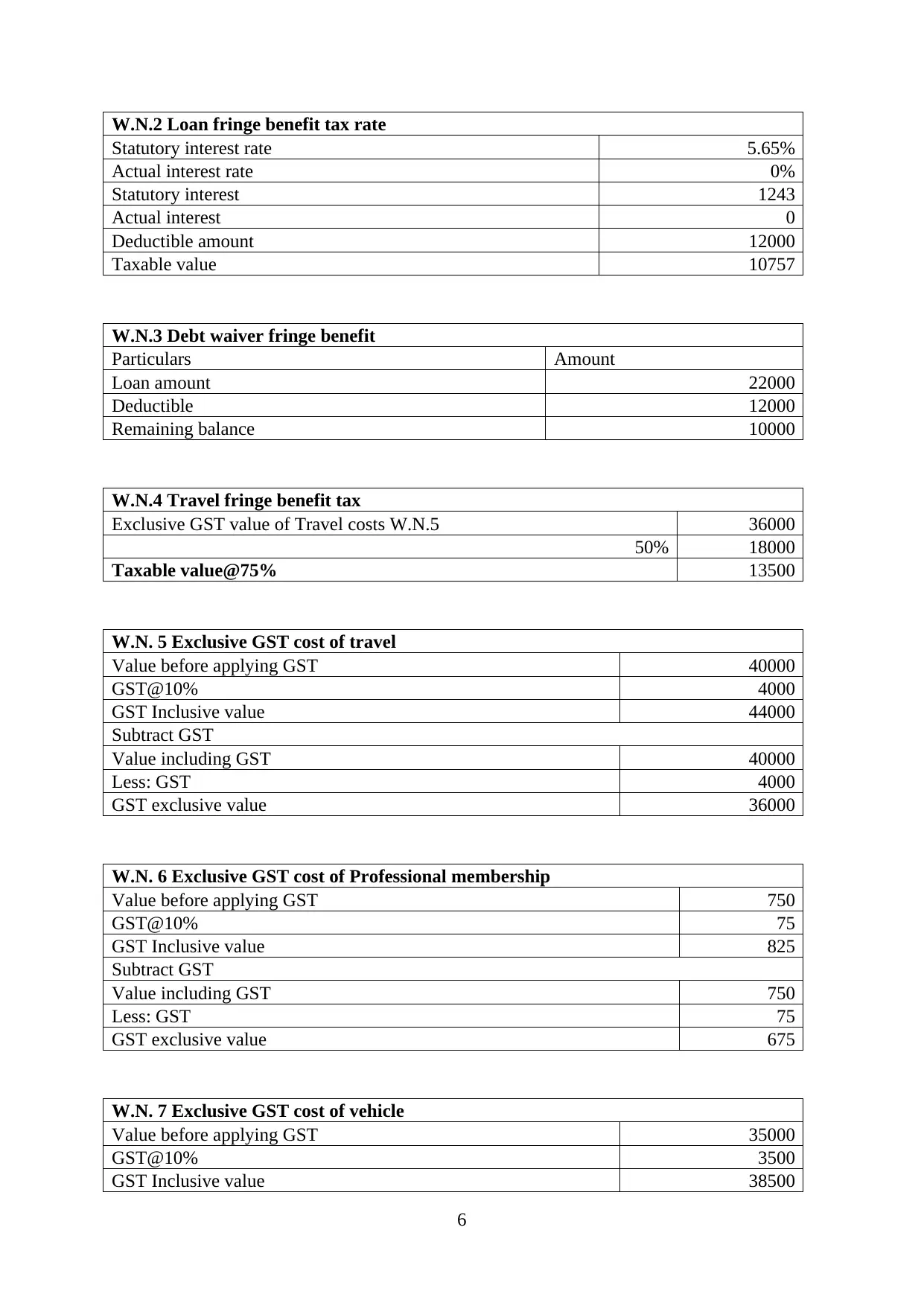

W.N.2 Loan fringe benefit tax rate

Statutory interest rate 5.65%

Actual interest rate 0%

Statutory interest 1243

Actual interest 0

Deductible amount 12000

Taxable value 10757

W.N.3 Debt waiver fringe benefit

Particulars Amount

Loan amount 22000

Deductible 12000

Remaining balance 10000

W.N.4 Travel fringe benefit tax

Exclusive GST value of Travel costs W.N.5 36000

50% 18000

Taxable value@75% 13500

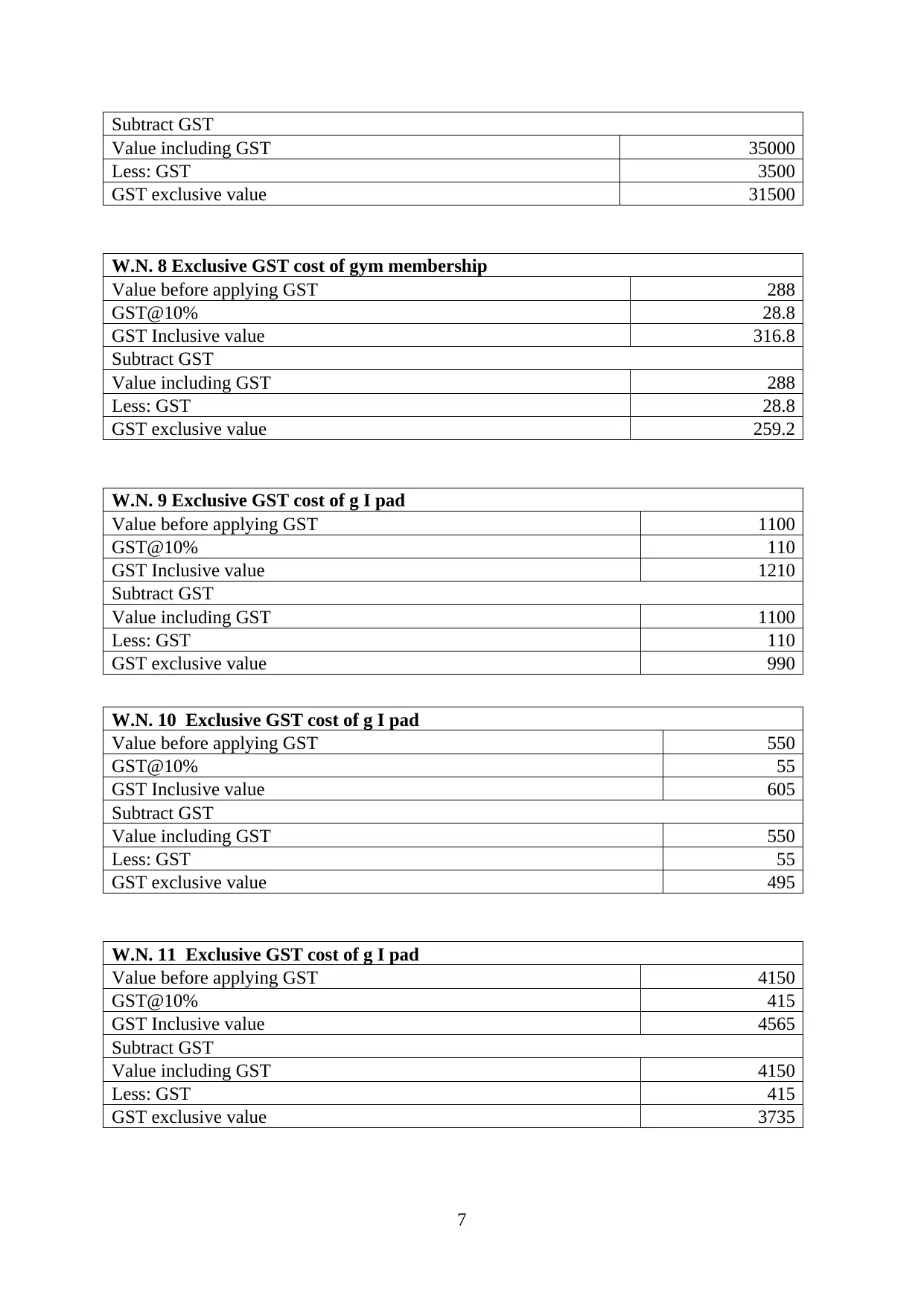

W.N. 5 Exclusive GST cost of travel

Value before applying GST 40000

GST@10% 4000

GST Inclusive value 44000

Subtract GST

Value including GST 40000

Less: GST 4000

GST exclusive value 36000

W.N. 6 Exclusive GST cost of Professional membership

Value before applying GST 750

GST@10% 75

GST Inclusive value 825

Subtract GST

Value including GST 750

Less: GST 75

GST exclusive value 675

W.N. 7 Exclusive GST cost of vehicle

Value before applying GST 35000

GST@10% 3500

GST Inclusive value 38500

6

Statutory interest rate 5.65%

Actual interest rate 0%

Statutory interest 1243

Actual interest 0

Deductible amount 12000

Taxable value 10757

W.N.3 Debt waiver fringe benefit

Particulars Amount

Loan amount 22000

Deductible 12000

Remaining balance 10000

W.N.4 Travel fringe benefit tax

Exclusive GST value of Travel costs W.N.5 36000

50% 18000

Taxable value@75% 13500

W.N. 5 Exclusive GST cost of travel

Value before applying GST 40000

GST@10% 4000

GST Inclusive value 44000

Subtract GST

Value including GST 40000

Less: GST 4000

GST exclusive value 36000

W.N. 6 Exclusive GST cost of Professional membership

Value before applying GST 750

GST@10% 75

GST Inclusive value 825

Subtract GST

Value including GST 750

Less: GST 75

GST exclusive value 675

W.N. 7 Exclusive GST cost of vehicle

Value before applying GST 35000

GST@10% 3500

GST Inclusive value 38500

6

Subtract GST

Value including GST 35000

Less: GST 3500

GST exclusive value 31500

W.N. 8 Exclusive GST cost of gym membership

Value before applying GST 288

GST@10% 28.8

GST Inclusive value 316.8

Subtract GST

Value including GST 288

Less: GST 28.8

GST exclusive value 259.2

W.N. 9 Exclusive GST cost of g I pad

Value before applying GST 1100

GST@10% 110

GST Inclusive value 1210

Subtract GST

Value including GST 1100

Less: GST 110

GST exclusive value 990

W.N. 10 Exclusive GST cost of g I pad

Value before applying GST 550

GST@10% 55

GST Inclusive value 605

Subtract GST

Value including GST 550

Less: GST 55

GST exclusive value 495

W.N. 11 Exclusive GST cost of g I pad

Value before applying GST 4150

GST@10% 415

GST Inclusive value 4565

Subtract GST

Value including GST 4150

Less: GST 415

GST exclusive value 3735

7

Value including GST 35000

Less: GST 3500

GST exclusive value 31500

W.N. 8 Exclusive GST cost of gym membership

Value before applying GST 288

GST@10% 28.8

GST Inclusive value 316.8

Subtract GST

Value including GST 288

Less: GST 28.8

GST exclusive value 259.2

W.N. 9 Exclusive GST cost of g I pad

Value before applying GST 1100

GST@10% 110

GST Inclusive value 1210

Subtract GST

Value including GST 1100

Less: GST 110

GST exclusive value 990

W.N. 10 Exclusive GST cost of g I pad

Value before applying GST 550

GST@10% 55

GST Inclusive value 605

Subtract GST

Value including GST 550

Less: GST 55

GST exclusive value 495

W.N. 11 Exclusive GST cost of g I pad

Value before applying GST 4150

GST@10% 415

GST Inclusive value 4565

Subtract GST

Value including GST 4150

Less: GST 415

GST exclusive value 3735

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

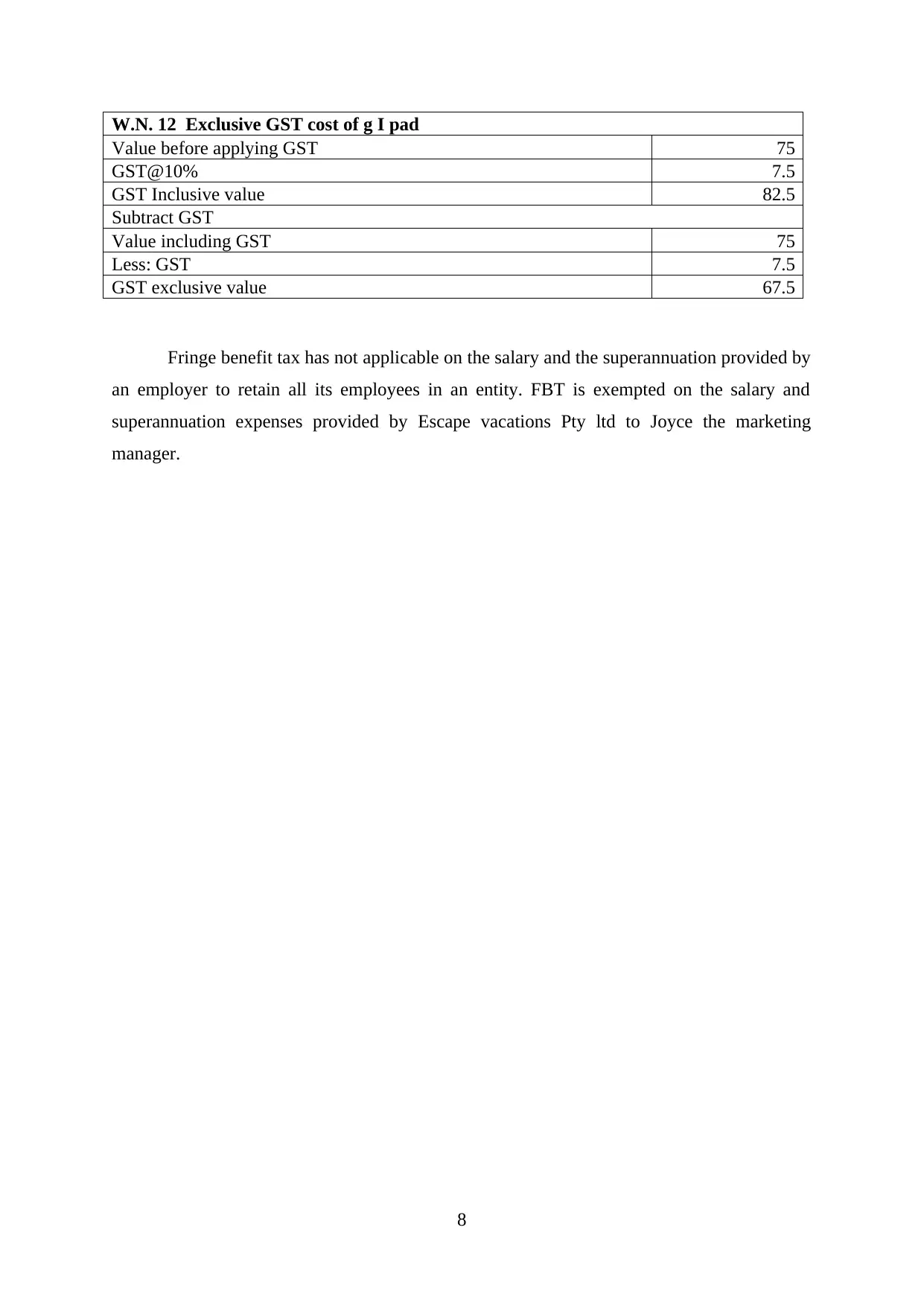

W.N. 12 Exclusive GST cost of g I pad

Value before applying GST 75

GST@10% 7.5

GST Inclusive value 82.5

Subtract GST

Value including GST 75

Less: GST 7.5

GST exclusive value 67.5

Fringe benefit tax has not applicable on the salary and the superannuation provided by

an employer to retain all its employees in an entity. FBT is exempted on the salary and

superannuation expenses provided by Escape vacations Pty ltd to Joyce the marketing

manager.

8

Value before applying GST 75

GST@10% 7.5

GST Inclusive value 82.5

Subtract GST

Value including GST 75

Less: GST 7.5

GST exclusive value 67.5

Fringe benefit tax has not applicable on the salary and the superannuation provided by

an employer to retain all its employees in an entity. FBT is exempted on the salary and

superannuation expenses provided by Escape vacations Pty ltd to Joyce the marketing

manager.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Butler, C. and Calcott, P., 2017. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, pp.1-19.

Estin, A.L. ed., 2017. The multi-cultural family. Routledge.

Hedrick, K., 2017. Getting out of (self-) harm's way: A study of factors associated with self-

harm among asylum seekers in Australian immigration detention. Journal of Forensic and

Legal Medicine.

Lanis, R., McClure, R. and Zirnsak, M., 2017. Tax aggressiveness of alcohol and bottling

companies in Australia.

Maurer, L., Port, C., Roth, T. and Walker, J., 2017. A Brave New Post-BEPS World: New

Double Tax Treaty Between Germany and Australia Implements BEPS Measures. Intertax.

45(4). pp.310-321.

Raftery, A., 2017. 101 Ways to Save Money on Your Tax-Legally! 2017-2018. John Wiley &

Sons.

Robertson, S., 2017. Infrastructures of insecurity: Housing and language testing in Asia-

Australia migration. Geoforum. 82. pp.13-20.

Shum, C., Fay, J. and Lui, G., 2017. Individual Income Tax: A Cross-Continental

Comparison. World. 7(1). pp.64-88.

Temple, J. B., Rice, J. M. and McDonald, P. F., 2017. The Journal of the Economics of

Ageing.

To, H., Grafton, R.Q. and Regan, S., 2017. Immigration and labour market outcomes in

Australia: Findings from HILDA 2001–2014. Economic Analysis and Policy. 55. pp.1-13.

Visser, A., 2017. Tax and employee transport. Tax Breaks Newsletter, 2017(376), pp.8-8.

9

Books and journals

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Butler, C. and Calcott, P., 2017. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, pp.1-19.

Estin, A.L. ed., 2017. The multi-cultural family. Routledge.

Hedrick, K., 2017. Getting out of (self-) harm's way: A study of factors associated with self-

harm among asylum seekers in Australian immigration detention. Journal of Forensic and

Legal Medicine.

Lanis, R., McClure, R. and Zirnsak, M., 2017. Tax aggressiveness of alcohol and bottling

companies in Australia.

Maurer, L., Port, C., Roth, T. and Walker, J., 2017. A Brave New Post-BEPS World: New

Double Tax Treaty Between Germany and Australia Implements BEPS Measures. Intertax.

45(4). pp.310-321.

Raftery, A., 2017. 101 Ways to Save Money on Your Tax-Legally! 2017-2018. John Wiley &

Sons.

Robertson, S., 2017. Infrastructures of insecurity: Housing and language testing in Asia-

Australia migration. Geoforum. 82. pp.13-20.

Shum, C., Fay, J. and Lui, G., 2017. Individual Income Tax: A Cross-Continental

Comparison. World. 7(1). pp.64-88.

Temple, J. B., Rice, J. M. and McDonald, P. F., 2017. The Journal of the Economics of

Ageing.

To, H., Grafton, R.Q. and Regan, S., 2017. Immigration and labour market outcomes in

Australia: Findings from HILDA 2001–2014. Economic Analysis and Policy. 55. pp.1-13.

Visser, A., 2017. Tax and employee transport. Tax Breaks Newsletter, 2017(376), pp.8-8.

9

Walters, R. and Zeller, B., 2017. A Comparative Study of Australia and Slovenia’s Private

International Laws and the Application of Citizenship and Residence. Liverpool Law

Review. 38(3). pp.325-338.

Online

Income tax estimator, 2017. Available through: < https://www.ato.gov.au/Calculators-and-

tools/Income-tax-estimator/> [Accessed on 27th October 2017].

Residency tests, 2017. Available through: < https://www.ato.gov.au/individuals/international-

tax-for-individuals/work-out-your-tax-residency/residency-tests/> [Accessed on 27th

October 2017].

10

International Laws and the Application of Citizenship and Residence. Liverpool Law

Review. 38(3). pp.325-338.

Online

Income tax estimator, 2017. Available through: < https://www.ato.gov.au/Calculators-and-

tools/Income-tax-estimator/> [Accessed on 27th October 2017].

Residency tests, 2017. Available through: < https://www.ato.gov.au/individuals/international-

tax-for-individuals/work-out-your-tax-residency/residency-tests/> [Accessed on 27th

October 2017].

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.