Tax Implication and Planning: City Sky Corporation and Individual

VerifiedAdded on 2022/10/18

|12

|3064

|374

Report

AI Summary

This report delves into the tax implications for City Sky Corporation and an individual named Emma, analyzing their tax liabilities and exploring tax planning strategies. The report addresses the Goods and Service Tax (GST) implications for City Sky Corporation, particularly concerning input tax credits and the services provided by a legal advisor. It examines the applicability of GST based on the company's and the advisor's financial thresholds. The report also computes the capital gain (CG) tax (CGT) liabilities for Emma, considering the sale of a capital land, shares in Rio Tinto, a stamp collection, and a grand piano. The analysis includes detailed calculations of capital gains, considering various costs and expenses incurred. Furthermore, the report references Australian taxation rules and regulations, including the Income Tax Act and Capital Gains Tax provisions, to determine the tax implications of each transaction. The report's objective is to provide a comprehensive overview of tax liabilities and the importance of tax planning in minimizing tax burdens for both entities.

Running Head: - Tax Implication on the company 0 | P a g e

Tax Implication on the company

Module Number

0

Tax Implication on the company

Module Number

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax Implication on the company` 1 | P a g e

Table of Contents

Introduction.................................................................................................................................................2

Answer to the given question-1...............................................................................................................2

Issue........................................................................................................................................................2

Rule.........................................................................................................................................................2

Application..............................................................................................................................................3

Conclusion...............................................................................................................................................4

Answer to the question no 2 –................................................................................................................5

Conclusion...................................................................................................................................................9

References.................................................................................................................................................10

1

Table of Contents

Introduction.................................................................................................................................................2

Answer to the given question-1...............................................................................................................2

Issue........................................................................................................................................................2

Rule.........................................................................................................................................................2

Application..............................................................................................................................................3

Conclusion...............................................................................................................................................4

Answer to the question no 2 –................................................................................................................5

Conclusion...................................................................................................................................................9

References.................................................................................................................................................10

1

Tax Implication on the company` 2 | P a g e

Introduction

This report has revealed the tax implication and taxation planning made by the company

and individual to compute the total taxable liabilities. In the starting of this report, tax

implication and the total tax liability of the company has been computed. After that the different

aspects of the taxation rules and regulations to compute the tax to be paid by the assesse has been

made. This report has shown that in order to compute the proper tax liabilities and reducing the

tax burden of the individual, there is required to implement the proper tax planning. In the

starting, GST tax credit and tax implication has been given in context with the tax liabilities of

the City Sky Corporation limited.

Answer to the given question-1

Issue

Whether the City Sky Co of the input tax credit entitlements that they may be entitled as per GST?

Rule

The organization considered in the tax assessment is City Sky Corporation limited. It is a private

corporation limited organization which is registered under the society and corporation act.

However, this company falls under the Goods and Service Tax computed under the Goods and

Service Act of Australia. The City and Sky Company manages the speculation made in the

property and furthermore incorporate structure properties which goes under Australian Goods

and Service Tax Act (Brabazon, 2019). The City Sky Corporation limited has obtained a vacant

land in the Southern piece of Brisbane where the organization is setting up to raise tall structure

with 15 lofts, so they can sell the its structure independently However, the Maurice Blackburn,

an area legal advisor was enlisted by City Sky Corporation limited to take help for his legitimate

2

Introduction

This report has revealed the tax implication and taxation planning made by the company

and individual to compute the total taxable liabilities. In the starting of this report, tax

implication and the total tax liability of the company has been computed. After that the different

aspects of the taxation rules and regulations to compute the tax to be paid by the assesse has been

made. This report has shown that in order to compute the proper tax liabilities and reducing the

tax burden of the individual, there is required to implement the proper tax planning. In the

starting, GST tax credit and tax implication has been given in context with the tax liabilities of

the City Sky Corporation limited.

Answer to the given question-1

Issue

Whether the City Sky Co of the input tax credit entitlements that they may be entitled as per GST?

Rule

The organization considered in the tax assessment is City Sky Corporation limited. It is a private

corporation limited organization which is registered under the society and corporation act.

However, this company falls under the Goods and Service Tax computed under the Goods and

Service Act of Australia. The City and Sky Company manages the speculation made in the

property and furthermore incorporate structure properties which goes under Australian Goods

and Service Tax Act (Brabazon, 2019). The City Sky Corporation limited has obtained a vacant

land in the Southern piece of Brisbane where the organization is setting up to raise tall structure

with 15 lofts, so they can sell the its structure independently However, the Maurice Blackburn,

an area legal advisor was enlisted by City Sky Corporation limited to take help for his legitimate

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax Implication on the company` 3 | P a g e

administrations for purchasing the vacant land (Evans, Minas, & Lim, 2015). Attorney Maurice

Blackburn was paid a charge of $33,000 for giving his administrations required for the

improvement and renovating the building accompanied with the total 15 apartments.

Furthermore, offering his lawful administrations to the clients, Maurice Blackburn likewise wins

income of $300,000 per annum from a perceived private concern. Maurice Blackburn is being

paid by City Sky Corporation limited for his administrations (Edmonds, 2015). His duty is to

build up the structure of 15 lofts with the goal that the organization can sell them, as the typical

idea of their industry and the sum paid for legitimate administrations to Maurice Blackburn can

be brought from the division of the merchandise sold by City Sky Corporation limited (Faccio &

Xu, 2015). The charge paid to the legal advisor by the organization is at risk for duty

contribution by City Sky Corporation limited. The expense is determined as the word related

profit picked up by legal advisor Maurice Blackburn consequently of the legitimate

administrations given by the legal counselor to City Sky Company. As the aggregate sum of

$33,000 is the division of the expense to the association, the City Sky Corporation limited can

profit the total duty commitment on the all-out expense (Braithwaite, 2017).

Application

As per the given laws and regulations under the Goods and Service Act, it is considered that any

organization or industry having the yearly salary of $75000 for the association or is offering any

administrations and a pay of $150000 which is the least skirt a firm or an organization requires

or the NGO or non-benefit organizations. In the given case, it has been found that they are

qualified for paying tax under the Goods and Service Act of Australia. Hence, an autonomous

exchange business and friends of a legal counselor will likewise be recorded under Goods and

Service Act (Faccio, & Xu, 2015). Subsequently, Maurice Blackburn, the legal counselor, is

3

administrations for purchasing the vacant land (Evans, Minas, & Lim, 2015). Attorney Maurice

Blackburn was paid a charge of $33,000 for giving his administrations required for the

improvement and renovating the building accompanied with the total 15 apartments.

Furthermore, offering his lawful administrations to the clients, Maurice Blackburn likewise wins

income of $300,000 per annum from a perceived private concern. Maurice Blackburn is being

paid by City Sky Corporation limited for his administrations (Edmonds, 2015). His duty is to

build up the structure of 15 lofts with the goal that the organization can sell them, as the typical

idea of their industry and the sum paid for legitimate administrations to Maurice Blackburn can

be brought from the division of the merchandise sold by City Sky Corporation limited (Faccio &

Xu, 2015). The charge paid to the legal advisor by the organization is at risk for duty

contribution by City Sky Corporation limited. The expense is determined as the word related

profit picked up by legal advisor Maurice Blackburn consequently of the legitimate

administrations given by the legal counselor to City Sky Company. As the aggregate sum of

$33,000 is the division of the expense to the association, the City Sky Corporation limited can

profit the total duty commitment on the all-out expense (Braithwaite, 2017).

Application

As per the given laws and regulations under the Goods and Service Act, it is considered that any

organization or industry having the yearly salary of $75000 for the association or is offering any

administrations and a pay of $150000 which is the least skirt a firm or an organization requires

or the NGO or non-benefit organizations. In the given case, it has been found that they are

qualified for paying tax under the Goods and Service Act of Australia. Hence, an autonomous

exchange business and friends of a legal counselor will likewise be recorded under Goods and

Service Act (Faccio, & Xu, 2015). Subsequently, Maurice Blackburn, the legal counselor, is

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax Implication on the company` 4 | P a g e

permitted to the make good on the regulatory obligation risk to City Sky Corporation limited for

the expenses he gathers for offering his legitimate support of the association in both the cases,

either gathering the charges as the business gaining which falls under Income Tax Act or getting

the lawful charges in the autonomous business (Krever, 2013).

Conclusion

As Maurice Blackburn works in his already set up business and he is also liable to pay GST on

the goods and services sold under the Goods and Service Act of Australia. Then again, the City

Sky Corporation limited is additionally qualified to get the duty risk from Maurice Blackburn, as

the organization pays the charges to the legal advisor for benefiting his legitimate

administrations for structure the vacant land is the division of the measure of a definitive item the

organization manages (Dixon, & Nassios, 2016).

4

permitted to the make good on the regulatory obligation risk to City Sky Corporation limited for

the expenses he gathers for offering his legitimate support of the association in both the cases,

either gathering the charges as the business gaining which falls under Income Tax Act or getting

the lawful charges in the autonomous business (Krever, 2013).

Conclusion

As Maurice Blackburn works in his already set up business and he is also liable to pay GST on

the goods and services sold under the Goods and Service Act of Australia. Then again, the City

Sky Corporation limited is additionally qualified to get the duty risk from Maurice Blackburn, as

the organization pays the charges to the legal advisor for benefiting his legitimate

administrations for structure the vacant land is the division of the measure of a definitive item the

organization manages (Dixon, & Nassios, 2016).

4

Tax Implication on the company` 5 | P a g e

Answer to the question no 2 –

In the given case, it has been found that the person Emma, who is liable to pay tax on her

income will be assessed under the Australian taxation rules and regulations. However, in the

given case, computation of the capital gain (CG) tax (CGT) of the individual in the various

situation has been given.

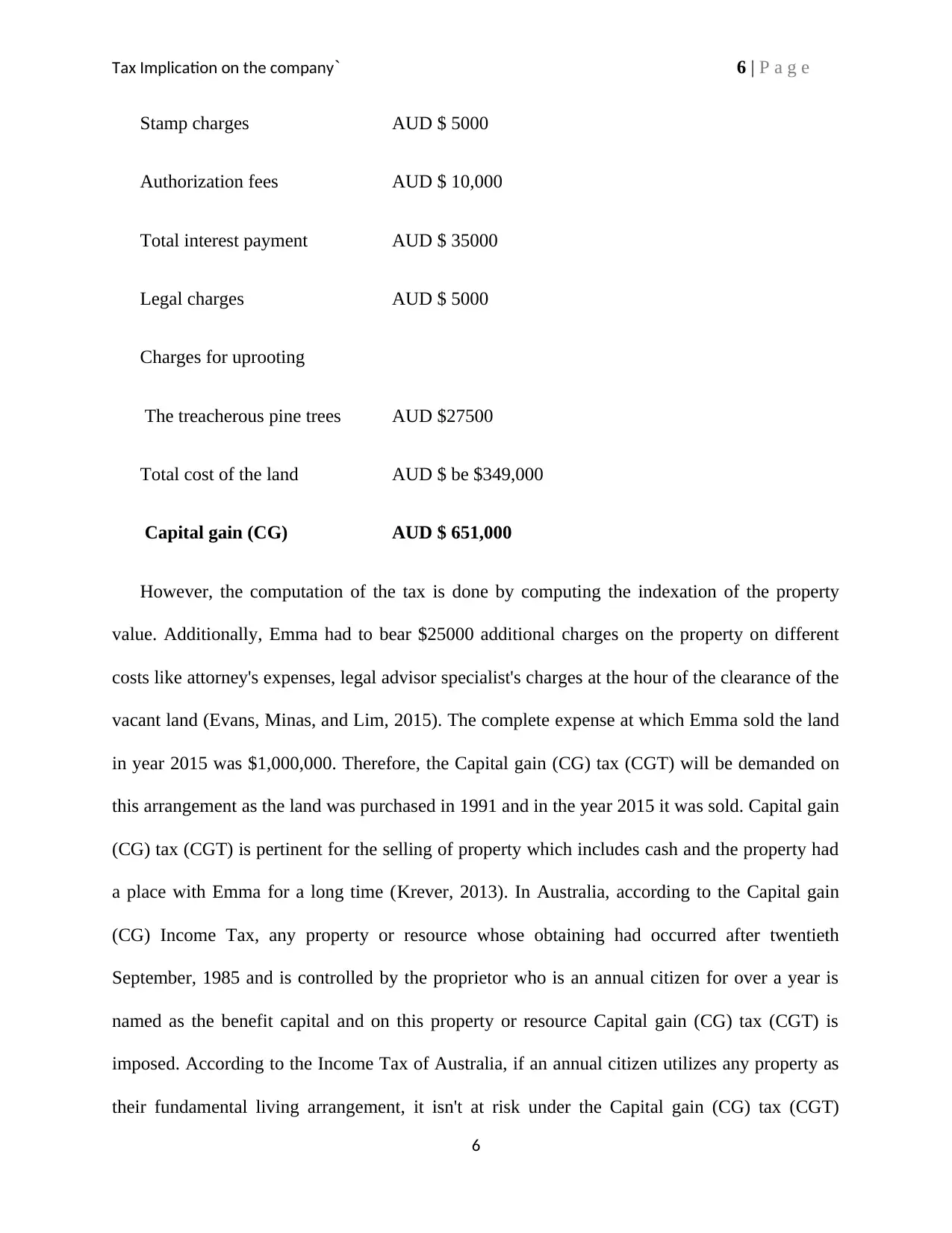

1. Capital gain (CG) tax (CGT) on the sale of the capital land of $1,000,000 –

In the given case, Emma being an Australian resident purchased the land with a view to keep

it for the investment purpose in the 1991. This property was purchased for the AUD $ 25000.

After that, it was found that Emma paid the total balance of the AUD $ 5000 for stamp charges

and total payment of AUD $ 10,000 was being paid by her to the authority as authorization fees

for purchasing the given land (Burkhauser, Hahn, & Wilkins, 2015). However, in the given case,

it was found that Emma took the loan for purchasing the land and on which total interest

payment of AUD $ 32000 was given by her. After that in the 2015, Emma had fight with her

neighbor for the reason of misused by the same land by them (Dixon, & Nassios, 2016). It was

found that the same issue was cleared between both and amount of AUD $ 5000 was paid by

Emma to legal advisor as legal fees, nonetheless, throughout the period of the trespass, Emma

spent total amount AUD $ 27500 for uprooting the treacherous pine trees that were grown on the

empty land (Keen, & Ligthart, 2016).

Computation of the tax liability

This property was purchased for the AUD $ 25000

Additional charges costing

5

Answer to the question no 2 –

In the given case, it has been found that the person Emma, who is liable to pay tax on her

income will be assessed under the Australian taxation rules and regulations. However, in the

given case, computation of the capital gain (CG) tax (CGT) of the individual in the various

situation has been given.

1. Capital gain (CG) tax (CGT) on the sale of the capital land of $1,000,000 –

In the given case, Emma being an Australian resident purchased the land with a view to keep

it for the investment purpose in the 1991. This property was purchased for the AUD $ 25000.

After that, it was found that Emma paid the total balance of the AUD $ 5000 for stamp charges

and total payment of AUD $ 10,000 was being paid by her to the authority as authorization fees

for purchasing the given land (Burkhauser, Hahn, & Wilkins, 2015). However, in the given case,

it was found that Emma took the loan for purchasing the land and on which total interest

payment of AUD $ 32000 was given by her. After that in the 2015, Emma had fight with her

neighbor for the reason of misused by the same land by them (Dixon, & Nassios, 2016). It was

found that the same issue was cleared between both and amount of AUD $ 5000 was paid by

Emma to legal advisor as legal fees, nonetheless, throughout the period of the trespass, Emma

spent total amount AUD $ 27500 for uprooting the treacherous pine trees that were grown on the

empty land (Keen, & Ligthart, 2016).

Computation of the tax liability

This property was purchased for the AUD $ 25000

Additional charges costing

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax Implication on the company` 6 | P a g e

Stamp charges AUD $ 5000

Authorization fees AUD $ 10,000

Total interest payment AUD $ 35000

Legal charges AUD $ 5000

Charges for uprooting

The treacherous pine trees AUD $27500

Total cost of the land AUD $ be $349,000

Capital gain (CG) AUD $ 651,000

However, the computation of the tax is done by computing the indexation of the property

value. Additionally, Emma had to bear $25000 additional charges on the property on different

costs like attorney's expenses, legal advisor specialist's charges at the hour of the clearance of the

vacant land (Evans, Minas, and Lim, 2015). The complete expense at which Emma sold the land

in year 2015 was $1,000,000. Therefore, the Capital gain (CG) tax (CGT) will be demanded on

this arrangement as the land was purchased in 1991 and in the year 2015 it was sold. Capital gain

(CG) tax (CGT) is pertinent for the selling of property which includes cash and the property had

a place with Emma for a long time (Krever, 2013). In Australia, according to the Capital gain

(CG) Income Tax, any property or resource whose obtaining had occurred after twentieth

September, 1985 and is controlled by the proprietor who is an annual citizen for over a year is

named as the benefit capital and on this property or resource Capital gain (CG) tax (CGT) is

imposed. According to the Income Tax of Australia, if an annual citizen utilizes any property as

their fundamental living arrangement, it isn't at risk under the Capital gain (CG) tax (CGT)

6

Stamp charges AUD $ 5000

Authorization fees AUD $ 10,000

Total interest payment AUD $ 35000

Legal charges AUD $ 5000

Charges for uprooting

The treacherous pine trees AUD $27500

Total cost of the land AUD $ be $349,000

Capital gain (CG) AUD $ 651,000

However, the computation of the tax is done by computing the indexation of the property

value. Additionally, Emma had to bear $25000 additional charges on the property on different

costs like attorney's expenses, legal advisor specialist's charges at the hour of the clearance of the

vacant land (Evans, Minas, and Lim, 2015). The complete expense at which Emma sold the land

in year 2015 was $1,000,000. Therefore, the Capital gain (CG) tax (CGT) will be demanded on

this arrangement as the land was purchased in 1991 and in the year 2015 it was sold. Capital gain

(CG) tax (CGT) is pertinent for the selling of property which includes cash and the property had

a place with Emma for a long time (Krever, 2013). In Australia, according to the Capital gain

(CG) Income Tax, any property or resource whose obtaining had occurred after twentieth

September, 1985 and is controlled by the proprietor who is an annual citizen for over a year is

named as the benefit capital and on this property or resource Capital gain (CG) tax (CGT) is

imposed. According to the Income Tax of Australia, if an annual citizen utilizes any property as

their fundamental living arrangement, it isn't at risk under the Capital gain (CG) tax (CGT)

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax Implication on the company` 7 | P a g e

(Wilkins, 2015). Subsequently, as Emma had not utilized the property as her primary home, the

Capital gain (CG) tax (CGT) won't be appropriate on the clearance of Emma's territory

(Larrimore, et al. 2016). The other purpose behind the utilization of Capital gain (CG) tax

(CGT) on this land is that since Emma isn't procuring anything out of this unfilled property so

Capital gain (CG) tax (CGT) will be imposed on this land and the exchange in question and this

land will be named as Capital Asset. Therefore, in the given case, it has been found that Emma

can assess the complete Capital gain (CG) tax (CGT) collected in this arrangement by including

every one of the costs she made while she claimed that vacant land including the costs she made

like fixing, dispensing with the pine trees that were developed on the land before it got sold. All

these use will be included the absolute expense of the property. Additionally the other mount

which Emma paid such as intrigue paid for purchasing the property which was $32000, $5000 as

legal stamp costing, and $10000 as the expenses paid to the legal advisor (Llamas, Araar, &

Huesca, 2017). These all will be summarized in the complete expense. Indeed, even every one

of the costs like water cost, board cost and the protection caused will to likewise be incorporated

into the intimal purchasing costing of the land. The sum Emma spent for settling the issue with

the neighbor of that land in the year 2005 will also be included and it will be amounted to

expenses AUD $ 5000. The sum sent on marking, legal advisor's charges and the dealer's

expenses which is all out $25000 will likewise be included in the total purchase cost of the land.

The cost at which the property was sold is $1,000,000, the cost of the property was $250,000 and

the absolute consumption turns out to be $349,000. Along these lines, the sum $651,000 will be

represented Capital gain (CG) and same will be used by the Emma while determining her capital

gain (CG) tax liabilities (López, Figueroa, & Gutiérrez, 2016).

2. Selling of 1000 shares of Emma in Rio Tinto at a price of $50.85 per share –

7

(Wilkins, 2015). Subsequently, as Emma had not utilized the property as her primary home, the

Capital gain (CG) tax (CGT) won't be appropriate on the clearance of Emma's territory

(Larrimore, et al. 2016). The other purpose behind the utilization of Capital gain (CG) tax

(CGT) on this land is that since Emma isn't procuring anything out of this unfilled property so

Capital gain (CG) tax (CGT) will be imposed on this land and the exchange in question and this

land will be named as Capital Asset. Therefore, in the given case, it has been found that Emma

can assess the complete Capital gain (CG) tax (CGT) collected in this arrangement by including

every one of the costs she made while she claimed that vacant land including the costs she made

like fixing, dispensing with the pine trees that were developed on the land before it got sold. All

these use will be included the absolute expense of the property. Additionally the other mount

which Emma paid such as intrigue paid for purchasing the property which was $32000, $5000 as

legal stamp costing, and $10000 as the expenses paid to the legal advisor (Llamas, Araar, &

Huesca, 2017). These all will be summarized in the complete expense. Indeed, even every one

of the costs like water cost, board cost and the protection caused will to likewise be incorporated

into the intimal purchasing costing of the land. The sum Emma spent for settling the issue with

the neighbor of that land in the year 2005 will also be included and it will be amounted to

expenses AUD $ 5000. The sum sent on marking, legal advisor's charges and the dealer's

expenses which is all out $25000 will likewise be included in the total purchase cost of the land.

The cost at which the property was sold is $1,000,000, the cost of the property was $250,000 and

the absolute consumption turns out to be $349,000. Along these lines, the sum $651,000 will be

represented Capital gain (CG) and same will be used by the Emma while determining her capital

gain (CG) tax liabilities (López, Figueroa, & Gutiérrez, 2016).

2. Selling of 1000 shares of Emma in Rio Tinto at a price of $50.85 per share –

7

Tax Implication on the company` 8 | P a g e

In Rio Tinto Emma sold 1000 shares and gave a fee of 2% for selling these shares at the

rate of $50.85 per share (Llamas, Araar, and Huesca, 2017). In year 1982, Emma in the

beginning bought the shares at the rate of $3.5 each share. Since, these shares were bought in

1982 by Emma, they shall be not considered as Capital Asset and Capital gain (CG) will also not

be applied to the benefit received by the share selling (Modigliani, & Miller, 2013). The head of

Income Tax Capital gain (CG) of Australia quotes that before 20th September 1985, all the assets

including properties bought for investing or shares are not termed as Capital Asset and hence,

they will not be applicable to Capital gain (CG) tax (CGT) on such dealings (Chardon,

Freudenberg, and Brimble 2016).

3. Selling of Emma’s stamp collection which she bought in January 2015 at $60,000

from a stamp collector –

In the given case, it is found that in the year 2015, January, Emma acquired the various

stamps form the stamp collector who was selling it. The total amount of sum was paid by her

was AUD $ 60,000 and selling price of the same was AUD % 50,000 in 2015. Furthermore, she

also had to pay AUD $ 5000 for collecting the stamps. It is further observed that shares were

scarified by her in the one year of buying and there was no capital gain (CG) tax on the same

assets. All the shares purchased under the given conditions (Sold before year) will be exempt

from the taxation purpose (Niemirowski, Baldwin, &Wearing, 2013).

4. Selling of Emma’s grand piano at the rate of $30000 –

In this given case, it is observed that Emma was indulged in selling the Grand piano for

the amount of AUD $ 30,000. However, she purchased the same piano for AUD $ 30,000 in

2015. She held the same assets for more than 15 years as it is considered that piano was

8

In Rio Tinto Emma sold 1000 shares and gave a fee of 2% for selling these shares at the

rate of $50.85 per share (Llamas, Araar, and Huesca, 2017). In year 1982, Emma in the

beginning bought the shares at the rate of $3.5 each share. Since, these shares were bought in

1982 by Emma, they shall be not considered as Capital Asset and Capital gain (CG) will also not

be applied to the benefit received by the share selling (Modigliani, & Miller, 2013). The head of

Income Tax Capital gain (CG) of Australia quotes that before 20th September 1985, all the assets

including properties bought for investing or shares are not termed as Capital Asset and hence,

they will not be applicable to Capital gain (CG) tax (CGT) on such dealings (Chardon,

Freudenberg, and Brimble 2016).

3. Selling of Emma’s stamp collection which she bought in January 2015 at $60,000

from a stamp collector –

In the given case, it is found that in the year 2015, January, Emma acquired the various

stamps form the stamp collector who was selling it. The total amount of sum was paid by her

was AUD $ 60,000 and selling price of the same was AUD % 50,000 in 2015. Furthermore, she

also had to pay AUD $ 5000 for collecting the stamps. It is further observed that shares were

scarified by her in the one year of buying and there was no capital gain (CG) tax on the same

assets. All the shares purchased under the given conditions (Sold before year) will be exempt

from the taxation purpose (Niemirowski, Baldwin, &Wearing, 2013).

4. Selling of Emma’s grand piano at the rate of $30000 –

In this given case, it is observed that Emma was indulged in selling the Grand piano for

the amount of AUD $ 30,000. However, she purchased the same piano for AUD $ 30,000 in

2015. She held the same assets for more than 15 years as it is considered that piano was

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax Implication on the company` 9 | P a g e

purchased by here in 2000 and it has been more than 15 years since the purchase of the piano.

Nonetheless, there will be depreciation on the piano with the rate of 40% and Emma made profit

of AUD 30,000 in the capital gain (CG) Australian income tax (Seim, 2017).

Conclusion

After assessing all the taxation rules and capital gain (CG) taxation implication, it has

been found that Emma would have to determine her taxation liabilities as per the capital gain

(CG) taxation rules and act. It has been observed that, there is required to implement the proper

tax planning to determine the tax liability of the Emma on her capital gain (CG).

9

purchased by here in 2000 and it has been more than 15 years since the purchase of the piano.

Nonetheless, there will be depreciation on the piano with the rate of 40% and Emma made profit

of AUD 30,000 in the capital gain (CG) Australian income tax (Seim, 2017).

Conclusion

After assessing all the taxation rules and capital gain (CG) taxation implication, it has

been found that Emma would have to determine her taxation liabilities as per the capital gain

(CG) taxation rules and act. It has been observed that, there is required to implement the proper

tax planning to determine the tax liability of the Emma on her capital gain (CG).

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax Implication on the company` 10 | P a g e

References

Auerbach, A. J., & Hassett, K. (2015). Capital taxation in the twenty-first century. American

Economic Review, 105(5), 38-42.

Biørn, E. (2017). Taxation, technology, and the user cost of capital (Vol. 182). Elsevier.

Burkhauser, R. V., Hahn, M. H., & Wilkins, R. (2015). Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), 181-

205.

Dixon, J.,& Nassios, J. 2016. Modelling the impacts of a cut to company tax in Australia. Centre

of Policy Studies (CoPS), Victoria University.

Edmonds, R., 2015. Structural tax reform: What should be brought to the table. Austl. Tax F., 30,

p.393.

Evans, C., Minas, J. & Lim, Y., 2015. Taxing personal capital gain (CG)s in Australia: an

alternative way forward. Austl. Tax F., 30, p.735.

Faccio, M. &Xu, J., 2015. Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), pp.277-300.

Faccio, M., & Xu, J. (2015). Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), 277-300.

Keen, M., & Ligthart, J. E. (2016). Information sharing and international taxation: a primer.

International Tax and Public Finance, 13(1), 81-110.

Krever, R. (2013). Taming complexity in Australian income tax. Sydney L. Rev., 25, 467.

Larrimore, J., Burkhauser, R. V., Auten, G., & Armour, P. (2016). Recent trends in US top

income shares in tax record data using more comprehensive measures of income

including accrued capital gains (No. w23007). National Bureau of Economic Research.

Llamas, L., Araar, A., & Huesca, L. (2017). Income redistribution and inequality in the Mexican

tax-benefit system. Cuadernos de Economía, 36(SPE72), 301-325.

10

References

Auerbach, A. J., & Hassett, K. (2015). Capital taxation in the twenty-first century. American

Economic Review, 105(5), 38-42.

Biørn, E. (2017). Taxation, technology, and the user cost of capital (Vol. 182). Elsevier.

Burkhauser, R. V., Hahn, M. H., & Wilkins, R. (2015). Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), 181-

205.

Dixon, J.,& Nassios, J. 2016. Modelling the impacts of a cut to company tax in Australia. Centre

of Policy Studies (CoPS), Victoria University.

Edmonds, R., 2015. Structural tax reform: What should be brought to the table. Austl. Tax F., 30,

p.393.

Evans, C., Minas, J. & Lim, Y., 2015. Taxing personal capital gain (CG)s in Australia: an

alternative way forward. Austl. Tax F., 30, p.735.

Faccio, M. &Xu, J., 2015. Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), pp.277-300.

Faccio, M., & Xu, J. (2015). Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), 277-300.

Keen, M., & Ligthart, J. E. (2016). Information sharing and international taxation: a primer.

International Tax and Public Finance, 13(1), 81-110.

Krever, R. (2013). Taming complexity in Australian income tax. Sydney L. Rev., 25, 467.

Larrimore, J., Burkhauser, R. V., Auten, G., & Armour, P. (2016). Recent trends in US top

income shares in tax record data using more comprehensive measures of income

including accrued capital gains (No. w23007). National Bureau of Economic Research.

Llamas, L., Araar, A., & Huesca, L. (2017). Income redistribution and inequality in the Mexican

tax-benefit system. Cuadernos de Economía, 36(SPE72), 301-325.

10

Tax Implication on the company` 11 | P a g e

López, R. E., Figueroa, E., & Gutiérrez, P. (2016). Fundamental accrued capital gains and the

measurement of top incomes: An application to Chile. The Journal of Economic

Inequality, 14(4), 379-394.

Modigliani, F., & Miller, M. H. (2013). Corporate income taxes and the cost of capital: a

correction. The American economic review, 53(3), 433-443.

Niemirowski, P., Baldwin, S., & Wearing, A. J. (2013). Tax related behaviours, beliefs, attitudes

and values and taxpayer compliance in Australia. J. Austl. Tax'n, 6, 132.

Seim, D. (2017). Behavioral responses to wealth taxes: Evidence from Sweden. American

Economic Journal: Economic Policy, 9(4), 395-421.

11

López, R. E., Figueroa, E., & Gutiérrez, P. (2016). Fundamental accrued capital gains and the

measurement of top incomes: An application to Chile. The Journal of Economic

Inequality, 14(4), 379-394.

Modigliani, F., & Miller, M. H. (2013). Corporate income taxes and the cost of capital: a

correction. The American economic review, 53(3), 433-443.

Niemirowski, P., Baldwin, S., & Wearing, A. J. (2013). Tax related behaviours, beliefs, attitudes

and values and taxpayer compliance in Australia. J. Austl. Tax'n, 6, 132.

Seim, D. (2017). Behavioral responses to wealth taxes: Evidence from Sweden. American

Economic Journal: Economic Policy, 9(4), 395-421.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.