HI6028 Taxation Theory, Practice & Law Assignment Solution

VerifiedAdded on 2023/06/03

|13

|2792

|335

Homework Assignment

AI Summary

This assignment solution addresses a taxation problem faced by a tax consultant. The client, an investor and antique collector, sold several assets during the tax year 2017/2018. The assignment analyzes the capital gains tax (CGT) implications of selling vacant land, an antique bed, shares, a painting (pre-CGT asset), and a violin (personal use asset). It determines the appropriate CGT events, cost bases, and application of relevant tax rulings and concessions. The solution also covers fringe benefits tax (FBT), specifically car fringe benefits and loan fringe benefits provided to an employee, calculating the taxable value and FBT implications. The assignment provides a detailed analysis of the tax implications of these transactions, including relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997) and the Fringe Benefits Tax Assessment Act 1986 (FBTAA), offering a comprehensive guide to understanding these complex tax scenarios.

Taxation Theory, Practice & Law

[Pick the date]

STUDENT NAME/ID;STUDENT NAME

[Pick the date]

STUDENT NAME/ID;STUDENT NAME

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

As per the situation presented, there is a client who has sold certain assets in the tax year

2017/2018. The aim is to offer consultation to this client with regards to the potential tax

implications that may arise on account of these transactions particularly with regards to capital

gains or capital losses that are realised from asset sale. It is imperative to note that the possibility

of the receipts being treated as revenue has been eliminated taking into consideration that the

client does not run any business where there is any trading in any of the given assets. This

essentially hints that the proceeds from the sale of assets would be capital and the only CGT

(Capital Gains Tax) would imply on the potential gains or losses realised in the process of

liquidation.

Liquidation of Vacant land

The first critical aspect is to highlight if the given asset falls within the ambit of pre-CGT asset or

not. This question becomes vital owing to the presence of s. 149-10 ITAA 1997 which allows

complete exemption from CGT liability (Barkoczy, 2017). In order to qualify as a pre-CGT

asset, the central condition is the acquisition date to be September 19, 1985 or before and not

after this date. The land block fails to satisfy the pre-CGT asset qualification criterion and hence

would be eligible for application of CGT.

The second aspect is to indicate the appropriate CGT event which is triggered by the decision to

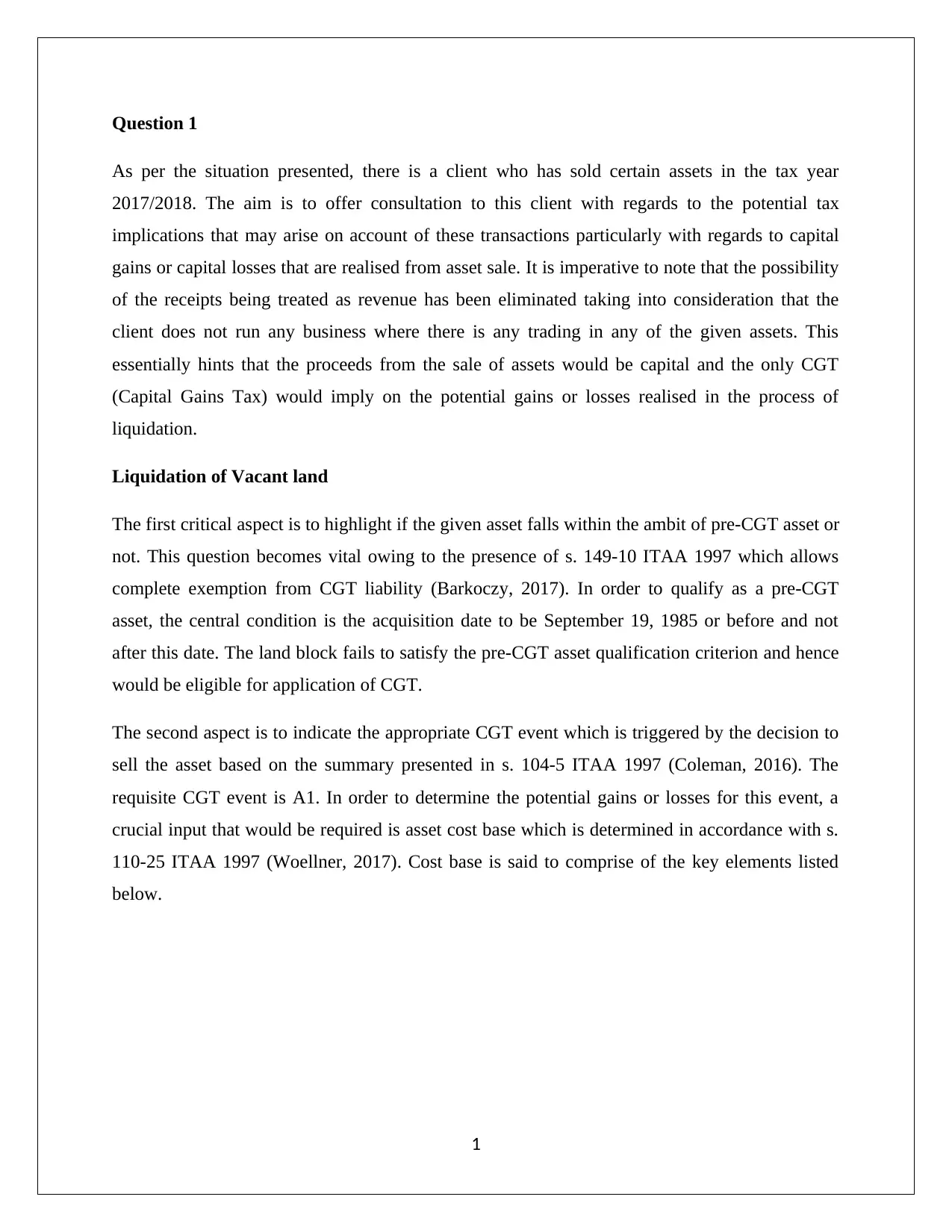

sell the asset based on the summary presented in s. 104-5 ITAA 1997 (Coleman, 2016). The

requisite CGT event is A1. In order to determine the potential gains or losses for this event, a

crucial input that would be required is asset cost base which is determined in accordance with s.

110-25 ITAA 1997 (Woellner, 2017). Cost base is said to comprise of the key elements listed

below.

1

As per the situation presented, there is a client who has sold certain assets in the tax year

2017/2018. The aim is to offer consultation to this client with regards to the potential tax

implications that may arise on account of these transactions particularly with regards to capital

gains or capital losses that are realised from asset sale. It is imperative to note that the possibility

of the receipts being treated as revenue has been eliminated taking into consideration that the

client does not run any business where there is any trading in any of the given assets. This

essentially hints that the proceeds from the sale of assets would be capital and the only CGT

(Capital Gains Tax) would imply on the potential gains or losses realised in the process of

liquidation.

Liquidation of Vacant land

The first critical aspect is to highlight if the given asset falls within the ambit of pre-CGT asset or

not. This question becomes vital owing to the presence of s. 149-10 ITAA 1997 which allows

complete exemption from CGT liability (Barkoczy, 2017). In order to qualify as a pre-CGT

asset, the central condition is the acquisition date to be September 19, 1985 or before and not

after this date. The land block fails to satisfy the pre-CGT asset qualification criterion and hence

would be eligible for application of CGT.

The second aspect is to indicate the appropriate CGT event which is triggered by the decision to

sell the asset based on the summary presented in s. 104-5 ITAA 1997 (Coleman, 2016). The

requisite CGT event is A1. In order to determine the potential gains or losses for this event, a

crucial input that would be required is asset cost base which is determined in accordance with s.

110-25 ITAA 1997 (Woellner, 2017). Cost base is said to comprise of the key elements listed

below.

1

Considering the facts related to sale of land, a pertinent issue arises which deals with land being

sold in the current tax year with receipts expected in the next year. In such a situation, a potential

issue arises in relation to timing of taxation. Tax ruling TR 94/29 opines in this matter that the

relevant tax treatment in case of sale of asset ought to be carried out when the contract for the

asset sale has been executed even though there may be a time delay in receipt of associated cash

(Coleman, 2016). Further, s. 102-5 ITAA 1997 requires that any capital gains that arise in

current year or accumulated from previous year need to be neutralised against the capital gains.

Concessions are provided in terms of capital gains as per s. 115-25 which allows a 50%

reduction in long term capital gains. It is imperative to understand that long term capital gains

are associated with assets with a holding period higher than one year (Wilmot, 2014).

The CGT implications arising on the land block owing to sale would be considered in the givn3e

tax year only as per TR 94/29 (Barkoczy, 2017). Also, the gains realised on this asset are long

term which makes the asset eligible for deduction under s. 115-25 as highlighted below.

2

sold in the current tax year with receipts expected in the next year. In such a situation, a potential

issue arises in relation to timing of taxation. Tax ruling TR 94/29 opines in this matter that the

relevant tax treatment in case of sale of asset ought to be carried out when the contract for the

asset sale has been executed even though there may be a time delay in receipt of associated cash

(Coleman, 2016). Further, s. 102-5 ITAA 1997 requires that any capital gains that arise in

current year or accumulated from previous year need to be neutralised against the capital gains.

Concessions are provided in terms of capital gains as per s. 115-25 which allows a 50%

reduction in long term capital gains. It is imperative to understand that long term capital gains

are associated with assets with a holding period higher than one year (Wilmot, 2014).

The CGT implications arising on the land block owing to sale would be considered in the givn3e

tax year only as per TR 94/29 (Barkoczy, 2017). Also, the gains realised on this asset are long

term which makes the asset eligible for deduction under s. 115-25 as highlighted below.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Liquidation of Antique bed

Antique belongs to the sub-category of collectable as is apparent from s. 118-10 which defines

these assets. As per this section, for CGT to be levied on these assets a necessary condition is

that the asset procurement price (also called buying price) must exceed $ 500. The antique bed

has complied with this necessary condition besides being purchased after levying of CGT and

therefore would be considered for CGT consequences based on the relevant information. The

disposal of bed leads to A1 CGT event and need to compute the cost base of the bed which

would comprise of the cost undertaken for value improvement through mattresses.

Also, the client has not engaged in transaction of sale of bed but the same has been stolen. Hence

the realised proceeds comprise of the money that has been obtained from insurance despite the

actual market value being higher. Additionally, the holding period of this asset is sufficiently

long so as to warrant a 50% discount on the capital gains in line with s. 115-25 ITAA 1997 as

highlighted below.

3

Antique belongs to the sub-category of collectable as is apparent from s. 118-10 which defines

these assets. As per this section, for CGT to be levied on these assets a necessary condition is

that the asset procurement price (also called buying price) must exceed $ 500. The antique bed

has complied with this necessary condition besides being purchased after levying of CGT and

therefore would be considered for CGT consequences based on the relevant information. The

disposal of bed leads to A1 CGT event and need to compute the cost base of the bed which

would comprise of the cost undertaken for value improvement through mattresses.

Also, the client has not engaged in transaction of sale of bed but the same has been stolen. Hence

the realised proceeds comprise of the money that has been obtained from insurance despite the

actual market value being higher. Additionally, the holding period of this asset is sufficiently

long so as to warrant a 50% discount on the capital gains in line with s. 115-25 ITAA 1997 as

highlighted below.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Liquidation of Painting

The critical aspect is to highlight if the given asset falls within the ambit of pre-CGT asset or not.

This question becomes vital owing to the presence of s. 149-10 ITAA 1997 which allows

complete exemption from CGT liability (Reuters, 2017). In order to qualify as a pre-CGT asset,

the central condition is the acquisition date to be September 19, 1985 or before and not after this

date. The painting asset succeeds to satisfy the pre-CGT asset qualification criterion and hence

would be eligible for exemption of CGT (Sadiq, et.al., 2015). Hence, no CGT consequence for

client on painting related proceeds.

Liquidation of Shares

The share purchase for the various companies has been done after the levying of CGT and

therefore none of the shares fail to comply with the definition of pre-CGT asset. Besides, CGT

event A1 is triggered by the share sale and hence in order to derive the underlying capital gains

or capital losses, information about the cost base of these shares need computation as per s. 110-

25 (Reuters, 2017). The discount method highlighted as per s. 115-25 would be applied for the

shares of those companies which have been held by the client for a period in excess of one year.

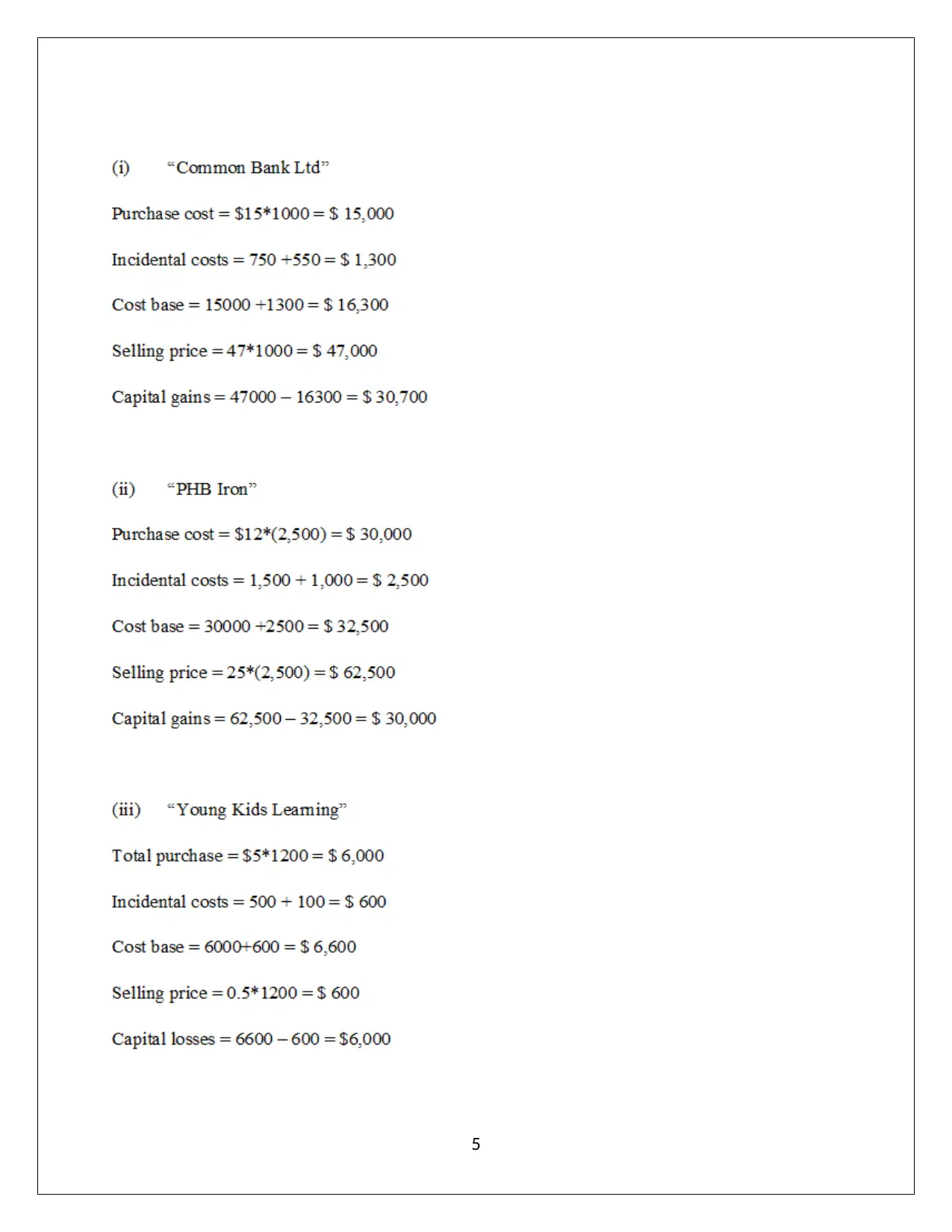

The computation of the capital gains derived on each of the shares in accordance with the

methodology prescribed by the A1 capital event is exhibited below (Sadiq, et.al., 2015).

4

The critical aspect is to highlight if the given asset falls within the ambit of pre-CGT asset or not.

This question becomes vital owing to the presence of s. 149-10 ITAA 1997 which allows

complete exemption from CGT liability (Reuters, 2017). In order to qualify as a pre-CGT asset,

the central condition is the acquisition date to be September 19, 1985 or before and not after this

date. The painting asset succeeds to satisfy the pre-CGT asset qualification criterion and hence

would be eligible for exemption of CGT (Sadiq, et.al., 2015). Hence, no CGT consequence for

client on painting related proceeds.

Liquidation of Shares

The share purchase for the various companies has been done after the levying of CGT and

therefore none of the shares fail to comply with the definition of pre-CGT asset. Besides, CGT

event A1 is triggered by the share sale and hence in order to derive the underlying capital gains

or capital losses, information about the cost base of these shares need computation as per s. 110-

25 (Reuters, 2017). The discount method highlighted as per s. 115-25 would be applied for the

shares of those companies which have been held by the client for a period in excess of one year.

The computation of the capital gains derived on each of the shares in accordance with the

methodology prescribed by the A1 capital event is exhibited below (Sadiq, et.al., 2015).

4

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

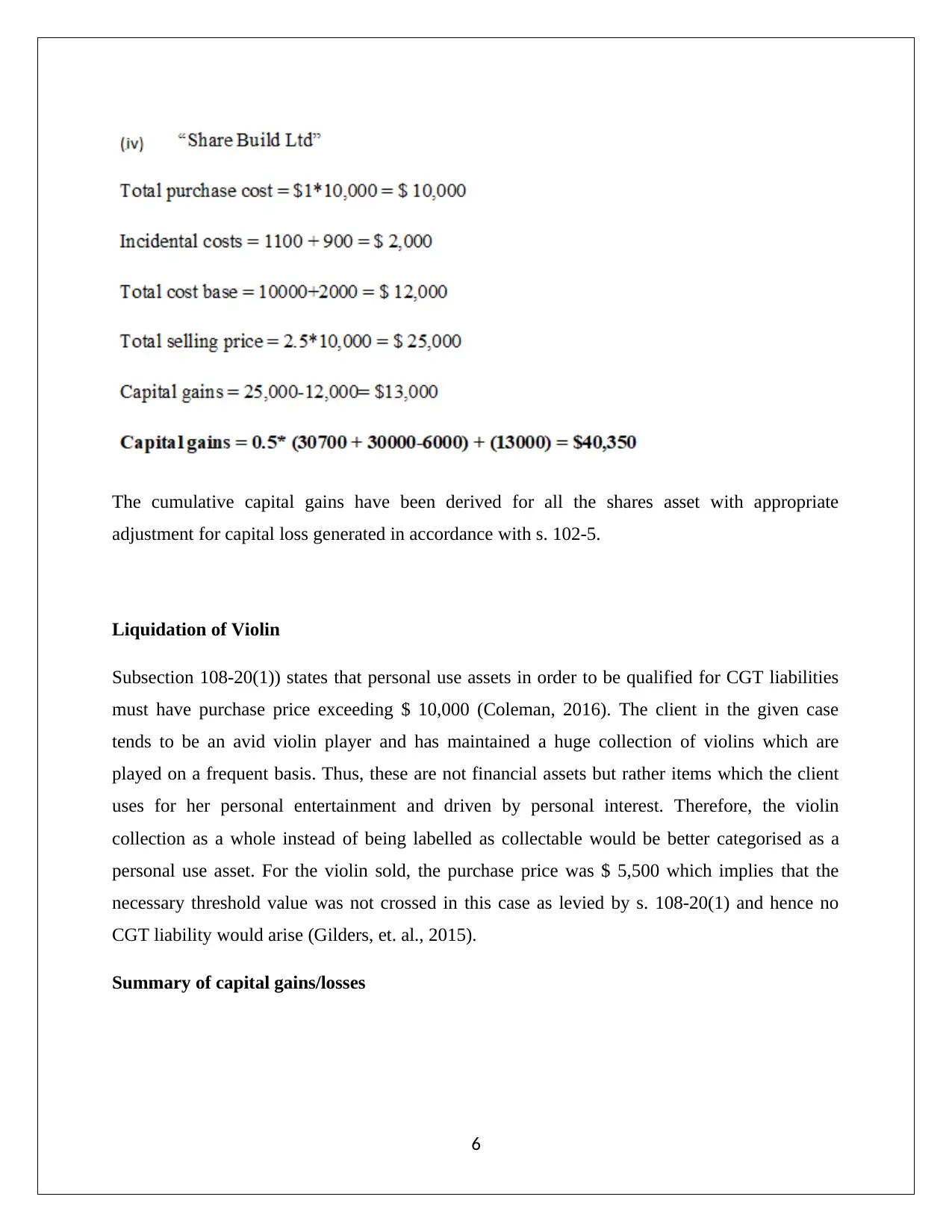

The cumulative capital gains have been derived for all the shares asset with appropriate

adjustment for capital loss generated in accordance with s. 102-5.

Liquidation of Violin

Subsection 108-20(1)) states that personal use assets in order to be qualified for CGT liabilities

must have purchase price exceeding $ 10,000 (Coleman, 2016). The client in the given case

tends to be an avid violin player and has maintained a huge collection of violins which are

played on a frequent basis. Thus, these are not financial assets but rather items which the client

uses for her personal entertainment and driven by personal interest. Therefore, the violin

collection as a whole instead of being labelled as collectable would be better categorised as a

personal use asset. For the violin sold, the purchase price was $ 5,500 which implies that the

necessary threshold value was not crossed in this case as levied by s. 108-20(1) and hence no

CGT liability would arise (Gilders, et. al., 2015).

Summary of capital gains/losses

6

adjustment for capital loss generated in accordance with s. 102-5.

Liquidation of Violin

Subsection 108-20(1)) states that personal use assets in order to be qualified for CGT liabilities

must have purchase price exceeding $ 10,000 (Coleman, 2016). The client in the given case

tends to be an avid violin player and has maintained a huge collection of violins which are

played on a frequent basis. Thus, these are not financial assets but rather items which the client

uses for her personal entertainment and driven by personal interest. Therefore, the violin

collection as a whole instead of being labelled as collectable would be better categorised as a

personal use asset. For the violin sold, the purchase price was $ 5,500 which implies that the

necessary threshold value was not crossed in this case as levied by s. 108-20(1) and hence no

CGT liability would arise (Gilders, et. al., 2015).

Summary of capital gains/losses

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is apparent from the above capital gains arising from individual assets that total taxable gains

for the client comes out as $139,100 for FY2018 which would be suitably levied CGT.

Question 2

(a) Potential non-cash personal benefits extended to employees are referred to as fringe benefits.

It is imperative to note that job related benefits such as car for office work does not constitute

as fringe benefit. For working out the tax implications of the benefit extended, there is a

dedicated tax law i.e. Fringe Benefits Tax Assessment Act 1986 (FBTAA). There is a need of

this separate tax law as the tax treatment of these benefits is different from the conventional

benefits under ITAA 1997 and ITAA 1936. Here, instead of taxing the benefit recipient, the

benefit provider is instead taxed. In wake of the given scenario, the fringe benefits

applicable are indicated below.

“Car Fringe Benefits”

A mandatory condition that ought to be fulfilled for the extension of car fringe benefits is that the

car that employer has provided the employee can be used for personal purpose by the employee.

Limiting the use of car only to professional purpose would not lead to car benefit extension in

accordance with s. 7 FBTAA 1986 (Gilders, et. al., 2015). Hence, the critical aspect of car fringe

benefit is personal use with/without the presence of professional use. The personal use might be

allowed by providing verbal or written permission (Krever, 2017). Alternately, the conduct of the

parties involved may also hint the presence of personal use. A key action in this regards is

parking of car at the garage located at the employee’s house or near the same where personal use

7

for the client comes out as $139,100 for FY2018 which would be suitably levied CGT.

Question 2

(a) Potential non-cash personal benefits extended to employees are referred to as fringe benefits.

It is imperative to note that job related benefits such as car for office work does not constitute

as fringe benefit. For working out the tax implications of the benefit extended, there is a

dedicated tax law i.e. Fringe Benefits Tax Assessment Act 1986 (FBTAA). There is a need of

this separate tax law as the tax treatment of these benefits is different from the conventional

benefits under ITAA 1997 and ITAA 1936. Here, instead of taxing the benefit recipient, the

benefit provider is instead taxed. In wake of the given scenario, the fringe benefits

applicable are indicated below.

“Car Fringe Benefits”

A mandatory condition that ought to be fulfilled for the extension of car fringe benefits is that the

car that employer has provided the employee can be used for personal purpose by the employee.

Limiting the use of car only to professional purpose would not lead to car benefit extension in

accordance with s. 7 FBTAA 1986 (Gilders, et. al., 2015). Hence, the critical aspect of car fringe

benefit is personal use with/without the presence of professional use. The personal use might be

allowed by providing verbal or written permission (Krever, 2017). Alternately, the conduct of the

parties involved may also hint the presence of personal use. A key action in this regards is

parking of car at the garage located at the employee’s house or near the same where personal use

7

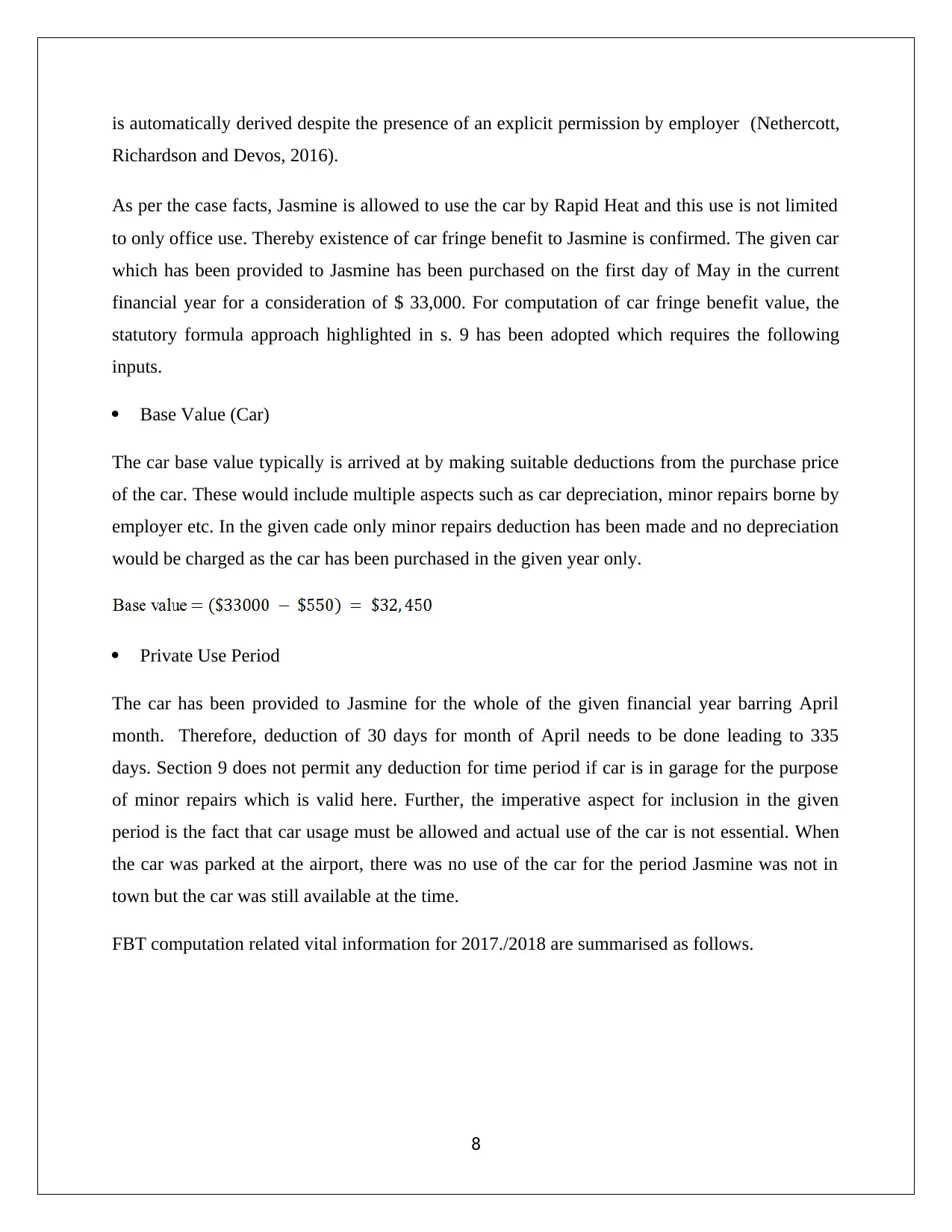

is automatically derived despite the presence of an explicit permission by employer (Nethercott,

Richardson and Devos, 2016).

As per the case facts, Jasmine is allowed to use the car by Rapid Heat and this use is not limited

to only office use. Thereby existence of car fringe benefit to Jasmine is confirmed. The given car

which has been provided to Jasmine has been purchased on the first day of May in the current

financial year for a consideration of $ 33,000. For computation of car fringe benefit value, the

statutory formula approach highlighted in s. 9 has been adopted which requires the following

inputs.

Base Value (Car)

The car base value typically is arrived at by making suitable deductions from the purchase price

of the car. These would include multiple aspects such as car depreciation, minor repairs borne by

employer etc. In the given cade only minor repairs deduction has been made and no depreciation

would be charged as the car has been purchased in the given year only.

Private Use Period

The car has been provided to Jasmine for the whole of the given financial year barring April

month. Therefore, deduction of 30 days for month of April needs to be done leading to 335

days. Section 9 does not permit any deduction for time period if car is in garage for the purpose

of minor repairs which is valid here. Further, the imperative aspect for inclusion in the given

period is the fact that car usage must be allowed and actual use of the car is not essential. When

the car was parked at the airport, there was no use of the car for the period Jasmine was not in

town but the car was still available at the time.

FBT computation related vital information for 2017./2018 are summarised as follows.

8

Richardson and Devos, 2016).

As per the case facts, Jasmine is allowed to use the car by Rapid Heat and this use is not limited

to only office use. Thereby existence of car fringe benefit to Jasmine is confirmed. The given car

which has been provided to Jasmine has been purchased on the first day of May in the current

financial year for a consideration of $ 33,000. For computation of car fringe benefit value, the

statutory formula approach highlighted in s. 9 has been adopted which requires the following

inputs.

Base Value (Car)

The car base value typically is arrived at by making suitable deductions from the purchase price

of the car. These would include multiple aspects such as car depreciation, minor repairs borne by

employer etc. In the given cade only minor repairs deduction has been made and no depreciation

would be charged as the car has been purchased in the given year only.

Private Use Period

The car has been provided to Jasmine for the whole of the given financial year barring April

month. Therefore, deduction of 30 days for month of April needs to be done leading to 335

days. Section 9 does not permit any deduction for time period if car is in garage for the purpose

of minor repairs which is valid here. Further, the imperative aspect for inclusion in the given

period is the fact that car usage must be allowed and actual use of the car is not essential. When

the car was parked at the airport, there was no use of the car for the period Jasmine was not in

town but the car was still available at the time.

FBT computation related vital information for 2017./2018 are summarised as follows.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

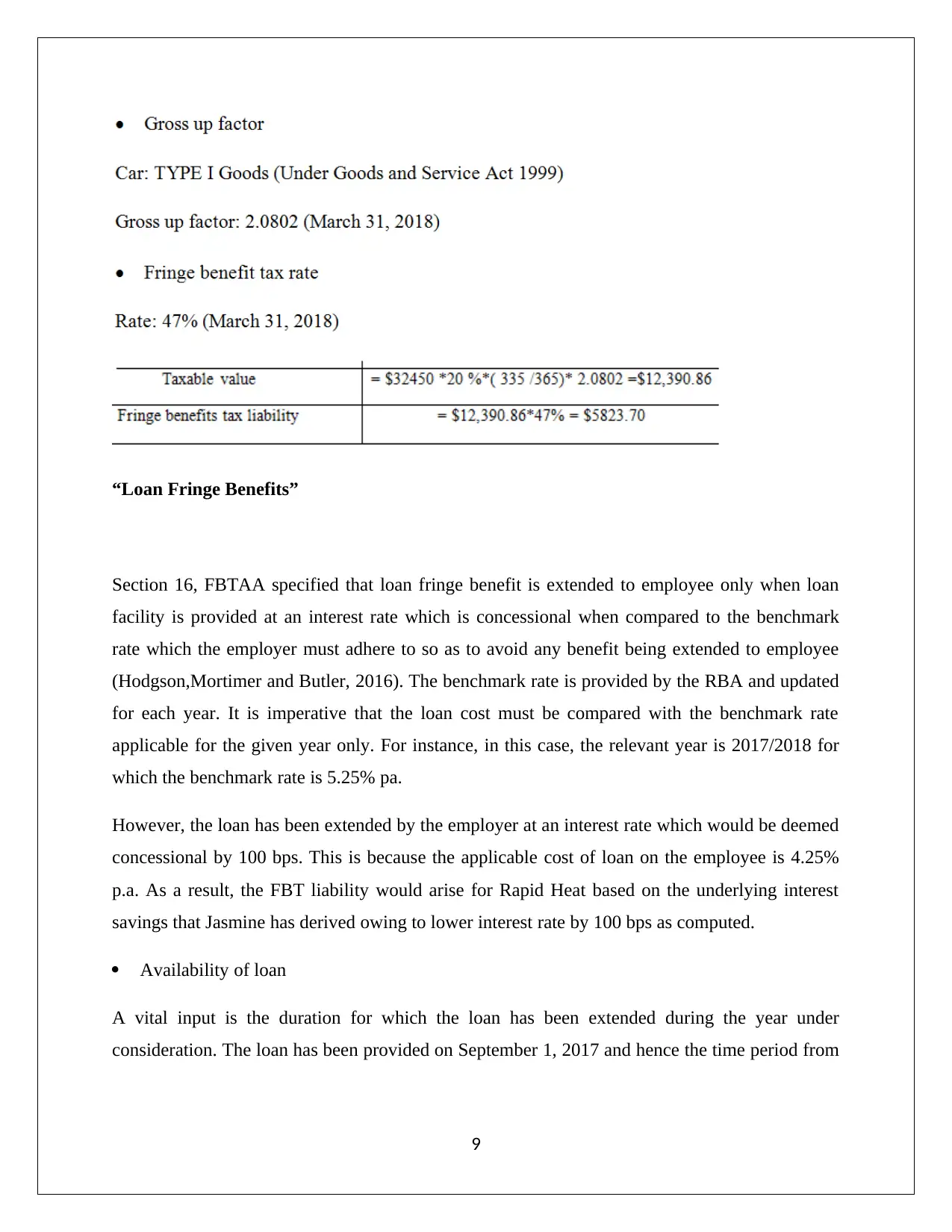

“Loan Fringe Benefits”

Section 16, FBTAA specified that loan fringe benefit is extended to employee only when loan

facility is provided at an interest rate which is concessional when compared to the benchmark

rate which the employer must adhere to so as to avoid any benefit being extended to employee

(Hodgson,Mortimer and Butler, 2016). The benchmark rate is provided by the RBA and updated

for each year. It is imperative that the loan cost must be compared with the benchmark rate

applicable for the given year only. For instance, in this case, the relevant year is 2017/2018 for

which the benchmark rate is 5.25% pa.

However, the loan has been extended by the employer at an interest rate which would be deemed

concessional by 100 bps. This is because the applicable cost of loan on the employee is 4.25%

p.a. As a result, the FBT liability would arise for Rapid Heat based on the underlying interest

savings that Jasmine has derived owing to lower interest rate by 100 bps as computed.

Availability of loan

A vital input is the duration for which the loan has been extended during the year under

consideration. The loan has been provided on September 1, 2017 and hence the time period from

9

Section 16, FBTAA specified that loan fringe benefit is extended to employee only when loan

facility is provided at an interest rate which is concessional when compared to the benchmark

rate which the employer must adhere to so as to avoid any benefit being extended to employee

(Hodgson,Mortimer and Butler, 2016). The benchmark rate is provided by the RBA and updated

for each year. It is imperative that the loan cost must be compared with the benchmark rate

applicable for the given year only. For instance, in this case, the relevant year is 2017/2018 for

which the benchmark rate is 5.25% pa.

However, the loan has been extended by the employer at an interest rate which would be deemed

concessional by 100 bps. This is because the applicable cost of loan on the employee is 4.25%

p.a. As a result, the FBT liability would arise for Rapid Heat based on the underlying interest

savings that Jasmine has derived owing to lower interest rate by 100 bps as computed.

Availability of loan

A vital input is the duration for which the loan has been extended during the year under

consideration. The loan has been provided on September 1, 2017 and hence the time period from

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

this date to the end of the financial year would be considered for computation as exhibited

below.

A crucial aspect is highlighted by s. 19, FBTAA is that potential deduction by employer may be

claimed if the use of the loan proceeds by employee is such that it leads to generation of

assessable income for the employee. However, this deduction rule does not provide any

deduction in tax for the use of loan proceeds by an associate of employee. The given details

highlight that $ 450,000 loan amount is utilised by Jasmine in the holiday home acquisition

which on not being used as a main residence is likely to be used for income generation. On the

other hand, the remainder money to the tune of $ 50,000 has been given to her husband for share

market investment. No deduction for Rapid Heat is possible on amount extended to Jasmine’s

husband despite income production.

“Expenses Fringe Benefits”

It is expected that employees would meet their own personal expenses. However, at times, the

employer tends help in this regards by paying for personal expenses (Krever, 2017). A special

case in this case arises if discount is provided by employer on an internally produced good

leading to the internal expense fringe benefit (Deutsch, et.al., 2015).

The scenario narrated reflects that the electric heater was available for $ 2,600 for any person

who wanted to purchase directly from the company i.e. Rapid Heat. However, the company

10

below.

A crucial aspect is highlighted by s. 19, FBTAA is that potential deduction by employer may be

claimed if the use of the loan proceeds by employee is such that it leads to generation of

assessable income for the employee. However, this deduction rule does not provide any

deduction in tax for the use of loan proceeds by an associate of employee. The given details

highlight that $ 450,000 loan amount is utilised by Jasmine in the holiday home acquisition

which on not being used as a main residence is likely to be used for income generation. On the

other hand, the remainder money to the tune of $ 50,000 has been given to her husband for share

market investment. No deduction for Rapid Heat is possible on amount extended to Jasmine’s

husband despite income production.

“Expenses Fringe Benefits”

It is expected that employees would meet their own personal expenses. However, at times, the

employer tends help in this regards by paying for personal expenses (Krever, 2017). A special

case in this case arises if discount is provided by employer on an internally produced good

leading to the internal expense fringe benefit (Deutsch, et.al., 2015).

The scenario narrated reflects that the electric heater was available for $ 2,600 for any person

who wanted to purchase directly from the company i.e. Rapid Heat. However, the company

10

provides the same heater for $ 1,300 to Jasmine which implies that the remaining expense has

been borne by the employer resulting in expense fringe benefit.

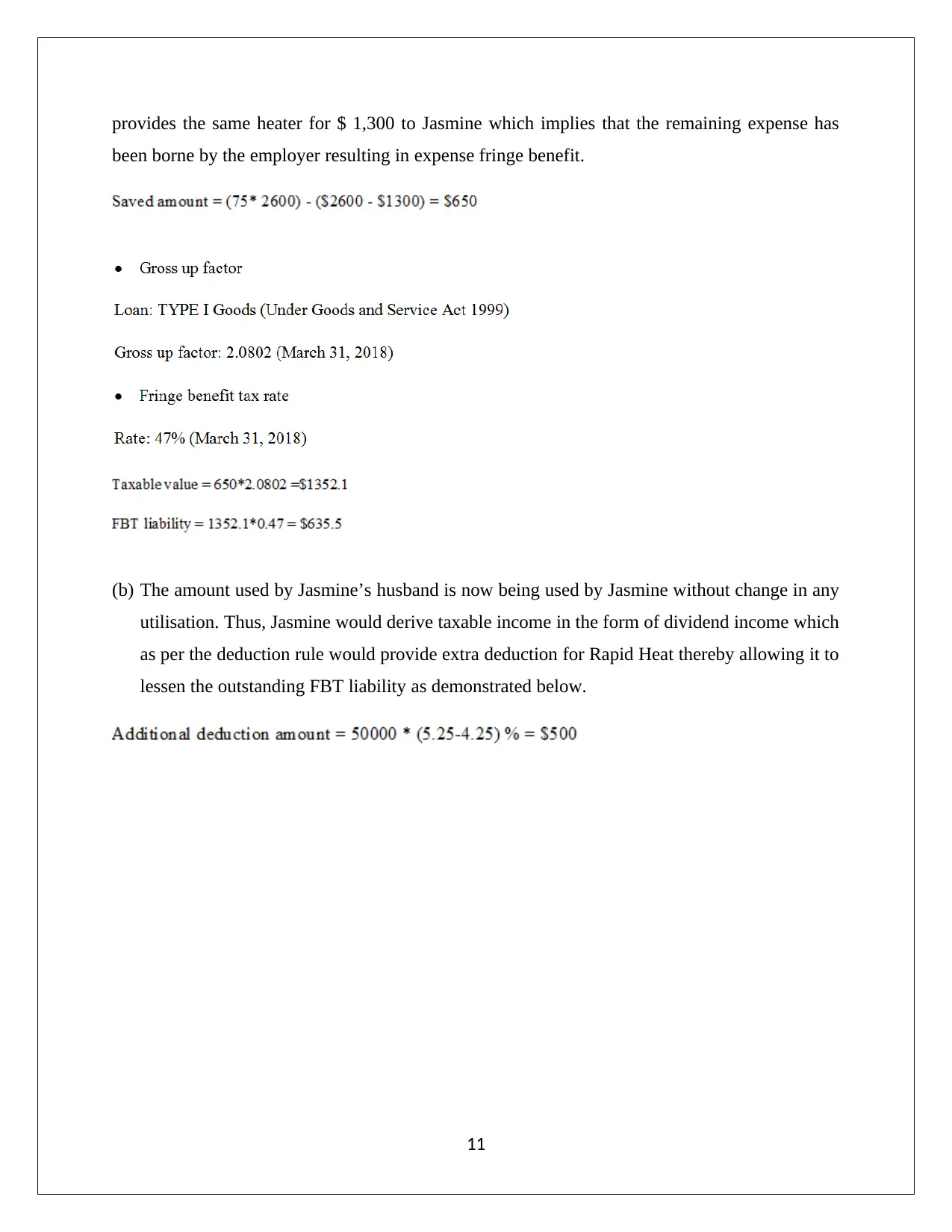

(b) The amount used by Jasmine’s husband is now being used by Jasmine without change in any

utilisation. Thus, Jasmine would derive taxable income in the form of dividend income which

as per the deduction rule would provide extra deduction for Rapid Heat thereby allowing it to

lessen the outstanding FBT liability as demonstrated below.

11

been borne by the employer resulting in expense fringe benefit.

(b) The amount used by Jasmine’s husband is now being used by Jasmine without change in any

utilisation. Thus, Jasmine would derive taxable income in the form of dividend income which

as per the deduction rule would provide extra deduction for Rapid Heat thereby allowing it to

lessen the outstanding FBT liability as demonstrated below.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.