Taxation Law Report: Analyzing Tax Implications of Business Sale

VerifiedAdded on 2023/01/04

|6

|688

|24

Report

AI Summary

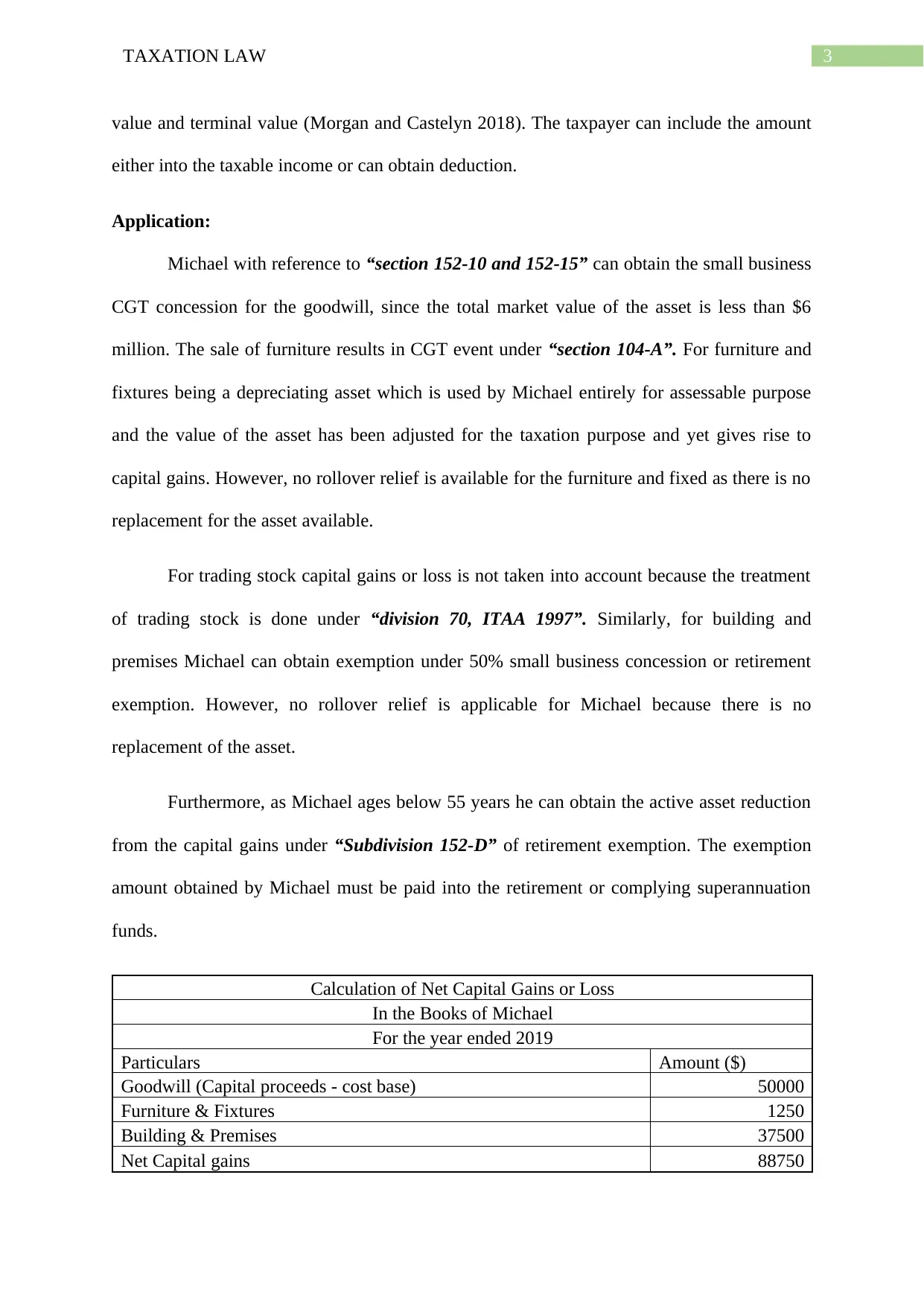

This report analyzes the tax consequences of Michael's mechanical workshop sale, addressing the implications of capital gains tax (CGT) and small business CGT concessions. The report examines the sale of goodwill, fittings and fixtures, trading stock, and building premises, considering their respective tax treatments under Australian taxation law. It assesses Michael's eligibility for various exemptions, including the 15-year exemption, 50% CGT reduction, and retirement exemption, based on the provided market values, adjusted values, and cost bases of the assets. The analysis includes calculations of net capital gains or losses for each asset and concludes with recommendations regarding potential tax savings and compliance with relevant tax regulations. The report references key sections of the Income Tax Assessment Act 1997 and ATO guidelines to support its findings.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.