Tax Implications of Investment Companies Under Singapore Law

VerifiedAdded on 2023/06/15

|10

|2200

|339

Report

AI Summary

This report examines the tax implications for investment holding and investment dealing companies operating in Singapore, highlighting differences in deductibility of expenses, capital allowances, and business losses under the Singapore Income Tax Act (SITA) 1947. Investment holding companies primarily derive income from passive sources like interest, dividends, and rents, whereas dealing companies generate income from trading activities involving the purchase and sale of properties and shares. The report details how SITA sections 10(1)(a), 10E, 10(1)(f), and 10(1)(d) apply to these companies, including the treatment of dividend, interest, and rental income. It further discusses deductible expenses, capital allowances, and provides tax advice, ultimately recommending the investment dealing company structure due to its greater flexibility in trading activities, capital allowances, and tax exemptions for new companies.

Running Head: TAXATION

Taxation

Name of the student

Name of the university

Author note

Taxation

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION

Executive summary

The primary purpose of the report is to identify the tax implications of investment companies

which can be categorized into an investment holding company and an investment dealing

company. There are significant differences which are present in relation to the treatment of

capital allowance and business losses arising towards these companies which have been analyzed

in the report. The source through which an investment holding company derives its income is

primarily passive in nature such as interest, dividends and rents on held properties and shares. On

the other hand a dealing company derives its income from trade activities such as purchase and

sale of properties and shares owned by it. There are also differences in relation to the deduction

of expenses from the taxable income of both the companies. The restrictions on deductibility of

such expenses are less on a dealing company as compared to a holding company. Thus these

factors needs to be considered while selecting one of the business structures towards an

investment business.

TAXATION

Executive summary

The primary purpose of the report is to identify the tax implications of investment companies

which can be categorized into an investment holding company and an investment dealing

company. There are significant differences which are present in relation to the treatment of

capital allowance and business losses arising towards these companies which have been analyzed

in the report. The source through which an investment holding company derives its income is

primarily passive in nature such as interest, dividends and rents on held properties and shares. On

the other hand a dealing company derives its income from trade activities such as purchase and

sale of properties and shares owned by it. There are also differences in relation to the deduction

of expenses from the taxable income of both the companies. The restrictions on deductibility of

such expenses are less on a dealing company as compared to a holding company. Thus these

factors needs to be considered while selecting one of the business structures towards an

investment business.

2

TAXATION

Table of Contents

Introduction......................................................................................................................................2

Application of the SITA on the companies.....................................................................................2

Dividend Income (10)(1)(d).........................................................................................................3

Interest Income 10 (1)(d).............................................................................................................4

Rental income 10(1)(f).................................................................................................................4

Deductible expenses........................................................................................................................5

Capital allowance.............................................................................................................................6

Tax advice on both the structure......................................................................................................7

Summary..........................................................................................................................................7

References........................................................................................................................................8

TAXATION

Table of Contents

Introduction......................................................................................................................................2

Application of the SITA on the companies.....................................................................................2

Dividend Income (10)(1)(d).........................................................................................................3

Interest Income 10 (1)(d).............................................................................................................4

Rental income 10(1)(f).................................................................................................................4

Deductible expenses........................................................................................................................5

Capital allowance.............................................................................................................................6

Tax advice on both the structure......................................................................................................7

Summary..........................................................................................................................................7

References........................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION

Introduction

This paper deals with provisions in relation to the tax implications which are imposed in

an investment holding company and an investment dealing company operating in Singapore. The

tax implications on both the companies are different in relation to the deductibility of expenses,

capital allowance and business losses. These are governed through the provisions of the

Singapore Income Tax Act 1947. Primary difference between an investment holding company

and an investment dealing company are that a holding company primarily derives it income from

passive income sources and dealing company derives its income from direct income sources

(Dyreng, Hoopes & Wilde, 2016). This is because an investment holding company is the owner

of investments like shares and properties on long term basis and gets investment income such as

rental, dividend or interest income. The basic purpose of such company is holding investment.

On the other hand an investment dealing company also holds investments in form of shares and

property however they are treated as a trading stock and income is derived by selling and

purchasing such investments (TAX@SG, 2018).

Application of the SITA on the companies

The SITA is the primary legislation which deals with provisions in relation of

computation of tax towards these companies. This section of the report deals with the

implications of subsection 10 (1)(a), 10E, 10(1)(f) and 10(1)(d) on these companies in relation to

their tax implications. In relation to an IH company income tax is payable on incomes which

have accrued or been derived from Singapore or income which have been attained from outside

Singapore in Singapore such as income from foreign received in Singapore. The major form of

income which is gained by a IH are dividends and interest dealt by s10 (1)(d) and Rental income

TAXATION

Introduction

This paper deals with provisions in relation to the tax implications which are imposed in

an investment holding company and an investment dealing company operating in Singapore. The

tax implications on both the companies are different in relation to the deductibility of expenses,

capital allowance and business losses. These are governed through the provisions of the

Singapore Income Tax Act 1947. Primary difference between an investment holding company

and an investment dealing company are that a holding company primarily derives it income from

passive income sources and dealing company derives its income from direct income sources

(Dyreng, Hoopes & Wilde, 2016). This is because an investment holding company is the owner

of investments like shares and properties on long term basis and gets investment income such as

rental, dividend or interest income. The basic purpose of such company is holding investment.

On the other hand an investment dealing company also holds investments in form of shares and

property however they are treated as a trading stock and income is derived by selling and

purchasing such investments (TAX@SG, 2018).

Application of the SITA on the companies

The SITA is the primary legislation which deals with provisions in relation of

computation of tax towards these companies. This section of the report deals with the

implications of subsection 10 (1)(a), 10E, 10(1)(f) and 10(1)(d) on these companies in relation to

their tax implications. In relation to an IH company income tax is payable on incomes which

have accrued or been derived from Singapore or income which have been attained from outside

Singapore in Singapore such as income from foreign received in Singapore. The major form of

income which is gained by a IH are dividends and interest dealt by s10 (1)(d) and Rental income

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION

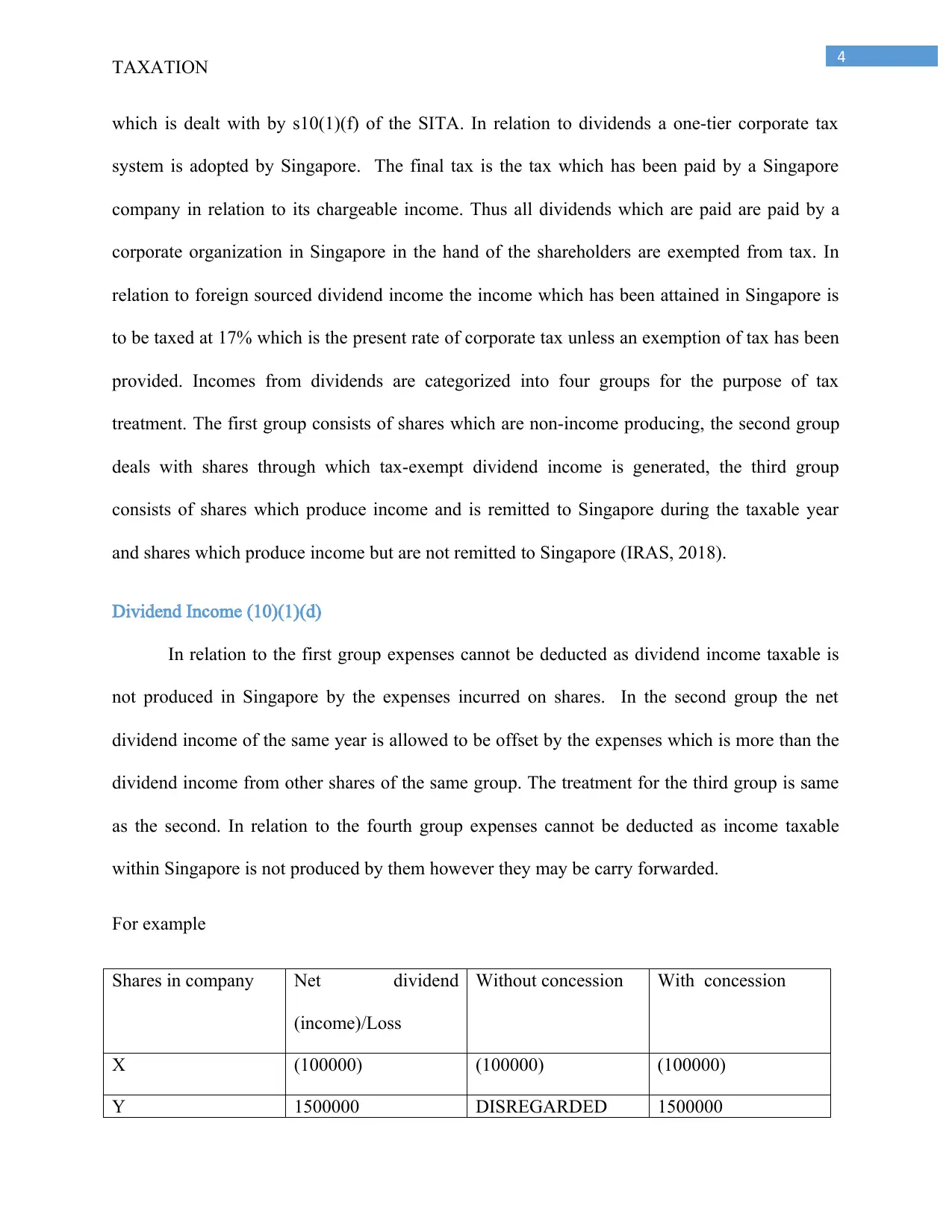

which is dealt with by s10(1)(f) of the SITA. In relation to dividends a one-tier corporate tax

system is adopted by Singapore. The final tax is the tax which has been paid by a Singapore

company in relation to its chargeable income. Thus all dividends which are paid are paid by a

corporate organization in Singapore in the hand of the shareholders are exempted from tax. In

relation to foreign sourced dividend income the income which has been attained in Singapore is

to be taxed at 17% which is the present rate of corporate tax unless an exemption of tax has been

provided. Incomes from dividends are categorized into four groups for the purpose of tax

treatment. The first group consists of shares which are non-income producing, the second group

deals with shares through which tax-exempt dividend income is generated, the third group

consists of shares which produce income and is remitted to Singapore during the taxable year

and shares which produce income but are not remitted to Singapore (IRAS, 2018).

Dividend Income (10)(1)(d)

In relation to the first group expenses cannot be deducted as dividend income taxable is

not produced in Singapore by the expenses incurred on shares. In the second group the net

dividend income of the same year is allowed to be offset by the expenses which is more than the

dividend income from other shares of the same group. The treatment for the third group is same

as the second. In relation to the fourth group expenses cannot be deducted as income taxable

within Singapore is not produced by them however they may be carry forwarded.

For example

Shares in company Net dividend

(income)/Loss

Without concession With concession

X (100000) (100000) (100000)

Y 1500000 DISREGARDED 1500000

TAXATION

which is dealt with by s10(1)(f) of the SITA. In relation to dividends a one-tier corporate tax

system is adopted by Singapore. The final tax is the tax which has been paid by a Singapore

company in relation to its chargeable income. Thus all dividends which are paid are paid by a

corporate organization in Singapore in the hand of the shareholders are exempted from tax. In

relation to foreign sourced dividend income the income which has been attained in Singapore is

to be taxed at 17% which is the present rate of corporate tax unless an exemption of tax has been

provided. Incomes from dividends are categorized into four groups for the purpose of tax

treatment. The first group consists of shares which are non-income producing, the second group

deals with shares through which tax-exempt dividend income is generated, the third group

consists of shares which produce income and is remitted to Singapore during the taxable year

and shares which produce income but are not remitted to Singapore (IRAS, 2018).

Dividend Income (10)(1)(d)

In relation to the first group expenses cannot be deducted as dividend income taxable is

not produced in Singapore by the expenses incurred on shares. In the second group the net

dividend income of the same year is allowed to be offset by the expenses which is more than the

dividend income from other shares of the same group. The treatment for the third group is same

as the second. In relation to the fourth group expenses cannot be deducted as income taxable

within Singapore is not produced by them however they may be carry forwarded.

For example

Shares in company Net dividend

(income)/Loss

Without concession With concession

X (100000) (100000) (100000)

Y 1500000 DISREGARDED 1500000

5

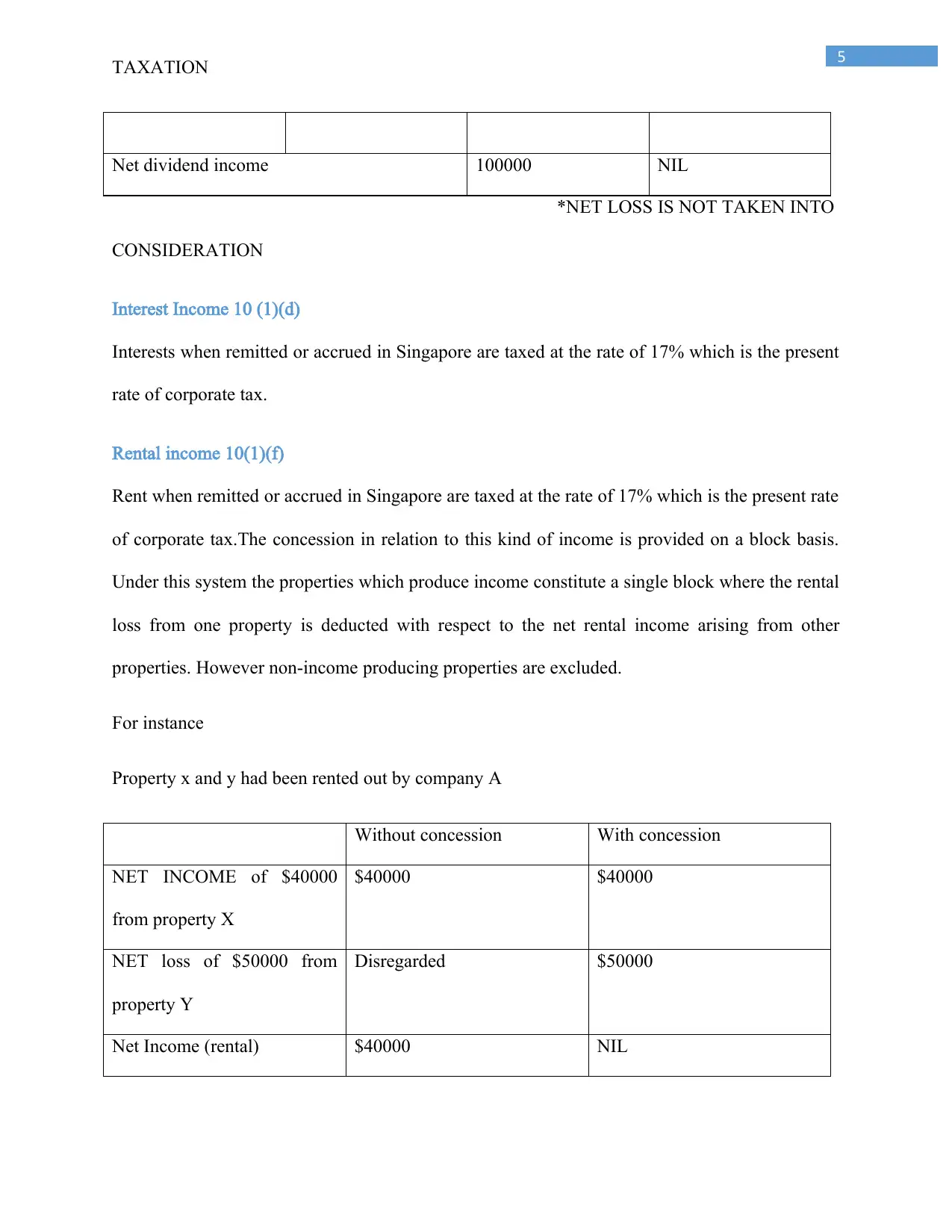

TAXATION

Net dividend income 100000 NIL

*NET LOSS IS NOT TAKEN INTO

CONSIDERATION

Interest Income 10 (1)(d)

Interests when remitted or accrued in Singapore are taxed at the rate of 17% which is the present

rate of corporate tax.

Rental income 10(1)(f)

Rent when remitted or accrued in Singapore are taxed at the rate of 17% which is the present rate

of corporate tax.The concession in relation to this kind of income is provided on a block basis.

Under this system the properties which produce income constitute a single block where the rental

loss from one property is deducted with respect to the net rental income arising from other

properties. However non-income producing properties are excluded.

For instance

Property x and y had been rented out by company A

Without concession With concession

NET INCOME of $40000

from property X

$40000 $40000

NET loss of $50000 from

property Y

Disregarded $50000

Net Income (rental) $40000 NIL

TAXATION

Net dividend income 100000 NIL

*NET LOSS IS NOT TAKEN INTO

CONSIDERATION

Interest Income 10 (1)(d)

Interests when remitted or accrued in Singapore are taxed at the rate of 17% which is the present

rate of corporate tax.

Rental income 10(1)(f)

Rent when remitted or accrued in Singapore are taxed at the rate of 17% which is the present rate

of corporate tax.The concession in relation to this kind of income is provided on a block basis.

Under this system the properties which produce income constitute a single block where the rental

loss from one property is deducted with respect to the net rental income arising from other

properties. However non-income producing properties are excluded.

For instance

Property x and y had been rented out by company A

Without concession With concession

NET INCOME of $40000

from property X

$40000 $40000

NET loss of $50000 from

property Y

Disregarded $50000

Net Income (rental) $40000 NIL

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION

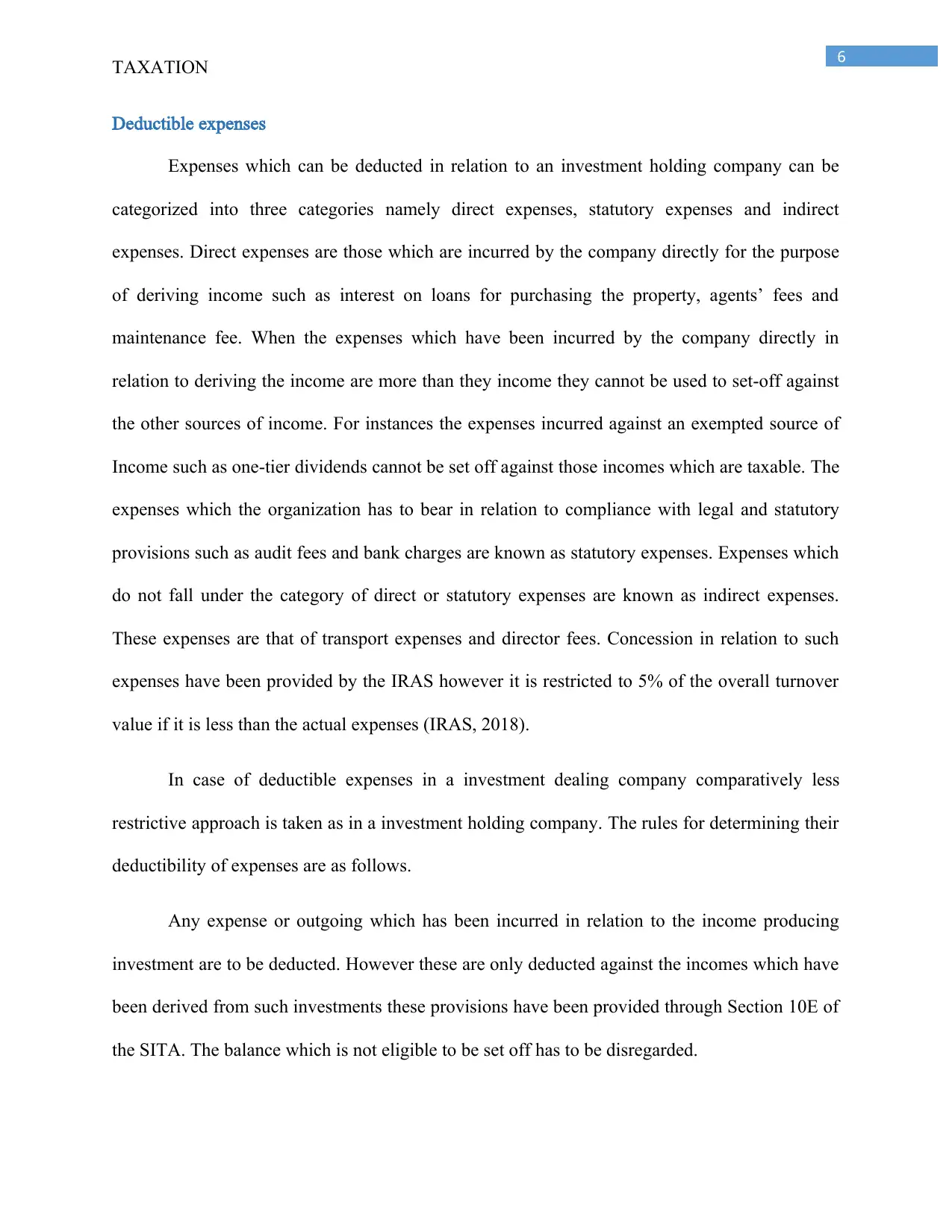

Deductible expenses

Expenses which can be deducted in relation to an investment holding company can be

categorized into three categories namely direct expenses, statutory expenses and indirect

expenses. Direct expenses are those which are incurred by the company directly for the purpose

of deriving income such as interest on loans for purchasing the property, agents’ fees and

maintenance fee. When the expenses which have been incurred by the company directly in

relation to deriving the income are more than they income they cannot be used to set-off against

the other sources of income. For instances the expenses incurred against an exempted source of

Income such as one-tier dividends cannot be set off against those incomes which are taxable. The

expenses which the organization has to bear in relation to compliance with legal and statutory

provisions such as audit fees and bank charges are known as statutory expenses. Expenses which

do not fall under the category of direct or statutory expenses are known as indirect expenses.

These expenses are that of transport expenses and director fees. Concession in relation to such

expenses have been provided by the IRAS however it is restricted to 5% of the overall turnover

value if it is less than the actual expenses (IRAS, 2018).

In case of deductible expenses in a investment dealing company comparatively less

restrictive approach is taken as in a investment holding company. The rules for determining their

deductibility of expenses are as follows.

Any expense or outgoing which has been incurred in relation to the income producing

investment are to be deducted. However these are only deducted against the incomes which have

been derived from such investments these provisions have been provided through Section 10E of

the SITA. The balance which is not eligible to be set off has to be disregarded.

TAXATION

Deductible expenses

Expenses which can be deducted in relation to an investment holding company can be

categorized into three categories namely direct expenses, statutory expenses and indirect

expenses. Direct expenses are those which are incurred by the company directly for the purpose

of deriving income such as interest on loans for purchasing the property, agents’ fees and

maintenance fee. When the expenses which have been incurred by the company directly in

relation to deriving the income are more than they income they cannot be used to set-off against

the other sources of income. For instances the expenses incurred against an exempted source of

Income such as one-tier dividends cannot be set off against those incomes which are taxable. The

expenses which the organization has to bear in relation to compliance with legal and statutory

provisions such as audit fees and bank charges are known as statutory expenses. Expenses which

do not fall under the category of direct or statutory expenses are known as indirect expenses.

These expenses are that of transport expenses and director fees. Concession in relation to such

expenses have been provided by the IRAS however it is restricted to 5% of the overall turnover

value if it is less than the actual expenses (IRAS, 2018).

In case of deductible expenses in a investment dealing company comparatively less

restrictive approach is taken as in a investment holding company. The rules for determining their

deductibility of expenses are as follows.

Any expense or outgoing which has been incurred in relation to the income producing

investment are to be deducted. However these are only deducted against the incomes which have

been derived from such investments these provisions have been provided through Section 10E of

the SITA. The balance which is not eligible to be set off has to be disregarded.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION

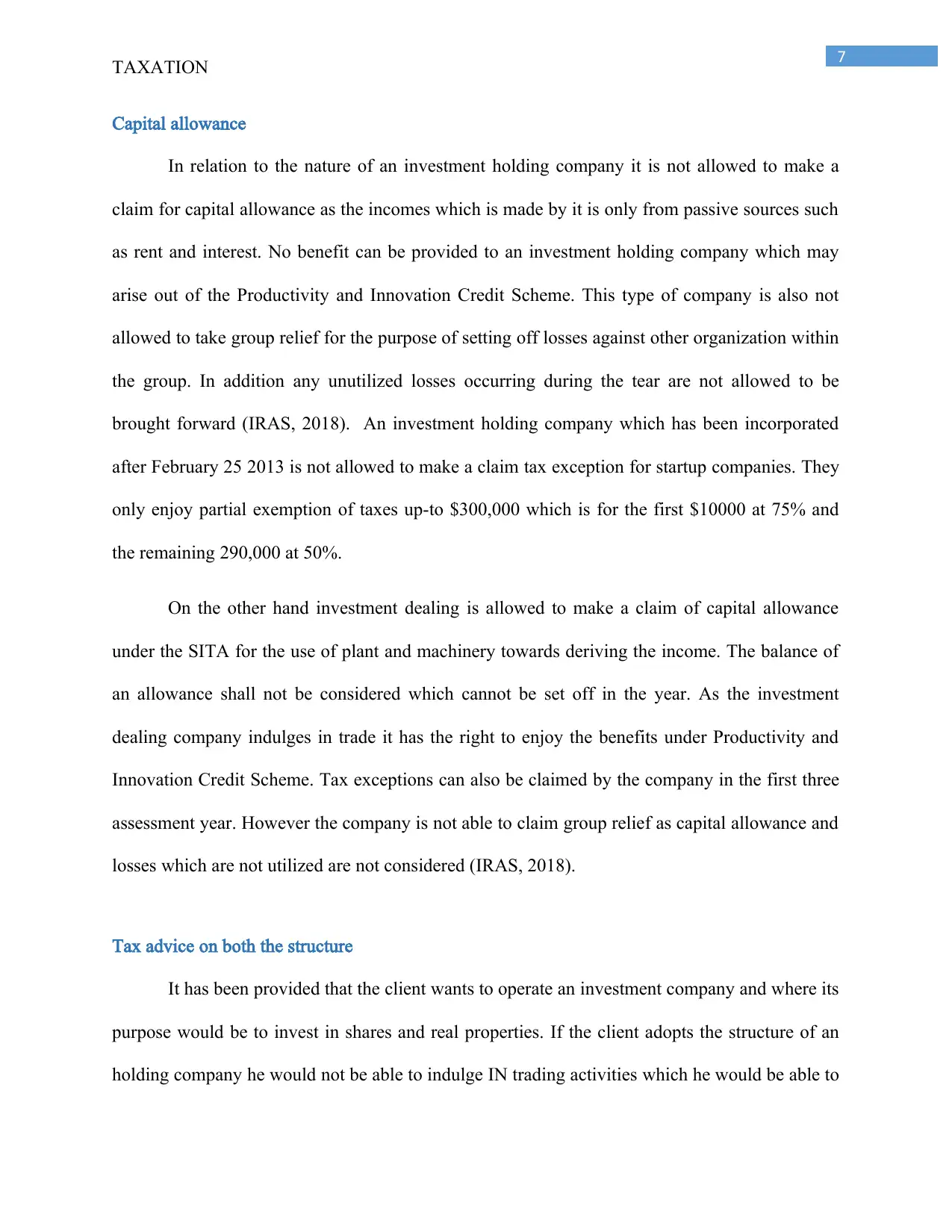

Capital allowance

In relation to the nature of an investment holding company it is not allowed to make a

claim for capital allowance as the incomes which is made by it is only from passive sources such

as rent and interest. No benefit can be provided to an investment holding company which may

arise out of the Productivity and Innovation Credit Scheme. This type of company is also not

allowed to take group relief for the purpose of setting off losses against other organization within

the group. In addition any unutilized losses occurring during the tear are not allowed to be

brought forward (IRAS, 2018). An investment holding company which has been incorporated

after February 25 2013 is not allowed to make a claim tax exception for startup companies. They

only enjoy partial exemption of taxes up-to $300,000 which is for the first $10000 at 75% and

the remaining 290,000 at 50%.

On the other hand investment dealing is allowed to make a claim of capital allowance

under the SITA for the use of plant and machinery towards deriving the income. The balance of

an allowance shall not be considered which cannot be set off in the year. As the investment

dealing company indulges in trade it has the right to enjoy the benefits under Productivity and

Innovation Credit Scheme. Tax exceptions can also be claimed by the company in the first three

assessment year. However the company is not able to claim group relief as capital allowance and

losses which are not utilized are not considered (IRAS, 2018).

Tax advice on both the structure

It has been provided that the client wants to operate an investment company and where its

purpose would be to invest in shares and real properties. If the client adopts the structure of an

holding company he would not be able to indulge IN trading activities which he would be able to

TAXATION

Capital allowance

In relation to the nature of an investment holding company it is not allowed to make a

claim for capital allowance as the incomes which is made by it is only from passive sources such

as rent and interest. No benefit can be provided to an investment holding company which may

arise out of the Productivity and Innovation Credit Scheme. This type of company is also not

allowed to take group relief for the purpose of setting off losses against other organization within

the group. In addition any unutilized losses occurring during the tear are not allowed to be

brought forward (IRAS, 2018). An investment holding company which has been incorporated

after February 25 2013 is not allowed to make a claim tax exception for startup companies. They

only enjoy partial exemption of taxes up-to $300,000 which is for the first $10000 at 75% and

the remaining 290,000 at 50%.

On the other hand investment dealing is allowed to make a claim of capital allowance

under the SITA for the use of plant and machinery towards deriving the income. The balance of

an allowance shall not be considered which cannot be set off in the year. As the investment

dealing company indulges in trade it has the right to enjoy the benefits under Productivity and

Innovation Credit Scheme. Tax exceptions can also be claimed by the company in the first three

assessment year. However the company is not able to claim group relief as capital allowance and

losses which are not utilized are not considered (IRAS, 2018).

Tax advice on both the structure

It has been provided that the client wants to operate an investment company and where its

purpose would be to invest in shares and real properties. If the client adopts the structure of an

holding company he would not be able to indulge IN trading activities which he would be able to

8

TAXATION

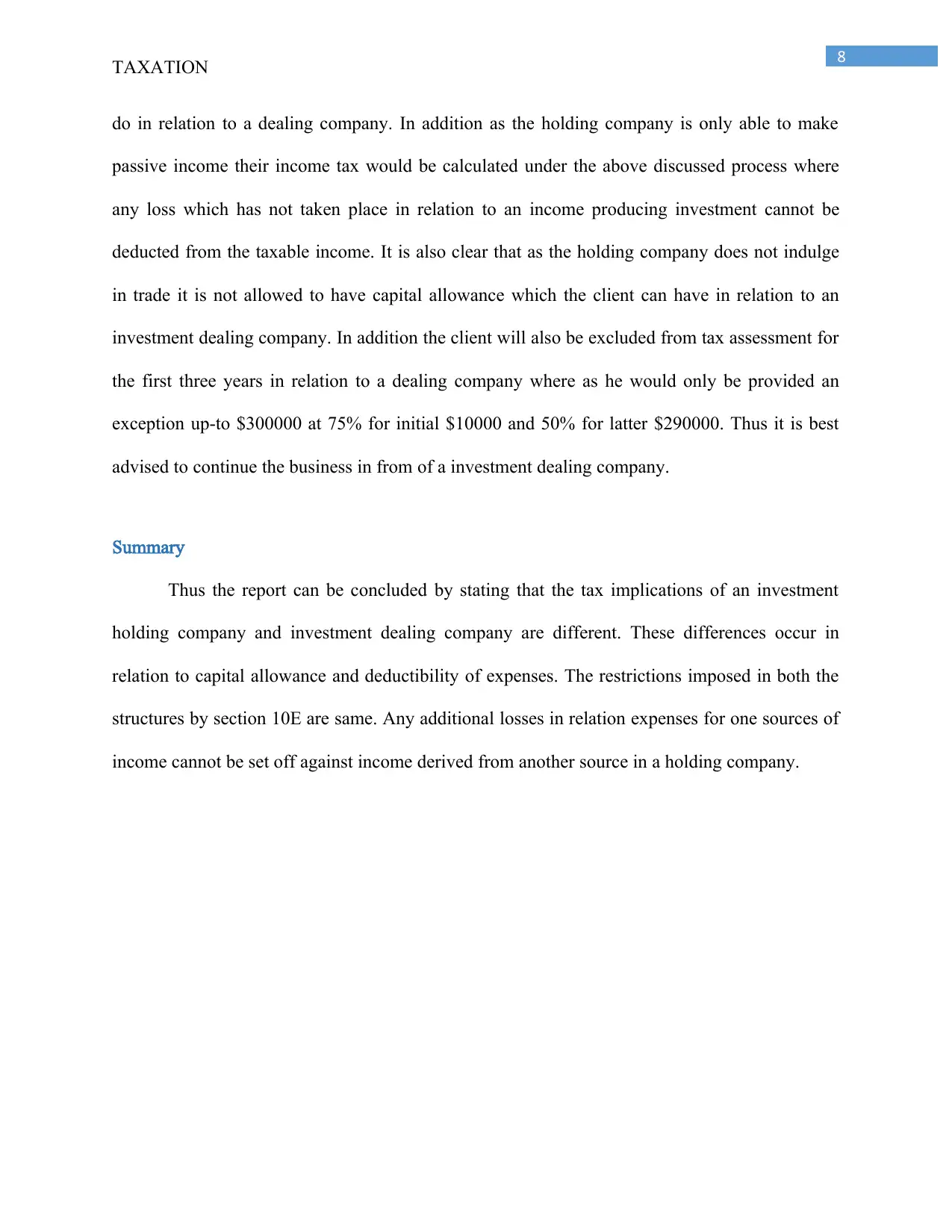

do in relation to a dealing company. In addition as the holding company is only able to make

passive income their income tax would be calculated under the above discussed process where

any loss which has not taken place in relation to an income producing investment cannot be

deducted from the taxable income. It is also clear that as the holding company does not indulge

in trade it is not allowed to have capital allowance which the client can have in relation to an

investment dealing company. In addition the client will also be excluded from tax assessment for

the first three years in relation to a dealing company where as he would only be provided an

exception up-to $300000 at 75% for initial $10000 and 50% for latter $290000. Thus it is best

advised to continue the business in from of a investment dealing company.

Summary

Thus the report can be concluded by stating that the tax implications of an investment

holding company and investment dealing company are different. These differences occur in

relation to capital allowance and deductibility of expenses. The restrictions imposed in both the

structures by section 10E are same. Any additional losses in relation expenses for one sources of

income cannot be set off against income derived from another source in a holding company.

TAXATION

do in relation to a dealing company. In addition as the holding company is only able to make

passive income their income tax would be calculated under the above discussed process where

any loss which has not taken place in relation to an income producing investment cannot be

deducted from the taxable income. It is also clear that as the holding company does not indulge

in trade it is not allowed to have capital allowance which the client can have in relation to an

investment dealing company. In addition the client will also be excluded from tax assessment for

the first three years in relation to a dealing company where as he would only be provided an

exception up-to $300000 at 75% for initial $10000 and 50% for latter $290000. Thus it is best

advised to continue the business in from of a investment dealing company.

Summary

Thus the report can be concluded by stating that the tax implications of an investment

holding company and investment dealing company are different. These differences occur in

relation to capital allowance and deductibility of expenses. The restrictions imposed in both the

structures by section 10E are same. Any additional losses in relation expenses for one sources of

income cannot be set off against income derived from another source in a holding company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION

References

Dyreng, S. D., Hoopes, J. L., & Wilde, J. H. (2016). Public pressure and corporate tax behavior.

Journal of Accounting Research, 54(1), 147-186.

Investment Holding Companies - IRAS. (2018). Iras.gov.sg. Retrieved 3 February 2018, from

https://www.iras.gov.sg/irashome/Businesses/Companies/Working-out-Corporate-

Income-Taxes/Specific-industries/Investment-Holding-Companies/

IRAS (2018). Iras.gov.sg. Retrieved 3 February 2018, from

https://www.iras.gov.sg/irashome/uploadedFiles/IRASHome/Businesses/Basic

%20Format%20of%20Tax%20Computation%20for%20an%20Investment%20Holding

%20Company.pdf

IRAS (2018). Retrieved 3 February 2018, from

https://www.iras.gov.sg/irashome/uploadedFiles/IRASHome/News_and_Events/Events/

Seminar%20on%20Taxation%20of%20Investment%20Holding%20Companies%202017

IRAS streamlines e-Tax Guides on “Ascertainment of income from business of making

investment” - TAX@SG. (2018). TAX@SG. Retrieved 3 February 2018, from

https://taxsg.com/2011/09/08/iras-streamlines-e-tax-guides-on-

%E2%80%9Cascertainment-of-income-from-business-of-making-investment

%E2%80%9D/

TAXATION

References

Dyreng, S. D., Hoopes, J. L., & Wilde, J. H. (2016). Public pressure and corporate tax behavior.

Journal of Accounting Research, 54(1), 147-186.

Investment Holding Companies - IRAS. (2018). Iras.gov.sg. Retrieved 3 February 2018, from

https://www.iras.gov.sg/irashome/Businesses/Companies/Working-out-Corporate-

Income-Taxes/Specific-industries/Investment-Holding-Companies/

IRAS (2018). Iras.gov.sg. Retrieved 3 February 2018, from

https://www.iras.gov.sg/irashome/uploadedFiles/IRASHome/Businesses/Basic

%20Format%20of%20Tax%20Computation%20for%20an%20Investment%20Holding

%20Company.pdf

IRAS (2018). Retrieved 3 February 2018, from

https://www.iras.gov.sg/irashome/uploadedFiles/IRASHome/News_and_Events/Events/

Seminar%20on%20Taxation%20of%20Investment%20Holding%20Companies%202017

IRAS streamlines e-Tax Guides on “Ascertainment of income from business of making

investment” - TAX@SG. (2018). TAX@SG. Retrieved 3 February 2018, from

https://taxsg.com/2011/09/08/iras-streamlines-e-tax-guides-on-

%E2%80%9Cascertainment-of-income-from-business-of-making-investment

%E2%80%9D/

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.