Tax Law: Income Tax, Medicare Levy, and Financial Income Calculations

VerifiedAdded on 2020/05/28

|9

|988

|57

Homework Assignment

AI Summary

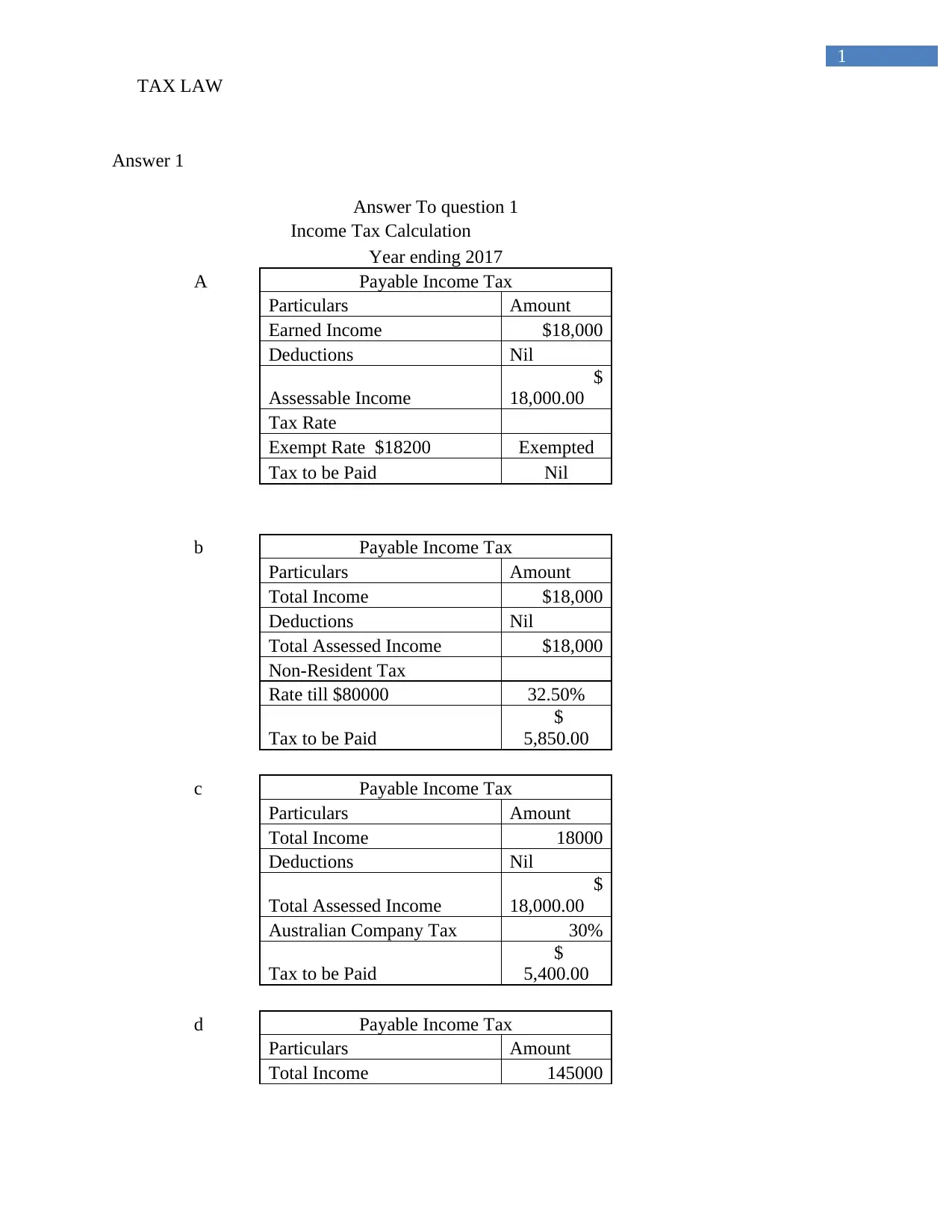

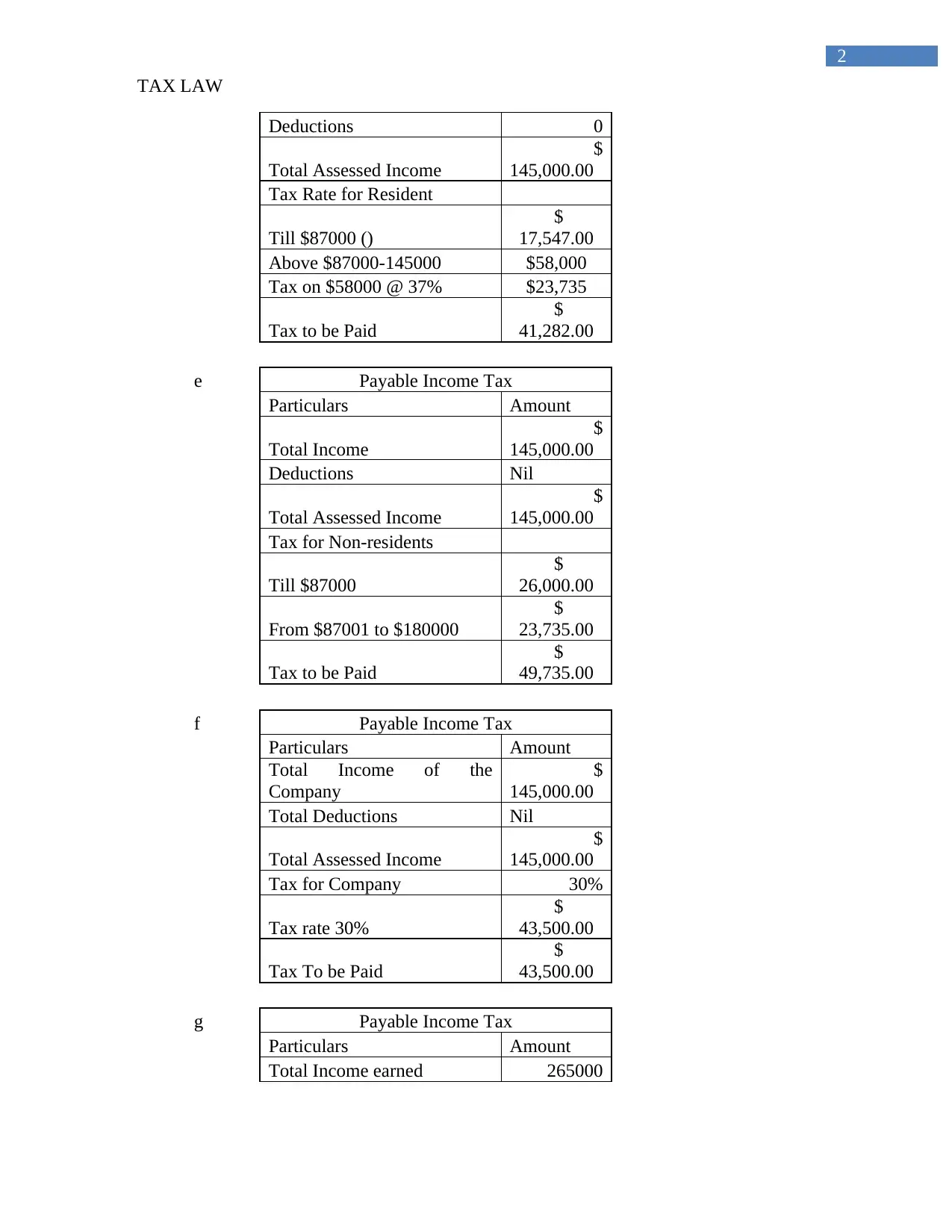

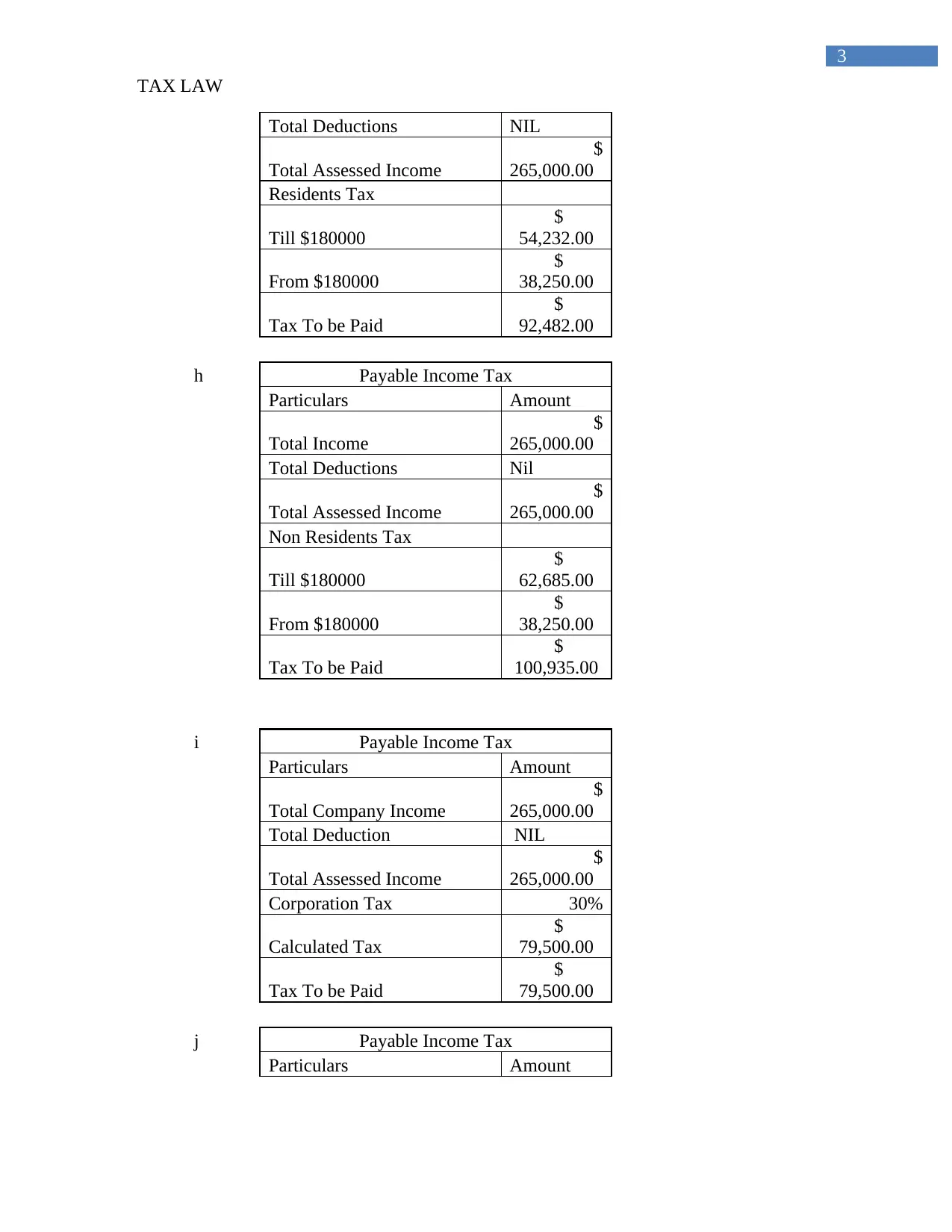

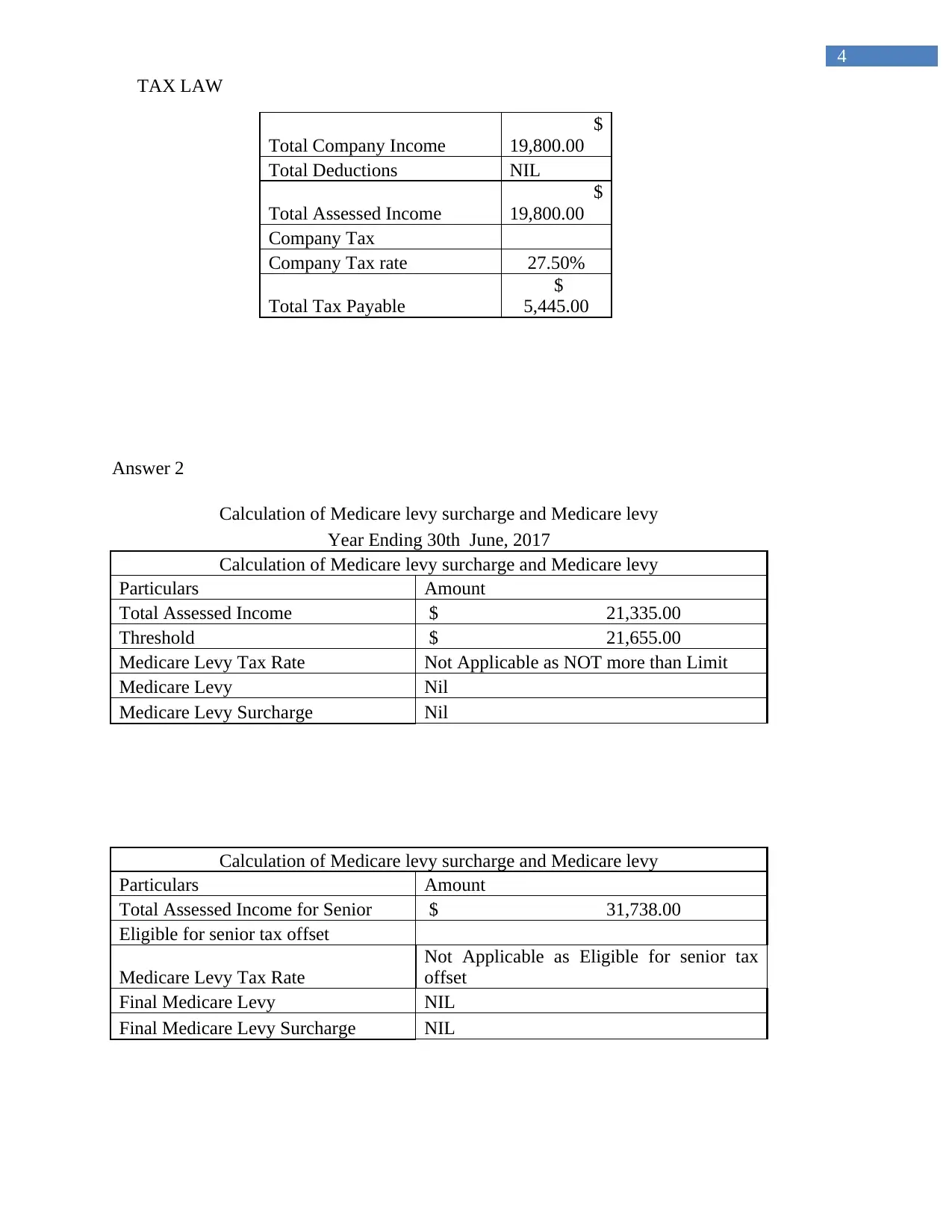

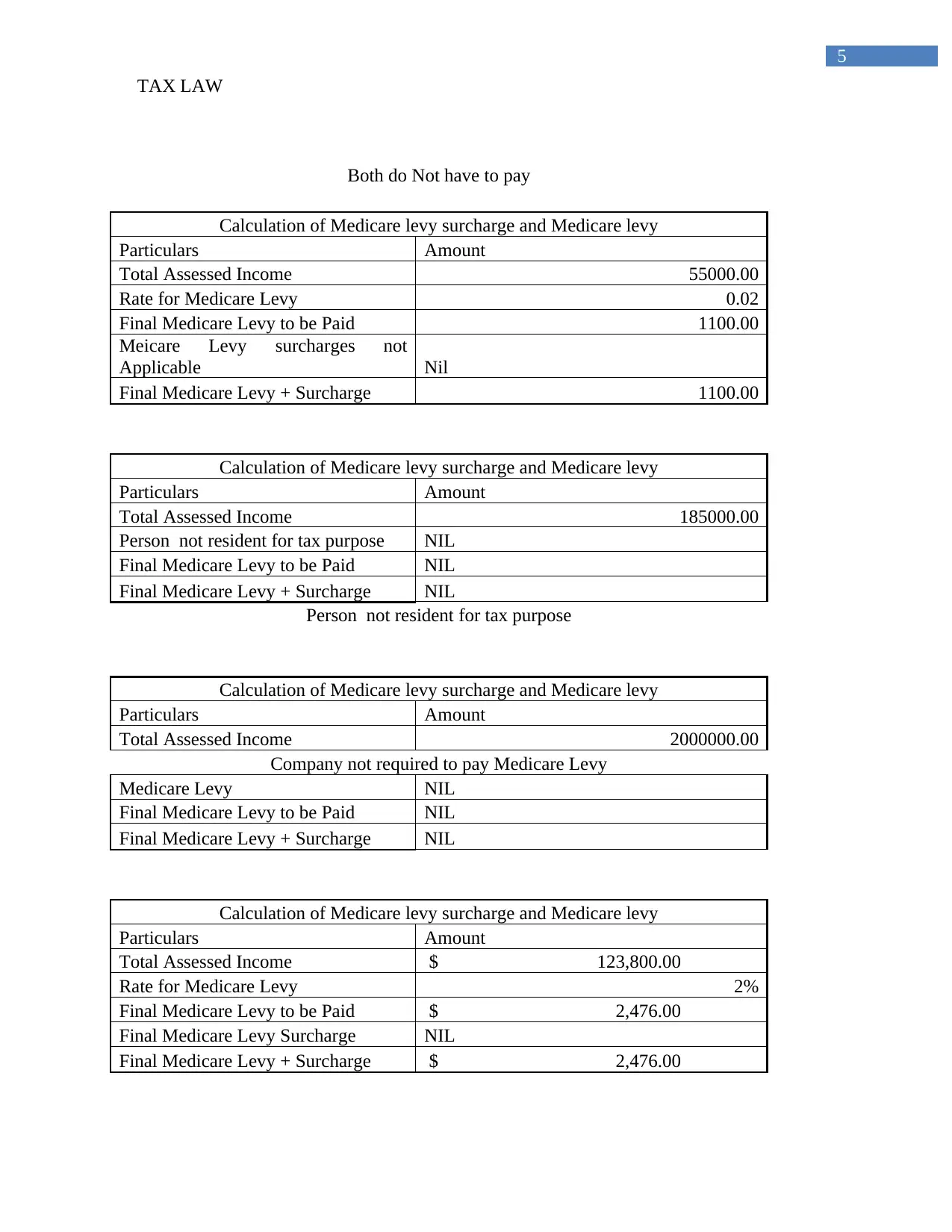

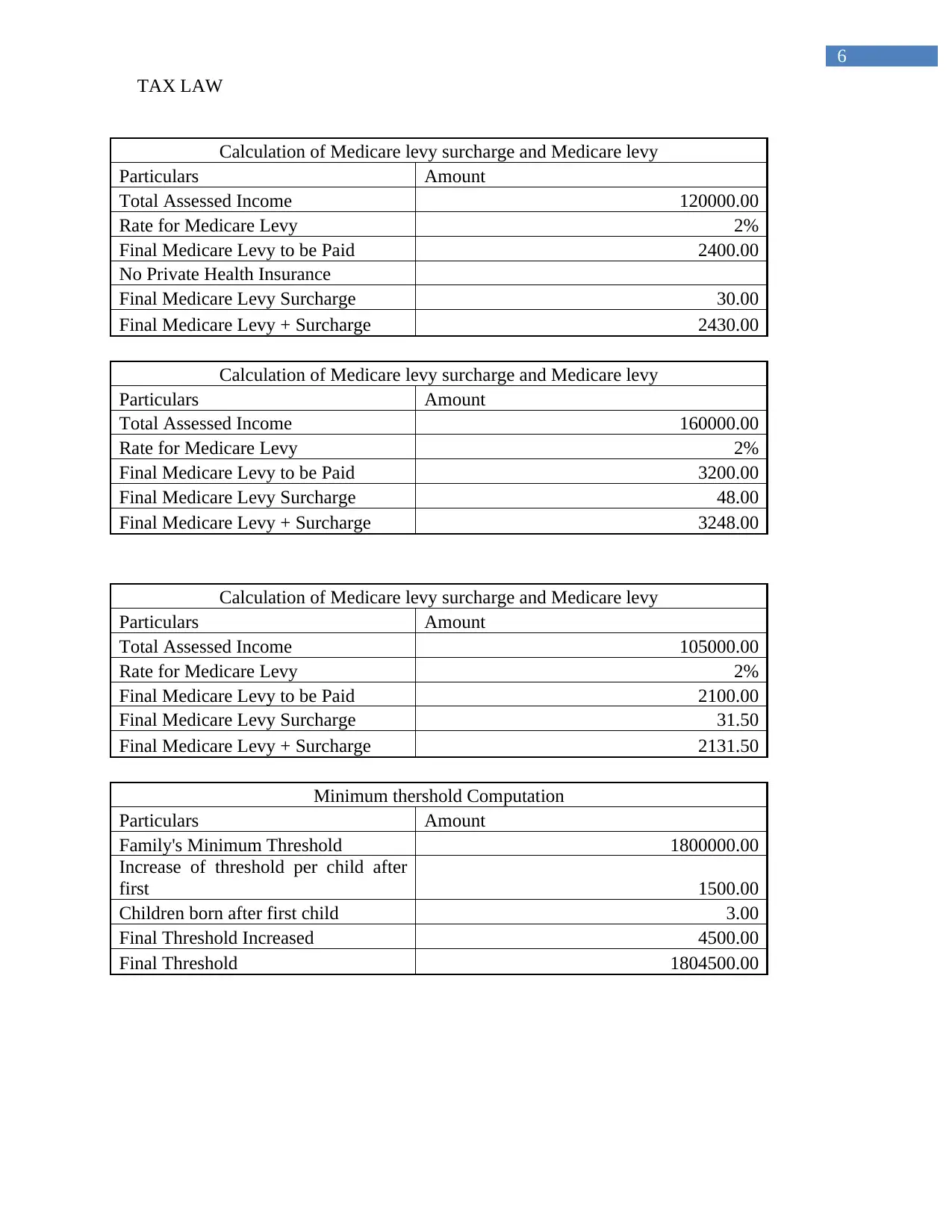

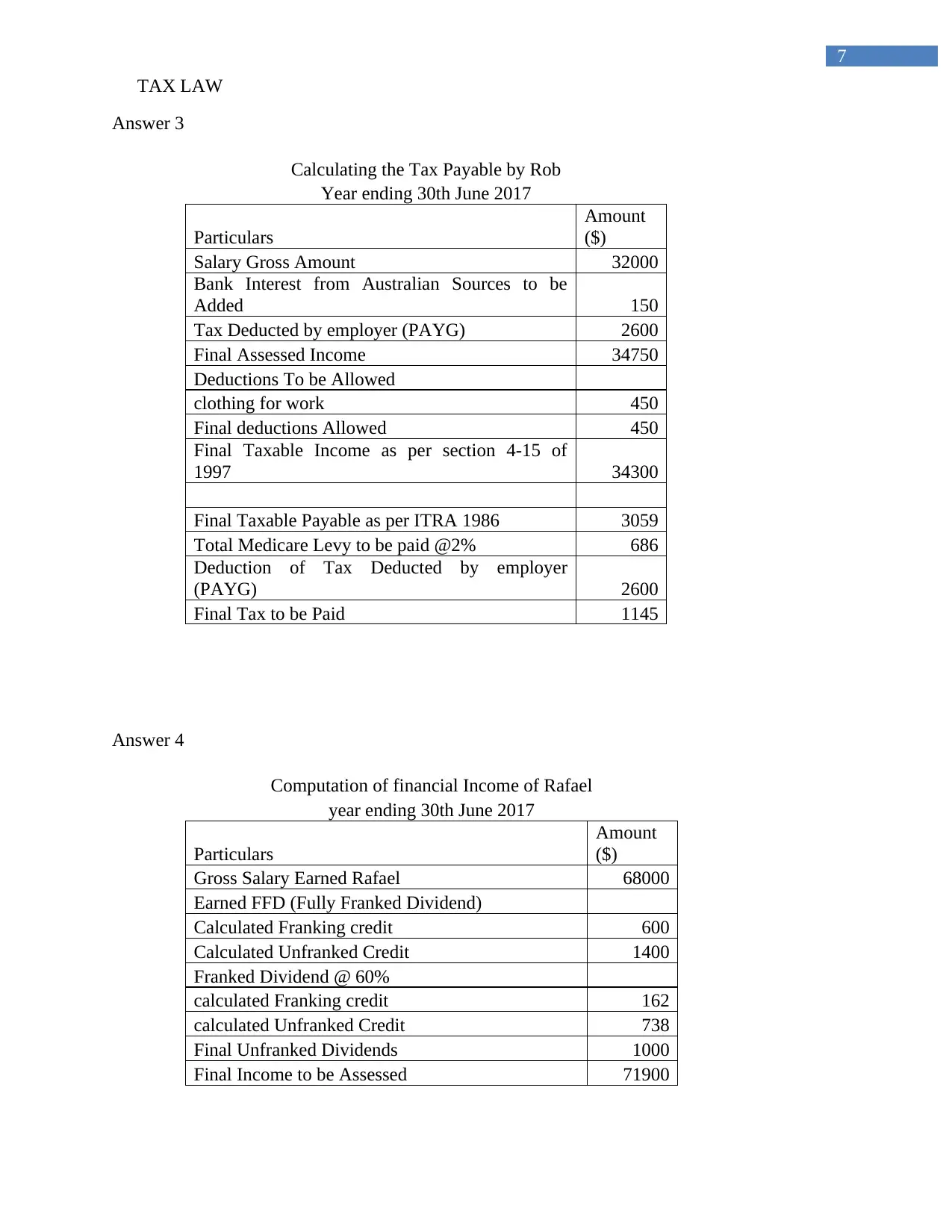

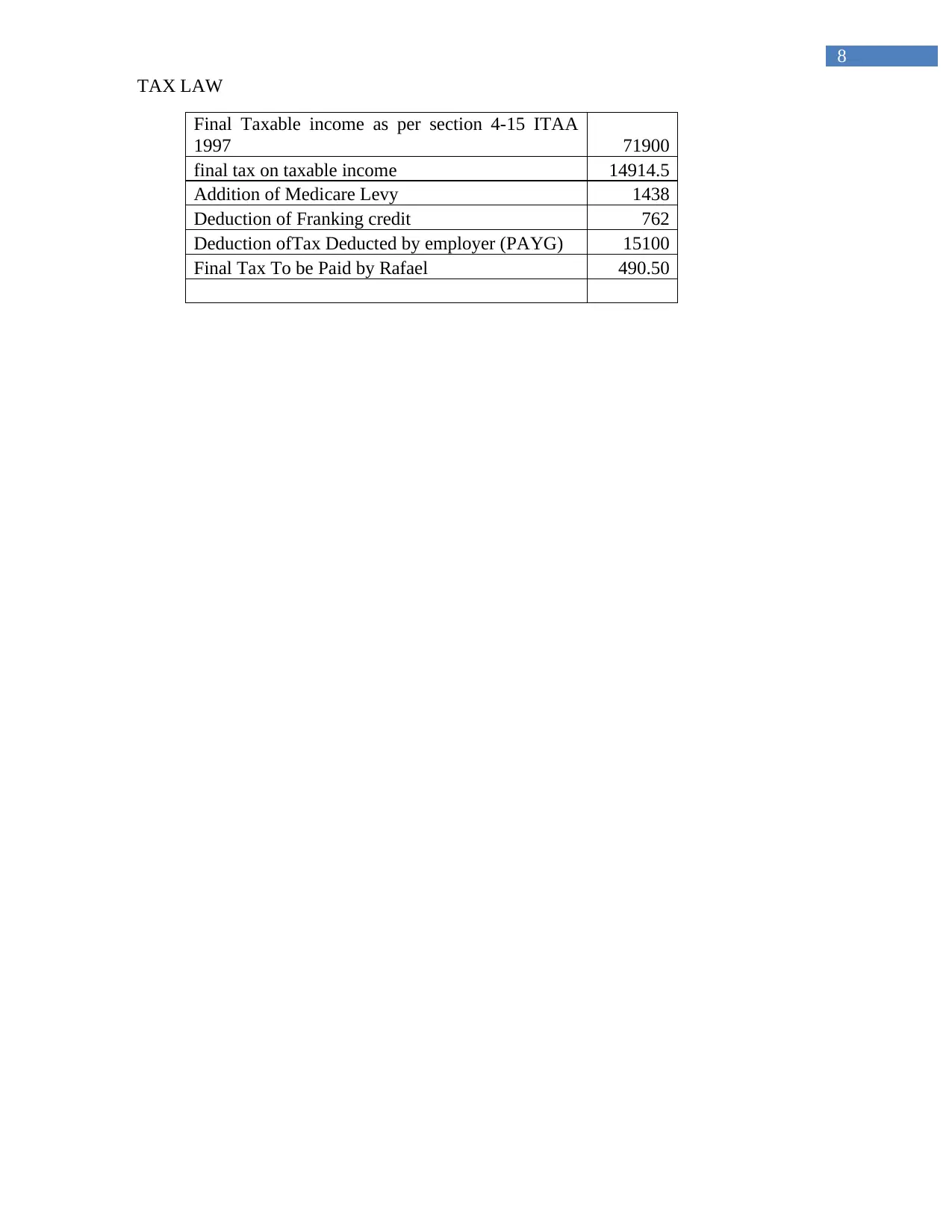

This document presents a comprehensive solution to a tax law assignment, focusing on various aspects of income tax and Medicare levy calculations. It includes detailed computations for different scenarios, such as calculating income tax for individuals, non-residents, and companies, using provided tax rates and deductions. The assignment also addresses the calculation of Medicare levy and Medicare levy surcharge, considering different income thresholds and residency statuses. Furthermore, it provides a breakdown of financial income, including franked and unfranked dividends, and calculates the final tax payable. The solution demonstrates a clear understanding of relevant tax laws and regulations, offering step-by-step calculations to arrive at the final tax liabilities.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.