Taxation Law Assignment: Income Tax, Statutory Income and CGT Analysis

VerifiedAdded on 2022/09/07

|9

|2130

|22

Homework Assignment

AI Summary

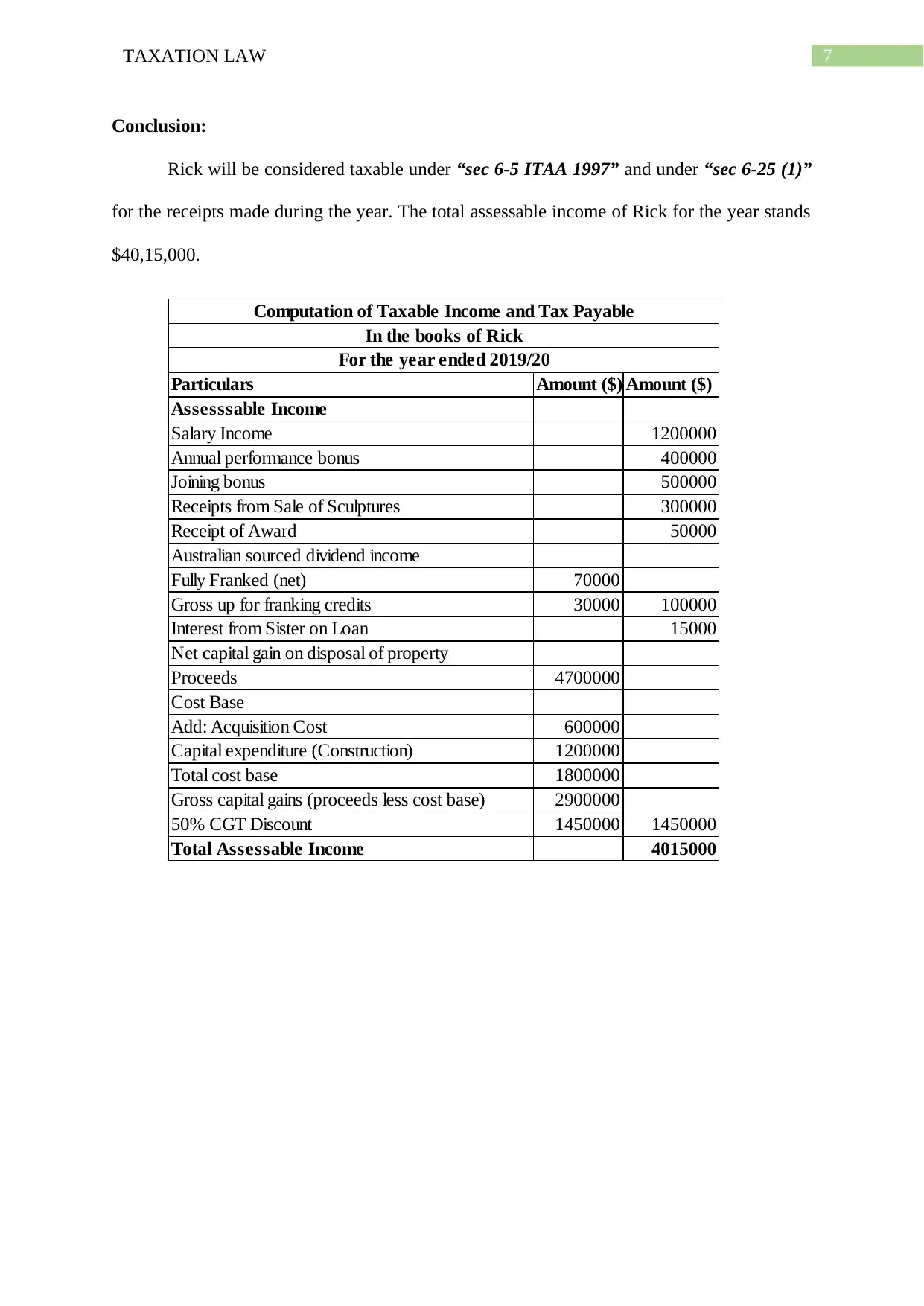

This document provides a comprehensive solution to a Taxation Law assignment, focusing on the assessment of income and the application of relevant tax legislation. The assignment addresses multiple issues related to ordinary income, statutory income, and capital gains tax (CGT). It analyzes various scenarios, including income from employment (salary, bonuses), sign-on fees, business income (artwork sales), and CGT implications of land subdivision and the sale of townhouses. The solution references key sections of the Income Tax Assessment Act 1997 (ITAA 1997) and the Income Tax Assessment Act 1936 (ITAA 1936), along with relevant case law, to determine the taxability of different income streams. The analysis covers topics such as personal exertion, business activities, CGT events, dividends, and interest income. The assignment concludes with a summary of the assessable income for the given scenarios, providing a clear understanding of the tax implications for the taxpayer. References to legal precedents and statutory provisions are included to support the analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.