University Finance: Tax Assignment - Income Tax and GST Analysis

VerifiedAdded on 2020/04/07

|11

|1448

|113

Homework Assignment

AI Summary

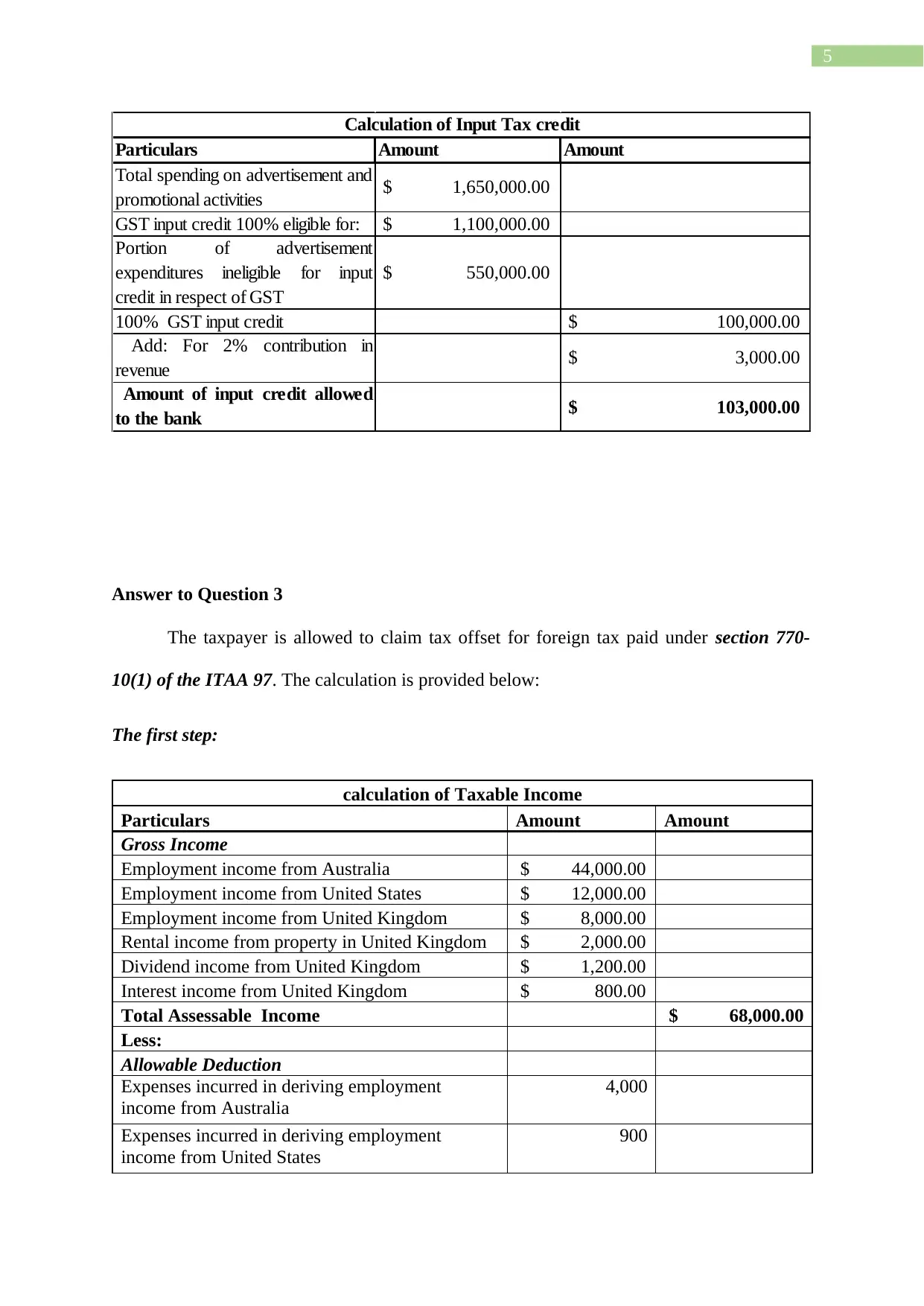

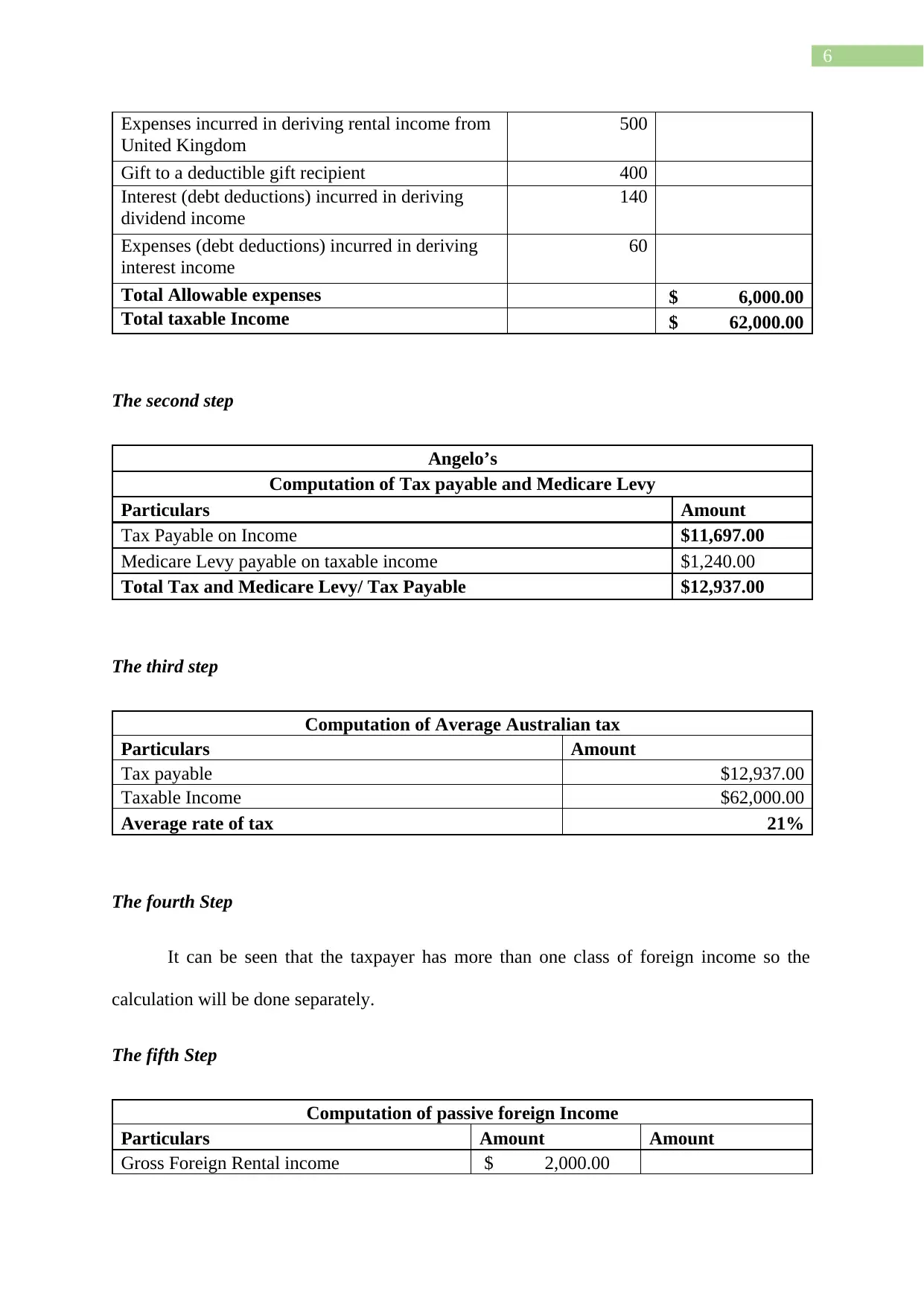

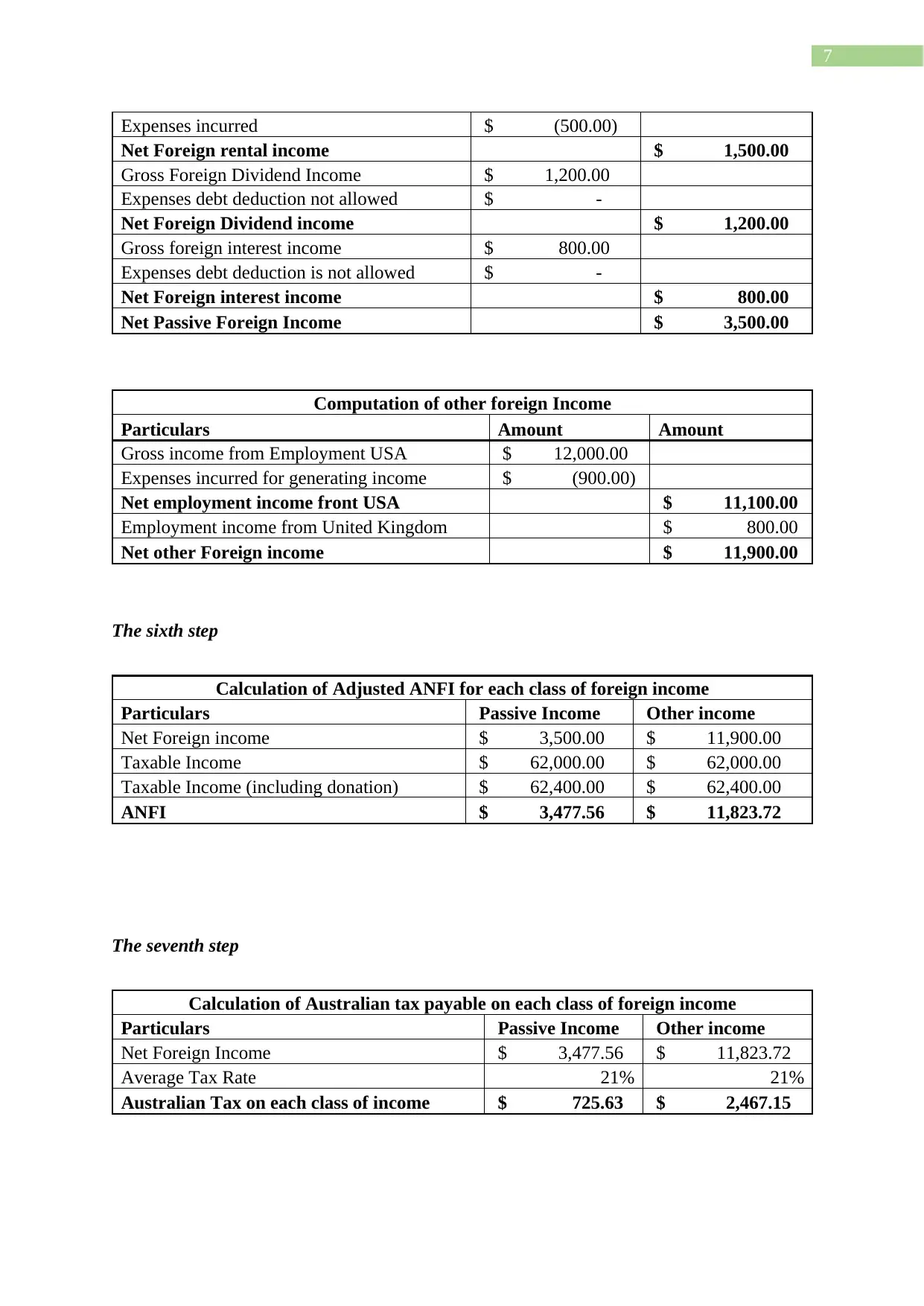

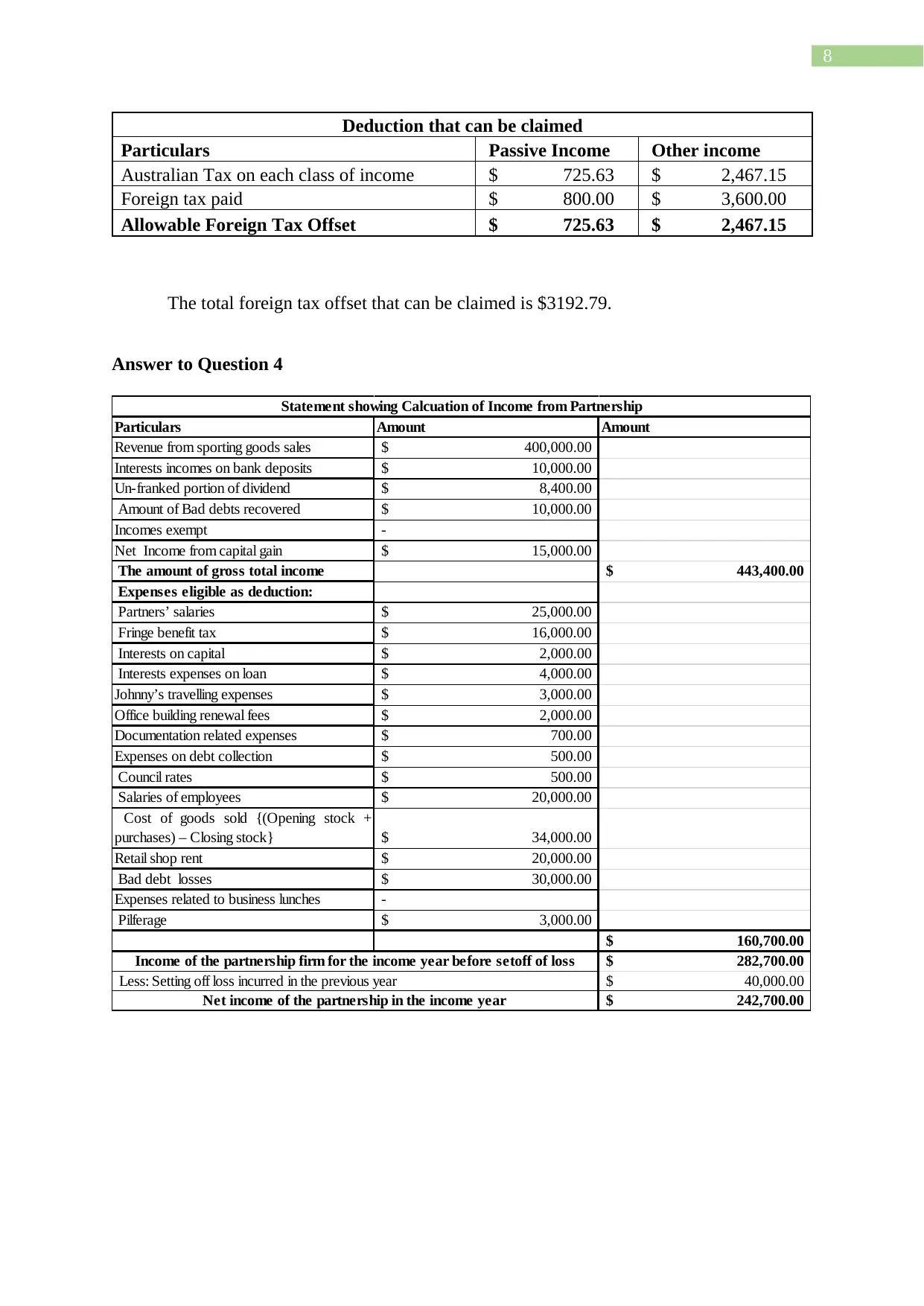

This assignment solution addresses various aspects of taxation, including income tax assessment, GST input credit, and foreign tax offsets. The first question delves into deductible expenses under the Income Tax Assessment Act 1997, while the second examines the eligibility for input credit of GST on advertising expenses. The third question provides a detailed calculation of taxable income, tax payable, and foreign tax offset, considering both passive and other foreign income sources. The assignment demonstrates the calculation of average tax rates and allowable deductions, and provides a final calculation for the total foreign tax offset that can be claimed. References to relevant literature are included at the end of the document.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.