Taxation Law Assignment: Analysis of Tax Laws and Regulations

VerifiedAdded on 2023/01/24

|16

|3983

|50

Homework Assignment

AI Summary

This taxation law assignment provides comprehensive answers to five key questions, covering various aspects of Australian taxation. The first question explores topics like effective life of depreciating assets, tax offsets, tax rates, capital gains tax, CGT events, and the calculation of income tax, drawing on relevant sections of the ITAA 1997 and case law. The second question delves into allowable deductions, analyzing scenarios related to business expenses, apportionment of expenses, personal expenses, losses, and preliminary expenses, with reference to established legal precedents. The third question examines CGT events, including granting of leases, enjoyment of title, main residence exemptions, and the application of the discount method. The fourth question addresses the tax treatment of prize winnings and the relationship with income-producing activities. The assignment provides a detailed analysis of each scenario, citing relevant sections of tax law and case law to support the conclusions. The assignment covers a wide range of taxation concepts, including income tax, capital gains tax, and tax deductions, making it a valuable resource for students of taxation law. The document is contributed by a student to be published on the website Desklib. Desklib is a platform which provides all the necessary AI based study tools for students.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................4

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to A:..........................................................................................................................5

Answer to B:..........................................................................................................................5

Answer to C:..........................................................................................................................6

Answer to D:..........................................................................................................................6

Answer E:...............................................................................................................................7

Answer to question 3:.................................................................................................................7

Answer A:..............................................................................................................................7

Answer B:...............................................................................................................................7

Answer C:...............................................................................................................................8

Answer to D:..........................................................................................................................8

Table of Contents

Answer to question 1:.................................................................................................................3

Answer A:..............................................................................................................................3

Answer B:...............................................................................................................................3

Answer C:...............................................................................................................................3

Answer D:..............................................................................................................................3

Answer F:...............................................................................................................................4

Answer G:..............................................................................................................................4

Answer H:..............................................................................................................................4

Answer I:................................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to A:..........................................................................................................................5

Answer to B:..........................................................................................................................5

Answer to C:..........................................................................................................................6

Answer to D:..........................................................................................................................6

Answer E:...............................................................................................................................7

Answer to question 3:.................................................................................................................7

Answer A:..............................................................................................................................7

Answer B:...............................................................................................................................7

Answer C:...............................................................................................................................8

Answer to D:..........................................................................................................................8

2TAXATION LAW

Answer to question 4:.................................................................................................................9

Answer A:..............................................................................................................................9

Answer B:.............................................................................................................................10

Answer C:.............................................................................................................................10

Answer D:............................................................................................................................10

Answer E:.............................................................................................................................11

Answer to question 5:...............................................................................................................11

Issues:...................................................................................................................................11

Laws:....................................................................................................................................11

Application:..........................................................................................................................12

Conclusion:..........................................................................................................................12

References:...............................................................................................................................13

Answer to question 4:.................................................................................................................9

Answer A:..............................................................................................................................9

Answer B:.............................................................................................................................10

Answer C:.............................................................................................................................10

Answer D:............................................................................................................................10

Answer E:.............................................................................................................................11

Answer to question 5:...............................................................................................................11

Issues:...................................................................................................................................11

Laws:....................................................................................................................................11

Application:..........................................................................................................................12

Conclusion:..........................................................................................................................12

References:...............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 1:

Answer A:

The effective life of the depreciating asset has been discussed under the taxation

ruling of TR 2018/4. The ruling explains the method used by taxation commissioner to

determine the assets effective life under “section 40-100, ITAA 1997” (Blackstone &

Christian, 2014).

Answer B:

Details regarding the claim of tax offset is given in “Division 13, ITAA 1997”.

Answer C:

In the year 2018/19 the highest rate of tax that is applicable on the resident taxpayer of

Australia is

Assessable Income Range Tax rate

180,001 or above 54,097 + 45c for each $1 above 180,000

Answer D:

Capital gains that are made from the assets used privately with the cost of asset is less

than $10,000 ought to be omitted under “section 118-10 (3), ITAA 1997” (Grange et al.,

2014).

Answer E:

CGT event B1 under “section 104-15” is associated with the usage and enjoyment of

the title before it passes (Jover-Ledesma, 2014). A CGT event B1 come about if a taxpayer

enters into the contract with another entity in respect to which there is a right of using and

enjoying the title of the CGT asset that a taxpayer has kept is passed to another entity. A CGT

Answer to question 1:

Answer A:

The effective life of the depreciating asset has been discussed under the taxation

ruling of TR 2018/4. The ruling explains the method used by taxation commissioner to

determine the assets effective life under “section 40-100, ITAA 1997” (Blackstone &

Christian, 2014).

Answer B:

Details regarding the claim of tax offset is given in “Division 13, ITAA 1997”.

Answer C:

In the year 2018/19 the highest rate of tax that is applicable on the resident taxpayer of

Australia is

Assessable Income Range Tax rate

180,001 or above 54,097 + 45c for each $1 above 180,000

Answer D:

Capital gains that are made from the assets used privately with the cost of asset is less

than $10,000 ought to be omitted under “section 118-10 (3), ITAA 1997” (Grange et al.,

2014).

Answer E:

CGT event B1 under “section 104-15” is associated with the usage and enjoyment of

the title before it passes (Jover-Ledesma, 2014). A CGT event B1 come about if a taxpayer

enters into the contract with another entity in respect to which there is a right of using and

enjoying the title of the CGT asset that a taxpayer has kept is passed to another entity. A CGT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

event B1 happens when the title in the asset will or might pass to another entity at or prior to

the termination of the settlement.

Answer F:

As per “section 4-10 of the ITAA 1997” a taxpayer is obligatory required to pay the

income tax each year (Kenny, 2013). However, under “section 4-10 (3), of the ITAA 1997”

to calculate the income tax for the financial year the formula is given below;

Income tax = [Taxable Income x Rate] – Tax Offsets

Answer G:

The court of law in “FC of T v Day 2008 ATC 20-064” held that the legal spending

that was occurred by the taxpayer is the course of producing or gaining the taxable income

and hence the “paragraph 8-1 (1) (a), ITAA 1997” was met. The majority of the federal

court judgment held that the expenditure was not considered as personal in nature, because

they were occurred in respect of the taxpayer’s position as the public servant and was not

unrelated to his services (Krever, 2015). The commissioner of taxation held that the legal

spending was occurred by the taxpayer in producing the chargeable income and hence

allowed for deduction under “section 8-1, ITAA 1997”.

Answer H:

The differences between the marginal rate of tax and average rate of tax is given below;

a. The average rate of tax is related to the measurement of tax burden. The marginal rate

of tax is related to the measurement of effect of tax on the incentives to earn,

investments or expenditure.

b. The average rate of tax represents the whole quantity of tax that is divided by the total

revenue. The marginal rate of tax represents the rising tax that is paid on the rising

income.

event B1 happens when the title in the asset will or might pass to another entity at or prior to

the termination of the settlement.

Answer F:

As per “section 4-10 of the ITAA 1997” a taxpayer is obligatory required to pay the

income tax each year (Kenny, 2013). However, under “section 4-10 (3), of the ITAA 1997”

to calculate the income tax for the financial year the formula is given below;

Income tax = [Taxable Income x Rate] – Tax Offsets

Answer G:

The court of law in “FC of T v Day 2008 ATC 20-064” held that the legal spending

that was occurred by the taxpayer is the course of producing or gaining the taxable income

and hence the “paragraph 8-1 (1) (a), ITAA 1997” was met. The majority of the federal

court judgment held that the expenditure was not considered as personal in nature, because

they were occurred in respect of the taxpayer’s position as the public servant and was not

unrelated to his services (Krever, 2015). The commissioner of taxation held that the legal

spending was occurred by the taxpayer in producing the chargeable income and hence

allowed for deduction under “section 8-1, ITAA 1997”.

Answer H:

The differences between the marginal rate of tax and average rate of tax is given below;

a. The average rate of tax is related to the measurement of tax burden. The marginal rate

of tax is related to the measurement of effect of tax on the incentives to earn,

investments or expenditure.

b. The average rate of tax represents the whole quantity of tax that is divided by the total

revenue. The marginal rate of tax represents the rising tax that is paid on the rising

income.

5TAXATION LAW

c. The average tax rate is used as the measurement of the household burden of tax i.e.

how the tax creates an impact on the ability of the household to consume presently or

in future (Morgan et al., 2013). The marginal rate of tax is regarded as the degree

based on which the taxes would create an impact on the household economic

incentives particularly whether to save more or take more risks in investment

portfolio.

Answer I:

Consumption tax is regarded as the tax that is paid directly or indirectly by the

consumers particularly the excise, sales or use of duties, rates and some kind of property

levies. The consumption tax is generally levied on the expenditure of goods and services.

Answer to question 2:

Answer to A:

As per the positive limbs of “section 8-1, ITAA 1997” a taxpayer is allowable to

claim income tax deduction from his or her assessable income for any kind of loss or

outgoings till the extent that it is occurred in producing the taxpayer’s taxable income or

occurred mainly at the time of carrying on the business for creating the chargeable proceeds.

Brett took the loan against his personal house to pay the wages of employee. It can be

understood that the loan interest arose here is in the course of business for generating Brett’s

taxable earnings. The expenses content the positive limbs of “section 8-1, ITAA 1997” and

Brett will be allowed deduction for loan interest.

Answer to B:

In some of the situation loss or outgoings may be required to be apportioned. In other

words, only partially allowed for deduction (Sadiq & Coleman, 2013). If a part of expense is

c. The average tax rate is used as the measurement of the household burden of tax i.e.

how the tax creates an impact on the ability of the household to consume presently or

in future (Morgan et al., 2013). The marginal rate of tax is regarded as the degree

based on which the taxes would create an impact on the household economic

incentives particularly whether to save more or take more risks in investment

portfolio.

Answer I:

Consumption tax is regarded as the tax that is paid directly or indirectly by the

consumers particularly the excise, sales or use of duties, rates and some kind of property

levies. The consumption tax is generally levied on the expenditure of goods and services.

Answer to question 2:

Answer to A:

As per the positive limbs of “section 8-1, ITAA 1997” a taxpayer is allowable to

claim income tax deduction from his or her assessable income for any kind of loss or

outgoings till the extent that it is occurred in producing the taxpayer’s taxable income or

occurred mainly at the time of carrying on the business for creating the chargeable proceeds.

Brett took the loan against his personal house to pay the wages of employee. It can be

understood that the loan interest arose here is in the course of business for generating Brett’s

taxable earnings. The expenses content the positive limbs of “section 8-1, ITAA 1997” and

Brett will be allowed deduction for loan interest.

Answer to B:

In some of the situation loss or outgoings may be required to be apportioned. In other

words, only partially allowed for deduction (Sadiq & Coleman, 2013). If a part of expense is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

occurred for both the private and business purpose then, a deduction is permitted to taxpayer

only for business purpose.

The mobile phone bill expense accounted for $500 where 60% of the total cost was

for the business purpose and the rest 40% is for private purpose. In this situation the expenses

should be apportioned by Julie and she is only permitted to claim deduction for 60% of

mobile phone expenses as it is related to derivation of assessable income and the rest 40%

must be ignored as it is a private expense.

Answer to C:

An expense that is personal or domestic in nature is not permissible for income tax

deduction because it is not meeting the criteria for positive limbs or it is not permitted for

allowable deduction in terms of second negative limb of “section 8-1 (2)(b), ITAA 1997”

(Sadiq, 2014). The court denied deduction to taxpayer in “Lodge v FCT (1972)” for the

childcare expenses because the expense was not relevant in earning taxable income.

Sally here incurred $1,200 for babysitting purpose to mind her child when she goes to

work. Citing “Lodge v FCT (1972)” the babysitter expenses is not allowable for tax

deduction under second negative limb of “section 8-1 (2)(b), ITAA 1997” for the reason that

the expense was not relevant in earning taxable income.

Answer to D:

Losses or outgoings where the financial resources of the taxpayer have been

diminished is allowable for deduction in positive limbs of “section 8-1, ITAA 1997”. The

taxation commissioner allowed taxpayer with deduction in “Charles Moore & Co (WA) Pty

Ltd v FCT (1956)” for money that was stolen for the taxpayer (Woellner, 2013).

Jerry reported a loss of $20,000 as one of his long term employee stolen goods from

the business. Citing, “Charles Moore & Co (WA) Pty Ltd v FCT (1956)” Jerry is entitled to

occurred for both the private and business purpose then, a deduction is permitted to taxpayer

only for business purpose.

The mobile phone bill expense accounted for $500 where 60% of the total cost was

for the business purpose and the rest 40% is for private purpose. In this situation the expenses

should be apportioned by Julie and she is only permitted to claim deduction for 60% of

mobile phone expenses as it is related to derivation of assessable income and the rest 40%

must be ignored as it is a private expense.

Answer to C:

An expense that is personal or domestic in nature is not permissible for income tax

deduction because it is not meeting the criteria for positive limbs or it is not permitted for

allowable deduction in terms of second negative limb of “section 8-1 (2)(b), ITAA 1997”

(Sadiq, 2014). The court denied deduction to taxpayer in “Lodge v FCT (1972)” for the

childcare expenses because the expense was not relevant in earning taxable income.

Sally here incurred $1,200 for babysitting purpose to mind her child when she goes to

work. Citing “Lodge v FCT (1972)” the babysitter expenses is not allowable for tax

deduction under second negative limb of “section 8-1 (2)(b), ITAA 1997” for the reason that

the expense was not relevant in earning taxable income.

Answer to D:

Losses or outgoings where the financial resources of the taxpayer have been

diminished is allowable for deduction in positive limbs of “section 8-1, ITAA 1997”. The

taxation commissioner allowed taxpayer with deduction in “Charles Moore & Co (WA) Pty

Ltd v FCT (1956)” for money that was stolen for the taxpayer (Woellner, 2013).

Jerry reported a loss of $20,000 as one of his long term employee stolen goods from

the business. Citing, “Charles Moore & Co (WA) Pty Ltd v FCT (1956)” Jerry is entitled to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

deduction for tax purpose under “section 8-1, ITAA 1997” for the stolen goods from business

because it is a loss of financial resources for the taxpayer.

Answer E:

An outgoing that are considered preliminary to producing income or business activity

is not allowable for deduction under “section 8-1, ITAA 1997” because it is not in the course

of earning income. In “FCT v Madellena (1971)” expenses occurred in getting the new

employment is not in the course of attaining income and non-deductible because it occurred

at a point very soon (Woellner et al., 2014).

Legal expense of $5,000 for contesting local government election is not allowed for

deduction under the general legislative provision of “section 8-1, ITAA 1997” because it is

not in the course of earning income. The expenses have occurred at a point that is very soon.

Answer to question 3:

Answer A:

As per ATO a taxpayer can apply the CGT event F2 when a taxpayer grants, renews

or extend the long term lease. It can be applicable if the taxpayer is the owner of the

underlying land or if they grant the sub-lease (Barkoczy, 2016). However, the taxpayer

should denote that CGT discount is not applicable when CGT event F2 happens.

As per the case facts of Andy he is the owner of the land and grants the lease to Brian

for five year based on the premium of $5,000. The granting of lease by Andy to Brian for

five-year period at a premium result in the CGT event F2. Conversely, Andy should

understand that the CGT discount is not applicable on making the disposal of land.

Answer B:

A CGT event B1 happens when the enjoyment prior the title is passed to another

person. On making the use of the CGT asset that passes the capital gains derived from the

deduction for tax purpose under “section 8-1, ITAA 1997” for the stolen goods from business

because it is a loss of financial resources for the taxpayer.

Answer E:

An outgoing that are considered preliminary to producing income or business activity

is not allowable for deduction under “section 8-1, ITAA 1997” because it is not in the course

of earning income. In “FCT v Madellena (1971)” expenses occurred in getting the new

employment is not in the course of attaining income and non-deductible because it occurred

at a point very soon (Woellner et al., 2014).

Legal expense of $5,000 for contesting local government election is not allowed for

deduction under the general legislative provision of “section 8-1, ITAA 1997” because it is

not in the course of earning income. The expenses have occurred at a point that is very soon.

Answer to question 3:

Answer A:

As per ATO a taxpayer can apply the CGT event F2 when a taxpayer grants, renews

or extend the long term lease. It can be applicable if the taxpayer is the owner of the

underlying land or if they grant the sub-lease (Barkoczy, 2016). However, the taxpayer

should denote that CGT discount is not applicable when CGT event F2 happens.

As per the case facts of Andy he is the owner of the land and grants the lease to Brian

for five year based on the premium of $5,000. The granting of lease by Andy to Brian for

five-year period at a premium result in the CGT event F2. Conversely, Andy should

understand that the CGT discount is not applicable on making the disposal of land.

Answer B:

A CGT event B1 happens when the enjoyment prior the title is passed to another

person. On making the use of the CGT asset that passes the capital gains derived from the

8TAXATION LAW

proceeds after deducting the costs base results in CGT event B1. The usage as well as

enjoyment of asset from the practical perspective takes place when the ownership of asset is

passed to the new owner where the new owner is allowed to rent and profits. John granted the

Farm Ltd with the option of purchasing the farm for $800,000. The option of purchasing the

land for $800,000 amounts to CGT event B1. Consequently, John will be allowed to apply

50% CGT discount before passing the title of land.

Answer C:

A taxpayer main residence is usually excluded from capital gains tax. To get main

residence exemption, the property should have the residence on it and the taxpayer should

have lived in it (Jones & Rhoades-Catanach, 2015). The taxpayers are not entitled to

exemption for the vacant land. A taxpayer is only entitled for exemption to the main

residence if the dwelling has been the home for taxpayer all through the entire period

(Freudenberg et al., 2017). Additionally, a taxpayer is only eligible for claiming full main

residence exemption if the home has not been used for generating income and that the

taxpayer has not utilized the house for business purpose such as renting it out or flipping it.

In the current situation Jamie and Olivia has bought the property and has rented it out

immediately for two years. After making it their main residence in 2008 they later sold it in

2018. A partial main residence exemption from CGT can be claimed by Jamie and Olivia.

But they should note that a discount method or 50% CGT discount will be applicable on the

capital gains made from the sale of residence.

Answer to D:

A taxpayer is allowed to use the discount method to compute the net amount of

capital gains on majority of the assets that has been owned by the taxpayer for a period of 12

months or more.

proceeds after deducting the costs base results in CGT event B1. The usage as well as

enjoyment of asset from the practical perspective takes place when the ownership of asset is

passed to the new owner where the new owner is allowed to rent and profits. John granted the

Farm Ltd with the option of purchasing the farm for $800,000. The option of purchasing the

land for $800,000 amounts to CGT event B1. Consequently, John will be allowed to apply

50% CGT discount before passing the title of land.

Answer C:

A taxpayer main residence is usually excluded from capital gains tax. To get main

residence exemption, the property should have the residence on it and the taxpayer should

have lived in it (Jones & Rhoades-Catanach, 2015). The taxpayers are not entitled to

exemption for the vacant land. A taxpayer is only entitled for exemption to the main

residence if the dwelling has been the home for taxpayer all through the entire period

(Freudenberg et al., 2017). Additionally, a taxpayer is only eligible for claiming full main

residence exemption if the home has not been used for generating income and that the

taxpayer has not utilized the house for business purpose such as renting it out or flipping it.

In the current situation Jamie and Olivia has bought the property and has rented it out

immediately for two years. After making it their main residence in 2008 they later sold it in

2018. A partial main residence exemption from CGT can be claimed by Jamie and Olivia.

But they should note that a discount method or 50% CGT discount will be applicable on the

capital gains made from the sale of residence.

Answer to D:

A taxpayer is allowed to use the discount method to compute the net amount of

capital gains on majority of the assets that has been owned by the taxpayer for a period of 12

months or more.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

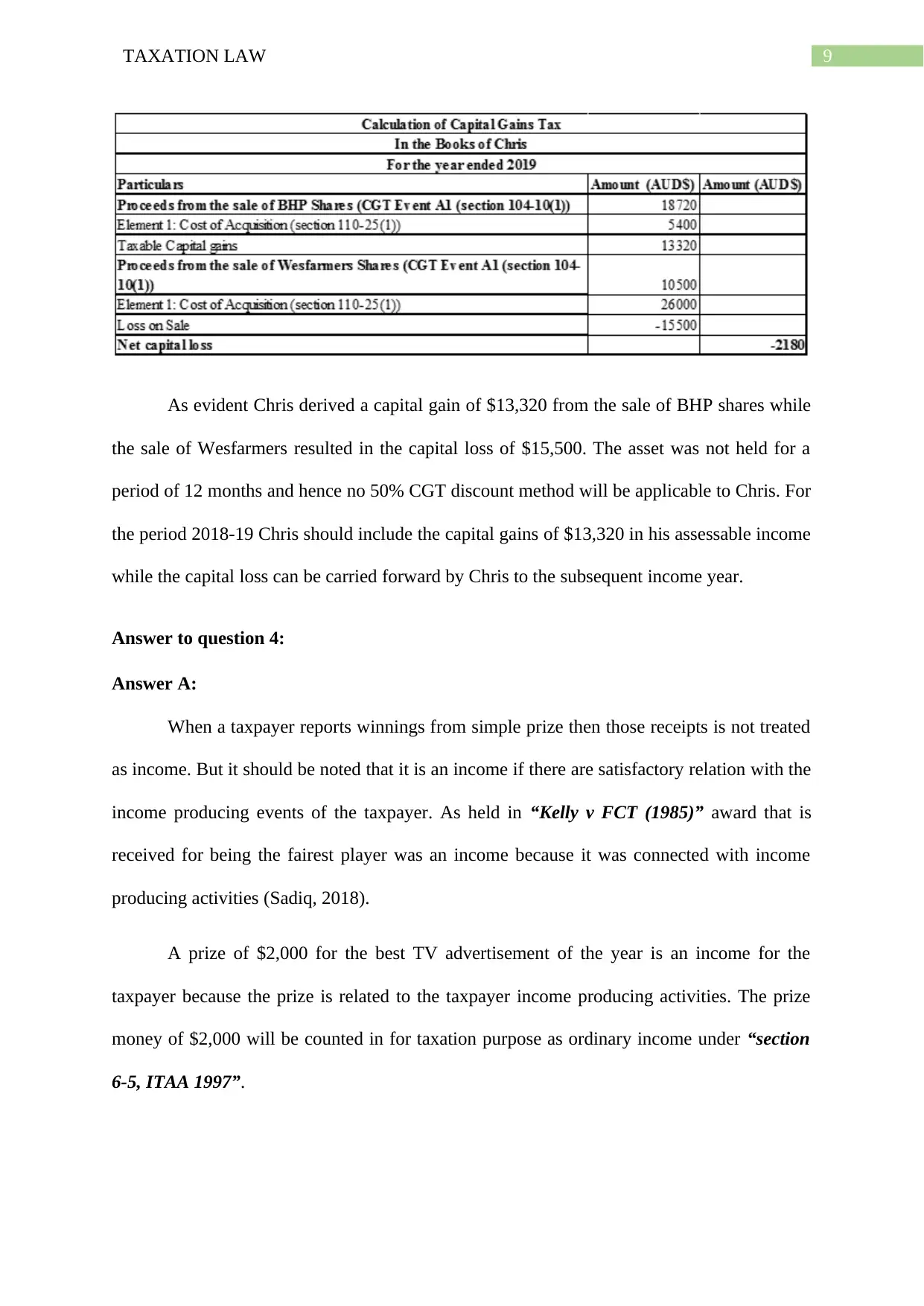

9TAXATION LAW

As evident Chris derived a capital gain of $13,320 from the sale of BHP shares while

the sale of Wesfarmers resulted in the capital loss of $15,500. The asset was not held for a

period of 12 months and hence no 50% CGT discount method will be applicable to Chris. For

the period 2018-19 Chris should include the capital gains of $13,320 in his assessable income

while the capital loss can be carried forward by Chris to the subsequent income year.

Answer to question 4:

Answer A:

When a taxpayer reports winnings from simple prize then those receipts is not treated

as income. But it should be noted that it is an income if there are satisfactory relation with the

income producing events of the taxpayer. As held in “Kelly v FCT (1985)” award that is

received for being the fairest player was an income because it was connected with income

producing activities (Sadiq, 2018).

A prize of $2,000 for the best TV advertisement of the year is an income for the

taxpayer because the prize is related to the taxpayer income producing activities. The prize

money of $2,000 will be counted in for taxation purpose as ordinary income under “section

6-5, ITAA 1997”.

As evident Chris derived a capital gain of $13,320 from the sale of BHP shares while

the sale of Wesfarmers resulted in the capital loss of $15,500. The asset was not held for a

period of 12 months and hence no 50% CGT discount method will be applicable to Chris. For

the period 2018-19 Chris should include the capital gains of $13,320 in his assessable income

while the capital loss can be carried forward by Chris to the subsequent income year.

Answer to question 4:

Answer A:

When a taxpayer reports winnings from simple prize then those receipts is not treated

as income. But it should be noted that it is an income if there are satisfactory relation with the

income producing events of the taxpayer. As held in “Kelly v FCT (1985)” award that is

received for being the fairest player was an income because it was connected with income

producing activities (Sadiq, 2018).

A prize of $2,000 for the best TV advertisement of the year is an income for the

taxpayer because the prize is related to the taxpayer income producing activities. The prize

money of $2,000 will be counted in for taxation purpose as ordinary income under “section

6-5, ITAA 1997”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Answer B:

Accordingly, as defined in “section 6-1, ITAA 1997” where a taxpayer reports the

earnings from the private effort it generally includes the salaries, wages, allowances etc.

which is received by the taxpayer by working as the employee in relation to the services that

is provided (Butler, 2019). In the current case the amount of $500 that is received by

employee in the form of travelling cost that is incurred to travel from Sydney to the place of

work is cannot be regarded as income because it amounts to reimbursement of expenses for

the employer. Therefore, the amount will not be included for assessment purpose.

Answer C:

As a general rule, it must be noted that a gain that is having the nature of simple gift is

not having the character of income. As held in “Scott v FCT (1966)” the gift of $10,000 from

the longstanding wife of client out of the husband estate was not held as having the character

of income (Morgan et al., 2018).

The taxpayer received the $1,000 iphone as gift from the client. Referring to “Scott v

FCT (1966)” the gift of $1,000 cannot be held as income under the ordinary conceptions

because it only amounts to simple gift.

Answer D:

Receipts derived by the taxpayer as lump sum payment may result in capital gains.

Nevertheless, as defined in the “paragraph 118-37 (1) (b), ITAA 1997” the taxpayers are

required to ignore the receipts for the capital gains tax purpose when the amount received is

related to the compensation or damages for the personal wrong, injury or illness (Morgan &

Castelyn, 2018).

Answer B:

Accordingly, as defined in “section 6-1, ITAA 1997” where a taxpayer reports the

earnings from the private effort it generally includes the salaries, wages, allowances etc.

which is received by the taxpayer by working as the employee in relation to the services that

is provided (Butler, 2019). In the current case the amount of $500 that is received by

employee in the form of travelling cost that is incurred to travel from Sydney to the place of

work is cannot be regarded as income because it amounts to reimbursement of expenses for

the employer. Therefore, the amount will not be included for assessment purpose.

Answer C:

As a general rule, it must be noted that a gain that is having the nature of simple gift is

not having the character of income. As held in “Scott v FCT (1966)” the gift of $10,000 from

the longstanding wife of client out of the husband estate was not held as having the character

of income (Morgan et al., 2018).

The taxpayer received the $1,000 iphone as gift from the client. Referring to “Scott v

FCT (1966)” the gift of $1,000 cannot be held as income under the ordinary conceptions

because it only amounts to simple gift.

Answer D:

Receipts derived by the taxpayer as lump sum payment may result in capital gains.

Nevertheless, as defined in the “paragraph 118-37 (1) (b), ITAA 1997” the taxpayers are

required to ignore the receipts for the capital gains tax purpose when the amount received is

related to the compensation or damages for the personal wrong, injury or illness (Morgan &

Castelyn, 2018).

11TAXATION LAW

It is noted that a compensatory receipt of $10,000 that has been received by the

taxpayer for personal injury is not an income under ordinary concepts. These kinds of

payments are considered as tax free payment.

Answer E:

Where a taxpayer anticipates to earn a taxable income in the future year as the reason

of presently being entitled to income for future year is considered too remote to provide any

kind of connection with the current income year (Pert et al., 2018). The shares were held by

taxpayer which was purchased in 30th June for $5 but it is presently trending for $7.50. The

shares are yet to be sold by the taxpayer and an income is anticipated to earn in future year.

Therefore, it does not amount to income because it is too remote to hold any connection with

the current income year.

Answer to question 5:

Issues:

The present case brings forward the issue of ascertaining whether the taxpayer is an

Australian resident under the meaning of “section 6 (1), ITAA 1997”.

Laws:

The legislative provision of “section 6 (1), ITAA 1997” lay down an explanation that

the resident of Australia is regarded as the person apart from the company that is living in

Australia lest the taxation official is satisfied that the person’s fixed location or place where

he or she actually lives is out of Australia (Robin, 2019). Only one of the four test should be

satisfied by the person in order to be held as the Australian resident.

The primary test for determining the residency position is the dwelling in relation

with the ordinary concepts. This implies that to dwell on a permanent basis or for the

significant period of time (Robin & Barkoczy, 2019). This take account of the time that is

It is noted that a compensatory receipt of $10,000 that has been received by the

taxpayer for personal injury is not an income under ordinary concepts. These kinds of

payments are considered as tax free payment.

Answer E:

Where a taxpayer anticipates to earn a taxable income in the future year as the reason

of presently being entitled to income for future year is considered too remote to provide any

kind of connection with the current income year (Pert et al., 2018). The shares were held by

taxpayer which was purchased in 30th June for $5 but it is presently trending for $7.50. The

shares are yet to be sold by the taxpayer and an income is anticipated to earn in future year.

Therefore, it does not amount to income because it is too remote to hold any connection with

the current income year.

Answer to question 5:

Issues:

The present case brings forward the issue of ascertaining whether the taxpayer is an

Australian resident under the meaning of “section 6 (1), ITAA 1997”.

Laws:

The legislative provision of “section 6 (1), ITAA 1997” lay down an explanation that

the resident of Australia is regarded as the person apart from the company that is living in

Australia lest the taxation official is satisfied that the person’s fixed location or place where

he or she actually lives is out of Australia (Robin, 2019). Only one of the four test should be

satisfied by the person in order to be held as the Australian resident.

The primary test for determining the residency position is the dwelling in relation

with the ordinary concepts. This implies that to dwell on a permanent basis or for the

significant period of time (Robin & Barkoczy, 2019). This take account of the time that is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.