Taxation Law Assignment - Analysis of Tax Issues and Rules

VerifiedAdded on 2019/10/31

|14

|2554

|162

Homework Assignment

AI Summary

This document presents a detailed analysis of a taxation law assignment, addressing five key issues. The assignment explores capital gains and losses, fringe benefit tax, the distribution of income or loss in rental properties, tax avoidance strategies, and the income generated by primary producers engaged in forestry. Each question includes an analysis of the relevant rules, applications of those rules to the specific facts, and a conclusion. The document references key legislation such as the ITAA 1997 and various taxation rulings, as well as relevant case law. The analysis covers topics such as personal use assets, collectables, interest offsets, co-ownership of rental properties, and the concept of royalties. The assignment provides a comprehensive overview of the legal principles involved and their practical application in the context of taxation law.

Running head: TAXATION LAW

Taxation Law

Name of the University

Name of the Student

Authors Note

Course ID

Taxation Law

Name of the University

Name of the Student

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................3

Issue:..........................................................................................................................................3

Rule:...........................................................................................................................................3

Application:................................................................................................................................3

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to question 2:.................................................................................................................4

Issue:..........................................................................................................................................4

Rule:...........................................................................................................................................4

Application:................................................................................................................................4

Conclusion:................................................................................................................................5

Answer to question 3:.................................................................................................................5

Issue:..........................................................................................................................................5

Rule:...........................................................................................................................................6

Application:................................................................................................................................6

Conclusion:................................................................................................................................7

Answer to question 4:.................................................................................................................7

Answer to question 5:.................................................................................................................8

Issue:..........................................................................................................................................8

Rule:...........................................................................................................................................8

Table of Contents

Answer to question 1:.................................................................................................................3

Issue:..........................................................................................................................................3

Rule:...........................................................................................................................................3

Application:................................................................................................................................3

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to question 2:.................................................................................................................4

Issue:..........................................................................................................................................4

Rule:...........................................................................................................................................4

Application:................................................................................................................................4

Conclusion:................................................................................................................................5

Answer to question 3:.................................................................................................................5

Issue:..........................................................................................................................................5

Rule:...........................................................................................................................................6

Application:................................................................................................................................6

Conclusion:................................................................................................................................7

Answer to question 4:.................................................................................................................7

Answer to question 5:.................................................................................................................8

Issue:..........................................................................................................................................8

Rule:...........................................................................................................................................8

2TAXATION LAW

Applications:..............................................................................................................................9

Conclusion:..............................................................................................................................10

Reference list:...........................................................................................................................11

Applications:..............................................................................................................................9

Conclusion:..............................................................................................................................10

Reference list:...........................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

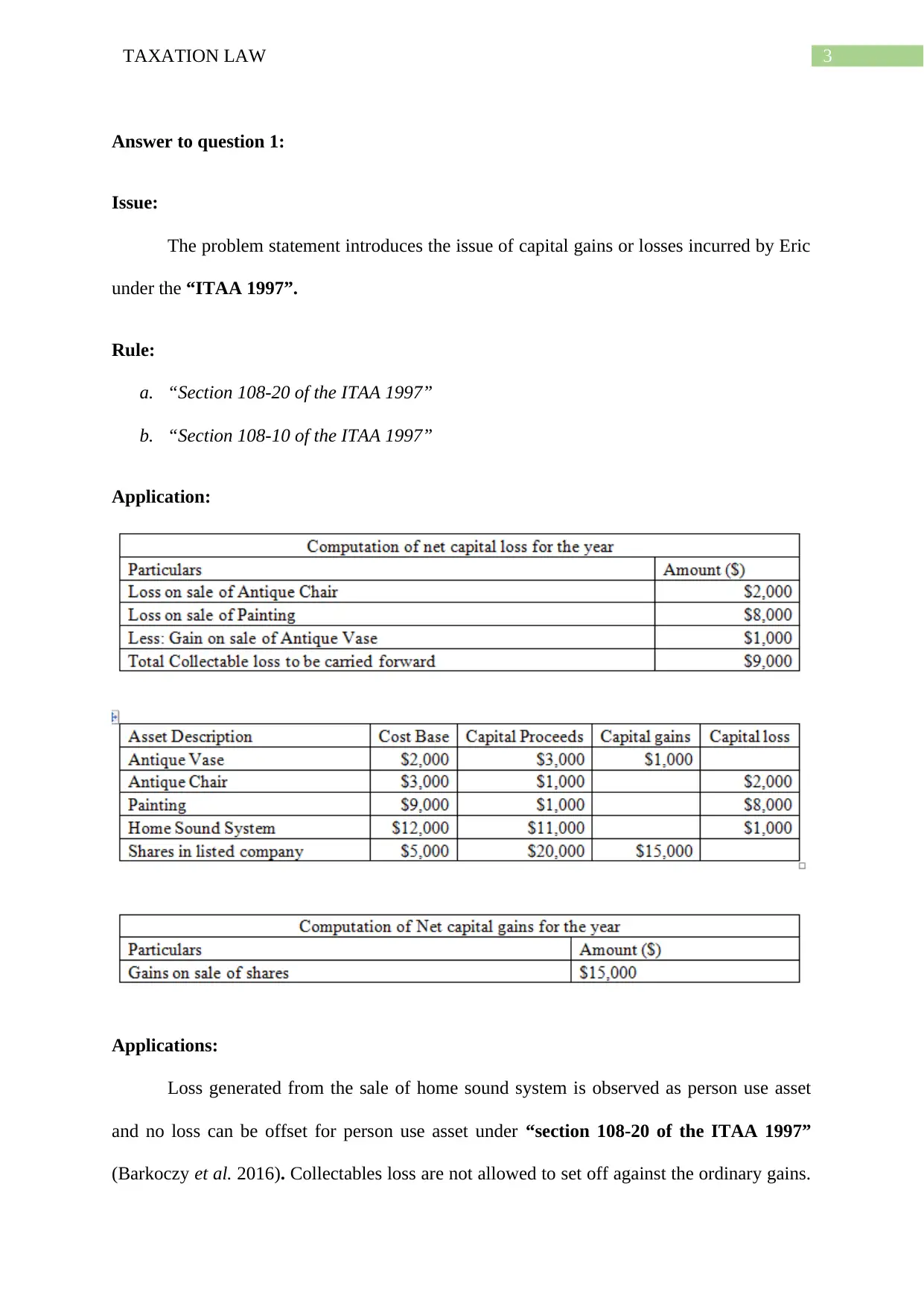

Answer to question 1:

Issue:

The problem statement introduces the issue of capital gains or losses incurred by Eric

under the “ITAA 1997”.

Rule:

a. “Section 108-20 of the ITAA 1997”

b. “Section 108-10 of the ITAA 1997”

Application:

Applications:

Loss generated from the sale of home sound system is observed as person use asset

and no loss can be offset for person use asset under “section 108-20 of the ITAA 1997”

(Barkoczy et al. 2016). Collectables loss are not allowed to set off against the ordinary gains.

Answer to question 1:

Issue:

The problem statement introduces the issue of capital gains or losses incurred by Eric

under the “ITAA 1997”.

Rule:

a. “Section 108-20 of the ITAA 1997”

b. “Section 108-10 of the ITAA 1997”

Application:

Applications:

Loss generated from the sale of home sound system is observed as person use asset

and no loss can be offset for person use asset under “section 108-20 of the ITAA 1997”

(Barkoczy et al. 2016). Collectables loss are not allowed to set off against the ordinary gains.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Eric derived collectable loss and the same is disallowed from being considered for offset

under “section 108-10 of the ITAA 1997”. Eric only made gains from the sale of share so

his capital gains for the year stands $15,000.

Conclusion:

The above analysis defines that losses from collectables and personal use assets are

not allowed for offset from the ordinary gains since Eric only derived gains from sale of

shares.

Answer to question 2:

Issue:

The statement brings in the issue of Fringe Benefit Tax relating to the offset of

interest payment at the end of the loan period.

Rule:

a. Taxation rulings of TR 93/6

b. Fringe Benefit Tax Assessment Act 1986

Application:

As bought forward by the “taxation rulings of TR 93/6” banks and financial

institutions on certain occasions makes arrangement of interest offset for loan accounts. Such

arrangement enables the customers to offset the loan interest and they are simultaneously not

required for paying any income tax (Coleman and Sadiq 2016). In conformity with the

taxation ruling of “Taxation rulings of TR 93/6” if Brian is freed from paying interest at the

end of the loan period rather than paying at monthly instalment then he will be not required to

pay any form of income tax for such interest offset.

Eric derived collectable loss and the same is disallowed from being considered for offset

under “section 108-10 of the ITAA 1997”. Eric only made gains from the sale of share so

his capital gains for the year stands $15,000.

Conclusion:

The above analysis defines that losses from collectables and personal use assets are

not allowed for offset from the ordinary gains since Eric only derived gains from sale of

shares.

Answer to question 2:

Issue:

The statement brings in the issue of Fringe Benefit Tax relating to the offset of

interest payment at the end of the loan period.

Rule:

a. Taxation rulings of TR 93/6

b. Fringe Benefit Tax Assessment Act 1986

Application:

As bought forward by the “taxation rulings of TR 93/6” banks and financial

institutions on certain occasions makes arrangement of interest offset for loan accounts. Such

arrangement enables the customers to offset the loan interest and they are simultaneously not

required for paying any income tax (Coleman and Sadiq 2016). In conformity with the

taxation ruling of “Taxation rulings of TR 93/6” if Brian is freed from paying interest at the

end of the loan period rather than paying at monthly instalment then he will be not required to

pay any form of income tax for such interest offset.

5TAXATION LAW

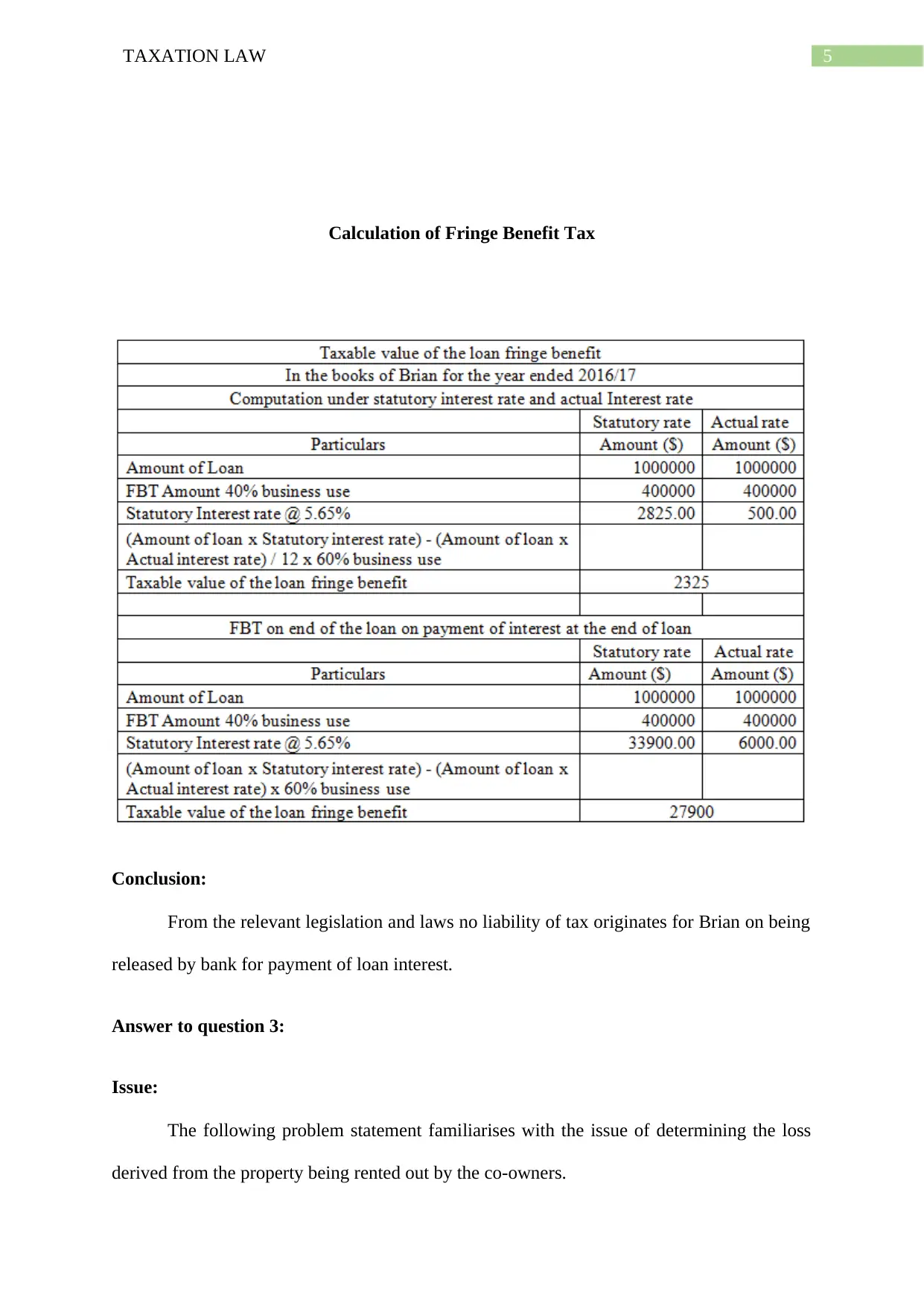

Calculation of Fringe Benefit Tax

Conclusion:

From the relevant legislation and laws no liability of tax originates for Brian on being

released by bank for payment of loan interest.

Answer to question 3:

Issue:

The following problem statement familiarises with the issue of determining the loss

derived from the property being rented out by the co-owners.

Calculation of Fringe Benefit Tax

Conclusion:

From the relevant legislation and laws no liability of tax originates for Brian on being

released by bank for payment of loan interest.

Answer to question 3:

Issue:

The following problem statement familiarises with the issue of determining the loss

derived from the property being rented out by the co-owners.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Rule:

a. “Taxation rulings of TR 93/32”

b. “F.C. of T. v McDonald (1987)”

c. “Section 51 of the ITAA 1997”

Application:

An elucidation relating to the distribution of the net income or loss incurred by the co-

owners of the rental property has been defined under the “taxation ruling of TR 93/32”. The

aforesaid ruling assess the assessable position of the joint owners that are engaged in the

business of rental property and their activities are not accounted as execution of business

activities (Harris et al. 2015). The problem statement introduces the circumstances of Jack

and Jill who agreed to purchase a rental property and letting out the same as the joint owners.

The clause contained that Jack will be only getting 10% of the profit from the

property whereas Jill will be getting 90% share of the profit from the property. The clause

further contained an agreement that Jack will be shouldering the entire amount of loss derived

from such property. The aforesaid “Taxation ruling of 93/32” puts forward that joint owners

of the rental property is accounted as partnership under the purview of income tax (Kenny

2013). Nevertheless, it is disallowed from being viewed as partnership under the general law.

The ruling further defines that the joint owners are not regarded as the partners under

the context of the general law with the agreement of partnership whether in writing or orally

hardly has any kind of effect on the distribution of the income or loss derived from such

property (Kenny, Blissenden and Villios 2017). Jack and Jill under the case study are viewed

as the partners in context of the income tax and the business activities does not accounts to be

partnership under the general law. The co-ownership between them are usually held as joint

tenants or tenants in common.

Rule:

a. “Taxation rulings of TR 93/32”

b. “F.C. of T. v McDonald (1987)”

c. “Section 51 of the ITAA 1997”

Application:

An elucidation relating to the distribution of the net income or loss incurred by the co-

owners of the rental property has been defined under the “taxation ruling of TR 93/32”. The

aforesaid ruling assess the assessable position of the joint owners that are engaged in the

business of rental property and their activities are not accounted as execution of business

activities (Harris et al. 2015). The problem statement introduces the circumstances of Jack

and Jill who agreed to purchase a rental property and letting out the same as the joint owners.

The clause contained that Jack will be only getting 10% of the profit from the

property whereas Jill will be getting 90% share of the profit from the property. The clause

further contained an agreement that Jack will be shouldering the entire amount of loss derived

from such property. The aforesaid “Taxation ruling of 93/32” puts forward that joint owners

of the rental property is accounted as partnership under the purview of income tax (Kenny

2013). Nevertheless, it is disallowed from being viewed as partnership under the general law.

The ruling further defines that the joint owners are not regarded as the partners under

the context of the general law with the agreement of partnership whether in writing or orally

hardly has any kind of effect on the distribution of the income or loss derived from such

property (Kenny, Blissenden and Villios 2017). Jack and Jill under the case study are viewed

as the partners in context of the income tax and the business activities does not accounts to be

partnership under the general law. The co-ownership between them are usually held as joint

tenants or tenants in common.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Quoting the incidence of “F.C. of T. v McDonald (1987)” where the co-owners

partnership accounted for income tax purpose but was not regarded as partnership under the

general law (Keyzer, Goff and Fisher 2015). The judgement denoted that though the

taxpayers constituted to be co-owners in text of the law and justice however the losses must

be shared among the respondents equally. Similarly in the situation of Jack and Jill no form

of deductions is allowed by virtue of the agreement with the respondents are entitled for

shouldering one-half of the loss as well. Jack was indulged in two important detriments. In

the initial stages Jack provided a large portion of the income to his wife Jill and covered her

investment from any kind of loss. The presumption relating to the loss sharing was willingly

made by Jack which wholly formed a domestic arrangement of covering the finance of his

wife Jill. Therefore, section 51 disallows deductions of loss by virtue of partnership

agreement.

In the second part of the problem statement, if both Jack and Jill decides to sell the

property then it is imperative to determine the cost base and lowered cost of the property that

must be included in the amount that was paid to acquire the property. Consequently the

capital gains and loss must be shared in accordance with the interest of ownership in the

rental property (Krever 2013).

Conclusion:

The problem statement can be bought to an end by stating that the no partnership

existed under the context of general law and one-half of the loss should be allocated to the

respondents.

Answer to question 4:

On denoting the event of tax avoidance, the case of “IRC v Duke of

Westminster [1936]” has been quoted on numerous occasion (Sadiq 2016). Duke under this

Quoting the incidence of “F.C. of T. v McDonald (1987)” where the co-owners

partnership accounted for income tax purpose but was not regarded as partnership under the

general law (Keyzer, Goff and Fisher 2015). The judgement denoted that though the

taxpayers constituted to be co-owners in text of the law and justice however the losses must

be shared among the respondents equally. Similarly in the situation of Jack and Jill no form

of deductions is allowed by virtue of the agreement with the respondents are entitled for

shouldering one-half of the loss as well. Jack was indulged in two important detriments. In

the initial stages Jack provided a large portion of the income to his wife Jill and covered her

investment from any kind of loss. The presumption relating to the loss sharing was willingly

made by Jack which wholly formed a domestic arrangement of covering the finance of his

wife Jill. Therefore, section 51 disallows deductions of loss by virtue of partnership

agreement.

In the second part of the problem statement, if both Jack and Jill decides to sell the

property then it is imperative to determine the cost base and lowered cost of the property that

must be included in the amount that was paid to acquire the property. Consequently the

capital gains and loss must be shared in accordance with the interest of ownership in the

rental property (Krever 2013).

Conclusion:

The problem statement can be bought to an end by stating that the no partnership

existed under the context of general law and one-half of the loss should be allocated to the

respondents.

Answer to question 4:

On denoting the event of tax avoidance, the case of “IRC v Duke of

Westminster [1936]” has been quoted on numerous occasion (Sadiq 2016). Duke under this

8TAXATION LAW

appointed a gardener and the salary that was paid to the gardener in the form of post-tax

profit of Duke. With the objective of avoiding tax Duke stopped the payment of the salary of

the gardener and drew up a covenant of identical sum. As the expenditure incurred was

allowed for income tax deductions this ultimately reduced the tax liability of Duke. A

suitable method of reducing the taxable income are used by the individual and it was

understood that if a legal method is employed in reducing the taxable burden then an

individual cannot be forced to pay anything more than the tax amount.

In contrary to this, the principles of WT Ramsay v. IRC was used to li9mit the

practices of the tax avoidance used by the individual taxpayers (Milton 2013). The principle

established that there should be commercial motive attached to the transaction. If the

commercial transaction carries pre-arranged ambiguous steps that does not render any

commercial purpose rather than saving tax, then the suitable approach is to levy tax on the

degree of commercial transaction as the whole.

In the current age of Australia, if a person is successful in ordering tax assignment

with the purpose of securing the results, the taxpayers could not be in their ingenuity be

forced to pay any higher amount of tax (Woellner 2013). It is depicted from the decision that

the commercial entities and the individual taxpayer are allowed to structure their financial

reports for the purpose of reducing tax in a manner that the structure is inside the concept of

law.

Answer to question 5:

Issue:

The primary issue of this problem statement is ascertaining the income produced from

the activities of primary producer engaged in the activities of forestry.

appointed a gardener and the salary that was paid to the gardener in the form of post-tax

profit of Duke. With the objective of avoiding tax Duke stopped the payment of the salary of

the gardener and drew up a covenant of identical sum. As the expenditure incurred was

allowed for income tax deductions this ultimately reduced the tax liability of Duke. A

suitable method of reducing the taxable income are used by the individual and it was

understood that if a legal method is employed in reducing the taxable burden then an

individual cannot be forced to pay anything more than the tax amount.

In contrary to this, the principles of WT Ramsay v. IRC was used to li9mit the

practices of the tax avoidance used by the individual taxpayers (Milton 2013). The principle

established that there should be commercial motive attached to the transaction. If the

commercial transaction carries pre-arranged ambiguous steps that does not render any

commercial purpose rather than saving tax, then the suitable approach is to levy tax on the

degree of commercial transaction as the whole.

In the current age of Australia, if a person is successful in ordering tax assignment

with the purpose of securing the results, the taxpayers could not be in their ingenuity be

forced to pay any higher amount of tax (Woellner 2013). It is depicted from the decision that

the commercial entities and the individual taxpayer are allowed to structure their financial

reports for the purpose of reducing tax in a manner that the structure is inside the concept of

law.

Answer to question 5:

Issue:

The primary issue of this problem statement is ascertaining the income produced from

the activities of primary producer engaged in the activities of forestry.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Rule:

a. Subsection 6 (1) of the ITAA 1936

b. McCauley v. The Federal Commissioner of Taxation (1944)

c. Subsection 36(1)

d. section 26 (f)

Applications:

The case study opens up by stating that Bill owned a large land that had wide amount

of pine trees on it. Bill at the initial stages thought of cattle grazing. Later a logging company

arrived with the offer of paying Bill a sum of $1,000 for every 100 meter of timber the

logging can cut from his land. An important considerations from the taxation rulings of TR

95/6” has been denoted that puts forward the outcomes relating to income tax arising out of

the operations of primary productions and forestry (Pyrmont 2014).

The previously mentioned ruling effectively puts forward that a person generating

returns from the sale of timber would be viewed as assessable income from the forestry

activities irrespective of the fact that the person was engaged in the functions of forestry

activities (Grange, Jover and Maydew 2014). The ruling is imposed on person carrying on the

forestry operations as well as on those that are not engaged in the functions of forestry

operations but sells timber for earning incomes. According to the proviso of “subsection 6

(1) of the ITAA 1936” a person getting involve in the forestry operations are treated as

primary producer under the purview of income tax if it is found that forestry operations

becomes the portion of business functions (James 2013).

Under the context of the “subsection 6 (1) of the ITAA 1936” the definition of

primary producer represents planting and cutting of timber in a cultivated area that is planted

with the objective of felling or cutting down the trees in the cultivated area or a forest (Jover

Rule:

a. Subsection 6 (1) of the ITAA 1936

b. McCauley v. The Federal Commissioner of Taxation (1944)

c. Subsection 36(1)

d. section 26 (f)

Applications:

The case study opens up by stating that Bill owned a large land that had wide amount

of pine trees on it. Bill at the initial stages thought of cattle grazing. Later a logging company

arrived with the offer of paying Bill a sum of $1,000 for every 100 meter of timber the

logging can cut from his land. An important considerations from the taxation rulings of TR

95/6” has been denoted that puts forward the outcomes relating to income tax arising out of

the operations of primary productions and forestry (Pyrmont 2014).

The previously mentioned ruling effectively puts forward that a person generating

returns from the sale of timber would be viewed as assessable income from the forestry

activities irrespective of the fact that the person was engaged in the functions of forestry

activities (Grange, Jover and Maydew 2014). The ruling is imposed on person carrying on the

forestry operations as well as on those that are not engaged in the functions of forestry

operations but sells timber for earning incomes. According to the proviso of “subsection 6

(1) of the ITAA 1936” a person getting involve in the forestry operations are treated as

primary producer under the purview of income tax if it is found that forestry operations

becomes the portion of business functions (James 2013).

Under the context of the “subsection 6 (1) of the ITAA 1936” the definition of

primary producer represents planting and cutting of timber in a cultivated area that is planted

with the objective of felling or cutting down the trees in the cultivated area or a forest (Jover

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

2014). The evidence supported in the case study represents that Bill must be treated as

primary producer for being indulgent in the functions of primary production in context of

“subsection 6 (1) of the ITAA 1997” for agreeing to felling down the trees in a land that he

owned.

The forestry processes also defines that an individual would be still considered to be

involved in the activities of forestry operations even though the trees in the vegetation were

not planted for felling them (Anderson, Dickfos and Brown 2016). In the present case study,

Bill did not planted those pine trees for the purpose of felling it however the revenue derived

from the felling of trees would be treated as earnings for Bill and would have income tax

consequences. The reason for considering the income as taxable income is because the pine

trees constituted a part of the business assets and the receipt of income from felling of such

trees constituted taxable income under subsection 36(1).

On the other side of problem statement, if Bill is paid with a large amount of $50,000

by giving the right to the logging firm of cutting the timber as much as they want then such

kind of amount received would be accounted as “Royalties” under “section 26 (f)”. The

receipt of large sum of money represents royalties which represents that the right was granted

to cut down the trees. Bill as a consequence of this will not be treated as primary producer

since he did not planted the pine trees for sale. Quoting the reference of “McCauley v. F. C

of T (1944)” amount received for granting the rights of removing the trees represents the

right of doing so (Barkoczy 2016). Therefore, the sum of $50,000 would be treated as

royalties for Bill and are subjected to income tax under section 26 (f) of the act.

Conclusion:

As denoted from the assessment, that cutting of timber and selling the same would be

treated as royalties and would be liable for tax.

2014). The evidence supported in the case study represents that Bill must be treated as

primary producer for being indulgent in the functions of primary production in context of

“subsection 6 (1) of the ITAA 1997” for agreeing to felling down the trees in a land that he

owned.

The forestry processes also defines that an individual would be still considered to be

involved in the activities of forestry operations even though the trees in the vegetation were

not planted for felling them (Anderson, Dickfos and Brown 2016). In the present case study,

Bill did not planted those pine trees for the purpose of felling it however the revenue derived

from the felling of trees would be treated as earnings for Bill and would have income tax

consequences. The reason for considering the income as taxable income is because the pine

trees constituted a part of the business assets and the receipt of income from felling of such

trees constituted taxable income under subsection 36(1).

On the other side of problem statement, if Bill is paid with a large amount of $50,000

by giving the right to the logging firm of cutting the timber as much as they want then such

kind of amount received would be accounted as “Royalties” under “section 26 (f)”. The

receipt of large sum of money represents royalties which represents that the right was granted

to cut down the trees. Bill as a consequence of this will not be treated as primary producer

since he did not planted the pine trees for sale. Quoting the reference of “McCauley v. F. C

of T (1944)” amount received for granting the rights of removing the trees represents the

right of doing so (Barkoczy 2016). Therefore, the sum of $50,000 would be treated as

royalties for Bill and are subjected to income tax under section 26 (f) of the act.

Conclusion:

As denoted from the assessment, that cutting of timber and selling the same would be

treated as royalties and would be liable for tax.

11TAXATION LAW

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.