University Taxation Law Case Study Assignment Analysis

VerifiedAdded on 2023/04/19

|11

|2499

|273

Homework Assignment

AI Summary

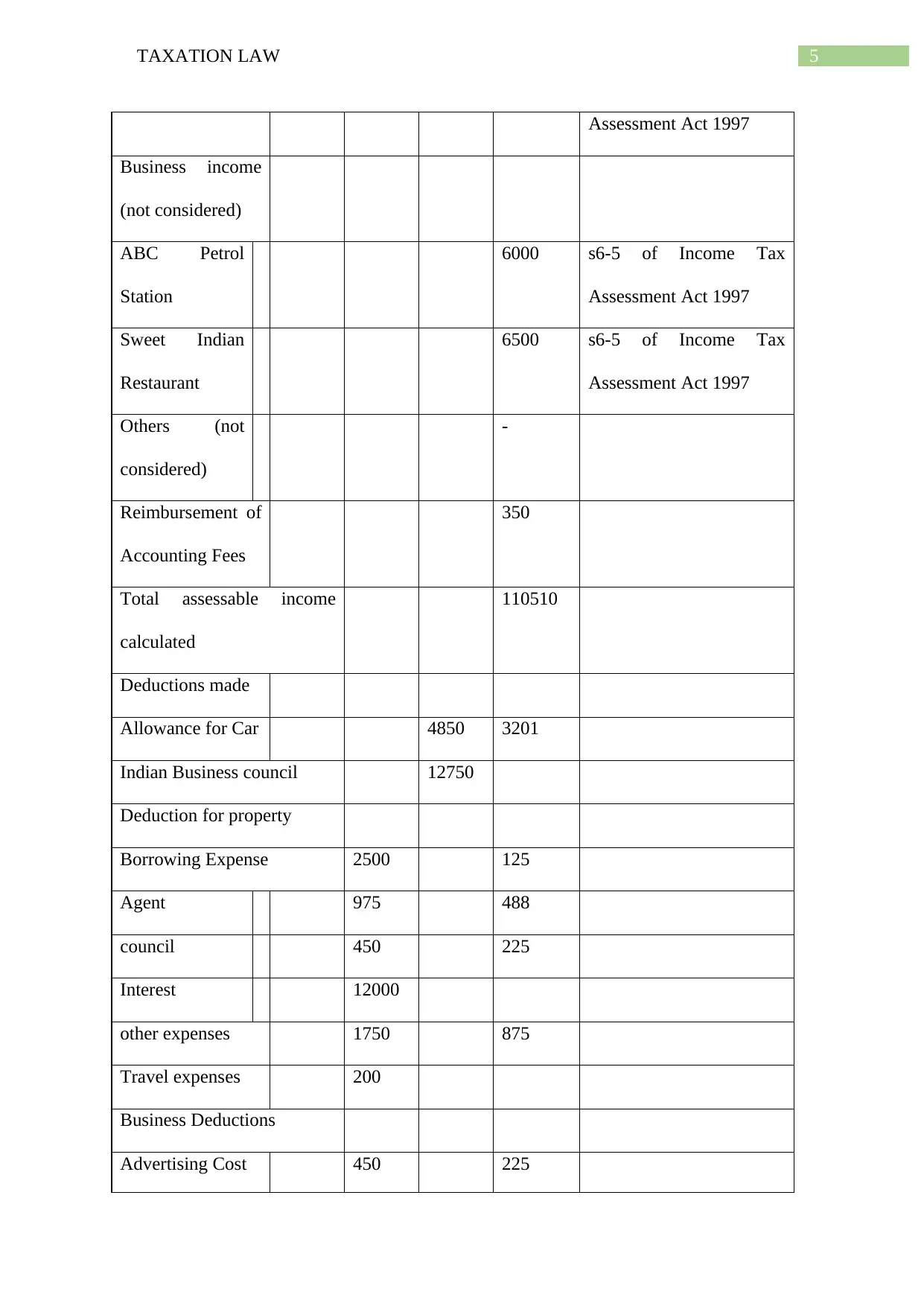

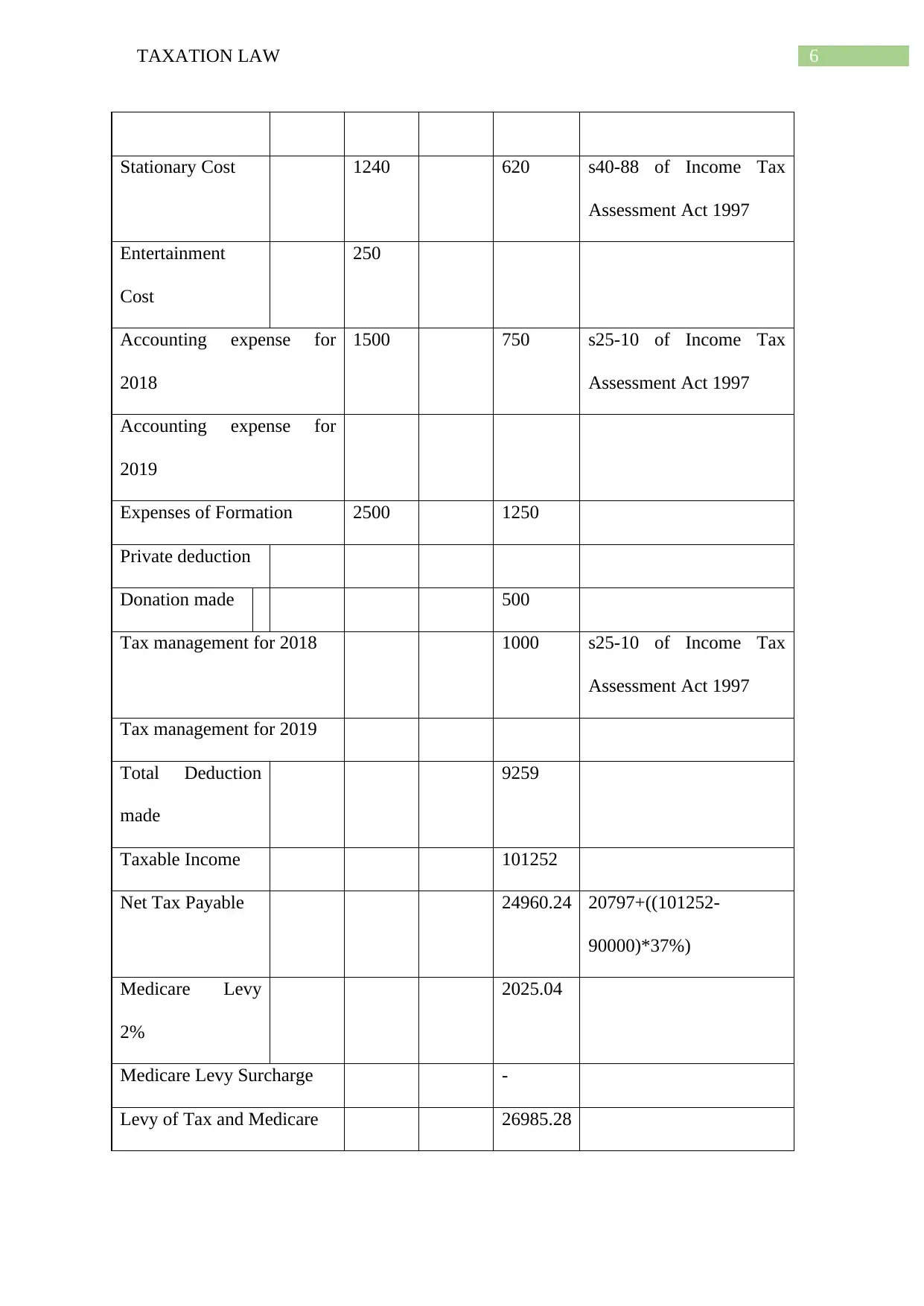

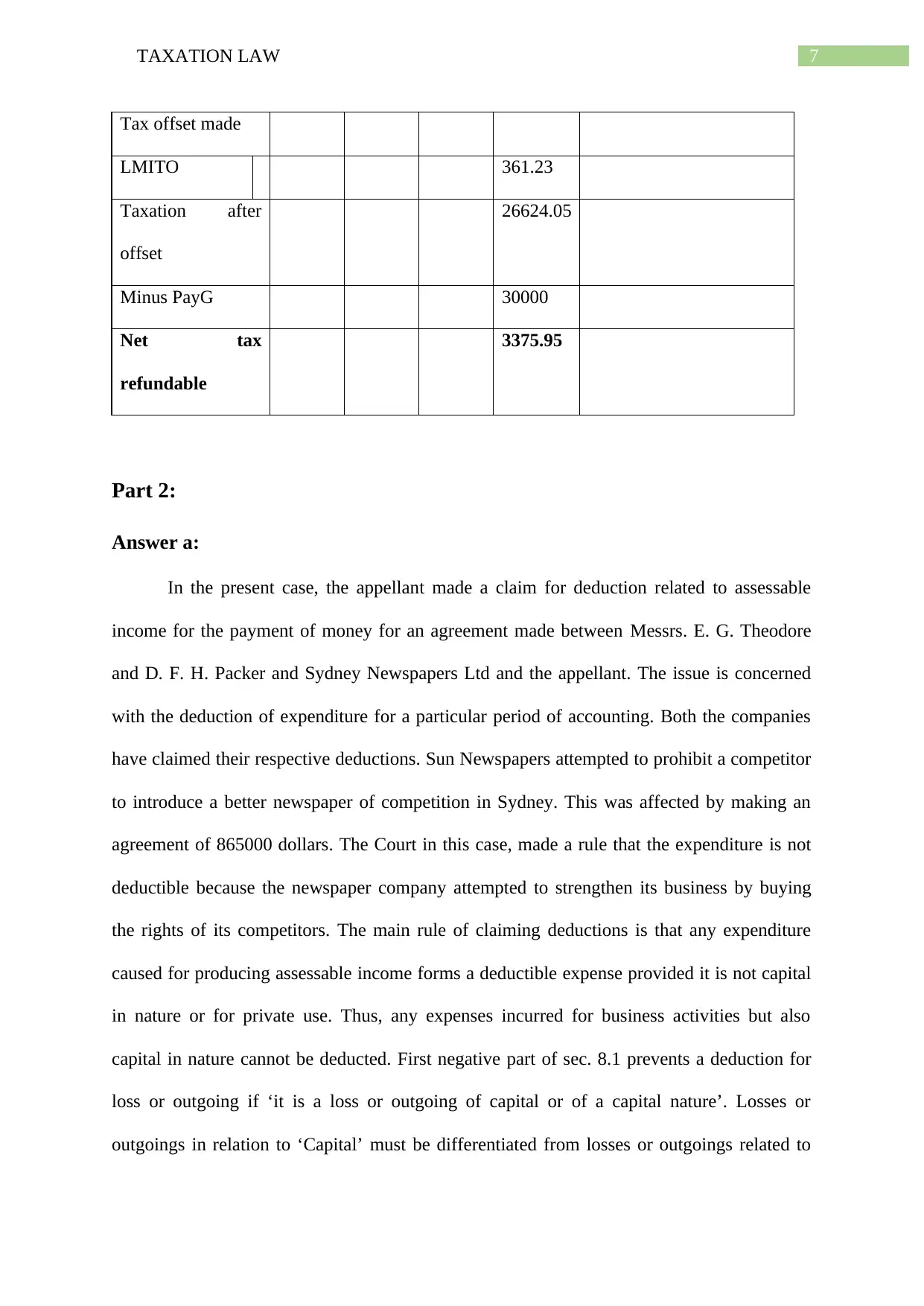

This assignment delves into a taxation law case study, examining the tax residency status of an individual, Arun Sharma, and determining his tax obligations for the financial year 2018-2019. The analysis applies relevant rules of law, including the Resides test under Common law and factors outlined in Taxation Ruling 98/17, to establish Arun's Australian residency. The assignment then calculates Arun's assessable income, considering salary, car allowance, gifts, and business income, while differentiating between ordinary income and windfall gains. It also addresses deductible expenses, referencing sections of the Income Tax Assessment Act 1997 (ITAA 97) to determine allowable deductions. Part 2 of the assignment focuses on expenditure deductibility, analyzing a court case concerning the deduction of expenses for strengthening a business. The assignment discusses tests like the 'enduring benefit', 'business entity' and 'once and for all' to differentiate between capital and revenue expenditures. The document concludes with a detailed tax calculation, including taxable income, net tax payable, and tax offsets.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.