Taxation Law: Analysis of Tax Issues, Scenarios and Relevant Laws

VerifiedAdded on 2019/10/30

|14

|2345

|356

Homework Assignment

AI Summary

This taxation law assignment provides detailed answers to five key tax-related questions. The analysis covers issues related to capital gains and losses, the computation of Fringe Benefit Tax (FBT), the distribution of losses from jointly owned rental property, the legality of tax avoidance, and the tax implications of cutting down timber. Each answer includes relevant laws, applications of those laws to the given scenarios, and conclusions. The assignment references key sections of the ITAA 1997 and ITAA 1936, taxation rulings (TR), and relevant case law, such as IRC v Duke Westminster and McCauley v FC of T. The document explores the tax treatment of various scenarios, including the offset of capital losses, FBT on loan interest, the allocation of rental property losses between joint owners, the legal implications of tax avoidance strategies, and the taxation of income derived from timber operations, including the distinction between income from felling timber and royalties received for granting timber rights.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issue:..........................................................................................................................................2

Laws:..........................................................................................................................................2

Applications...............................................................................................................................2

Application:................................................................................................................................3

Conclusion:................................................................................................................................3

Answer to question 2:.................................................................................................................3

Issue:..........................................................................................................................................3

Laws:..........................................................................................................................................3

Applications:..............................................................................................................................4

Applications:..............................................................................................................................4

Conclusion:................................................................................................................................5

Answer to question 3:.................................................................................................................5

Issue:..........................................................................................................................................5

Laws:..........................................................................................................................................5

Applications:..............................................................................................................................5

Conclusion:................................................................................................................................7

Answer to question 4:.................................................................................................................7

Answer to question 5:.................................................................................................................8

Issue:..........................................................................................................................................8

Table of Contents

Answer to question 1:.................................................................................................................2

Issue:..........................................................................................................................................2

Laws:..........................................................................................................................................2

Applications...............................................................................................................................2

Application:................................................................................................................................3

Conclusion:................................................................................................................................3

Answer to question 2:.................................................................................................................3

Issue:..........................................................................................................................................3

Laws:..........................................................................................................................................3

Applications:..............................................................................................................................4

Applications:..............................................................................................................................4

Conclusion:................................................................................................................................5

Answer to question 3:.................................................................................................................5

Issue:..........................................................................................................................................5

Laws:..........................................................................................................................................5

Applications:..............................................................................................................................5

Conclusion:................................................................................................................................7

Answer to question 4:.................................................................................................................7

Answer to question 5:.................................................................................................................8

Issue:..........................................................................................................................................8

2TAXATION LAW

Laws:..........................................................................................................................................8

Application:................................................................................................................................8

Conclusion:..............................................................................................................................10

Reference list:...........................................................................................................................11

Laws:..........................................................................................................................................8

Application:................................................................................................................................8

Conclusion:..............................................................................................................................10

Reference list:...........................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

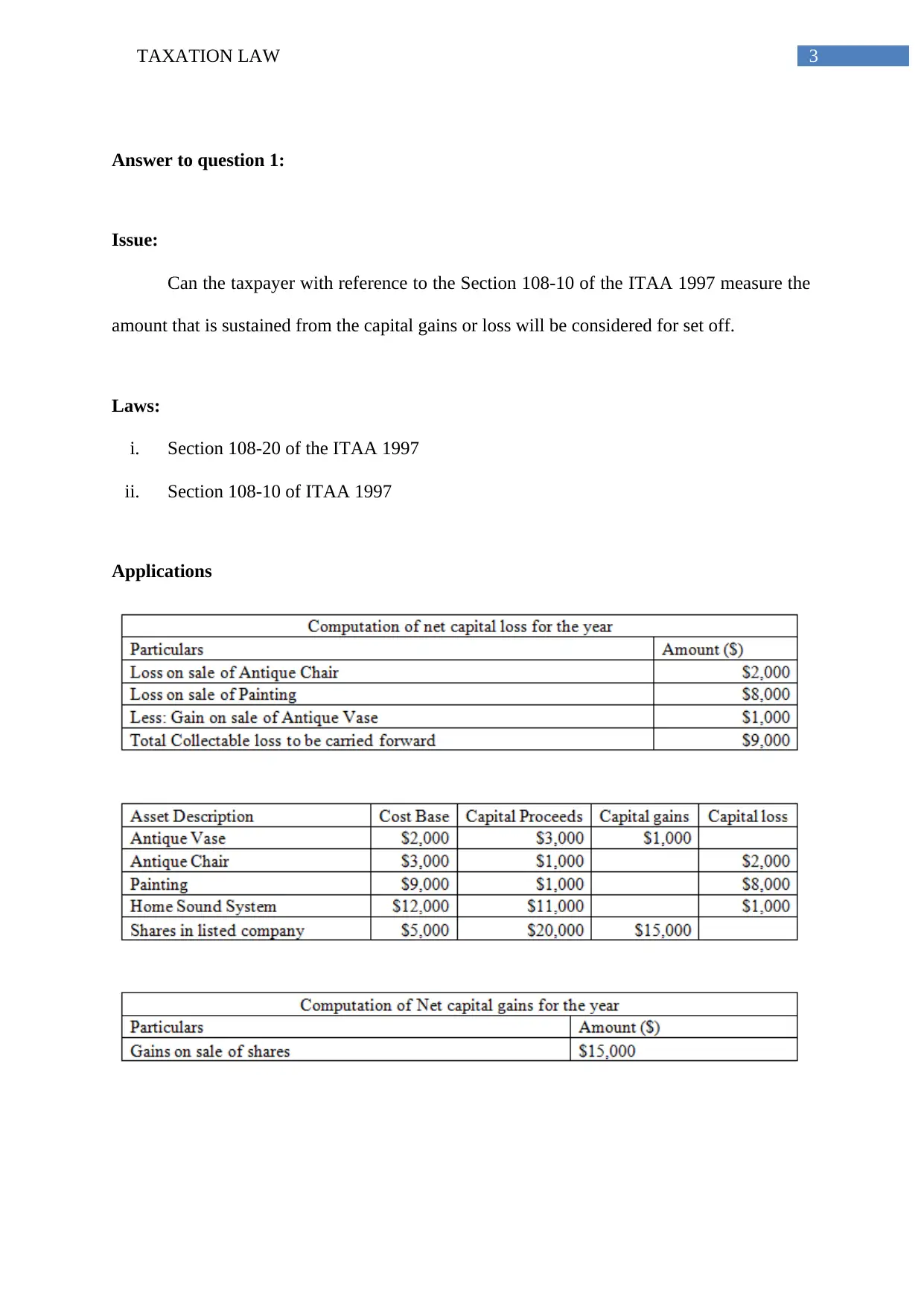

Answer to question 1:

Issue:

Can the taxpayer with reference to the Section 108-10 of the ITAA 1997 measure the

amount that is sustained from the capital gains or loss will be considered for set off.

Laws:

i. Section 108-20 of the ITAA 1997

ii. Section 108-10 of ITAA 1997

Applications

Answer to question 1:

Issue:

Can the taxpayer with reference to the Section 108-10 of the ITAA 1997 measure the

amount that is sustained from the capital gains or loss will be considered for set off.

Laws:

i. Section 108-20 of the ITAA 1997

ii. Section 108-10 of ITAA 1997

Applications

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Application:

The current circumstances of the taxpayer states that the loss that is sustained from the

sale of the sound system will be not be approved for set off. This is because loss originating

from the sale of the home sound system having a nature of personal asset will not be allowed

for set off. The guiding principles of section 108-10 of ITAA 1997 gives the evidence that

loss of collectable nature cannot be considered for offset against the ordinary gains from the

sale of shares will not be allowed for set off (Coleman & Sadiq, 2017). In consistency with

the section 108-10 of the ITAA 1997 Eric produced profits on the event of sale of ordinary

assets with no existent year capital or any form of reductions that are pertinent. Consequently

the capital gains for Eric was arrived at $15,000.

Conclusion:

From the conversation it is found that Eric will not be able to set off the loss sustained

from the collectibles because he solely derived revenue upon the sale of the assets of ordinary

nature.

Answer to question 2:

Issue:

The scenario introduces the issue that deals with the computation of FBT that has been

defined under the fringe benefit act 1986.

Laws:

i. Fringe Benefit Tax Act 1986

ii. Taxation Rulings TR 93/6

Application:

The current circumstances of the taxpayer states that the loss that is sustained from the

sale of the sound system will be not be approved for set off. This is because loss originating

from the sale of the home sound system having a nature of personal asset will not be allowed

for set off. The guiding principles of section 108-10 of ITAA 1997 gives the evidence that

loss of collectable nature cannot be considered for offset against the ordinary gains from the

sale of shares will not be allowed for set off (Coleman & Sadiq, 2017). In consistency with

the section 108-10 of the ITAA 1997 Eric produced profits on the event of sale of ordinary

assets with no existent year capital or any form of reductions that are pertinent. Consequently

the capital gains for Eric was arrived at $15,000.

Conclusion:

From the conversation it is found that Eric will not be able to set off the loss sustained

from the collectibles because he solely derived revenue upon the sale of the assets of ordinary

nature.

Answer to question 2:

Issue:

The scenario introduces the issue that deals with the computation of FBT that has been

defined under the fringe benefit act 1986.

Laws:

i. Fringe Benefit Tax Act 1986

ii. Taxation Rulings TR 93/6

5TAXATION LAW

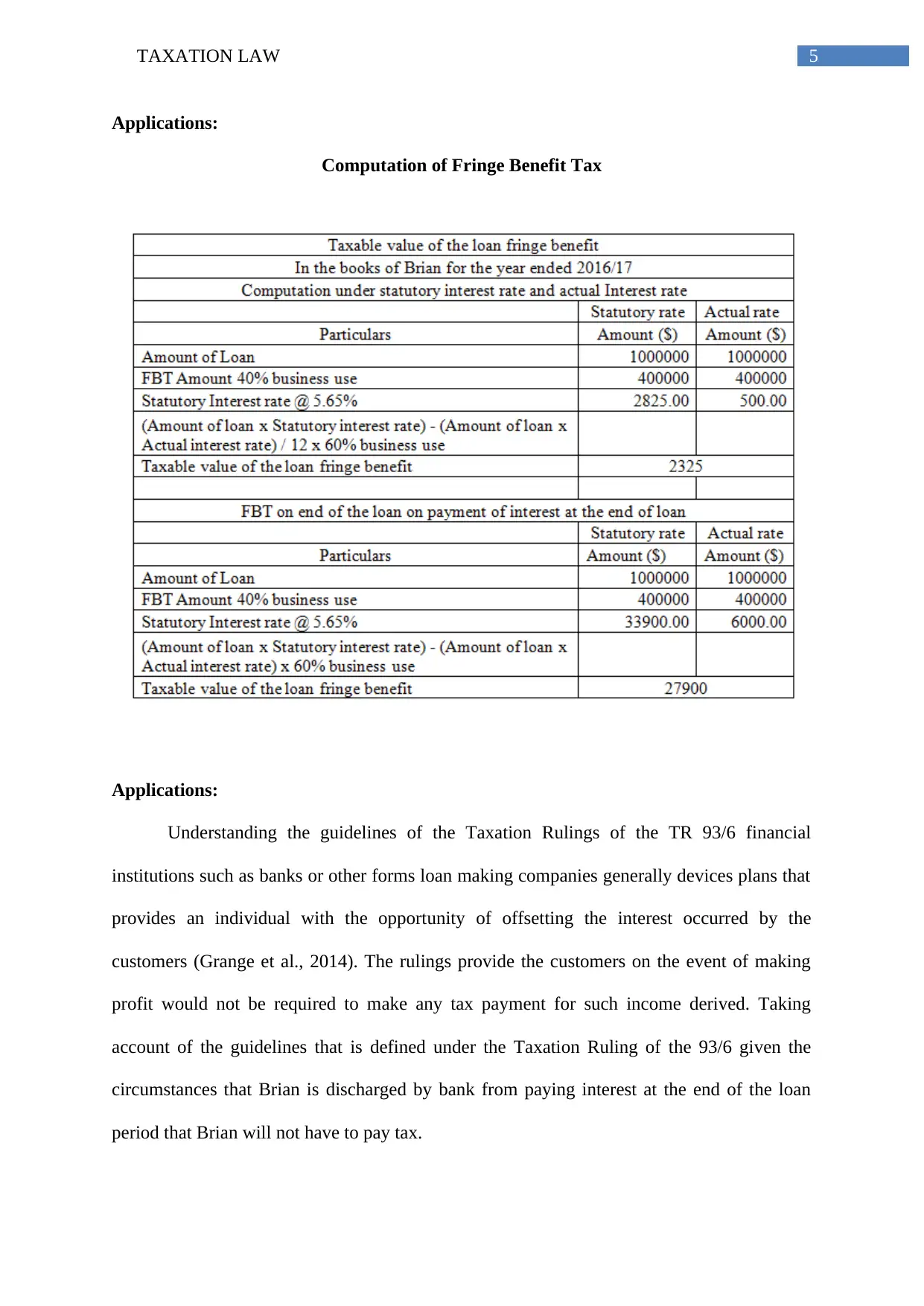

Applications:

Computation of Fringe Benefit Tax

Applications:

Understanding the guidelines of the Taxation Rulings of the TR 93/6 financial

institutions such as banks or other forms loan making companies generally devices plans that

provides an individual with the opportunity of offsetting the interest occurred by the

customers (Grange et al., 2014). The rulings provide the customers on the event of making

profit would not be required to make any tax payment for such income derived. Taking

account of the guidelines that is defined under the Taxation Ruling of the 93/6 given the

circumstances that Brian is discharged by bank from paying interest at the end of the loan

period that Brian will not have to pay tax.

Applications:

Computation of Fringe Benefit Tax

Applications:

Understanding the guidelines of the Taxation Rulings of the TR 93/6 financial

institutions such as banks or other forms loan making companies generally devices plans that

provides an individual with the opportunity of offsetting the interest occurred by the

customers (Grange et al., 2014). The rulings provide the customers on the event of making

profit would not be required to make any tax payment for such income derived. Taking

account of the guidelines that is defined under the Taxation Ruling of the 93/6 given the

circumstances that Brian is discharged by bank from paying interest at the end of the loan

period that Brian will not have to pay tax.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Conclusion:

From the above conversation it is understood, if the loan interest is payable at the end

of the loan then no income tax is required to be paid by him to the bank.

Answer to question 3:

Issue:

The following matter is linked with the distribution of loss that is sustained by

taxpayers in this context from joint ownership of the rental property.

Laws:

i. FC of T v McDonald

ii. Section 51 of the ITAA 1997

iii. Taxation ruling TR 93/23

Applications:

In conformity with the Taxation Ruling TR 93/32 guidelines has been defined under

this rulings that provides the explanation arising from the division of the income or any form

of loss derived from the rent property amid the joint owners of the property (James, 2015).

Moreover, the above discussed ruling lay down the guidelines of gauging into the assessable

position of the co-owners that are not accountable for carrying on the business within the

defined activities. Jack and Jill in this context are being evaluated on their assessable position

from the property that is rented by them. Jack in this context will be eligible for 10% of the

profits from the property and Jill will be getting 90% profits from the rented property.

Conclusion:

From the above conversation it is understood, if the loan interest is payable at the end

of the loan then no income tax is required to be paid by him to the bank.

Answer to question 3:

Issue:

The following matter is linked with the distribution of loss that is sustained by

taxpayers in this context from joint ownership of the rental property.

Laws:

i. FC of T v McDonald

ii. Section 51 of the ITAA 1997

iii. Taxation ruling TR 93/23

Applications:

In conformity with the Taxation Ruling TR 93/32 guidelines has been defined under

this rulings that provides the explanation arising from the division of the income or any form

of loss derived from the rent property amid the joint owners of the property (James, 2015).

Moreover, the above discussed ruling lay down the guidelines of gauging into the assessable

position of the co-owners that are not accountable for carrying on the business within the

defined activities. Jack and Jill in this context are being evaluated on their assessable position

from the property that is rented by them. Jack in this context will be eligible for 10% of the

profits from the property and Jill will be getting 90% profits from the rented property.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

As it has been defined under the TR 92/32 joint ownership of the rental property can

be defined as the partnership for the purpose of income tax however it is not concerned with

the partnership that is defined under the notion of general law (Jover, 2014). The ruling does

not include the joint ownership of any business practice that meets the purpose of the income

tax. The loss of income that is sustained from the rented property is administered with the

help of joint ownership together with the allocation of profits and losses. It is understood

from the current context of Jack and Jill the joint ownership of rented property forms the

foundations of the income tax and will not be accounted as the partnership in regard to the

principles of general law.

The principles of Taxation ruling TR 92/32 provides an explanation that joint

ownership of the rented property are not treated as partnership under the general law (Kenny,

2013). The partnership agreement in this case of Jack and Jill contains either oral or written

agreement having no effect on the share of income or loss derived from the rental property.

The agreement clause contained that Jack will be accountable for 100% of the loss that is

derived from the rental property. As it has been found in the case of FC of T v McDonald

(1987) where the agreement between them contained that Mr McDonald will be entitled to

25% of the profits whereas Mrs McDonald would be getting 75% of the profit from the

property (Krever, 2013). Therefore on suffering loss Mr McDonald will have to shoulder

100% of such loss. This was primarily done to advance the income of his wife and

indemnifying from any such loss.

Similarly in the present context the partnership between Jack and Jill, the partnership

between them would not be viewed as partnership under the general law and losses arising

out of such rented property should be shared equally between them.

As it has been defined under the TR 92/32 joint ownership of the rental property can

be defined as the partnership for the purpose of income tax however it is not concerned with

the partnership that is defined under the notion of general law (Jover, 2014). The ruling does

not include the joint ownership of any business practice that meets the purpose of the income

tax. The loss of income that is sustained from the rented property is administered with the

help of joint ownership together with the allocation of profits and losses. It is understood

from the current context of Jack and Jill the joint ownership of rented property forms the

foundations of the income tax and will not be accounted as the partnership in regard to the

principles of general law.

The principles of Taxation ruling TR 92/32 provides an explanation that joint

ownership of the rented property are not treated as partnership under the general law (Kenny,

2013). The partnership agreement in this case of Jack and Jill contains either oral or written

agreement having no effect on the share of income or loss derived from the rental property.

The agreement clause contained that Jack will be accountable for 100% of the loss that is

derived from the rental property. As it has been found in the case of FC of T v McDonald

(1987) where the agreement between them contained that Mr McDonald will be entitled to

25% of the profits whereas Mrs McDonald would be getting 75% of the profit from the

property (Krever, 2013). Therefore on suffering loss Mr McDonald will have to shoulder

100% of such loss. This was primarily done to advance the income of his wife and

indemnifying from any such loss.

Similarly in the present context the partnership between Jack and Jill, the partnership

between them would not be viewed as partnership under the general law and losses arising

out of such rented property should be shared equally between them.

8TAXATION LAW

Conclusion:

From the above discussed scenario it is understood that both Jack and Jill will be

required to share out the loss on equal basis and the joint ownership between them does not

accounts as partnership.

Answer to question 4:

One of the most quoted ruling on this subject that confirms that tax avoidance is

considered as acceptable and legal that originates in the case of IRC v Duke Westminster

(1936). The Duke of Westminster paid his Gardener wages based on the weekly basis and

entered into the contract through which he stopped paying the wage and drew up the

covenant agreement to pay an equivalent amount. The Gardener yet received the identical

amount in the form of wages but the Duke gained the advantage of the tax benefit since under

the law that was applied during the time when the covenant lowered the liability of the Duke

to surtax (Braithwaite, 2017). The case defines that every individual is eligible to order for

his tax affairs with the objective that tax attaching under this appropriate acts is lower than it

would have otherwise been. An individual cannot be forced to pay any increased amount of

tax.

On applying the fact in the present age these principles defines that given that a

person is successful in ordering them for the purpose of obtaining this result then the

taxpayers in their ingenuity will not be forced to pay any amount of increased sum of tax

(Sadiq et al., 2014). The decision under this case provides an individual with the opportunity

of reducing their tax liability in agreement with the financial framework of law.

Conclusion:

From the above discussed scenario it is understood that both Jack and Jill will be

required to share out the loss on equal basis and the joint ownership between them does not

accounts as partnership.

Answer to question 4:

One of the most quoted ruling on this subject that confirms that tax avoidance is

considered as acceptable and legal that originates in the case of IRC v Duke Westminster

(1936). The Duke of Westminster paid his Gardener wages based on the weekly basis and

entered into the contract through which he stopped paying the wage and drew up the

covenant agreement to pay an equivalent amount. The Gardener yet received the identical

amount in the form of wages but the Duke gained the advantage of the tax benefit since under

the law that was applied during the time when the covenant lowered the liability of the Duke

to surtax (Braithwaite, 2017). The case defines that every individual is eligible to order for

his tax affairs with the objective that tax attaching under this appropriate acts is lower than it

would have otherwise been. An individual cannot be forced to pay any increased amount of

tax.

On applying the fact in the present age these principles defines that given that a

person is successful in ordering them for the purpose of obtaining this result then the

taxpayers in their ingenuity will not be forced to pay any amount of increased sum of tax

(Sadiq et al., 2014). The decision under this case provides an individual with the opportunity

of reducing their tax liability in agreement with the financial framework of law.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Answer to question 5:

Issue:

Taking account of the present issue an assessment has been done relating to the

cutting down of timber under subsection 6 (1) of the ITAA 1997.

Laws:

i. Subsection 6 (1) of the ITAA 1936

ii. McCauley v FC of T

Application:

From the current issue of Bill it is found that he is the owner of the land that

numerous pine trees. He at the initial stages decided to clear the land for grazing sheep but on

being approached by the logging company that agreed to pay $1000 for every 100 meter of

timber that the logging firm can take from Bill’s land.

As it has been defined in the Taxation ruling TR 95/6 it deals with the income tax rulings

that rise from the activities of the primary production and forestry (Milton, 2013). It also

defines the degree till which an individual deriving the income from the forestry activities is

assessable. The ruling is applicable to both the individual taxpayers that indulge in forestry

activities or business of primary production such as disposing the timber. Considering the

explanation of the Subsection 6 (1) of the ITAA 1936 an individual taxpayer having

associations with the forest operations will be treated as the primary producer for income tax

provided that the activities of forest operations are viewed as performing business activities

(Woellner, 2013).

Answer to question 5:

Issue:

Taking account of the present issue an assessment has been done relating to the

cutting down of timber under subsection 6 (1) of the ITAA 1997.

Laws:

i. Subsection 6 (1) of the ITAA 1936

ii. McCauley v FC of T

Application:

From the current issue of Bill it is found that he is the owner of the land that

numerous pine trees. He at the initial stages decided to clear the land for grazing sheep but on

being approached by the logging company that agreed to pay $1000 for every 100 meter of

timber that the logging firm can take from Bill’s land.

As it has been defined in the Taxation ruling TR 95/6 it deals with the income tax rulings

that rise from the activities of the primary production and forestry (Milton, 2013). It also

defines the degree till which an individual deriving the income from the forestry activities is

assessable. The ruling is applicable to both the individual taxpayers that indulge in forestry

activities or business of primary production such as disposing the timber. Considering the

explanation of the Subsection 6 (1) of the ITAA 1936 an individual taxpayer having

associations with the forest operations will be treated as the primary producer for income tax

provided that the activities of forest operations are viewed as performing business activities

(Woellner, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Primary production can be referred as the planting of trees and tending down of trees

in a particular plantation under subsection 6 (1) of the ITAA 1997 that is originally intended

for cutting or tending of trees in a vegetation (Woellner et al., 2014). Bill in the present

context is treated as the primary producer because he is engaged in the business of primary

production for tending down the pine trees on a large piece of land that is owned by him.

Forest operations are usually known as those operations where there is a planting or tending

of trees in the vegetation in spite of the fact that the taxpayer did not originally planted the

trees.

In context of the above explanation, Bill did not planted the trees however the sum

that is received by him from the sale of felled by timber would be considered for assessment.

In spite of the fact that the sales comprised of the either entirely or the portion of the assets

having commercial values, tending of trees would be treated as receipts and would be

included in his taxable income under subsection 36 (1).

In the alternative scenario if the taxpayer was paid a large amount of $50,000 by

simply assigning the right to the logging company for cutting down the necessary quantity of

timber then the receipts received from the timber would be regarded as the “Royalties”. As

defined under the section 26 (f) receiving royalties from the tending of timber would be

treated as the assessable income and will be included in the assessable income in the year

during which the trees were tended (Morgan et al., 2013). Royalties that is received by Bill

from felling of timber would be treated as carrying the business of forest operations. In

respect of the judgement stated in McCauley v The Federal Commissioner of Taxation

payments that is received by grantor by assigning the right of tending the timber. Therefore,

the amount that will be received by Bill in the alternative scenario from the sale of timber

would be included in the taxable income in compliance with the section 26 (f).

Primary production can be referred as the planting of trees and tending down of trees

in a particular plantation under subsection 6 (1) of the ITAA 1997 that is originally intended

for cutting or tending of trees in a vegetation (Woellner et al., 2014). Bill in the present

context is treated as the primary producer because he is engaged in the business of primary

production for tending down the pine trees on a large piece of land that is owned by him.

Forest operations are usually known as those operations where there is a planting or tending

of trees in the vegetation in spite of the fact that the taxpayer did not originally planted the

trees.

In context of the above explanation, Bill did not planted the trees however the sum

that is received by him from the sale of felled by timber would be considered for assessment.

In spite of the fact that the sales comprised of the either entirely or the portion of the assets

having commercial values, tending of trees would be treated as receipts and would be

included in his taxable income under subsection 36 (1).

In the alternative scenario if the taxpayer was paid a large amount of $50,000 by

simply assigning the right to the logging company for cutting down the necessary quantity of

timber then the receipts received from the timber would be regarded as the “Royalties”. As

defined under the section 26 (f) receiving royalties from the tending of timber would be

treated as the assessable income and will be included in the assessable income in the year

during which the trees were tended (Morgan et al., 2013). Royalties that is received by Bill

from felling of timber would be treated as carrying the business of forest operations. In

respect of the judgement stated in McCauley v The Federal Commissioner of Taxation

payments that is received by grantor by assigning the right of tending the timber. Therefore,

the amount that will be received by Bill in the alternative scenario from the sale of timber

would be included in the taxable income in compliance with the section 26 (f).

11TAXATION LAW

Conclusion:

From the above stated analysis it can be defined that the amount that is received by

Bill from tending of timber would be considered as the taxable income and in the alternative

scenario if the a lump sum is received for granting of right then it would be treated as

royalties.

Conclusion:

From the above stated analysis it can be defined that the amount that is received by

Bill from tending of timber would be considered as the taxable income and in the alternative

scenario if the a lump sum is received for granting of right then it would be treated as

royalties.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.